optimal control for jump processes, hjb...

TRANSCRIPT

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Optimal control for jump processes,HJB equations

Jakub Petrasek

Department of Probability and Mathematical StatisticsFaculty of Mathematics and Physics, Charles University in Prague

Seminar in Stochastic Modelling in Economics and Finance

January 10, 2011

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Outline

1 IntroductionMotivationLevy processes

2 Optimal ControlModel set-upDynamic programming principle

3 ApplicationFormulation of problemApplication of dynamic programming principleComparison with no-jump case

4 Maximmum principleModel set-upOptimality conditionRelation to dynamic programming

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Outline

1 IntroductionMotivationLevy processes

2 Optimal ControlModel set-upDynamic programming principle

3 ApplicationFormulation of problemApplication of dynamic programming principleComparison with no-jump case

4 Maximmum principleModel set-upOptimality conditionRelation to dynamic programming

1

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Economic model

At each t ≥ 0 an agent owns a capital Xt by investing in two assets

a riskfree bond that pays interest rate r ,

dBt = rBtdt.

a risky asset with dynamics (geometric Brownian motion +jumps)

dSt = S(t−)

(αdt + σdWt +

∫ ∞−1

zN(dt,dz)

).

At each t ≥ 0 an agent controls

the number of stocks ∆t in his portfolio,

and possibly consumption Ct .

2

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Admissible strategies

Definition

A strategy (∆t , t ≥ 0) is admissible if

1 it is predictable,

2 the portfolio (Xt , t ≥ 0) is self-financing, i.e.

dXt = ∆tdSt + (Xt −∆tSt)dBt .

We denote the set of admissible strategies by A(x) for a given capitalX0 = x .

We can substitute for dSt and dBt and obtain

dXt = ∆tSt−

((α− r)dt + σdWt +

∫ ∞−1

zN(dt,dz)

)+ rXtdt.

3

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Objective of investment

The objective of an agent is to maximize his utility from investmentsby using admissible strategies ∆t(∆t ,Ct). His aim is

1 to maximize his consumption over infinite horizon

sup(∆t ,Ct)∈A(x)

∫ ∞0

e−βtE U(Ct)dt, (1.1)

where β is a discount factor

2 to maximize his terminal utility of terminal wealth in a givenhorizon T

sup∆t∈A(x)

E U(XT ), (1.2)

3 combination of the first two

sup(∆t ,Ct)∈A(x)

E U(XT ) +

∫ T

0

e−βtE U(Ct)dt

. (1.3)

4

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Levy process - definition

Definition

Let(

Ω,F , Ftt≥0 ,P)

be a filtered probability space. An adapted

process Lt is called a Levy process if it is continuous in probabilityand has stationary, independent increments.

TheoremLet Lt be a Levy process. Then Lt has the decomposition

Lt = b + σWt +

∫|z|≤1

zN(t, dz) +

∫|z|>1

zN(t, dz), 0 ≤ t <∞.(1.4)

where b ∈ R, σ ≥ 0, (N) N is a (compensated) Poisson randommeasure with a Levy measure ν, all adapted to filtration Ftt≥0.

5

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Levy process - Ito formula

Theorem (Ito formula)

Suppose Lt ∈ R is an Levy process of the form

dLt = bdt + σdWt +

∫ ∞−1

zN(t, dz).

Let f ∈ C1,2(R+ × R) and define Yt = f (t, Lt). Then Yt is again anLevy process and

dYt = ft(t, Lt)dt + fx(t, Lt) (bdt + σdWt) +1

2fxx(t, Lt)σ2dt

+

∫ ∞−1

(f (t, Lt− + z)− f (t, Lt−)) N(dt, dz)

+

∫ ∞−1

(f (t, Lt− + z)− f (t, Lt−)− fx(t, Lt−)z) ν(dz)dt.

6

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Levy process - Generator

Definition

Suppose f : R2 → R. Then the generator A of process Lt (from theprevious theorem) is defined as

Af (s, x) = limt→0+

1

tE [f (s + t, Ls+t)− f (s, x)] ,

where Ls = x .

Theorem

Suppose f ∈ C1,2(R+ × R). Then Af (s, x) exists and

Af (s, x) = ft(s, x) + fx(s, x)b +1

2fxx(s, x)σ2

+

∫ ∞−1

(f (s, x + z)− f (s, x)− fx(s, x)z) ν(dz).

7

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Outline

1 IntroductionMotivationLevy processes

2 Optimal ControlModel set-upDynamic programming principle

3 ApplicationFormulation of problemApplication of dynamic programming principleComparison with no-jump case

4 Maximmum principleModel set-upOptimality conditionRelation to dynamic programming

8

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

State process

Yt = Y(u)t is a stochastic process (on filtered probability space) with

dynamics

dYt = b(Yt , ut)dt + σt(Yt , ut)dWt +

∫Rγ(Yt− , ut− , z)N(dt,dz),

Y0 = y ∈ Rk

where

b : Rk ×U → Rk , σ : Rk ×U → Rk×m, γ : Rk ×U ×Rk → Rk×l

are given functions (time homogenous), W is Wiener process (on the

given probability space), N compensated Poisson random measureand U ⊂ Rp given set.

u(t) = u(t, ω) : R+ × Ω→ U

is predictable control process and Yt = Y(u)t is a controlled

jump-diffusion.9

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Performance criterion

For a fixed T (possibly T =∞) we define

J(u)(y) = E

[∫ T

0

f (Yt , ut)dt + g(YT )

],

wheref : S × U → R, g : Rk → R

are given continuous functions, S is called solvency region.

DefinitionControl u is admissible, denote u ∈ A if the state process has aunique, strong solution for all x ∈ S and

E

[∫ T

0

f (Yt , ut)dt + g(YT )

]<∞.

10

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

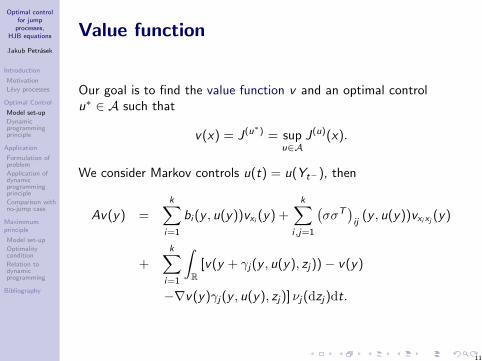

Value function

Our goal is to find the value function v and an optimal controlu∗ ∈ A such that

v(x) = J(u∗) = supu∈A

J(u)(x).

We consider Markov controls u(t) = u(Yt−), then

Av(y) =k∑

i=1

bi (y , u(y))vxi (y) +k∑

i,j=1

(σσT

)ij

(y , u(y))vxixj (y)

+k∑

i=1

∫R

[v(y + γj(y , u(y), zj))− v(y)

−∇v(y)γj(y , u(y), zj)] νj(dzj)dt.

11

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Revision

If we start the state process from any t ∈ [0,T − h] it holds

v(Yt) ≥ E

[∫ t+h

t

f (Ys , u(Ys))ds + v(Y(u)t+h)

](2.1)

with equality for u∗ = u. We know that

E tv(Y(u)t+h) = v(Yt) +

∫ t+h

t

A(u)v(Ys)ds

and by substitution into (2.1) we obtain

0 ≥ E

[∫ t+h

t

(f (Ys , u(Ys)) + A(u)v(Ys)

)ds

]

or in differential0 ≥ f (y , u(y)) + A(u)v(y),

for any u and equality holds for u = u∗.12

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

HJB for optimal control of jump diffusion

Lemma (Verification lemma)

Let v ∈ C1,2 satisfies the following

1 limt→T v(Yt) = g(YT )

2 For any u ∈ A(x)

f (y , u(y)) + A(u)v(y) ≤ 0.

3 There is u ∈ A(y) such that

f (y , u(y)) + A(u)v(y) = 0.

Thenu = u∗.

andv(y) = v(y) = J(u∗)(y), for any y ∈ S.

13

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Remarks

Verification theorem holds also for random time T however withadditional requirements.

Example

T = inf t > 0,Yt /∈ S

The Hamilton-Jacobi-Bellman equation provides ”only”sufficient condition for an optimum, but not necessary, which isprovided by Pontryagin Maximum principle.

14

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Outline

1 IntroductionMotivationLevy processes

2 Optimal ControlModel set-upDynamic programming principle

3 ApplicationFormulation of problemApplication of dynamic programming principleComparison with no-jump case

4 Maximmum principleModel set-upOptimality conditionRelation to dynamic programming

15

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Investor’s question

We refer back to the motivation example. An investor puts hismoney into risky St and riskless Bt asset. His portfolio Xt evolves

dXt = ∆tSt−

((α− r)dt + σdWt +

∫ ∞−1

zN(dt,dz)

)+rXtdt−ctXtdt.

and he wants to maximize utility from his consumption

sup(∆t ,Ct)∈A(x)

∫ ∞0

e−βtE U(Ct)dt, (3.1)

Investor knows that his utility is given by the power utility function,i.e.

U(x) =x1−p

1− p, p > 0, p 6= 1,

= log(x), p = 1.

16

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

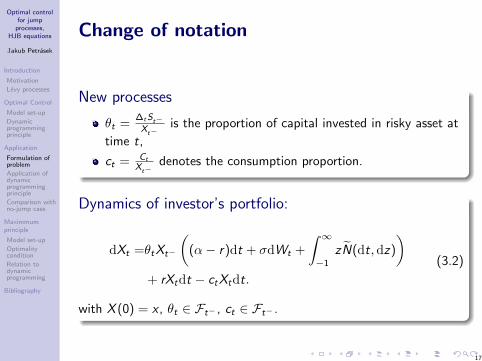

Change of notation

New processes

θt =∆tSt−Xt−

is the proportion of capital invested in risky asset at

time t,

ct = Ct

Xt−denotes the consumption proportion.

Dynamics of investor’s portfolio:

dXt =θtXt−

((α− r)dt + σdWt +

∫ ∞−1

zN(dt,dz)

)+ rXtdt − ctXtdt.

(3.2)

with X (0) = x , θt ∈ Ft− , ct ∈ Ft− .

17

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Computation of generator

We would like to apply the verificatin lemma on the controlledprocess Yt = (t,Xt)T , with Y0 = (0, x)T .

Generator of v(Yt)

A(u)v(y) = vt + ((α− r)θ + r − c) xvx +1

2σ2θ2x2vxx

+

∫ ∞−1

(v(t, x + xθz)1−p − v(t, x)− θzvx

)ν(dz).

’Consumption’

f (y , u(y)) = e−βtU(cx).

18

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

PDE

We guess the form of the value function, v(t, x) = Ke−βtx1−p

A(u)v(y) = Ke−βtx1−p [−β + ((α− r)θ + r − c) (1− p)

− 1

2σ2θ2p(1− p)

+

∫ ∞−1

((1 + θz)1−p − 1− θz(1− p)

)ν(dz)

]= Ke−βtx1−p [−β + (r − c) (1− p) + h(θ)] .

A(u)v(y) + f (y , u(y))

= Ke−βtx1−p

[−β + (r − c)(1− p) + h(θ) +

c1−p

K (1− p)

].(3.3)

19

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

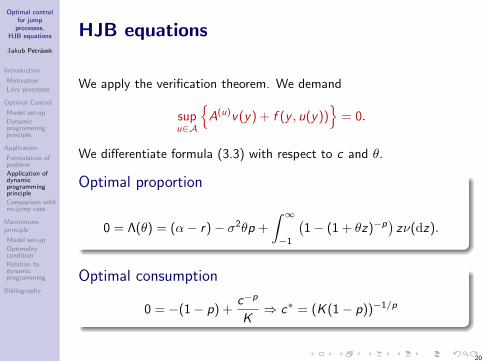

HJB equations

We apply the verification theorem. We demand

supu∈A

A(u)v(y) + f (y , u(y))

= 0.

We differentiate formula (3.3) with respect to c and θ.

Optimal proportion

0 = Λ(θ) = (α− r)− σ2θp +

∫ ∞−1

(1− (1 + θz)−p

)zν(dz).

Optimal consumption

0 = −(1− p) +c−p

K⇒ c∗ = (K (1− p))−1/p

20

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

HJB equations

Constant K

Finally we substitute θ∗ and c∗ into equation (3.3) and demandequality to zero

0 = A(u∗)v(y) + f (y , u∗(y))

0 = Ke−βtx1−p [−β + r(1− p) + h(θ∗)

− K−1/p(1− p)−1/p+1 + (K (1− p))−1/p]

= Ke−βtx1−p[−β + r(1− p) + h(θ∗)− p (K (1− p))−1/p

]

⇒ nontrivial solution is

K =1

1− p[β − r(1− p)− h(θ∗)p]−p

.

21

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

HJB equations

Theorem (Optimal Proportion and Consumption)

Assume the portfolio (3.2) and the objective. Let

Λ(θ∗) = 0

andβ − r(1− p)− h(θ∗) > 0.

Then

θ∗ is the optimal proportion,

c∗ = (K (1− p))−1/p

v(0, x) = Kx1−p is the value function,

where

K =1

1− p[β − r(1− p)− h(θ∗)p]−p

. (3.4)

22

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

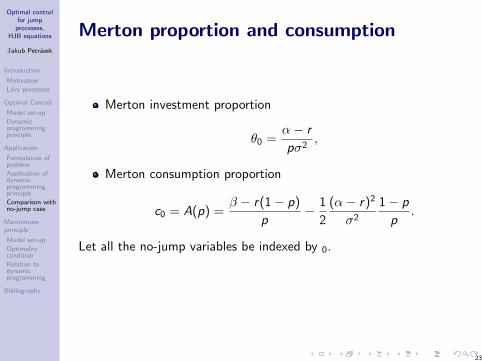

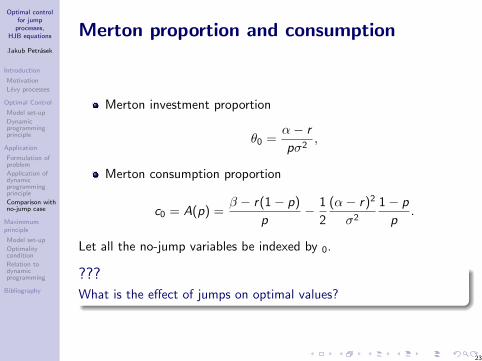

Merton proportion and consumption

Merton investment proportion

θ0 =α− r

pσ2,

Merton consumption proportion

c0 = A(p) =β − r(1− p)

p− 1

2

(α− r)2

σ2

1− p

p.

Let all the no-jump variables be indexed by 0.

???What is the effect of jumps on optimal values?

23

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Merton proportion and consumption

Merton investment proportion

θ0 =α− r

pσ2,

Merton consumption proportion

c0 = A(p) =β − r(1− p)

p− 1

2

(α− r)2

σ2

1− p

p.

Let all the no-jump variables be indexed by 0.

???What is the effect of jumps on optimal values?

23

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Optimal (jumps included) proportion andconsumption

Optimal proportion θ∗ solves the equation

Λ(θ∗) = (α− r)− σ2θp +

∫ ∞−1

(1− (1 + θz)−p

)zν(dz) = 0.

Optimal consumption

c∗ = (K (1− p))−1/p

for a constant K given by equation (3.4).

24

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Function Λ

We know that for Λ0(θ) solves the Merton problem and can see that

1

Λ(0) = α− r ,

Λ(θ) is a decreasing function of θ.

2 Function (1− (1 + θz)−p) z is positive for z ∈ (−1/θ,∞).

We conclude thatΛ(θ) < Λ0(θ).

Corollary

θ∗ ≤ θ0,

v ≤ v0,

c∗ ≤ c0, p > 1,

c∗ ≥ c0, 0 < p < 1.

25

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Comparison with Merton cont.

x1 (money units in St)

x2 (money units in Bt)

the Merton line (ν = 0)

risk increasing jumps

(x1 = θ01−θ0x2)

S

S

risk decreasing jumps

26

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Approximation of small jumps

Let us suppose that the measure ν has light tails (jumps are small inabsolute value). We can use the taylor expansion

1− (1 + θz)−p = pzθ + o(z2)

and after the substitution into Λ

θ∗ ≈ 1

p

α− r

σ2 +∫∞−1

z2ν(dz),

i.e. for smaller jumps we can approximate Levy process by a

Brownian motion with volatility√σ2 +

∫∞−1

z2ν(dz).

27

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Investor’s question II

An investor wants to maximize his utility from the terminal wealth

sup∆t∈A(x)

E U(XT ) (3.5)

Optimal strategy

It is optimal to put constant proportion θ∗ of his money into the riskyasset, same as in the previous.

28

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Outline

1 IntroductionMotivationLevy processes

2 Optimal ControlModel set-upDynamic programming principle

3 ApplicationFormulation of problemApplication of dynamic programming principleComparison with no-jump case

4 Maximmum principleModel set-upOptimality conditionRelation to dynamic programming

29

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Maximum principle - intro

Alternative approach for solving optimal control.In the deterministic case introduced by Russian mathematicianLev Pontryagin.

State process

Xt = X(u)t with dynamics

dXt = b(t,Xt , ut)dt+σt(t,Xt , ut)dWt+

∫Rγ(t,Xt− , ut− , z)N(dt,dz).

Objective

J(u) = E

[∫ T

0

f (t,Xt , ut)dt + g(XT )

],

for T <∞ deterministic, f continuous, g concave. We want to findan admissible policy u∗ ∈ A such that

J(u∗) = supu∈A

J(u).

30

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

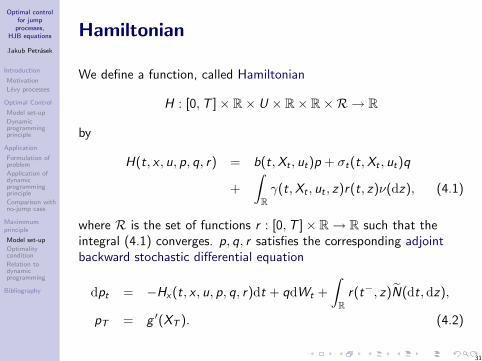

Hamiltonian

We define a function, called Hamiltonian

H : [0,T ]× R× U × R× R×R → R

by

H(t, x , u, p, q, r) = b(t,Xt , ut)p + σt(t,Xt , ut)q

+

∫Rγ(t,Xt , ut , z)r(t, z)ν(dz), (4.1)

where R is the set of functions r : [0,T ]× R→ R such that theintegral (4.1) converges. p, q, r satisfies the corresponding adjointbackward stochastic differential equation

dpt = −Hx(t, x , u, p, q, r)dt + qdWt +

∫R

r(t−, z)N(dt,dz),

pT = g ′(XT ). (4.2)

31

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Optimality condition

Let u, u∗ ∈ A and let X ∗t = X(u∗)t , Xt = X

(u)t be the corresponding

state processes. We know that u∗ is optimal if

J(u∗) ≥ J(u), ∀u ∈ A,

and after substitution

J(u∗)−J(u) = E

[∫ T

0

(f (t,X ∗t , u∗t )− f (t,Xt , ut)) dt + g(X ∗T )− g(XT )

]

Assumption

We assume that the integrals in the following derivation are finite.

32

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

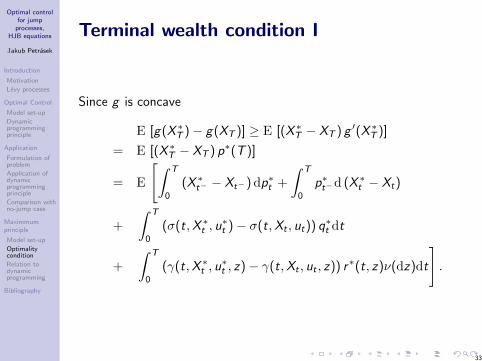

Terminal wealth condition I

Since g is concave

E [g(X ∗T )− g(XT )] ≥ E [(X ∗T − XT ) g ′(X ∗T )]

= E [(X ∗T − XT ) p∗(T )]

= E

[∫ T

0

(X ∗t− − Xt−) dp∗t +

∫ T

0

p∗t−d (X ∗t − Xt)

+

∫ T

0

(σ(t,X ∗t , u∗t )− σ(t,Xt , ut)) q∗t dt

+

∫ T

0

(γ(t,X ∗t , u∗t , z)− γ(t,Xt , ut , z)) r∗(t, z)ν(dz)dt

].

33

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Terminal wealth condition II

We substitute into pt and Xt and not rewrite m’gales with zeroexpected value

= E

[∫ T

0

− (X ∗t − Xt) Hx(t,X ∗t , u∗t , p∗t , q∗t , r∗(t, .))dt

+

∫ T

0

p∗t (b(t,X ∗t , u∗t )− b(t,Xt , ut)) dt

+

∫ T

0

(σ(t,X ∗t , u∗t )− σ(t,Xt , ut)) q∗t dt

+

∫ T

0

(γ(t,X ∗t , u∗t , z)− γ(t,Xt , ut , z)) r∗(t, z)ν(dz)dt

].

34

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

’Consumption’ condition

By the definition of H

E

[∫ T

0

(f (t,X ∗t , u∗t )− f (t,Xt , ut)) dt

]

= E

[∫ T

0

(H(t,X ∗t , u∗t , p∗t , q∗t , r∗(t, .))

−H(t,Xt , ut , p∗t , q∗t , r∗(t, .))) dt

−∫ T

0

p∗t (b(t,X ∗t , u∗t )− b(t,Xt , ut)) dt

−∫ T

0

(σ(t,X ∗t , u∗t )− σ(t,Xt , ut)) q∗t dt

−∫ T

0

(γ(t,X ∗t , u∗t , z)− γ(t,Xt , ut , z)) r∗(t, z)ν(dz)dt

].

35

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Terminal wealth + ’Consumption’ condition

J(u∗) − J(u) ≥ E

[∫ T

0

(H(t,X ∗t , u∗t , p∗t , q∗t , r∗(t, .))

−H(t,Xt , ut , p∗t , q∗t , r∗(t, .))) dt

−∫ T

0

(X ∗t − Xt) Hx(t,X ∗t , u∗t , p∗t , q∗t , r∗(t, .))dt

]

and if we find condition such that

J(u∗) − J(u) ≥ 0 (4.3)

we know that u∗ is the optimal control.

36

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Theorem

Theorem (Sufficient maximum principle)

Let u∗ ∈ A with corresponding solution X ∗ = X (u∗) and supposethere exists a solution (p∗t , q

∗t , r∗(t, z)) of the corresponding adjoint

equation. Moreover, suppose that

H(t,X ∗t , u∗t , p∗t , q∗t , r∗(t, .)) = sup

u∈UH(t,X ∗t , u, p

∗t , q∗t , r∗(t, .)), t ∈ [0,T ],

andH∗(x) = max

u∈UH(t, x , u, p∗t , q

∗t , r∗(t, .)) (4.4)

exists and is a concave function of x, t ∈ [0,T ] (Arrow condition).Then u∗ is optimal control.

37

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Remarks to theorem

Condition (4.4) is guaranteed by concavity of the functionH(t, x , u, p∗t , q

∗t , r∗(t, .)) in (x , u), t ∈ [0,T ].

To finish the proof, denote

h(t, x , u) = H(t, x , u, p∗t , q∗t , r∗(t, .))

andh∗(t, x) = max

u∈Ah(t, x , u)

Optimality condition (4.3) holds if

0 ≤ h∗(t, x∗)− h(t, x , u)− (x∗ − x)h∗′(t, x∗)

≥ h∗(t, x∗)− h∗(t, x)− (x∗ − x)h∗′(t, x∗) ≥ 0.

because h∗ is concave in x for t ∈ [0,T ].

38

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Relation to dynamic programming

For the dynamic programming we define criterion

J(u)(s, x) = E

[∫ T−s

0

f (t + s,Xt , ut)dt + g(XT−s)

],

v(s, x) = supu∈A

J(u)(s, x).

Theorem

Assume v ∈ C1,3 and that there exists an optimal control u∗t andcorresponding state process X ∗t for the maximum principle problem.Define

pt = vx(t,X ∗t ),

qt = σ(t,X ∗t , u∗t )vxx(t,X ∗t ),

r(t, z) = vx(t,X ∗t + γ(t,X ∗t , u∗t , z))− vx(t,X ∗t ).

Then pt , qt , r(t, .) solve the adjoint equation (4.2).39

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

Bibliography

R. Cont and P. Tankov.Financial modelling with jump processes.Chapman & Hall/CRC Financial Mathematics Series., 2004.

K. Janecek.Advanced topics in financial mathematics.Study material, MFF UK, 2008.

B. Øksendal and A. Sulem.Applied stochastic control of jump diffusions. 2nd ed.Universitext. Berlin: Springer., 2007.

40

Optimal controlfor jump

processes,HJB equations

Jakub Petrasek

Introduction

Motivation

Levy processes

Optimal Control

Model set-up

Dynamicprogrammingprinciple

Application

Formulation ofproblem

Application ofdynamicprogrammingprinciple

Comparison withno-jump case

Maximmumprinciple

Model set-up

Optimalitycondition

Relation todynamicprogramming

Bibliography

...

Thank you for attention

41