outlook on indian equity market – july 2014 fileby icra, an associate of moody’s investors...

TRANSCRIPT

For institutional investors

1

Outlook on Indian Equity Market – July 2014

Canara Robeco is a meeting of two renowned financial service institutions to bring together their core competencies

The Partnership • Asset Management expertise from Robeco, a global pure-play asset

manager and distribution expertise and local understanding from Canara Bank

• Canara Bank holds 51% in the JV while Robeco Group NV holds 49%

2

Canara HSBC Oriental Life

Insurance

Canbank Factors Limited

Gilt Securities Trading CanFin Homes

Canara Robeco Asset

Management

Canbank Venture Capital

Fund

Cancan Computer Services

Canbank Financial Services

Canara Bank : 106 years of banking expertise

Global CSR Excellence and Leadership Awards 2014 from CSR World Congress

55 Million+ customers & over 4750 branches to service them

Rated AAA* by ICRA, An associate of Moody’s

Investors service

Aggregate business balance sheet of INR 4.62 Lac Crs

*Rating reaffirmed by ICRA on Dec 18 2013

3

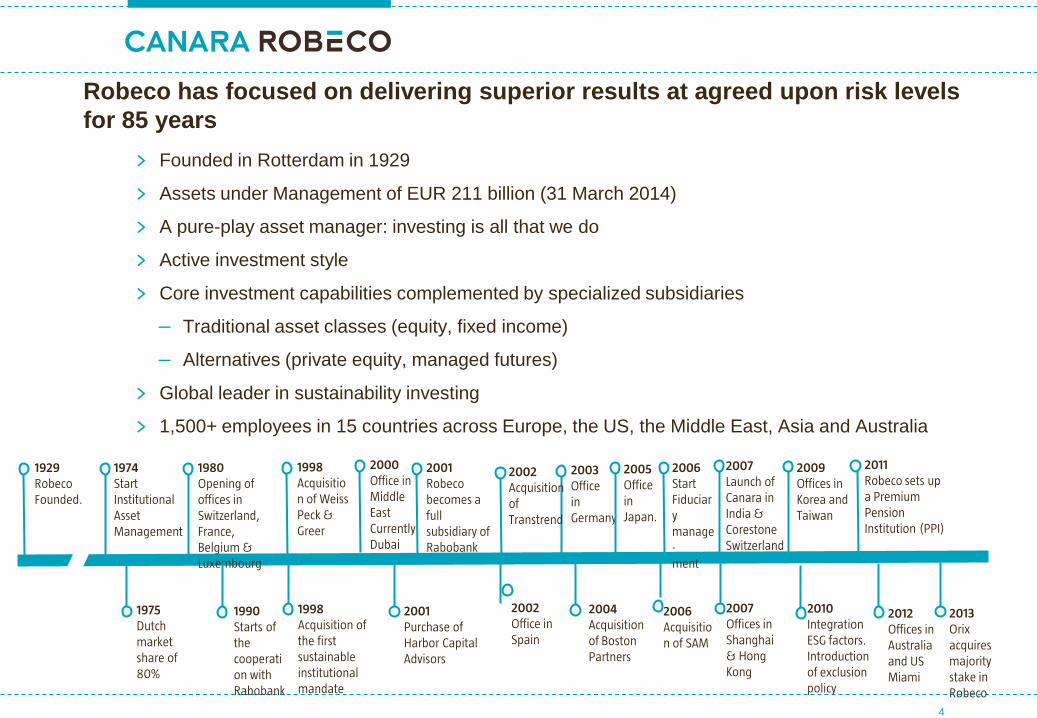

> Founded in Rotterdam in 1929

> Assets under Management of EUR 211 billion (31 March 2014)

> A pure-play asset manager: investing is all that we do

> Active investment style

> Core investment capabilities complemented by specialized subsidiaries

– Traditional asset classes (equity, fixed income)

– Alternatives (private equity, managed futures)

> Global leader in sustainability investing

> 1,500+ employees in 15 countries across Europe, the US, the Middle East, Asia and Australia

4

1929 Robeco Founded.

1980 Opening of offices in Switzerland, France, Belgium & Luxembourg

1975 Dutch market share of 80%

1990 Starts of the cooperation with Rabobank

2002 Office in Spain

2007 Offices in Shanghai & Hong Kong

2007 Launch of Canara in India & Corestone Switzerland

2010 Integration ESG factors. Introduction of exclusion policy

2011 Robeco sets up a Premium Pension Institution (PPI)

2012 Offices in Australia and US Miami

2003 Office in Germany

2001 Robeco becomes a full subsidiary of Rabobank

2001 Purchase of Harbor Capital Advisors

2000 Office in Middle East Currently Dubai

2005 Office in Japan.

1974 Start Institutional Asset Management

1998 Acquisition of the first sustainable institutional mandate

1998 Acquisition of Weiss Peck & Greer

2006 Start Fiduciary manage- ment

2006 Acquisition of SAM

2004 Acquisition of Boston Partners

2002 Acquisition of Transtrend

2009 Offices in Korea and Taiwan

2013 Orix acquires majority stake in Robeco

Robeco has focused on delivering superior results at agreed upon risk levels for 85 years

Disciplines to maintain Portfolio Management Focus

Back Office

Trading

Risk Management

Client Servicing

Compliance

Canara Robeco

Local expertise, International strength

5

Investment Management Mid Office

Product Management

6

Asset under Management

2123.19

151.86

3952.53

144.32

Month end AUM as on 30th June, 2014 (Rs. in crores)

Equity ETF Fixed Income Fund of Fund

CANARA ROBECO – Equity Team Ravi Gopalkrishnan, Head - Equities Fund Manager - CR Equity Diversified, Large Cap+, Infrastructure, Emerging Equities, MIP Responsible for overall performance Indian equities. Focus on fundamentals, integrates macro view –MS in Finance from Drexel University, Philadelphia, MBA in Finance from Bradley University, Peoria, IL –24 years of experience, in research and asset management with Pramerica AM, Principal PNB AM, SUN F&C & UTI –With Canara Robeco since September 2012

Krishna Sanghvi, Senior Fund Manager - Equities Fund Manager - CR Equity Tax Saver, Balance, FORCE, Capital Protection Oriented Fund Series 2 Co - Fund Manager - Emerging Equities Responsible for fund management –MMS (Finance) from NMIMS, ICWA, CFA from ICFAI University –17 years of experience in the Financial Services Industry including Kotak Mahindra Finance and Kotak AM –With Canara Robeco since September 2012

Nimesh Chandan, Head - Offshore Investments and Business Development

Responsible for advising portfolios of international clients

– MBA from University of Mumbai – 12 years of research & asset management

experience with Birla Sunlife, SBI Socgen and ICICI Prudential amongst others

– With Canara Robeco since July 2008

Yogesh Patil, Co-Fund Manager Co - Fund Manager - CR Infrastructure

– MBA from University of Pune – 11 years of experience with Sahara Mutual Fund, Religare, Man

Financial and UTI securities – With Canara Robeco since October 2009

Hemang Kapasi, Indian Equity Analyst Co Fund Manager : CR FORCE Focus on fundamental research − 9 Years of experience − joined October 2008

7

India’s Present: An opportunity

Stable Government at centre - Mr. Modi provides justification for the optimism

Reform push expected from new Government

FII positive on Indian market

Strong economic recovery expected

8

• January ’14

• Global liquidity driving most asset

classes

• Risk of accelerated FED Tapering

• Markets expecting a change in

Government at the centre

• Improving current a/c and trade

balances

• Declining inflation trajectory and

expectation of stable to declining

interest rates

9

What has changed post election and Budget…?

• June ’14 • India witnesses a majority government after

three decades with BJP garnering highest

ever 282 seats

• Expectation of Good days ahead, with focus

on growth and employment creation

• Continuation of measures to curtail fiscal

deficit by the new government

• Foreign flows continues to remain strong in

Indian markets

• Expectation of Interest rates decline in 6 to 9

months period

What has changed….

Improving Current account and Trade balance on the back of improving exports and lower non-gold imports

Declining inflation trajectory & Stable to declining interest rates - Inflation has come off sharply in last quarter, especially the consumer price inflation

Index of Industrial production has recorded some improvement in the last two months after moving in a narrow range for an year

10

Increased confidence in India is visible in the India allocation of GEMs Funds as well

12

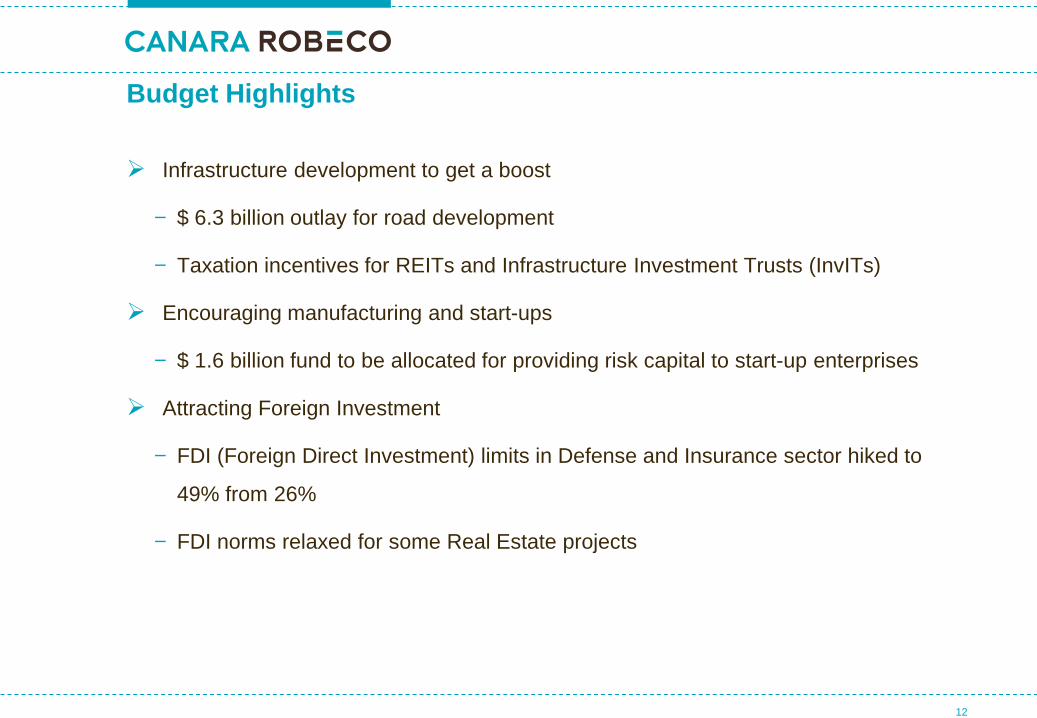

Budget Highlights

Infrastructure development to get a boost

− $ 6.3 billion outlay for road development

− Taxation incentives for REITs and Infrastructure Investment Trusts (InvITs)

Encouraging manufacturing and start-ups

− $ 1.6 billion fund to be allocated for providing risk capital to start-up enterprises

Attracting Foreign Investment

− FDI (Foreign Direct Investment) limits in Defense and Insurance sector hiked to

49% from 26%

− FDI norms relaxed for some Real Estate projects

13

Going forward...

Revival in Investment Growth

Liberalisation of FDI

Subsidy Reduction

Control on Inflation

Tax Reforms – Implementation of GST (Goods and Services Tax) and DTC (Direct

Tax Code). Should add 1.5% to the GDP when fully implemented

• Markets have run up a lot....... • Is this the right time to buy ?

Empirical evidence suggest periods of high growth have always been accompanied by above average valuations

15

81 129 181 250 266 291 278 280 216 236 272 348 450 523 718

833 820 834 1,024

1,123 1,184 1,339

1,525 1,811

FY93-96: 45% CAGR

FY96-03: 1% CAGR

FY03-08: 25% CAGR

FY08-14: 8% CAGR

FY14-16E: 16% CAGR

FY93-FY13: 14% CAGR

24.28 24.60

8.30

24.65

16.03

6

12

18

24

30

Mar

/93

Mar

/94

Mar

/95

Mar

/96

Mar

/97

Mar

/98

Mar

/99

Mar

/00

Mar

/01

Mar

/02

Mar

/03

Mar

/04

Mar

/05

Mar

/06

Mar

/07

Mar

/08

Mar

/09

Mar

/10

Mar

/11

Mar

/12

Mar

/13

Mar

/14

Sensex P/E (x) Sensex CAGR 14%

Sensex CAGR -1%

Sensex CAGR 39% Sensex CAGR -1%

Average of 14.9x

Sensex CAGR 14%

Sensex CAGR -1%

Sensex CAGR 39% Sensex CAGR -1%

Average of 14.9x

Sensex EPS

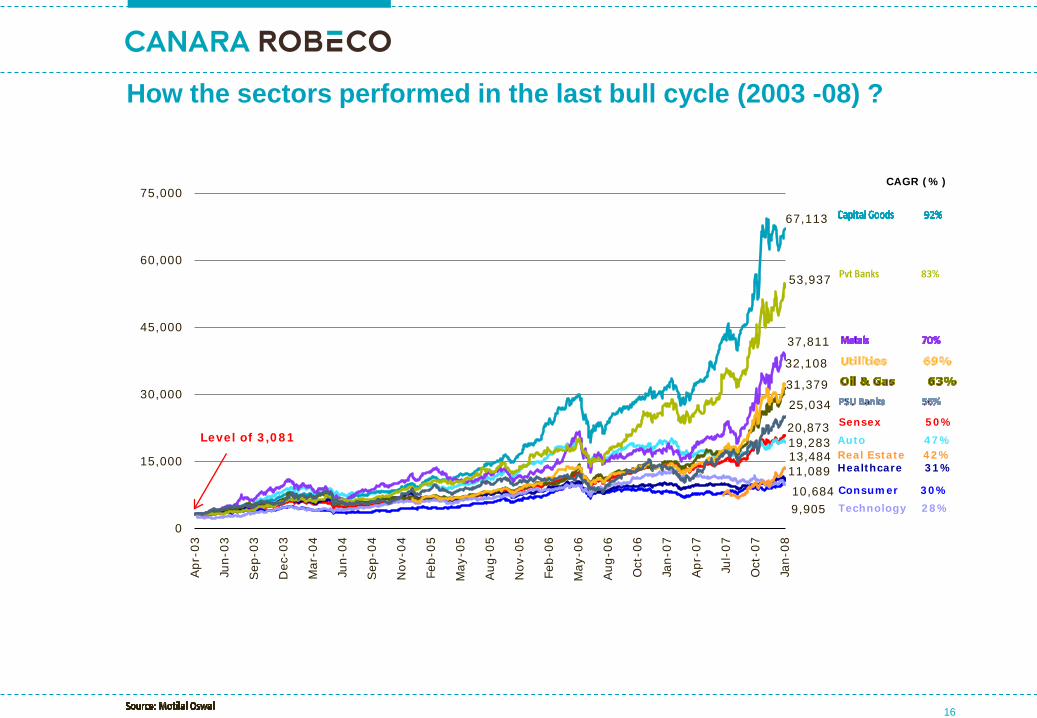

How the sectors performed in the last bull cycle (2003 -08) ?

16

20,873 19,283

10,684

67,113

11,089

37,811

31,379

9,905

32,108

13,484

53,937

25,034

0

15,000

30,000

45,000

60,000

75,000 Apr

-03

Jun-

03

Sep

-03

Dec

-03

Mar

-04

Jun-

04

Sep

-04

Nov

-04

Feb-

05

May

-05

Aug

-05

Nov

-05

Feb-

06

May

-06

Aug

-06

Oct

-06

Jan-

07

Apr

-07

Jul-

07

Oct

-07

Jan-

08

Consumer 30%

Auto 47%

Healthcare 31%

Technology 28%

Sensex 50%

Real Estate 42%

Pvt Banks 83%

CAGR (%)

Level of 3,081

What has changed since January to June ’14…?

17

11.6

13.3

6.2

-5.2

38.3

-1.7

63.2

1.4

4.5

-8.4

10.7

-20.0 0.0 20.0 40.0 60.0 80.0

Consumer Discretionary

Consumer Staples

Energy

Financials

Health Care

Industrials

Information Technology

Materials

Telecommunication Services

Utilities

Sensex

Total Return 2013

25.2

7.7

39.4

34.0

0.5

61.7

-7.8

42.9

7.9

26.7

21.9

-20.0 0.0 20.0 40.0 60.0 80.0

Total Return YTD (2014)

As on June 2014

Our Portfolio stance and preferred bets

• Given a strong mandate for the government focus would be more on domestic sectors i.e

(Industrials, Financials, Consumer discretionary, Energy) that will benefit from economic

growth

• With economy bottoming out and expectation of a stable government, we had already

started increasing our allocation towards high beta sectors such as Financials and

Industrials in Jan/Feb 14

• We prefer domestic companies with operating leverage, strong balance sheet and cash

levels

• We also prefer domestic sectors which are geared towards domestic consumption.

• We have turned cautious on domestic staples on account of slowing growth and very high

valuations

18

Current Portfolio stance

Sector Overweight / Underweight

Consumer Discretionary Overweight

Consumer Staples Underweight

Energy Neutral

Financials Overweight

Healthcare Underweight

Industrials Overweight

Information technology Underweight

Materials Underweight

Telecom Overweight

Utilities Underweight

19

Likely scenario near term

• With the favourable outcome of elections & positive cues in the Budget, markets have

rallied , going forward the corporate earnings announcements for the Q1FY15 will

impact market sentiment

• News flow from US Fed on Tapering plans is likely to drive global risk appetite and

liquidity

• Domestic Interest rates likely to remain stable with bias towards decline in later part of

the year

• Mid-caps likely to remain in lime-light given the low relative valuations

• Our portfolio focus is shifting towards:

– Increasing weights in high quality midcaps

– Adding companies which are trading at a steep discount to their intrinsic value,

turnaround opportunities, SOTP ideas

20

FII flows

21

9.5 9.2 10.9 5.8

13.1

-10.4

23.4 25.0

8.5

25.8

13.7 0.3 0.1

3.2 6.4

17.7

13.1

5.1

-4.1 -0.9 -12.7

-8.9

9.8 9.3 14.1 12.1 30.8 2.7 28.4 20.9 7.6 13.1 4.8

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

FII (USDb) DII (USDb) Total USDb

Total Flows: USD107b FII: USD61b DII: USD46b

Total Flows: USD46b FII: USD73b DII: USD-27b

Disclaimer

Mutual Fund Investments are subject to market risk, read all scheme related documents carefully.

The information used towards formulating the outlook have been obtained from sources published by third parties. While such publications are believed to be reliable, however, neither the AMC, its officers, the trustees, the Fund nor any of their affiliates or representatives assume any responsibility for the accuracy of such information and assume no financial liability whatsoever to the user of this document. This document is strictly confidential and meant for private circulation only and should not at any point of time be construed to be an invitation to the public for subscribing to the units of Canara Robeco Mutual Fund. Please note that this is not an advertisement. The document is solely for the information and understanding of intended recipients only. Internal views, estimates, opinions expressed herein may or may not materialize. These views, estimates, opinions alone are not sufficient and should not be used for the development or implementation of an investment strategy. Forward looking statements are based on internal views and assumptions and subject to known and unknown risks and uncertainties which could materially impact or differ the actual results or performance from those expressed or implied under those statements.

22

23

Corporate Office Canara Robeco Asset Management Company Ltd. 4th Floor, Construction House, 5, Walchand Hirachand Road, Ballard Estate, Mumbai - 400 001 http://www.canararobeco.com

Phone: +91 22 66585000 Fax: +91 22 66585012

THANK YOU