organic and inorganic cultivation of sugarcane and … · 2018-12-15 · 5.3 cost and returns...

TRANSCRIPT

ORGANIC AND INORGANIC CULTIVATION OF SUGARCANE AND JAGGERY PREPARATION IN

BAGALKOT DISTRICT: AN ECONOMIC ANALYSIS

Thesis submitted to the University of Agricultural Sciences, Dharwad

in partial fulfillment of the requirements for the Degree of

MASTER OF SCIENCE (AGRICULTURE)

IN

AGRICULTURAL ECONOMICS

By MANJUNATH SHIVANAIKAR

DEPARTMENT OF AGRICULTURAL ECONOMICS COLLEGE OF AGRICULTURE, DHARWAD

UNIVERSITY OF AGRICULTURAL SCIENCES, DHARWAD – 580 005

JUNE, 2012

ADVISORY COMMITTEE

DHARWAD (S. S. GULEDGUDDA) JUNE, 2012 MAJOR ADVISOR

Approved by :

Chairman : ____________________________ (S. S. GULEDGUDDA)

Members : 1. __________________________ (H. BASAVARAJ)

2. __________________________ (S. M. MUNDINAMANI)

3. __________________________ (A. BHEEMAPPA)

4. __________________________ (Y. N. HAVALDAR)

5. __________________________ (S. DEVENDRAPPA)

CONTENTS

Sl. No.

Chapter Particulars

CERTIFICATE

ACKNOWLEDGEMENT

LIST OF TABLES

LIST OF FIGURES

1. INTRODUCTION

REVIEW OF LITERATURE

2.1 Cost and returns involved under organic and inorganic cultivation of crops

2.2 Investment pattern in agro-processing units

2.3 Cost and returns in processing of agricultural commodities

2.4 Shifting from inorganic to organic farming

2.

2.5 Problems of organic farmers

METHODOLOGY

3.1 Description of the study area

3.2 Sampling procedure

3.

3.3 Analytical techniques

3.4 Terms and concepts used in the study

RESULTS

4.1 General characteristics of the sugarcane sample farmers

4.2 Cropping pattern and major crops grown

4.3 Cost and returns involved in organic and inorganic sugarcane farms

4.4 Investment pattern in establishment of jaggery processing units (one tonne capacity per day)

4.5 Cost and returns involved in both organic and inorganic jaggery preparation per processing unit per annum.

4.6 Reasons for shifting from inorganic to organic sugarcane production

4.

4.7 Problems of organic sugarcane farmers

Contd…….

DISCUSSION

5.1 General characteristics of the sample farmers and jaggery processors

5.2 Cropping pattern and major crops grown

5.3 Cost and returns involved in both organic and inorganic sugarcane farms

5.4 Investment pattern in jaggery processing unit

5.5 Cost and returns involved in both organic and inorganic jaggery preparation

5.6 Reasons for shifting from inorganic to organic cultivation of sugarcane

5.

5.7 Problems of organic sugarcane farmers

6. SUMMARY AND POLICY IMPLICATIONS

REFERENCES

APPENDICES

LIST OF TABLES

Table No.

Title

3.1 District-wise area under sugarcane in Karnataka

3.2 Taluk-wise area under sugarcane cultivation in Bagalkot District

3.3 Land utilization pattern in Mudhol and Jamkhandi taluks of Bagalkot district during 2010-2011

3.4 Key indicators of Mudhol and Jamkhandi Taluks of Bagalkot district during 2010-2011

3.5 Source of Irrigation and area Irrigated in Mudhol and Jamkhandi taluks of Bagalkot district during 2010-2011

3.6 Sampled villages and farmers in Bagalkot district

3.7 Sampled villages and jaggery processors in Bagalkot district

4.1 General characteristics of sample sugarcane farmers

4.2 Cropping pattern of the sample sugarcane farmers

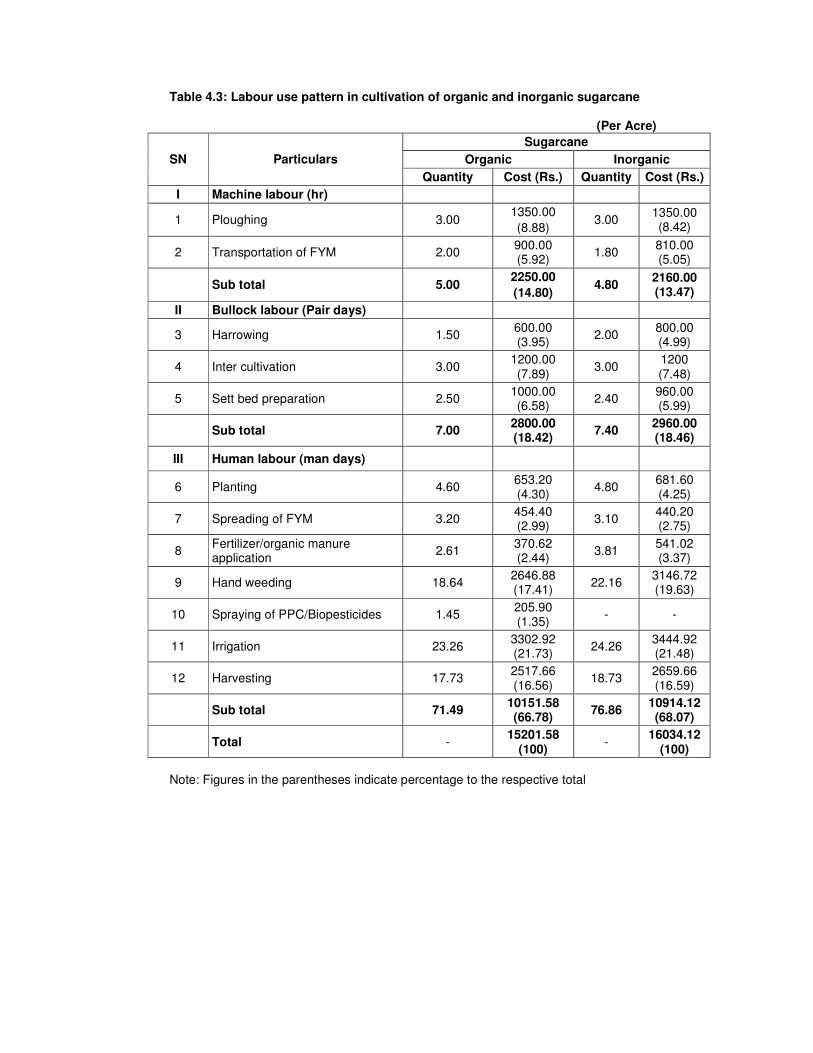

4.3 Labour use pattern in cultivation of organic and inorganic sugarcane

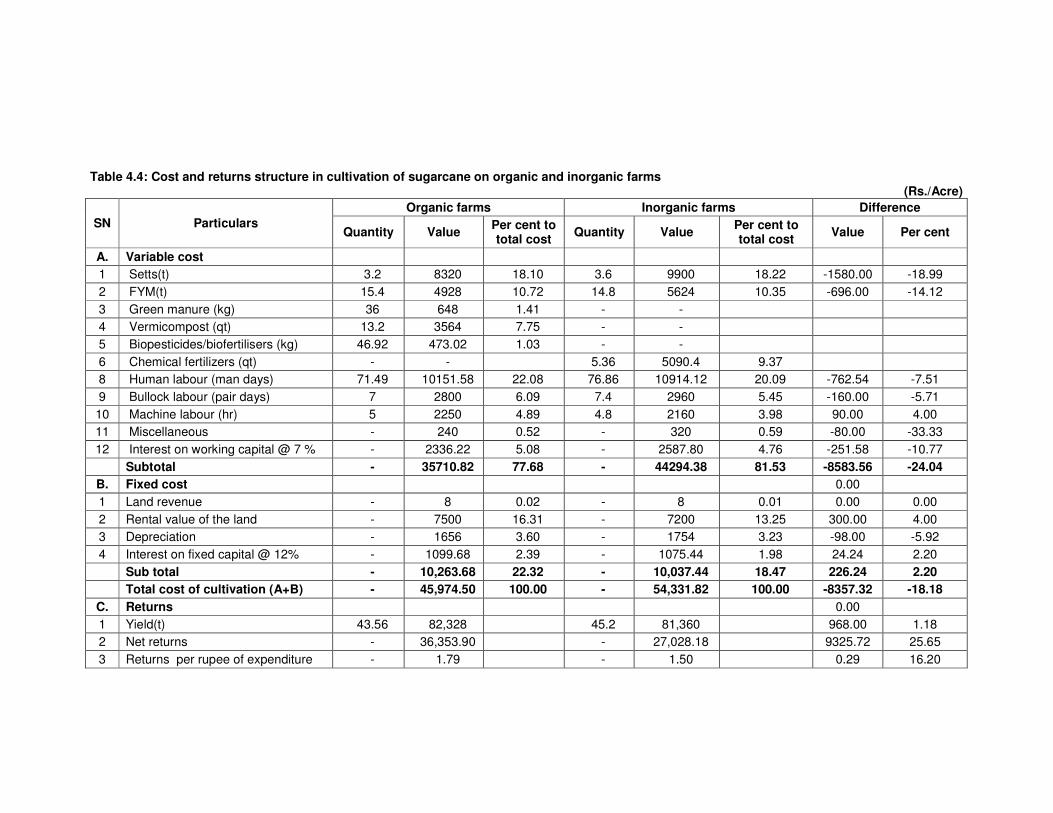

4.4 Cost and returns structure in cultivation of sugarcane on organic and inorganic farms

4.5 Investment pattern in establishment of jaggery processing unit (one tonne capacity per day)

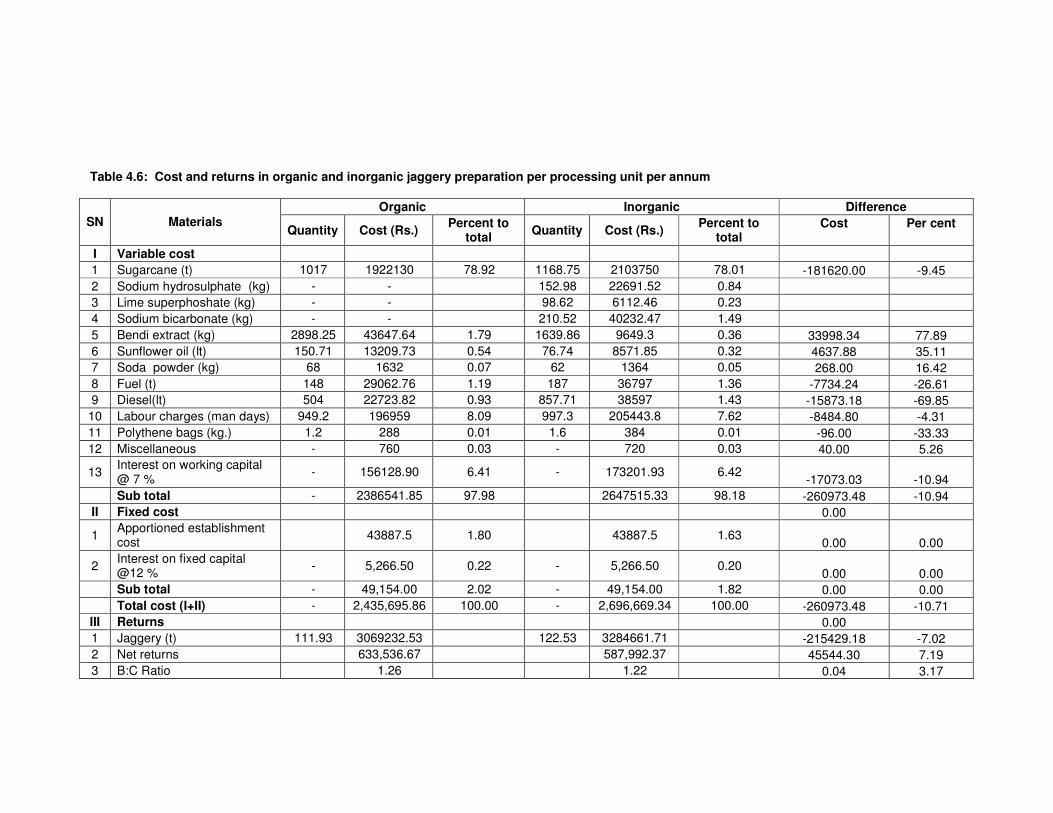

4.6 Cost and returns in organic and inorganic jaggery preparation per processing unit per annum

4.7 Cost and returns in organic and inorganic jaggery production (Rs/t)

4.8 Break-even analyses in organic and inorganic jaggery preparation per processing unit

4.9 Financial feasibility of investment in organic and inorganic jaggery processing

4.10 Reasons for shifting from inorganic to organic sugarcane production

4.11 Problems of organic sugarcane farmers

LIST OF FIGURE

Figure No.

Title

1 Map showing a study area

2 Graphical representation of the farmers

3 Graphical representation of the sample jaggery processors

4 Labour use pattern in organic and inorganic cultivation of sugarcane

5 Per ton cost of organic and inorganic jaggery production

LIST OF APPENDICES

Appendix No.

Title

I State wise areas under sugarcane in India (2010-11)

II Projections of sweetener requirement vis-à-vis sugarcane production in India up to 2020 AD

1. INTRODUCTION

Sugarcane (Saccharam officinarum) is native to India and has been cultivated from the historic times over the years and also it is a major commercial crop next to cotton in India. Sugarcane is most important source of sugar. Indian agro-climatic conditions are favourable for the production of sugarcane. Sugarcane plays a pivotal role in the agro-industrial economy of India and in fact on real economy, performance of sugar industry is directly related to the sugarcane production in India.

The main sugarcane growing states in India are Uttar Pradesh, Maharashtra, Karnataka, Andhra Pradesh, Haryana, Bihar, Gujarat and Punjab. Sugarcane is grown extensively in India. During 2010-11,the crop occupied over 49.40 lakh hectares in the country with a production of 3391.68 lakh tonnes, of which 66 per cent is concentrated in the northern part of the country (Appendix-I). In Karnataka, sugarcane is being cultivated over an area of 4.21 lakh hectares with a production of 375.95 lakh tonnes (Appendix-I) of cane and stands third in India with respect to area coverage next only to Uttar Pradesh and Maharashtra. In the recent past, there has been an increasing trend in both area and production of sugarcane in the state. Some of the important sugarcane growing districts in Karnataka state are Bagalkot, Belguam, Mandya, Bidar, Bellary and Bijapur.

Organic production systems are based on specific standards precisely formulated for food production and aims at achieving agro-ecosystems, which are socially and ecologically sustainable. It is based on minimizing the use of external inputs through use of on-farm resources efficiently compared to agriculture based on the use of chemical fertilizers and pesticides. Thus, the use of synthetic fertilizers and pesticides is avoided.

Sugarcane in India is processed into sugar, gur and khandasari and undergoes considerable weight reduction during processing. The methods of converting sugarcane and manufacturing sugar, gur and khandasari are different but a great value is added in the manufacturing of these consumable final products. Further, it offers employment opportunity to millions of people. Gur is prepared in almost all parts of the country where sugarcane is grown extensively. Gul, Gud, Jaggery, Vellum and Bella are the different names known in different parts of the country.

Organic jaggery is a pure, wholesome, unrefined whole sugar which contains the natural goodness of minerals and vitamins. It comes from the sap of sugarcane and its flavour is described as an aromatic blend between brown sugar and molasses with sweet undertones. But organic jaggery is superior compared to conventional jaggery. Because, it is processed without the use of chemicals, organic jaggery retains many vital vitamins and minerals, such as calcium, phosphorus, magnesium and potassium. In fact, organic jaggery has a mineral content approximately 50 times greater than refined sugar and five times more than brown sugar.

Nutritional and medicinal value of jaggery

The acceptable taste and nutritive value of jaggery has attracted man since ancient times. Jaggery is also called “Non Centrifugal Sugar” or “Artison Sugar”. It forms an important item of Indian diet for its high nutritive value and as a sweetening agent. White sugar contains only sucrose (99.70%), whereas jaggery has sucrose (51 %), protein (0.25%), glucose (21.20%) and minerals (3.40%) in addition to traces of fats (0.02 to 0.03%), calcium (0.39%), vitamin A, vitamin B, Phosphate (0.025%) and provides 383 K cal/100g jaggery (Shrilakshmi, 2003).

Dietary sucrose (sugar) is mixed blessings which makes food more attractive and appetizing but excessive consumption often leads to various kinds of pathological conditions like, dental curies, coronary thrombosis, ischemic heart disease, diabetes, acidity, depression and obesity etc., Some studies have also shown that high sugar intake leads to higher cancer risk. Jaggery which is an alternate sweetener derived from sugarcane crop is health friendly. In Ayurveda, jaggery is considered to be the best of all the sugarcane preparations (Shrilakshmi, 2003).

“The wise live without injuring nature as the bee drinks honey without harming the flowers” (The Buddha). In the same way our agriculture manipulation should not disturb the natural ecosystem and resource base for the future generation.

India is the land of agriculture; it has a rich and vivid basic natural resources base in terms of land, water, climate, rainfall, flora and fauna. However, these natural resources are faced with a severe demographic pressure. India has about 16 per cent of the world’s human population and 15 per cent of the world’s livestock population. But to meet their requirement we have only 2 per cent of the world’s geographical area, one per cent of rain water, one per cent of forest and 0.5 per cent of meadow (pasture).

According to 2011 census, GOI, India’s population has reached 1.21 billion. India has been adding an incredible 1.5 crore to her population every year with the growth rate of two per cent per annum. With the current food grain production of 245 million tonnes, India is committed to add 102 million tonnes more by the year 2021 AD to feed the estimated population of 1324 millions. The per capta availability of land has decreased from 0.48 hectare in 1951 to 0.20 hectares in 1981 and further, it declined to 0.15 hectare in 2001. The demand for food grains has to be met by raising the productivity of the land and simultaneously the soil health should also be maintained (Hosmani et al., 2000).

From 1960 onwards the green revolution succeeded in increasing the farmer’s income and yield of major crops because of the introduction of high yielding varieties and wide use of synthetic fertilizers and pesticides. The major effect of green revolution is that our agriculture was chemicalised. As the availability of land is decreasing day by day, application of fertilizers and pesticides has become a must to meet the demand for food grain. The effect of prolonged and over usage of chemicals on soil results in human health hazards and pollution of the environment. Now, once again the agricultural production has become stagnant and is not able to keep pace with the rapid growing population. So these problems have made us now to think of some other alternative methods of increasing food production. It is in this context the organic farming has drawn the attention of agricultural scientists, farmers and policy makers. Organic farming is not a new concept; it has been a way of life and tradition with our farming community over centuries.

Thus, in developing countries the twin challenges are production of sufficient food for the rapid growing population from available land and prevention of environmental degradation. Meeting of one challenge, if we want to increase the food production to a level to feed the growing population, this certainly cannot be done without the use of chemical fertilizers and plant protection chemicals because high yielding varieties and hybrids are highly responsive to fertilizers and susceptible to pests and diseases. The use of chemical fertilizers and plant protection chemicals for increasing agricultural production will lead to environmental degradation. To avoid environmental degradation, chemical fertilizers and plant protection chemicals are not used in agricultural production, food production cannot be increased to a level to feed the growing population. Hence, to face these two challenges simultaneously we have to adopt a compromising practice that is “organic farming”

Need for organic farming:

Intensification of agricultural production by way of widespread use of concentrated fertilizer and pesticides has resulted manifold increase in the production and productivity of crops. However, the ill effects of these agrochemicals are clearly visible on soil health, soil microbes, quality of ground water, fodder and food material. Thus organic farming is certainly becoming necessary for the following reasons:

- It is a sustainable and eco-friendly technology. - It improves quality and nutritive value of the farm produce. - It encourages sustainable livelihood of the producer as well as safeguards the

consumer’s health.

- It improves the physical, chemical and biological health of the soil. - It promotes healthy use of natural resources and minimizes all forms of pollution. - Toxicity and residues are the main problems of the agro-chemicals in farm produce. - Finally continuous decrease in input use efficiency under conventional farming.

Definition and concept:

The aim of organic farming is to have an ecologically sustainable farm production, which includes conservation of the natural habitat and resources, minimum pollution to soil, air and water. The cultivation is done without the use of synthetic chemicals like fertilizers, pesticides, herbicides and growth regulators.

Organic agriculture is a production system that avoids or largely excludes the use of synthetic compounded inputs viz., fertilizers, pesticides, growth regulators and livestock feed additives. It follows natural way of farming based on ancient teachings. Organic farming systems relay on crop rotation, crop residues, animal manures and mechanical cultivation to maintain the soil productivity and tilth to supply plant nutrients and control weeds. It has considerable economic, environmental and sustainability implications. In India, it has been an age old practice but has undergone considerable metamorphosis during green revolution. To produce more food grains in India, conventional farming is needed but its increasing cost factor; adulteration and untimely availability discourage the farmers to go for their large scale application. Under such situation, organic farming seems to be only economical and viable option. It may be defined as “A kind of diversified agriculture, where in, crops and livestock are managed through the use of integrated technologies with preference to depend on locally available matter at the farm’’. It emphasizes more on optimization of the yield potential of crops and livestock under a given set of farming conditions rather than yield maximization.

Principles of organic farming

1. To produce food of high quality in sufficient quantity.

2. To encourage and enhance biological cycles within the farming system involving micro organisms, soil flora, plants and animals

3. To maintain and increase the long term fertility of soils.

4. To create a harmonious balance between crop production and animal husbandry.

5. To produce fully bio-degradable organic products.

6. To minimize all forms of pollution

7. To promote the healthy use proper care of water, water resources and all lives therein.

The United States and other developed countries have some farm policies to support organic farming. But for India and other third-world nations, the concept of organic farming is only at debating stage. In future, our approach for organic agriculture should be to secure the advantages and economics of working with nature by bringing in more and more crops under organic farming and to obtain greatest yield of most nutritious crops while maintaining fertility of the soil and it should reduce the cost of cultivation to the extent possible.

Keeping all these aspects in view the present study was undertaken in Bagalkot district of Karnataka state, to analyse the economics of organic and inorganic cultivation of sugarcane and jaggery preparation with the following objectives.

Specific objectives of the study are

1. To study the cost and returns involved under organic and inorganic sugarcane cultivation

2. To analyze the investment pattern in jaggery processing units 3. To study the cost and returns involved under organic and inorganic jaggery

preparation. 4. To ascertain the reasons for shifting from inorganic to organic cultivation of

sugarcane 5. To enumerate the problems of organic sugarcane farmers

Hypotheses

1. The cost involved under organic is less than inorganic sugarcane cultivation and returns from organic is more than inorganic sugarcane cultivation.

2. The cost involved under organic is less than inorganic jaggery preparation and returns from organic is more than inorganic jaggery preparation

Special features of the study

Today, there is an increasing awareness about alternative or natural or organic or sustainable farming in view of energy shortage, food safety and soil and environmental pollution arising out of chemical or inorganic farming. Thus, the organic farming will definitely help to create a healthy society and a country of prosperous agriculture and healthy environment of Northern Karnataka.

Organic farming is practiced in most of the crops in Bagalkot district. This study aims to analyse the various aspects of organic farming in comparison with inorganic farming practiced in sugarcane cultivation as well as jaggery preparation in the district.

Limitations of the study

Since data were collected by survey method, the inherent lacunae associated with this type of enquiry have crept into the study. Even though, the estimates were provided by the recall memory of the sample respondents because of the non-maintenance of records and accounts on the farm sincere efforts have been bestowed to elicite as accurate and reliable estimates as possible by cross questioning. However, the degree of discrepancy if any, would be negligible as the estimates presented are in averages.

Importantly the qualitative aspect of organic agriculture could not be captured in this study because soil fertility and productivity status could not be estimated. Further the produce could not be tested for the pesticide residue due to lack of appropriate facilities.

Presentation of the study

The entire study has been divided into six chapters. Chapter-I deals with the introduction to the topic, the specific objectives of the study and significance of the study. Chapter-II deals with the review of literature on earlier studies bearing on the objectives of present study. Chapter-III is devoted to the description of the study area, sampling frame, the nature and source of data, the tools and techniques of analysis adopted for evaluating the objectives and terms and concepts used in the study. Chapter-IV presents results under appropriate heads. Chapter-V discusses the results of the study. Finally, chapter-VI summerises the overall results, draws conclusions and outline the policy implications emerging from the study.

2. REVIEW OF LITERATURE

This chapter presents review of research work on organic and inorganic cultivation crops and agro processing. The reviews are presented under the following heads:

2.1 Cost and returns involved under organic and inorganic cultivation of crops

2.2 Investment pattern in agro-processing units

2.3 Cost and returns in processing of agricultural commodities

2.4 Shifting from inorganic to organic farming

2.5 Problems of organic farmers

2.1 Cost and returns involved under organic and inorganic cultivation of crops

Sujatha et al. (2006) studied the comparative analysis of efficiency of organic farming and inorganic farming in Karimnagar district of Andhra Pradesh. The study revealed that the cost on human labour has been found higher in organic cultivation of rice and cotton as organic farming is labour intensive, where as in inorganic farming, the cost of manures, fertilizers and pesticides are higher compared to organic cultivation of rice and cotton. The net returns have been found higher in organic farming in both the crops compared to inorganic farming though the total cost of cultivation has been more in inorganic farming compared to organic farming.

Sushil Kumar et al. (2006) studied the impact of drought on cost and returns from cereal crops under different organic and inorganic farming systems in Himachal Pradesh. The study has revealed the cost of cultivation right from cost C1 to cost C2 to be less in organic farming system than inorganic farming system farms. The cost of production per quintal of produce has also been lower on organic farming system than inorganic farming system.

Waykar et al. (2006) studied the economics of grape production under organic and inorganic farming in the Nasik district of Maharashtra. The study revealed that, per hectare total cost of cultivation has been found Rs. 14675 for organic grapes and Rs. 209035 for inorganic grapes.

Kshirsagar (2008) conducted the study on organic sugarcane (O S) farming for enhancing farmers’ income and reducing the degradation of land and water resources in Maharashtra. The study has revealed that the average cost of cultivation of OS crop was Rs.37017.38 per ha has against Rs.43163.81 per ha for inorganic crop, reflecting 14.24 per cent lower cost on OS farms, this is because of non-use of chemical fertilizers and less cost incurred on irrigation, seed and plant protection and the gross value of production (GVP) and profits were higher on OS farms than the inorganic sugarcane (IS) farms. The GVP from OS farms amounted to Rs. 116711.38 per ha as against Rs. 112087.84 per ha from OS crop thereby enhancing farmers income.

Sale and Yadav (2008) studied the sugarcane cultivation with an integrated approach in Kolhapur District of Maharashtra. This study was conducted to examine the per hectare resource use structure in organic and inorganic sugarcane farming, calculate the per hectare cost of cultivation in organic and inorganic sugarcane farming and compare the economics of the two farming systems. Results showed that the per hectare cost of suru sugarcane with inorganic and organic farming were Rs. 66,572.73 and Rs. 57,275.72, respectively and the per tonne cost of production of sugarcane were estimated as Rs. 660.83 and Rs.712.42 in inorganic and organic farming, respectively.

Bai et al. (2009) studied economics of organic farming vis-a-vis conventional production of robusta coffee in Chickmagalur region, India. In this study a self-help group consisting of fifteen growers practicing organic cultivation of coffee over a decade and fifteen conventional robusta small growers were surveyed in the Koppa zone for comparing the cost of production of coffee.

The results indicated that the total cost of cultivation of organic robusta coffee was comparatively high (Rs. 34,940/ha.) than the conventional cultivation (Rs 27,640/ha.), which translated into a cost of production of Rs. 32 per kg and Rs. 25 per kg, respectively. The cost of production was high in organic cultivation mainly due to high input costs. The growers' felt that the incidence of pests and diseases was low in organic system of farming compared to conventional system. However, the premium price for organic coffee were not commensurate with high cost of production, as there was surplus production of organic coffee world over.

Franz et al. (2009) studied the assessing the economic viability of organic cotton production in Uzbekistan: A First Look, Cotton in Uzbekistan is produced in rotation with winter wheat and rice according to national quotas. Production methods are unsustainable, economically and ecologically risky, contributing to soil degradation, water depletion and poor health. A comparative study on conventional production system with an integrated organic system in Western Uzbekistan revealed higher profits under an organic farming system. Combined with policies to improve the existing cotton value chain, organic cotton production could result in higher revenue while reducing pressure on the environment and improving livelihoods.

Dhandhalya et al. (2010) conducted a study on organic wheat farming for sustainable agriculture in Saurashtra region of Gujarat state. The study has revealed that the cost of cultivation and yield performance in organic and conventional farming has not changed significantly. In organic farming, yield reduction was observed in initial years of adoption but later on, it takes normal level.

Ganesh (2010) conducted a study on an economic analysis of organic farming in North Karnataka: A case study of organic villages. The results revealed that the FYM and vermicompost together accounted for 68 per cent of the total input cost in organic farms whereas cost of fertilizers and pesticides accounted a major share (67 %) in conventional farms. The annual input cost of organic farm was 15.39 per cent less as compared to conventional farm. Organic farm was less expensive to the extent of 13.69 per cent in field crops under rainfed and 12.10 per cent under irrigated situations and was yielding more net returns (16.49 %) in perennial crops. Cost of production in paddy, arecanut, jowar, soybean and chick pea was lower in organic farms. Cotton and onion were more profitable under conventional farming. The regression coefficients of fertilizer and pesticide were negative indicating over utilization of these inputs. Organic farming enhanced income of 70 per cent farmers and created employment for 81.67 per cent. In view of the above benefits revealed by the organic village farmers, organic village programme of the state government need to be further extended to Hobli-level. Most of the organic produces were sold in conventional markets due to non-availability of separate organic market in the locality. The study recommends creation of separate organic markets at taluk level for major commodities in the area. There is a need to provide premium price for organic produces.

Ramesh et al. (2010) studied status of organic farming in India. A survey was made on certified organic farms in the country to ascertain the real benefits and feasibility of organic farming in terms of the production potential, economics and soil health in comparison to the conventional farms. The study revealed that organic farming, in spite of the reduction in crop productivity by 9.2%, provided higher net profit to farmers by 22.0% compared to conventional farming. This was mainly due to the availability of premium price (20-40%) for the certified organic produce and reduction in the cost of cultivation by 11.7%. In cases, where such premium prices were not available and the cost of cultivation was higher primarily due to purchased off-farm inputs, organic farming was not found economically feasible. However, there was an overall improvement in soil quality in terms of various parameters, viz. physical, chemical, biological properties, availability of macro-and micronutrients, indicating an enhanced soil health and sustainability of crop production in organic farming system.

Tripathi et al. (2010) conducted study on comparative economics of organic and inorganic farming. The investigation was undertaken to estimate cost and returns in organic and inorganic farming considering cotton, pigeonpea, mung in Kharif season and wheat in Rabi season. For these, total 100 samples were studied out of which 50 were organic cultivators and 50 were inorganic cultivators. The gross income was observed higher in organic farming. Input-output ratios were higher in organic farming as compared to inorganic farming.

They were 1.49 against 1.27 for cotton, 1.64 against 1.53, for pigeonpea, 1.54 against 1.38 for mung and 1.49 against 1.28 for wheat at cost ‘C’.

Singh and Grover (2011) studied the economic viability of organic farming: An empirical experience of wheat cultivation in Punjab. The study revealed that the total variable cost on per acre bases for the cultivation of organic wheat has been found higher (Rs.20,185/acre) than inorganic (Rs.16,700/acre) wheat. The lower crop yield in organic wheat (6.79 qt/acre) less was well compensated by the higher market price.

Zhang et al. (2011) conducted the study on the benefit-cost analyses and development counter measures of organic rice production. The comparative analyses of the conditions and technical and economic indexes of producing organic rice and conventional rice were made by surveying the rice production in Chongming County. The results showed that the technical conditions of organic rice production was higher than that of conventional rice production; and at the current price level, organic rice production was more profitable than conventional rice production.

2.2 Investment pattern in agro-processing units

The investment in processing units needed for various kinds of machinery and building. These investments are made at particular point of time yielding returns continuously over a period of time. Hence, the studies which involved cash flow techniques and financial ratios were reviewed here.

Nagaraj (1987) employed discounted cash flow techniques to evaluate financial feasibility of investment in coconut gardens assuming a discount rate of 15 per cent. The results indicated that the NPW was Rs.19,112.18, Rs.20,663.73, Rs.30,021.64 and Rs.59,476.87, respectively for one hectare of marginal, small, rainfed large and irrigated large farms. The benefit cost ratio for the respective groups was 1.17, 1.15, 1.30 and 1.22 and IRR was 28.84, 24.02, 44.92 and 27.04 per cent, respectively for the above mentioned groups.

Hemanth (1991) studied appraisal of investments in bakery through discounted cash flow techniques and reported 55.50 per cent and 1.08 of IRR and BCR, respectively at 15 per cent discount factor indicating that investment on bakery processing unit was highly profitable.

Teggi (1995) in his study on production and marketing of jaggery in Ghataprabha command area of Karnataka, reported that the investment made in the establishment of jaggery processing unit was recovered within a short period of one years. The NPV of jaggery processing units at 15 per cent discount rate was estimated at Rs.9,07,324.50 over the average life span of jaggery processing unit (10 years). Positive and high net present values reiterated the profitability in jaggery production. The IRR in jaggery processing was more than 100 per cent. It is mainly due to generation of returns from the very beginning. This revealed that the jaggery processing units were economically feasible even at higher discount rates. The benefit-cost ratio was quite appealing (1.16). The encouraging project indicators revealed the economic feasibility of jaggery processing units.

Suresh (2001) in the study on performance of organic farming in Shimoga district of Karnataka reported that per acre net income obtained in organic farms (Rs.19367.96) was more than inorganic farms (Rs.13691.02). This was due to 18.10 per cent higher yields obtained on organic farms over the inorganic farms. And the B:C ratio in case of organic method of cultivation (2.04) was noticed to be higher than inorganic method of cultivation.

Nandimath (2008) in his study on economics of jaggery production in Karnataka reported that the investment made in the establishment of jaggery processing unit was recovered within a short period of 1.7 years. The NPV of jaggery processing units at 12 per cent discount rate was estimated at Rs.10, 30,268 over the average life span of jaggery processing unit (10 years). Positive and high net present values reiterated the profitability in jaggery production. The IRR in jaggery processing was more than 100 per cent. It is mainly due to generation of returns from the very beginning. This revealed that the jaggery processing units were economically feasible even at higher discount rates. The benefit-cost ratio was quite appealing. The encouraging project indicators revealed the economic feasibility of jaggery processing units.

Kumar and Chinnapa (2010) conducted the study on economic analysis of cashew processing in Karnataka.The study revealed that the processing aspects of cashew nut in Karnataka is based on primary data collected from 30 cashew processing units spread over Udupi and Dakshina Kannada Districts of Karnataka. The data were analysed using descriptive statistics, investment measures and break-even analysis. Investment feasibility of cashew processing units was done using discounted cash flow techniques such as Net Present Value, Benefit-Cost Ratio and Internal Rate of Return. The study indicated that variable cost of processing of cashew nut worked out to Rs. 48,844 per tonne of which the cost of raw materials constituted major item with 81.01 per cent. The marketing costs and fixed costs were in the order of Rs. 3862 per tonne and Rs. 2289 per tonne, respectively. The total cost of processing inclusive of variable cost, marketing cost and fixed cost came to Rs. 54,433 per tonne. Processing units realized net returns of Rs.3,880, Rs.3,537 and Rs.3,009 per tonne in large, medium and small size units, respectively. Business ratios indicated that the medium and large size units were more efficient compared to the small size units. Investment on cashew processing was economically viable as indicated by results of Net Present Value, Benefit Cost Ratio and Internal Rate of Returns. Further, scope for increasing the efficiency and reducing the cost of small processing units was observed.

Naveen et al. (2010) conducted a study on investment analysis in grapevine orchards. The study was conducted in Bijapur district of Karnataka state with overall objectives of studying the feasibility of investment in grapevine orchards. Data were collected from 60 grape wine growers spread over in the district. The per hectare establishment cost were Rs. 3, 94,377.44, The total maintenance cost during bearing period was Rs. 1, 86,043.25. The average yield of grapevine orchards was 14 tonnes per hectare per year and average returns were Rs. 5, 29,787. The study further revealed that NPV for grapevine orchards was Rs. 16, 26,956, the B-C ratio was 2.2, Pay Back period was 3.2 years and IRR was 42.33 per cent.

Ramrao (2011) conducted a study on an economic appraisal of manufacturing and marketing of jaggery in Andhra Pradesh state. He reported that the life span of the jaggery manufacturing units is considered as ten (10) years. The discount rate chosen was 15% which was also the interest rate charged by banks. Sensitivity analysis was carried out at 12 and 18% discount rates. BCR and NPW at 15% discount factor were 1.12 and Rs. 2,13,138.25, respectively. Sensitivity analysis showed that at 12% discount rate the BCR was 1.10 and NPW was Rs. 2,63,158.73. At 18% discount rate the BCR was 1.1 and NPW was Rs.1,70,123.23. The jaggery manufacturing units were found to be profitable at chosen discount factors as the BCR was greater than one (>1) and NPW was positive. The IRR was found to be high (>50). The establishment of jaggery manufacturing units involves considerable costs. From the table it is clear that the investment required for establishing jaggery manufacturing unit was Rs. 1,23,112. The value of the land (Rs.64,264.46) attributed to 52.2% of the total cost. The cost of cane crusher (Rs. 26,887.66) and electric motor (Rs.14,662.64) together contributed to 33.75% of the total cost.

2.3 Cost and returns in processing of agricultural commodities

Muralidharan (1981) investigated the cost of establishing gur units with different capacities and it ranged from Rs. 36,000 for 5 HP, Rs. 43, 920.80 for 7.5 HP, Rs.46, 678. for 10 HP and Rs.65, 185 for 15 HP units. On an average the unit processing cost of gur worked out to be Rs.43.05 per quintal. The input cost was the highest for single element which was Rs.9.77 per quintal (22. 69%) of the total cost. The element costing next highest was labour expense which was Rs.8.64 per quintal (20.02 %). The fixed cost amounted to be Rs. 7,878.56 and variable cost was Rs.18,361.69 with a total cost of Rs.26, 240.25.

Singh et al. (1981) reported that cost of processing of arhar included the cost of fixed resources (the processing plant) and the cost on working capital (the cost for operating the plant). The average investment on fixed and working capital based on five processing units worked out to Rs.13,50,000 and Rs.1,01,920, respectively. The gross income worked out to Rs.50, 24,250. The cost of arhar plus operating cost came to Rs.48, 40,420. Average cost of processing of arhar dal came to Rs. 5.50 per quintal.

Ananth Ram (1989) in his study on economics of processing and marketing of gur in Indore district of Madhya Pradesh revealed that a sum of Rs.6.80 per quintal of gur was the processing cost of sugarcane under power of kolha units.

He noticed that the processing cost differed from unit to unit. The level of capital investment, type of crusher used and the quantity of sugarcane crushed were the factors influencing the processing cost.

Raju and Ramesh (1989) worked out cost of production in jaggery on per hectare basis of sugarcane cultivated. The cost of production of jaggery worked out to be Rs.28,417 per hectare of sugarcane area. About 70 per cent of the total cost accounted for the production of sugarcane. The other major items of cost were wages paid to human labour, rent paid for the use of crushers and chemical ingredients. The jaggery production from one hectare of sugarcane worked out to be 93.28 quintals. The net returns of jaggery production per hectare from sugarcane were estimated to be Rs.5,127 with a total return of Rs. 33,724.

A study by Nagaraj et al. (1989) revealed that the overhead costs in fruit processing accounted for only 12.25 per cent of the total cost of the remaining expenses the cost of fresh fruit accounted for 48.5 per cent of the total cost followed by other material cost (12.50%), labour (7%), advertisement (6%) and taxes (5%).

In a study by Rohal et al. (1989) the average cost of processing of sugarcane into khandasari worked out to Rs.8.54 per Kg. The economic analysis of capital structure in khandasari unit showed a better capital turn over (Rs.1.83 per rupee investment) which indicated further scope of capital investment in the industry.

Raikar (1990) in his study on investment in processing of cashewnut in Karnataka observed that the utilization of installed capacity depended upon the volume of cashew nuts procured. The per quintal cost of processing worked out to Rs.553.54. Interest on capital was the major component (53.62%) in the total cost of processing of cashew nuts followed by wage for piece rate workers (20.36%) and the cost of tin (11.71%). It was found that raw material cost alone formed 72 per cent of the total cost.

Subramanyam and Sudha (1993) reported that the cost of processing one tonne of finished tomato products was around Rs.11, 185 with a total return of Rs.13, 603. The raw material and packing accounted for 71 per cent of the processing cost. The input-output ratio was 2.22. The sensitivity analysis revealed that the processing was highly profitable with a price of Rs.1300 to 1600 tonne for fresh fruits with a conversion ratio of 6 per cent and the price of finished product at Rs. 2500 per tonne. They further reported that each tonne of tomato processed would result in an additional return of Rs.2596 which was nearly three times more than the net returns realized from sale of fresh tomato.

Suryawanshi et al. (1994) reported that the cost of jaggery production was Rs.565 per quintal. They further noticed that 98 quintals of jaggery was prepared from the sugarcane grown on one hectare. They reported that the per hectare total cost of sugarcane cultivation was Rs. 41, 484 and the output per hectare was 89. 93 tonnes. The cost of production per tonne of jaggery was Rs.446.

Malik and Singh (1999) analyzed the cost and returns of sugarcane production in Hardwar district of western Uttar Pradesh. In case of reserve area (< 10 kms from sugar mills) cost A1, A2, B1, B2, C1, C2, gross income from main product and byproduct were Rs.21605, Rs.21605, Rs.24724, Rs.3390.8, Rs.28231, Rs.37415, Rs.45002 and Rs.4419 respectively. In far area (>10 kms from sugar mills ) the above costs in the same order were Rs. 21366, Rs.21366, Rs.24498, Rs.33293, Rs.28009, Rs.42758, and Rs.4416, respectively.

Lohar et al. (2000) estimated per tonne cost of production of sugarcane, per quintal production of jaggery, per quintal manufacturing of sugar and profitability of production of jaggery and sugar. The study was conducted with sample of 30 jaggery producers from six villages in Karveer, Tahsil, Kolhapur district, Maharashtra, India and it revealed that profitability is more in jaggery production.

Pawar and Dongare (2001) studied the jaggery processing in India revealed that, India produces 10.3 million tonnes of jaggery (gur) annually. Tremendous scope exists for improving the manufacturing process. This paper reports on data collected from 23 processing units in the Satara and Kolhapur districts of Maharashtra and makes recommendations for the production of quality jaggery.

Shivaramu et al. (2002) undertaken a detailed survey of jaggery-making units in Cauvery Command Area of Karnataka, India to evaluate the performance of a triple pan jaggery making furnace compared to local types. It was noted that the local types, i.e., single pan and double pan furnaces, took more time in boiling and also affected the quality of jaggery produced. Local furnaces also contained less safer inorganic clarificants and bleaching agents (sodium bicarbonate and sodium hydrosulfites) as compared to the triple pan jaggery, which contained bhendi mucilage. Because of the shorter boiling period, the daily production rate of jaggery in a triple pan furnace was 11.5 q, as compared to 7-8 q in local types. Using the triple pan furnace, the net returns were almost 2-2.5 times more (Rs.1,22,000/year) than with local types (Rs.51,000-65,000/year). In conclusion, the triple pan furnace is more efficient than the local types of furnaces.

Mungare et al. (2005) conducted an experiment at the Regional Sugarcane and Jaggery Research Station, Kolhapur, Maharashtra, India to investigate the clarification efficiency of some synthetic and herbal clarificants suitable for quality jaggery. Based on this it was concluded that application of synthetic clarificants viz., Bhendi Powder SN 22 mg/lit (2ppm) with Bhendi plant 2 kg/100 lit of sugarcane juice is recommended for maximum removal of scum, improving the colour and higher jaggery recovery.

Ramrao (2011) conducted a study on an economic appraisal of manufacturing and marketing of jaggery in Andhra Pradesh state, he reported that the present study sugarcane is accounting for 68.22% of the total cost of jaggery production, sugarcane is one of the key factors in deciding the price of jaggery. For preparing jaggery of one quintal the total cost incurred was Rs. 1,872, out of which 68.2, 10.1, 17.5 and 4.2% costs were incurred on sugarcane and additives, machines rent, labour charges and transport charges respectively. Further, BCR was arrived as 1.19. That is jaggery farmers are getting profits of 19 paisa for one rupee of investment. The time period (PBP) required for achieving the break even volume of output was 66 days, as the average production from the each manufacturing is on an average was 540 kg per day. On an average the jaggery units worked for 120–130 days in the region. From the above analysis, It can be inferred that jaggery production is profitable to the farmers.

From the foregoing reviews it was clear that the cost of processing farm products varied from commodity to commodity, over place and time as well. This was also true in the case of jaggery preparation. Some of the important factors which appeared to influence the processing cost in jaggery were quantity of cane crushed, crushing capacity, type of crusher used, type and quantities of chemical ingredients used and wages paid to the labour force. The length of crushing period also influenced to the processing cost in jaggery.

The review revealed that jaggery production was a major traditional enterprise in sugarcane producing areas. At times, jaggery making was profitable to cane producers than supply to sugar factory. The cost of sugarcane was the major cost item in jaggery production. The investment in jaggery processing units was found to be profitable.

2.4 Shifting from Inorganic to Organic farming

Anand Kumar (1998) found that increasing cost of chemical inputs (63 %), increase on the net return in organic farming (11 %), as the reasons behind shifting to organic farming.

Bruggen et al. (2003) studied the integrated approaches to root disease management in organic farming systems in Marijkeweg, Netherlands and they concluded that conventional agriculture has had major environmental impacts, in particular with respect to soil degradation. Soil structure, fertility, microbial and faunal biodiversity have declined and root diseases are common unless genetic resistance, soil fumigation and/or seed treatments are used. Primarily for environmental reasons and increasing demands for safe and healthy food from the public, farmers have switched over to organic production at an increasing rate.

Loganandan and Singh (2003) observed that more number of respondents (54 %) in Erode district of Tamil Nadu had the motive of environment safety to shift to organic farming followed by financial motives (40 %), soil health oriented motives (34 %), motivation by significant others viz., neighbouring organic farmers, environmental activists etc (30 %), quality of output related motives (24 %), motivation by media (24 %) and philosophical motives (18 %).

Anjugam et al. (2006) studied the economics of usage of bio-inputs in sugarcane to identify the determinants of adoption of bio-inputs and suggest alternate measures for their increased use in sugarcane cultivation in the western zone of Tamil Nadu. The results have revealed that access to bio-inputs, adequate information from the sugar mill; no health hazards have significant positive influence on profitability of adoption of bio-inputs usage in sugarcane.

Anita (2006) conducted a study of Agrocel Industries Ltd., in the Kutch district of Gujarat in reference with promotion of organic cotton cultivation. The study revealed that the farmers are enjoying a net gain of 14 to 20 per cent, resulting from higher revenues and lower costs. The motivation of the farmers to take up organic farming on contract is not based on returns alone; there are benefits like supply of seeds, bio-pesticides, bio-fertilizers, etc. on credit at their door step and that too at subsidized rates; hassle free marketing of output, regular visits of field staff for guidelines and timely payment by the company.

Jaswinder and Kalra (2006) conducted a case study on organic farming in Punjab (India) among 60 farmers. Majority of the respondent farmers were satisfied with contract organic farming. Technical guidance and inputs were provided by firms. Most of the farm operations were done by respondents manually. The total area under organic farming in selected districts was 14.98 per cent of the total operational land holding of the selected respondents and was likely to be increased marginally to 15.14 per cent in next year. The major reasons for opting organic farming reported by the respondents were: easy marketing, additional benefits (certification of farm and premium price), availability of inputs and technical guidance from firms.

Kalamkar (2006) studied the progress, possibilities and constraints of organic farming in India and he revealed that organic farming systems have attracted increasing attention world over due to wide adverse effects of conventional agricultural practices on human diet, environment and sustainability of agricultural production.

Murthy et al. (2008) studied the organic farming practitioners and their perception in Dakshin Kannada and Udupi districts of coastal Karnataka. The main reasons expressed by the organic farmers for adoption were increased pest and disease infestation through chemical fertilizers, loss of soil characters, less profit in chemical farming and health hazard.

Sengar et al. (2010) conducted study on organic agriculture: a prerequisite for sustainability. Organic farming is a production system that avoids or largely excludes the use of synthetically compounded fertilizers, pesticides, growth regulators and livestock feed additives. To the maximum extent organic farming systems rely on crop rotations, crop residues, animal manures, legumes, green manures, off-farm organic wastes, and aspects of biological pest control to maintain soil productivity and tilt, to support plant nutrients and to control insects, weeds and other pests. The main argument against the adoption of organic farming is its relative inefficiency in resulting into sustainable and adequate crop yields immediately, though organic farming is the only way to attain sustainability in agriculture in the long run. In this context, the rediscovered theme of organic farming can reach its expected goal over a long period of 8-10 years gradually replacing the chemical farming. In the transition period, simultaneous use of both the systems may have to be inevitably advocated. Organic farming alone has potential to achieve such sustainability as all the organic farming practices are in the tune with natural processes of an agro-eco-system.

Argiles and Duch (2010) conducted a study on a comparison of the economic and environmental performances of conventional and organic farming: evidence from financial statements. While conventional farming systems face serious problems of sustainability, organic agriculture is seen as a more environmentally friendly system since it favours renewable resources, recycles nutrients, uses the environment's own systems for controlling pests and diseases, sustains ecosystems, protects soils, and reduces pollution. At the same time organic farming promotes animal welfare, the use of natural foodstuffs, product diversity and the avoidance of waste, among other practices. However, the future of organic agriculture will depend on its economic viability and on the determination shown by governments to protect these practices. This paper performs panel regressions with a sample of Catalan farms (Spain) to test the influence of organic farming on farm output, costs and incomes. It analyses the cost structures of both types of farming and comments on their social and environmental performance.

Suresh Reddy (2010) studied the organic farming: status, issues and prospects –a review, it shown that opinion about organic farming are divergent, especially among the experts disagreements about the profitability and yield increase in organic farming are acute , but there is a strong consensus on its eco-friendly nature and inherent ability to protect human health. There are many people who are in favour of organic agriculture, advocate a careful conversion of farms into organic, so that yield loss is taken care to the extent possible.

2.5 Problems of organic farming

Restrepo and Rivera (1997) studied the contribution of the university to the development of organic farming in Latin America. The study revealed that though there was increasing interest in organic farming in Latin America, it has not yet reached the agenda at national policy-making level due to lack of knowledge or opposition. Some of the limitations affecting the widespread adoption of organic farming include lack of human resources, resistance to this method, commercial and economic pressure, land tenure problems, and lack of vision from the universities who could be training organic farming professionals

Ramaswamy et al. (1999) stated that jaggery making is a traditional enterprise in Tamil Nadu and is more profitable to cane producers than supply to the factory. The substantially higher price, immediate disbursements of sale proceeds for the sale of cane, missing registration in time with factory, delay in cutting and complex procedure of transactions with the factory make the cane growers favour cane supply to jaggery making. On the other hand absence of price risk, labour shortage in the case of own jaggery making, financial and technical assistance extended by the factory are the major factors attracting supply of cane to factory. The experience in jaggery making has negative influence on the cane supply to factory. Labour shortage had significant influence in encouraging farmers to supply the cane to the sugar mills. Distance of factory appears less significant in the decision process as the modern transport system viz., tractor had made transport of cane a non issue.

Chothe and Borkar (2000) observed that more number of respondents (61.33 %) in Nagpur district of Maharashtra had the problem of lack of knowledge about biofertilizers, followed by lack of knowledge about benefits of biofertilizers (56.66 %) and lack of knowledge about method of biofertilziers application (52 %), extension workers never show method and result demonstration (41.33 %), no evidence by agricultural department (25.32 %) and non-availability of agriculture guidance in village (20 %).

Saxena and Singh (2000) reported that, a high per cent of organic farmers in Malwa region of Madya Pradesh (70.90 %) had the problem of non-availability of biofertilizer culture of good quality followed by lack of knowledge and skill about improved methods of compost making (63.40 %). Similarly, lack of awareness about the time, concentration and method of biofertilizer application (59.10 %) and non-availability of vermicompost in adequate quantity (43.63 %) were the other problems noticed with organic growing farmers.

Thimmareddy (2001) reported that the majority of the farmers (70 %) of North Karnataka expressed the problem of no separate market for organically grown produce, followed by 40 per cent of the respondents expressed the problem of decline in returns in the initial period (3-4 years) of organic farming. Similarly, the labour problem was expressed by 30 per cent of the respondents whereas 20 per cent of the respondents expressed the problem of non-availability of organic pesticides and lack of published literature on organic farming and a less per cent (10%) of respondents expressed the problem of non-availability of good quality compost, no support and encouragement from sugarcane factory management to produce sugarcane by organic methods, no remunerative price for organic produce and discouragement by people in continued adoption of organic cultivation.

Nain et al. (2002) reported that the irregularity in the distribution of sugarcane purchase indent, delay in payment of sugar cane to the farmers, delay in unloading, lack of transportation facilities etc., were the major problems reported by the selected respondents in marketing of sugarcane to the sugar mills.

Usha et al. (2004) conducted a study to investigate the prevailing processing practices being followed by jaggery manufacturers in the Cauvery Command Area of Karnataka, and Study revealed high income manufacturers used a triple pan furnace while the majority used a double pan furnace due to lower investment and skill required.

It was found that sodium bicarbonate, sodium hydrosulfite and sodium formaldehyde sulfoxylate were the inorganic additives commonly used by all. Besides this, some used trisodium phosphate, while the majority used Magnafloc, of which the chemical composition was unknown. Some chemicals were found to be unlabelled and the safety limits not set by quality control institutions. Organic additives include bhendi mucilage and coconut or castor oil to get the light golden yellow colour and crystalline texture of jaggery. Pan cleaning with dilute HCl was regular and daily among triple pan furnace users, but a majority of double pan furnace users cleaned their pans once every 3 days. None of the manufacturers used disinfectants. A majority of manufacturers stored jaggery in jute bags or in open storage with an average storage time of less than one week. Forty of the manufacturers felt a need for an improvement in colour and hardness and were concerned with discolouration during storage. It is concluded that jaggery manufacturers are not satisfied with the jaggery they produce. This may prompt them to use chemicals indiscriminately to achieve good colour and texture. The manufacturing units are also unhygienic.

Venkatram and Mani (2006) studied the prospects and constraints in adoption of organic farming in Tamil Nadu. The study revealed that the major obstacles in practicing pure organic agriculture have been identified as limited technological options, large marginal costs and risk in shifting to a new system from the conventional farming, low awareness about the organic farming system, lack of marketing and technical infrastructure and added cost by way of inspection and certification.

Mallikarjun (2008) studied the production and marketing management behaviour of organic vegetable growers in Belgaum district, Karnataka. The study revealed that all the respondents expressed that problems of non-availability of labour and lack of research support for providing rationality of traditional organic practices, fluctuation in prices of the commodities, lack of minimum support price and inaccurate weighing instruments used by vegetable venders. While, majority of them expressed the need for fixing profitable minimum support price for organic produce (77.14 %) and establishing separate market for the sale of organic produce (72.14 %).

Dhandhalya et al. (2010) conducted a study on organic wheat farming for sustainable agriculture in Saurashtra region of Gujarat state. The study revealed that lack of marketing network was the main hurdle in disposal of organic wheat, nearly 97 per cent respondents strongly supported that organic farming is a sustainable in the long-run. Organic farming system will also help to promote livestock based integrated farming system and sustain rural livelihood with increased income and employment. The extent of adoption status among the sample farmers has been found fairly well. To encourage organic farming and to realize its full benefits, promotion of certification programme and assured market will go a long way to promote organic farming in Saurashtra region of Gujarat.

Tripathi et al. (2010) conducted study on comparative economics of organic and inorganic farming. The study revealed that the major constraints observed in organic farming were lack of awareness, high input cost, low yield, certification from government and poor market linkage.

3. METHODOLOGY This chapter deals with the description of the study area, selection of samples, the

sampling techniques adopted, the nature and source of data, various tools and techniques employed in analyzing the data. At the end of the chapter, some of the important concepts and terms used in the study are defined and explained to facilitate a clear understanding of the issues with which the current investigation is concerned. This chapter is organized under the following broad sections:

3.1 Selection and description of the study area

3.2 Data base and sampling procedure

3.3 Analytical tools used

3.4 Terms and concepts defined

3.1 Description of the study area

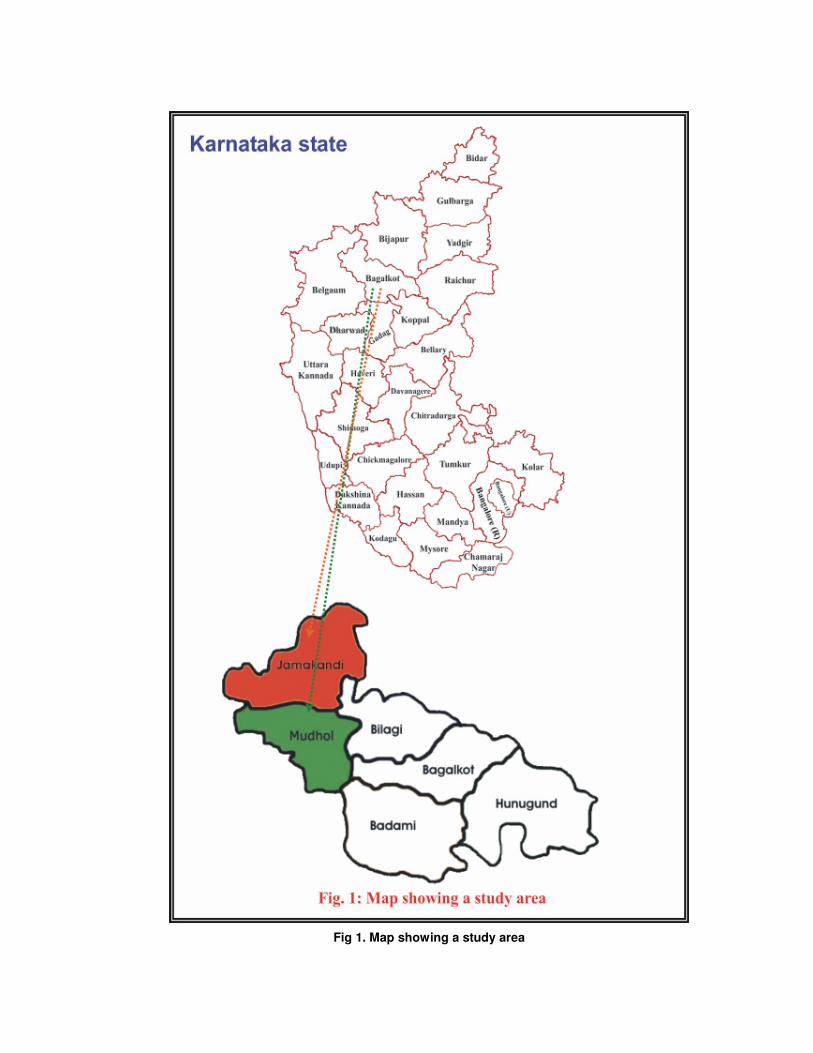

Bagalkot district is located in the Northern part of Karnataka which is the part of larger Deccan plateau. It lies between North latitude 16.12˚ and East longitude of 75.45˚. The district is bounded by Bijapur district towards North, Gadag district towards South, Raichur district towards East, Koppal district towards South-East and Belgaum district towards West.

Bagalkot is the second largest district in Belgaum division and occupies an area of 6,588 Sq.km. with a population of 18,90,826. The district comprises of 6 taluks and 627 villages. The rainfall across the district was 641.60 mm. Rivers like Malaprabha, Ghataprabha and Krishna flows in the district.

3.2 Sampling procedure

Multistage random sampling procedure was followed. In the first stage, in Karnataka Bagalkot district was selected based on number of jaggery units working in the district on one hand and on the other, district represents highest area under sugarcane (Table 3.1). However, Belgaum district was excluded because of inclusion of large number of taluks due to undivided district of North Karnataka. In the next stage, Jamkhandi and Mudhol taluks were selected based on maximum area under sugarcane (Table 3.2).

3.2.1 Selection of the study area

The total geographical area of Bagalkot district was 6,58,877 ha (Table 3.3) , of which net area sown was 4,72,386 ha (71.70 %) followed by area under forest 81055 ha(12.30%), land not available for cultivation 53713 ha (8.15%), fallow land 45985 ha (6.98 %), and other uncultivated land excluding fallow land was 5738 ha (0.87%).

The annual average rainfall of Bagalkot district was 641.6 mm (Table 3.4) and the total area under major crops in the district was 401894 ha, in which total pulses occupied maximum area 144216 ha (35.88 %), followed by sugarcane 104798 (26.08 %), maize 82119 (20.43 %), bajra 34045 (8.47%), wheat 20943 (5.21 %), sorghum 13407 (3.34 %) and cotton 2366 (0.59 %).

Ghataprabha (Mudhol, Jamakhandi and Bilgi taluks), Malaprabha (Badami taluk) and Krishna (Bagalkot and Hunagund taluk) rivers irrigates 3,04,569 ha, of area in Bagalkot district (Table 3.5). The major source of irrigation was from rivers, tanks and ponds (1,23,996 ha) followed by canals (54,825 ha), bore well (1,08,341 ha), wells (14,474 ha ) and lift irrigation (2,933 ha).

Sugarcane is one of the important cash crops grown in Karnataka, which plays a major role in the state’s economy. The crop is grown on an area of 4.21 lakh hectares with a production of 375.95 lakh tonne (Appendix-I). It is cultivated extensively in 16 districts of the state. The district-wise area under sugarcane in Karnataka is represented in Table 3.1. It is evident from the table that Belgaum district ranks first in cultivation of sugarcane with an area of 1,98,917 hectare (40.05 per cent) and production of about 149.73 lakh tonne (46.44 per cent) followed by Bagalkot and Mandya districts with an area of 88,497 and 47,944 hectares, respectively with production of about 64.49 and 26.82 lakh tonne, respectively.

Fig 1. Map showing a study area

Table 3.1: District-wise area under sugarcane in Karnataka

Districts Area under

Sugarcane(ha)

Production

(lakh tonnes)

Productivity

(tonnes/ha)

Bagalkot 88497 (17.82) 65.49 (20.31) 108

Belguam 198917 (40.05) 149.73 (46.44) 107

Bellary 3923 (0.79) 2.39 (0.74) 102

Bidar 29026 (5.84) 18.06 (5.60) 74

Bijapur 44113 (8.88) 18.92 (5.87) 72

Chamrajnagar 11914 (2.40) 7.20 (2.23) 89

Chikkaballapur 41 (0.01) 0.04 (0.01) 101

Chikmagalur 1437 (0.29) 0.05 (0.02) 136

Dakshina Kannada 32 (0.01) 0.02 (0.01) 101

Davangere 8502 (1.71) 4.53 (1.41) 129

Dharwad 5405 (1.09) 0.61 (0.19) 74

Gagad 959 (0.19) 0.10 (0.03) 101

Gulbarga 18939 (3.81) 7.63 (2.37) 67

Hassan 6777 (1.36) 2.35 (0.73) 123

Haveri 2372 (0.48) 0.72 (0.22) 79

Kopal 943 (0.19) 0.32 (0.10) 101

Mandya 47944 (9.65) 26.82 (8.32) 116

Mysore 13393 (2.70) 8.97 (2.78) 112

Raichur 46 (0.01) 0.03 (0.01) 101

Ramnagar 1071 (0.22) 0.88 (0.27) 107

Shimoga 7811 (1.57) 4.55 (1.41) 128

Tumkur 2935 (0.59) 1.89 (0.59) 118

Udippi 118 (0.02) 0.05 (0.02) 101

Uttarakannada 1262 (0.25) 1.05 (0.33) 88

Others* 317 (0.06) 0.00 (0.00) 0

Karnataka 496694 (100) 322.41 (100) 101

* Others – Bangalore (Rural and urban), Chitradurga and Kolar Source: Directorate of Economic and Statistics 2010-2011, Govt. of Karnataka, Banglore. Note: Figures in the parentheses indicate percentage to the respective total

Bagalkot is the second largest sugarcane producing district in Northern Karnataka, the total area and production of sugarcane accounting for 17.82 per cent and 20.31 per cent of the state sugarcane area and production. Organic cultivation of sugarcane is practiced largely in the district. Hence, the Bagalkot district was purposively selected for the study. And also large number of farmers practice the organic as well as inorganic cultivation of sugarcane in the district.

3.2.2 Selection of the sample taluks

Taluk-wise area under sugarcane in Bagalkot district is presented in Table 3.2. Although the crop is cultivated in almost all the taluks, cultivation of the crop is heavily concentrated in Jamkhandi (42.53%) and Mudhol (35.71%) taluks. This is mainly because of the fact that these two taluks are served by assured canal irrigation. Keeping in view of the objectives of this study, these two taluks were considered for in-depth analysis based on maximum area under sugarcane cultivation in the district (Fig. 1). Further, of the 412 jaggery processing units located in the district as many as 180 units (43.69 %) are operating in these two taluks.

The total geographical area of Mudhol and Jamakhandi taluk was 95450 ha and 116853 ha, respectively (Table 3.3). In Mudhol taluk the net area sown was 79515 ha (83.31 %) followed by area under forest 5218 ha (5.47 %), land not available for cultivation 6539 ha (6.85 %), fallow land 3299 ha (3.46 %), and other uncultivated land excluding fallow land was 879 ha (0.92 %) and in case of Jamakhandi taluk the net area sown was 91045 ha (77.91 %) followed by area under forest 11410 ha (9.76 %), land not available for cultivation 7107 ha (6.08 %), fallow land 5459 ha (4.67 %), and other uncultivated land excluding fallow land was 1832 ha (1.57 %).

The soils of Mudhol and Jamkhandi taluks are derived from trap rocks, sand stones and lime stones. Both kharif and rabi crops are grown in medium black soils and only rabi crops are raised in deep black soils.

The total area under major crops in Mudhol taluk was 73286 ha (Table 3.4), in which sugarcane occupied maximum area 37419 ha (51.06 %), followed by maize 18033 ha (24.61), total pulses 7608 ha (10.38 %), wheat 6099 ha (8.32 %), sorghum 2895 ha (3.95 %), bajra 1000 ha (1.32 %), and cotton 232 ha (0.32 %).

Ghataprabha left bank canal irrigates 76376 ha in Mudhol and 91596 ha in Jamakhandi taluk of Bagalkot district (Table 3.5). The major sources of irrigation in Mudhol taluk was from other sources like rivers, tanks and ponds (28249 ha) followed by canals (22990 ha), bore well (19847 ha) and wells (5290 ha) and in case of Jamakhandi taluk major sources of irrigation were from other sources like rivers, tanks and ponds (57093 ha) followed by canals (12931 ha), bore well (12720 ha), wells (6510 ha) and lift irrigation (2342 ha).

3.2.2 Description of the selected sample villages and sugarcane farmers

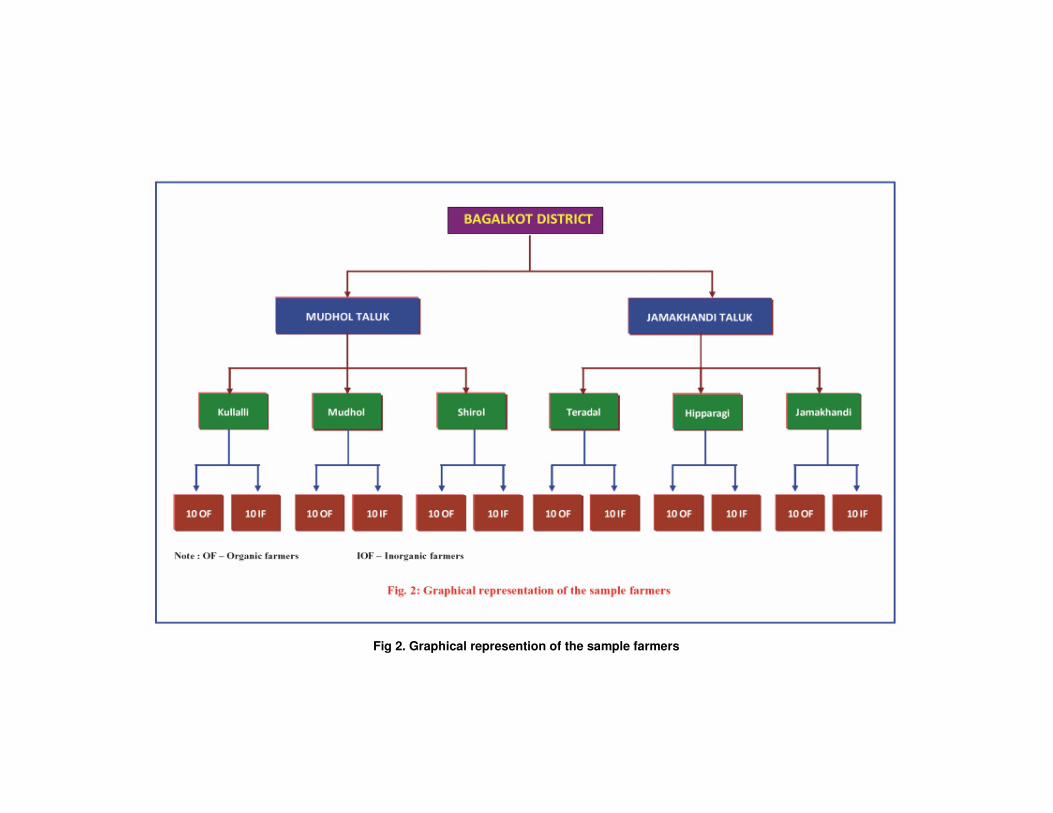

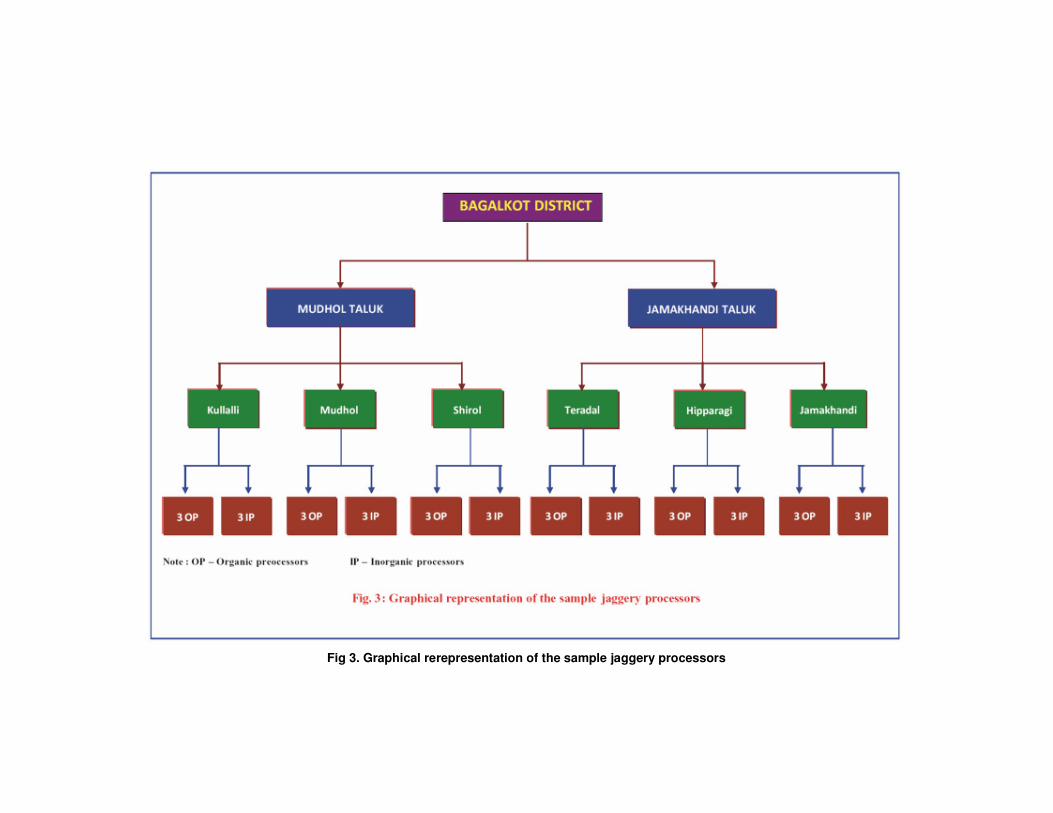

The list of villages growing sugarcane and jaggery preparation was obtained from the office of the Assistant Director of Agriculture at Mudhol and Jamkhandi taluks. From this list, a total of three villages were selected randomly from each taluk. In each sampled village, the primary data was collected from the sample farmers of both 30 organic and 30 inorganic sugarcane cultivating farmers and 9 organic and 9 inorganic jaggery processing units were selected randomly from each selected taluks, with a total sample size of 120 sugarcane cultivating (Table 3.6) and 36 farmers having jaggery units (Table 3.7). All organic farmers which were selected all members of Ranna Savayava Krishi Sanste, Bagalkot, which is provide certification to all members.

3.2.3 Nature and sources of data

For evaluating the objectives, both primary and secondary data were used in the study. Pre-tested and well-structured schedules were used for eliciting the required information from the sample respondents. The data pertaining to area under sugarcane, inputs used and output realized in organic and inorganic sugarcane cultivation along with their market values, investment requirement for establishing jaggery processing units in physical and monetary values, cost incurred in jaggery processing and quantities of both organic and inorganic jaggery produced were collected through personal interview method.

Table 3.2: Taluk-wise area under sugarcane cultivation in Bagalkot District

SN Taluk Area (ha) Per cent to total cultivated area

1 Badami 5122 4.89

2 Bagalkot 5455 5.21

3 Bilgi 11115 10.61

4 Hungund 1118 1.07

5 Jamkhandi 44569 42.51

6 Mudhol 37419 35.71

Total 104798 100.00

Source: District Statistical Office, Bagalkot (2010-2011).

Information on place and time of sale, price received, cost incurred in marketing were also collected from the sample respondents. The data for the present study were collected for the crop year 2011-12.

The information on area under sugarcane, number of jaggery processing units operating in the study area during 2010-11 was obtained through various statistical reports published by the Office of the District Statistical Officer, Bagalkot.

3.3 Analytical techniques

To fulfill the specific objectives of the study, based on the nature and extent of data, the following analytical tools and techniques were employed.

1. Tabular method

2. Budgeting technique

3. Financial analysis

4. Break-even analysis

3.3.1 Tabular presentation

The tabular presentation method was followed to study the general characteristics of sample of both organic and inorganic sugarcane farmers, the average cost and returns involved in organic and inorganic sugarcane cultivation, reasons for shifting over to organic farming and problems faced by the organic farmers.

3.3.2 Budgeting Technique

The budgeting technique method was followed to compute the average cost and returns involved in organic and inorganic jaggery processing unit, averages and percentages were worked out for the purpose of comparison. The major cost items involved in jaggery processing units have been detailed as follows

a. Raw material cost

Sugarcane is the one of major raw material used in jaggery processing. All the jaggery processors processed the sugarcane grown on their own lands and /or the sugarcane purchased from neighbouring farmers. Hence, the sugarcane cost was computed taking sugar factory price wherever owned sugarcane was used. Actual price paid including the transport charges was considered wherever it was purchased.

Table 3.3: Land utilization pattern in Mudhol and Jamkhandi taluks of Bagalkot district during 2010-2011

Mudhol taluk Jamkhandi taluk Bagalkot district

SN Particulars

Area (ha)

Per cent to

total

geographical

area

Area (ha)

Per cent to

total

geographical

area

Area (ha)

Per cent to

total

geographical

area

1 Area under forest 5218 5.47 11410 9.76 81055 12.30

2 Land not available for cultivation 6539 6.85 7107 6.08 53713 8.15

3 Other uncultivated land excluding

fallow land 879 0.92 1832 1.57 5738 0.87

4 Fallow land 3299 3.46 5459 4.67 45985 6.98

5

Net area sown 79515 83.30 91045 77.92 472386 71.70

6 Total geographical area 95450 100.00 116853 100.00 658877 100.00

Source: District Statistical Office, Bagalkot (2010-2011).

Table 3.4: Key indicators of Mudhol and Jamkhandi Taluks of Bagalkot district during

2010-2011

Taluks SN Particulars

Mudhol Jamkhandi

Bagalkot

District

1 Geographical area(ha) 95450 116853 658877

2 Population (No) 275174 408441 1651892

3 Normal rainfall (mm) 683.5 672.0 641.6

4 Forest area (ha) 5218 11410 81055

5 Total cultivated area (ha) 96484 106002 608723

6 Irrigated area (ha) 76376 91596 304569

7 Area under major crops (ha)

a) Maize 18033(24.61) 24124(28.78) 82119(20.43)

b) Sorghum 2895(3.95) 3238(3.86) 13407(3.34)

c) Wheat 6099(8.32) 4987(5.95) 20943(5.21)

d) Sugarcane 37419(51.06) 44569(53.16) 104798(26.08)

e) Bajra 1000(1.32) 988(1.18) 34045(8.47)

f) Cotton 232(0.32) 134(0.16) 2366(0.59)

g) Total pulses 7608(10.38) 5795(6.91) 144216(35.88)

Total 73286(100.00) 83835(100.00) 401894(100.00)

8 Jaggery processing units (No) 84 96 412

Source: District Statistical Office, Bagalkot (2010-2011).

Table 3.5: Source of Irrigation and area Irrigated in Mudhol and Jamkhandi taluks of Bagalkot district during 2010-2011

Mudhol taluk Jamkhandi taluk Bagalkot district

SN Source of irrigation Gross irrigated

area (ha) Per cent

Gross irrigated

area (ha) Per cent

Gross irrigated

area (ha) Per cent

1 Canals 22990 30.10 12931 14.12 54825 18.00

2 Wells 5290 6.93 6510 7.11 14474 4.75

3 Borewells 19847 26.00 12720 13.89 108341 35.57

4 Lift irrigation - - 2342 2.56 2933 0.96

5 *Other sources 28249 37.00 57093 62.32 123996 40.72

Total 76376 100.00 91596 100.00 304569 100.00

* Other sources: Rivers, tanks, and ponds

Source: District Statistical Office, Bagalkot (2010-2011)

Table 3.6: Sampled villages and farmers in Bagalkot district

Sugarcane sample farmers

Taluks Villages

Organic Inorganic

Grand total

(n=120)

Mudhol taluk a. Kulali

b. Mudhol

c. Shirol

10

10

10

10

10

10

20

20

20

Subtotal 3 30 30 60

Jamkhandi taluk a. Teradal

b. Hipparagi

c. Jamakhandi

10

10

10

10

10

10

20

20

20

Subtotal 3 30 30 60

Grand total 6 60 60 120

Table 3.7: Sampled villages and jaggery processors in Bagalkot district

Jaggery processors

Taluks Villages

Organic Inorganic

Grand total

(n=36)

Mudhol taluk a. Kulali

b. Mudhol

c. Shirol

3

3

3

3

3

3

6

6

6

Subtotal 3 9 9 18

Jamkhandi taluk a. Teradal

b. Hipparagi

c. Jamakhandi

3

3

3

3

3

3

6

6

6

Subtotal 3 9 9 18

Grand total 6 18 18 36

Fig 2. Graphical represention of the sample farmers

Fig 3. Graphical rerepresentation of the sample jaggery processors

b. Processing cost

Different chemicals/materials are used in jaggery processing; the costs of chemicals/materials used in jaggery processing were calculated at the actual price paid by the processor including transportation charges. The other costs included in processing were, wages paid to labour, fuel charges, interest on investment and depreciation. Depreciation was computed by using straight line method. The interest on investment was calculated at a rate of 12 per cent per annum on the book value. The actual wages paid to the labor were considered as labour charges. Baggase was the by-product of the jaggery processing units. Baggase was the major source of fuel for the jaggery processing units. However, the baggase produced from each unit was not sufficient to meet the entire fuel requirement of the respective processing units. A part of the fuel requirement was therefore, met by purchasing from other processors. The actual price paid for purchasing the fuel including the transportation cost was considered.

c. Cost of establishing jaggery processing unit

The jaggery processing units considered for the study were established in different years. Therefore, the written down values of all the machineries/equipments were considered and compounded to the reference year (2011-12) for the purpose of computing cost of establishing jaggery processing unit. Cost of each machinery/equipment including the shed requirement for establishing jaggery processing unit was considered.

3.3.3 Financial analysis

The financial feasibility of investment in jaggery processing unit is mainly based on the incremental cost and returns accruing from processing units over it life span. The Pay-Back Period (PBP), Net Present Worth (NPW), Benefit-Cost Ratio (BCR) and Internal Rate of Returns (IRR) were used as appraisal criteria for evaluating financial viability of jaggery processing units.

Pay-Back Period (PBP): Pay-back period refers to the length of time period required for an investment to generate the net cash income to be equal to the original investment. This time period is expressed in years.

I PBP =

Y

Where,

I = Initial investment

Y= Net cash flow

Net Present Worth (NPW): The net present worth represents the discounted value of the net cash inflow to the project .The N.P.V has been defined as fallows.

NPW

=

n

Σ Yn r =1

(1 + r)-n

] – C

Where

Yn= Series of net cash inflows

r = Discount Rate

C = Initial cost of investment

n = Time period

Benefit-Cost Ratio (BCR): It is the ratio of discounted project benefits to project cost. It has been defined as fallows.

Yi

BCR =

n

Σ

i=l (1+i)

n

÷ C

Where,

Yi, r, n and C are as defined in NPV

Internal Rate of Returns (IRR): It is the discount rate at which the net present value of the project is zero.

IRR

Many workers have argued that the opportunity cost of capital, cost of borrowing and social rate of time preference should be the criteria in selecting appropriate discount rate in the financial analysis. Hence, the cost of borrowing (12%) was considered as discount rate in the present investigation. A ten year time horizon was considered for the present investigation. An attempt was made to test the sensitivity of the benefits of processing units to changing prices of inputs and output.

3.3.4 Break even analysis: The break-even analysis was also attempted to estimate the level of jaggery production at which the returns are just sufficient to recover the initial investment in processing units. The break-even volume of output was determined with help of the following formula.

Break-even output = Fixed cost

unit variable cost - unit output price