oregon department of revenue 2019–2020 update and

TRANSCRIPT

Online CLE

Oregon Department of Revenue 2019–2020 Update and Corporate Activity Tax (CAT)

.5 General CLE credit

From the Oregon State Bar CLE seminar 20th Annual Oregon Tax Institute, presented September 15–18, 2020

© 2020 Betsy Imholt, Leah Putnam. All rights reserved.

ii

Chapter 3

Presentation Slides: Oregon Corporate Activity Tax (CAT)

Betsy ImholtDirector, Oregon Department of Revenue

Salem, Oregon

Leah PutnamCAT Manager, Oregon Department of Revenue

Salem, Oregon

Chapter 3—Presentation Slides: Oregon Corporate Activity Tax (CAT)

3–ii20th Annual Oregon Tax Institute

Chapter 3—Presentation Slides: Oregon Corporate Activity Tax (CAT)

3–120th Annual Oregon Tax Institute

Oregon Corporate Activity Tax (CAT)

Leah [email protected]

• Overview.

• Thresholds, registration, filing & payment due dates.

• What is commercial activity?

• CAT taxpayers and excluded entities.

• Additional CAT Information

• Summary of changes in House Bill 4202.

• Administrative rules.

• Additional resources and how to contact us.

2

Corporate Activity Tax

Chapter 3—Presentation Slides: Oregon Corporate Activity Tax (CAT)

3–220th Annual Oregon Tax Institute

Overview

3

• The CAT is a tax for the privilege of doing business in Oregon and is based on commercial activity done in the state.

• It’s applied to Oregon taxable commercial activity in excess of $1 million. The tax is computed as $250 plus 0.57 percent of taxable Oregon commercial activity above $1 million.

• It’s imposed on all types of business entities.

• It’s in addition to the state's current income taxes on businesses. Revenue from the CAT will be transferred to the Fund for Student Success and will be used for education spending.

What is CAT?

4

Chapter 3—Presentation Slides: Oregon Corporate Activity Tax (CAT)

3–320th Annual Oregon Tax Institute

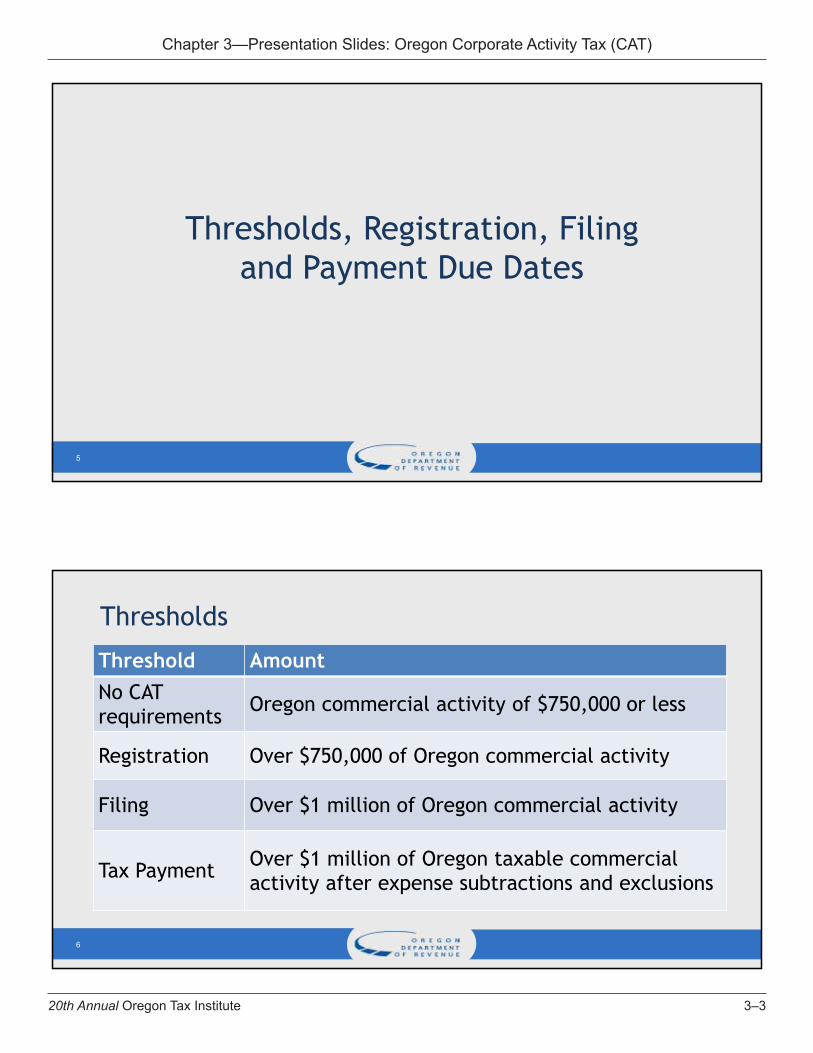

Thresholds, Registration, Filing and Payment Due Dates

5

6

Threshold AmountNo CAT requirements Oregon commercial activity of $750,000 or less

Registration Over $750,000 of Oregon commercial activity

Filing Over $1 million of Oregon commercial activity

Tax Payment Over $1 million of Oregon taxable commercial activity after expense subtractions and exclusions

Thresholds

Chapter 3—Presentation Slides: Oregon Corporate Activity Tax (CAT)

3–420th Annual Oregon Tax Institute

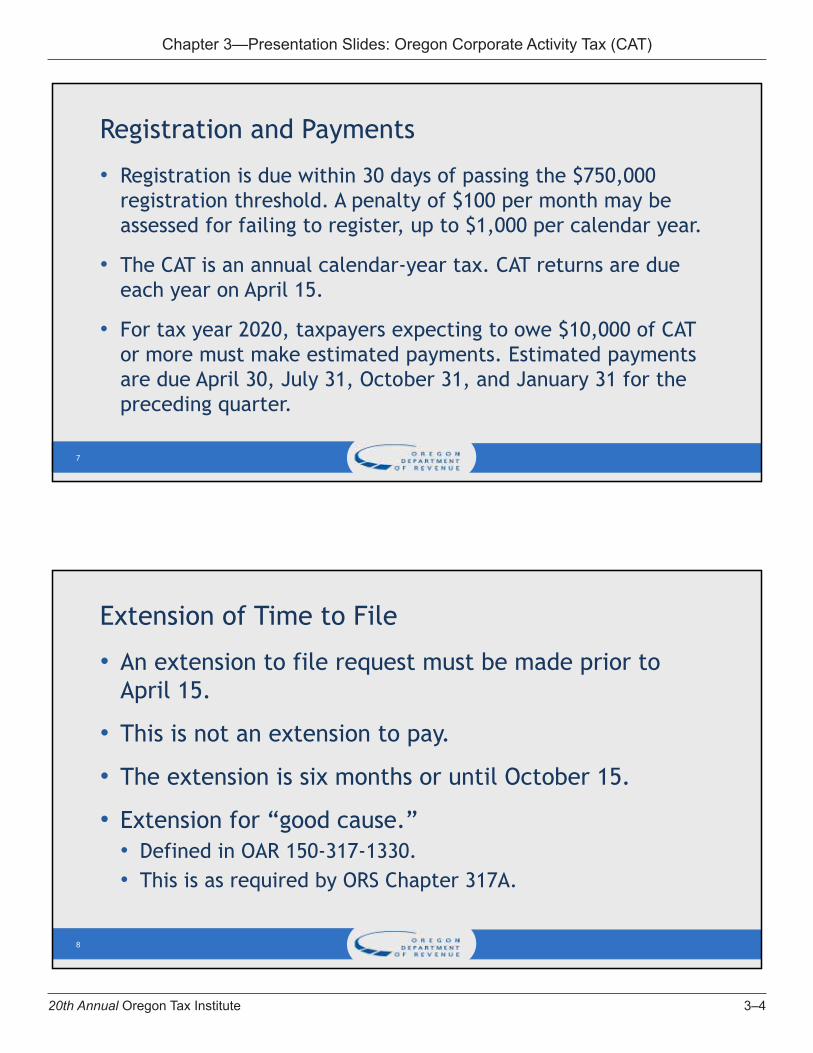

• Registration is due within 30 days of passing the $750,000 registration threshold. A penalty of $100 per month may be assessed for failing to register, up to $1,000 per calendar year.

• The CAT is an annual calendar-year tax. CAT returns are due each year on April 15.

• For tax year 2020, taxpayers expecting to owe $10,000 of CAT or more must make estimated payments. Estimated payments are due April 30, July 31, October 31, and January 31 for the preceding quarter.

Registration and Payments

7

Extension of Time to File

8

• An extension to file request must be made prior to April 15.

• This is not an extension to pay.

• The extension is six months or until October 15.

• Extension for “good cause.” • Defined in OAR 150-317-1330. • This is as required by ORS Chapter 317A.

Chapter 3—Presentation Slides: Oregon Corporate Activity Tax (CAT)

3–520th Annual Oregon Tax Institute

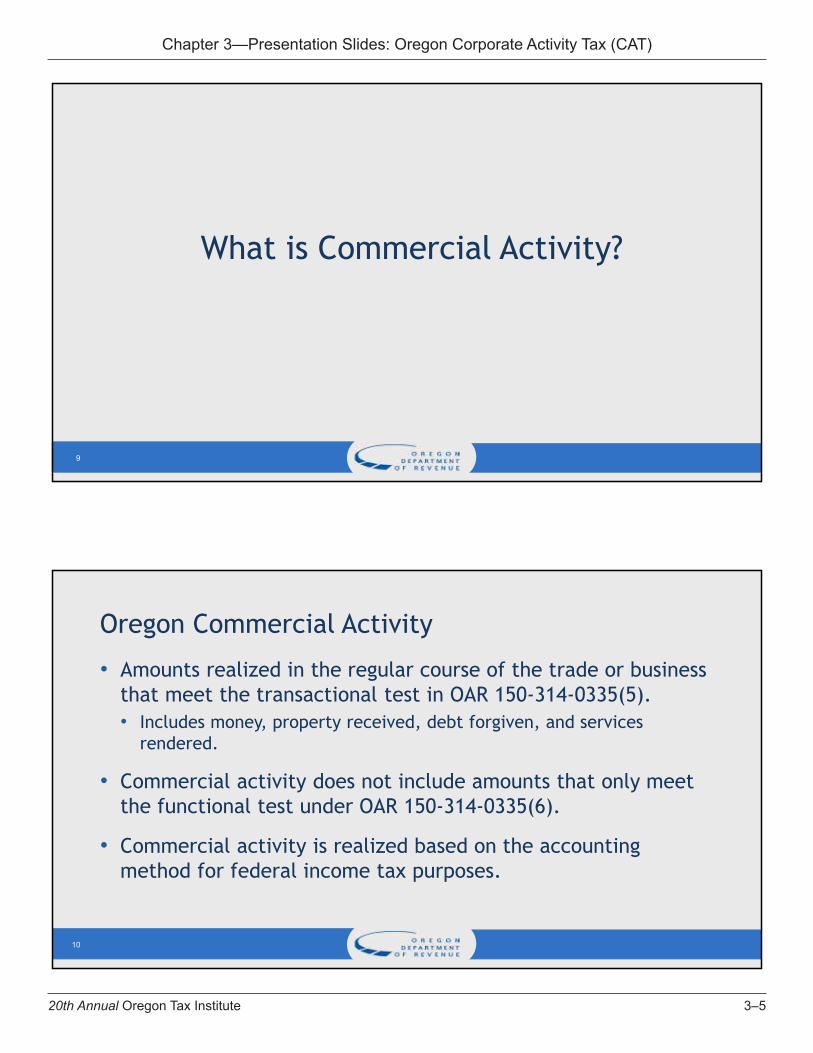

What is Commercial Activity?

9

Oregon Commercial Activity

10

• Amounts realized in the regular course of the trade or business that meet the transactional test in OAR 150-314-0335(5).• Includes money, property received, debt forgiven, and services

rendered.

• Commercial activity does not include amounts that only meet the functional test under OAR 150-314-0335(6).

• Commercial activity is realized based on the accounting method for federal income tax purposes.

Chapter 3—Presentation Slides: Oregon Corporate Activity Tax (CAT)

3–620th Annual Oregon Tax Institute

While commercial activity includes most business receipts, certain items are excluded and are not subject to the CAT. For example:• Receipts from the wholesale and retail sales of groceries.

• Sales of items or services that are delivered outside of Oregon.

• Farmers sales to agricultural cooperatives described in Section 1381 of the Internal Revenue Code.

• Amounts received by an agent on behalf of another in excess of the agent’s fee or commission.

• Receipts from transactions between members of the same unitary group.

• Distributive income received from a pass-through entity.

Oregon Commercial Activity Exclusions

11

CAT Taxpayers andExcluded Entities

12

Chapter 3—Presentation Slides: Oregon Corporate Activity Tax (CAT)

3–720th Annual Oregon Tax Institute

Entities subject to the CAT include, but are not limited to:• Individuals/sole proprietorships.• Partnerships.• LLCs.• Clubs.• C-corporations.• S-corporations.• Estates or trusts with commercial activity.• Any other entity.

Who is Subject?

13

1. United by more than 50 percent common ownership.

2. Unitary business must have one of the following:A. Centralized management or a common executive force.

B. Centralized administrative services or functions resulting in economies of scale.

C. Flow of goods, capital resources or services demonstrating functional integration.

Unitary Groups

14

Chapter 3—Presentation Slides: Oregon Corporate Activity Tax (CAT)

3–820th Annual Oregon Tax Institute

• Members of a unitary group may be in the same general line of business, such as manufacturing, wholesaling or retailing. Or, members may be in multiple lines of business that constitute steps in a vertically integrated process, such as the steps involved in the production of natural resources, which might include exploration, mining, refining, and marketing.

• Unitary groups must register, file, and pay as a single taxpayer.

• House Bill 4202 from the first 2020 special session created a modified group election which will be covered later.

Unitary Groups (cont.)

15

• IRC 501 organizations.

• Farmers’ cooperatives, if under section 521.

• Governmental entities.

• State tuition programs under section 529.

• Hospitals and long-term care facilities that are Medicare providers.

• Businesses with $750,000 or less in Oregon commercial activity.

Excluded persons

16

Chapter 3—Presentation Slides: Oregon Corporate Activity Tax (CAT)

3–920th Annual Oregon Tax Institute

Additional CAT Information

17

Cost Subtraction

18

• The law that established the CAT, specifically ORS 317A.119, allows taxpayers to subtract from commercial activity sourced to Oregon 35 percent of the greater of cost inputs or labor costs related to that activity.

• Taxpayers with commercial activity in and outside of Oregon, as well as those with excluded items, may have to apportion their cost inputs or labor costs as described in OAR 150-317-1200.

• Your cost subtraction may not exceed 95 percent of your Oregon commercial activity.

Chapter 3—Presentation Slides: Oregon Corporate Activity Tax (CAT)

3–1020th Annual Oregon Tax Institute

• Estimated payments can be calculated using “Worksheet OR-CAT” found on our website. Estimated payments can be made using one of these options:• Electronic payment using a credit or debit card on Revenue

Online.• By mail. If paying by mail, send each payment with a Form

OR-CAT-V voucher.• ACH Credit. Submit your application by going to Revenue

Online and clicking on ”Apply for ACH credit.”

Calculate and Pay Estimated Payments

19

• PLEASE NOTE• The department will not assess penalties for underestimating

quarterly payments in 2020 if the business has made a good faith effort to determine the required installment.

• Nor will the department assess a penalty for failure to make a quarterly payment if a business doesn't have the financial ability to make the estimated payment due to the impact of COVID-19.

Calculate and Pay Estimated Payments (cont.)

20

Chapter 3—Presentation Slides: Oregon Corporate Activity Tax (CAT)

3–1120th Annual Oregon Tax Institute

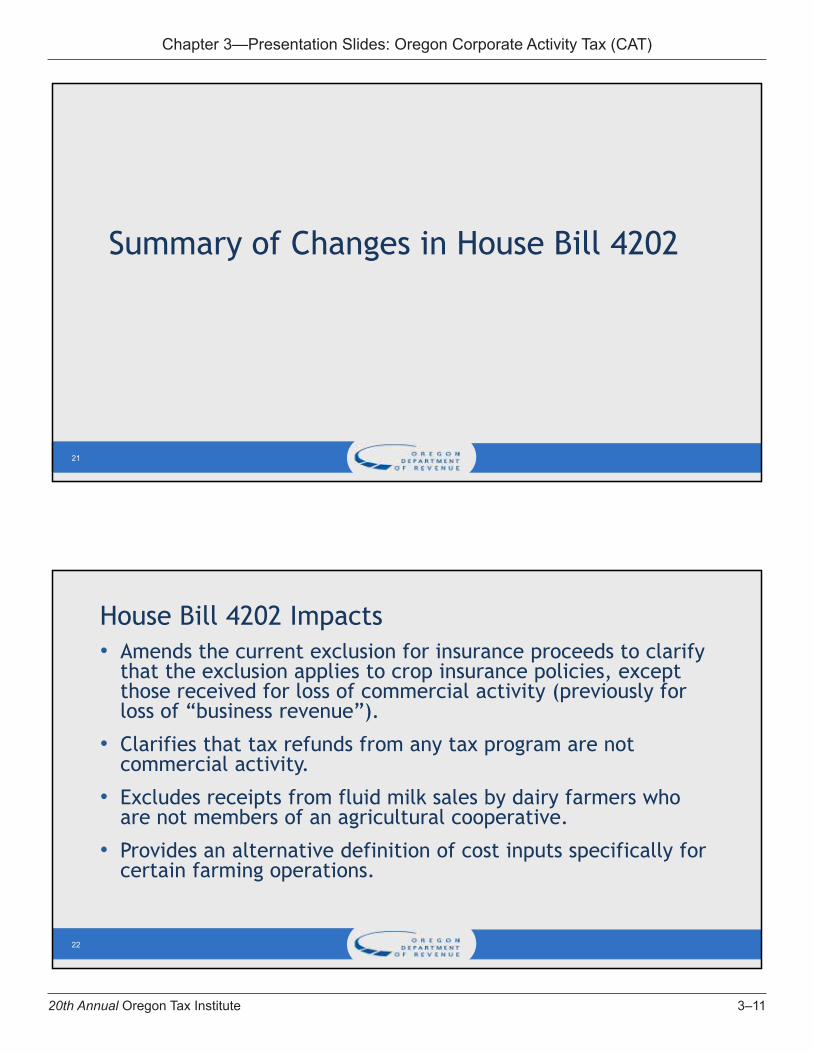

Summary of Changes in House Bill 4202

21

• Amends the current exclusion for insurance proceeds to clarify that the exclusion applies to crop insurance policies, except those received for loss of commercial activity (previously for loss of “business revenue”).

• Clarifies that tax refunds from any tax program are not commercial activity.

• Excludes receipts from fluid milk sales by dairy farmers who are not members of an agricultural cooperative.

• Provides an alternative definition of cost inputs specifically for certain farming operations.

House Bill 4202 Impacts

22

Chapter 3—Presentation Slides: Oregon Corporate Activity Tax (CAT)

3–1220th Annual Oregon Tax Institute

• Eliminates requirement that a taxpayer re-register for CAT annually, except under certain circumstances.

• Adds manufactured dwelling park non-profit cooperatives to the list of excluded entities.

• Allows CAT unitary group taxpayers to exclude certain members of the unitary group, provided the member has no commercial activity or other connection to Oregon.

• Clarifies the calculation method for purposes of the 35 percent subtraction of cost inputs or labor costs.

House Bill 4202 Impacts (cont.)

23

• Provides that a farming operation selling agricultural commodities to a wholesaler or broker may exclude receipts if the wholesaler or broker provides the farming operation with certification that the purchased commodities will be sold out of state. Alternatively, the farming operation may apply an industry average to estimate the portion that will be sold out of state.

• Reduces the penalty for underpayment of quarterly estimated payments to 5 percent, adds a safe harbor provision, and extends the 80 percent threshold for estimated quarterly payments through tax year 2021.

House Bill 4202 Impacts (cont.)

24

Chapter 3—Presentation Slides: Oregon Corporate Activity Tax (CAT)

3–1320th Annual Oregon Tax Institute

Administrative Rules

25

• Round 1: 17 permanent rules were effective June 18, 2020.

• Round 2: 4 Rules became permanent July 29, 2020.

• First fall rules process set October 27—December 2, 2020.

• Seven rules currently scheduled: Four amended rules, two new rules, and one temporary rule

• Second fall rules process starts November 24.

• Eight potential new rules to be effective January 1, 2021

Administrative rules

26

Chapter 3—Presentation Slides: Oregon Corporate Activity Tax (CAT)

3–1420th Annual Oregon Tax Institute

Sourcing of Commercial Activity

27

OAR 150-317-1030: Sales of Tangible Personal PropertySourced to Oregon if the property is delivered to a purchaser within Oregon.

• Regardless of F.O.B. point.

• Whether transported by seller, purchaser, or common carrier.

Exception: Throwback rules do not apply to CAT.

Sourcing of Commercial Activity

28

OAR 150-317-1040: Sales other than Tangible Personal Property

• Rules are similar to market-based sourcing.

• If leasing or renting property, it is sourced to Oregon if the property is in Oregon.

• If services are delivered to a location in Oregon

Chapter 3—Presentation Slides: Oregon Corporate Activity Tax (CAT)

3–1520th Annual Oregon Tax Institute

Sourcing of Commercial Activity

29

OAR 150-317-1050: Sourcing for Financial Institutions

• Sourced to Oregon if it is from business conducted in Oregon. E.g.,• Interest, fees, and penalties from loans not secured by real

property are sourced to Oregon if the borrower is located in Oregon.

• Credit card fees, interest, and penalties sourced to Oregon if the cardholder’s billing address is in Oregon.

Agent Exclusion

30

OAR 150-317-1100: Agent Exclusion

A person is an agent if the person acts on behalf of and subject to the control of another person (a principal).

• A determination of whether a person is acting as an agent is based on a consideration of the facts and circumstances surrounding the relationship between the agent and the principal.

• Property, money and other amounts received or acquired by an agent on behalf of another in excess of the agent’s commission, fee or other remuneration are excluded from commercial activity.

Chapter 3—Presentation Slides: Oregon Corporate Activity Tax (CAT)

3–1620th Annual Oregon Tax Institute

Retail and Wholesale Groceries

31

Receipts from the retail or wholesale sale of groceries are excluded.• Groceries means food and beverages for home consumption as defined for

the Supplemental Nutrition Assistance Program (SNAP).

• Groceries does not mean: Alcoholic beverages, tobacco, cannabinoid edibles, hot food for immediate consumption, or food that is hot at the point of sale.

• Must be a wholesale or retail sale (see OAR 150-317-1140 and 150-317-1150).

Retail Sales of Groceries

32

OAR 150-317-1150: Retail Sales of Groceries Exclusion

Requirement 1: The sale is of a grocery item as defined for SNAP.

Requirement 2: The seller typically intends/expects that the sale of the food is to the final consumer for home consumption. Factors considered:

• Average gross receipts from sale of groceries vs. receipts from the sale of hot food or prepared food.

• On-site dining facilities and percentage of floor space dedicated to dining vs. grocery shelving.

• Business advertising and marketing.

Note: The rule provides a safe harbor for stores authorized or qualifying as retail food stores for purposes of SNAP.

Chapter 3—Presentation Slides: Oregon Corporate Activity Tax (CAT)

3–1720th Annual Oregon Tax Institute

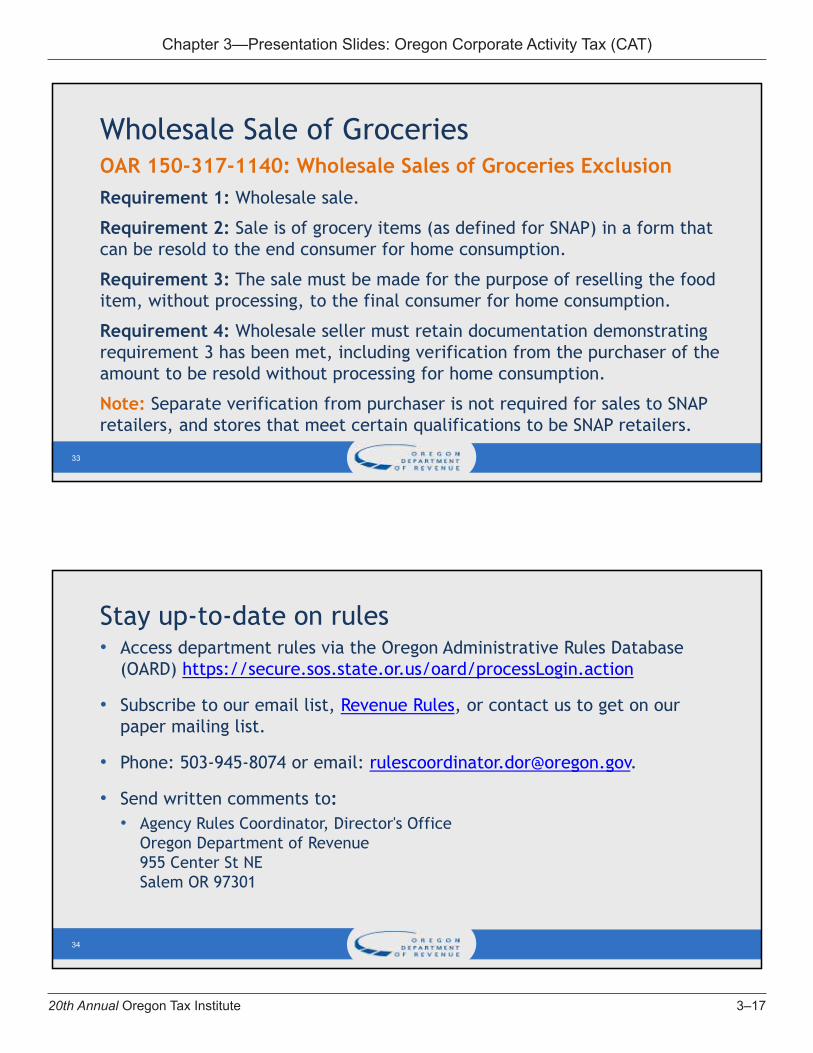

Wholesale Sale of Groceries

33

OAR 150-317-1140: Wholesale Sales of Groceries ExclusionRequirement 1: Wholesale sale.

Requirement 2: Sale is of grocery items (as defined for SNAP) in a form that can be resold to the end consumer for home consumption.

Requirement 3: The sale must be made for the purpose of reselling the food item, without processing, to the final consumer for home consumption.

Requirement 4: Wholesale seller must retain documentation demonstrating requirement 3 has been met, including verification from the purchaser of the amount to be resold without processing for home consumption.

Note: Separate verification from purchaser is not required for sales to SNAP retailers, and stores that meet certain qualifications to be SNAP retailers.

• Access department rules via the Oregon Administrative Rules Database (OARD) https://secure.sos.state.or.us/oard/processLogin.action

• Subscribe to our email list, Revenue Rules, or contact us to get on our paper mailing list.

• Phone: 503-945-8074 or email: [email protected].

• Send written comments to: • Agency Rules Coordinator, Director's Office

Oregon Department of Revenue955 Center St NESalem OR 97301

Stay up-to-date on rules

34

Chapter 3—Presentation Slides: Oregon Corporate Activity Tax (CAT)

3–1820th Annual Oregon Tax Institute

Additional Resources and How to Contact Us

35

• Visit our website for additional information about the CAT such as FAQs, Beyond the FAQs, and links to items such as our rules page, payment information, and more.

https://www.oregon.gov/dor/programs/businesses/Pages/corporate-activity-tax.aspx

Resources Available

36

Chapter 3—Presentation Slides: Oregon Corporate Activity Tax (CAT)

3–1920th Annual Oregon Tax Institute

• General questions and taxpayer assistance:

• Email: [email protected].

• Call 503-945-8005 8 a.m.—4 p.m. Monday-Friday.

• Follow us on Twitter at @ORRevenue, #oregonCAT.

• You can also subscribe to our mailing list via our website to receive additional information as it becomes available.

Additional CAT Resources

37

38

Questions?

Chapter 3—Presentation Slides: Oregon Corporate Activity Tax (CAT)

3–2020th Annual Oregon Tax Institute