overview of comments received on proposed changes … received on reg cc propos… · overview of...

TRANSCRIPT

Overview of Comments Received onProposed Changes to Regulation CC

August 3, 2011Joseph Baressi

Financial Services Project LeaderRetail Payments Section

Division of Reserve Bank Operations and Payment Systems

202-452-3959

1

Agenda

• Recent history

• Overview of current regulation

• Walk-through of topics

– Current regulation

– Board’s proposal

– Comments

2

Disclaimer

• I am expressing my personal views, not the Board’s position.

• This presentation includes only an overview of the proposal and the public comments received. I will not address every topic raised by the proposal or by the public comments.

• With respect to the topics that are discussed, the presentation does not purport to –– Capture all comment letters or completely reflect the content of any

single comment letter; – Assess the value or strength of the comments.

• Possibilities with respect to any future final rule will not be discussed.

3

Recent History

• Reg CC proposal published on Board website on March 3.– www.federalreserve.gov/newsevents/press/bcreg/20110303a.htm

• Proposal published in Federal Register on March 25.– http://edocket.access.gpo.gov/2011/pdf/2011-5449.pdf

• Public comment period closed on June 3. Comments received are posted on the Board’s website.– http://www.federalreserve.gov/generalinfo/foia/index.cfm?doc_id=R-

1409&doc_ver=1&ShowAll=Yes– (The comments can also be reached via the press-release page.)

• The Consumer Financial Protection Bureau launched on July 21, 2011.– Any final rule with respect to the proposed revisions to the funds-

availability provisions (subpart B) would be joint with the Bureau.

4

Overview of Current Regulation

• Subpart A – definitions.

• Subpart B – funds-availability provisions.– Implements the Expedited Funds Availability Act of 1987.

• Subpart C – collection and return of checks.– Adopted by the Board pursuant to the regulatory authority

granted to it under the EFAA.– Can be varied by agreement. (§ 229.37)

• Subpart D – substitute checks.– Implements the Check 21 Act of 2003.– Cannot be varied by agreement, except as specified. (§ 229.60)

5

Walk-Through of Topics

6

Funds-Availability Provisions

7

Eliminate Obsolete ProvisionsRelated to Nonlocal Checks

Current rule: Local and nonlocal checks must be made available for withdrawal within 2 and 5 business days, respectively.

Note: “Nonlocal checks” is a null set.

Proposal: Eliminate distinctions between local and nonlocal checks and limit the general hold period to 2 business days.

Comments received: Supportive.

8

Proposed Revisions to the ModelFunds-Availability Hold Notices

Current rule: Sections 229.13(g) and 229.16(c) require a bank to provide notice to the customer of a hold the bank places on deposited funds. Appendix C to the regulation provides model notices.

Proposal: Changes related to the format, content, and timing/delivery of the hold notices.

Comments received: Strong concerns.• Dislike the tabular format, 8.5 x 11 paper size, and

the addition of the total deposit amount.• Dislike the proposed changes related to delivery of

the notices. But, a few did support.9

Proposed Revisions to the ModelFunds-Availability Policy Disclosures

Current rule: Various sections of subpart B contain provisions applicable to a bank’s disclosure of its funds-availability policy. Appendix C provides model disclosures.

Proposal: Change disclosures’ format and content.

Comments received: Mixed.• Concern with 8.5 x 11 paper size.• Some general support for the tabular format and revised,

briefer language.• But, in the context of this general support, many voiced

specific concerns. E.g., the wording of the proposed disclosures’ new language related to a bank’s charge back of a check that is returned unpaid.

10

Safe-Harbor Period for Exception Holds

Current rule: A bank may apply an exception hold to a check deposit in certain circumstances. The safe-harbor period for the exception hold is 7 business days.

Proposal: Shorten this safe harbor to 4 business days. A longer exception hold would continue to be permitted, but the bank would have the burden of demonstrating the hold was reasonable.

Comments received: Very few comments in support.• Many stated that, if shortened, the safe harbor should be

no less than 5 business days.• Many credit unions and associations opposed any

shortening of the safe harbor.

11

Other Topics

Raised by proposal:

• Availability of deposits at non-proprietary ATMs.

• Repeated overdrafts exception; declined debit-card authorizations.

Raised by comments:

• Whether the funds-availability provisions apply to items deposited through remote deposit capture (RDC).

• Modifying the § 229.13(e) exception hold, reasonable cause to doubt collectibility, to address –– An unauthorized ACH credit.– A check drawn on a retired routing number.

12

Electronic CheckClearing and Return

13

Expeditious Return Requirement

Current rule: A paying bank that determines not to pay a check must return the check expeditiously, unless an exception applies.

Proposal: Add a new exception ((§ 229.30(b)): The expeditious return requirement does not apply if the depositary bank has not agreed to accept returned checks electronically.

Comments received: Almost all in support.

BUT…14

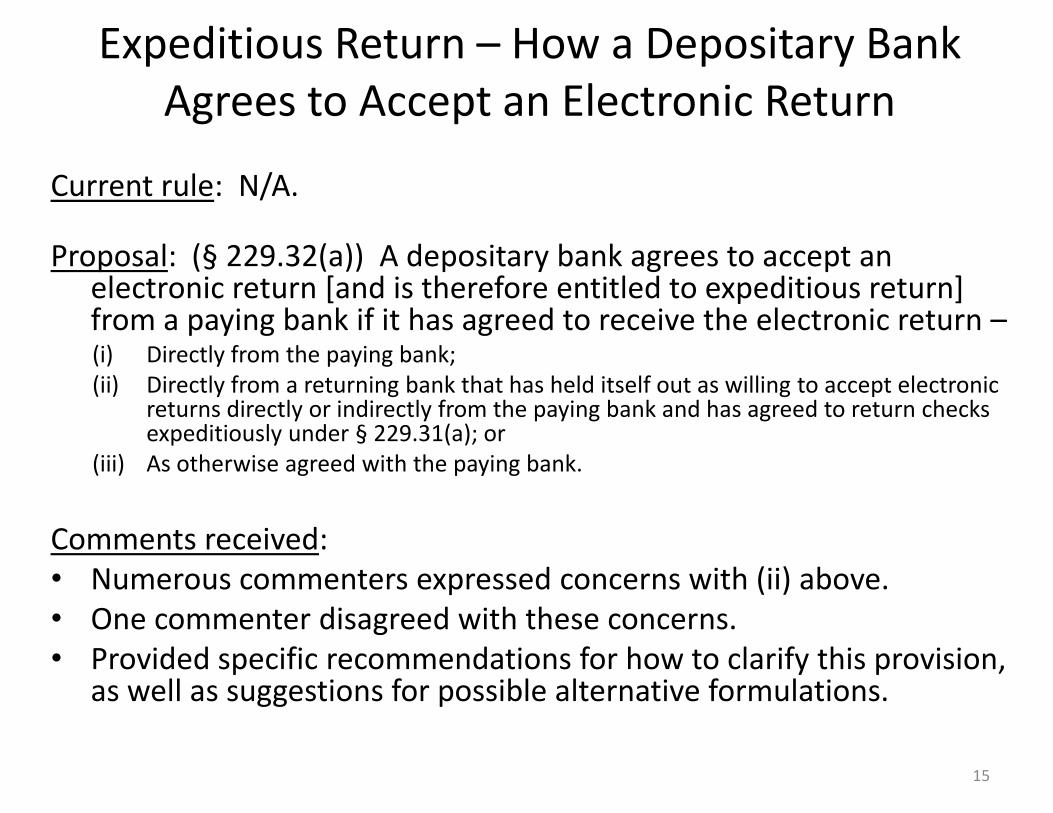

Expeditious Return – How a Depositary Bank Agrees to Accept an Electronic Return

Current rule: N/A.

Proposal: (§ 229.32(a)) A depositary bank agrees to accept an electronic return [and is therefore entitled to expeditious return] from a paying bank if it has agreed to receive the electronic return –(i) Directly from the paying bank;(ii) Directly from a returning bank that has held itself out as willing to accept electronic

returns directly or indirectly from the paying bank and has agreed to return checks expeditiously under § 229.31(a); or

(iii) As otherwise agreed with the paying bank.

Comments received: • Numerous commenters expressed concerns with (ii) above.• One commenter disagreed with these concerns.• Provided specific recommendations for how to clarify this provision,

as well as suggestions for possible alternative formulations.

15

Notice of Nonpayment Requirement

Current rule: A paying bank that declines to pay a check over $2,500 must provide notice of nonpayment to the depositary bank by 2 business days after the day the check was presented to the paying bank.

Proposal: Eliminate the notice of nonpayment requirement.

Comments received: Mixed. Some support, but also some credit unions and their associations opposed.

16

Definition of Electronic Collection Item

Current rule: N/A.

Proposal: Define new term, electronic collection item, in proposed § 229.2(s) (and electronic return in § 229.2(v)).

Comments received:

• Paying bank has agreed to receive.– Commenters found this prong of the definition to be too limiting.

• Is sufficient to create a substitute check.– General support.

• Some commenters requested clarification that banks can agree to collect electronic check images or data, notwithstanding that the image/data is not an ECI, and that the provisions of the regulation would not apply to exchanges of such image/data.

• One commenter expressed opposition to the possibility of such an arrangement.

• Conforms with X9.100-187 and its UCD, unless parties otherwise agree.– Comments mixed.

17

Transfer and Presentment Warranties for an Electronic Collection Item or Electronic Return

Current rule: N/A.

Proposal: (§ 229.34(a)) Apply new “Check-21-like” warranties to an electronic collection item and electronic return.

Comments received:• Generally supportive.• Opposition to extending the proposed new warranties to the

drawer or owner of the check.• Some commenters requested clarification that the warranties

may be varied by agreement; for example, in the case of electronic items known to contain imperfect images.– One commenter expressed opposition to the possibility of varying the

warranties by agreement.

18

Electronically Created Items

Current rule: N/A.

Proposal: (§ 229.34(e)) The warranties in § 229.34, including the proposed new Check-21-like warranties, would apply when a bank transfers or presents an electronic image and related electronic information as if it were an electronic collection item or electronic return.

– Would protect a bank that receives an electronic item against potential liability resulting from creating a substitute check for which there was no prior original check.

– The regulation’s current warranty of authorization for a remotely created check (RCC)(§ 229.34(c)) would apply to a “paperless RCC.”

Comments received: Generally supportive.• Some commenters thought the proposal should go farther –

– Make paperless RCCs subject to all provisions of subpart C.– Modify the regulation’s original check definition to include paperless RCCs, such that they

would be checks for all purposes of the regulation.

• Suggestions that the rule clarify that banks exchanging electronic items may agree to vary or waive the application of § 229.34(e).

• Differing views as to whether an “electronic payment order” should be addressed by the regulation.

19

Same-Day Settlement Rule

Current rule: Paying banks must provide same-day settlement for paper checks presented in accordance with certain requirements.

Proposal: Allow a paying bank to require checks presented for same-day settlement to be presented electronically. A paying bank, however, must have agreed to receive electronic collection items from the presenting bank under proposed § 229.36(a).

Comments received:• Many commenters found the proposal to be unclear, and

requested re-proposal.• Others supported the proposal, but recommended

clarifications.

20

Refer to Maker Reason for Return

Current rule: Commentary to § 229.30(d) states that a reason for return such as “Refer to Maker” is permissible in appropriate cases.

Proposal: Amend the commentary to state that refer to maker is insufficient as a reason for return, because it is an instruction to the recipient of the returned check and not a reason for return (e.g., insufficient funds).

Comments received:• Almost all expressed concern or opposition –

– For positive-pay items, the drawer may want the payee to contact it, and the paying bank may not know the factual basis for the drawer’s refer to maker instruction.

– Because refer to maker is used in positive-pay and RDC systems, banks and their customers would need at least 2 years to make the necessary changes.

– Question what prompted the proposed change at this time.

• One commenter supported the proposal.

21

Other Topics

Raised by proposal:

• Notice in lieu of return.

• Modification of midnight-deadline extension in § 229.30(c).

• Qualification of returned checks.

Raised by comments:

• Requests to re-visit regulation’s definition of remotely created check.

• Suggestion that a new paragraph (e) be added to § 229.36 –

– (e) Presumption of alteration for certain checks. When a paying bank or a draweepays a check that was presented as a substitute check or an electronic collection item, and not the original check, and there is a claim that such check was payable in an amount or to a person not authorized by the drawer, the original check shall be presumed to have been altered unless it can be proven otherwise by a preponderance of the evidence.

22