overview of the first nine months of...

TRANSCRIPT

OVERVIEW OF THE FIRST NINE MONTHS OF 2013/14

Q3 2013/14

While the first quarter of 2014 marked a

promising start to the year for the fashion

industry, which reported growth rates of

approx. 3% compared to the first three

months of the previous year, the ensuing

months were rather disillusioning.

With like-for-like sales up by 5.2%, GERRY

WEBER International AG clearly

outperformed the German market as a whole

in the first half of the financial year 2013/14

(1 November 2013 – 30 April 2014).

For the months of our third quarter (May to

July), TW Testclub, an independent panel of

trade magazine Textilwirtschaft, reports for

the textile sector 2% growth in May, followed

by sharp year-on-year declines of -7% and -

8%, respectively for June and July.

The GERRY WEBER Group still clearly

outperformed the market as a whole in the

third quarter, when like-for-like Retail sales

remained stable compared to the third

quarter of the previous year.

In spite of these stable like-for-like Retail

sales in Q3 2013/14 and the additional

expansion-related 12.7% increase in the

GERRY WEBER International AG Interim Report Q3 2013/14

1

Retail segment’s sales revenues to EUR

104.9 million (Q3 previous year: EUR 93.1

million), total Group sales revenues (Retail

and Wholesale) remained almost constant,

down by -0.9% to EUR 187.2 million

compared to the prior year quarter. Sales

revenues in the Wholesale segment

amounted to EUR 82.3 million in Q3 2013/14

EUR (Q3 previous year: EUR 95.8 million).

The GERRY WEBER Group was

nevertheless able to increase its gross

margin by approx. 260 basis points to 59.4%

on almost comparable sales. This clearly

reflects the company’s improved profitability.

While third-quarter EBITDA remained almost

constant at EUR 22.7 million compared to Q3

2012/13 (EUR 22.6 million), EBIT declined

from EUR 17.4 million in the third quarter of

the previous year to EUR 16.0 million due to

increased depreciation/amortisation (EUR

6.7 million).

9M 2013/14

Profitable growth and, hence, improved profit

margins are primary objectives pursued by

the GERRY WEBER Group. This was

achieved in the first nine months of 2013/14,

when the gross margin increased from

53.8% to 56.4% and the EBIT margin

climbed from 10.2% to 10.9%.

The improved profitability is even more

remarkable as sales revenues in the first

nine months of the current financial year rose

Q3 2013/14 Q3 2012/13 9M 2013/14 9M 2012/13

in EUR million 01.05.14 - 31.07.14 01.05.13 - 31.07.13 01.11.13 - 31.07.14 01.11.12 - 31.07.13

Sales 187.2 189.0 600.0 592.8

Wholesale 82.3 95.8 306.4 333.1

Retail 104.9 93.2 293.6 259.7

Earnings key figures

EBITDA 22.7 22.6 84.5 76.1

EBITDA margin 12.1% 12.0% 14.1% 12.8%

EBIT 16.0 17.4 65.5 60.7

EBIT margin 8.5% 9.2% 10.9% 10.2%

EBT 14.9 16.7 61.7 58.5

EBT margin 7.9% 8.9% 10.3% 9.9%

Net income of the period 10.4 11.5 43.1 40.8

GERRY WEBER International AG Interim Report Q3 2013/14

2

moderately by 1.2% to EUR 600.0 million

(previous year: EUR 592.8 million). The

increase is attributable not only to the Retail

segment‘s like-for-like growth of 3.4% but

above all the expansion of the Group’s own

sales space in the past two years.

In spite of the ongoing expansion of the

Group’s own Retail operations and the

increasing implementation of the vertical

integration processes and the related

expenses, nine-month earnings before

interest and taxes (EBIT) were up by 7.9% to

EUR 65.5 million (9M previous year: EUR

60.7 million).

As a result, consolidated earnings after taxes

increased by 5.6% to EUR 43.1 million,

which is equivalent to earnings per share of

EUR 0.94 (9M previous year: EUR 0.89).

In view of the extraordinary importance of the

fourth quarter for our business model, we

continue to believe that we will reach the

performance indicators set out in our January

guidance.

9M 2013/14 9M 2012/13

in EUR million 01.11.13 - 30.04.14 01.11.12 - 31.07.13

Total assets 605.3 477.6

Equity 410.2 369.5

Debt Capital 195.1 108.1

Equity ratio 67.8% 77.4%

Key figures

High share price (in Euro) 39.24 38.35

Low share price (in Euro) 28.76 30.18

Earnings per share (in Euro) 0.94 0.89

Investments 47.5 17.8

Number of employees (average) 4,957 4,723

GERRY WEBER International AG Interim Report Q3 2013/14

3

THE GERRY WEBER SHARE While the global financial markets showed

great volatility in the first half of 2014, the

general trend was positive. Having passed

the 10,000 points mark in June, the DAX

reached an all-time high of 10,051 points on

20 June. In July, geopolitical events in the

Middle East and in Ukraine and the monetary

policies of the major central banks caused

growing uncertainty in the capital markets

and led to a marked slump in share prices.

The GERRY WEBER share delivered a very

positive performance in the first nine months,

reaching an all-time high of EUR 39.24 on 3

June 2014. Following a weaker performance

in the 2012/13 financial year, the GERRY

WEBER share opened the financial year

2013/14 at EUR 30.49 on 1 November 2013.

While the performance remained moderate in

the first quarter, the share price picked up in

the second and third quarter. At the end of

the third quarter on 31 July 2014, the share

price amounted to EUR 34.14, having gained

12.0% during the first nine months of the

financial year. The MDAX, in which the

GERRY WEBER share is listed, gained

1.35% during the same period, which means

that the GERRY WEBER share clearly

outperformed its benchmark index. An

average of 91,825 GERRY WEBER shares

per day were traded (Xetra) on 187 trading

days. On 31 July 2014, the market

capitalisation of the GERRY WEBER share

amounted to EUR 1,521 million.

In response to the growing interest shown by

foreign investors, we participated in the

German Investment Seminar in New York in

the third quarter of the current financial year,

where we informed existing but also new

potential investors about our business model

and our ongoing growth strategy. The first

nine months of the current financial year also

saw us participate in another four national

and international conferences and talk to

round about 120 investors on eight roadshow

days. In the coming quarter, our investors

and private shareholders will again be

informed about the business performance of

the GERRY WEBER Group at investor

conferences and roadshows as well as

various investor forums.

GERRY WEBER International AG Interim Report Q3 2013/14

4

GERRY WEBER International AG Interim Report Q3 2013/14

5

INTERIM GROUP MANAGEMENT REPORT on the first nine months of 2013/14

from 1 November 2013 to 31 July 2014

Sales performance

As in the two previous quarters of 2013/14,

GERRY WEBER International AG was able

to make a positive difference from the

general trend in the German fashion market

also in the third quarter. While the first half of

our financial year was characterised by an

almost balanced market environment, the

latter deteriorated in June and July 2014.

Having increased by 2% in May 2014, sales

revenues dropped sharply compared to the

previous year in June (-7 %) and July (-8 %).

While the GERRY WEBER Group was

unable to fully isolate itself from the negative

market environment in May and July 2014,

our like-for-like Retail sales did not decline

and remained stable on a quarterly basis.

Not least due to the increasing difficult

market environment, in which re-orders of

our Wholesale customers fell short of our

expectations, in particular, total Group sales

revenues declined by a moderate 0.9% to

EUR 187.2 million in the third quarter of

2013/14 compared to the prior year period.

Lower sales revenues in the Wholesale

segment (EUR 82.3 million) were not entirely

offset by the 12.7% increase in Retail

revenues, which climbed to EUR 104.9

million in the third quarter.

Total Group sales revenues in the first nine

months of 2013/14 amounted to EUR 600.0

million (9M previous year: EUR 592.8 Mio.),

which represents an increase of 1.2%.

A major contribution to this sales growth in

the first nine months was made by the Retail

segment, whose relative share in total Group

revenues climbed from 43.8% to 48.9%.

Performance of the Retail segment

Having climbed by 13.3% in H1 2013/14,

Retail revenues increased by 12.7 to EUR

104.9 million in the third quarter. Retail

revenues for the nine-month period of

2013/14 totalled EUR 293.6 million, which

represents an increase by 13.0% on the prior

year period.

Wholesale 51,1 %

(VJ: 56,2%)

Retail48,9 %

(VJ: 43,8%)

Sales split by segments 9M 2013/14

GERRY WEBER International AG Interim Report Q3 2013/14

6

The positive development of the Retail

segment is attributable to both a 3.4%

increase in like-for-like sales (9M) and to the

growing sales generated by the stores

opened in the past two years. The 3.4%

increase in like-for-like Retail sales means

that we clearly outperformed the market as a

whole.

The company-managed Houses of GERRY

WEBER and mono-label stores contributed

76.5% to the Retail segment’s total nine-

month revenues. The number of company-

managed stores increased by 39 (net) to 607

as of 31 July 2014.

In the context of the ongoing vertical

integration of our distribution channels, the

concession stores are playing an

increasingly important role. In contrast to the

shop-in-shops, which form part of the

Wholesale segment, the concession stores

are rented from our retail partners, which

gives us full control over the goods that are

available in these stores. At present, we

operate 115 concession stores exclusively in

European countries outside Germany.

The chart shows a breakdown of Retail

revenues by distribution channels.

Performance of the Wholesale segment

When analysing the Wholesale revenues, it

should be noted that the figures for the first

nine months of the previous financial year

included sales to 18 Belgian and eight

Houses of GERRY WEBER run by

franchisees. As we acquired majority

shareholdings in our Belgian and Norwegian

franchisees with effect from 1 August 2013

and 1 June 2014, respectively, these

revenues are now counted towards the Retail

segment.

Accordingly, Wholesale revenues declined

by 14.1% to EUR 82.3 million in the third

quarter of 2013/14 Q3 previous year: EUR

HoGWs+Mono 76.5%

(prev:75.1%)

Concession5.1%

(prev:4.8%)

Outlets12.9%

(prev: 14.7%)

Online Shops5.5%

(prev: 5.4%)

Sales split Retail 9M 2013/14

GERRY WEBER International AG Interim Report Q3 2013/14

7

95.8 million). As already in the previous year,

we again delisted a number of Wholesale

partners who failed to meet our strict credit

assessments. The re-ordering behaviour of

our Wholesale customers also contributed to

the reduction in Wholesale revenues.

Because of the difficult market environment

in June and July 2014, re-orders remained

clearly below our expectations, which means

that sales to existing Wholesale customers

also failed to improve.

Due to the reclassification of the revenues

generated by the 18 Belgian HoGWs to the

Retail segment as well as lower pre-order

volumes, Wholesale revenues were down on

the previous year already in the first two

quarters of our financial year (-5.6%). As

another eight Norwegian stores were taken

over with effect from 1 June 2014, their

revenues were reclassified to the Retail

segment as well; as a result, Wholesale

revenues for the first nine months of 2013/14

declined by a total of 8.0% to EUR 306.4

million (9M previous year: EUR 333.1

million).

Accordingly, the relative contribution made

by the Wholesale segment to total Group

revenues dropped from 56.2% in the first

nine months of the previous year to 51.1% in

the same period of the current financial year.

The decline in the Wholesale segment’s

share in total Group revenues reflects not

only the expansion of our Retail operations

but also the ongoing implementation of our

vertical integration strategy.

Performance of the distribution channels

The distribution channels of the fashion

industry have changed considerably in the

past years. Fully vertically integrated sales

formats will continue gaining ground in the

market. The GERRY WEBER Group opened

its first own House of GERRY WEBER

already back in 1999. The number of

company-managed stores increased at a

disproportionate rate especially in the past

financial years. At the end Q3 2013/14, the

company operated 751 own stores in

Germany and abroad. This clearly reflects

the growing importance of fully vertically

integrated distribution structures at GERRY

WEBER.

The aim of the vertical integration strategy is

to assume control over merchandise

management in more and more stores and to

get the collections to the sales floors even

more quickly.

In the first nine months of the current

financial year, the number of company-

managed stores increased from 701 to 751.

Own stores comprise the Houses of GERRY

WEBER and the mono-label stores as well

as the concession stores and the outlet

centres. See the chart below for a detailed

breakdown of the individual distribution

channels.

The number of own stores outside Germany

increased by 40 (net). Besides new store

openings in Belgium and Poland as well as

market entries in the Czech Republic,

Slovakia and Sweden, the acquisition of 25

Norwegian stores made an important

contribution to our increased Retail presence

in Europe. As of the end of Q3 2013/14,

GERRY WEBER International AG Interim Report Q3 2013/14

8

GERRY WEBER apparel was sold in

company-managed stores in 14 European

countries.

As we expanded our Retail operations in

Germany and abroad, the number of factory

outlets increased from 22 to 29 during the

reporting period; eight of these outlet centres

are located outside Germany.

At 272, the number of franchised Houses of

GERRY WEBER would seem to have

remained constant in the first nine months

(31 Oct. 2013: 271 franchised stores). It

should be noted, however, that eight

Norwegian franchised stores now form part

of the Retail segment following the June

2014 takeover. A total of 20 new franchised

stores were opened, including eight in

Russia and five in Switzerland. Franchised

stores were closed in Poland and Italy,

mostly for strategic reasons.

The shop-in-shops are another important

distribution channel of the Wholesale

segment. Their number declined from 2,816

at the end of the financial year on 31 October

2013 to 2,770. This decline is primarily

attributable to the fact that smaller shop-in-

shops were merged into larger, more visible

shops as well as to portfolio adjustments.

E-commerce is gaining importance primarily

for our TAIFUN and SAMOON brands and is

therefore being expanded on an international

scale. The EU online shop for Sweden,

Belgium, France and the UK was launched in

June 2014, which means that our own Retail

operations are now complemented by e-

shops in a total of nine countries.

9M 2013/14 2012/13

31.07.2014 31.10.2013

RETAIL

Houses of GERRY WEBER 469 424

Monolabel Stores 138 144

Concession Flächen 115 111

Factory Outlets 29 22

WHOLESALE

Houses of GERRY WEBER 272 271

Shop-in-Shops 2.770 2.816

GERRY WEBER International AG Interim Report Q3 2013/14

9

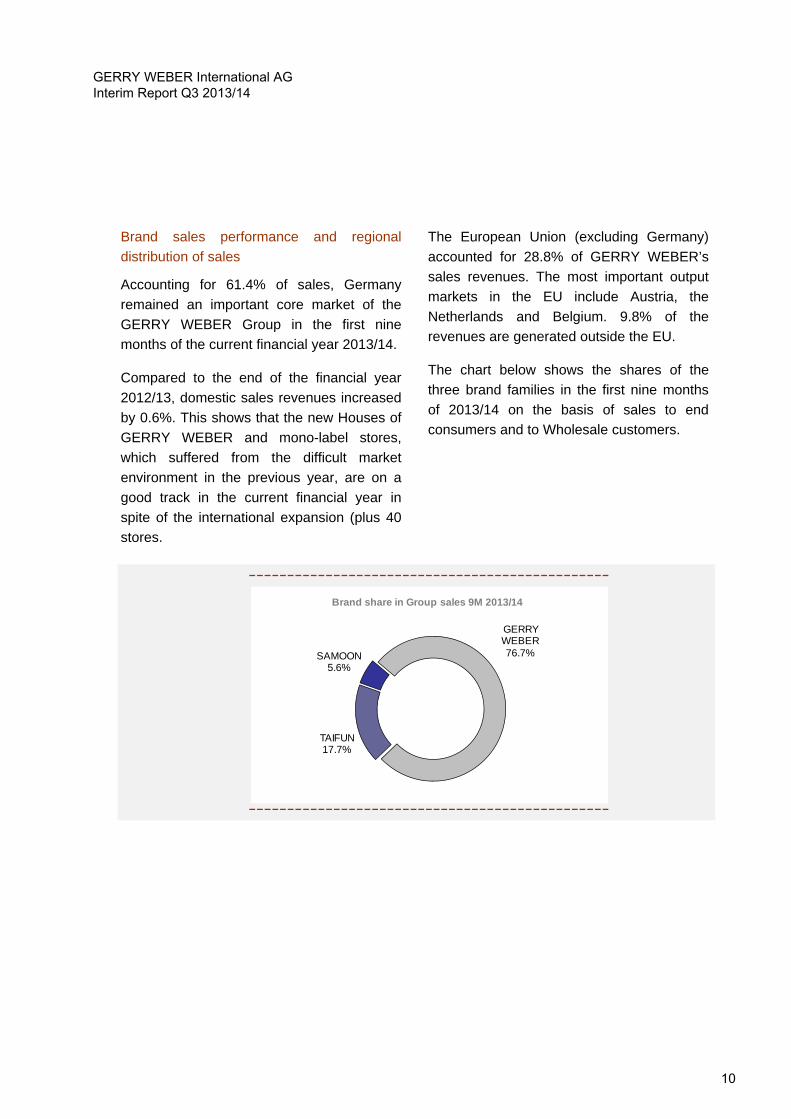

Brand sales performance and regional

distribution of sales

Accounting for 61.4% of sales, Germany

remained an important core market of the

GERRY WEBER Group in the first nine

months of the current financial year 2013/14.

Compared to the end of the financial year

2012/13, domestic sales revenues increased

by 0.6%. This shows that the new Houses of

GERRY WEBER and mono-label stores,

which suffered from the difficult market

environment in the previous year, are on a

good track in the current financial year in

spite of the international expansion (plus 40

stores.

The European Union (excluding Germany)

accounted for 28.8% of GERRY WEBER’s

sales revenues. The most important output

markets in the EU include Austria, the

Netherlands and Belgium. 9.8% of the

revenues are generated outside the EU.

The chart below shows the shares of the

three brand families in the first nine months

of 2013/14 on the basis of sales to end

consumers and to Wholesale customers.

GERRY WEBER 76.7%

TAIFUN17.7%

SAMOON5.6%

Brand share in Group sales 9M 2013/14

GERRY WEBER International AG Interim Report Q3 2013/14

10

Earnings

Q3 2013/14

The Retail segment’s continuously growing

contribution to the business model again led

to a notable improvement in the gross margin

in the third quarter of 2013/14. In spite of a

moderate 0.9% decline in sales revenues,

the gross result climbed from EUR 107.4

million to EUR 111.1 million in the third

quarter of the current financial year.

Accordingly, the gross margin improved from

56.8% to 59.4% in Q3 2013/14.

The ongoing expansion of GERRY WEBER

International AG influenced the Group’s

earnings also in the third quarter of 2013/14.

Higher personnel expenses and rents for the

company’s own stores as well as one-time

expenses relating to the acquisition of 25

Norwegian stores, including eight franchised

Houses of GERRY WEBER, led to increased

expense items in the third quarter. Add to

this the fact that newly opened stores

generally make a lower contribution to the

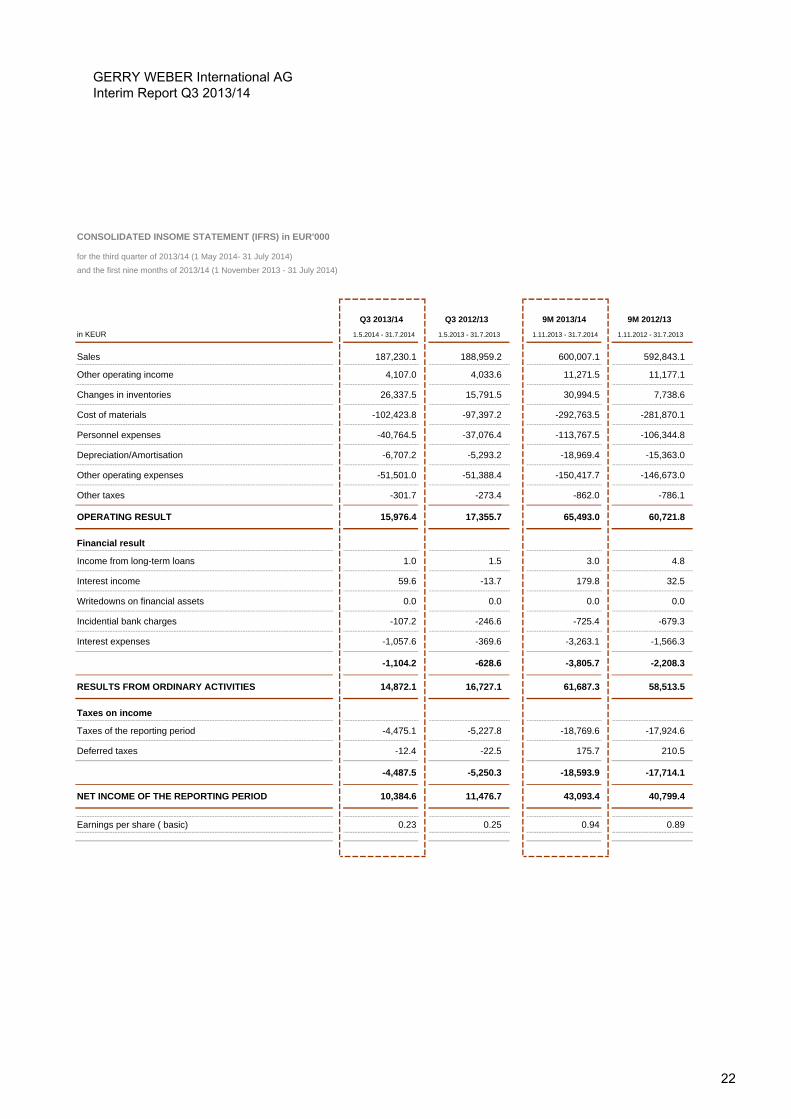

Q3 2013/14 Q3 2012/13 9M 2013/14 9M 2012/13

in KEUR 01.05.14 - 31.07.14 01.05.13 - 31.07.13 01.11.13 - 31.07.14 01.11.12 - 31.07.13

Sales 187,230.1 188,959.2 600,007.1 592,843.1

Other operating income 4,107.0 4,033.6 11,271.5 11,177.1

Changes in inventories 26,337.5 15,791.5 30,994.5 7,738.6

Cost of materials -102,423.8 -97,397.2 -292,763.5 -281,870.1

Personnel expenses -40,764.5 -37,076.4 -113,767.5 -106,344.8

Depreciation/Amortisation -6,707.2 -5,293.2 -18,969.4 -15,363.0

Other operating expenses -51,501.0 -51,388.4 -150,417.7 -146,673.0

Other taxes -301.7 -273.4 -862.0 -786.1

OPERATING RESULT 15,976.4 17,355.7 65,493.0 60,721.8

Financial result -1,104.3 -628.6 -3,805.8 -2,208.3

RESULTS FROM ORDINARY ACTIVITIES 14,872.1 16,727.1 -61,687.2 58,513.5

Taxes on income -4,487.5 -5,250.3 -18,593.9 -17,714.1

NET INCOME OF THE REPORTING PERIOD 10,384.6 11,476.8 43,093.3 40,799.4

GERRY WEBER International AG Interim Report Q3 2013/14

11

company’s profits during the first few months

after their opening. A newly opened store

typically needs some 24 to 30 months to

reach an average revenue level and make an

average contribution to earnings.

Personnel expenses increased by EUR 3.7

million to EUR 40.8 million in the third

quarter. At the same time, the number of

employees rose from 4,723 to 5,139 on 31

July. (Annual Average: 4,957)

In spite of partly higher fixed costs, e.g. the

rents for the company’s own stores, other

operating expenses remained almost

constant at EUR 51.5 million in the third

quarter (Q3 previous year: EUR 51.4 million).

Taking into account the improved gross

margin and the increased expansion-related

expenses, earnings before interest, taxes,

depreciation and amortisation (EBITDA)

remained almost unchanged at EUR 22.7

million (Q3 previous year: EUR 22.6 million).

Accordingly, the EBITDA margin remained

constant at 12.1%.

Depreciation/amortisation increased from

EUR 5.3 million in the prior year quarter to

EUR 6.7 million also due to the expansion of

the Retail operations and the related

investments in fixed assets. With EBITDA

remaining unchanged, the increase in

depreciation/amortisation led to a 7.9%

decline in EBIT to EUR 16.0 million in Q3

2013/14.

The negative financial result increased

moderately to EUR 1.1 million compared to

the third quarter of the previous year (EUR

0.6 million) but remained almost unchanged

compared to the previous quarters of the

current financial year. The increase on the

previous year is attributable to the interests

of a EUR 75 million note loan in November

2013 to finance the new logistic centre. The

result after taxes for the third quarter 2013/14

amounted to EUR 10.4 million. The moderate

decline by 9.5% led to lower earnings per

share, which declined from EUR 0.25 to EUR

0.23 in the third quarter.

9M 2013/14

Compared to the growth in sales revenues in

the first nine months of 2013/14 (+1.2%), the

gross result increased at a disproportionate

6.1% to EUR 338.2 million (9M previous

year: EUR 318.7 million). As outlined above,

the Retail segment’s higher share in total

revenues had a particularly positive effect on

the gross margin, which consequently

climbed from 53.8% to 56.4% (+260 basis

points).

Improved inventory management and the

resulting faster inventory turnover as well as

our flexible procurement structures also

contributed to the higher gross margin and,

hence, to the company’s improved

profitability.

The number of company-managed stores

increased by 119 to 751 over the past twelve

months (since 1 August 2013). Our own

stores are run by our own staff, which means

that personnel expenses increased at a

higher rate than sales revenues. In the nine-

month period, personnel expenses rose by

7.0% to EUR 113.8 million compared to the

first nine months of the previous year. In this

context, it should be noted that the sales

revenues generated by a newly opened store

slowly rise to an average level, whereas fixed

costs such as personnel expenses and rents

are partly incurred already prior to the

GERRY WEBER International AG Interim Report Q3 2013/14

12

opening. Personnel expenses as a

percentage of sales revenues climbed from

17.9% to 19.0%. As more and more

company-managed stores become

established in their locations, we expect to

be able to reduce personnel expenses as a

percentage of sales revenues.

Compared to personnel expenses, other

operating expenses rose only moderately in

the nine-month period. This is mainly due to

positive effects affecting the revenue-related

cost items such as transport and logistics,

which increased at a lower rate than fixed

costs. Other operating expenses totalled

EUR 150.4 million at the nine-month stage

(9M previous year: EUR 146.7 million), which

represents an increase of 2.6%.

Earnings before interest, taxes, depreciation

and amortisation (EBITDA) were up by a

high 11.0% on the previous year and

amounted to EUR 84.5 million (EUR 76.1

million). The improved EBITDA clearly

reflects the increased profitability of GERRY

WEBER Group.

In the last months new company-managed

stores were opened and existing franchised

stores were taken over and transferred to the

Retail segment. As this led to an increase in

the Group’s assets and depreciation

/amortisation rose by 23.5% to EUR 19.0

million (9M previous year: EUR 15.4 million).

Earnings before interest and taxes (EBIT) for

the full period amounted to EUR 65.5 million,

compared to EUR 60.7 million in the first nine

months of the previous year, which

represents an increase of 7.9%, Taking into

account the financial result (EUR -3.8 million)

and income taxes (EUR –18.6 million), the

GERRY WEBER Group’s net income for the

period after taxes amounted to EUR 40.8

million (9M previous year: EUR 40.8 million).

This represents an increase by 5.6%.

Accordingly, earnings per share improved

from EUR 0.89 to EUR 0.94 per share.

Net worth position

Since the end of the financial year 2012/13,

total assets of GERRY WEBER International

AG have increased by approx. EUR 73.7

million or 13.9% to EUR 605.3 million.

On the assets side of the balance sheet,

non-current assets were primarily influenced

by changes in intangible assets and property,

plant and equipment. At EUR 85.4 million,

intangible assets were up by approx EUR

15.3 million or 21.8% on the end of the

financial year 2012/13. This increase is

mainly the result of the recognition of

intangible assets acquired against payment

such as customer relationships, which were

acquired in conjunction with the acquisition of

25 Norwegian stores, including eight former

franchised Houses of GERRY WEBER.

As of 31 July 2014, property, plant and

equipment totalled EUR 178.9 million,

compared to EUR 165.9 million at the end of

the financial year 2012/13. This represents

an increase of 7.9%, which is due to the

ongoing expansion of the company’s Retail

operations, among other things. Advance

payments for work in progress climbed from

EUR 1.4 million to EUR 13.4 million at the

end of Q3 2013/14. Work in progress

primarily comprises construction measures

GERRY WEBER International AG Interim Report Q3 2013/14

13

related to the construction of our new logistic

centre close to our company headquarters.

At EUR 26.9 million, the carrying amount of

the Hall 30 investment property remained

almost unchanged (31 July 2013: EUR 27.3

million). Non-current assets totalled EUR

300.6 million, compared to EUR 274.9 million

at the end of the financial year 2012/13.

Current assets were primarily influenced by

an increase in inventories, in other current

assets as well as in cash and cash

equivalents.

Inventories increased by 26.7% or EUR 29.8

million compared to the end of the financial

year 2012/13 and amounted to EUR 141.2

million at the nine-month stage 2013/14. This

strong growth is due to the expansion of the

company-managed Retail stores as well as

to the seasonal increase in inventories during

the third quarter, in which the first part of the

autumn/winter collection is usually delivered

to the central warehouses.

Cash and cash equivalents rose by 18.6%

from EUR 65.6 million to EUR 77.8 million.

The third quarter of our financial year is

characterised by an outflow of cash used to

pre-finance a major part of the autumn/winter

collection, which, as outlined above, is

delivered to our customers and our own

stores in the following months. Also in the

third quarter, the company pays out the

dividend, which led to an outflow of cash of

EUR 34.4 million in Q3 2013/14. Current

trade receivables declined from EUR 65.8

million to EUR 54.9 million. The decrease by

16.6% is primarily attributable to the different

reporting dates.

Equity capital increased from EUR 395.8

million at the end of the previous financial

year to EUR 410.2 million as of 31 July 2014,

primarily due to the allocation of the higher

net income for the period. Against the

background of the increase in total assets

mentioned above, the Group’s equity ratio

declined moderately from 74.4% at the end

of the past financial year to 67.8%.

Non-current liabilities increased from EUR

48.5 million on 31 October 2013 to EUR

128.6 million. The increase is primarily

attributable to the note loan issued in

November 2013. As a result, non-current

financial liabilities climbed from EUR 5.7

million to EUR 85.8 million.

Other non-current liabilities in the amount of

EUR 24.3 million result from the majority

interests in the Dutch and Belgian Houses of

GERRY WEBER and concession stores. The

GERRY WEBER Group holds 51% in the

companies operating these stores. As there

is a mutual option right for the acquisition of

the remaining 49%, the anticipated purchase

price of these shares is recognised under

“Other non-current liabilities”.

Current liabilities declined from EUR 87.4

million to EUR 66.5 million in the first nine

months of 2013/14. This is primarily due to

the payment of current tax liabilities, which

sent other current liabilities falling to EUR

11.6 million (31 Oct. 2013: EUR 27.7 million).

GERRY WEBER International AG Interim Report Q3 2013/14

14

Financial assets and investments

Due to the increase in earnings before

interest and taxes in the first nine months of

2013/14, cash flow from operating activities

was up by 88.4% to EUR 16.4 million on the

same period of the previous year (EUR 8.7

million). Taking into account increased

interest payments for the note loan of EUR

2.0 million (9M previous year: EUR 1.0

million), cash flow from current operations

doubled to EUR 13.9 million (9M previous

year: EUR 7.0 million).

Investments in property, plant and equipment

as well as intangible assets stood at EUR

42.0 million at the nine-month stage, up by a

high EUR 24.4 million on the same period of

the previous financial year. Besides the

investments in the expansion of our Retail

operations, this is primarily attributable to the

acquisition of 25 Norwegian stores, which

were taken over with effect from 1 June

2014. In addition, the first investments were

made in our new logistic centre, construction

of which commenced in April 2014. Against

the background of the acquisition in Norway,

the outflow of cash for the acquisition of fully

consolidated entities amounted to EUR 5.2

million. The outflow of cash from investing

activities totalled EUR 47.0 million (9M

previous year: EUR 17.4 million).

Cash flow from financing activities is

influenced by the dividend payment for the

financial year 2012/13 in the amount of EUR

34.4 million on the one hand and by funds

raised in the amount of EUR 79.7 million on

the other hand. These primarily result from

the issue of a EUR 75 million note loan. At

the bottom line, cash flow from financing

activities totalled EUR 45.3 million.

As a result of the inflow and outflow of cash

described above, cash and cash equivalents

increased by EUR 12.2 million to EUR 77.8

million (1 November 2013: EUR 65.6 million).

Segment report

GERRY WEBER International AG

distinguishes between two main segments,

“Production and Wholesale" and “Retail", as

well as “Other segments”. The Wholesale

segment comprises all distribution structures

with external specialist retailers as well as all

development and production processes for

our merchandise including transport and

logistics. The “Retail“ segment is almost

exclusively a distribution segment and

includes all company-managed Houses of

GERRY WEBER, mono-label stores,

concession shops, outlet stores as well as

the individual national online shops. “Other

segments” mainly comprise the income and

expenses as well as the assets and liabilities

of the Hall 30 investment property. Income

and expenses as well as assets and liabilities

of the holding company are allocated

proportionately to the individual segments.

Due to the decline in Wholesale revenues

from EUR 333.1 million in the first nine

months of the previous year to EUR 306.4

million, the segment’s earnings before tax

also dropped from EUR 51.1 million to EUR

39.1 million. As discussed above, much of

this reduction is attributable to the

reclassification of revenues from the

GERRY WEBER International AG Interim Report Q3 2013/14

15

Wholesale segment to the Retail segment.

The Wholesale sales to 18 Belgian and eight

Norwegian Houses of GERRY WEBER have

been counted towards the Retail segment

since 1 August 2013 and 1 June 2014,

respectively, when these stores were taken

over.

The reclassification of stores to the Retail

segment is also reflected in the number of

franchised Houses of GERRY WEBER.

Although 20 franchised stores were opened,

their number remained almost constant, at

272, compared to the end of the financial

year.

Against the background of the allocation of

the holding company’s assets and liabilities

to the individual segments, the Wholesale

segment’s assets rose by 14.9% to EUR

397.8 million. Accordingly, the segment’s

liabilities also increased from EUR 53.7

million in the first nine months of the previous

financial year to EUR 73.2 million on 31 July

2014.

Wholesale investments in non-current assets

amounted to EUR 18.7 million in the first nine

months of 2013/14, compared to EUR 6.4

million in the previous year. The Wholesale

segment’s average headcount declined from

1,370 to 1,281.

Due to the strong 13% increase in the Retail

segment’s nine-month revenues to EUR

293.6 million, earnings before taxes (EBT)

improved to EUR 19.1 million. This

represents an almost fourfold increase in

EBT compared to the first nine months of the

previous year (9M previous year: EUR 5.0

million). As explained above, the increase in

sales revenues is due not only to the

expansion of our own sales space but also to

a 3.4% increase in like-for-like Retail sales in

the first nine months of 2013/14.

The consistent implementation of our Retail

expansion strategy and the takeover of

existing franchised stores led to an increase

in assets and hence to a sharp rise in the

Retail segment’s depreciation/amortisation,

which climbed from EUR 7.9 million in the

first nine months of the previous financial

year to EUR 11.3 million in the nine-month

period 2013/14.

As outlined under “Performance of the

distribution channels”, the number of

company-managed stores increased from

701 at the end of the financial year on 31

October 2013 to 751. This includes eleven

stores closed between November 2013 and

July 2014.

As investments in the Retail segment’s non-

current assets increased from EUR 10.9

million to EUR 28.8 million (nine-month

comparison), the segment’s assets also

picked up by 35.9% to EUR 300.3 million. At

the same time, the Retail segment also

posted higher liabilities of EUR 245.8 million

(9M previous year: EUR 169.7 million).

GERRY WEBER’s own stores are run by the

Group’s own staff, which is why the Retail

segment’s average headcount increased

from 3,352 to 3,675 (+9.6%).

GERRY WEBER International AG Interim Report Q3 2013/14

16

OPPORTUNITY AND RISK REPORT

As a global fashion and lifestyle company,

we are exposed to changes and

uncertainties which may result from national

and international external conditions but also

from internal factors.

This is why risk management is an integral

element of corporate governance in the

GERRY WEBER Group. GERRY WEBER

focuses on identifying, assessing, managing

and monitoring risks in the context of a

comprehensible risk management and

control system covering all corporate

processes. The aim is to identify positive

developments at an early stage and to seize

the resulting opportunities in the interest of

the company.

The GERRY WEBER Group generates about

61.4% of its sales revenues in Germany.

While the German economy showed a

positive trend, almost as planned, in the first

months of 2014, geopolitical events made

themselves felt primarily in the second

quarter of 2014. Accordingly, the GfK

consumer confidence index indicated

considerable uncertainty among consumers

for the first time in months. While income

expectations and purchasing propensity have

remained relatively stable so far, economic

expectations suffered a notable setback in

August, when the index fell by 35.5 points to

10.4 points.

While German consumers remain in a

spending mood, they seem to be paying

more and more attention to geopolitical

developments. Uncertainty about the

potential consequences for the German

economy is growing. In particular, the

sanctions against Russia, which have

already had a clearly adverse impact on

exports, could become a real threat to the

German economy.

Should geopolitical events have an adverse

impact on economic activity and/or consumer

behaviour in one of our output markets, we

have installed mechanisms to assess

potential risks to the GERRY WEBER Group

and to minimise them by taking appropriate

measures.

For a detailed description of our risk

management system, the control systems for

the accounting processes and the

opportunities and risks in the GERRY

WEBER Group, please refer to the risk report

in the 2012/13 Annual Report. The

statements made in this risk report remain

valid.

Since the beginning of the fiscal year

2013/14, no material changes have occurred

regarding the opportunity risks to our

company’s future. Based on current

knowledge, there are no risks that could

jeopardise the existence of the GERRY

WEBER Group.

GERRY WEBER International AG Interim Report Q3 2013/14

17

POST-BALANCE SHEET EVENTS

After the end of the reporting period (1 May -

31 July 2014), no events occurred which are

expected to have a material impact on the

net worth, financial and earnings position of

GERRY WEBER International AG.

FORECAST REPORT

Forward-looking statements

The present forecast report of GERRY

WEBER International AG reflects

management’s expectations regarding the

future geopolitical, macroeconomic, sector-

specific and company-specific developments

which many influence the company’s

business activities. It is based on

management’s knowledge at the time of the

preparation of the report.

As a fashion and lifestyle company, GERRY

WEBER International AG is primarily

exposed to the spending mood of end

consumers in the individual sales regions as

well as to the footfall in city centres and

stores. Consumer spending is influenced, on

the one hand, by the economic situation and

private households' income trend and, on the

other hand, by factors such as the weather or

special events such as large sports events,

which may influence consumers’ spending

propensity. Geopolitical developments

outside the home market such as the current

crises in the Middle East and Ukraine may

also influence consumers’ purchasing

propensity. In spite of the growing regional

diversification, approx. 61.4% of the sales

revenues were generated in Germany in the

first nine months of 2013/14. Consumer

spending in Germany thus remains the most

important factor influencing the sales

revenues of GERRY WEBER International

AG.

Economic situation and industry

environment

Eurozone

In July, Germany’s Gesellschaft für

Konsumforschung (GfK) published its

consumer confidence figures for Europe,

which painted a moderately positive picture.

While British consumers believed in a

positive economic trend and expected the

economic recovery to continue, there was

great uncertainty among French consumers.

In Southern Europe, especially in Italy, there

was generally cautious optimism among

consumers, while consumers in Greece,

Spain and Portugal believed in a slow

notable upswing and a way out of the crisis.

The generally positive picture has probably

clouded over somewhat in the meantime.

The escalation of the situation in eastern

Ukraine and the increasing sanctions

together with the crises in Israel and Iraq are

causing growing uncertainty. Experts

meanwhile consider the 1% growth forecast

issued by the European Central Bank (ECB)

in June to be too optimistic and therefore

expect it to be downgraded. The weak euro

and growing deflationary tendencies are also

GERRY WEBER International AG Interim Report Q3 2013/14

18

fuelling fears of an extended period of

stagnation in the eurozone.

Russia

Accounting for approx. 3% to 4% of sales

revenues, Russia is an important export

country for the GERRY WEBER Group. On

the one hand trade sanctions are putting a

damper on the Russian economy and on the

other hand the weak rouble and rising food

prices are causing additional uncertainty

among our local customers. We are closely

monitoring the situation in Russia and have

looked at various scenarios for our planning.

At this stage, however, we do not expect to

see a strong influence on the sales revenues

of the GERRY WEBER Group as a whole,

even though sales in Russia may be dented

somewhat. Moreover, our consumers in

Russia have above-average incomes, which

makes them less dependent on economic

developments in their country.

Germany

The consumer climate in Germany no longer

remains unaffected by the geopolitical

fluctuations and, for the first time, no longer

defies the general trend in Europe. Besides

the crises in Ukraine, Israel and Iraq, it is

primarily the fear of a trade war with Russia,

in conjunction with additional sanctions,

which is influencing the Russian and German

economies. In particular, the manufacturing

sector is suffering from the sanctions.

Exports to Russia dropped by as much as

15.5% in the first half of 2014. This trend is

also reflected in the Ifo Business Climate

Index, which declined for the fourth

consecutive time.

This trend is also reflected in consumer

expectations. While economic expectations

reached a new high of 45.9 points in July -

the highest level since German reunification -

they slumped to 10.4 points in August.

According to the GfK, this is the strongest

decline since 1980. Income expectations

also fell from a high of 54.7 points in July to

50.1 points in August. Purchasing propensity

was the only component to stay at a high

level of 49.3 points. Overall, however, the

consumer climate index stayed at a relatively

high level. Consumer confidence stood at 8.9

points in August 2014, up from 7.0 points in

August 2013. The GfK projects a further

decline to 8.6 points for September.

Industry environment

After a mixed year-end, the start to the

calendar year 2014 was positive throughout,

according to TW-Testclub, a panel of

German trade magazine Textilwirtschaft.

April was the first month in which sales

revenues remained below retailers’

expectations. June and July were

disappointing as sales were down by -8%

and -7%, respectively, on the previous year.

Tropical temperatures and thunderstorms on

the one hand and the Soccer World Cup on

the other hand led to lower footfall in city

centres and stores and, hence, to declining

sales. Between January and July, sales

declined by a total of -1%. Reporting an

increase of 3.2% in like-for-like sales for the

first nine months of the current fiscal year,

GERRY WEBER International AG Interim Report Q3 2013/14

19

GERRY WEBER International AG performed

much better than the market as a whole. At

+7%, sales figures for August showed a very

positive trend, according to Textilwirtschaft,

which makes us optimistic for the fourth

quarter.

Strategic outlook

In the first nine months of the fiscal year

2013/14, we have shown that we are well on

track to reach the targets we have set

ourselves for 2013/14. Due to our unique

brand positioning, our operational strengths,

our customer structure and, most

importantly, the international growth

opportunities, the “GERRY WEBER growth

story” remains intact. We will therefore stick

to our strategies:

The strategic positioning of the GERRY

WEBER Group primarily focuses on the

further expansion, especially outside

Germany, and the ongoing vertical

integration of the business model but also on

the modernisation of our collections in line

with consumer requirements. Our operating

activities in the coming months will therefore

focus on:

Expansion of the Retail operations,

especially in European countries outside

Germany

Ongoing internationalisation of the

distribution structures and, in this context,

expansion of the global market presence

Increase of the international market

penetration of TAIFUN and SAMOON

Ongoing vertical integration through the

reinforcement of the Retail segment, the

concession store model and the maximum

order limit arrangements in the Wholesale

segment

Development and expansion of the multi-

channel approach through the start-up of

the company’s own logistic warehouse

Ongoing modernisation of the collections

We will continue to expand the Retail

segment by opening company-managed

Houses of GERRY WEBER but also other

vertical distribution structures such as

concession stores. The expansion will focus

on neighbouring European countries as well

as Scandinavia and Eastern Europe.

We also intend to grow our Wholesale

segment and will open further Houses of

GERRY WEBER and shop-in-shops together

with franchisees and distribution partners,

primarily outside the eurozone. The main

target regions are Russia, the Middle East

and the US.

Besides the ongoing expansion, vertical

integration is another key element of our

strategic positioning. We aim to exert greater

influence on what products our customers

specify for their stores and to get our

collections to the retail stores as quickly as

possible. We want to provide our Wholesale

partners with more support in optimising their

space management. We offer our distribution

partners to take advantage of our expertise

and our knowledge in the form of our

maximum order limit arrangements, under

GERRY WEBER International AG Interim Report Q3 2013/14

20

which the customer merely specifies an order

limit and our experts choose the products for

the customer’s respective store.

Having implemented our strategies with great

determination over the past years, we will

continue to push them forward in the coming

months in order to allow the GERRY WEBER

Group to continue growing.

Anticipated business performance

Looking back on the first nine months of the

financial year 2013/14 and based on the

assumption of a stable environment,

including positive weather conditions, we

project a positive trend for the company for

the fourth quarter of the financial year

2013/14 and the coming months. While the

economic environment in our German core

market seems to be weakening somewhat

temporarily, spending propensity among

German consumers remains at a high level.

This is not least confirmed by

Textilwirtschaft’s sales figures for August

2014. Should the situation in the current

hotspots deteriorate, however, economic

effects could have an adverse impact on our

customer’s spending propensity. Business

with our Wholesale partners in Russia could

also be adversely affected by further

sanctions.

General statement by the Managing Board

regarding the forecast

By introducing an additional collection

comprising 29 items (NY-Collection) and

launching our first TV commercial we have

laid the basis for achieving our objectives in

Q4 2014/14 - regardless of the general

market situation.

At the nine-month stage of the financial year

2013/14, we continue to believe that we will

reach the performance indicators announced

in January provided that the overall

framework conditions remains unchanged.

GERRY WEBER International AG Interim Report Q3 2013/14

21

Q3 2013/14 Q3 2012/13 9M 2013/14 9M 2012/13

in KEUR 1.5.2014 - 31.7.2014 1.5.2013 - 31.7.2013 1.11.2013 - 31.7.2014 1.11.2012 - 31.7.2013

Sales 187,230.1 188,959.2 600,007.1 592,843.1

Other operating income 4,107.0 4,033.6 11,271.5 11,177.1

Changes in inventories 26,337.5 15,791.5 30,994.5 7,738.6

Cost of materials -102,423.8 -97,397.2 -292,763.5 -281,870.1

Personnel expenses -40,764.5 -37,076.4 -113,767.5 -106,344.8

Depreciation/Amortisation -6,707.2 -5,293.2 -18,969.4 -15,363.0

Other operating expenses -51,501.0 -51,388.4 -150,417.7 -146,673.0

Other taxes -301.7 -273.4 -862.0 -786.1

OPERATING RESULT 15,976.4 17,355.7 65,493.0 60,721.8

Financial result

Income from long-term loans 1.0 1.5 3.0 4.8

Interest income 59.6 -13.7 179.8 32.5

Writedowns on financial assets 0.0 0.0 0.0 0.0

Incidential bank charges -107.2 -246.6 -725.4 -679.3

Interest expenses -1,057.6 -369.6 -3,263.1 -1,566.3

-1,104.2 -628.6 -3,805.7 -2,208.3

RESULTS FROM ORDINARY ACTIVITIES 14,872.1 16,727.1 61,687.3 58,513.5

Taxes on income

Taxes of the reporting period -4,475.1 -5,227.8 -18,769.6 -17,924.6

Deferred taxes -12.4 -22.5 175.7 210.5

-4,487.5 -5,250.3 -18,593.9 -17,714.1

NET INCOME OF THE REPORTING PERIOD 10,384.6 11,476.7 43,093.4 40,799.4

Earnings per share ( basic) 0.23 0.25 0.94 0.89

for the third quarter of 2013/14 (1 May 2014- 31 July 2014)

CONSOLIDATED INSOME STATEMENT (IFRS) in EUR'000

and the first nine months of 2013/14 (1 November 2013 - 31 July 2014)

GERRY WEBER International AG Interim Report Q3 2013/14

22

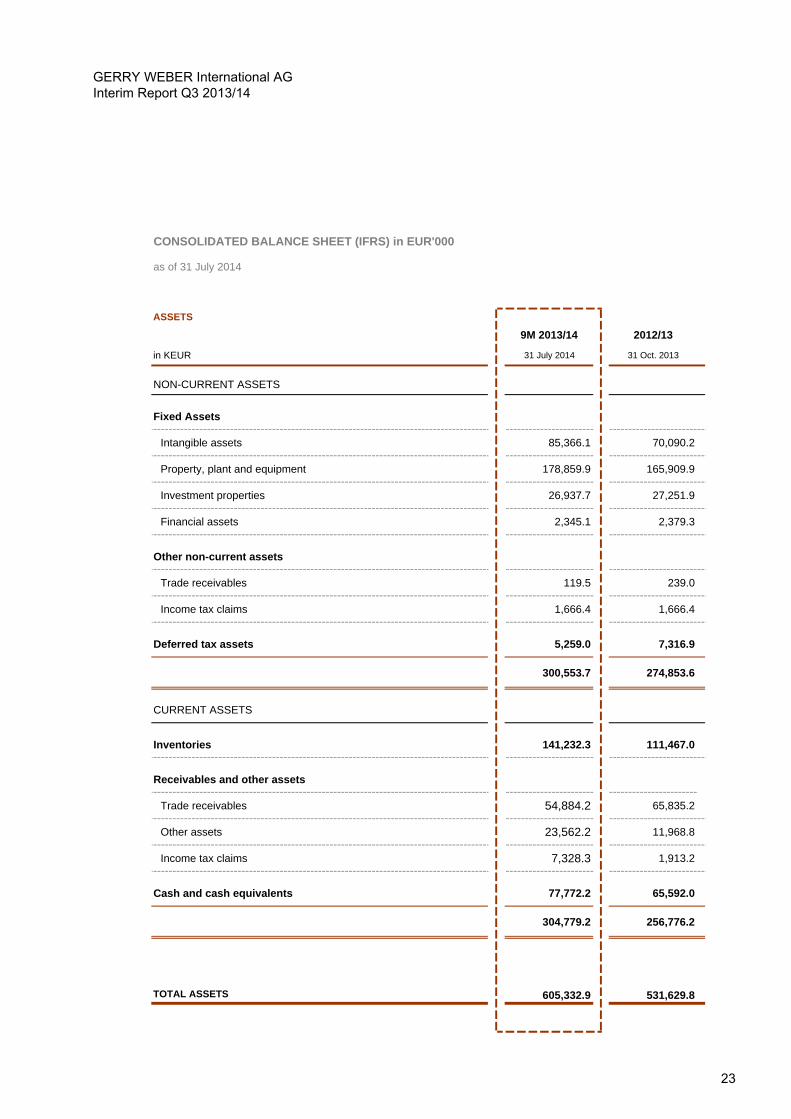

CONSOLIDATED BALANCE SHEET (IFRS) in EUR'000

ASSETS

9M 2013/14 2012/13

in KEUR 31 July 2014 31 Oct. 2013

NON-CURRENT ASSETS

Fixed Assets

Intangible assets 85,366.1 70,090.2

Property, plant and equipment 178,859.9 165,909.9

Investment properties 26,937.7 27,251.9

Financial assets 2,345.1 2,379.3

Other non-current assets

Trade receivables 119.5 239.0

Income tax claims 1,666.4 1,666.4

Deferred tax assets 5,259.0 7,316.9

300,553.7 274,853.6

CURRENT ASSETS

Inventories 141,232.3 111,467.0

Receivables and other assets

Trade receivables 54,884.2 65,835.2

Other assets 23,562.2 11,968.8

Income tax claims 7,328.3 1,913.2

Cash and cash equivalents 77,772.2 65,592.0

304,779.2 256,776.2

TOTAL ASSETS 605,332.9 531,629.8

as of 31 July 2014

GERRY WEBER International AG Interim Report Q3 2013/14

23

CONSOLIDATED BALANCE SHEET (IFRS) in EUR'000

EQUITY AND LIABILITIES

9M 2013/14 2012/13

in KEUR 31 July 2014 31 Oct. 2013

EQUITY

Share capital 45,906.0 45,906.0

Capital reserve 102,386.9 102,386.9

Retained earnings 195,341.7 195,341.7

Accumulated other comprehensive income/loss acc. to IAS 39 1,672.5 -4,223.9

Exchange differences -400.8 -225.5

Accumulated profits 65,245.4 56,581.5

410,151.7 395,766.7

NON-CURRENT LIABILITIES

Provisions for personnel 18.5 60.7

Other provisions 5,816.3 5,479.1

Financial liabilities 85,833.3 5,725.0

Other liabilities 24,324.0 24,836.7

Deferred tax liabilities 12,647.9 12,354.5

128,640.0 48,456.0

CURRENT LIABILITIES

Provisions

Tax liabilities 636.0 1,920.3

Provisions for personnel 11,706.5 13,150.0

Other provisions 8,331.3 8,273.4

LIABILITIES

Financial liabilities 5,636.1 6,008.2

Trade payables 28,629.8 30,330.8

Other liabilities 11,601.5 27,724.4

66,541.2 87,407.1

TOTAL EQUITY AND LIABILITIES 605,332.9 531,629.8

as of 31 July 2014

GERRY WEBER International AG Interim Report Q3 2013/14

24

9M 2013/14 Capital stock Capital Retained Accumulated Exchange Accumulated Equityreserves earnings other comp differences profits

in KEUR income / loss

As of 1 November 2013 45,906.0 102,386.9 195,341.7 -4,223.9 -225.6 56,581.5 395,766.6

Sale of own shares -34,429.4 -34,429.4

Allocation of retained earnings of the AG from the net income of the year

0.0

Adjustments of exchange differences -175.2 -175.2

Changes in equity acc. to IAS 39 5,896.4 5,896.4

Net income of the reporting period 43,093.3 43,093.3

As of 31 July 2013 45,906.0 102,386.9 195,341.7 1,672.5 -400.8 65,245.4 410,151.7

9M 2012/13 Capital stock Capital Retained Accumulated Exchange Accumulated Equityreserves earnings other comprehensdifferences profits

in KEUR income/loss

As of 1 November 2012 45,906.0 102,386.9 140,341.7 -212.5 -400.5 74,983.1 363,004.7

Sale of own shares -34,429.4 -34,429.4

Allocation of retained earnings of the AG from the net income of the year

20,000.0 -20,000.0 0.0

Adjustments of exchange differences -156.6 -156.6

Changes in equity acc. to IAS 39 303.1 303.1

Net income of the reporting period 40,799.4 40,799.4

As of 31 July 2013 45,906.0 102,386.9 160,341.7 90.6 -557.1 61,353.1 369,521.2

STATEMENT OF CHANGES IN GROUP EQUITY (IFRS) in EUR'000for the first nine months of 2013/14 (1 November 2013 - 31 July 2014)

GERRY WEBER International AG Interim Report Q3 2013/14

25

CONSOLIDATED CASH FLOW STATEMENT (IFRS) in EUR'000

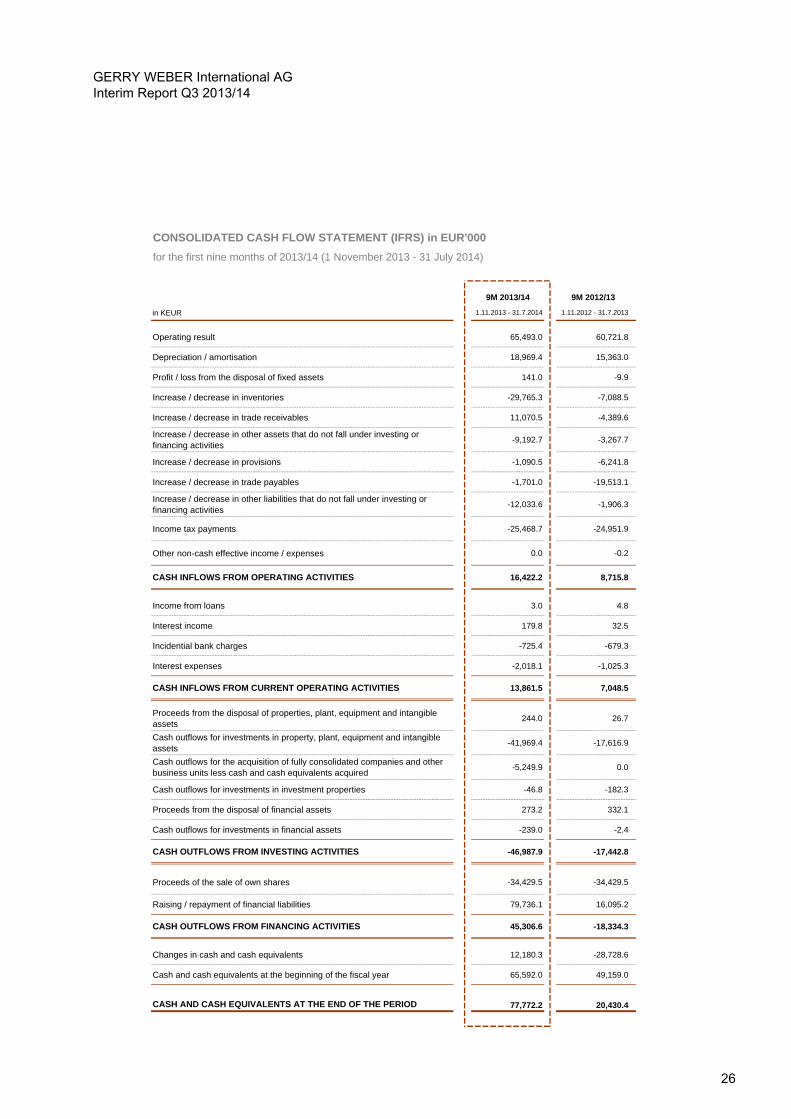

9M 2013/14 9M 2012/13

in KEUR 1.11.2013 - 31.7.2014 1.11.2012 - 31.7.2013

Operating result 65,493.0 60,721.8

Depreciation / amortisation 18,969.4 15,363.0

Profit / loss from the disposal of fixed assets 141.0 -9.9

Increase / decrease in inventories -29,765.3 -7,088.5

Increase / decrease in trade receivables 11,070.5 -4,389.6

Increase / decrease in other assets that do not fall under investing or financing activities

-9,192.7 -3,267.7

Increase / decrease in provisions -1,090.5 -6,241.8

Increase / decrease in trade payables -1,701.0 -19,513.1

Increase / decrease in other liabilities that do not fall under investing or financing activities

-12,033.6 -1,906.3

Income tax payments -25,468.7 -24,951.9

Other non-cash effective income / expenses 0.0 -0.2

CASH INFLOWS FROM OPERATING ACTIVITIES 16,422.2 8,715.8

Income from loans 3.0 4.8

Interest income 179.8 32.5

Incidential bank charges -725.4 -679.3

Interest expenses -2,018.1 -1,025.3

CASH INFLOWS FROM CURRENT OPERATING ACTIVITIES 13,861.5 7,048.5

Proceeds from the disposal of properties, plant, equipment and intangible assets

244.0 26.7

Cash outflows for investments in property, plant, equipment and intangible assets

-41,969.4 -17,616.9

Cash outflows for the acquisition of fully consolidated companies and other business units less cash and cash equivalents acquired

-5,249.9 0.0

Cash outflows for investments in investment properties -46.8 -182.3

Proceeds from the disposal of financial assets 273.2 332.1

Cash outflows for investments in financial assets -239.0 -2.4

CASH OUTFLOWS FROM INVESTING ACTIVITIES -46,987.9 -17,442.8

Proceeds of the sale of own shares -34,429.5 -34,429.5

Raising / repayment of financial liabilities 79,736.1 16,095.2

CASH OUTFLOWS FROM FINANCING ACTIVITIES 45,306.6 -18,334.3

Changes in cash and cash equivalents 12,180.3 -28,728.6

Cash and cash equivalents at the beginning of the fiscal year 65,592.0 49,159.0

CASH AND CASH EQUIVALENTS AT THE END OF THE PERIOD 77,772.2 20,430.4

for the first nine months of 2013/14 (1 November 2013 - 31 July 2014)

GERRY WEBER International AG Interim Report Q3 2013/14

26

Explanatory notes on the interim consolidated financial statements of GERRY WEBER International AG for the

period ended 31 July 2014 (first nine months of the fiscal year 2013/14)

General information and accounting basis

GERRY WEBER International AG is a listed joint stock company headquartered in

Neulehenstraße 8, D – 33790 Halle (Westphalia/Germany).

The present abridged consolidated financial statements were prepared pursuant to section 37x

para. 3 WpHG in accordance with the International Financial Reporting Standards (IFRS) and

the related interpretations by the International Accounting Standards Board (IASB) for interim

financial reporting such as they have been adopted by the European Union. Accordingly, these

financial statements do not contain all information and notes that are required for year-end

consolidated financial statements pursuant to IFRS.

The interim consolidated financial statements for the third quarter 2013/14 (1 November 2013

– 31 July 2014) were prepared in accordance with IAS 34 “Interim Financial Reporting“ and

were not reviewed by the auditors. The accounting and valuation methods and the principles of

consolidation have basically remained unchanged compared to the latest consolidated

financial statements for the year ended 31 October 2013. The interim consolidated financial

statements for the third quarter and the first nine months of the fiscal year 2013/14 were

prepared in Euros.

The Managing Board is of the opinion that the present unaudited interim consolidated financial

statements contain all necessary information to give a true and fair view of the business

performance and the earnings position in the reporting period. The results achieved in the first

nine months of the financial year 2013/14 (1 November 2013 – 31 July 2014) do not

necessarily provide an indication as to the future results.

Pursuant to IAS 34 “Interim Financial Reporting“, the Managing Board must make

discretionary decisions, estimates and assumptions in the preparation of the interim

consolidated financial statements. These may influence the application of accounting

standards and the recognition of assets and liabilities as well as income and expenses. The

actual results may differ from these estimates in individual cases.

The present interim consolidated financial statements comprise the interim financial

statements of GERRY WEBER International AG and all its subsidiaries for the period ended

31 July 2014. The subsidiaries are fully consolidated. As of the reporting date, the basis of

consolidation comprises 37 subsidiaries. In five of its subsidiaries abroad GERRY WEBER

GERRY WEBER International AG Interim Report Q3 2013/14

27

International AG holds 51% interest stake; in the rest the company holds 100%. All

subsidiaries have been integrated into the consolidated financial statements in accordance

with the rules for full consolidation.

Currency translation

The functional currency of GERRY WEBER International AG is the euro. Foreign currency

transactions in the separate financial statements of GERRY WEBER International AG and its

subsidiaries are translated at the exchange rates prevailing at the time of the transaction. As of

the balance sheet date, monetary items in foreign currency are shown at the closing rate.

Exchange differences are recognised in profit or loss.

The interim financial statements of the consolidated Group companies prepared in foreign

currencies are translated according to the concept of the functional currency using the

modified closing rate procedure. Accordingly, assets and liabilities, with the exception of equity

capital, are translated at the closing rate, while income and expenses are translated at the

average annual exchange rate. Effects from the currency translation of the equity capital are

recognised in equity.

Intangible assets

Goodwill is recognised in accordance with IFRS 3 and tested for impairment on an annual

basis and whenever there are indications of impairment.

Purchased intangible assets are recognised at cost, taking ancillary costs and cost reductions

into account, and amortised using the straight-line method. Furthermore, the item includes

exclusive rights of supply to Houses of GERRY WEBER operated by third parties as well as

advantageous lease agreements resulting from acquired stores. The advantageous lease

agreements recognised as depreciable intangible assets are written down over the remaining

term of the leases using the straight-line method. In addition, customer relationships were

identified in the context of the takeover of 51% shares in three Belgian and two Dutch

companies, which have been recognized at the present value. The same applies for the

acquisition of 25 Norwegian stores, which have been fully consolidated in the consolidated financial

statement of GERRY WEBER International AG since 1 June 2014.

Due to the majority takeover in three Belgian companies in August 2013 and the acquisition of

two operating companies of the 25 Norwegian stores in June 2014, intangible assets

increased from EUR 70.1 million as of 31 October 2013 to EUR 85.4 Mio. at the end of the

reporting period Q3.

GERRY WEBER International AG Interim Report Q3 2013/14

28

Accumulated other comprehensive income / loss

The GERRY WEBER International AG Group holds derivative financial instruments only to

hedge currency risks arising from operations. According to IAS 39, all derivative financial

instruments must be recognised at their fair value. If the financial instruments used are

effective hedges in the context of a hedging relationship as defined in IAS 39 (cash flow

hedges), fluctuations in the fair value have no effect on profit or loss during the term of the

derivative. Fluctuations in the fair value are recognised in the respective equity item. The

effects of the remeasurement of financial instruments accounted after taxes. As at 31 July

2014 effects of the fluctuations in the fair value of financial instruments were recognised after

deferred taxes in the respectively equity item in an amount of EUR 1.7 million (31 October

2013: EUR -4.2 million).

Financial liabilities (non-current)

As at 31 July 2014 non-current financial liabilities increased in comparison to the end of fiscal

2012/13 from EUR 5.7 million to EUR 85.8 million. The increase is due to the issuance of a

EUR 75 million note loan in November 2013, which will be used, among other things, to

finance the planned logistic centre as well as general working capital requirements.

Oversubscribed several times, the note loan was issued at 100% of the nominal value and will

be repaid at the end of the respective term. Investors could choose between terms of three,

five and seven years as well as fixed and variable interest rates. The average fixed interest

rate is 2.3%. Across all tranches the interest rate in the first nine month of the fiscal year was

below 2 %.

Other liabilities (non-current)

GERRY WEBER International AG holds 51% of the shares in the Dutch GERRY WEBER

Retail B.V. and GERRY WEBER Incompany B.V. as well as in the Belgian ARW Retail –

GERRY WEBER NV, Coast Retail – GERRY WEBER NV and ARW – GERRY WEBER Belux

BVBA. The acquired companies sell textiles at retail level and operated retail stores as well as

concession shops in the Netherlands and Belgium. For the remaining 49% shares in the

named companies, Gerry Weber International AG has a call option, while the seller has a put

option. Pursuant to IAS 32, these obligations must be recognised at fair value. Liabilities from

minority options were recognised under other non-current liabilities and amounted to EUR 24.3

million on 31 July 2014 (31 October 2013: EUR 24.8 million).

GERRY WEBER International AG Interim Report Q3 2013/14

29

Earnings per share

Earnings per share are determined on the basis of the net income for the period after taxes

that is attributable to the shareholders of GERRY WEBER International AG and the average

number of shares outstanding in the reporting period.

The average number of shares outstanding is determined on a pro-rata temporis basis as

shown below.

Accordingly, earnings per share of Q3 2013/14 (1.02.2013 – 31.07.2014) amounted to EUR

0.23 (Q3 previous year: EUR 0.25). Thus earnings per share amount to EUR 0.94 for the first

nine months of the fiscal year 2013/14. (9M 2012/13: EUR 0.89).

Segment reporting

GERRY WEBER International AG distinguishes in two main segments: “Production and

Wholesale“ and “Retail“ as well as in “other segments”. The Wholesale segment comprises all

distribution structures with external customers; these include the franchised Houses of GERRY

WEBER worldwide, the shop-in-shops in our retail partners’ stores as well as the multi-label

business. The ”Production and Wholesale“ segment also comprises all development and

production processes for our merchandise, including transport and logistics. The “Retail“

segment is almost exclusively a distribution segment and includes all company-managed

Houses of GERRY WEBER, monolabel stores, concession shops, outlet stores as well as the

individual national online shops. Other segments comprises in particular earnings and

expenses as well as assets and liabilities of our investment property „Hall 30”. Income and

9M 2013/14 9M 2012/13

1.11.2013-31.7.2014 1.11.2012-31.7.2013

November 2013 45,905,960 x 1/12 45,905,960 x 1/12

December 2013 45,905,960 x 1/12 45,905,960 x 1/12

January 2014 45,905,960 x 1/12 45,905,960 x 1/12

February 2014 45,905,960 x 1/12 45,905,960 x 1/12

March 2014 45,905,960 x 1/12 45,905,960 x 1/12

April 2014 45,905,960 x 1/12 45,905,960 x 1/12

May 2014 45,905,960 x 1/12 45,905,960 x 1/12

June 2014 45,905,960 x 1/12 45,905,960 x 1/12

July 2014 45,905,960 x 1/12 45,905,960 x 1/12

= 45,905,960 units = 45,905,960 units

GERRY WEBER International AG Interim Report Q3 2013/14

30

expenses as well as assets and liabilities of the holding company are assigned to the

segments as incurred.

3rd Quarter 2013/14 Production and Retail Other Consolidated Totalwholesale segments entries

in KEUR

Sales by segment 82.297,9 104.932,2 0,0 0,0 187.230,1

EBT (Earnings Before Tax) 7.557,4 5.244,3 446,0 1.624,4 14.872,1

Depreciation of property, plant and equipment 2.474,9 4.084,8 147,5 0,0 6.707,2

Interest income 113,7 8,1 0,0 -62,3 59,5

Interest expenses 444,8 681,6 0,0 -68,8 1.057,6

Assets 397.845,7 300.316,4 29.795,7 -122.624,9 605.332,9

Liabilities 73.158,7 245.804,4 0,0 -123.781,9 195.181,2

Investments in non-current assets 12.140,3 19.633,3 14,6 0,0 31.788,2

Number of employees (31 July 2014) 1.281 3.675 1 0 4.957

3rd Quarter 2012/13 Production and Retail Other Consolidated Totalwholesale segments entries

in KEUR

Sales by segment 95.817,8 93.141,4 0,0 0,0 188.959,2

EBT (Earnings Before Tax) 17.668,6 448,2 404,6 -1.794,3 16.727,1

Depreciation of property, plant and equipment 2.550,0 3.052,1 153,7 -462,7 5.293,1

Interest income 167,2 14,6 0,0 -195,5 -13,7

Interest expenses 220,7 108,3 0,0 40,6 369,6

Assets 346.235,3 220.903,4 30.234,0 -119.764,0 477.608,7

Liabilities 53.736,4 169.748,1 0,0 -115.396,9 108.087,6

Investments in non-current assets 1.649,5 1.653,1 97,2 0,0 3.399,8

Number of employees (31 July 2013) 1.370 3.352 1 0 4.723

GERRY WEBER International AG Interim Report Q3 2013/14

31

A detailed segment report is stated in the management report of this interim report.

9M 2013/14 Production and Retail Other Consolidated Totalwholesale segments entries

in KEUR

Sales by segment 306.432,5 293.574,6 0,0 0,0 600.007,1

EBT (Earnings Before Tax) 39.052,4 19.137,5 1.363,9 2.133,5 61.687,3

Depreciation of property, plant and equipment 7.249,6 11.276,2 443,6 0,0 18.969,4

Interest income 344,9 61,8 0,0 -226,9 179,8

Interest expenses 1.644,7 1.840,7 0,0 -222,2 3.263,2

Assets 397.845,7 300.316,4 29.795,7 -122.624,9 605.332,9

Liabilities 73.158,7 245.804,4 0,0 -123.781,9 195.181,2

Investments in non-current assets 18.669,8 28.794,1 46,8 0,0 47.510,7

Number of employees (31 July 2014) 1.281 3.675 1 0 4.957

9M 2012/13 Ladiesware Ladiesware Other Consolidated Totalproduction and Retail segments entries

in KEUR wholesale

Sales by segment 333.144,1 259.699,0 0,0 0,0 592.843,1

EBT (Earnings Before Tax) 51.110,5 4.981,2 1.202,8 1.219,0 58.513,5

Depreciation of property, plant and equipment 7.186,5 7.900,7 438,7 -163,0 15.362,9

Interest income 328,1 14,6 0,0 -310,1 32,6

Interest expenses 1.115,6 657,5 0,0 -206,7 1.566,4

Assets 346.235,3 220.903,4 30.234,0 -119.764,0 477.608,7

Liabilities 53.736,3 169.748,1 0,0 -115.396,9 108.087,5

Investments in non-current assets 6.355,1 10.888,4 558,4 0,0 17.801,9

Number of employees (31 July 2013) 1.370 3.352 1 0 4.723

GERRY WEBER International AG Interim Report Q3 2013/14

32

Financial Calendar

Investor Relations Contact:

GERRY WEBER International AG

Neulehenstraße 8

33790 Halle / Westphalia

www.gerryweber.com

Claudia Kellert Anne Hengelage

Head of Investor Relations Manager Investor Relations

phone: +49 (0) 5201 185 0 phone: +49 (0) 5201 185 0

email: [email protected] email: [email protected]

Disclaimer

This interim report contains forward-looking statements that are based on assumptions and/or

estimates by the management of GERRY WEBER International AG. While it is assumed that

these forward-looking statements are realistic, no guarantee can be given that these

expectations will actually materialise. Rounding differences may occur in the percentages and

figures stated in this report

Publication of the Nine Month Report 2013/14 12 September 2014

Merrill Lynch Global Consumer Conference, London 18 September 2014

Baader Investment Conference, Munich 24 September 2014

Roadshow Zurich, Lugano 29/30 September 2014

MM Warburg London Conference 19 November 2014

End of the fiscal year 2013/14 31 October 2014

GERRY WEBER International AG Interim Report Q3 2013/14

33