option_greeks

TRANSCRIPT

1

Image page

INTRODUCTION TO OPTION GREEKS

Rates, Commodities & FX Derivative Application

Specialists

FX DERIVATIVES

Abukar Ali (2015)

2

Bulletedpage

Gamma, Delta, Theta, Vega,....and Rho

Option Sensitivities:

THE GREEKS

3

Bulletedpage

• When a bank trades a derivative, it should understand all the

risks associated with the product and hedge its position

accordingly

• Once the sale is done, the product is added to an existing

book of options, and it is the book that must be risk

managed.

• In order to see where the risks lie, the trader hedging a

derivative will need to know the sensitivity of the

derivative’s price to the various parameters that impact its

value.

• The sensitivities of an option’s price, also known as hedge

ratios, are commonly referred to as the GREEKS since

many of them are labelled and referred to by Greek letters

4

Bulletedpage

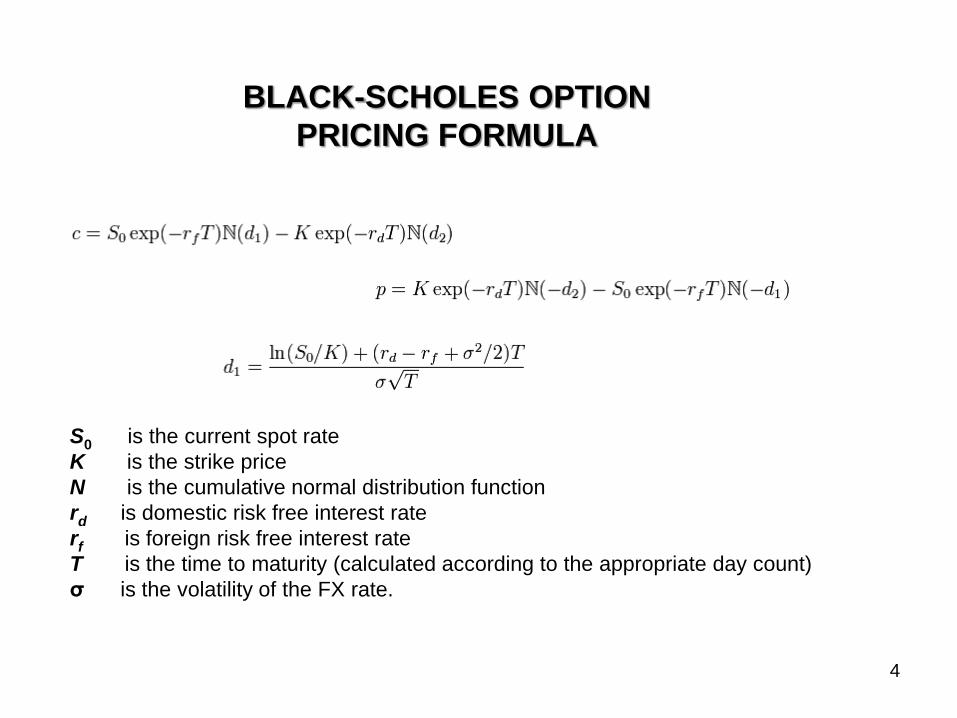

BLACK-SCHOLES OPTION

PRICING FORMULA

S0 is the current spot rate

K is the strike price

N is the cumulative normal distribution function

rd is domestic risk free interest rate

rf is foreign risk free interest rate

T is the time to maturity (calculated according to the appropriate day count)

σ is the volatility of the FX rate.

5

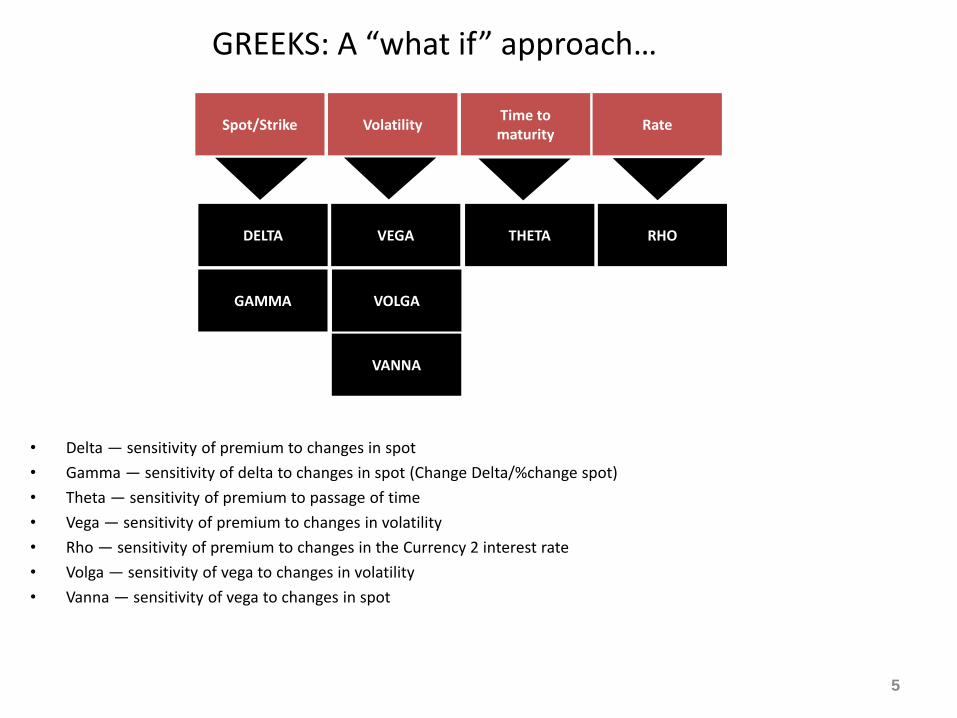

GREEKS: A “what if” approach…

Spot/StrikeTime to maturity

Volatility Rate

DELTA THETAVEGA RHO

GAMMA VOLGA

VANNA

• Delta — sensitivity of premium to changes in spot

• Gamma — sensitivity of delta to changes in spot (Change Delta/%change spot)

• Theta — sensitivity of premium to passage of time

• Vega — sensitivity of premium to changes in volatility

• Rho — sensitivity of premium to changes in the Currency 2 interest rate

• Volga — sensitivity of vega to changes in volatility

• Vanna — sensitivity of vega to changes in spot

6

Blach-Scholes

Values Spot Volatility

Time to

Expiry

Interest

Rate

Option Price Delta Vega Theta Rho

Delta Gamma Vanna Charm

Gamma Speed Zomma Color

Vega Vanna Volga DvegaDtime

Partial Derivatives of the BSM Model

Vanna: partial derivative of delta wrp to volatility (DdeltaDvol)

Volga: partial derivative of vega wrp to volatility (DvegaDvol)

7

Hiring a trader is a like selling volatility. If he does very well or very poorly,

you are out of a job. An old option proverb

DELTA (Aka Hedge Ratio)

• Approximately, delta can be expressed as:

(change in the option price / change in underlying exchange rate)

• Delta is the underlying a trader would hedge against a particular

option to cover the spot sensitivity.

• Example: approximate delta

• [(150.00 - 100.00) / 1000 ] / [ 1.2394 - 1.2294] = 0.5000

An option’s price sensitivity to price changes in the underlying instrument is known as its delta

8

DELTA

• Consider a EUR/USD position, Call on EUR / Put on USD, Notional EUR

10,000,000. Strike = ATMF, Expiring 04/29/2012.

• Delta (spot) = 51.100%

• To hedge the risk against losses due to underlying move, the trader needs

to buy/sell equivalent of:

(51.100/100)*10,000,000 = EUR 5,110,000

Example:

A trader sells EUR PUT USD CALL , notional = EUR10,000,000 expiry in 6

Months. the traders risk is that in 6 months, the option is exercised and

there will be a payout of dollars and receipts of EUR. The trader’s hedge

against this risk would therefore be to buy USD and sell EUR, thus

hedging the delta amount because this represents the likely hood of

exercise.

Example 2 over: Trader sells 35delta Put Option, what is his initial hedge?

9

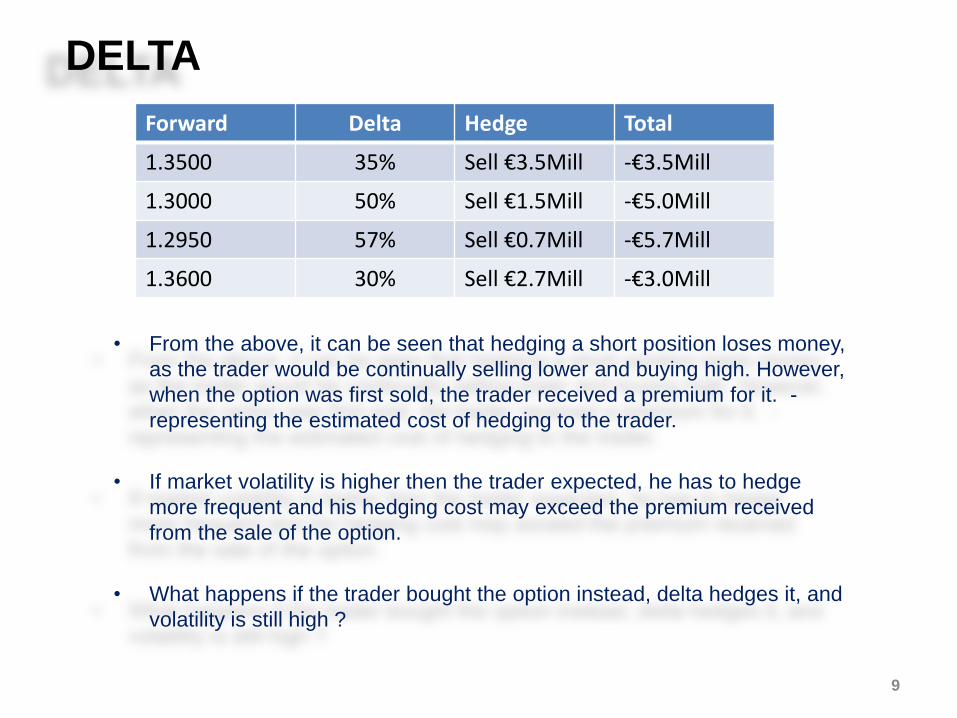

DELTA

• From the above, it can be seen that hedging a short position loses money,

as the trader would be continually selling lower and buying high. However,

when the option was first sold, the trader received a premium for it. -

representing the estimated cost of hedging to the trader.

• If market volatility is higher then the trader expected, he has to hedge

more frequent and his hedging cost may exceed the premium received

from the sale of the option.

• What happens if the trader bought the option instead, delta hedges it, and

volatility is still high ?

Forward Delta Hedge Total

1.3500 35% Sell €3.5Mill -€3.5Mill

1.3000 50% Sell €1.5Mill -€5.0Mill

1.2950 57% Sell €0.7Mill -€5.7Mill

1.3600 30% Sell €2.7Mill -€3.0Mill

10

Exactly the same option but this

time Volatility is set at 50%

EUR/USD, 3M, EUR=1M, STRIKE = ATMF, VOL , VOL = 12% (BID/ASK)

DELTA characteristics.

• On a call option, delta will range from 0% when OTM to 50% ATM

then to 100% when deep ITM. What about delta of a put option ?

11

Bulletedpage

Conclusion

• Delta will change if any of the factors influencing the option

changes.

• Delta tend to increase as it gets closer to expiration for near

or at the money options.

• Delta is not constant; and

• Delta is subject to change given changes in implied

volatility

12

Bulletedpage

One day in mid 1994, the dealing rooms in the united states were rocked

with the new of the bankruptcy of a hedge fund, costing a minimum of

$600 millions to their investors. What worried the community was that

the blown-up fund was meant to be “market neutral.” …….

In theory the fund would warehouse cheap securities, hedge them, and

achieve above-average returns for the Florida residents.

One trader was asked by his manager to explain the results. He shouted:

“That guy did not get the second derivative right.”

Taken from N.Taleb’s Dynamic Hedging book.

13

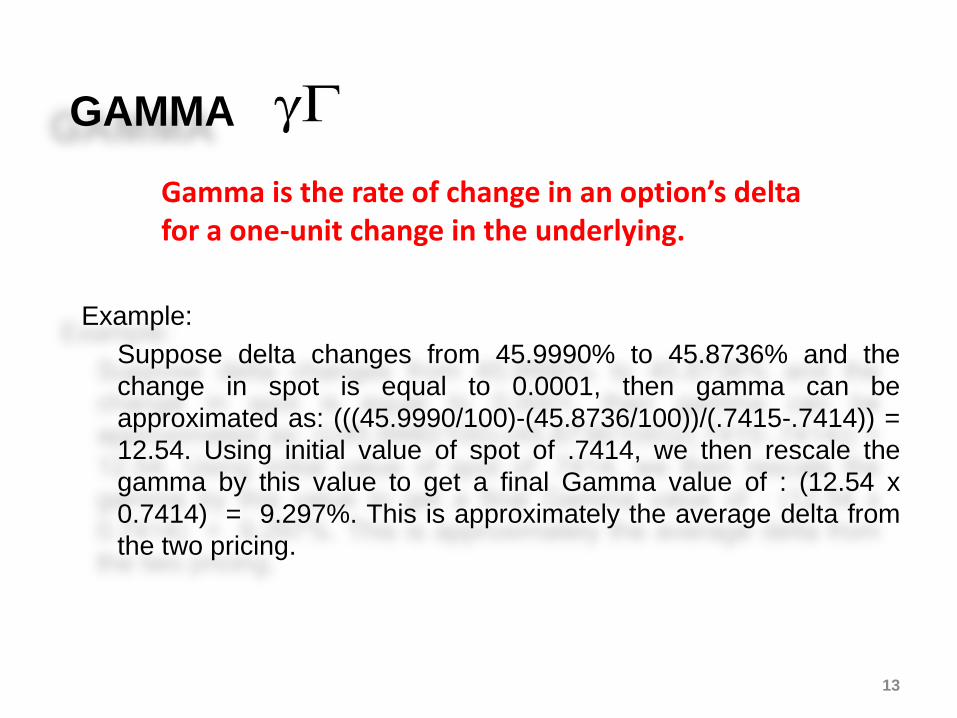

GAMMA

Example:

Suppose delta changes from 45.9990% to 45.8736% and the

change in spot is equal to 0.0001, then gamma can be

approximated as: (((45.9990/100)-(45.8736/100))/(.7415-.7414)) =

12.54. Using initial value of spot of .7414, we then rescale the

gamma by this value to get a final Gamma value of : (12.54 x

0.7414) = 9.297%. This is approximately the average delta from

the two pricing.

Gamma is the rate of change in an option’s delta for a one-unit change in the underlying.

14

Bulletedpage

GAMMA

• Gamma provides estimates of how much it will cost to delta hedge.

• An option’s Gamma is at its greatest when an option is ATM and decreases

as the price of the underlying moves further away from the strike price.

• Gamma is greater for short-term options then long-term options

• Gamma is positive for long options and negative for short options

BY convention, Gamma can be expressed in two ways:

• A Gamma of say 5.0 will mean that for a 1% change in the underlying price,

the delta will change by 5.00 units, that is from 50% to 55.00%; and

• A Gamma of 3% will mean for a one unit change in the underlying price, the

delta will change by 3%, for example, from 50% to 51.5%

GAMMA• Gamma - the rate of change in delta per unit change in the price of the underlying.

This rate of change of delta, given a change in spot can be as written as;

• Gamma is at its highest for vanilla options when spot trades around 50delta, the slope of the Delta change is at its steepest.

15

16

Vanilla (Long & Short Gamma): EUR/USD, 3M, EUR=1M, STRIKE = ATMF, VOL

GAMMA

.

17

Bulletedpage

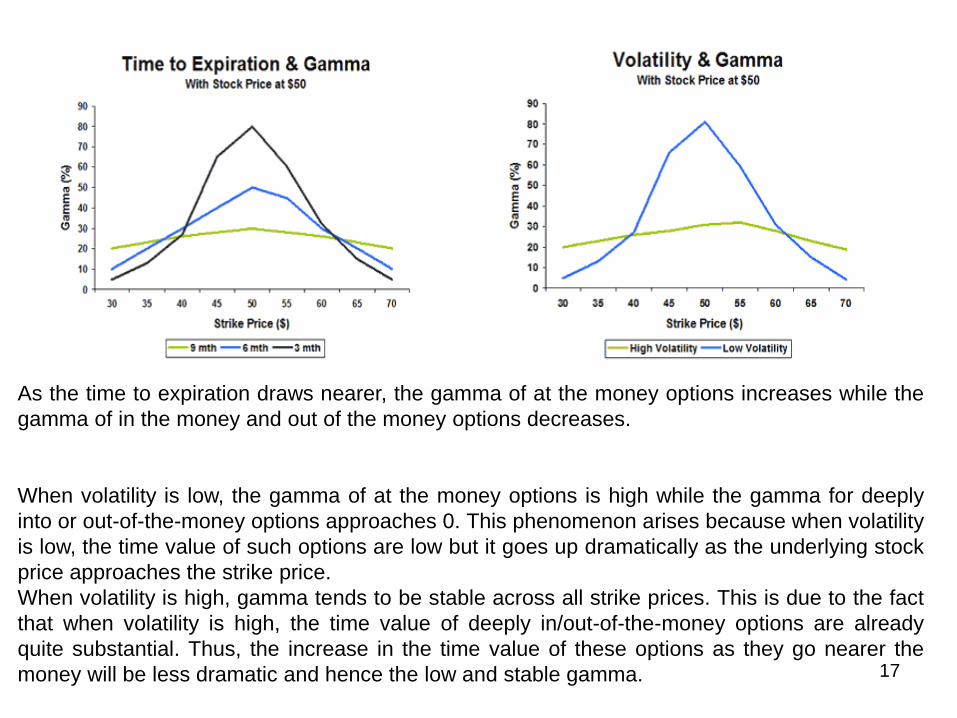

As the time to expiration draws nearer, the gamma of at the money options increases while the

gamma of in the money and out of the money options decreases.

When volatility is low, the gamma of at the money options is high while the gamma for deeply

into or out-of-the-money options approaches 0. This phenomenon arises because when volatility

is low, the time value of such options are low but it goes up dramatically as the underlying stock

price approaches the strike price.

When volatility is high, gamma tends to be stable across all strike prices. This is due to the fact

that when volatility is high, the time value of deeply in/out-of-the-money options are already

quite substantial. Thus, the increase in the time value of these options as they go nearer the

money will be less dramatic and hence the low and stable gamma.

18

I prefer the judgement of a 55-year old trader to that of a 25-year old

mathematician Alan Greenspan

THETA

The option's theta is a measurement of the option's time decay. The theta

measures the rate at which options lose their value, specifically the time value, as

the expiration date draws nearer. Generally expressed as a negative number, the

theta of an option reflects the amount by which the option's value will decrease

every day.

Example:

A call option with a current price of EUR 53,300 and a theta of EUR100 will

experience a drop in price of EUR -100 per day. So in two days' time, the price of

the option should fall to EUR 53,200.

The theta is a loss in time value of an option portfolio that results from the passage of time.

19

Vanilla (Short & Long Theta): EUR/USD, 3M, EUR=1M, STRIKE = ATMF, VOL

THETA characteristics.

20

Bulletedpage

Theta

• Long term options have theta of almost zero as they do not lose value on a

daily basis.

• Theta is higher for short dated options, especially ATM options (this is due to

the fact that such options have highest time value and thus have more

premium to lose each day)

• Theta goes up as the option near the expiration as time decay is at its

greatest during that period.

21

Bulletedpage

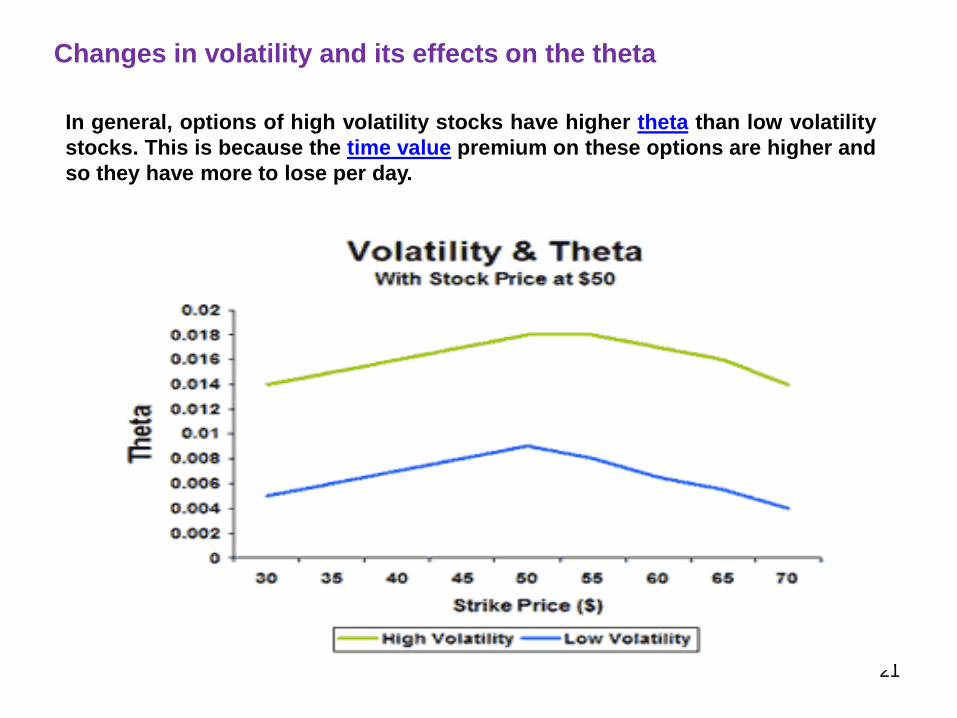

Changes in volatility and its effects on the theta

In general, options of high volatility stocks have higher theta than low volatility

stocks. This is because the time value premium on these options are higher and

so they have more to lose per day.

Vega• Vega- the change in the option’s price for a 1% change in volatility.

•

• Vega is highest for ATM options and increases for options that have longer dated expires.

• Second order derivatives on Vega include Volga and Vanna. • Volga, is the change of Vega given a change in volatility, noticeable in a long wing position

where as volatility increase the probability of exercise increases making the options closer to ATM, increasing the Vega.

• Vanna, is the change of Vega given the change in spot, noticeable with a risk reversal as spot moves towards the Long position and away from the short position the Vega will increase and vice-versa.

• OVML Vega Chart 22

Vega• Vega does not move in a linear fashion along the curve. When the market

moves aggressively often participants look to buy back short-dated options (Gamma) first pushing up the front of curve more than the back

• Portfolio has €100m long 3month against €100m short 1 year. Clearly there is more Vega in the 1 year but Weighted Vega that takes into account the market observation of the tail wagging the dog and after we make the adjustment by time value. The Vega position is similar.

• XLTP and OVRA (Weighted Vega)23

1W 2W 3W 1M 2M 3M 6M 1Y 2Y 3Y

Imp

lied

Vo

lati

litie

s

Tenor

Current Implied Volatility Maximum Minimum

Vanna – Volga( 2nd order vega risk sensitivity )

Change in vega with respect to the

underlying spot

For simple vanillas Risk Reversals

exhibit the highest vanna

Vanna (dvega/dspot)

Spot

Spot

Profit

Vega

Long

VolatilityShort

Volatility

Volga (dvega/dvol)

Change in vega with respect to the

volatility

For simple vanillas, Butterflies

exhibit the highest volga

Normal Dist.

When volatility

increases, tail

vega risk

increases faster

In other words, the vega of low delta strikes changes

faster than ATM strikes, i.e. higher volga

Calculate change of vega for a RR by

changing spot (±1%). Vanna is the %

change of vega with respect to spot

Strike

ATM

Vo

lga

Calculate change of vega for a BF by

changing vol curve (±1%). Volga is the %

change of vega with respect to vol.

RECAP: Buying a vanilla call ….notice the Greeks

GammaDelta

Vega Volga