organizational structures -- how can finance ministry

TRANSCRIPT

Organizational structures -- how can finance ministry respond to new

challenges?

“CASE OF MALAYSIA”

FINANCE MINISTRIES IN THE 21ST CENTURY: Challenges, Institutions and Capabilities 25-26 March 2015, Johannesburg, South Africa

1

MOHD SAKERI ABDUL KADIR National Budget Office

Ministry of Finance, Malaysia

2

Traditional

PPBS

MBS

OBB

Detailed

Controls &

Discipline

Programs &

Performance

Accountability,

flexibility &

delegation

1957 - 1968

1969 - 1990

1990 - 2012

• Incremental

line item

budgeting

• Disaggregated

Budget

• Budget

Ceilings

• Program

Agreements

• Exceptions

Reporting

• Evaluation

• Program

Performance

• Program-

Activities

• Performance

Indicators

• Evaluation

Intro: Malaysia’s Budgetary Reform Initiatives

3

Need to shift focus from outputs to outcomes

Lack of vertical and horizontal integration

Cross cutting issues among agencies, overlapping

programs, increasing redundancy

Focus on compliance (budgeting) as opposed to

performance

Lack of systematic monitoring system and poor

information system

Evaluation done on an ad hoc basis

New Challenges in Managing the Public Sector

Performance in Malaysia

3

Inland Rev.

Board

Customs

Dept. Policy

Sys. &

Control

Ministry of Finance

4

P1 P2 P4 P5

1. Tax Analysis

2. Econ & Int’l

3. Nat. Budget

Office

4. Loan & Fin. Mgt

1. Gov Invest. &

MoF Inc

2. Monitoring and

Control

3. Strategic Fin.

4. OBB Project

Team

1. Govt Procurement

2. Housing Loan Mgt

3. Remuneration

Policy, Public

Money & Mgt

4. IT Mgt

5. Fed Treasury

(Sabah)

6. Fed Treasury

(S’wak)

7. Customs Appeal

Tribunal

8. Income Tax

Appeal Comm.

1. Inland

Revenue

Board

Acc. Gen.

Dept.

Accountant

General

Department with

seven (7) Sub-

Programs

Under MBS, MOF’s Programming Structure is

Based on the Organizational Structure

SECTOR/ PROGRAM

Valuation

Dept.

Mgt.

Services

P3 P6 P7

1. Management

2. Customs services

3. Enforcement

1. Valuation

Services

2. Training &

Research

3. National Asset

& Properties

Info. Centre

ACTIVITY/ SUB-PROGRAM

Note: Not all MOF’s programs/sub-programs are included in the above structure

5

Traditional

PPBS

MBS

OBB

Detailed

Controls &

Discipline

Programs &

Performance

Accountability,

flexibility &

delegation

1957 - 1968

1969 - 1990

1990 - 2012

2012 >

• Incremental

line item

budgeting

• Disaggregated

Budget

• Budget

Ceilings

• Program

Agreements

• Exceptions

Reporting

• Evaluation

• Integration

• Alignment

• Budgeting for

results

• Results

Reporting

• Evaluation

• Program

Performance

• Program-

Activities

• Performance

Indicators

• Evaluation

Integrated

Approach

Outcome Based Budgeting (OBB)

Activity/Sub-Prog

Activity Outcome

KPI

Activity Output

PI

Activity/ Sub-Prog

Activity Outcome

KPI

Activity Output

PI

National level

National Strategic Thrusts

National Outcome

Key Performance Indicator

National Programme

Ministry level

Ministry’s Outcome

Key Perf. Indicator

Programme

Ministry level

Ministry’s Outcome

Key Perf. Indicator

Programme

Program level

Prog. Outcome

KPI

Activity

Program level

Prog. Outcome

KPI

Activity

Program level

Prog. Outcome

KPI

Activity

Program level

Prog. Outcome

KPI

Activity

Activity / Sub-Prog

Activity Outcome

KPI

Activity Output

PI

Activity/ Sub-Prog

Activity Outcome

KPI

Activity Output

PI

Activity/ Sub-Prog

Activity Outcome

KPI

Activity Output

PI

Activity/ Sub-Prog

Activity Outcome

KPI

Activity Output

PI

Activity / Sub-Prog

Activity Outcome

KPI

Activity Output

PI

Activity/ Sub-Prog

Activity Outcome

KPI

Activity Output

PI

Activity/Sub-Prog

Activity Outcome

KPI

Activity Output

PI

HORIZONTAL

LINKAGES

6

Integrated Approach under OBB

VE

RT

ICA

L

AL

IGN

ME

NT

MIN

ISTR

Y/A

GEN

CY

Activity/Sub-Program Heads as Activists

Top Management as Champions and Sponsors

Trainers as Coaches

Focal Persons & End Users

NA

TIO

NA

L Awareness & Briefings

Structured Training Programmes

Forum & Seminars

MyResults online system

7

OBB Implementation Strategy (O

BB

Team

)

OBB Strategic Programming Worshops

8

Ministry-level

outcome

Program

Ministry-level

outcome KPI

Effective fiscal management Prudent public financial management

• Deficit to GDP

• Debt to GDP

• Credit rating (2 out of 3 rating agencies)

• Percentage Non-oil tax rev to total revenue

• Auditor General’s Accountability Index

• Composite client satisfaction index

Fiscal Strategy Investment Strategy Public Finance

Services Ministry Management

Services

P1 P2 P3

Attainment of

Balanced Budget

• Total tax revenue

• Percentage gov

expenditure to

GDP

• Year-on-year

growth of Gov

Revenue to remain

higher than

Expenditure

Effective investment

strategy

• Percentage NPL of

strategic loans

(excl. loans to

state gov)

• Percentage gov

guarantees issued

in compliance to

set criteria and

within annual limits

• Percentage

projected dividend

vs target

Effective public

finance services

• Percentage

procurement >RM

500k awarded

through tender in

compliance to set

policies

• No. of audit

queries

Timely, effective &

client- focused

management

services

• Total Mgt Service

Cost / Total FTE

• Fulfillment of client

charter

More effective

public debt

management

• Percentage FG

debt interest

payment to total

OE

• Percentage of

deferred liabilities

to GDP

Program

Outcome &

KPI

Fair & efficient

public finance

services

• Percentage

decrease in

negative feedback

/ appeals

Act/Sub-Prog Act./Sub-Program Act./Sub-Program Act./Sub-Program Act./Sub-Program

Accounting

Management

P5

Act./Sub-Program

High performance

Treasury

• Achieved

performance KPIs

P4

Reliable and timely

financial information

• Financial statements

that comply with

standards

Effective accounting

service delivery

• Impact Studies on

training

effectiveness

• Accountability

Index

• Star Rating

• Client Satisfaction

Index

Under OBB, MOF’s New Results Framework is being

Developed Based on its Strategic Functions & Roles

... to greater strategic

policy and advisory focus

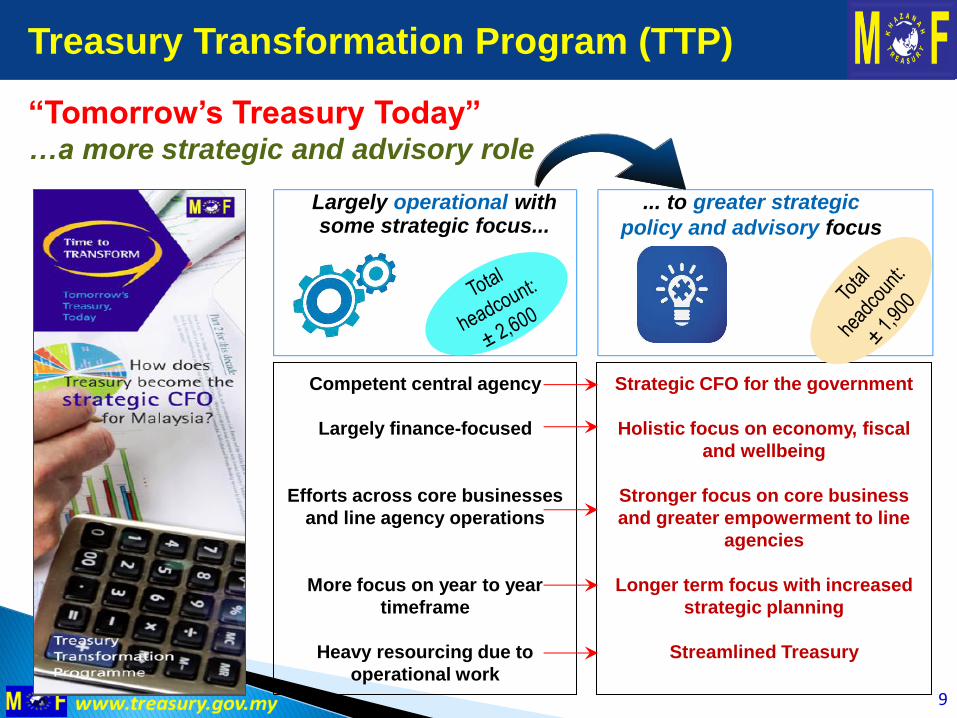

Largely operational with some strategic focus...

Competent central agency

Largely finance-focused

Efforts across core businesses

and line agency operations

More focus on year to year

timeframe

Heavy resourcing due to

operational work

Strategic CFO for the government

Holistic focus on economy, fiscal

and wellbeing

Stronger focus on core business

and greater empowerment to line

agencies

Longer term focus with increased

strategic planning

Streamlined Treasury

Treasury Transformation Program (TTP)

“Tomorrow’s Treasury Today” …a more strategic and advisory role

9

Ministry Mgt.

Services

Public Finance

Services Fiscal Strategy

Investment

Strategy

Ministry of Finance: Effective fiscal management

Prudent public financial management

10

P1 P2 P3 P4

1. Fiscal & Economic

2. Tax Division

3. National Budget

Office

4. Inland Revenue

Board

5. Customs

1. Strategic Investment

2. Statutory Bodies

Strategic Mgt

3. MOF Inc.

4. Public Asset Mgt

1. Govt Procurement

2. Housing Loans Div

3. Nat. Strategic Unit

4. Treasury Malaysia

Sabah

5. Treasury Malaysia

Sarawak

6. Customs Appeal

Tribunal

7. Income Tax Appeal

Commission

8. Valuation Dept

1. Remuneration Policy

and Corporate

Services

2. Strategic Corporate

and Communication

3. IT Management

Accounting

Management

Accountant General

Department with

seven (7) Sub-

Program

P5

MOF’s new Programming Structure is based on

identified results areas and its strategic functions

PROGRAM

ACTIVITY/ SUB-PROGRAM

Note: Not all MOF’s programs/sub-programs are included in the above structure

10

11

Challenges in Implementing OBB

Understanding the concepts

Role of management in strategy building

Quality of information in the results framework

Redefining the roles of budget review officers – focus on

performance & accountability

Sustainable capacity building and frequent movement of

OBB trainers

Translating business requirements into an IT system –

planning, budgeting, results reporting, M&E

Changes to the Ministry programming structure may require

changes to the Ministry organization structure.

thank you terima kasih

12

National Budget Office, Ministry of Finance Malaysia

Level 6, North Block, Ministry of Finance Complex

Precinct 2, Federal Government Administrative Centre

62592 Putrajaya

Tel : +603-88823850; Fax : +603-88823818

E-mail: [email protected]