optimal+portfolios+dq 2008s1

TRANSCRIPT

8/13/2019 Optimal+Portfolios+DQ 2008s1

http://slidepdf.com/reader/full/optimalportfoliosdq-2008s1 1/2

1

Session 7: Locating the ORP & OBPA.

The expected return and risk of a portfolio of risky assets, E(RP) and σ P, areexpressed as:

( ) ( )in

i

iP r E w R E ∑=

=1

,

21

1 11

22

⎟⎟⎟

⎠

⎞

⎜⎜⎜

⎝

⎛

+= ∑∑∑=

≠==

n

i

n

ji j

ij ji

n

i

iiP www σ σ σ

where wi and w j are the weights allocated to the respective risky assets,the total weight is one,E(r i) the expected return on risky asset i,n the total number of risky assets in the portfolio,

σ i the standard deviation of returns of risky asset i, and

σ ij the covariance of returns between risky assets i and j.

For a balanced portfolio, the expected return and risk, E(RB) and σ B, areexpressed as:

( ) ( ) ( ) f PPP B

r y R E y R E −+= 1 , ( ) ( ) PPr PPPr PPP B y y y y y f f

σ σ σ σ σ =−+−+= ,

2222 121

where yP is the weight allocated to the portfolio of risky assets,

B.When risk free lending and borrowing are not available, investors choose theportfolio of risky assets offering the highest utility.

Among all the portfolio of risky assets lying on the efficient frontier, investorschoose the one that touches their indifference curves tangentially.

IC’’’Expected return IC’’ ORPLRA efficient frontier

IC’Optimal risky portfolio for a less risk averse

ORPMRA P investor with a smaller A and gently sloped indifference curve

Optimal risky portfolio for a more risk averse investor with a larger A and steeper indifference curves

Standard deviation of returns

8/13/2019 Optimal+Portfolios+DQ 2008s1

http://slidepdf.com/reader/full/optimalportfoliosdq-2008s1 2/2

2

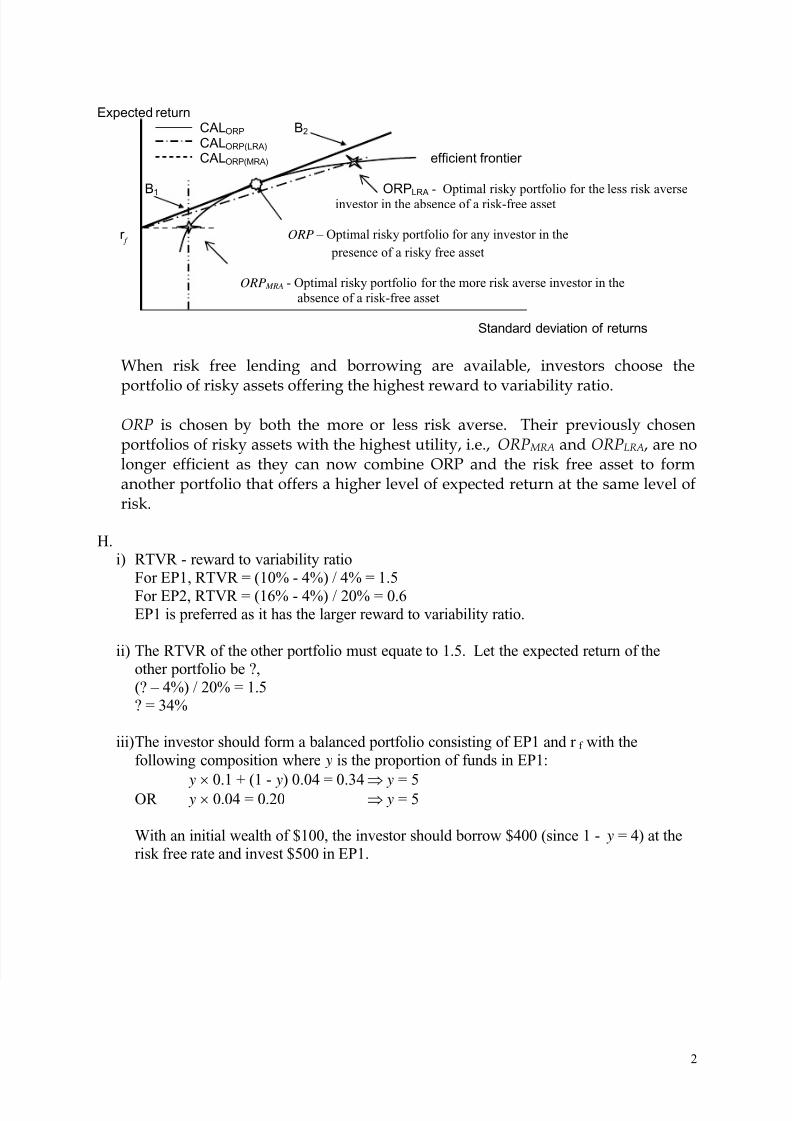

Expected returnCALORP B2 CALORP(LRA) CALORP(MRA) efficient frontier

B1 ORPLRA - Optimal risky portfolio for the less risk averseinvestor in the absence of a risk-free asset

r f ORP – Optimal risky portfolio for any investor in the

presence of a risky free asset

ORP MRA - Optimal risky portfolio for the more risk averse investor in theabsence of a risk-free asset

Standard deviation of returns

When risk free lending and borrowing are available, investors choose the

portfolio of risky assets offering the highest reward to variability ratio.

ORP is chosen by both the more or less risk averse. Their previously chosenportfolios of risky assets with the highest utility, i.e., ORP MRA and ORPLRA, are nolonger efficient as they can now combine ORP and the risk free asset to formanother portfolio that offers a higher level of expected return at the same level ofrisk.

H.i) RTVR - reward to variability ratio

For EP1, RTVR = (10% - 4%) / 4% = 1.5For EP2, RTVR = (16% - 4%) / 20% = 0.6EP1 is preferred as it has the larger reward to variability ratio.

ii) The RTVR of the other portfolio must equate to 1.5. Let the expected return of theother portfolio be ?,(? – 4%) / 20% = 1.5? = 34%

iii) The investor should form a balanced portfolio consisting of EP1 and r f with thefollowing composition where y is the proportion of funds in EP1:

y × 0.1 + (1 - y) 0.04 = 0.34⇒ y = 5OR y × 0.04 = 0.20 ⇒ y = 5

With an initial wealth of $100, the investor should borrow $400 (since 1 - y = 4) at therisk free rate and invest $500 in EP1.