oslo, 10 february 2015 q4 2014 presentation - evry · •gaining share in sme outsourcing o five...

TRANSCRIPT

Q4 2014

Presentation

CEO Terje Mjøs

Oslo, 10 February 2015

2

• Part I – Q4`14 Report

o Highlights

o Group

o Segments

o Key figures 2014

• Part II – Market outlook

• Summary

• Appendix

Q4 2014 presentation

Highlights

3

Q4 2014 presentation

• Apax offer of NOK 16 per share recommended by the Board of Directors

o Offer period extended until February 11

o Acceptance as of February 3 was approximately 87%

• Increase in order back-log of NOK 0.7 billion

o Contract with a group of savings banks awarded

• EBITA margins increasing

o EVRY Financial Services continues to strengthen its EBITA margin

o EVRY Sweden reports solid improvement

o EVRY Norway lagging

• Further reduction in working capital

Q

4

2

0

1

3

p

r

e

s

e

n

t

a

t

i

o

n

Group figures

EVRY Q4 2014 – Part I

4

Solid cash flow and increased EBITA margin

5

Q4 2014 presentation

• Revenue NOK 3,364 million (3,473)o Organically down -3 %

• EBITA** up to NOK 268 million (243)o Margin 8.0 (7%)

• Solid operational cash flow** of NOK 706million (691) in Q4o Working capital still declining

• Earnings per share** NOK 0.67 (0.46)

*Decision made to close EVRY Denmark A/S, hence business classified as

discontinued, EBITA and revenue figures restated accordingly

**Before non-recurring items

Key group figures*

Non-recurring items

6

Q4 2014 presentation

• Non-recurring items of NOK 138 million in the quarter

o Restructuring costs of NOK 75 million related to FTE

reductions in Norway and Sweden

- In line with guiding given in Q3

o Costs related to the strategic process in EVRY of NOK

63 million

• Costs related to close down of SAP unit in Denmark (NOK 17 million) included in the figure reported as discontinued operations

- Restructuring costs somewhat lower than guiding

given in Q3

Key group figures

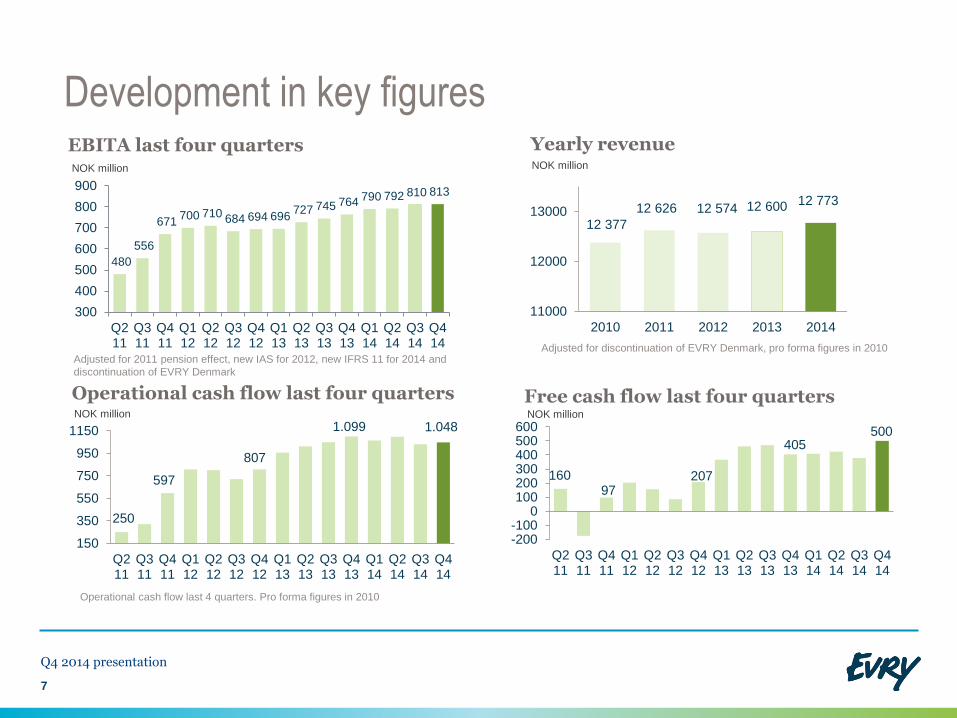

Development in key figures

7

Yearly revenueEBITA last four quarters

NOK million

Operational cash flow last 4 quarters. Pro forma figures in 2010

Operational cash flow last four quarters

Adjusted for 2011 pension effect, new IAS for 2012, new IFRS 11 for 2014 and

discontinuation of EVRY Denmark

NOK million NOK million

Q4 2014 presentation

Adjusted for discontinuation of EVRY Denmark, pro forma figures in 2010

480

556

671 700 710 684 694 696

727 745 764 790 792 810 813

300

400

500

600

700

800

900

Q211

Q311

Q411

Q112

Q212

Q312

Q412

Q113

Q213

Q313

Q413

Q114

Q214

Q314

Q414

12 377

12 626 12 574 12 600 12 773

11000

12000

13000

2010 2011 2012 2013 2014

250

597

807

1.099 1.048

150

350

550

750

950

1150

Q211

Q311

Q411

Q112

Q212

Q312

Q412

Q113

Q213

Q313

Q413

Q114

Q214

Q314

Q414

160 97

207

405 500

-200-100

0100200300400500600

Q211

Q311

Q411

Q112

Q212

Q312

Q412

Q113

Q213

Q313

Q413

Q114

Q214

Q314

Q414

Free cash flow last four quartersNOK million

Continued growth in Sweden and Financial Services

8

Q4 2014 presentation

12%

2%0% -2%

4%

12%10%

6%

1%

4% 3%

-5%

0%

5%

10%

15%

Q212

Q312

Q412

Q113

Q213

Q313

Q413

Q114

Q214

Q314

Q414

-3%

-9%

-5%

-7%

-4%-5%

1%

4%

1%

-1%

-7%-10%

-5%

0%

5%

Q212

Q312

Q412

Q113

Q213

Q313

Q413

Q114

Q214

Q314

Q414

14%

9%

-5% -4%

-9%

-6%

1%3%

6%

2% 1%

-10%

-5%

0%

5%

10%

15%

Q212

Q312

Q412

Q113

Q213

Q313

Q413

Q114

Q214

Q314

Q414

EVRY Financial Services

EVRY NorwayEVRY Sweden

3%

-1% -6% -6% -2%-2%

6%

3%2% 2%

-3%

-10%

-5%

0%

5%

10%

Q212

Q312

Q412

Q113

Q213

Q313

Q413

Q114

Q214

Q314

Q414

EVRY

0

1

2

3

4

5

6

0

200

400

600

2009 2010 2011 2012 2013 2014

Software developed in-house Ordinary capex Percentage

• Continued positive effects from the working capital project

• CAPEX decreasing

o Less investments within operations businesses

o Core and payment projects in EVRY Financial Services at full speed by end Q1 ‘15

Key financials

9

Q4 2014 presentation

NOK millionPercent of revenueCAPEX

Average last 4 quarters

Working capitalNOK millionPercent of revenue

Average last 4 quarters

Target

4%

5.7

6.5 6.7 6.86.3

6.05.5

5.1 4.94.5 4.3

3.83.3

2.9

0

1

2

3

4

5

6

7

8

Q311

Q411

Q112

Q212

Q312

Q412

Q113

Q213

Q313

Q413

Q114

Q214

Q314

Q414

Percent of revenue

Target

corridor

10

Q4 2014 presentation

Increase in order backlog

0

2000

4000

6000

8000

2015 2016 2017 2018

EVRY Norway EVRY Financial Services EVRY Sweden

Order backlog NOK 18 bnNOK million

Market highlights

17.1 16.816.1

15.5 15.3 15.0 15.3 15.3 15.114.2

16.6 16.5

18.4

17.318.0

10

12

14

16

18

20

Q211

Q311

Q411

Q112

Q212

Q312

Q412

Q113

Q213

Q313

Q413

Q114

Q214

Q314

Q414

Order backlog NOK billion

• Long-term partnership with four Norwegian banks

o Payment and core bank renewal NOK 1.2 bn

• Gaining share in SME outsourcing

o Five new customers signed

• Strategic wins in public sector

o Continued partnership with Folkeregisteret

o Healthcare in both Sweden and Norway

• New signings NOK 4.1 billion

o EVRY Financial Services NOK 1.7 billion

o EVRY Sweden NOK 0.9 billion

o EVRY Norway NOK 1.5 billion

Segments

EVRY Q4 2014

• Revenue NOK 988 million (959 )

o Organic growth driven by EVRY Card Services and Custom Solutions in Sweden

o Revenue from Solutions portfolio also increasing

• EBITA NOK 112 million (99 )

o Improved performance in Operations

o Revenue increase lifts EBITA margin

• CAPEX at low levels

o Depreciation well above investments

Highlights & Key figures

EVRY Financial Services – continued organic growth

12

Q4 2014 presentation

* Organic growth

NOK million Q4 2014 Q4 2013 Y/Y

Revenue 988 959 3%

EBITA 112 99 13%

EBITA margin 11.4% 10.3 %

CAPEX 32 55

Employees 1,457 1,490

Percent

Margin development EVRY Financial Services

EBITA-margin - moving average last 4 quarters

Target

corridor

8.58.9 9.2 9.4 9.4 9.3 9.1 9.2 8.9

9.49.8 10.1

3

6

9

12

Q112

Q212

Q312

Q412

Q113

Q213

Q313

Q413

Q114

Q214

Q314

Q414

• Revenue NOK 939 million (936 )

o SME IT operations shows healthy growth

o Market recovery still slow

• EBITA at NOK 101 million (77 )

o Restructuring giving effects

o Considerable improvement in consulting, utilisation rates up (+4.8%)

o Good performance in Healthcare and SME IT Operations continues

Highlights & Key figures

EVRY Sweden – solid margin improvement

13

Q4 2014 presentation

*Organic growth

NOK million Q4 2014 Q4 2013 Y/Y

Revenue 939 936 1%*

EBITA 101 77 31%

EBITA margin 10.8% 8.3 %

Capex 30 20

Utilisation 73.3% 68.5 %

Working days 62 62

Employees 2,219 2,308

Percent

Margin development EVRY Sweden

EBITA-margin - moving average last 4 quarters

6.7 7.0 7.1 7.1 6.8 6.6 6.5 6.4 6.5 6.4 6.67.3

2

4

6

8

10

Q112

Q212

Q312

Q412

Q113

Q213

Q313

Q413

Q114

Q214

Q314

Q414

Target

corridor

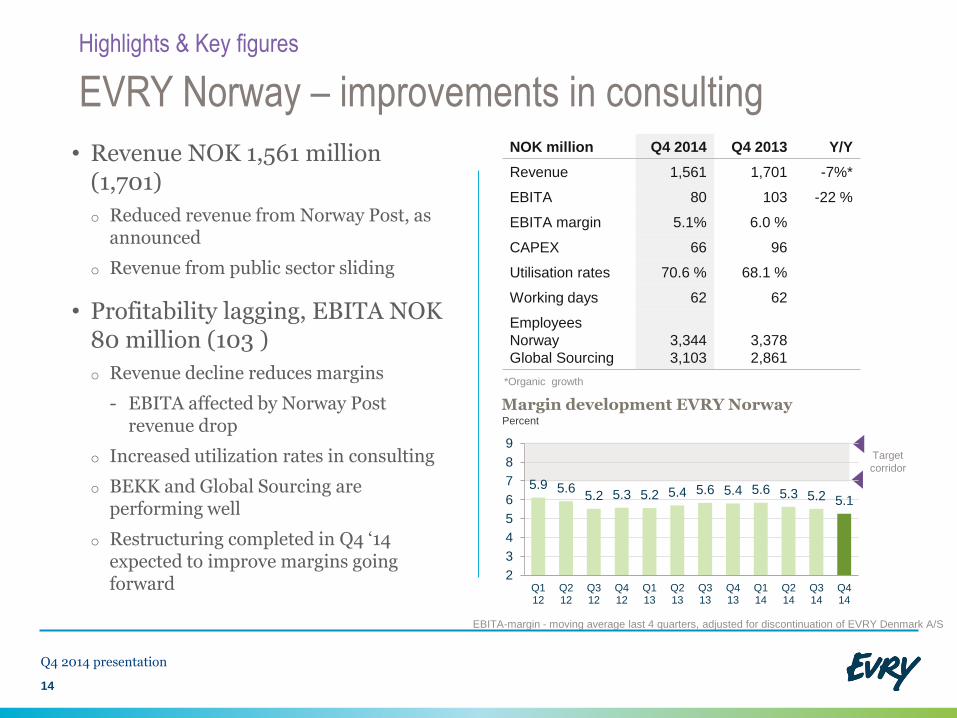

• Revenue NOK 1,561 million (1,701)

o Reduced revenue from Norway Post, as announced

o Revenue from public sector sliding

• Profitability lagging, EBITA NOK 80 million (103 )

o Revenue decline reduces margins

- EBITA affected by Norway Post revenue drop

o Increased utilization rates in consulting

o BEKK and Global Sourcing areperforming well

o Restructuring completed in Q4 ‘14 expected to improve margins goingforward

Highlights & Key figures

EVRY Norway – improvements in consulting

14

Q4 2014 presentation

*Organic growth

EBITA-margin - moving average last 4 quarters, adjusted for discontinuation of EVRY Denmark A/S

NOK million Q4 2014 Q4 2013 Y/Y

Revenue 1,561 1,701 -7%*

EBITA 80 103 -22 %

EBITA margin 5.1% 6.0 %

CAPEX 66 96

Utilisation rates 70.6 % 68.1 %

Working days 62 62

Employees

Norway

Global Sourcing

3,344

3,103

3,378

2,861

Percent

Margin development EVRY Norway

Target

corridor

5.9 5.65.2 5.3 5.2 5.4 5.6 5.4 5.6 5.3 5.2 5.1

2

3

4

5

6

7

8

9

Q112

Q212

Q312

Q412

Q113

Q213

Q313

Q413

Q114

Q214

Q314

Q414

Q

1

2

0

1

2

p

r

e

s

e

n

t

a

t

i

o

n

EVRY Q4 2014

Key figures 2014

1

5

Highlights & Key figures

EVRY full year 2014

16

Q4 2014 presentation

NOK million 2014 2013 Y/Y

Revenue 12,773 12,600 1 %*

EBITA** 813 764 6 %

EBITA margin 6.4% 6.1 %

EPS** 1.85 1.49

597

807

1099

1048

400

600

800

1000

2011 2012 2013 2014

Operational cash flow development

NOK million

559677 694

764 813

500

600

700

800

2010 2011 2012 2013 2014

EBITA development *

NOK million

* Organic growth ** Before non-recurring items* Before non-reccuring items, adjusted for discontinuation of EVRY Denmark A/S

97207

405 500

0

200

400

600

2011 2012 2013 2014

Free cash flow development

NOK million

Figures adjusted for discontinuation of EVRY Denmark A/S

Q

4

2

0

1

3

p

r

e

s

e

n

t

a

t

i

o

n

EVRY Q4 2014

Outlook

1

7

18

Q4 2014 presentation

Market outlook Sweden

• Domestic consumer and services markets areoffsetting negative global trends. Moderate upward adjustment to GDP outlook

• IT services market growth projected to improvecompared to 2014

Market outlook Norway

• Growth in IT services in Norway expected to exceedGDP growth somewhat

o GDP growth for 2015 projected to hit lowest level since2009

• Price pressure for generic consulting services expected to prevail in 2015

• Banks and financial institutions expected to increase IT spending, investing in channels and mobility

19

Q4 2014 presentation

Summary Q4`14

• Apax offer of NOK 16 per share recommended by the Board of Directors

o Offer period extended until February 11

o Acceptance as of February 3 was approximately 87%

• Increase in back-log of NOK 0.7 billion

o Contract with a group of savings banks awarded

• EBITA margins increasing, EBITA up to NOK 268 million (243)

o EVRY Financial Services higher up in the margin corridor

o EVRY Sweden reports solid improvement

o EVRY Norway lagging

• Working capital at lowest levels ever, 2.9% of last four quarters’ revenue

• Record high free cash flow in 2014 of NOK 500 million

o Operational cash flow stable

o Lower investments

Q

4

2

0

1

3

p

r

e

s

e

n

t

a

t

i

o

n

2

0

Q

4

2

0

1

3

p

r

e

s

e

n

t

a

t

i

o

n

EVRY Q4 2014

Appendix

2

1

Key consolidated figures for the Group*

22

Q4 2014 presentation

(NOK million) Q4 2014 Q4 2013 Change (%) 2014 2013 Change (%)

Operating revenue 3,364 3,473 -3 %1) 12,773 12,600 1 %1)

EBITDA 398 380 5 % 1,290 1,219 6 %

EBITA before non-recurring items 268 243 10 % 813 764 6 %

EBITA % before non-recurring items 8.0 % 7.0 % 6.4 % 6.1 %

EBIT before non-recurring items 260 235 780 731

Non-recurring items 138 586 271 621

EBIT 122 -351 509 110

Net financial items 3 -53 -89 -169

EBT 125 -404 421 -59

EPS (NOK)2) 0.67 0.46 1.85 1.49

Employees 10,350 10,295

Net interest bearing debt/EBITDA 2.46 2.49

* Adjusted for discontinuation of EVRY Denmark A/S 1) Organic growth 2) Before non-recurring items

Q

4

2

0

1

3

p

r

e

s

e

n

t

a

t

i

o

n

2

3