outlook: 2014 2023 - renapri

TRANSCRIPT

1st Annual Regional Agricultural Outlook: 2014 – 2023

Anticipating and responding to policy challenges in the decade ahead

Presentation at 1st Annual ReNAPRI Outlook Symposium Lusaka, Zambia

November 4th, 2014

Outline

1. ReNAPRI: localizing agricultural policy research

– The Network

– The Modelling Framework

2. Sector Level Analysis: 2014 – 2023 regional maize outlook

– Global outlook

– Regional outlook

3. Farm Level Analysis: benchmarking maize cost of production

4. Strategic Foresighting: border closing scenario

ReNAPRI: Localizing Agricultural Policy Research

• The Goal:

– Provide policy-makers with relevant and accurate information

• The Challenge:

– Regional agricultural policy research and outreach is largely driven by

non-African institutions

– In terms of implementation, this external analysis has yielded very little

fruit to date.

ReNAPRI: Localizing Agricultural Policy Research

• Regional Network of Agricultural Policy Research Institutes (ReNAPRI)

– Offers a unique solution:

• African-led, African-driven initiative with a ground-up approach to policy research

– Membership includes existing policy research institutes with a proven track-record of policy advisement within their respective countries.

• Institute for Social and Economic Research, University of Kinshasa - Democratic Republic of Congo

• Tegemeo Institute of Agricultural Policy and Development, Egerton University – Kenya

• Centre for Agricultural Research and Development, Lilongwe University of Agriculture & Natural Resources – Malawi

• CEPPAG, University of Eduardo Mondlane – Mozambique

• Bureau for Food and Agricultural Policy (BFAP). University of Pretoria & Stellenbosch - South Africa

• Department of Agriculture Economics and Agribusiness, Sokoine University of Agriculture - United Republic of Tanzania

• Indaba Agriculture Policy Research Institute (IAPRI) - Zambia

ReNAPRI: Localizing Agricultural Policy Research

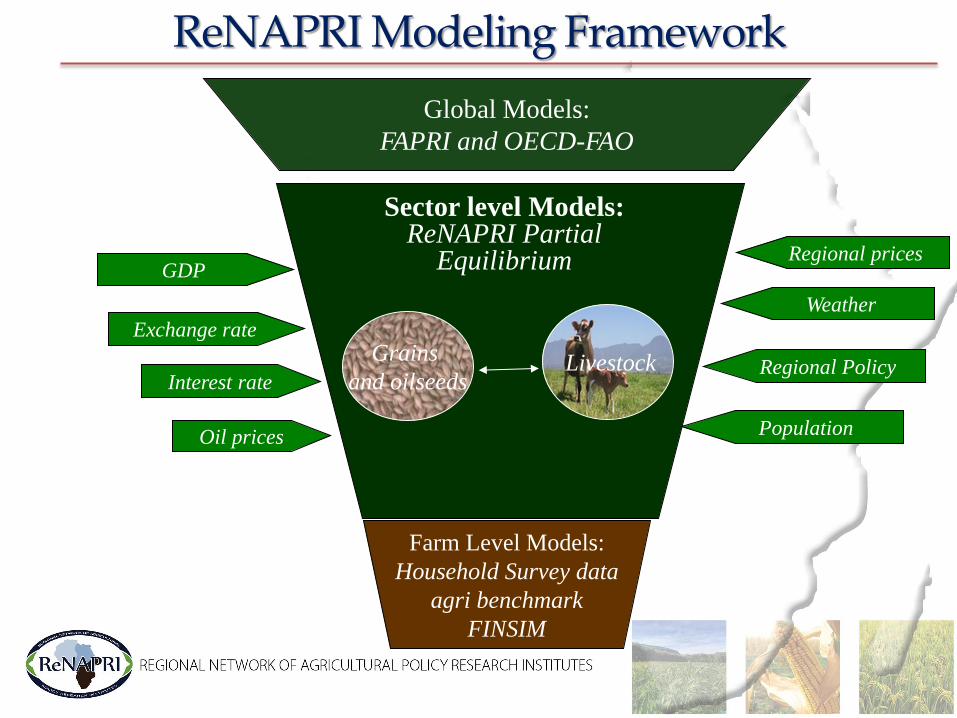

Global Models:

FAPRI and OECD-FAO

GDP

Exchange rate

Interest rate

Regional prices

Weather

Population

Regional Policy

Farm Level Models:

Household Survey data

agri benchmark

FINSIM

Sector level Models: ReNAPRI Partial

Equilibrium

Livestock Grains

and oilseeds

Oil prices

ReNAPRI Modeling Framework

Maize Markets: global drivers

Patrick Westhoff ([email protected]) FAPRI-MU director

University of Missouri www.fapri.missouri.edu

Agenda

• Why have world maize prices declined from recent record levels?

• What are the main drivers of future market prices?

• What can we expect?

• How uncertain are projections? Why?

U.S. maize export prices What went up has come back down

0

50

100

150

200

250

300

350

Jan 2010 Jan 2011 Jan 2012 Jan 2013 Jan 2014

Do

llars

per

to

nn

e

FOB Gulf

Source: USDA Economic Research Service. Last data point is September 2014.

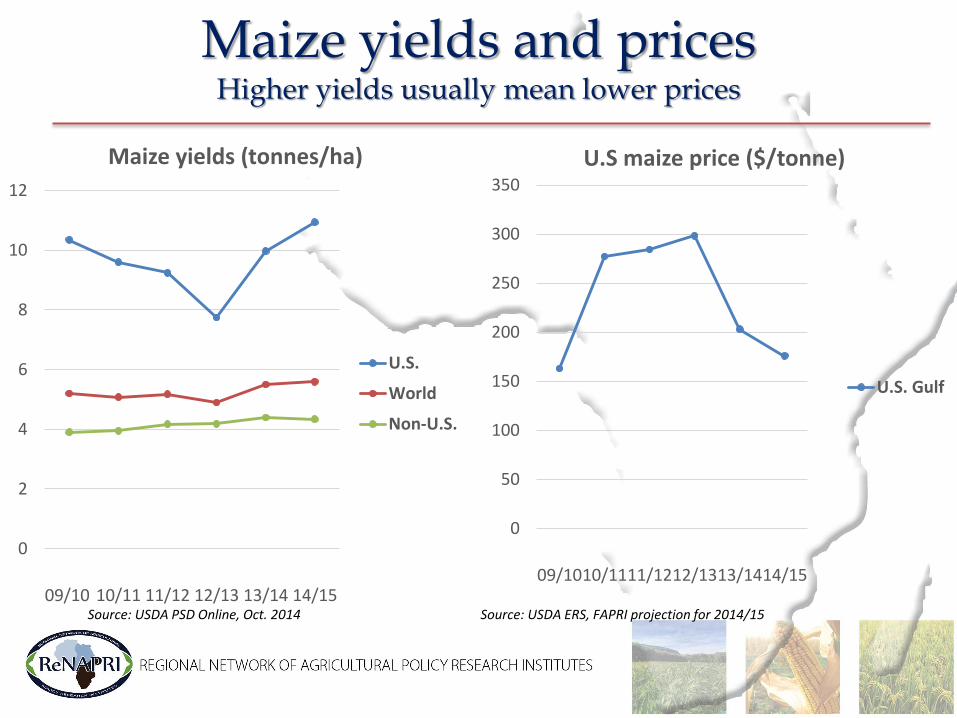

Maize yields and prices Higher yields usually mean lower prices

0

2

4

6

8

10

12

09/10 10/11 11/12 12/13 13/14 14/15

Maize yields (tonnes/ha)

U.S.

World

Non-U.S.

0

50

100

150

200

250

300

350

09/1010/1111/1212/1313/1414/15

U.S maize price ($/tonne)

U.S. Gulf

Source: USDA PSD Online, Oct. 2014 Source: USDA ERS, FAPRI projection for 2014/15

Maize Utilization

0

50

100

150

200

250

300

350

Mill

ion

to

nn

es

U.S. domestic maize use

Feed All other (inc. ethanol)

0

50

100

150

200

250

300

350

Mill

ion

to

nn

es

China domestic maize use

Feed All other (inc. ethanol)

Source: USDA PSD Online, Oct. 2014

World Maize Production, Use and Carryover Stocks

0

200

400

600

800

1000

1200

05/06 07/08 09/10 11/12 13/14 15/16 17/18 19/20 21/22 23/24

Mill

ion

to

nn

es

Production

Use

Stocks

Source: Unpublished FAPRI-MU baseline update, October 2014

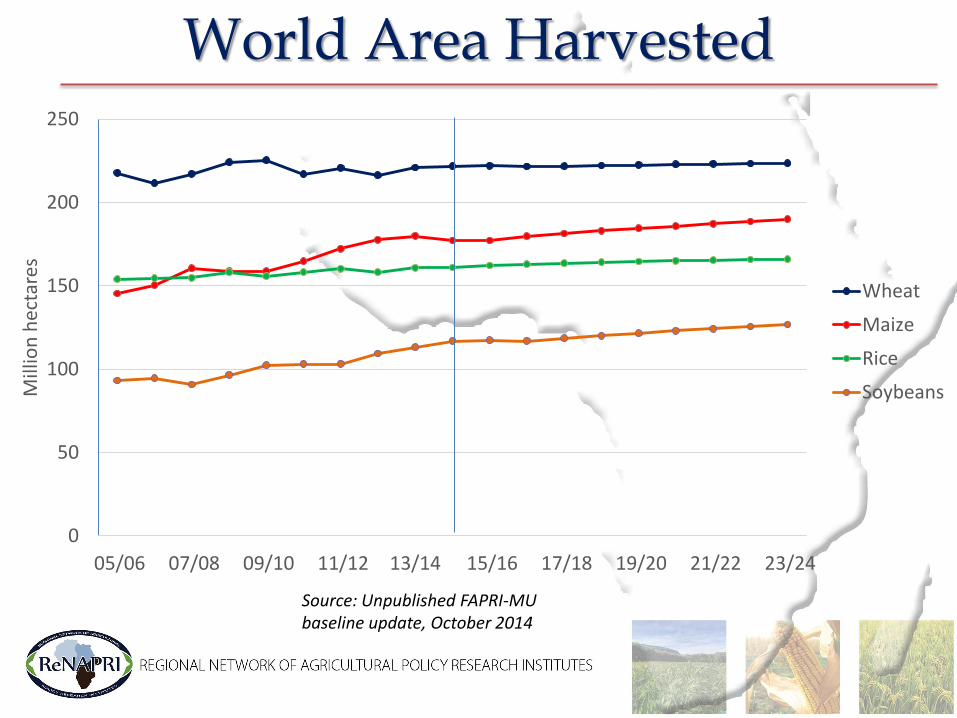

World Area Harvested

0

50

100

150

200

250

05/06 07/08 09/10 11/12 13/14 15/16 17/18 19/20 21/22 23/24

Mill

ion

hec

tare

s

Wheat

Maize

Rice

Soybeans

Source: Unpublished FAPRI-MU baseline update, October 2014

World Area Harvested

0

100

200

300

400

500

600

700

800

05/06 07/08 09/10 11/12 13/14 15/16 17/18 19/20 21/22 23/24

Mill

ion

hec

tare

s

Soybeans

Rice

Maize

Wheat

Source: Unpublished FAPRI-MU baseline update, October 2014

World crop yields

0

1

2

3

4

5

6

7

05/06 07/08 09/10 11/12 13/14 15/16 17/18 19/20 21/22 23/24

Ton

nes

per

hec

tare

Maize

Wheat

Milled rice

Soybeans

Source: Unpublished FAPRI-MU baseline update, October 2014

World Crop Use (total)

0

200

400

600

800

1000

1200

05/06 07/08 09/10 11/12 13/14 15/16 17/18 19/20 21/22 23/24

Mill

ion

to

nn

es

Maize

Wheat

Milled rice

Soybeans

Source: Unpublished FAPRI-MU baseline update, October 2014

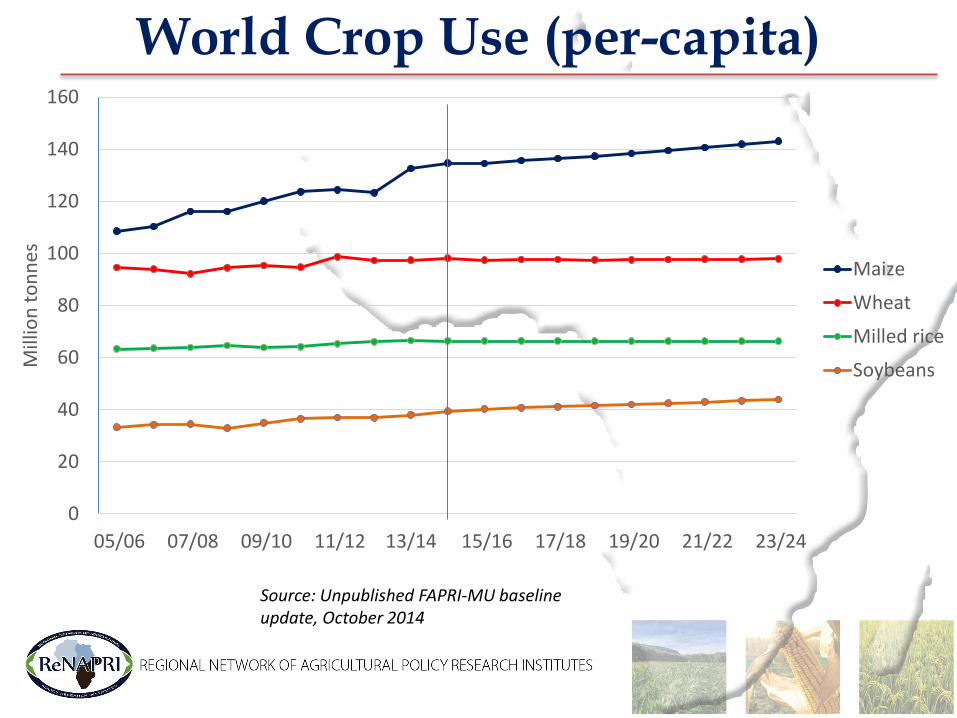

World Crop Use (per-capita)

0

20

40

60

80

100

120

140

160

05/06 07/08 09/10 11/12 13/14 15/16 17/18 19/20 21/22 23/24

Mill

ion

to

nn

es

Maize

Wheat

Milled rice

Soybeans

Source: Unpublished FAPRI-MU baseline update, October 2014

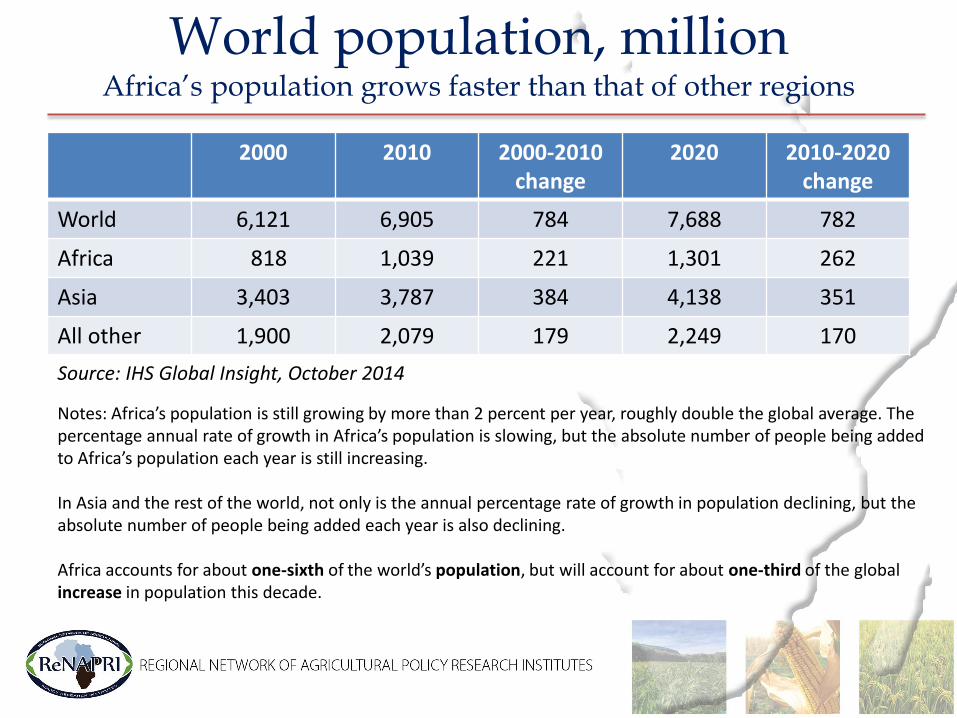

World population, million Africa’s population grows faster than that of other regions

2000 2010 2000-2010 change

2020 2010-2020 change

World 6,121 6,905 784 7,688 782

Africa 818 1,039 221 1,301 262

Asia 3,403 3,787 384 4,138 351

All other 1,900 2,079 179 2,249 170

Source: IHS Global Insight, October 2014

Notes: Africa’s population is still growing by more than 2 percent per year, roughly double the global average. The percentage annual rate of growth in Africa’s population is slowing, but the absolute number of people being added to Africa’s population each year is still increasing. In Asia and the rest of the world, not only is the annual percentage rate of growth in population declining, but the absolute number of people being added each year is also declining. Africa accounts for about one-sixth of the world’s population, but will account for about one-third of the global increase in population this decade.

U.S. Export Prices for Wheat and Maize

0

50

100

150

200

250

300

350

05/06 07/08 09/10 11/12 13/14 15/16 17/18 19/20 21/22 23/24

Do

llars

per

to

nn

e

Wheat

Maize

Source: Unpublished FAPRI-MU baseline update, October 2014

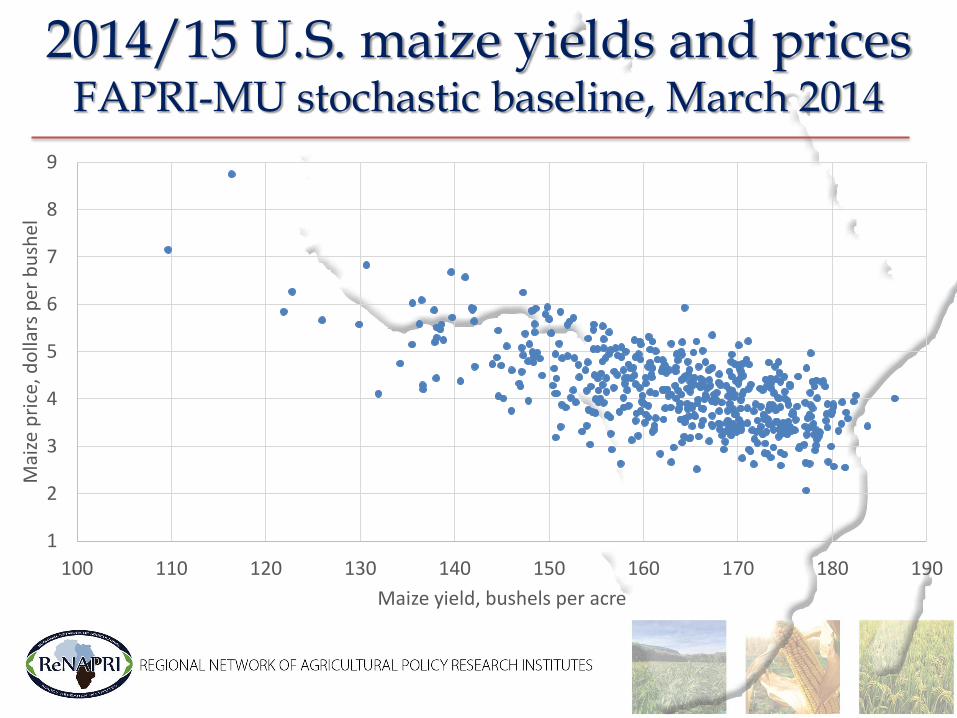

2014/15 U.S. maize yields and prices FAPRI-MU stochastic baseline, March 2014

1

2

3

4

5

6

7

8

9

100 110 120 130 140 150 160 170 180 190

Mai

ze p

rice

, do

llars

per

bu

shel

Maize yield, bushels per acre

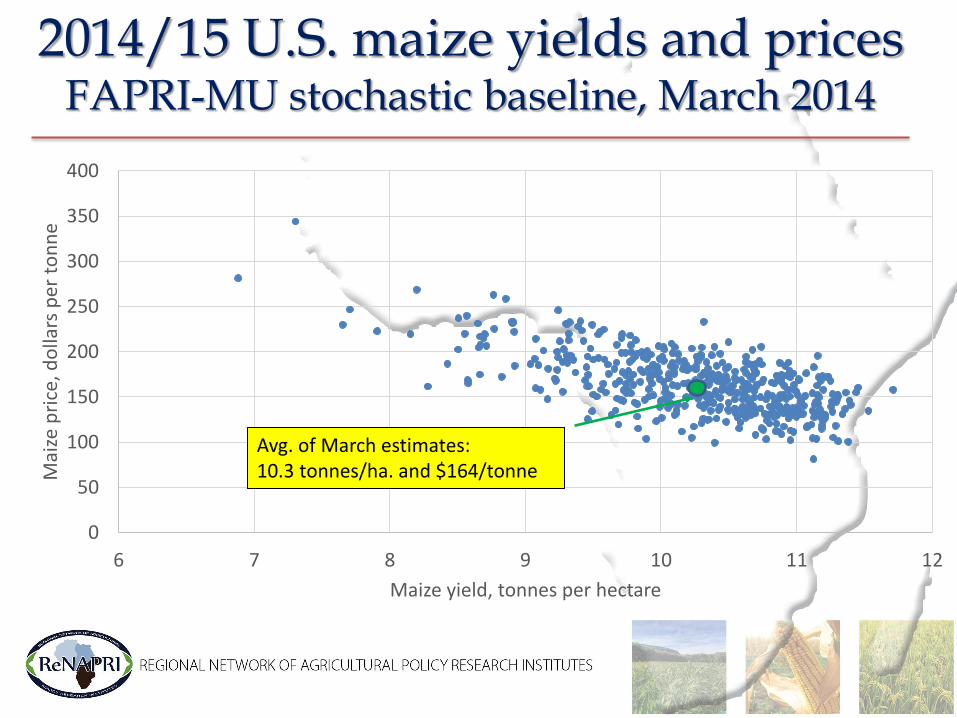

2014/15 U.S. maize yields and prices FAPRI-MU stochastic baseline, March 2014

0

50

100

150

200

250

300

350

400

6 7 8 9 10 11 12

Mai

ze p

rice

, do

llars

per

to

nn

e

Maize yield, tonnes per hectare

Avg. of March estimates: 10.3 tonnes/ha. and $164/tonne

2014/15 U.S. maize yields and prices FAPRI-MU stochastic baseline, March 2014

0

50

100

150

200

250

300

350

400

6 7 8 9 10 11 12

Mai

ze p

rice

, do

llars

per

to

nn

e

Maize yield, tonnes per hectare

October USDA estimates: 10.9 tonnes/ha. and $134/tonne

Avg. of March estimates: 10.3 tonnes/ha. and $164/tonne

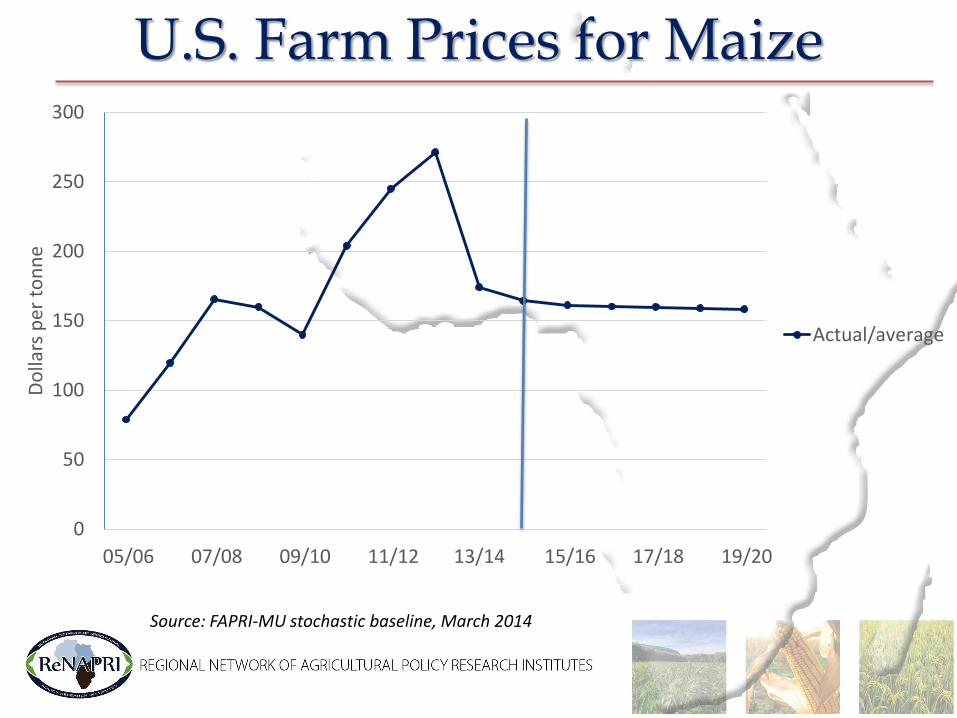

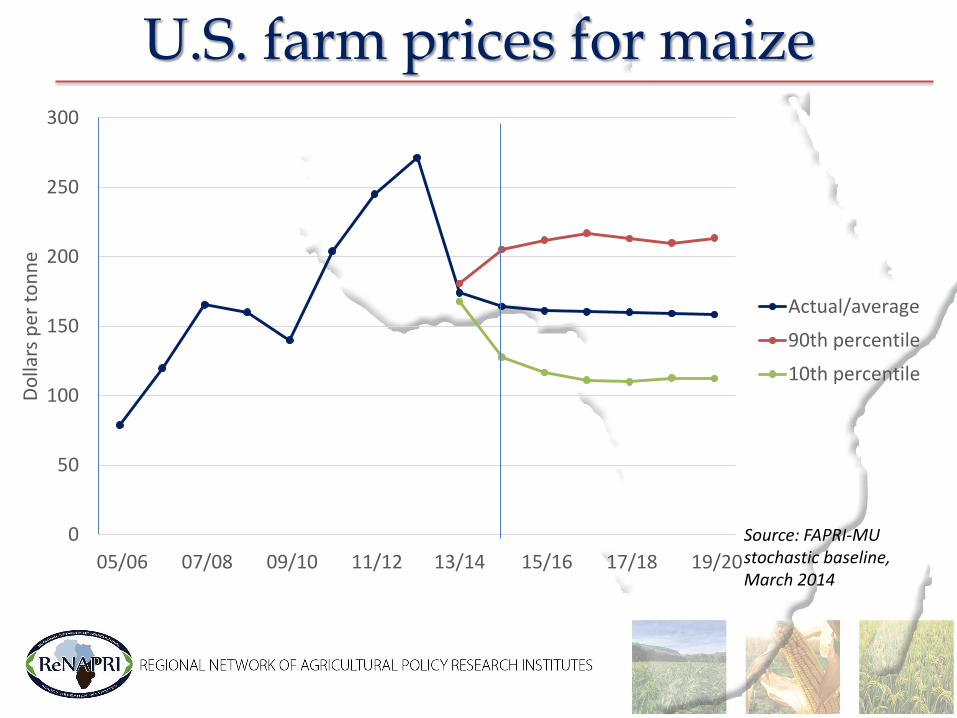

U.S. Farm Prices for Maize

Source: FAPRI-MU stochastic baseline, March 2014

0

50

100

150

200

250

300

05/06 07/08 09/10 11/12 13/14 15/16 17/18 19/20

Do

llars

per

to

nn

e

Actual/average

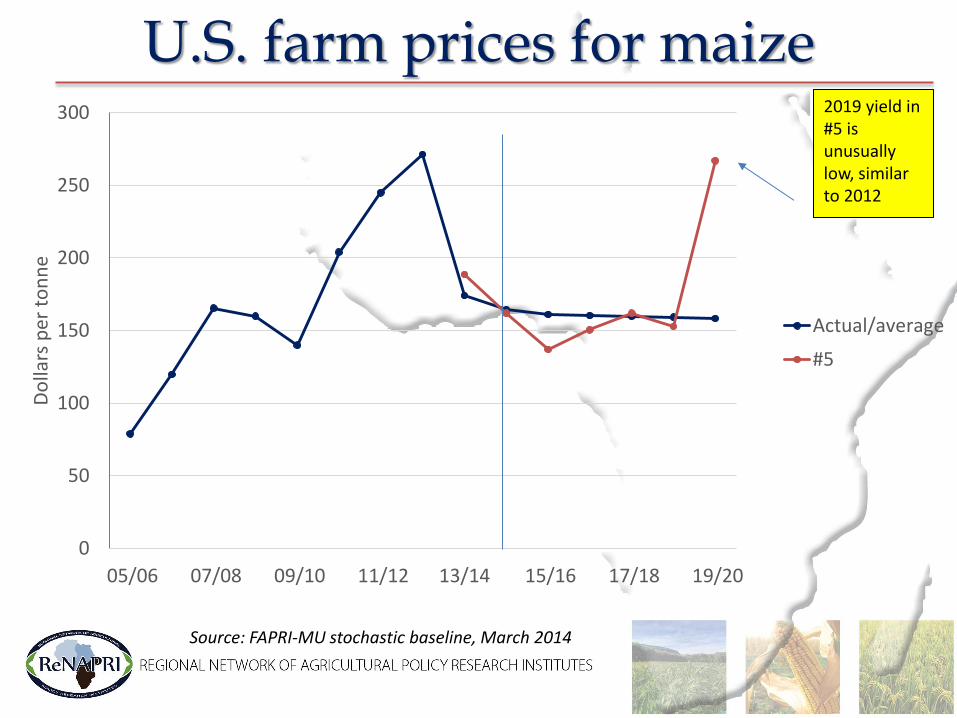

U.S. farm prices for maize

0

50

100

150

200

250

300

05/06 07/08 09/10 11/12 13/14 15/16 17/18 19/20

Do

llars

per

to

nn

e

Actual/average

#5

Source: FAPRI-MU stochastic baseline, March 2014

2019 yield in #5 is unusually low, similar to 2012

U.S. Farm Prices for Maize

Source: FAPRI-MU stochastic baseline, March 2014

0

50

100

150

200

250

300

05/06 07/08 09/10 11/12 13/14 15/16 17/18 19/20

Do

llars

per

to

nn

e

Actual/average

#5

#250

#495

U.S. farm prices for maize

0

50

100

150

200

250

300

05/06 07/08 09/10 11/12 13/14 15/16 17/18 19/20

Do

llars

per

to

nn

e

Actual/average

90th percentile

10th percentile

Source: FAPRI-MU stochastic baseline, March 2014

Final comments • Recent swings in global maize prices are largely due to U.S. weather,

which lowered yields in 2012 and raised them in 2014

• U.S. ethanol and China have been major sources of demand growth—China may continue to grow, but U.S. ethanol may not

• Longer-term price trends depend on relative rates of growth in technology (yields), population, and per-capita demand

• We expect maize prices to average above recent lows, but below 2012-13 peaks

• But in any given year, weather and other unpredictable factors will cause price volatility

Thanks!

• FAPRI-MU website: www.fapri.missouri.edu

• To contact Pat Westhoff:

– 1-573-882-4647

• FAPRI-MU team:

– Julian Binfield

– Sera Chiuchiarelli

– Deepayan Debnath

– Scott Gerlt

– Lauren Jackson

– Willi Meyers

– Wyatt Thompson

– Jarrett Whistance

– Peter Zimmel

Eastern and Southern Africa Maize Outlook: 2014 – 2023

Regional Outlook: Prices transmission

Source: ReNAPRI Outlook, November 2014

0

50

100

150

200

250

300

350

400

450

2000 2002 2004 2006 2008 2010 2012

US

$ /

to

n

World Price South Africa - Randfontein Kenya - Nairobi

Zambia - Lusaka Tanzania - Arusha Malawi - Lilongwe

Mozambique - Maputo DRC - Kinshasa

Regional Outlook: Prices transmission

Source: ReNAPRI Outlook, November 2014

0

50

100

150

200

250

300

350

2000 2002 2004 2006 2008 2010 2012

US

$ /

to

n

World Price South Africa - Randfontein

Regional Outlook: Maize Price Transmission

• Country specific price-setting mechanisms: South Africa

Consumption

Retailing

Processing

Trading

Storage

Production

May 2012 to April 2013

SubsistenceFarmers

Volume = 564,335

Commercial FarmersVolume = 10,360,000 tons

ImportsVolume =

341,000 tons

Informal (Gristing) Millers

Volume = 62,000 t

Animal FeedVolume = ?

Domesticstorage and tradingDelivery volume = 9,913,000 t

Formal millers: Human consumptionVolume = 4,147,000 t

Animal Feed

Independent Trader

Household Consumption

Formal & Informal Retailing

Livestock Industry

Exports:Maize product

128,000 t

Exports:Maize grain1,812,000 t

SAFEX

Source: SAGIS, 2013

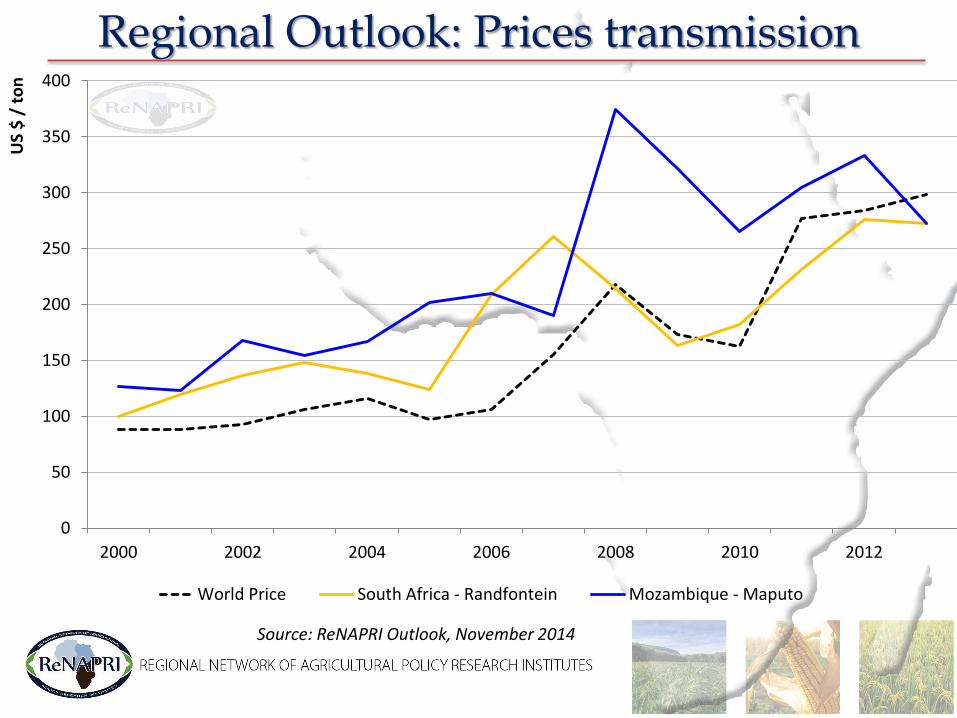

Regional Outlook: Prices transmission

Source: ReNAPRI Outlook, November 2014

0

50

100

150

200

250

300

350

400

2000 2002 2004 2006 2008 2010 2012

US

$ /

to

n

World Price South Africa - Randfontein Mozambique - Maputo

Regional Outlook: Prices transmission

Source: ReNAPRI Outlook, November 2014

0

50

100

150

200

250

300

350

2000 2002 2004 2006 2008 2010 2012

US

$ /

to

n

World Price Zambia - Lusaka

Regional Outlook: Maize Price Transmission

KEY

flow of maize gain

flow ofmealie meal or beer for human consumption

flow of maize product for animal feed

Maize figures from 2012/13 season

TRADE FLOW MAP OF GRAIN AND GRAN PRODUCTS IN ZAMBIA

small scale millers

Volume=200,000 tons

Vertically integrated

(production, storage,

processing, retailing and exporting)

Small holder Farmers

Volume = 2,532,800 tons

CommercialFarmers=Volume

=66,576

ImportsVolume=0

Farm retention for home

consumption=50,000tons

Animal FeedVolume

Private Grain Traders

Household Consumption

Formal & Informal Retaiers

Livestock IndustryMaize Grain Exports Mealie meal exports

FRA(national

reserved food)

Volume=500,000 tons

Large scale millersVolume

BreweriesVolume

Production

Storage

Trading

Processing

Retailing

Consumption

Small scale grain traders and assemblers

Regional Outlook: Prices transmission

Source: ReNAPRI Outlook, November 2014

0

50

100

150

200

250

300

350

400

2000 2002 2004 2006 2008 2010 2012

US

$ /

to

n

Zambia - Lusaka Malawi - Lilongwe

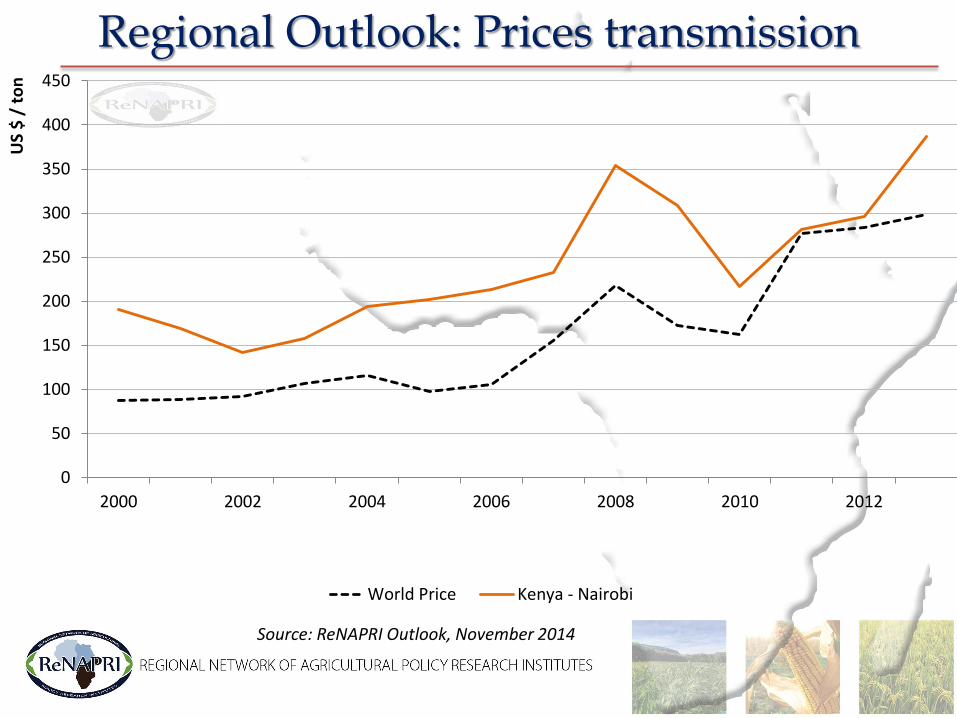

Regional Outlook: Prices transmission

Source: ReNAPRI Outlook, November 2014

0

50

100

150

200

250

300

350

400

450

2000 2002 2004 2006 2008 2010 2012

US

$ /

to

n

World Price Kenya - Nairobi

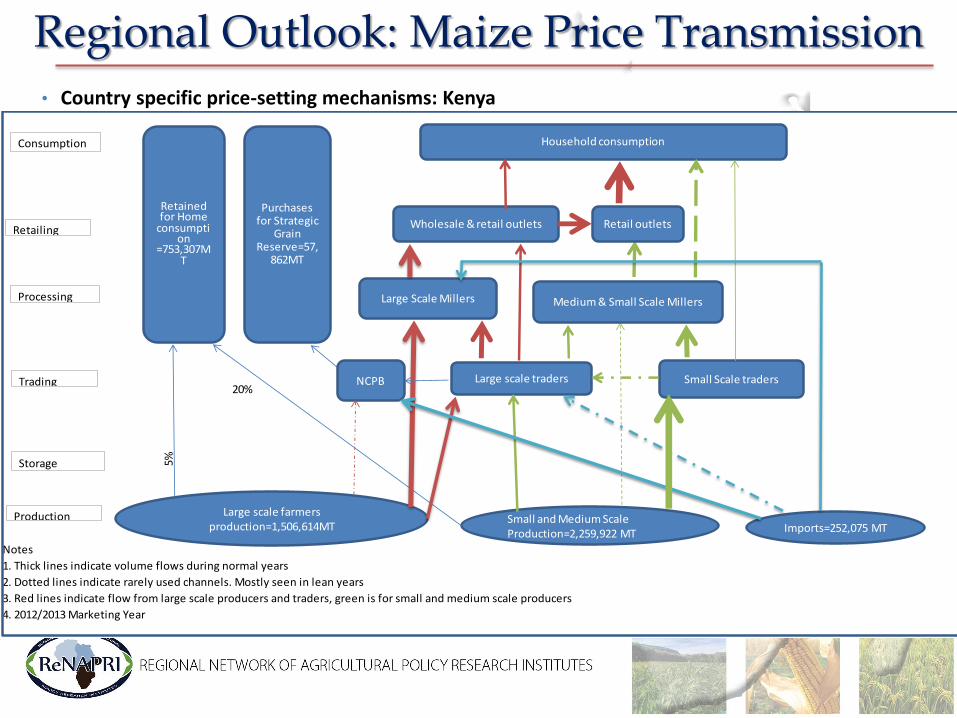

Regional Outlook: Maize Price Transmission

• Country specific price-setting mechanisms: Kenya

Notes

1. Thick lines indicate volume flows during normal years

2. Dotted lines indicate rarely used channels. Mostly seen in lean years

3. Red lines indicate flow from large scale producers and traders, green is for small and medium scale producers

4. 2012/2013 Marketing Year

Small and Medium Scale Production=2,259,922 MT

Large scale farmers production=1,506,614MT Imports=252,075 MT

Retained for Home

consumption

=753,307MT

Purchases for Strategic

Grain Reserve=57,

862MT

Large scale traders Small Scale tradersNCPB

Large Scale Millers

5%

20%

Household consumption

Medium & Small Scale Millers

Wholesale & retail outlets Retail outlets

Consumption

Retailing

Processing

Trading

Storage

Production

Regional Outlook: Prices transmission

Source: ReNAPRI Outlook, November 2014

0

50

100

150

200

250

300

350

400

450

2000 2002 2004 2006 2008 2010 2012

US

$ /

to

n

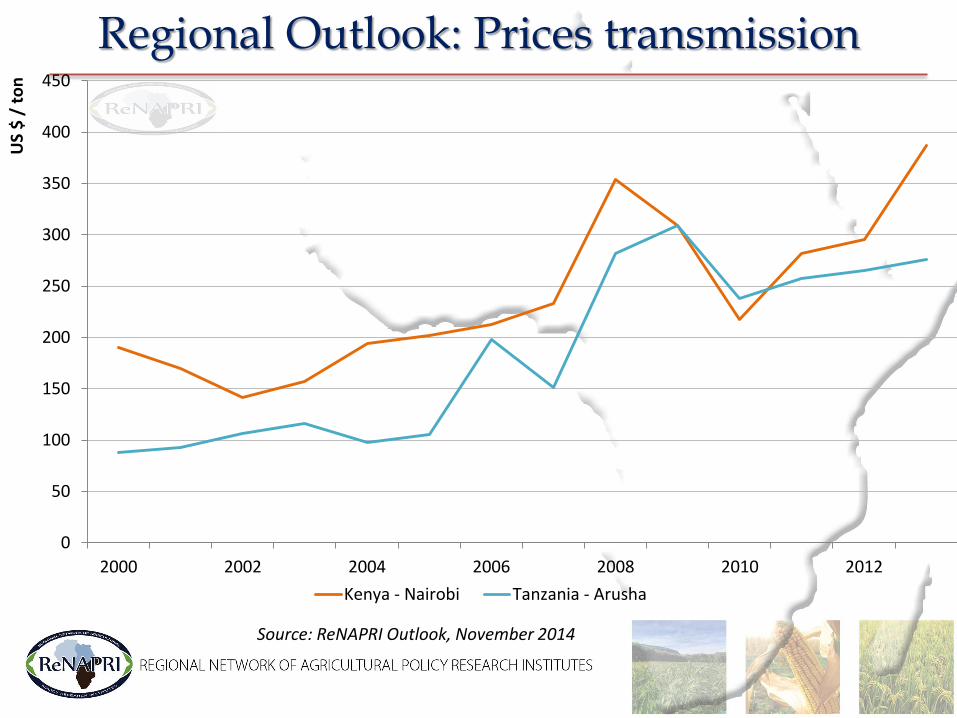

Kenya - Nairobi Tanzania - Arusha

Regional Outlook: Maize Price Transmission

• Country specific price-setting mechanisms: Tanzania Maize Value Chain

Consumption

Retailing

Processing

Trading

Storage

Production

KEY

flow of maize gain

flow of maize product for human consumption

flow of maize product for animal feed

Maize figures from 2011/12 season

Subsistence FarmersVolume = 5,104,248 tons

CommercialFarmers

Volume =

ImportsVolume =

Farm retention for home

consumption

Volume = 231,000 t

Small scale millers and tradingDelivery volume = 2,121,017 t

Animal FeedVolume =

Private Tradervolume: 860,639 t

Household Consumption

Formal & Informal Retailing

Livestock Industry

Exports:Maize produt

Volume =

Exports:Maize grainVolume =

NFRA(national reserved

food)

Volume = 200,000 t

Vertically integrated

(production, storage,

processing, retailing and exporting)

volume= t

Large scale millersVolume =

Regional Outlook: Prices transmission

Source: ReNAPRI Outlook, November 2014

0

50

100

150

200

250

300

350

400

450

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

US

$ /

to

n

World Price South Africa - Randfontein Kenya - Nairobi

Zambia - Lusaka Tanzania - Arusha Malawi - Lilongwe

Mozambique - Maputo DRC - Kinshasa

Regional Outlook: Production, Consumption & Trade

-5,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Tho

usa

nd

to

ns

Consumption - Feed Consumption - Food Production Net trade

Source: ReNAPRI Outlook, November 2014

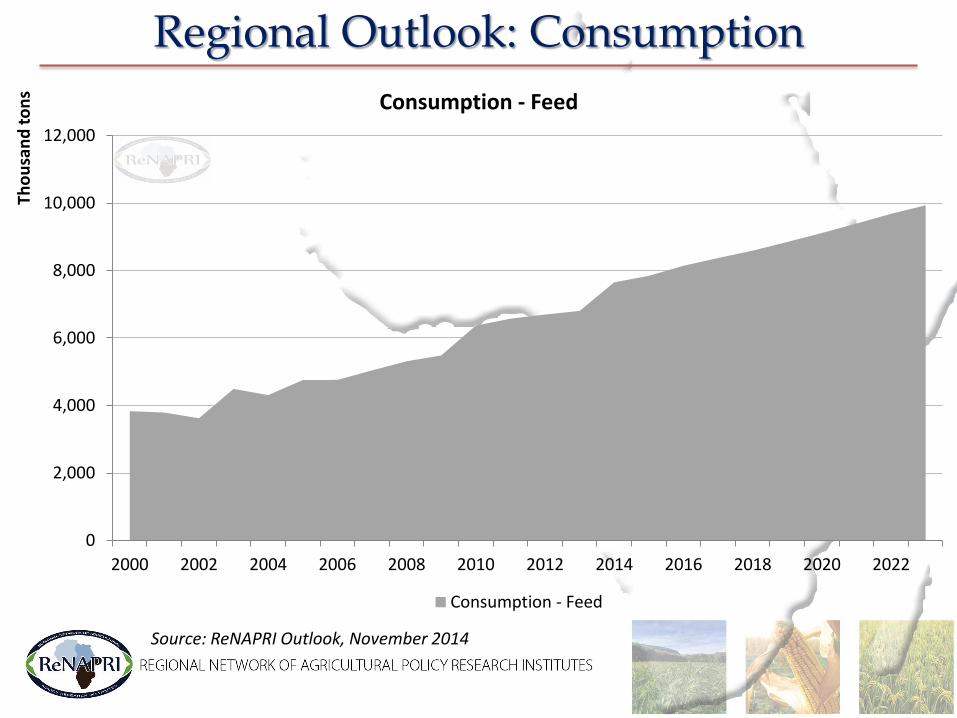

Regional Outlook: Consumption

0

2,000

4,000

6,000

8,000

10,000

12,000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Tho

usa

nd

to

ns Consumption - Feed

Consumption - Feed

Source: ReNAPRI Outlook, November 2014

• Rising per capita GDP and changing consumer diets underpinning increase demand by feed sector

Regional Outlook: Consumption

Source: ReNAPRI Outlook, November 2014

0

5000

10000

15000

20000

25000

30000

35000

0

500

1000

1500

2000

25002

00

0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

Zambia (ZMW) Mozambique (MZN) Tanzania (TZS) Kenya (KES)

Rea

l GD

P p

er C

apit

a (c

on

stan

t lo

cal c

urr

ency

)

SA R

eal G

DP

per

cap

ita

(co

nst

ant

ZAR

)

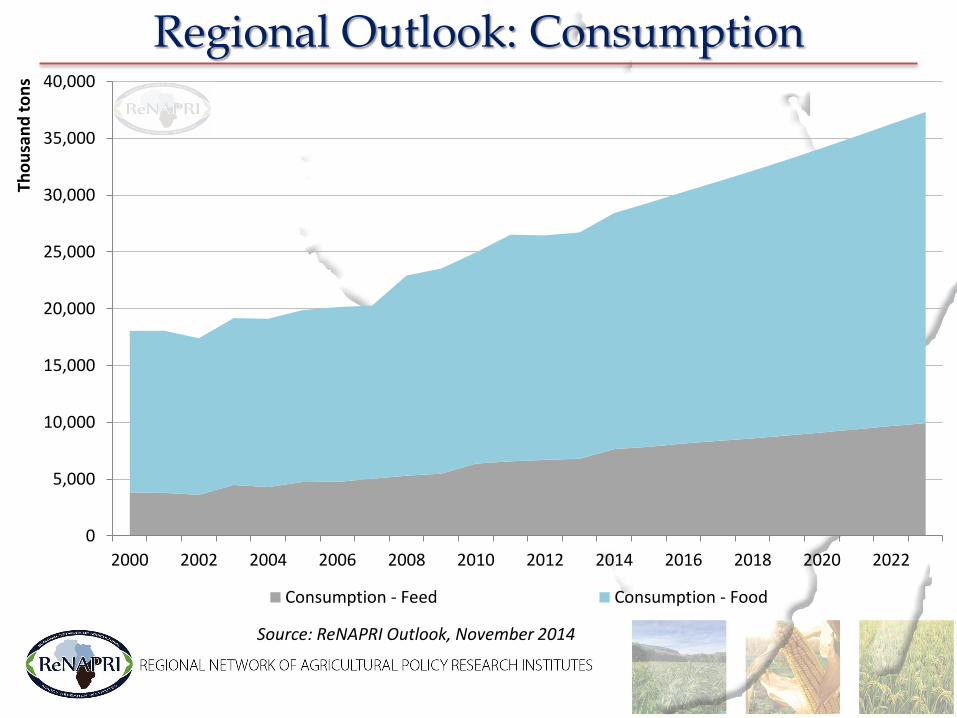

Regional Outlook: Consumption

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Tho

usa

nd

to

ns

Consumption - Feed Consumption - Food

Source: ReNAPRI Outlook, November 2014

• Population growth driving demand for human consumption

Regional Outlook: Consumption

0

10

20

30

40

50

60

70

80

90

100

South Africa Zambia Mozambique Tanzania Kenya Malawi DRC

Mill

ion

s

Source: ReNAPRI Outlook, November 2014

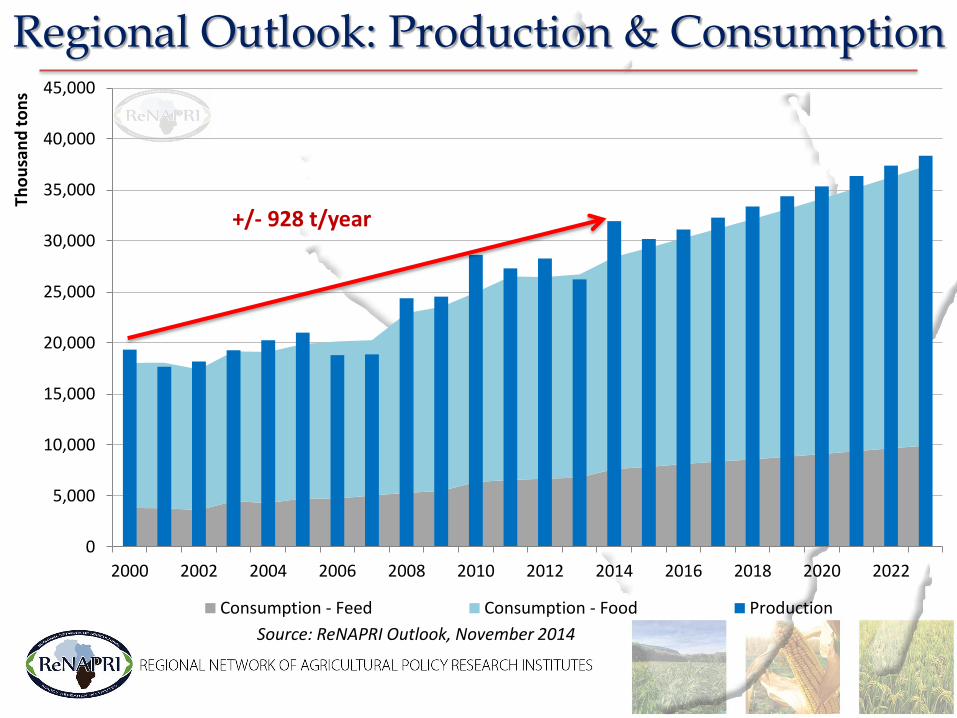

Regional Outlook: Production & Consumption

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Tho

usa

nd

to

ns

Consumption - Feed Consumption - Food Production

+/- 928 t/year

Source: ReNAPRI Outlook, November 2014

• Key Factors underlying production: Maize area harvested

Regional Outlook: Production

Source: ReNAPRI Outlook, November 2014

0

500

1000

1500

2000

2500

3000

3500

2003 2005 2007 2009 2011 2013

Tho

usa

nd

ha

South Africa Zambia Kenya Tanzania Malawi Mozambique DRC

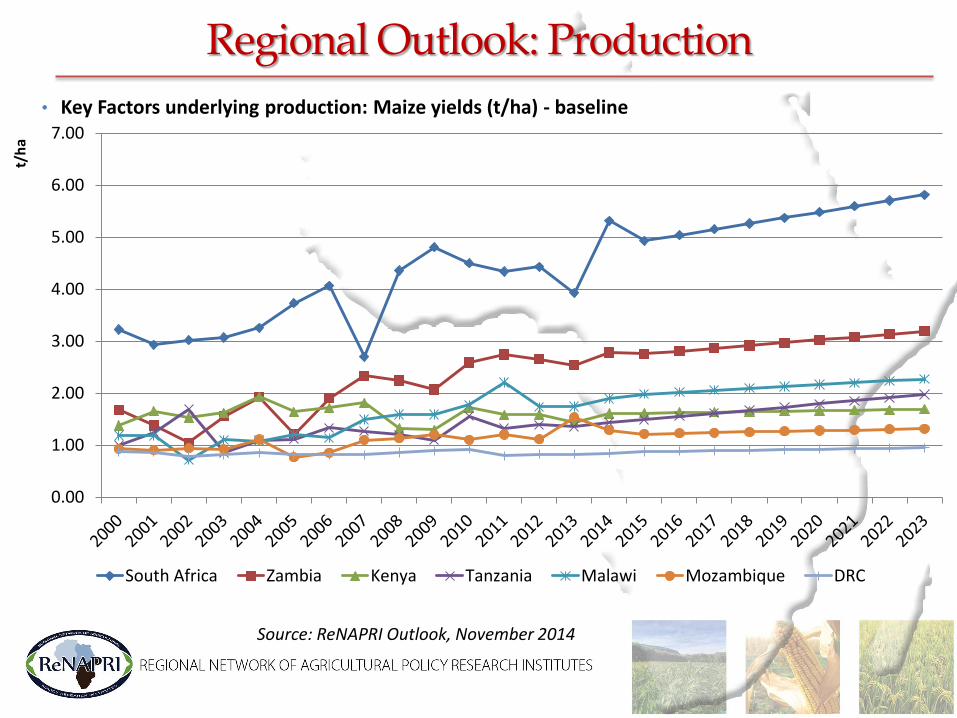

• Key Factors underlying production: Maize yields (t/ha)

Regional Outlook: Production

0.00

1.00

2.00

3.00

4.00

5.00

6.00

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014South Africa Zambia Kenya Tanzania Malawi Mozambique DRC

t/h

a

Source: ReNAPRI Outlook, November 2014

Regional Outlook: Production & Consumption

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Tho

usa

nd

to

ns

Consumption - Feed Consumption - Food Production

+/- 928 t/year

+/- 876 t/year

Source: ReNAPRI Outlook, November 2014

• Key Factors underlying production: Maize area harvested - baseline

Regional Outlook: Production

Source: ReNAPRI Outlook, November 2014

0

500

1000

1500

2000

2500

3000

3500

4000

2003 2005 2007 2009 2011 2013 2015 2017 2019 2021 2023

Tho

usa

nd

ha

South Africa Zambia Kenya Tanzania Malawi Mozambique DRC

• Key Factors underlying production: Maize yields (t/ha) - baseline

Regional Outlook: Production

Source: ReNAPRI Outlook, November 2014

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

South Africa Zambia Kenya Tanzania Malawi Mozambique DRC

t/h

a

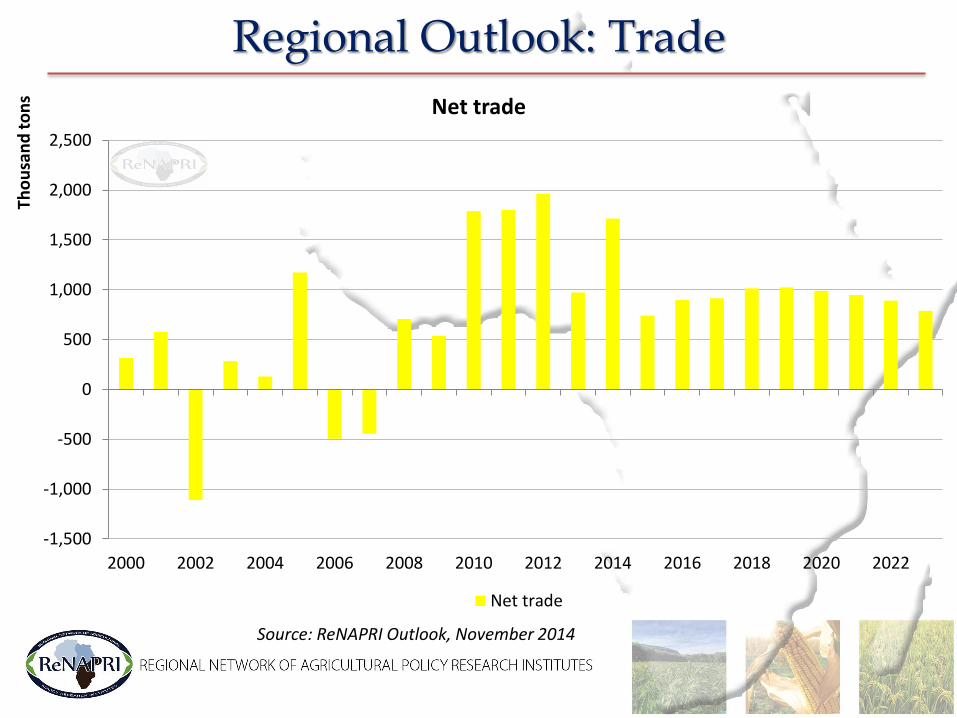

Regional Outlook: Trade

-1,500

-1,000

-500

0

500

1,000

1,500

2,000

2,500

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Tho

usa

nd

to

ns Net trade

Net trade

Source: ReNAPRI Outlook, November 2014

• Deficit Producer: DRC

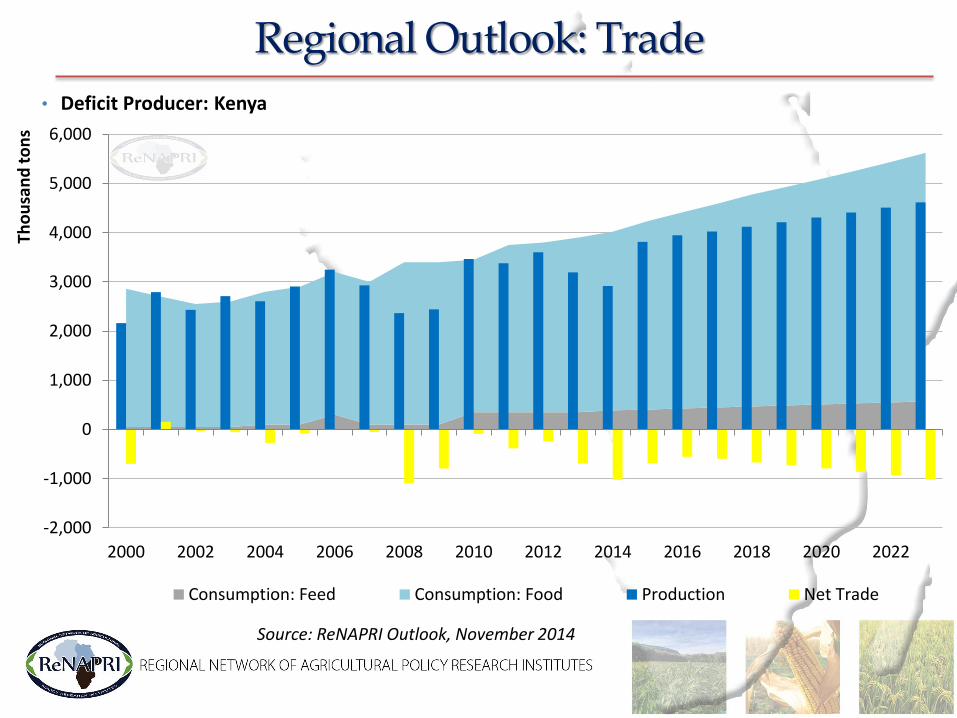

Regional Outlook: Trade

-1,000

-500

0

500

1,000

1,500

2,000

2,500

3,000

2008 2010 2012 2014 2016 2018 2020 2022

Tho

usa

nd

to

ns

Consumption: Feed Consumption: Food Production Net Trade

Source: ReNAPRI Outlook, November 2014

• Deficit Producer: Kenya

Regional Outlook: Trade

-2,000

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Tho

usa

nd

to

ns

Consumption: Feed Consumption: Food Production Net Trade

Source: ReNAPRI Outlook, November 2014

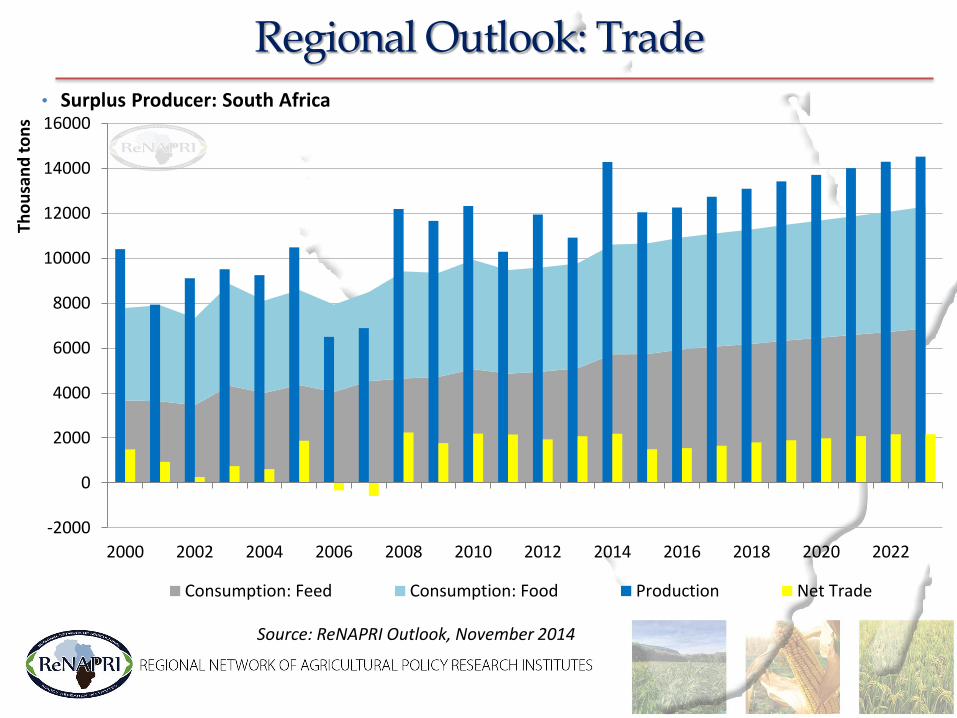

• Surplus Producer: South Africa

Regional Outlook: Trade

-2000

0

2000

4000

6000

8000

10000

12000

14000

16000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Tho

usa

nd

to

ns

Consumption: Feed Consumption: Food Production Net Trade

Source: ReNAPRI Outlook, November 2014

• Surplus Producer: Zambia

Regional Outlook: Trade

-1,000

0

1,000

2,000

3,000

4,000

5,000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Tho

usa

nd

to

ns

Consumption: Feed Consumption: Food Production Net Trade

Source: ReNAPRI Outlook, November 2014

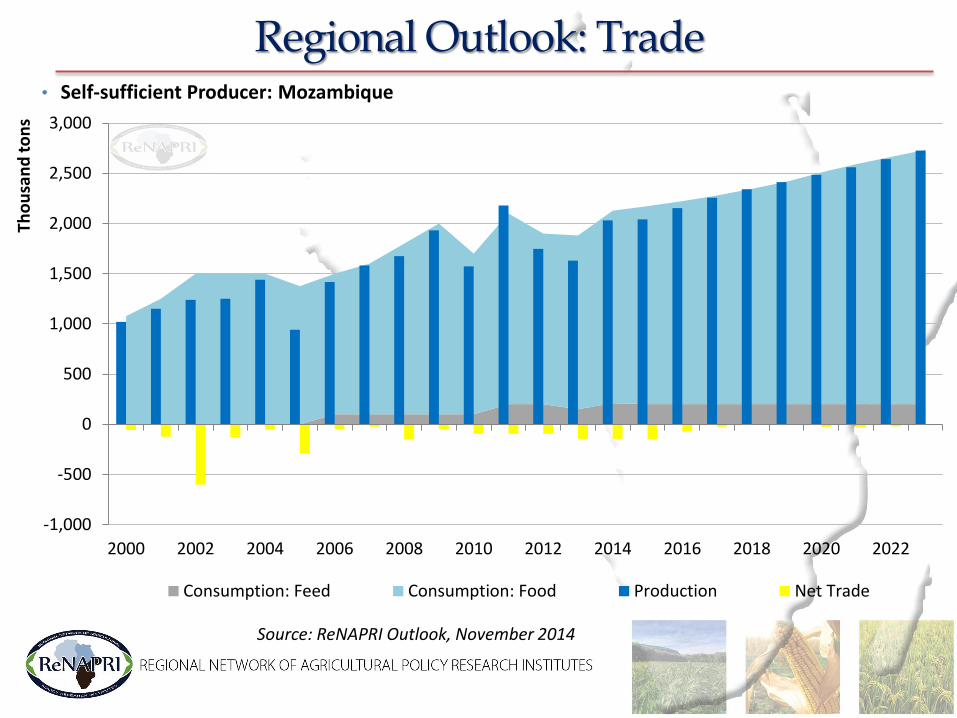

• Self-sufficient Producer: Mozambique

Regional Outlook: Trade

-1,000

-500

0

500

1,000

1,500

2,000

2,500

3,000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Tho

usa

nd

to

ns

Consumption: Feed Consumption: Food Production Net Trade

Source: ReNAPRI Outlook, November 2014

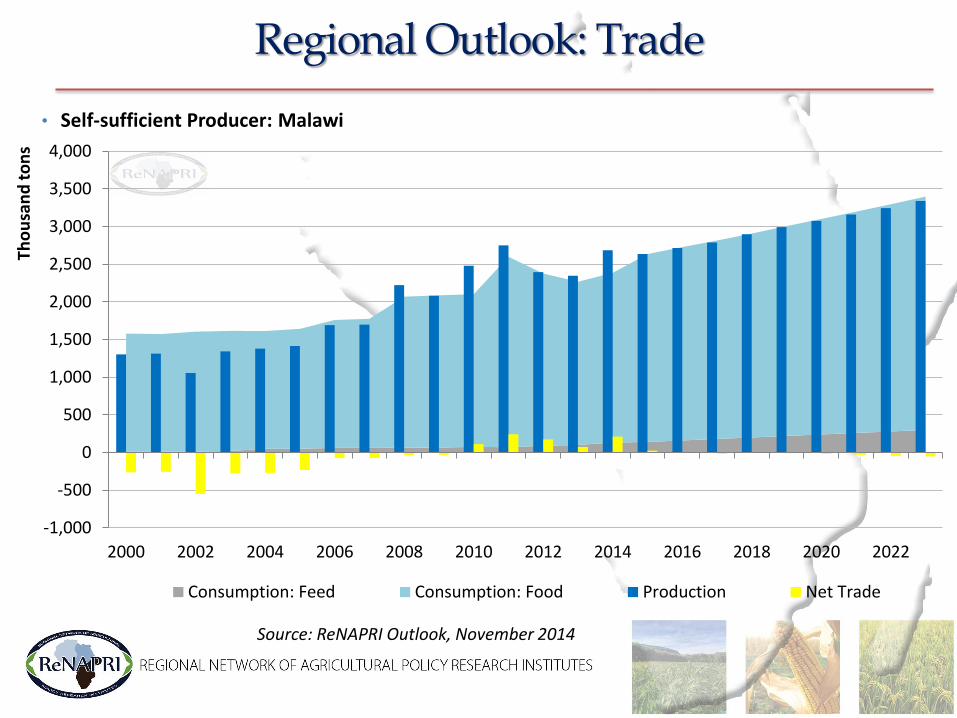

• Self-sufficient Producer: Malawi

Regional Outlook: Trade

-1,000

-500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Tho

usa

nd

to

ns

Consumption: Feed Consumption: Food Production Net Trade

Source: ReNAPRI Outlook, November 2014

• Self-sufficient Producer: Tanzania

Regional Outlook: Trade

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Tho

usa

nd

to

ns

Consumption: Feed Consumption: Food Production Net Trade

Source: ReNAPRI Outlook, November 2014

Regional Outlook: Production, Consumption & Trade

-5,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Tho

usa

nd

to

ns

Consumption - Feed Consumption - Food Production Net trade

Source: ReNAPRI Outlook, November 2014

Farm level analysis

Global Models:

FAPRI and OECD-FAO

GDP

Exchange rate

Interest rate

Regional prices

Weather

Population

Regional Policy

Farm Level Models:

Household Survey data

agri benchmark

FINSIM

Sector level Models: ReNAPRI Partial

Equilibrium

Livestock Grains

and oilseeds

Oil prices

ReNAPRI Modeling Framework

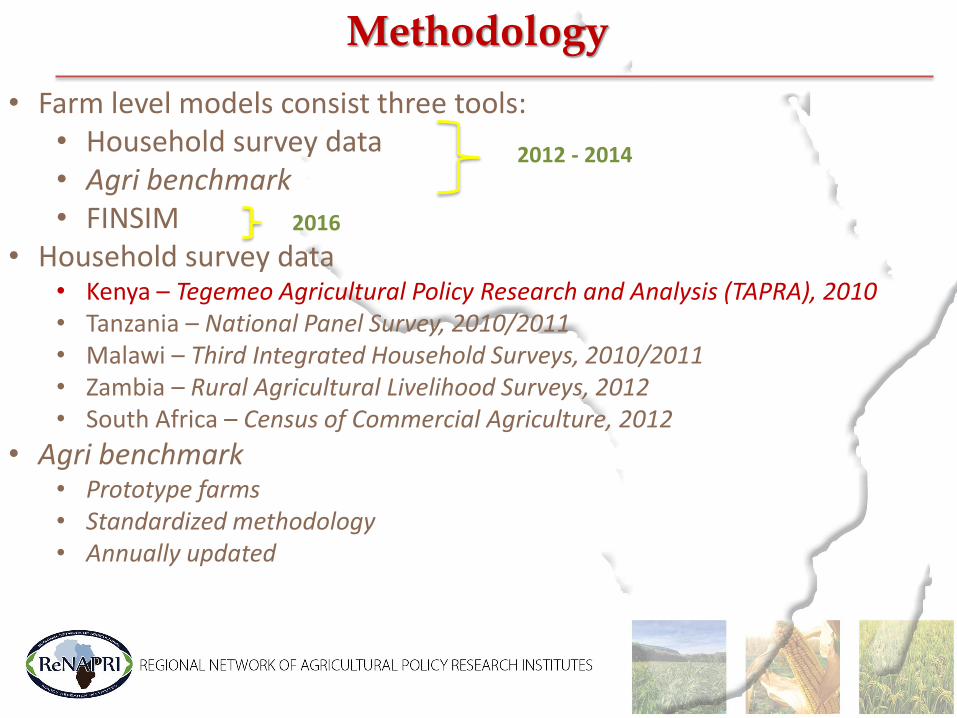

Methodology

• Farm level models consist three tools: • Household survey data • Agri benchmark • FINSIM

• Household survey data • Kenya – Tegemeo Agricultural Policy Research and Analysis (TAPRA), 2010 • Tanzania – National Panel Survey, 2010/2011 • Malawi – Third Integrated Household Surveys, 2010/2011 • Zambia – Rural Agricultural Livelihood Surveys, 2012 • South Africa – Census of Commercial Agriculture, 2012

• Agri benchmark • Prototype farms • Standardized methodology • Annually updated

2012 - 2014

2016

Methodology

• Survey Data and Agri benchmark locations

Case Study: Kenya

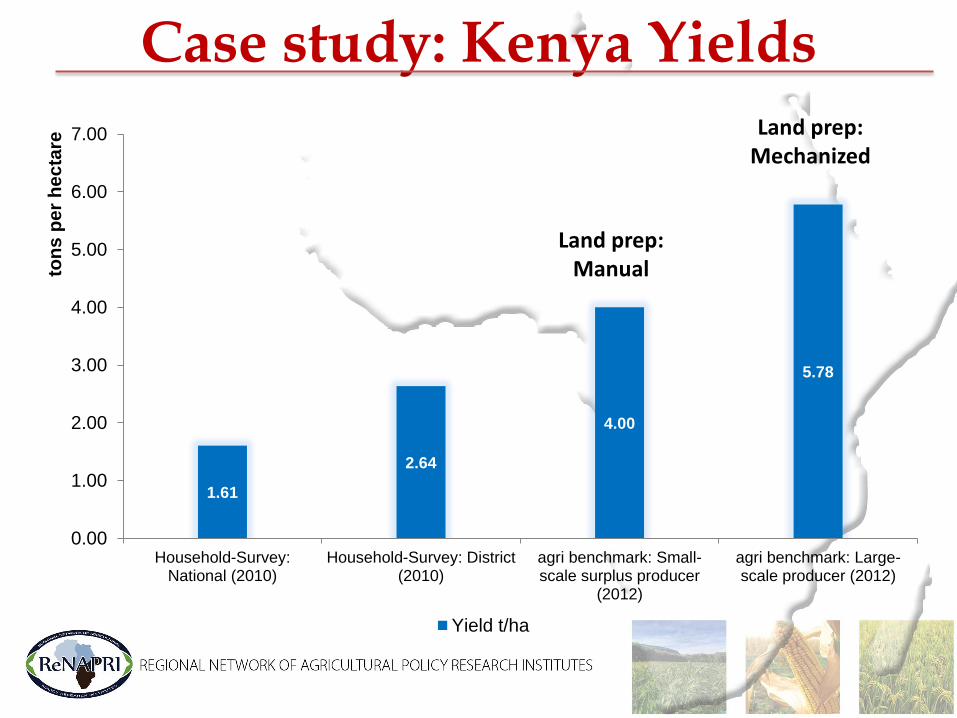

Case study: Kenya Yields

1.61

2.64

4.00

5.78

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

Household-Survey:National (2010)

Household-Survey: District(2010)

agri benchmark: Small-scale surplus producer

(2012)

agri benchmark: Large-scale producer (2012)

ton

s p

er

he

cta

re

Yield t/ha

Land prep: Mechanized

Land prep: Manual

Case study: Kenya Fertilizer & Seed

87

151

309

371 22.2

24.7 24.7 24.7

20.5

21.0

21.5

22.0

22.5

23.0

23.5

24.0

24.5

25.0

0

50

100

150

200

250

300

350

400

Household-Survey:National (2010)

Household-Survey:District (2010)

agri benchmark: Small-scale surplus producer

(2012)

agri benchmark: Large-scale producer (2012)

Se

ed

: k

g p

er

he

cta

re

Fe

rtil

ize

r: k

g p

er

he

cta

re

Fertilizer application rates kg/ha Seed application rates kg/ha

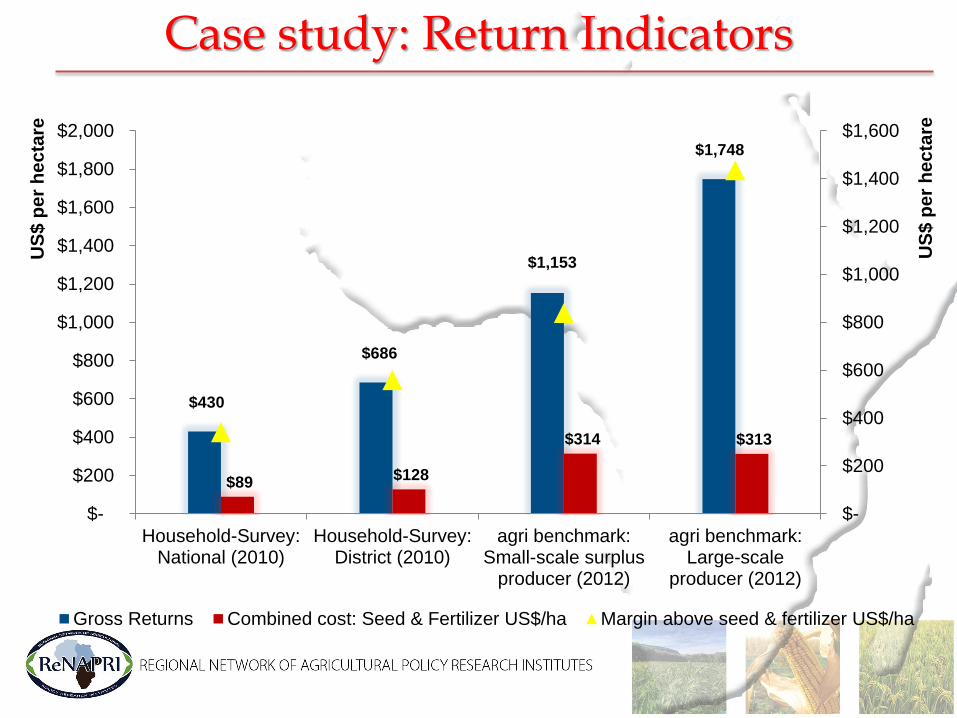

Case study: Return Indicators

$430

$686

$1,153

$1,748

$89 $128

$314 $313

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

Household-Survey:National (2010)

Household-Survey:District (2010)

agri benchmark:Small-scale surplus

producer (2012)

agri benchmark:Large-scale

producer (2012)

US

$ p

er

he

cta

re

US

$ p

er

he

cta

re

Gross Returns Combined cost: Seed & Fertilizer US$/ha Margin above seed & fertilizer US$/ha

Case Study: South Africa

Case Study: South Africa

• Specific case study in KwaZulu-Natal, South Africa - Same type of small-scale producer in the same area - Same size / same area - Difference: Mentorship (GSA vs. traditional)

Difference: Production Systems

Difference: Production Systems

• Lime application: 1 ton per hectare on farm with access to the support program - no lime application on farm that followed traditional methods

• Plant protection on the supported farms was done using chemical

treatments while traditional methods included only the use of hand hoes with manual labour

• A basal and top dressing fertilizer application on the farm that had

access to support while the traditional approach only had a basal application. The total NPK was less on the traditional approach as on the farm who obtained support.

• The type and amount of land preparations differed between the

two groups of farms

Case study: Return Indicators

Regional agri benchmark prototype farms network

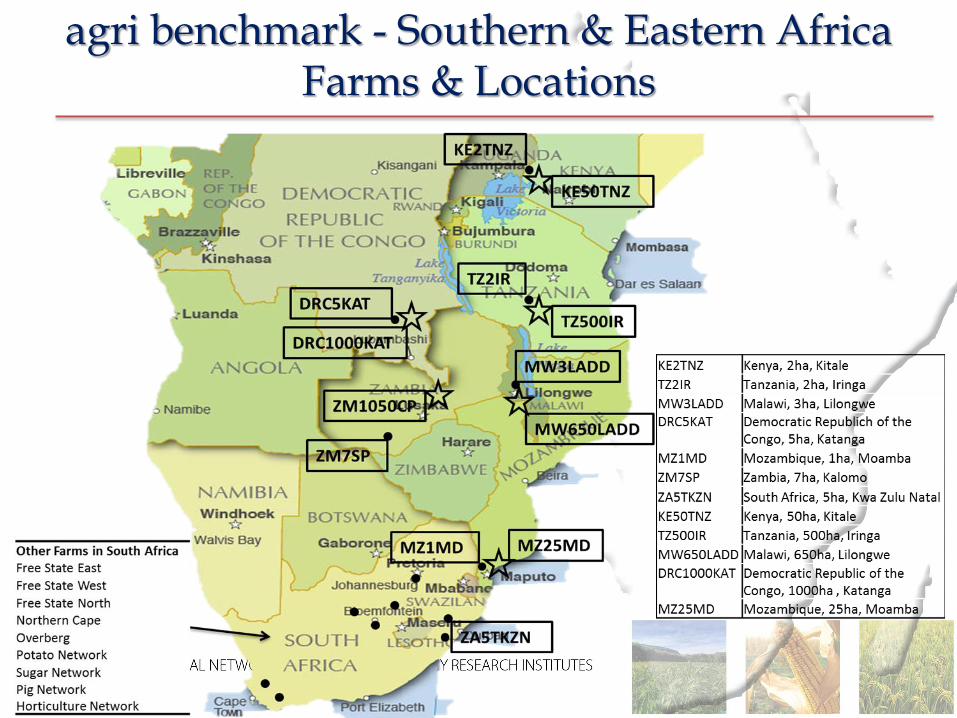

agri benchmark - Southern & Eastern Africa Farms & Locations

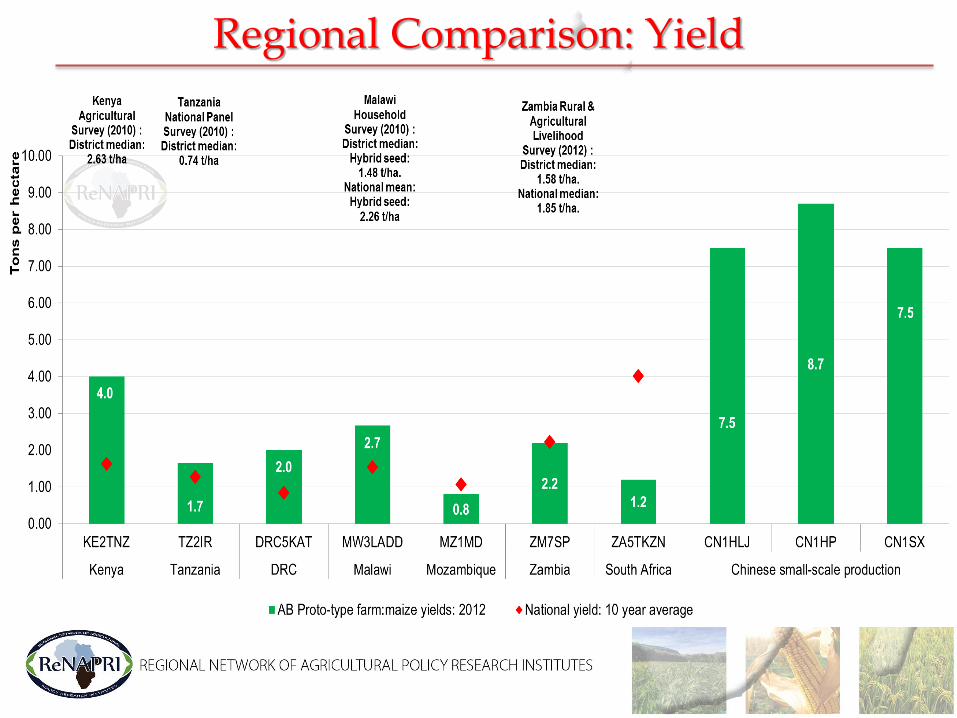

Regional Comparison: Yield

Nitrogen application & costs

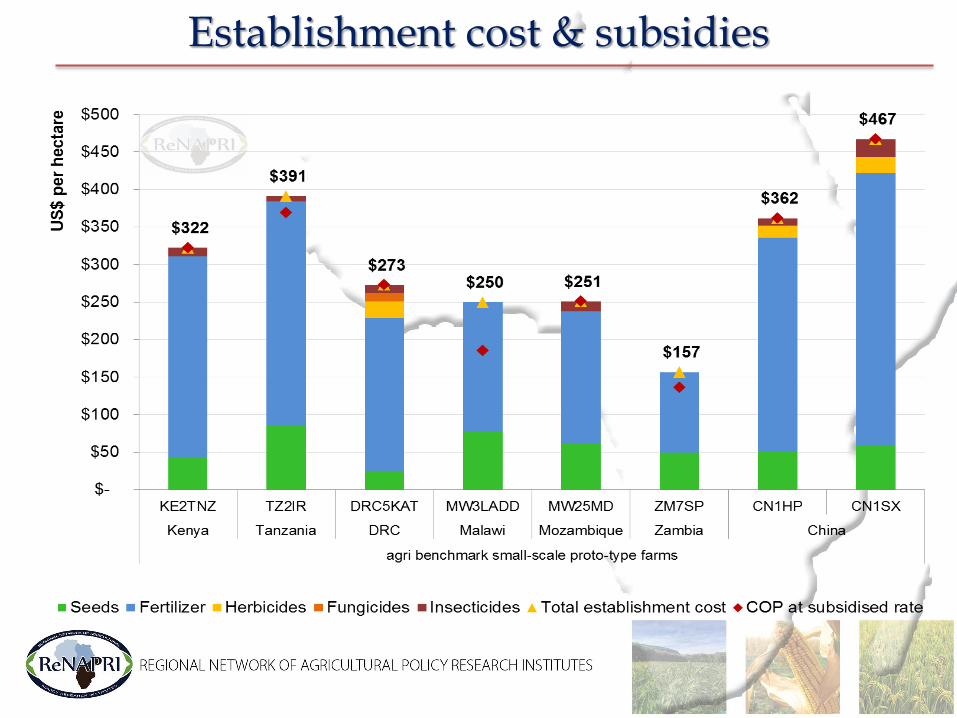

Establishment cost & subsidies

Scenario Planning & Strategic Foresighting:

Impacts of a Zambian maize export restriction

The scenario

• Zambia puts in place restrictions that reduce its 2015 maize exports by 200,000 tonnes

• All other policies in Zambia and in other countries remain as in the baseline

Impacts on Zambian maize markets in 2015

-200

76

13

111

-250

-200

-150

-100

-50

0

50

100

150

Exports Food use Feed use Endingstocks

Change from baseline, 1000 tonnes

-37

4 2

26

-27

-40

-30

-20

-10

0

10

20

30

Exports Fooduse

Feeduse

Endingstocks

Price

Change from baseline, percent

Impacts on regional maize markets in 2015

-200

51

18 15 11 11

94

-250

-200

-150

-100

-50

0

50

100

150

Change from baseline net exports, 1000 tonnes

-27

7

4 5

8 7

-30

-25

-20

-15

-10

-5

0

5

10

Zambia S.Africa

Kenya Malawi Moz. DRC

Change from baseline prices, percent

Impacts on Zambian maize in 2015 and 2016

-27

0 4 2

26

-37

-1 -2

0 3

8

1

-50

-40

-30

-20

-10

0

10

20

30

Price Production Food use Feed use Ending stocks Exports

Percentage change from baseline

2015 2016

Some lessons

• Lower prices in Zambia hurt producers, help consumers

• Reduced Zambian exports raise prices in other countries

– Exporters export more; importers import less

– Higher prices benefit producers, hurt consumers

• Changes in relative prices provide incentives for unsanctioned trade

• Effects can last beyond the year of the export restrictions

Political Context: Critical Questions

• Critical Questions:

– How do we achieve these targets?

– What is the Road-map to Implementation?

• Regional Network of Agricultural Policy Research Institutes (ReNAPRI)

– Offers a multifaceted approach to policy analysis:

Shukran

Nkosi

Obrigado

Merci

Thank you