opportunities in iptv carolyn wales sukun kim david leuenberger william watts ori weinroth

Post on 20-Dec-2015

219 views

TRANSCRIPT

Opportunities in IPTV

Carolyn WalesSukun Kim

David LeuenbergerWilliam WattsOri Weinroth

What is IPTV?

• Definition: systems where television and/or video signals are distributed to viewers using a broadband connection over Internet Protocol

• Viewing device is not a defining feature

• We will focus on the home subscriber segment

Why is IPTV Important?• IPTV allows new players into video distribution:

– Incumbent telecommunication companies– Original content providers– Start-ups

• IPTV allows a new user experience:– On demand– convergence of video with other applications (voice,

data) on one device and interface.– More interactivity

Channels of Video DistributionCable/Satellite

Distribution Telco DistributionOpen Internet Distribution

Use existing infrastructure

VOD limited by network infrastructure

Rollout of advanced services possible, but likely slow

PVR upgrade easy, immediate

Installing new FTTx networks

Switched architecture makes VOD easier

Incentive to plan-in advanced features

Low barriers to entry – many many players

Poorer quality than Cable or Telco distribution

Ecosystem encourages experimentation

Content producers can connect directly with customers

Addition of services not foreseen at deployment likely to be slow

Telcos: Responding to Cable’s Voice Incursion

• Using VoIP technology, MSOs start offering subscribers triple-play packages: voice, data, video.

• Telcos face significant threat to voice revenues.

• Telco reflex: offer video. NPV>0?

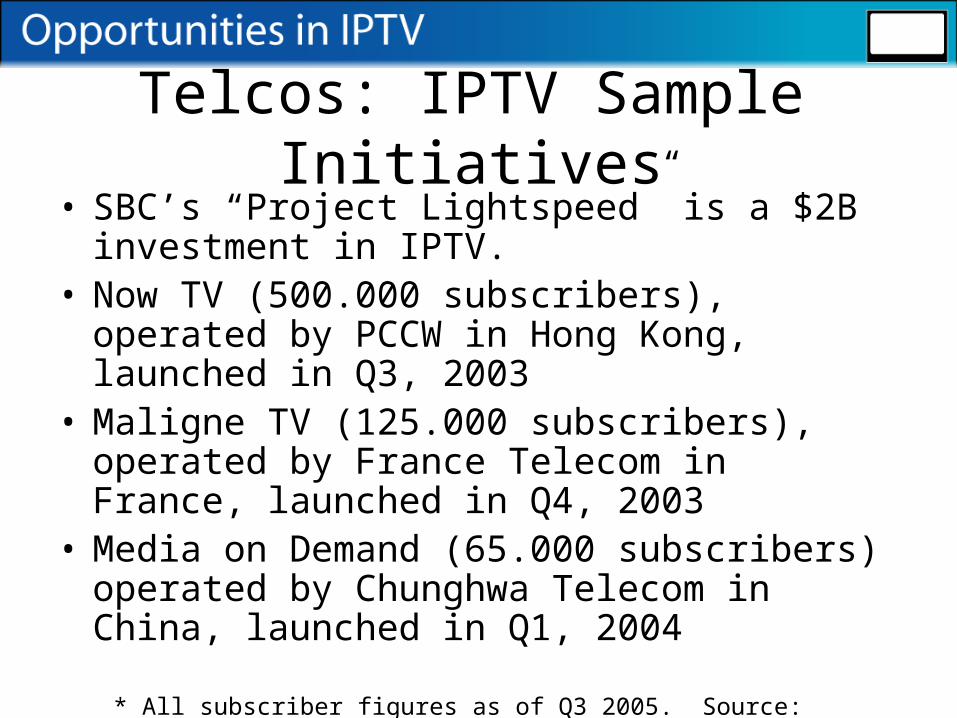

Telcos: IPTV Sample Initiatives• SBC’s “Project Lightspeed” is a $2B investment

in IPTV.• Now TV (500.000 subscribers), operated by

PCCW in Hong Kong, launched in Q3, 2003• Maligne TV (125.000 subscribers), operated by

France Telecom in France, launched in Q4, 2003

• Media on Demand (65.000 subscribers) operated by Chunghwa Telecom in China, launched in Q1, 2004

* All subscriber figures as of Q3 2005. Source: wikipedia.

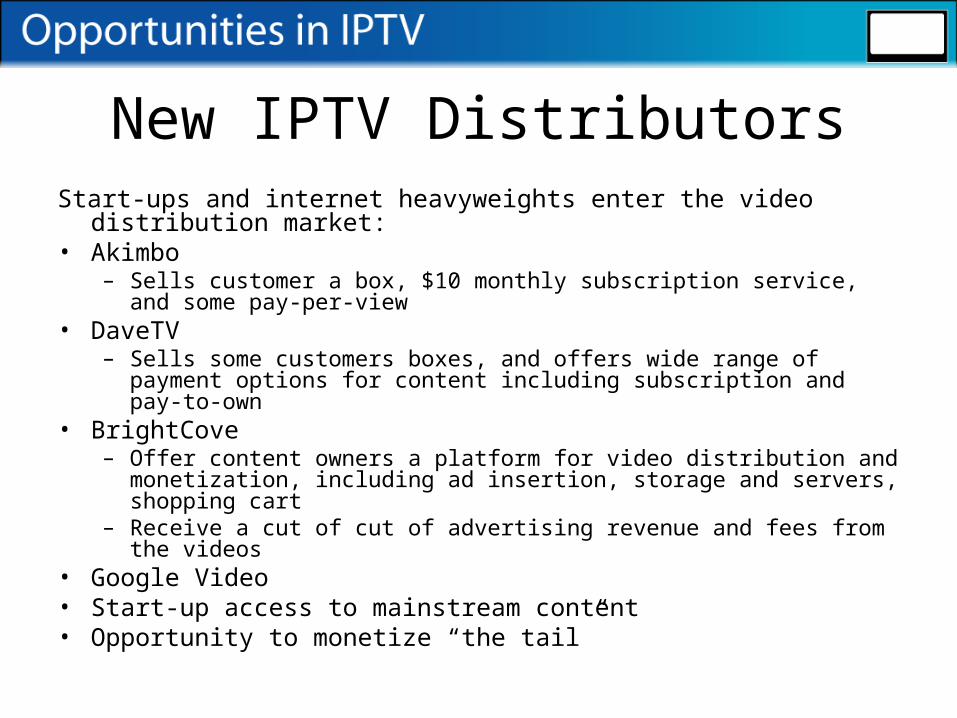

New IPTV DistributorsStart-ups and internet heavyweights enter the video distribution market:• Akimbo

– Sells customer a box, $10 monthly subscription service, and some pay-per-view

• DaveTV– Sells some customers boxes, and offers wide range of payment options

for content including subscription and pay-to-own• BrightCove

– Offer content owners a platform for video distribution and monetization, including ad insertion, storage and servers, shopping cart

– Receive a cut of cut of advertising revenue and fees from the videos• Google Video• Start-up access to mainstream content• Opportunity to monetize “the tail”

Content Providers Go Direct• MovieLink

– Owned by movie studios

– Pay-per-view. Prices range from $2-$5 per movie. Launching pay-to-own

– A lot of criticism of the current user experience

• The South Korean experience– Studios go direct to consumer over public internet network

– Pricing: $0.5-$1 depending on resolution (equivalent to $1.5-$3 in U.S.)

– Studio’s return bigger than when partnering with cable

– Result: popular TV series had 107K views per week (proportional to 650K views in US)

– Result: studios gain better understanding about viewing habits

• Channel conflict issues

Trends in Video• Increased personalization

– Users become “spoiled”– Content available on demand– Content available anywhere (devices include mobile)

• Content Multiplies – Inexpensive production tools– Culture of participation– Available distribution/monetization – virtuous cycle

• Convergence of Devices– IP network allows applications to run over multiple end-user

devices, over a single service delivery network

Trends in Video (continued)• New players in video distribution

– Akimbo, DaveTV, BrightCove, MovieLink

• Interactivity – Two-way nature of IP network enables unprecedented

interaction

• Targeted advertising– Required in a DVR home– Required where consumer has on-demand ad-free choices

• Cable/satellite broadcasting isn’t disappearing soon– Incumbents continue to add features

Changes in Video Industry Business Models

• Increased user sophistication and improved technology drive:– Variety in subscription models (subscribe to a series)

– Increased pay to own (not just DVDs)

– Increased pay-per-view (more VOD options)

• DVRs, VOD, and customer expectations drive change in advertising models:– Targeted Advertisements

– Opt-in, pay-to-watch

– Content integration with advertisement (Virtual Product Placement)

• Advertisers appear are becoming more comfortable with the New World

VC Opportunities• Start-ups selling IPTV tools to Telcos and their

competitors– Middleware (e.g. billing, user interface)– Bandwidth enhancers (hardware, compression software)– DRM– Targeted and embedded advertising (e.g United Virtualities’

Shoshmosis)– Search/recommendation tools

• Start-ups competing with Telcos in distribution• Start-ups providing tools to consumers

– Video recommendation tools, including on-line magazines– Search tools

VC Opportunities - continued• We will focus on video search and

recommendation tools

• A successful search tool will effectively address one or more of the following issues:

Crawling for Video• Crawlers have difficulty finding videos on the

web– 5-10% of video on the web are visble to crawlers on

static HTML pages as .mov, .avi, etc– Flash players, embedded video players, scripts pop-

up windows, sub-frames hide most video content

• Possible solutions:– Find video content based on webpage text– Find video content by emulating a user (e.g. Truveo)– Video self-identifies by set standards

Identify Video Content• Search engines need to identify what the video

contains• Possible solutions:

– Metadata such as MediaRSS and MPEG-7 input by producers or by aggregators

– Identify video content based on webpage text– Viewer generated metadata– Image recognition– Speech recognition– Indexing captions for the hearing impaired

Ranking Videos for Relevance

• Relevance solutions in video may utilize the same methods as text search

• However, linking as a relevance determinant is problematic

• Community as a filter may be more important

Copyright Protection• Video search engines need a method to not index

copyrighted content unless it is monetized.

– Currently no automated way to un-index or not index copyrighted videos

– Recent BitTorrent-studio announcement

• Currently, content owners fend for themselves

– Manually

– Aided by technology (Advestigo’s digital fingerprinting)

• Possible solutions:

– Copyright clearinghouse may help: Snocap (music registry)

Recommendation Engines• Professional content becomes fragmented

• Difficult for users to discover content of interest

• Recommendation engine required

• Recommendation engines as a service differentiator

• Two primary methods:

– Machine/algorithm (Google)

– Human/community (Yahoo)

Input Devices• Living room environment different from PC

environment.

• Current solutions (grid menus, remote) insufficient as content multiplies

• Possible solutions:

– Wireless keyboard (Microsoft)

– Voice recognition (AgileTV, OneVideo)

– New interfaces/devices (Hillcrest HoME)

Video Search Engine Business Models

• Should be similar to internet search engines:– Targeted advertising– Drive search for content provider for a fee– Be acquired by content provider

Q&A

Existing Video Distribution:Satellite

• Broadcast model.• Up to 215 channels offered.• Interactivity limited to TiVo-like functionality (with

purchase of DVR)• Monthly U.S. ARPU is $64.31*.• Only near-VOD available.

*Source DirectTV quaterly earnings statement 2005: http://media.corporate-ir.net/media_files/irol/12/127160/Q205Earnings.pdf

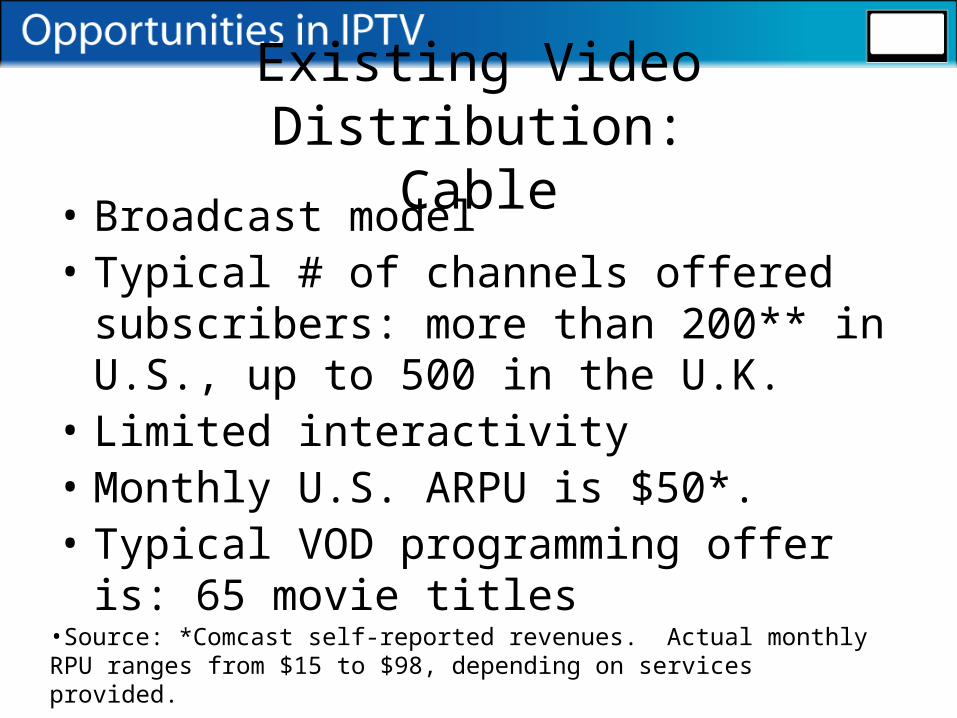

Existing Video Distribution:Cable

• Broadcast model• Typical # of channels offered subscribers:

more than 200** in U.S., up to 500 in the U.K.

• Limited interactivity• Monthly U.S. ARPU is $50*.• Typical VOD programming offer is: 65

movie titles•Source: *Comcast self-reported revenues. Actual monthly RPU ranges from $15 to $98, depending on services provided.

•**Courier News (Comcast New Jersey)

Telco IPTV Costs• Capital Expense

– Customer Premises Cost (CPE) = Set-Top boxes (STB), CAT-5 wiring, ADSL plug/modem, and home installation labor cost ≈ $655-$800

– Headend Equipments and VOD Servers: transcoders, rate shapers, video servers, core network ≈ $75-$200.

– Middleware Cost: software needed on both the server as well as the client side, including user authentication, content management, interactive program guide, customer relationship management (CRM), digital right management (DRM), billing, browser, MPEG-4 player $75-$150

– Access Network Cost: widely varying costs depending on network architecture and choice between fiber and DSL. Costs for fiber estimated at $672.

• Cost of Sales: estimated at 41% of ARPU.• Selling, General and Administrative (SG&A): estimated at 21% of

ARPU.

Telco IPTV Revenues• Video ARPU ≈ $45/subcriber/month• Advertising ≈ $6/subcriber/month• Equipment Rental ≈ $5/subcriber/month• As a general rule of thumb, adding a strategic

product (voice, data or video) can reduce churn by approximately 25% or more*.

* Yankee Group: “Driving Toward the Triple Play: The Telco Video Opportunity”

Building a Telco IPTV Offering

• Telco IPTV services operate over a private IP network, not the public Internet.

• A private network is required to ensure quality of service (QoS).

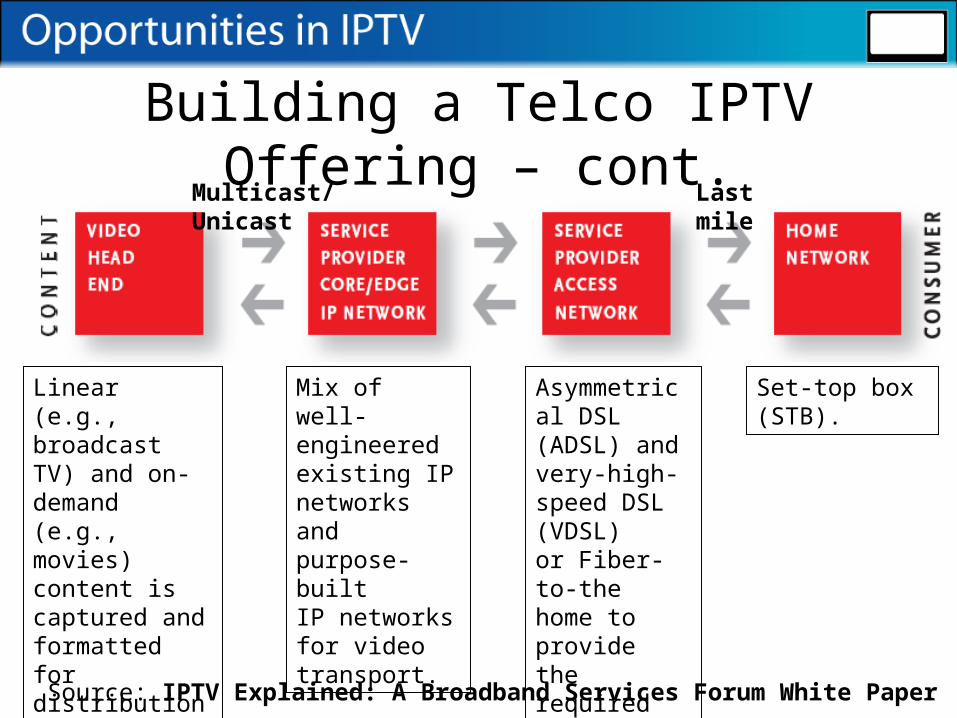

Building a Telco IPTV Offering – cont.

Source: IPTV Explained: A Broadband Services Forum White Paper

Linear (e.g., broadcast TV) and on-demand (e.g., movies) content is captured and formatted for distribution over the IP network.

Multicast/Unicast

Mix of well-engineered existing IP networks and purpose-builtIP networks for video transport.

Asymmetrical DSL (ADSL) and very-high-speed DSL (VDSL)or Fiber-to-the home to provide the required bandwidth.

Set-top box (STB).

Last mile

Telco IPTV Features• Price• number of channels• two-way interactivity• VOD• DVR• HDTV• integration with computer applications: photo,

music, voice• Search

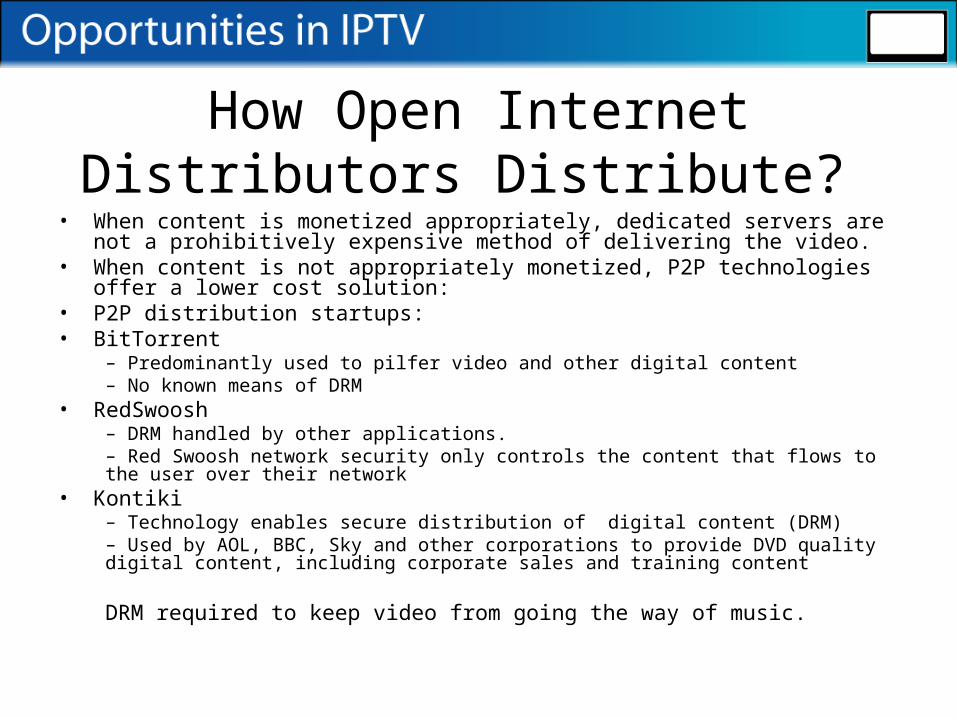

How Open Internet Distributors Distribute?

• When content is monetized appropriately, dedicated servers are not a prohibitively expensive method of delivering the video.

• When content is not appropriately monetized, P2P technologies offer a lower cost solution:

• P2P distribution startups:• BitTorrent

– Predominantly used to pilfer video and other digital content– No known means of DRM

• RedSwoosh– DRM handled by other applications. – Red Swoosh network security only controls the content that flows to the user over their network

• Kontiki– Technology enables secure distribution of digital content (DRM)– Used by AOL, BBC, Sky and other corporations to provide DVD quality digital content, including corporate sales and training content

DRM required to keep video from going the way of music.

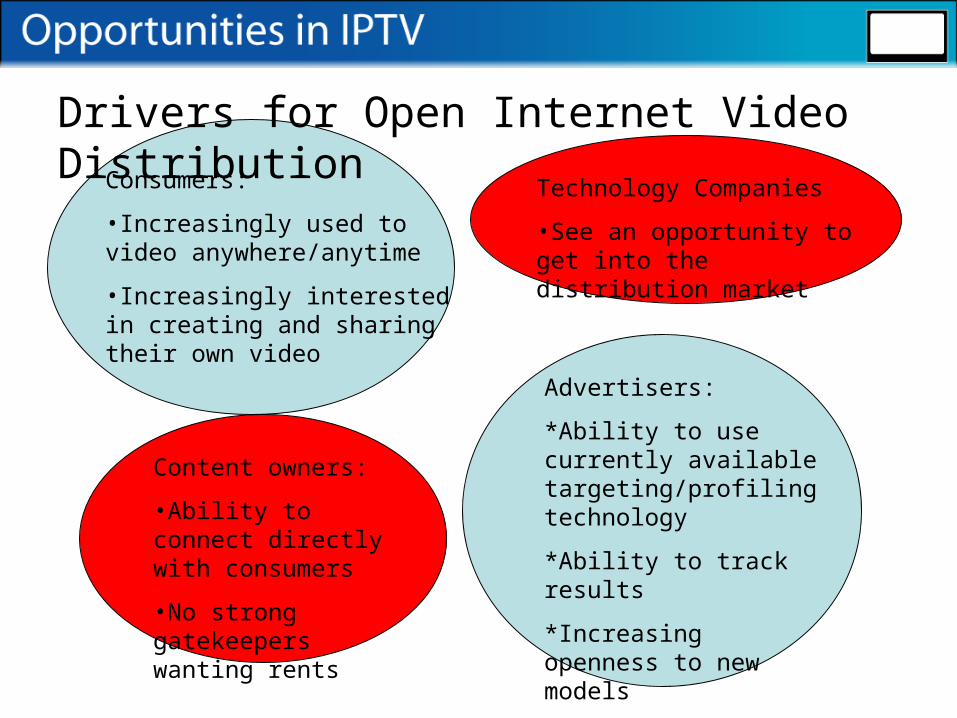

Drivers for Open Internet Video Distribution

Content owners:

•Ability to connect directly with consumers

•No strong gatekeepers wanting rents

Advertisers:

*Ability to use currently available targeting/profiling technology

*Ability to track results

*Increasing openness to new models

Consumers:

•Increasingly used to video anywhere/anytime

•Increasingly interested in creating and sharing their own video

Technology Companies

•See an opportunity to get into the distribution market