organized by - india...

TRANSCRIPT

For further details, please contact

Ms. Ranjita C. SoodSr. Asst Director-Chemicals Division

FICCIFederation House, 1 Tansen Marg, New Delhi-110 001

Tel: +91-11-2335 7350 (Dir)EPBX: +91-11-2373 8760-70 (Extn 474)

Fax: +91-11-2332 0714/ 2372 1504E- Mail: [email protected]

Mr. R K Bhatia Head-Chemicals Division

FICCIFederation House, 1 Tansen Marg, New Delhi-110 001

Tel: +91-11-2331 6540 (Dir)EPBX: +91-11-2373 8760-70 (Extn 395)

Fax: +91-11-2332 0714/ 2372 1504E- Mail: [email protected]

Website: www.ficci.com

CCFI INDIA

Organized by

Website: www.ficci.com

Dept of Chemicals & PetrochemicalsGovt of India

Conference on

AGROCHEM CALS AGROCHEM CALS 2011

February 10-11, 2011Venue: Nehru Centre, Mumbai

Theme: Opportunities, Challenges, Innovations and Imperatives for Growth of Indian Agrochemical Industry

R

Thank you Partners

Silver Partners

Platinum Partner

Kit Partner

Supported by

Knowledge Partner

Crystal Phosphates Ltd.

Cheminova India Ltd. Dhanuka Agritech Ltd. Hikal Ltd

Conference on

AGROCHEM CALS 2011

23

Content

n

n

n

n

n

n

n

Preface . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

Farming solutions - the next frontier for . . . . . . . . . . . . . . . . . . . . . 27

breakthrough growth of Indian agrochemical companies

Introduction to Agrochemicals . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

Global market overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

Indian market overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

IPM and newer methods of crop protection . . . . . . . . . . . . . . . . . . 52

Profiles of key manufacturers. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

Content

n

n

n

n

n

n

n

Preface . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 01

Farming solutions - the next frontier for . . . . . . . . . . . . . . . . . . . . . 03

breakthrough growth of Indian agrochemical companies

Introduction to Agrochemicals . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 07

Global market overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 09

Indian market overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

IPM and newer methods of crop protection . . . . . . . . . . . . . . . . . . 28

Profiles of key manufacturers. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

25

FICCI is jointly with Dept. of Chemicals & Petrochemicals, Ministry of Chemicals & Fertilizers, Govt. of

India is organizing "Conference on Agrochemicals-2011" on February 10-11, 2011 at Nehru Centre,

Mumbai. The theme of the conference is "Opportunities, Challenges, Innovations & Imperatives

for Growth of Indian Agrochemical Industry". The conference is supported by Crop Care Federation

of India, CropLife India & PMFAI.

The one and half days "Conference on Agrochemicals-2011" would provide a roadmap for the Indian

Agro industry in terms of globalization, the key issues involved in globalization, some of the

challenges faced by the industry in terms of improving the productivity and how the industry should

be more export oriented than it is today. Theme of the conference "Opportunities, Challenges,

Innovations & Imperatives for Growth of Indian Agrochemical industry" would indeed serve its

purpose by throughing light on Indian Agrochemicals Industry.

Recently Task Force on Chemicals was set up by Chemicals & Petrochemicals, Govt. of India, headed

by Shri Arun Maira, Member, Planning Commission, covering the entire chemical industry, divided

into various sub-sectors. I am heading the sub-sector Agrochemicals. Important Recommendations

on Agrochemicals will be mentioned in my "Theme Presentation" at the conference.

The global market of pesticides and agro industry is very huge ~$44 billion. Globally, due to higher

productivity, decline in the green movement, tight regulations and better crop management, the

pesticide industry is not growing very rapidly. In fact, it is stagnant or slightly declining. In India, the

agro industry has grown significantly over the last 30-40 years from a mere Rs.400 Cr. to over Rs.

8,000 Cr. today.

The Indian Agrochemical industry is the fourth largest in the world only after the US, Japan and

China and has undergone many changes over the years. Insecticides account for the largest share of

the Indian crop protection market - 55%. Fungicides - 20%, Herbicides - 20% and Bio-pesticides and

others - 5%. The consumption pattern is: paddy pesticides - 28%, cotton pesticides - 20% and others

52%. Exports account for over 47% of total Indian agrochemicals industry turnover.

In India 60%-70% of the population lives on agro income. Nearly, one-third of our GDP is agro-

based. We earn a very significant part of foreign exchange. The agrochemical industry can play a

very important and a very vital role. Our agro industry management is something we should debate

Jai HiremathChairman, National Chemicals Committee, FICCI Vice Chairman & Mg. Director, Hikal Ltd.

Preface

01

FICCI is jointly with Dept. of Chemicals & Petrochemicals, Ministry of Chemicals & Fertilizers, Govt. of

India is organizing "Conference on Agrochemicals-2011" on February 10-11, 2011 at Nehru Centre,

Mumbai. The theme of the conference is "Opportunities, Challenges, Innovations & Imperatives

for Growth of Indian Agrochemical Industry". The conference is supported by Crop Care Federation

of India, CropLife India & PMFAI.

The one and half days "Conference on Agrochemicals-2011" would provide a roadmap for the Indian

Agro industry in terms of globalization, the key issues involved in globalization, some of the

challenges faced by the industry in terms of improving the productivity and how the industry should

be more export oriented than it is today. Theme of the conference "Opportunities, Challenges,

Innovations & Imperatives for Growth of Indian Agrochemical industry" would indeed serve its

purpose by throughing light on Indian Agrochemicals Industry.

Recently Task Force on Chemicals was set up by Chemicals & Petrochemicals, Govt. of India, headed

by Shri Arun Maira, Member, Planning Commission, covering the entire chemical industry, divided

into various sub-sectors. I am heading the sub-sector Agrochemicals. Important Recommendations

on Agrochemicals will be mentioned in my "Theme Presentation" at the conference.

The global market of pesticides and agro industry is very huge ~$44 billion. Globally, due to higher

productivity, decline in the green movement, tight regulations and better crop management, the

pesticide industry is not growing very rapidly. In fact, it is stagnant or slightly declining. In India, the

agro industry has grown significantly over the last 30-40 years from a mere Rs.400 Cr. to over Rs.

8,000 Cr. today.

The Indian Agrochemical industry is the fourth largest in the world only after the US, Japan and

China and has undergone many changes over the years. Insecticides account for the largest share of

the Indian crop protection market - 55%. Fungicides - 20%, Herbicides - 20% and Bio-pesticides and

others - 5%. The consumption pattern is: paddy pesticides - 28%, cotton pesticides - 20% and others

52%. Exports account for over 47% of total Indian agrochemicals industry turnover.

In India 60%-70% of the population lives on agro income. Nearly, one-third of our GDP is agro-

based. We earn a very significant part of foreign exchange. The agrochemical industry can play a

very important and a very vital role. Our agro industry management is something we should debate

Jai HiremathChairman, National Chemicals Committee, FICCI Vice Chairman & Mg. Director, Hikal Ltd.

Preface

02

about, with over Rs.1,40,000 Cr. of food grains wasted in transportation after production. We can

always compare global numbers on the use of pesticides in India - about 600 grams per hectare

versus 7 kg. in USA and 13 kg in China, which shows lack of pesticide usage or technology in terms of

crop management. We need to address some of the issues of low productivity in our rural crop

management. The industry needs to take a step beyond selling the product to helping in better crop

management practices, which will in turn contribute to the growth of the domestic industry.

Continuous innovation has led to development of crop protection products with lower usage rates

and better degradability leading to lower environmental loading, improved human safety profile for

farmers, workers and consumers, high biological efficacy, selective control of target pests, increased

safety to specific beneficiaries, naturally occurring insects and organisms. India needs country-

specific research and investment opportunities, proper legislation on patent and data protection to

exploit our own intellectual skills.

There is tremendous opportunity for the Indian Pesticide Industry to manufacture and introduce off

patent products. However due to ambiguity in registration the progress of the industry has been on

hold. With our huge talent pool of qualified Indian scientists and technicians, we should look at

increasing investments and are well capable of introducing newer molecules. Ample opportunities

are available for growth. With better infrastructure and R&D programmes funded by Government,

the Indian agrochemical industry could look forward to a very robust 15%-20% growth in the future.

The comprehensive Report prepared by FICCI and Tata Strategic Management Group (TSMG)

would help potential foreign and domestic investors in understanding the vast investment

opportunities available in Indian Agrochemicals Industry. The report will also serve as a ready

reckoner for those connected with Agrochemical Industry.

This conference on agrochemicals is the most timely initiative and I am sure the participants would

benefit immensely from the event.

I wish the event all success.

Jai Hiremath

27

India has a population of 1.18 billion which is expected to reach 1.45 billion by 2030. This rising

population will lead to increasing demand for food grains. On the other hand, per capita land

available for agriculture has been steadily decreasing. This coupled with rapid urbanization and non

availability of agricultural manpower has had a strong impact on farm production. Agricultural

produce has not been growing in tune with demand. Currently average crop yields in India are much

lower than global benchmarks. For example, average yield for rice is 3.2 tons/ha in India vis-à-vis 4.2

tons/ha globally. Similarly, yields for soybean and corn are 1.0 and 2.4 tons/ha domestically

compared to 2.5 and 5.0 tons/ha globally. The current price increases of food products reflect the

situation having reached alarming levels and we have to rely on imports to meet our domestic

consumption. This is only expected to worsen further if we do not take necessary steps to reverse it.

Improving crop yields has become very critical and will become imperative in the future.

India has the resources necessary to meet all its increasing needs and be left with a handsome

surplus if we can use our significantly large area under cultivation effectively. This would however

call for a holistic 'friend of the farmer' approach, offering locally relevant farming solutions, where

agrochemical companies could lead and benefit by improving yield and productivity. The Indian

agrochemical industry, which is Rs. 15,000 Cr today, could grow well beyond its aspirational target of

Rs. 50,000 Cr by 2020. The opportunity lies in developing and executing innovative farming solutions

that address the needs of the Indian farmer with very low landholding size, resources and knowhow

available to him. Farming solutions would require a collaborative approach together with seed

technology, IT, nutrients and other service providers. For the agrochemical companies it implies that

to achieve such growth, capacity additions of over 100,000 tons would be required with significant

capital investments of over Rs 3,000 Cr. In addition, substantial investment will be required for R&D

and farmer-awareness activities.

Besides effectively creating farming solutions with other partners, the Indian agrochemical industry

itself faces critical challenges which could hinder its growth if not addressed effectively. The industry

is predominantly generic in nature with very little investment in R&D. Lack of awareness amongst

farmers on usage of agrochemicals and best practices followed globally is a major roadblock for the

growth of the industry. Current per capita consumption of pesticides in India continues to be very

low at 0.6 kg/ha compared to 7 kg/ha in USA and 13 kg/ha in China. It is estimated that crop losses

in India due to non usage of agrochemicals amount to Rs. 90,000 Cr p.a. Relatively weak IP

protection regime is another area of concern. A huge parallel market for spurious and spiked

Farming solutions - the next frontier for breakthrough growth of Indian agrochemical companies

26

about, with over Rs.1,40,000 Cr. of food grains wasted in transportation after production. We can

always compare global numbers on the use of pesticides in India - about 600 grams per hectare

versus 7 kg. in USA and 13 kg in China, which shows lack of pesticide usage or technology in terms of

crop management. We need to address some of the issues of low productivity in our rural crop

management. The industry needs to take a step beyond selling the product to helping in better crop

management practices, which will in turn contribute to the growth of the domestic industry.

Continuous innovation has led to development of crop protection products with lower usage rates

and better degradability leading to lower environmental loading, improved human safety profile for

farmers, workers and consumers, high biological efficacy, selective control of target pests, increased

safety to specific beneficiaries, naturally occurring insects and organisms. India needs country-

specific research and investment opportunities, proper legislation on patent and data protection to

exploit our own intellectual skills.

There is tremendous opportunity for the Indian Pesticide Industry to manufacture and introduce off

patent products. However due to ambiguity in registration the progress of the industry has been on

hold. With our huge talent pool of qualified Indian scientists and technicians, we should look at

increasing investments and are well capable of introducing newer molecules. Ample opportunities

are available for growth. With better infrastructure and R&D programmes funded by Government,

the Indian agrochemical industry could look forward to a very robust 15%-20% growth in the future.

The comprehensive Report prepared by FICCI and Tata Strategic Management Group (TSMG)

would help potential foreign and domestic investors in understanding the vast investment

opportunities available in Indian Agrochemicals Industry. The report will also serve as a ready

reckoner for those connected with Agrochemical Industry.

This conference on agrochemicals is the most timely initiative and I am sure the participants would

benefit immensely from the event.

I wish the event all success.

Jai Hiremath

03

India has a population of 1.18 billion which is expected to reach 1.45 billion by 2030. This rising

population will lead to increasing demand for food grains. On the other hand, per capita land

available for agriculture has been steadily decreasing. This coupled with rapid urbanization and non

availability of agricultural manpower has had a strong impact on farm production. Agricultural

produce has not been growing in tune with demand. Currently average crop yields in India are much

lower than global benchmarks. For example, average yield for rice is 3.2 tons/ha in India vis-à-vis 4.2

tons/ha globally. Similarly, yields for soybean and corn are 1.0 and 2.4 tons/ha domestically

compared to 2.5 and 5.0 tons/ha globally. The current price increases of food products reflect the

situation having reached alarming levels and we have to rely on imports to meet our domestic

consumption. This is only expected to worsen further if we do not take necessary steps to reverse it.

Improving crop yields has become very critical and will become imperative in the future.

India has the resources necessary to meet all its increasing needs and be left with a handsome

surplus if we can use our significantly large area under cultivation effectively. This would however

call for a holistic 'friend of the farmer' approach, offering locally relevant farming solutions, where

agrochemical companies could lead and benefit by improving yield and productivity. The Indian

agrochemical industry, which is Rs. 15,000 Cr today, could grow well beyond its aspirational target of

Rs. 50,000 Cr by 2020. The opportunity lies in developing and executing innovative farming solutions

that address the needs of the Indian farmer with very low landholding size, resources and knowhow

available to him. Farming solutions would require a collaborative approach together with seed

technology, IT, nutrients and other service providers. For the agrochemical companies it implies that

to achieve such growth, capacity additions of over 100,000 tons would be required with significant

capital investments of over Rs 3,000 Cr. In addition, substantial investment will be required for R&D

and farmer-awareness activities.

Besides effectively creating farming solutions with other partners, the Indian agrochemical industry

itself faces critical challenges which could hinder its growth if not addressed effectively. The industry

is predominantly generic in nature with very little investment in R&D. Lack of awareness amongst

farmers on usage of agrochemicals and best practices followed globally is a major roadblock for the

growth of the industry. Current per capita consumption of pesticides in India continues to be very

low at 0.6 kg/ha compared to 7 kg/ha in USA and 13 kg/ha in China. It is estimated that crop losses

in India due to non usage of agrochemicals amount to Rs. 90,000 Cr p.a. Relatively weak IP

protection regime is another area of concern. A huge parallel market for spurious and spiked

Farming solutions - the next frontier for breakthrough growth of Indian agrochemical companies

04

pesticides exists which leads to significant revenue loss for genuine manufacturers. In addition, long

lead times for new product registrations and non-availability of land and regulatory clearances are

hindrances to setting up new investments.

The Indian agricultural landscape is distinct from most other countries of the world and needs to be

well understood to arrive at relevant farming solutions. We have a largely fragmented land-holding

structure (refer fig.1) with subsistence farming in several regions. Farmers are typically not educated

or exposed to modern methods of farming. The fragmented and small landholdings translate to

lesser spending power by individual farmers for seeds, irrigation, fertilizer or agrochemicals. Deeper

understanding of the market by geography, perhaps even at a district level, becomes critical to

success. These differences need to be clearly understood and call for customized solutions to suit

India's diverse agro-climatic conditions.

Agrochemical companies can take the lead to look beyond the traditional offerings and adopt a

Fig. 1: Land ownership pattern by district - rural India

29

holistic approach to farm management to enable India to achieve its true potential in agriculture.

These companies have a strong farmer-connect and reach, with the potential to influence and

change the way farming is traditionally done in this country. If ever there was a burning platform

necessitating this, it is now!

The Indian market abounds with such examples where innovative and customized solutions have

grown the market and catapulted the first movers to market leaders. The automotive industry in

India received a strong fillip with India becoming a manufacturing hub for small cars. A call to

develop the low cost car meeting specific needs of the Indian customer who could not afford it

earlier, helped to create and proliferate the low end 'micro' segment. Similarly, the paint industry

experienced a huge growth with introduction of tinting machines which offer customized paint

solutions closer to point of sale, recognizing the Indian consumer's need for tailored shades and

'look and feel' before deciding. Castrol took the initiative to develop a completely new channel for

lubricant sales. This offset the disadvantage of not being able to utilize traditional sales channels,

which were controlled by PSUs, and created a robust distribution network for Indian motorists and

car owners through other points of sale.

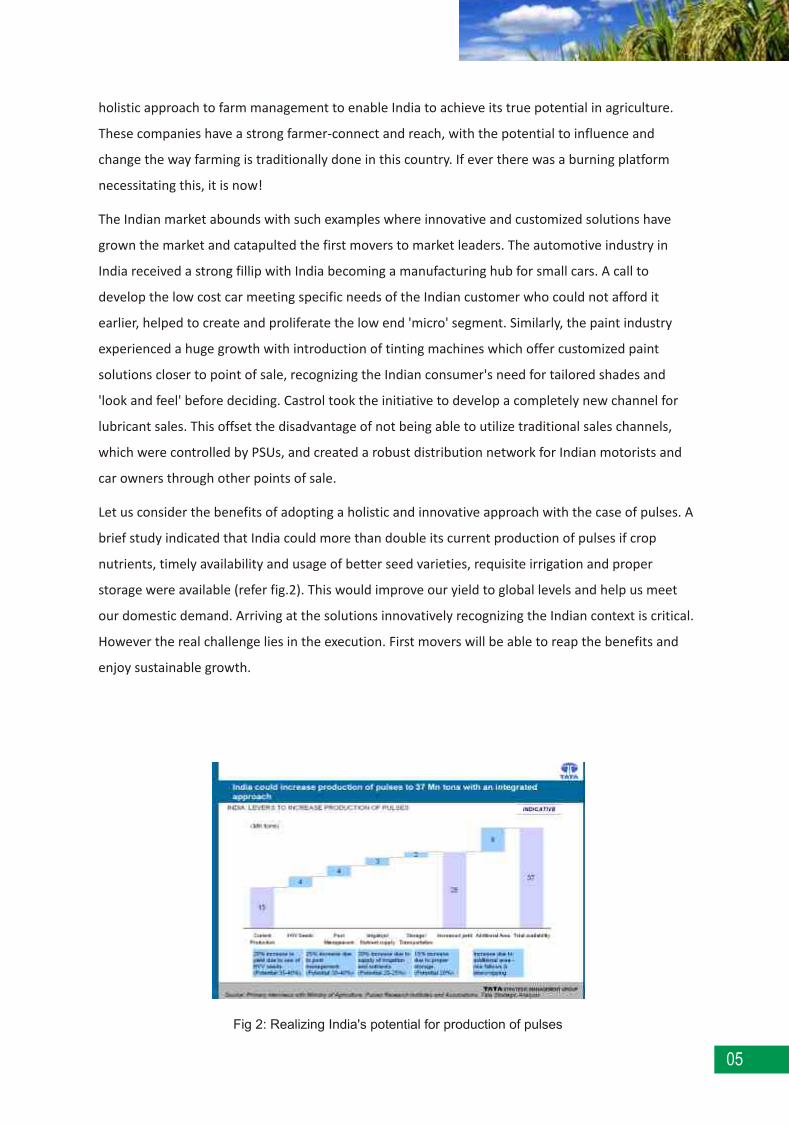

Let us consider the benefits of adopting a holistic and innovative approach with the case of pulses. A

brief study indicated that India could more than double its current production of pulses if crop

nutrients, timely availability and usage of better seed varieties, requisite irrigation and proper

storage were available (refer fig.2). This would improve our yield to global levels and help us meet

our domestic demand. Arriving at the solutions innovatively recognizing the Indian context is critical.

However the real challenge lies in the execution. First movers will be able to reap the benefits and

enjoy sustainable growth.

Fig 2: Realizing India's potential for production of pulses

28

pesticides exists which leads to significant revenue loss for genuine manufacturers. In addition, long

lead times for new product registrations and non-availability of land and regulatory clearances are

hindrances to setting up new investments.

The Indian agricultural landscape is distinct from most other countries of the world and needs to be

well understood to arrive at relevant farming solutions. We have a largely fragmented land-holding

structure (refer fig.1) with subsistence farming in several regions. Farmers are typically not educated

or exposed to modern methods of farming. The fragmented and small landholdings translate to

lesser spending power by individual farmers for seeds, irrigation, fertilizer or agrochemicals. Deeper

understanding of the market by geography, perhaps even at a district level, becomes critical to

success. These differences need to be clearly understood and call for customized solutions to suit

India's diverse agro-climatic conditions.

Agrochemical companies can take the lead to look beyond the traditional offerings and adopt a

Fig. 1: Land ownership pattern by district - rural India

05

holistic approach to farm management to enable India to achieve its true potential in agriculture.

These companies have a strong farmer-connect and reach, with the potential to influence and

change the way farming is traditionally done in this country. If ever there was a burning platform

necessitating this, it is now!

The Indian market abounds with such examples where innovative and customized solutions have

grown the market and catapulted the first movers to market leaders. The automotive industry in

India received a strong fillip with India becoming a manufacturing hub for small cars. A call to

develop the low cost car meeting specific needs of the Indian customer who could not afford it

earlier, helped to create and proliferate the low end 'micro' segment. Similarly, the paint industry

experienced a huge growth with introduction of tinting machines which offer customized paint

solutions closer to point of sale, recognizing the Indian consumer's need for tailored shades and

'look and feel' before deciding. Castrol took the initiative to develop a completely new channel for

lubricant sales. This offset the disadvantage of not being able to utilize traditional sales channels,

which were controlled by PSUs, and created a robust distribution network for Indian motorists and

car owners through other points of sale.

Let us consider the benefits of adopting a holistic and innovative approach with the case of pulses. A

brief study indicated that India could more than double its current production of pulses if crop

nutrients, timely availability and usage of better seed varieties, requisite irrigation and proper

storage were available (refer fig.2). This would improve our yield to global levels and help us meet

our domestic demand. Arriving at the solutions innovatively recognizing the Indian context is critical.

However the real challenge lies in the execution. First movers will be able to reap the benefits and

enjoy sustainable growth.

Fig 2: Realizing India's potential for production of pulses

06

Agrochemical companies could adopt specific crops or geographies within their sphere of influence

and help farmers increase output. This may mean working with various stakeholders such as

microfinance companies, adopting contract farming, increasing farmer awareness through

demonstrations and extension services, propagating better farm practices, ensuring right usage of

crop protection chemicals, increasing usage of hybrids/ GM seeds and providing better storage

facilities to reduce post harvest losses. The power of IT can be effectively leveraged to provide

farmers with timely advice and guidance for improving productivity, addressing pest related issues

and optimizing the value chain.

31

Chapter 1

Introduction

With increasing population, demand for food grains is increasing at a faster pace as compared to its

production. Moreover, every year, significant amount of crop yield is lost due to non usage of crop

protection products.

Agrochemicals are used to improve crop performance, yield or control pests, etc. Agrochemicals are

substances manufactured through chemical or biochemical processes containing the active

ingredient in a definite concentration along with other materials which improve its performance and

increase safety. For application, these are diluted with water in recommended doses and applied on

seeds, soil, irrigation water and crops to prevent the damages from pests.

There are broadly 5 categories of crop protection products:

1. Insecticides: Insecticides protect crops by killing insects or preventing their attack. Insecticides

may attack a particular type of insect or could be broad spectrum insecticides. Insecticides are

used to manage the pest population below the economic threshold level. E.g. Chlorpyrifos is

used to control insect pests in crops such as cotton, corn almonds, etc.

2. Fungicides: They are used to prevent the deterioration of crops due to fungi infestation.

Fungicides are classified as protectants or eradicants. Protectant fungicides prevent or inhibit

fungal growth and may have to be applied at regular intervals. Eradicant fungicides kill the pests

on application. E.g. Anilazine is used to control fungal attack on lawns and turfs, cereals, coffee

and various vegetables and other crops.

3. Herbicides: Herbicides or weedicides are used to prevent the growth of unwanted plants in a

crop field. Herbicides could be selective, which kill the unwanted plants without any harm to the

crop, or non-selective which kill all the plants. E.g. Glufosinate ammonium, a broad-spectrum

contact herbicide, is used to control weeds after the crop emerges or for total vegetation control

on land not used for cultivation.

4. Bio pesticides: These are derived from natural substances like plants, animals, bacteria and

certain minerals and control pests by nontoxic mechanisms. Bio-pesticides are considered eco-

friendly and easy to use. They could be classified as microbial pesticides, plant incorporated

protectants and biological pesticides. They are of low volume and high effect formulations and

require lesser dosages as compared to chemical pesticides. A growth area for bio-pesticides is in

the area of seed treatment and soil amendments. Example of bio-pesticides includes Bacillus

subtilis which is used as soil inoculant in horticulture and agriculture.

Introduction to Agrochemicals

30

Agrochemical companies could adopt specific crops or geographies within their sphere of influence

and help farmers increase output. This may mean working with various stakeholders such as

microfinance companies, adopting contract farming, increasing farmer awareness through

demonstrations and extension services, propagating better farm practices, ensuring right usage of

crop protection chemicals, increasing usage of hybrids/ GM seeds and providing better storage

facilities to reduce post harvest losses. The power of IT can be effectively leveraged to provide

farmers with timely advice and guidance for improving productivity, addressing pest related issues

and optimizing the value chain.

07

Chapter 1

Introduction

With increasing population, demand for food grains is increasing at a faster pace as compared to its

production. Moreover, every year, significant amount of crop yield is lost due to non usage of crop

protection products.

Agrochemicals are used to improve crop performance, yield or control pests, etc. Agrochemicals are

substances manufactured through chemical or biochemical processes containing the active

ingredient in a definite concentration along with other materials which improve its performance and

increase safety. For application, these are diluted with water in recommended doses and applied on

seeds, soil, irrigation water and crops to prevent the damages from pests.

There are broadly 5 categories of crop protection products:

1. Insecticides: Insecticides protect crops by killing insects or preventing their attack. Insecticides

may attack a particular type of insect or could be broad spectrum insecticides. Insecticides are

used to manage the pest population below the economic threshold level. E.g. Chlorpyrifos is

used to control insect pests in crops such as cotton, corn almonds, etc.

2. Fungicides: They are used to prevent the deterioration of crops due to fungi infestation.

Fungicides are classified as protectants or eradicants. Protectant fungicides prevent or inhibit

fungal growth and may have to be applied at regular intervals. Eradicant fungicides kill the pests

on application. E.g. Anilazine is used to control fungal attack on lawns and turfs, cereals, coffee

and various vegetables and other crops.

3. Herbicides: Herbicides or weedicides are used to prevent the growth of unwanted plants in a

crop field. Herbicides could be selective, which kill the unwanted plants without any harm to the

crop, or non-selective which kill all the plants. E.g. Glufosinate ammonium, a broad-spectrum

contact herbicide, is used to control weeds after the crop emerges or for total vegetation control

on land not used for cultivation.

4. Bio pesticides: These are derived from natural substances like plants, animals, bacteria and

certain minerals and control pests by nontoxic mechanisms. Bio-pesticides are considered eco-

friendly and easy to use. They could be classified as microbial pesticides, plant incorporated

protectants and biological pesticides. They are of low volume and high effect formulations and

require lesser dosages as compared to chemical pesticides. A growth area for bio-pesticides is in

the area of seed treatment and soil amendments. Example of bio-pesticides includes Bacillus

subtilis which is used as soil inoculant in horticulture and agriculture.

Introduction to Agrochemicals

08

5. Others (Nematocides, Rodenticides etc): Fumigants and rodenticides are used to prevent the

attack of pests during storage of crops. Plant growth regulators control or modify the plant growth

process and are most commonly used in cotton, rice and fruits.

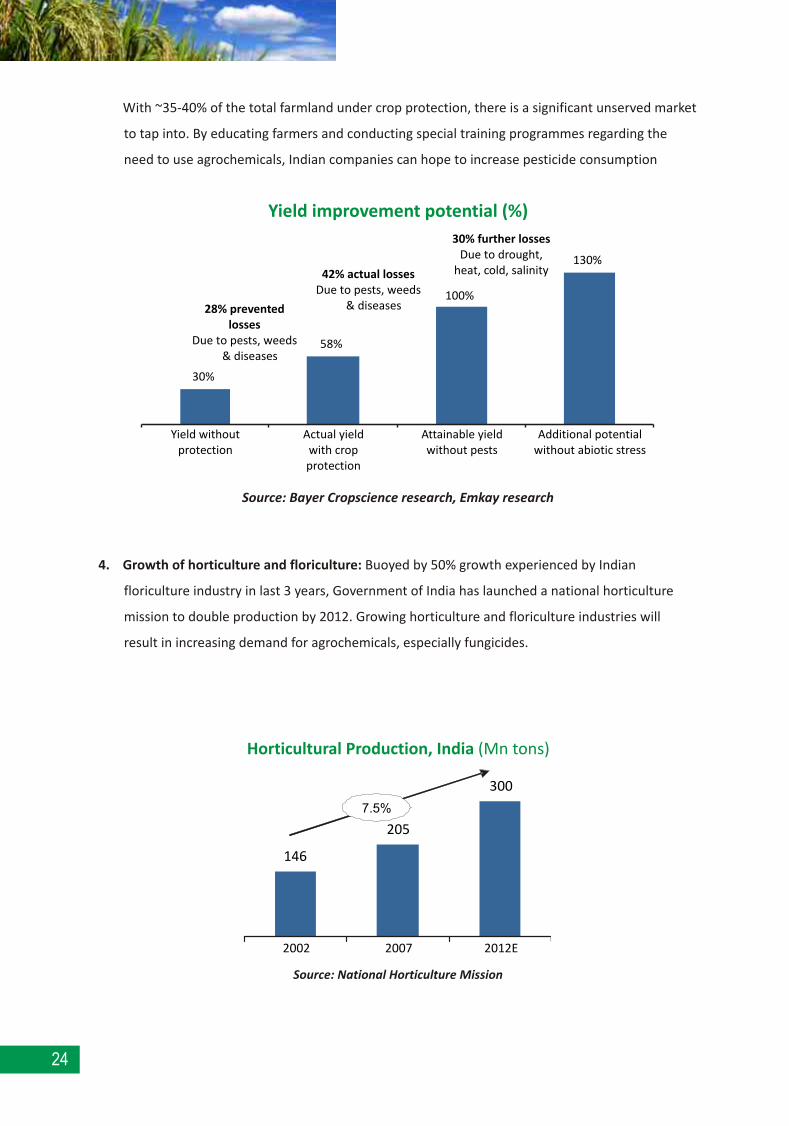

As per Govt. of India, crop losses due to non-usage of pesticides were 28% of the yield amounting to

~ Rs. 90,000 Cr per annum (2002 estimated). It is estimated that the present food grain production

can jump from 3 Trillion to 4 Trillion by using crop protection products.

Therefore, right usage of crop protection chemicals is essential in increasing agricultural production

by preventing crop losses before and after harvesting.

Weeds,33%

Rodents& Others,

15%

Disease26%

s

Insects,26%

Losses caused by different pests (%)

Source: Govt. of India estimates

33

Global market overview

The global crop protection industry has registered a growth of 6% p.a. from 2005 to reach USD 43.2

Bn in 2009. This market is expected to grow further owing to the increasing food and fuel needs and

is expected to grow at 4% p.a. to reach ~USD 54 Bn in 2015.

25.8

33.2

43.2

2001 2005 2009

Global Market size (USD Bn)

Source: Industry reports, Tata Strategic analysis

6%

2.1 Geographical distribution

The crop protection chemicals market is mainly concentrated in the major developed countries such

as United States and Western European nations. Europe has the largest share in the agrochemical

market followed by Asia, Latin America and North America. There is an increased usage of products

in Europe due to high commodity prices and in order to boost yield and quality. Increased demand

for palm oil has led to increasing usage of herbicides in Japan, Malaysia and Indonesia. Strong rice

prices and other food grains are driving the agrochemical consumption in India. In Latin America,

increased production of soybean and sugarcane for animal feed as well as for bio-fuels is the driving

the growth of agrochemical consumption.

Chapter 2

Global market overview

32

5. Others (Nematocides, Rodenticides etc): Fumigants and rodenticides are used to prevent the

attack of pests during storage of crops. Plant growth regulators control or modify the plant growth

process and are most commonly used in cotton, rice and fruits.

As per Govt. of India, crop losses due to non-usage of pesticides were 28% of the yield amounting to

~ Rs. 90,000 Cr per annum (2002 estimated). It is estimated that the present food grain production

can jump from 3 Trillion to 4 Trillion by using crop protection products.

Therefore, right usage of crop protection chemicals is essential in increasing agricultural production

by preventing crop losses before and after harvesting.

Weeds,33%

Rodents& Others,

15%

Disease26%

s

Insects,26%

Losses caused by different pests (%)

Source: Govt. of India estimates

09

Global market overview

The global crop protection industry has registered a growth of 6% p.a. from 2005 to reach USD 43.2

Bn in 2009. This market is expected to grow further owing to the increasing food and fuel needs and

is expected to grow at 4% p.a. to reach ~USD 54 Bn in 2015.

25.8

33.2

43.2

2001 2005 2009

Global Market size (USD Bn)

Source: Industry reports, Tata Strategic analysis

6%

2.1 Geographical distribution

The crop protection chemicals market is mainly concentrated in the major developed countries such

as United States and Western European nations. Europe has the largest share in the agrochemical

market followed by Asia, Latin America and North America. There is an increased usage of products

in Europe due to high commodity prices and in order to boost yield and quality. Increased demand

for palm oil has led to increasing usage of herbicides in Japan, Malaysia and Indonesia. Strong rice

prices and other food grains are driving the agrochemical consumption in India. In Latin America,

increased production of soybean and sugarcane for animal feed as well as for bio-fuels is the driving

the growth of agrochemical consumption.

Chapter 2

Global market overview

10

It is believed that the crop protection chemicals market has reached its saturation in developed

regions such as North America and Western Europe whereas regions such as Asia Pacific, Middle East

and Latin America will offer high growth opportunities in the future.

2.2 Global market scenario

The global crop protection market is fairly consolidated with top nine companies accounting for over

80% of the market. Syngenta, Bayer and BASF are the market leaders in the global crop protection

market.

Asia, 25%

LatinAmerica,

19%

ROW, 4%

NorthAmerica,

23% Europe,29%

Global geographical share, 2009

Source: GOI Task Force on Chemicals

Bayer,17.0%

BASF SE,10.9%

SumitomoChemical,

3.40%

Others,13.1%

Makhteshim-Agan Group,

5.50%

NufarmLimited,

5.9%

Dow, 8.8%

Dupont,5.7%

Monsanto,10.8%

SyngentaAG, 18.9%

Market share by Revenue, 2008 (%)

Source: Industry reports, Tata Strategic analysis

Global crop protection market is characterized by large number of mergers and acquisitions in the

recent years. Several large companies have consolidated their presence in the existing geographies

or ventured into newer areas through acquisitions of local companies. Some of the recent

acquisitions include Arysta LifeScience's acquisition of Volcano Agroscience Limited in 2005,

Nufarm's acquisition of Agripec (Brazil) in 2007. In 2010, Cheminova acquired insecticide business

from Isagro (Italy) to strengthen its presence in emerging markets of India and Italy.

Source: Industry articles, Tata Strategic analysis

Some recent acquisitions

2010

2009

2007

2006

2005

2005

Cheminova acquired the insecticide business business of Isagro to

as India

IsagroCheminova

Bayer CropScience acquired a biotechnology company, Athenix

Corp. The deal helped Bayer to Strengthen its R&D presence in

North America

Athenix Corp.Bayer

CropScience

Nufarm acquired 49.9% in Agripec in 2004. It acquired the remaining

50.1% to develop its business in South AmericaAgripec (Brazil)Nufarm Limitd

Nufarm Limited acquired crop protection business business of Agrisol

SRL to strengthen its presence in Italy

Arysta acquired 50% stake in Callietha Investments, including

Volcano Agroscience to increase its presence in South Africa. It later

acuired the remaining 50% in 2008

Makhteshim Agan acquired 70% of Biomark Trading House Ltd.

Acquisition enabled increased service & activity for Makhteshim-

Agan in Hungarian market

Highlights

Agrosol SRLNufarm Limited

Volcano

Agroscience

Arysta

Lifescience

Corporation

Biomark IncMakhteshim -

Agan Group

strengthen its presence in Italy & gain access to new markets such

Highlights

-

Year Target CompanyAcquirer

2.2.1 Distribution of global crop protection market - Product category

Herbicides are the most widely used agrochemical products globally, followed by insecticides and

fungicides. Fungicides is the highest growing segments as it helps increasing yield, improving quality

and in seed treatment. Individual sales of various categories however depend on climatic conditions

and crop variance.

35

34

It is believed that the crop protection chemicals market has reached its saturation in developed

regions such as North America and Western Europe whereas regions such as Asia Pacific, Middle East

and Latin America will offer high growth opportunities in the future.

2.2 Global market scenario

The global crop protection market is fairly consolidated with top nine companies accounting for over

80% of the market. Syngenta, Bayer and BASF are the market leaders in the global crop protection

market.

Asia, 25%

LatinAmerica,

19%

ROW, 4%

NorthAmerica,

23% Europe,29%

Global geographical share, 2009

Source: GOI Task Force on Chemicals

Bayer,17.0%

BASF SE,10.9%

SumitomoChemical,

3.40%

Others,13.1%

Makhteshim-Agan Group,

5.50%

NufarmLimited,

5.9%

Dow, 8.8%

Dupont,5.7%

Monsanto,10.8%

SyngentaAG, 18.9%

Market share by Revenue, 2008 (%)

Source: Industry reports, Tata Strategic analysis

Global crop protection market is characterized by large number of mergers and acquisitions in the

recent years. Several large companies have consolidated their presence in the existing geographies

or ventured into newer areas through acquisitions of local companies. Some of the recent

acquisitions include Arysta LifeScience's acquisition of Volcano Agroscience Limited in 2005,

Nufarm's acquisition of Agripec (Brazil) in 2007. In 2010, Cheminova acquired insecticide business

from Isagro (Italy) to strengthen its presence in emerging markets of India and Italy.

Source: Industry articles, Tata Strategic analysis

Some recent acquisitions

2010

2009

2007

2006

2005

2005

Cheminova acquired the insecticide business business of Isagro to

as India

IsagroCheminova

Bayer CropScience acquired a biotechnology company, Athenix

Corp. The deal helped Bayer to Strengthen its R&D presence in

North America

Athenix Corp.Bayer

CropScience

Nufarm acquired 49.9% in Agripec in 2004. It acquired the remaining

50.1% to develop its business in South AmericaAgripec (Brazil)Nufarm Limitd

Nufarm Limited acquired crop protection business business of Agrisol

SRL to strengthen its presence in Italy

Arysta acquired 50% stake in Callietha Investments, including

Volcano Agroscience to increase its presence in South Africa. It later

acuired the remaining 50% in 2008

Makhteshim Agan acquired 70% of Biomark Trading House Ltd.

Acquisition enabled increased service & activity for Makhteshim-

Agan in Hungarian market

Highlights

Agrosol SRLNufarm Limited

Volcano

Agroscience

Arysta

Lifescience

Corporation

Biomark IncMakhteshim -

Agan Group

strengthen its presence in Italy & gain access to new markets such

Highlights

-

Year Target CompanyAcquirer

2.2.1 Distribution of global crop protection market - Product category

Herbicides are the most widely used agrochemical products globally, followed by insecticides and

fungicides. Fungicides is the highest growing segments as it helps increasing yield, improving quality

and in seed treatment. Individual sales of various categories however depend on climatic conditions

and crop variance.

11

12

Herbicides are used in most of the regions of the world. However, major markets for herbicides are

North America and Europe due to the favorable climatic conditions in these regions. Insecticides are

more prevalent in Asian countries. This is due to higher growth of cotton, cereal, fruits and

vegetables in these regions which have higher incidence of insect attacks. Increased usage of

genetically modified crops in North America has reduced the usage of insecticides. Fungicides are

used in almost all agriculture markets of the world due to favorable climatic conditions for the fungal

growth.

Fungicides26%

Insecticides26%

Others, 3%

Herbicides45%

Market distribution by product category, 2009 (%)

Source: Phillips McDougall

Product category Top molecules - Global

Herbicides Glyphosate, Triazines, Sulphonyl urea

Insecticides Pyrethroids, Organophosphates, Neonicotenoids

Fungicides Triazoles, Strobillurin, Dithiocarbamates

2.2.2 Distribution of global crop protection market - Crop-wise

Globally, fruits and vegetables and cereals account for the largest share of the crop protection

industry.

37

2.3 Global Trade of crop protection products

India, China, France, Germany and US are the largest exporters of crop protection products while

Brazil, Canada, Poland, Russia and Mexico are the major importers.

Cereals,18.10%

Rice,8.70%

Cotton,5.40%

Others18.30%

Maize,13.20%

Soybean,10.10%

Fruits &vegetables

26.20%

Source: Phillips McDougall

Market distribution by crops, 2008 (%)

Leading agrochemicals exporting countries by sector, 2009 ($ Mn)

Insecticides Fungicides Herbicides

USA 609 Germany 951 USA 1165

France 545 France 917 France 1096

India 500 UK 578 Germany 1092

China 438 Spain 460 Belgium 943

Germany 423 Switzerland 341 China 758

Source: Phillips McDougall

2.4 Global Industry Challenges

1. Market saturation: The crop protection market is believed to have reached a saturation point in

most of the developed regions such as North America and Western Europe. Hence, there is

limited scope for growth in these markets.

36

Herbicides are used in most of the regions of the world. However, major markets for herbicides are

North America and Europe due to the favorable climatic conditions in these regions. Insecticides are

more prevalent in Asian countries. This is due to higher growth of cotton, cereal, fruits and

vegetables in these regions which have higher incidence of insect attacks. Increased usage of

genetically modified crops in North America has reduced the usage of insecticides. Fungicides are

used in almost all agriculture markets of the world due to favorable climatic conditions for the fungal

growth.

Fungicides26%

Insecticides26%

Others, 3%

Herbicides45%

Market distribution by product category, 2009 (%)

Source: Phillips McDougall

Product category Top molecules - Global

Herbicides Glyphosate, Triazines, Sulphonyl urea

Insecticides Pyrethroids, Organophosphates, Neonicotenoids

Fungicides Triazoles, Strobillurin, Dithiocarbamates

2.2.2 Distribution of global crop protection market - Crop-wise

Globally, fruits and vegetables and cereals account for the largest share of the crop protection

industry.

13

2.3 Global Trade of crop protection products

India, China, France, Germany and US are the largest exporters of crop protection products while

Brazil, Canada, Poland, Russia and Mexico are the major importers.

Cereals,18.10%

Rice,8.70%

Cotton,5.40%

Others18.30%

Maize,13.20%

Soybean,10.10%

Fruits &vegetables

26.20%

Source: Phillips McDougall

Market distribution by crops, 2008 (%)

Leading agrochemicals exporting countries by sector, 2009 ($ Mn)

Insecticides Fungicides Herbicides

USA 609 Germany 951 USA 1165

France 545 France 917 France 1096

India 500 UK 578 Germany 1092

China 438 Spain 460 Belgium 943

Germany 423 Switzerland 341 China 758

Source: Phillips McDougall

2.4 Global Industry Challenges

1. Market saturation: The crop protection market is believed to have reached a saturation point in

most of the developed regions such as North America and Western Europe. Hence, there is

limited scope for growth in these markets.

14

2. Evolution of biotechnology: Development of genetically modified crops in recent years,

especially for pest resistance would result in relatively lesser need for traditional crop protection

chemicals. However, this could lead to newer strains or pests driving need for other

agrochemicals. E.g. new sucking pests have emerged causing significant harm to the BT cotton.

3. Stringent regulations: Stringent environmental regulations across all countries increase the cost

of developing new products. These regulations are primarily affecting the older products while

at the same time resulting in delay in introduction of new products.

4. Mergers and Acquisitions effecting SMEs: Larger companies are acquiring/ entering into

strategic alliances with smaller companies to increase their market reach. This poses a threat to

local companies who are forced to reduce prices in order to compete, thereby leading to lower

margins.

5. Alternate methods for crop protection: Alternate methods such as natural products are being

increasingly used which would affect the chemicals market. For example, more and more

biological pesticides are being introduced.

12.4

14.514.1

16.7

2010E 2015E

North America Europe

3.2%

3.4%

CAGR

Crop Protection Market forecast (USD Bn)

Source: Industry reports, Tata Strategic analysis

39

Indian market overview

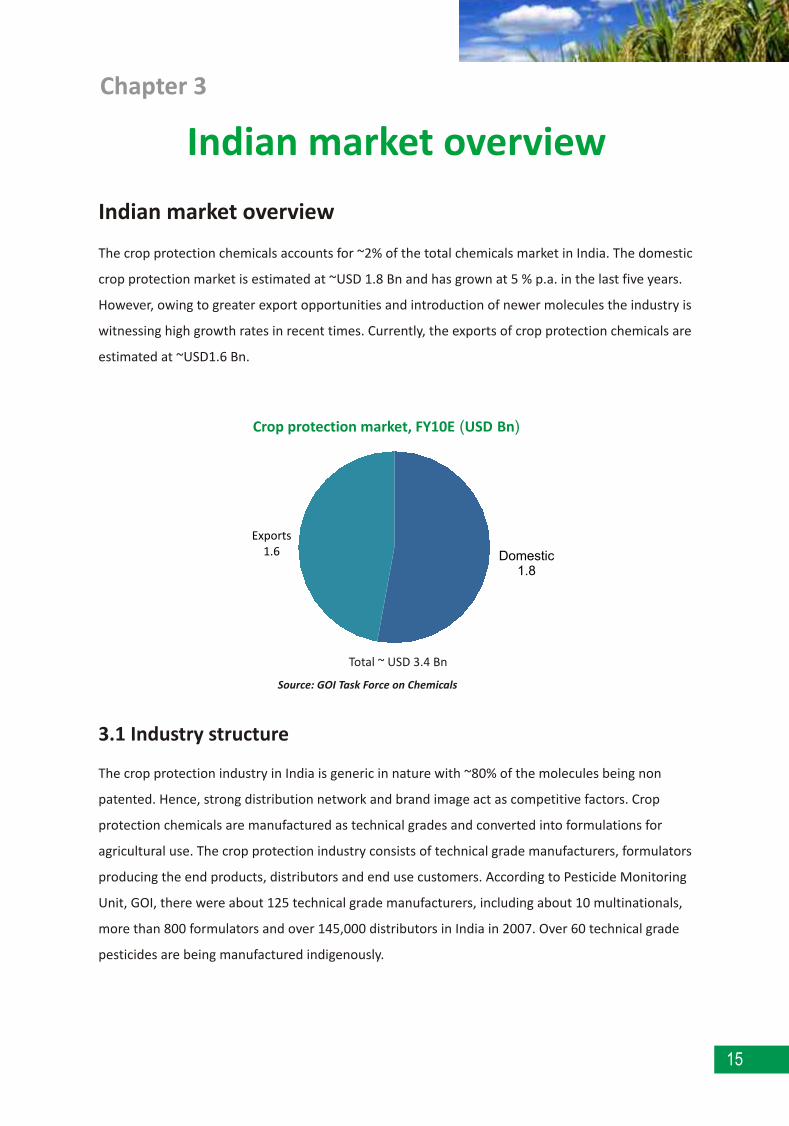

The crop protection chemicals accounts for ~2% of the total chemicals market in India. The domestic

crop protection market is estimated at ~USD 1.8 Bn and has grown at 5 % p.a. in the last five years.

However, owing to greater export opportunities and introduction of newer molecules the industry is

witnessing high growth rates in recent times. Currently, the exports of crop protection chemicals are

estimated at ~USD1.6 Bn.

3.1 Industry structure

The crop protection industry in India is generic in nature with ~80% of the molecules being non

patented. Hence, strong distribution network and brand image act as competitive factors. Crop

protection chemicals are manufactured as technical grades and converted into formulations for

agricultural use. The crop protection industry consists of technical grade manufacturers, formulators

producing the end products, distributors and end use customers. According to Pesticide Monitoring

Unit, GOI, there were about 125 technical grade manufacturers, including about 10 multinationals,

more than 800 formulators and over 145,000 distributors in India in 2007. Over 60 technical grade

pesticides are being manufactured indigenously.

Exports1.6 Domestic

1.8

Source: GOI Task Force on Chemicals

Crop protection market, FY10E (USD Bn)

Total ~ USD 3.4 Bn

Chapter 3

Indian market overview

38

2. Evolution of biotechnology: Development of genetically modified crops in recent years,

especially for pest resistance would result in relatively lesser need for traditional crop protection

chemicals. However, this could lead to newer strains or pests driving need for other

agrochemicals. E.g. new sucking pests have emerged causing significant harm to the BT cotton.

3. Stringent regulations: Stringent environmental regulations across all countries increase the cost

of developing new products. These regulations are primarily affecting the older products while

at the same time resulting in delay in introduction of new products.

4. Mergers and Acquisitions effecting SMEs: Larger companies are acquiring/ entering into

strategic alliances with smaller companies to increase their market reach. This poses a threat to

local companies who are forced to reduce prices in order to compete, thereby leading to lower

margins.

5. Alternate methods for crop protection: Alternate methods such as natural products are being

increasingly used which would affect the chemicals market. For example, more and more

biological pesticides are being introduced.

12.4

14.514.1

16.7

2010E 2015E

North America Europe

3.2%

3.4%

CAGR

Crop Protection Market forecast (USD Bn)

Source: Industry reports, Tata Strategic analysis

15

Indian market overview

The crop protection chemicals accounts for ~2% of the total chemicals market in India. The domestic

crop protection market is estimated at ~USD 1.8 Bn and has grown at 5 % p.a. in the last five years.

However, owing to greater export opportunities and introduction of newer molecules the industry is

witnessing high growth rates in recent times. Currently, the exports of crop protection chemicals are

estimated at ~USD1.6 Bn.

3.1 Industry structure

The crop protection industry in India is generic in nature with ~80% of the molecules being non

patented. Hence, strong distribution network and brand image act as competitive factors. Crop

protection chemicals are manufactured as technical grades and converted into formulations for

agricultural use. The crop protection industry consists of technical grade manufacturers, formulators

producing the end products, distributors and end use customers. According to Pesticide Monitoring

Unit, GOI, there were about 125 technical grade manufacturers, including about 10 multinationals,

more than 800 formulators and over 145,000 distributors in India in 2007. Over 60 technical grade

pesticides are being manufactured indigenously.

Exports1.6 Domestic

1.8

Source: GOI Task Force on Chemicals

Crop protection market, FY10E (USD Bn)

Total ~ USD 3.4 Bn

Chapter 3

Indian market overview

16

17

1312

7 7

5 5

0.6

Taiwan China Japan USA Korea France UK India

Per capita consumption: Fy09 (kg/ ha)

Source: Industry Report, Tata Strategic Estimates

Technical grade manufacturers sell high purity chemicals in bulk (generally in drums of 200-250 kgs.)

to formulators. Formulators, in turn, prepare formulations by adding inert carriers, solvents, surface

active agents, deodorants etc. These formulations are packed for retail sale and bought by the

farmers.

3.2 Indian market scenario

India due to its inherent strength of low-cost manufacturing and qualified low-cost manpower is a

net exporter of pesticides to countries such as USA and some European and African countries.

Exports formed ~47% of total industry turnover in Fy10.

The industry suffers from high inventory (owing to seasonal and irregular demand on account of

monsoons) and long credit periods to farmers, thus making operations 'working capital' intensive.

3.2.1 Domestic consumption

Consumption of crop protection products in India is among the lowest in the world. Per capita

consumption of crop protection products in India is 0.6 kg/ ha compared to 13 kg/ ha in China and 7

kg/ ha in USA. Some of the reasons for low consumption in India are low purchasing power of

farmers, lack of awareness among farmers, limited reach and lower accessibility of products. This

presents an immense opportunity for the crop protection industry to grow in India

Technical grademanufacturers

Formulators Distributors End usecustomers

41

3.2.2 Distribution of domestic crop protection market - Product category

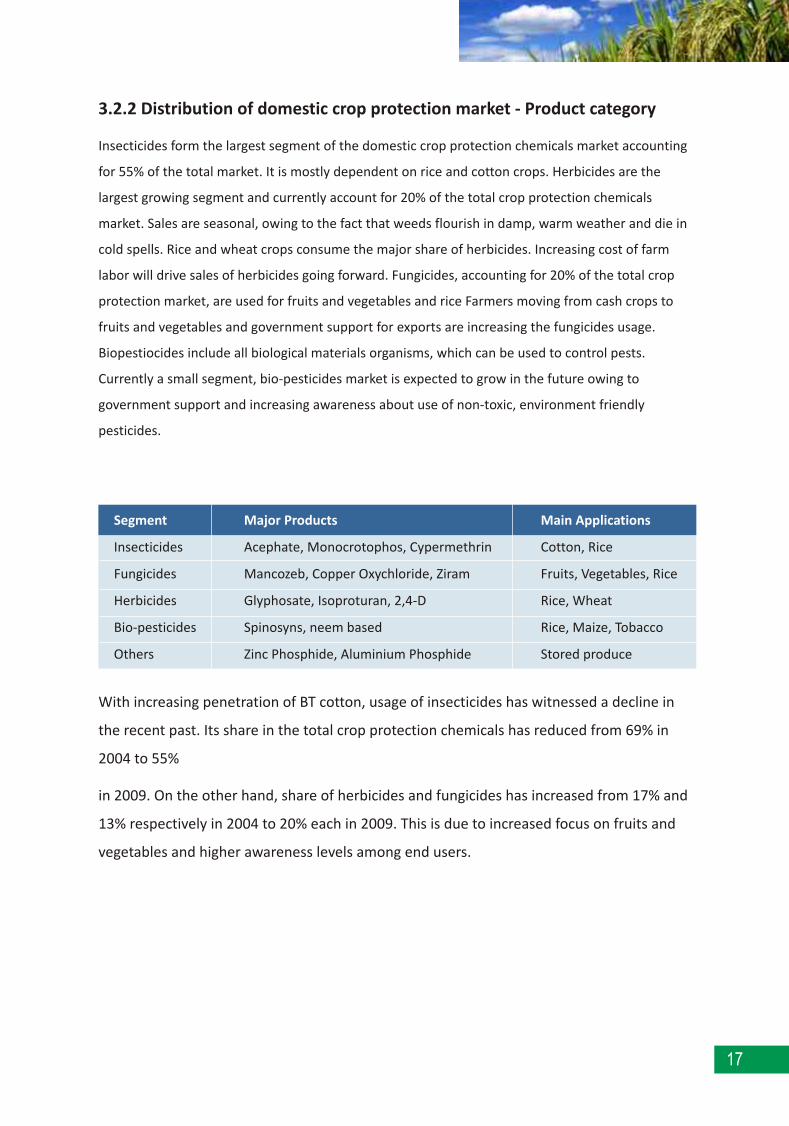

Insecticides form the largest segment of the domestic crop protection chemicals market accounting

for 55% of the total market. It is mostly dependent on rice and cotton crops. Herbicides are the

largest growing segment and currently account for 20% of the total crop protection chemicals

market. Sales are seasonal, owing to the fact that weeds flourish in damp, warm weather and die in

cold spells. Rice and wheat crops consume the major share of herbicides. Increasing cost of farm

labor will drive sales of herbicides going forward. Fungicides, accounting for 20% of the total crop

protection market, are used for fruits and vegetables and rice Farmers moving from cash crops to

fruits and vegetables and government support for exports are increasing the fungicides usage.

Biopestiocides include all biological materials organisms, which can be used to control pests.

Currently a small segment, bio-pesticides market is expected to grow in the future owing to

government support and increasing awareness about use of non-toxic, environment friendly

pesticides.

Segment Major Products Main Applications

Insecticides Acephate, Monocrotophos, Cypermethrin Cotton, Rice

Fungicides Mancozeb, Copper Oxychloride, Ziram Fruits, Vegetables, Rice

Herbicides Glyphosate, Isoproturan, 2,4-D Rice, Wheat

Bio-pesticides Spinosyns, neem based Rice, Maize, Tobacco

Others Zinc Phosphide, Aluminium Phosphide Stored produce

With increasing penetration of BT cotton, usage of insecticides has witnessed a decline in

the recent past. Its share in the total crop protection chemicals has reduced from 69% in

2004 to 55%

in 2009. On the other hand, share of herbicides and fungicides has increased from 17% and

13% respectively in 2004 to 20% each in 2009. This is due to increased focus on fruits and

vegetables and higher awareness levels among end users.

40

17

1312

7 7

5 5

0.6

Taiwan China Japan USA Korea France UK India

Per capita consumption: Fy09 (kg/ ha)

Source: Industry Report, Tata Strategic Estimates

Technical grade manufacturers sell high purity chemicals in bulk (generally in drums of 200-250 kgs.)

to formulators. Formulators, in turn, prepare formulations by adding inert carriers, solvents, surface

active agents, deodorants etc. These formulations are packed for retail sale and bought by the

farmers.

3.2 Indian market scenario

India due to its inherent strength of low-cost manufacturing and qualified low-cost manpower is a

net exporter of pesticides to countries such as USA and some European and African countries.

Exports formed ~47% of total industry turnover in Fy10.

The industry suffers from high inventory (owing to seasonal and irregular demand on account of

monsoons) and long credit periods to farmers, thus making operations 'working capital' intensive.

3.2.1 Domestic consumption

Consumption of crop protection products in India is among the lowest in the world. Per capita

consumption of crop protection products in India is 0.6 kg/ ha compared to 13 kg/ ha in China and 7

kg/ ha in USA. Some of the reasons for low consumption in India are low purchasing power of

farmers, lack of awareness among farmers, limited reach and lower accessibility of products. This

presents an immense opportunity for the crop protection industry to grow in India

Technical grademanufacturers

Formulators Distributors End usecustomers

17

3.2.2 Distribution of domestic crop protection market - Product category

Insecticides form the largest segment of the domestic crop protection chemicals market accounting

for 55% of the total market. It is mostly dependent on rice and cotton crops. Herbicides are the

largest growing segment and currently account for 20% of the total crop protection chemicals

market. Sales are seasonal, owing to the fact that weeds flourish in damp, warm weather and die in

cold spells. Rice and wheat crops consume the major share of herbicides. Increasing cost of farm

labor will drive sales of herbicides going forward. Fungicides, accounting for 20% of the total crop

protection market, are used for fruits and vegetables and rice Farmers moving from cash crops to

fruits and vegetables and government support for exports are increasing the fungicides usage.

Biopestiocides include all biological materials organisms, which can be used to control pests.

Currently a small segment, bio-pesticides market is expected to grow in the future owing to

government support and increasing awareness about use of non-toxic, environment friendly

pesticides.

Segment Major Products Main Applications

Insecticides Acephate, Monocrotophos, Cypermethrin Cotton, Rice

Fungicides Mancozeb, Copper Oxychloride, Ziram Fruits, Vegetables, Rice

Herbicides Glyphosate, Isoproturan, 2,4-D Rice, Wheat

Bio-pesticides Spinosyns, neem based Rice, Maize, Tobacco

Others Zinc Phosphide, Aluminium Phosphide Stored produce

With increasing penetration of BT cotton, usage of insecticides has witnessed a decline in

the recent past. Its share in the total crop protection chemicals has reduced from 69% in

2004 to 55%

in 2009. On the other hand, share of herbicides and fungicides has increased from 17% and

13% respectively in 2004 to 20% each in 2009. This is due to increased focus on fruits and

vegetables and higher awareness levels among end users.

18

3.2.3 Distribution of domestic crop protection market - Crop-wise

Paddy and cotton are the major consumers of crop protection chemicals accounting for 28% and

20% respectively of the total domestic crop protection chemicals market. Fruits and vegetables also

account for a significant share of the crop protection chemicals market.

Herbicides17%

Fungicides13%

Biopestici & Others, 1%

des

Insecticides69%

Source: Industry reports, Tata Strategic analysis Source: Industry reports, Tata Strategic analysis

Market distribution by product

category FY04 (% of total)

Market distribution by product

category FY09 (% )of total

Biopestici & Others, 5%

des

Fungicides20%

Herbicides20%

Insecticides55%

Cotton20%

Wheat6%

Pulses5%

Oilseeds5%

Others,16%

Vegetables14%

Fruits6%

Paddy28%

Crop wise pesticides consumption, FY09 (% of total)

Source: Industry reports, Tata Strategic analysis

43

In recent years, consumption of insecticides has decreased due to the introduction of BT cotton,

which has lower risk of pest attacks. As a result, pesticides usage on cotton as % of total has

decreased from 33% in 2005 to 20% in 2009. On the contrary, pesticides usage in paddy has been

increasing mostly due to increased popularity of hybrid varieties of rice, which require higher

amount of pesticides. Share of paddy in the total crop protection chemicals has increased from 24%

in 2005 to 28% in 2009. Consumption of pesticides by fruits and vegetables has been relatively stable

in the recent years.

3.2.4 Distribution of crop protection Market - State-wise

The top three states Andhra Pradesh, Maharashtra and Punjab account for ~50% of the total

pesticide consumption in India. Andhra Pradesh is the largest consumer of pesticides with a share of

24%.

33

2421

8 86

16

20

28

20

6

10

Cotton Paddy Fruits &vegetables

Wheat Pulses &oilseeds

Others

2005 2009

Crop wise pesticides consumption (% of total)

Source: Industry reports, Tata Strategic analysis

Maharashtra13%

Others23%

WestBengal

5%

Punjab11%

MP &Chattisgarh

8% Gujarat7%

Tamil Nadu5%

Haryana5%

Karnataka7%

AP24%

State-wise pesticides consumption Fy09 (% of total value)

Source: Industry reports, Tata Strategic analysis

42

3.2.3 Distribution of domestic crop protection market - Crop-wise

Paddy and cotton are the major consumers of crop protection chemicals accounting for 28% and

20% respectively of the total domestic crop protection chemicals market. Fruits and vegetables also

account for a significant share of the crop protection chemicals market.

Herbicides17%

Fungicides13%

Biopestici & Others, 1%

des

Insecticides69%

Source: Industry reports, Tata Strategic analysis Source: Industry reports, Tata Strategic analysis

Market distribution by product

category FY04 (% of total)

Market distribution by product

category FY09 (% )of total

Biopestici & Others, 5%

des

Fungicides20%

Herbicides20%

Insecticides55%

Cotton20%

Wheat6%

Pulses5%

Oilseeds5%

Others,16%

Vegetables14%

Fruits6%

Paddy28%

Crop wise pesticides consumption, FY09 (% of total)

Source: Industry reports, Tata Strategic analysis

19

In recent years, consumption of insecticides has decreased due to the introduction of BT cotton,

which has lower risk of pest attacks. As a result, pesticides usage on cotton as % of total has

decreased from 33% in 2005 to 20% in 2009. On the contrary, pesticides usage in paddy has been

increasing mostly due to increased popularity of hybrid varieties of rice, which require higher

amount of pesticides. Share of paddy in the total crop protection chemicals has increased from 24%

in 2005 to 28% in 2009. Consumption of pesticides by fruits and vegetables has been relatively stable

in the recent years.

3.2.4 Distribution of crop protection Market - State-wise

The top three states Andhra Pradesh, Maharashtra and Punjab account for ~50% of the total

pesticide consumption in India. Andhra Pradesh is the largest consumer of pesticides with a share of

24%.

33

2421

8 86

16

20

28

20

6

10

Cotton Paddy Fruits &vegetables

Wheat Pulses &oilseeds

Others

2005 2009

Crop wise pesticides consumption (% of total)

Source: Industry reports, Tata Strategic analysis

Maharashtra13%

Others23%

WestBengal

5%

Punjab11%

MP &Chattisgarh

8% Gujarat7%

Tamil Nadu5%

Haryana5%

Karnataka7%

AP24%

State-wise pesticides consumption Fy09 (% of total value)

Source: Industry reports, Tata Strategic analysis

20

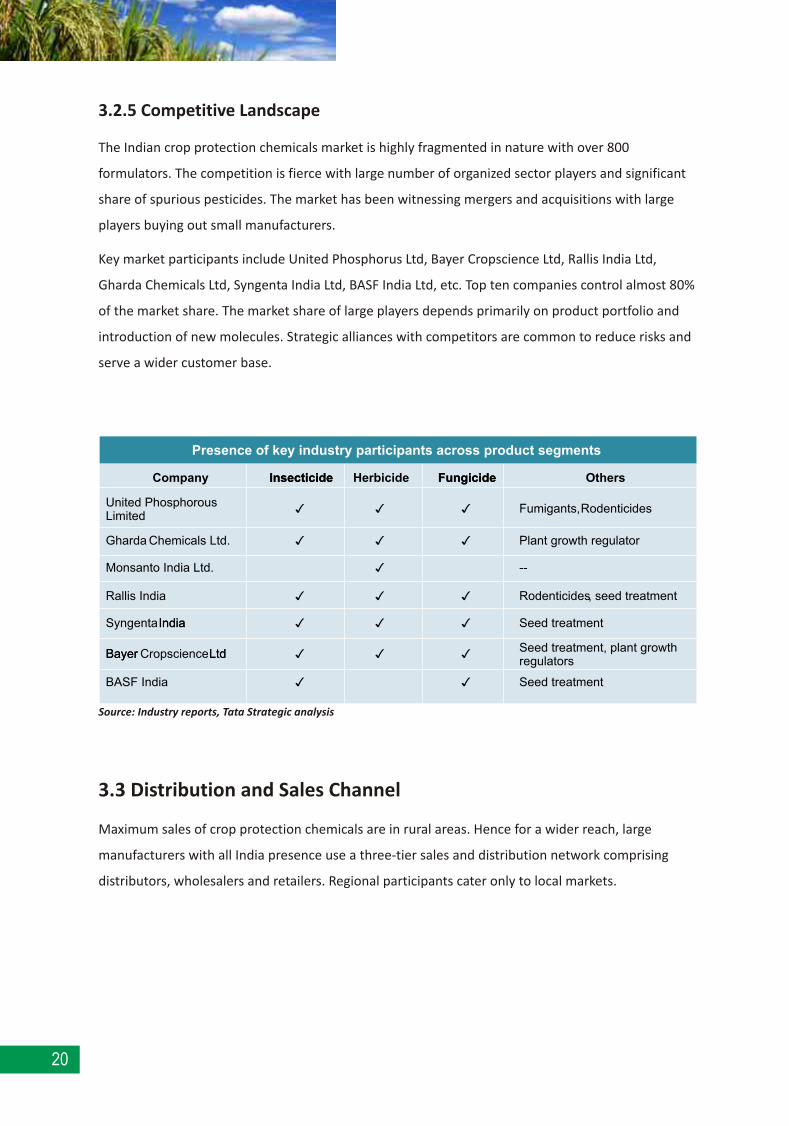

3.2.5 Competitive Landscape

The Indian crop protection chemicals market is highly fragmented in nature with over 800

formulators. The competition is fierce with large number of organized sector players and significant

share of spurious pesticides. The market has been witnessing mergers and acquisitions with large

players buying out small manufacturers.

Key market participants include United Phosphorus Ltd, Bayer Cropscience Ltd, Rallis India Ltd,

Gharda Chemicals Ltd, Syngenta India Ltd, BASF India Ltd, etc. Top ten companies control almost 80%

of the market share. The market share of large players depends primarily on product portfolio and

introduction of new molecules. Strategic alliances with competitors are common to reduce risks and

serve a wider customer base.

3.3 Distribution and Sales Channel

Maximum sales of crop protection chemicals are in rural areas. Hence for a wider reach, large

manufacturers with all India presence use a three-tier sales and distribution network comprising

distributors, wholesalers and retailers. Regional participants cater only to local markets.

Presence of key industry participants across product segments

3

3

3

3

3

3

Seed treatment

Seed treatment, plant growth regulators

Seed treatment

Rodenticides, seed treatment

--

Plant growth regulator

Fumigants, Rodenticides

Others

3BASF India

33Bayer CropscienceLtd

33SyngentaIndia

33Rallis India

3

3

3

Monsanto India Ltd.

3Gharda Chemicals Ltd.

3United Phosphorous Limited

Bayer Ltd

India

FungicideHerbicideInsecticideCompany FungicideInsecticide

Presence of key industry participants across product segments

Source: Industry reports, Tata Strategic analysis

45

Typically, a company with all India presence could have 400-1000 distributors catering to 25,000-

30,000 retailers. Companies keep their stocks in warehouses or depots from where it is supplied to

distributors. Multinationals, at times, enter into co-marketing and co-distribution arrangements with

Indian companies. For example, Syngenta entered into an agreement with Rallis for marketing of its

products in India. Mid size and small scale companies operate through direct marketing of their

products. Most companies also engage in extension services or field demonstrations to increase

farmer awareness and promote their products.

3.4 Import/ Exports

Indian exports of pesticides have been witnessing a strong growth in recent times. This is primarily

due to its competence in low-cost manufacturing and technically trained manpower. Seasonal

domestic demand, domestic overcapacity and better price realization in the overseas market have

also led to this trend. India has emerged as the thirteenth largest exporter of pesticides in the world.

However, most of the exports are off-patent products.

Currently, the total export value of crop protection chemicals amount to USD 1.6 Bn. America, Asia

(excluding Middle East) and Europe are the major exporting destinations. Key market drivers for

Indian crop protection market export are:

1. Excess capacity: India's production capacity is 146,000 MT against the production of 85,000 MT.

This excess capacity against domestic demand is a key growth driver for exports.

2. Low processing cost: Availability of cheap labor and low processing costs has made India a

manufacturing hub with several multinationals setting up their manufacturing facilities in India.

Technical Grade manufacturers In-house formulators

Formulators

Distributors

Retailers

Retailers/ Dealers Distributors

Retailers

End users

Crop protection distribution network

Source: Tata Strategic analysis

44

3.2.5 Competitive Landscape

The Indian crop protection chemicals market is highly fragmented in nature with over 800

formulators. The competition is fierce with large number of organized sector players and significant

share of spurious pesticides. The market has been witnessing mergers and acquisitions with large

players buying out small manufacturers.

Key market participants include United Phosphorus Ltd, Bayer Cropscience Ltd, Rallis India Ltd,

Gharda Chemicals Ltd, Syngenta India Ltd, BASF India Ltd, etc. Top ten companies control almost 80%

of the market share. The market share of large players depends primarily on product portfolio and

introduction of new molecules. Strategic alliances with competitors are common to reduce risks and

serve a wider customer base.

3.3 Distribution and Sales Channel

Maximum sales of crop protection chemicals are in rural areas. Hence for a wider reach, large

manufacturers with all India presence use a three-tier sales and distribution network comprising

distributors, wholesalers and retailers. Regional participants cater only to local markets.

Presence of key industry participants across product segments

3

3

3

3

3

3

Seed treatment

Seed treatment, plant growth regulators

Seed treatment

Rodenticides, seed treatment

--

Plant growth regulator

Fumigants, Rodenticides

Others

3BASF India

33Bayer CropscienceLtd

33SyngentaIndia

33Rallis India

3

3

3

Monsanto India Ltd.

3Gharda Chemicals Ltd.

3United Phosphorous Limited

Bayer Ltd

India

FungicideHerbicideInsecticideCompany FungicideInsecticide

Presence of key industry participants across product segments

Source: Industry reports, Tata Strategic analysis

21

Typically, a company with all India presence could have 400-1000 distributors catering to 25,000-

30,000 retailers. Companies keep their stocks in warehouses or depots from where it is supplied to

distributors. Multinationals, at times, enter into co-marketing and co-distribution arrangements with

Indian companies. For example, Syngenta entered into an agreement with Rallis for marketing of its

products in India. Mid size and small scale companies operate through direct marketing of their

products. Most companies also engage in extension services or field demonstrations to increase

farmer awareness and promote their products.

3.4 Import/ Exports

Indian exports of pesticides have been witnessing a strong growth in recent times. This is primarily

due to its competence in low-cost manufacturing and technically trained manpower. Seasonal

domestic demand, domestic overcapacity and better price realization in the overseas market have

also led to this trend. India has emerged as the thirteenth largest exporter of pesticides in the world.

However, most of the exports are off-patent products.

Currently, the total export value of crop protection chemicals amount to USD 1.6 Bn. America, Asia

(excluding Middle East) and Europe are the major exporting destinations. Key market drivers for

Indian crop protection market export are:

1. Excess capacity: India's production capacity is 146,000 MT against the production of 85,000 MT.

This excess capacity against domestic demand is a key growth driver for exports.

2. Low processing cost: Availability of cheap labor and low processing costs has made India a

manufacturing hub with several multinationals setting up their manufacturing facilities in India.

Technical Grade manufacturers In-house formulators

Formulators

Distributors

Retailers

Retailers/ Dealers Distributors

Retailers

End users

Crop protection distribution network

Source: Tata Strategic analysis

22

3. Availability of process technologies: India has a very strong presence in generic pesticide

manufacturing and has process technologies for more than 60 generic molecules.

However, complex registration procedures and decreasing market size for generic molecules in

United States and Europe pose a major challenge for the Indian crop protection chemicals export

3.5 Future Outlook

Since the Indian agricultural sector is highly dependent on monsoons, the market for agrochemicals

is expected to grow at a conservative growth rate of 8% p.a. to reach ~ USD 3.5 Bn by FY20. Exports

are expected to grow at a higher rate of 15% p.a. to reach ~ USD 7.3 Bn. by FY20.

1.8

3.5

2010 2020

8%

CAGR

Future growth Scenario - Domestic (USD Bn)

Source: GOI Task Force on Chemicals

47

Key growth drivers include:

1. Increasing demand for food grains: India has 16% of the world's population and less than 2% of

the total landmass. Increasing population and high emphasis on achieving food grain self-

sufficiency as highlighted in the FY10 budget, is expected to drive growth.

2. Limited farmland availability: India has ~190 Mn hectares of gross cultivated area and the scope

for bringing new areas under cultivation is severely limited. Available arable land per capita has

been reducing globally and is expected to reduce further. The pressure is therefore to increase

yield per hectare which can be achieved through increased usage of agrochemicals.

3. Low Productivity: India has low crop productivity as compared to other countries. Average

productivity in India stands at 2 MT/ha as compared to 6 MT/ha in USA and world average of 3

MT/ha. At the same time, India's pesticide consumption is also low at 0.60 kg/ha as compared to

the world average of 3 kg/ha. Hence, increased usage of pesticides could help the farmers to

improve crop productivity.

0.15

0.27

1998 2015E

World - Available arable land per capita (Ha)

Source: Yara Fertilizer Handbook, PotashCorp

7

13

0.6

3

65

23

USA China India World

Agrochemical usage (kg/ha) Productivity (MT/ha)

Average crop productivity and crop protection chemicals usage

Source: Industry reports, Tata Strategic analysis

46

3. Availability of process technologies: India has a very strong presence in generic pesticide

manufacturing and has process technologies for more than 60 generic molecules.

However, complex registration procedures and decreasing market size for generic molecules in

United States and Europe pose a major challenge for the Indian crop protection chemicals export

3.5 Future Outlook

Since the Indian agricultural sector is highly dependent on monsoons, the market for agrochemicals

is expected to grow at a conservative growth rate of 8% p.a. to reach ~ USD 3.5 Bn by FY20. Exports

are expected to grow at a higher rate of 15% p.a. to reach ~ USD 7.3 Bn. by FY20.

1.8

3.5

2010 2020

8%

CAGR

Future growth Scenario - Domestic (USD Bn)