opportunities and challenges in the integrated asean ... case of the philippine processed meats...

TRANSCRIPT

Opportunities and Challenges in the Integrated ASEAN Market:

The Case of the Philippine Processed Meats Industry

Pia P. Medrano

March 2015

Abstract

In light of the acceleration of the establishment of the ASEAN Economic Community by 2015, this

paper investigates the opportunities and challenges that faces the Philippine processed meats

industry. We analyze ASEAN imports and use Balassa (1961)’s index of Revealed Comparative

Advantage to identify promising opportunities for the Philippines. Finally, we use UNCTAD (2010)’s

index of Revealed Factor Intensity and review ASEAN-member nations’ import standards to pinpoint

challenges that have to be addressed. We find that while the Philippines can feasibly gain or maintain

already existing comparative advantage by increasing physical capitalization in some promising

sectors, there are non-tariff barriers such as Singapore’s strict sanitary and phytosanitary standards

and Malaysia and Indonesia’s halal standards for processed foods that must be hurdled in order to

capture the ASEAN opportunities in these sectors.

1 Introduction

The ASEAN Economic Community (AEC), aimed to be established by 2015, is the realization of the

region’s end goal of economic integration. The AEC will establish ASEAN as a single market and

production base, which shall comprise five core elements: (i) free flow of goods; (ii) free flow of

services; (iii) free flow of investment; (iv) freer flow of capital; and (v) free flow of skilled labor. In

addition, the AEC Blueprint (2008) envisions the single market and production base to include two

important components, namely, the region’s priority integration sectors, and food, agriculture and

forestry.

In light of this targeted establishment of the AEC by 2015, this paper seeks to investigate

opportunities and challenges for the Philippines, looking at the case of its processed meats industry.

The rest of the paper is organized in order to do so. Section 2 identifies ASEAN’s promising imports

of processed meats. Section 3 assesses the Philippines’ current competitiveness in each commodity

sector as measured via Balassa (1961)’s index of Revealed Comparative Advantage (RCA). Section 4

looks at what can be done by the Philippines in order to maintain or gain comparative advantage in

this industry by comparing UNCTAD (2010)’s index of Revealed Factor Intensity (RFI) for each

processed meats commodity with the Philippines’ existing capital (physical and human)

endowments. Section 5 studies the import standards imposed by the biggest markets in the ASEAN

region and reviews the Philippines’ current compliance with these standards. Finally, section 6

concludes.

2 Opportunities in the ASEAN Market: What are the ASEAN Promising Imports?

This paper took a look at the 11 meat commodities under Chapter 16 (Preparations of meat, fish or

of crustaceans, molluscs or other aquatic invertebrates) of the Harmonized System (HS) of

international tariff nomenclature, focusing on the six-digit level:

(1) 16 0100 Sausage and similar products of meat, meat offal/blood and food preparations based on these products

(2) 16 0210 Homogenized preparations of meat and meat offal

(3) 16 0220 Livers of any animal (prepared or preserved)

(4) 16 0231 Turkey meat and meat offal (prepared or preserved), excluding livers

(5) 16 0232 Fowl (gallus domesticus*) meat (prepared or preserved) *Gallus domesticus is known as the common domestic chicken.

(6) 16 0239 Domestic fowl, duck, goose and guinea fowl meat and meat offal (prepared or preserved), excluding livers

(7) 16 0241 Hams and cuts thereof of swine (prepared or preserved)

(8) 16 0242 Shoulders and cut thereof of swine (prepared or preserved)

(9) 16 0249 Swine meat and meat offal, excluding livers

(10) 16 0250 Bovine meat and meat offal, excluding livers

(11) 16 0290 Other animal meat and meat offal, excluding livers

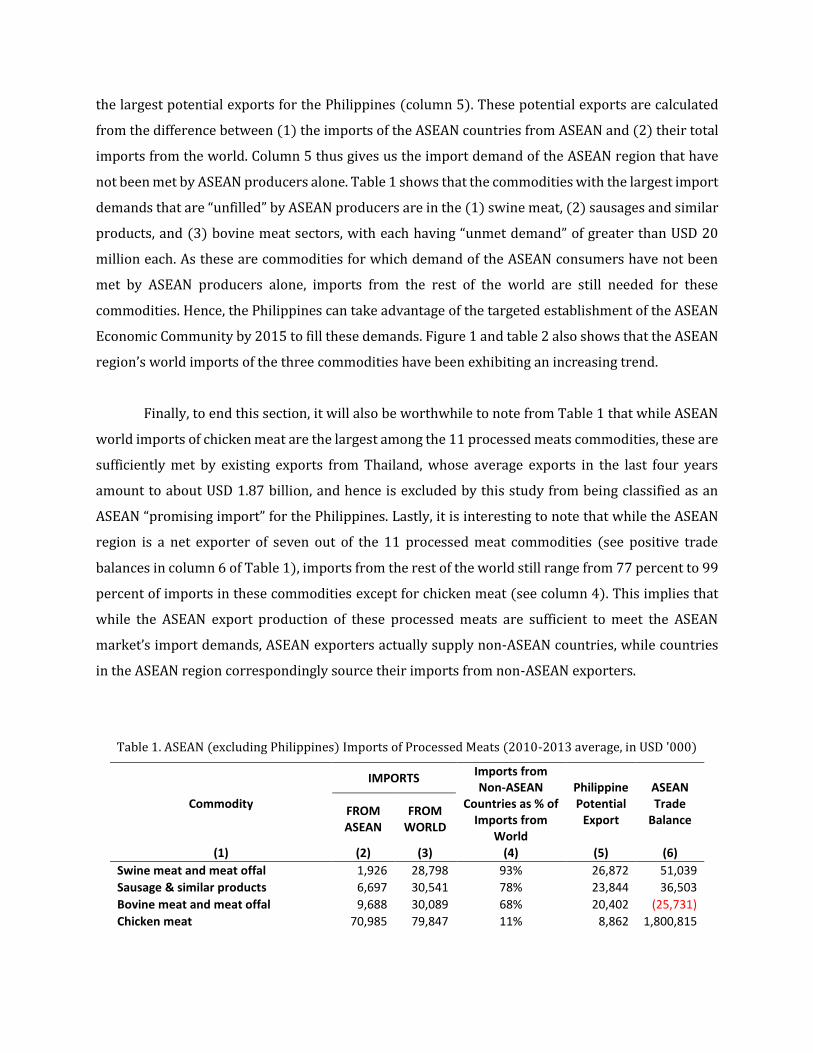

Among these 11 commodities, (1) swine meat, (2) sausage and similar products, and (3)

bovine meat are identified as the ASEAN market’s promising that the Philippines can tap. Table 1

looks at the ASEAN region’s imports of processed meats and lists the 11 commodities according to

the largest potential exports for the Philippines (column 5). These potential exports are calculated

from the difference between (1) the imports of the ASEAN countries from ASEAN and (2) their total

imports from the world. Column 5 thus gives us the import demand of the ASEAN region that have

not been met by ASEAN producers alone. Table 1 shows that the commodities with the largest import

demands that are “unfilled” by ASEAN producers are in the (1) swine meat, (2) sausages and similar

products, and (3) bovine meat sectors, with each having “unmet demand” of greater than USD 20

million each. As these are commodities for which demand of the ASEAN consumers have not been

met by ASEAN producers alone, imports from the rest of the world are still needed for these

commodities. Hence, the Philippines can take advantage of the targeted establishment of the ASEAN

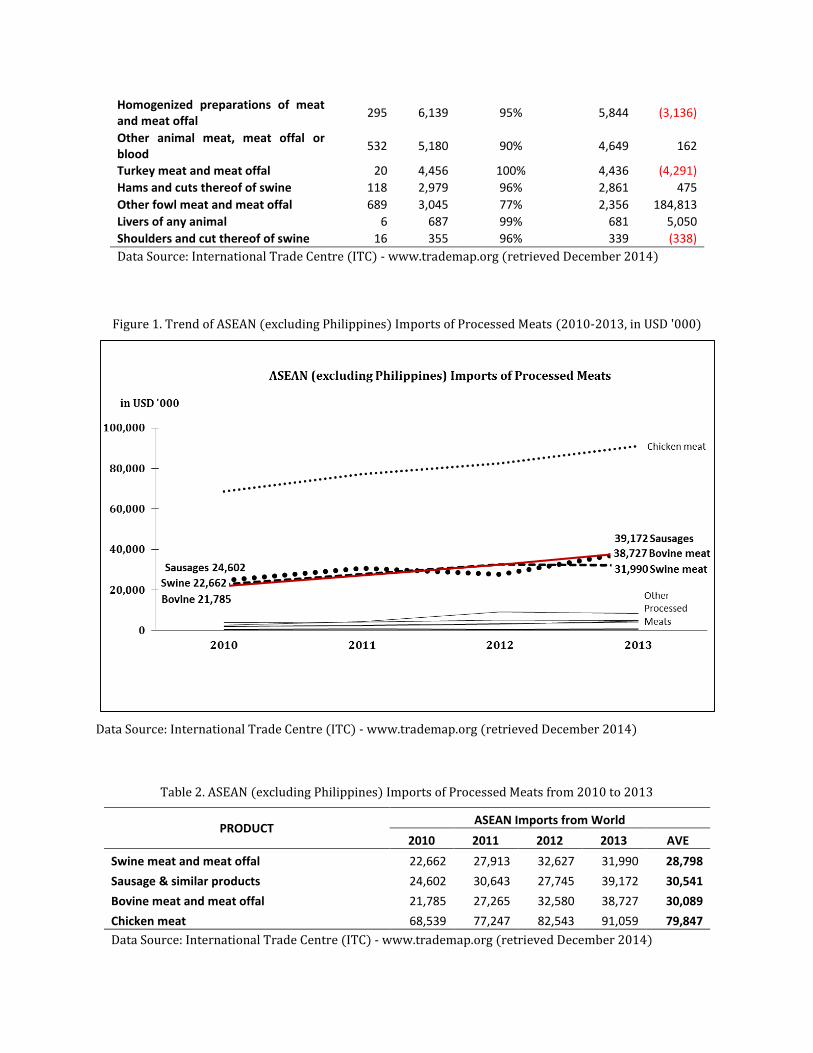

Economic Community by 2015 to fill these demands. Figure 1 and table 2 also shows that the ASEAN

region’s world imports of the three commodities have been exhibiting an increasing trend.

Finally, to end this section, it will also be worthwhile to note from Table 1 that while ASEAN

world imports of chicken meat are the largest among the 11 processed meats commodities, these are

sufficiently met by existing exports from Thailand, whose average exports in the last four years

amount to about USD 1.87 billion, and hence is excluded by this study from being classified as an

ASEAN “promising import” for the Philippines. Lastly, it is interesting to note that while the ASEAN

region is a net exporter of seven out of the 11 processed meat commodities (see positive trade

balances in column 6 of Table 1), imports from the rest of the world still range from 77 percent to 99

percent of imports in these commodities except for chicken meat (see column 4). This implies that

while the ASEAN export production of these processed meats are sufficient to meet the ASEAN

market’s import demands, ASEAN exporters actually supply non-ASEAN countries, while countries

in the ASEAN region correspondingly source their imports from non-ASEAN exporters.

Table 1. ASEAN (excluding Philippines) Imports of Processed Meats (2010-2013 average, in USD '000)

Commodity

IMPORTS Imports from Non-ASEAN

Countries as % of Imports from

World

Philippine Potential

Export

ASEAN Trade

Balance FROM ASEAN

FROM WORLD

(1) (2) (3) (4) (5) (6)

Swine meat and meat offal 1,926 28,798 93% 26,872 51,039

Sausage & similar products 6,697 30,541 78% 23,844 36,503

Bovine meat and meat offal 9,688 30,089 68% 20,402 (25,731)

Chicken meat 70,985 79,847 11% 8,862 1,800,815

Homogenized preparations of meat and meat offal

295 6,139 95% 5,844 (3,136)

Other animal meat, meat offal or blood

532 5,180 90% 4,649 162

Turkey meat and meat offal 20 4,456 100% 4,436 (4,291)

Hams and cuts thereof of swine 118 2,979 96% 2,861 475

Other fowl meat and meat offal 689 3,045 77% 2,356 184,813

Livers of any animal 6 687 99% 681 5,050

Shoulders and cut thereof of swine 16 355 96% 339 (338)

Data Source: International Trade Centre (ITC) - www.trademap.org (retrieved December 2014)

Figure 1. Trend of ASEAN (excluding Philippines) Imports of Processed Meats (2010-2013, in USD '000)

Data Source: International Trade Centre (ITC) - www.trademap.org (retrieved December 2014)

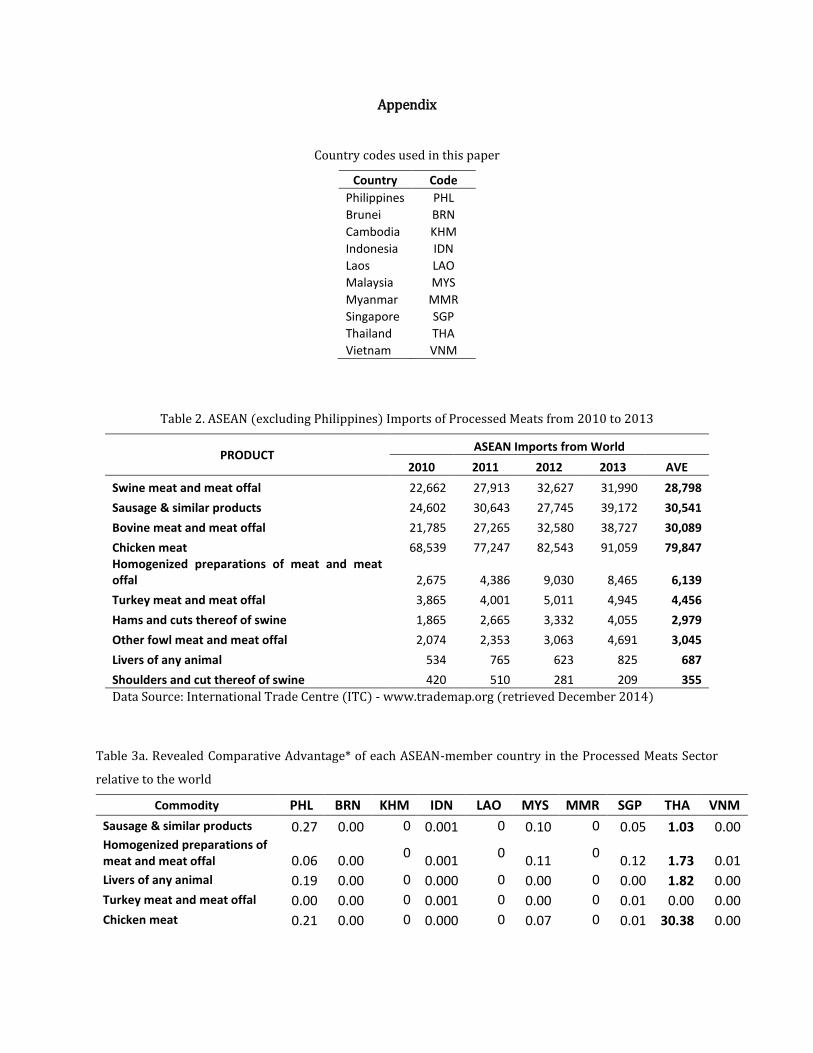

Table 2. ASEAN (excluding Philippines) Imports of Processed Meats from 2010 to 2013

PRODUCT ASEAN Imports from World

2010 2011 2012 2013 AVE

Swine meat and meat offal 22,662 27,913 32,627 31,990 28,798

Sausage & similar products 24,602 30,643 27,745 39,172 30,541

Bovine meat and meat offal 21,785 27,265 32,580 38,727 30,089

Chicken meat 68,539 77,247 82,543 91,059 79,847

Data Source: International Trade Centre (ITC) - www.trademap.org (retrieved December 2014)

3 Profile of the Philippine Exports Industry: Analysis of Revealed Comparative Advantage

This section assesses the Philippines’ existing comparative advantage in the processed meats sector

by generating a ‘revealed comparative advantage’ (RCA) index derived from Balassa’s (1965) RCA

measure.

This paper calculates the RCA of each ASEAN-member country through the following

equation:

𝑅𝐶𝐴𝐴𝑆𝐸𝐴𝑁𝑖𝑗=

𝑋𝑖𝑗 ∑ 𝑋𝑖𝑗𝑖⁄

∑ 𝑋𝑖𝑗𝑗 ∑ ∑ 𝑋𝑖𝑗𝑗𝑖⁄

𝑅𝐶𝐴𝐴𝑆𝐸𝐴𝑁𝑖𝑗=

𝑋𝑖𝑗 ∑ 𝑋𝑖𝑗𝑖⁄

(∑ 𝑋𝑖𝑗𝑗 − 𝑋𝑖𝑗) (∑ ∑ 𝑋𝑖𝑗𝑗𝑖 − ∑ 𝑋𝑖𝑗𝑖 )⁄

The numerator is similar to Balassa’s and represents the percentage share of a given sector in

national exports - 𝑋𝑖𝑗 are exports of sector 𝑖 from country 𝑗. The numerator thus gives us a feel of the

degree of specialization of country 𝑗 in sector 𝑖. The denominator, on the other hand, deviates from

Balassa’s, which uses the percentage share of the entire set of countries’ exports in a given sector in

the entire set of countries’ total exports. The denominator we use represents the percentage share of

the rest of the (ASEAN) region’s exports in a given sector in the rest of the (ASEAN) region’s total

exports. This denominator thus gives us a feel of the degree of specialization of the rest of the ASEAN

region in sector 𝑖. This denominator will enable us to have a more direct comparison of the degree of

specialization of country 𝑗 to the degree of specialization of the rest of the ASEAN region. When RCA

is greater than 1, the country is ‘revealed’ to have a higher degree of specialization in that sector over

the rest of the ASEAN nations. When RCA is less than 1, the country is ‘revealed’ to have a lower

degree of specialization in that sector compared to the rest of the ASEAN nations.

It will also be important to note why we only used the set of ASEAN nations (and not of the

entire world) in the calculation of our denominator. There are two reasons for this: (1) all ASEAN

nations (except for Thailand and Malaysia) turned out to have RCAs of less than 0.4 in all processed

meats commodity sectors when compared to the rest of the world, and (2) since this paper looks at

the processed meats industry in light of the 2015 ASEAN Integration, it appears appropriate to

compare the Philippines’ comparative advantage with only the other ASEAN countries as well, as as

espoused by the notion of regionalism, ASEAN countries will have preferential treatments over non-

ASEAN exporters.

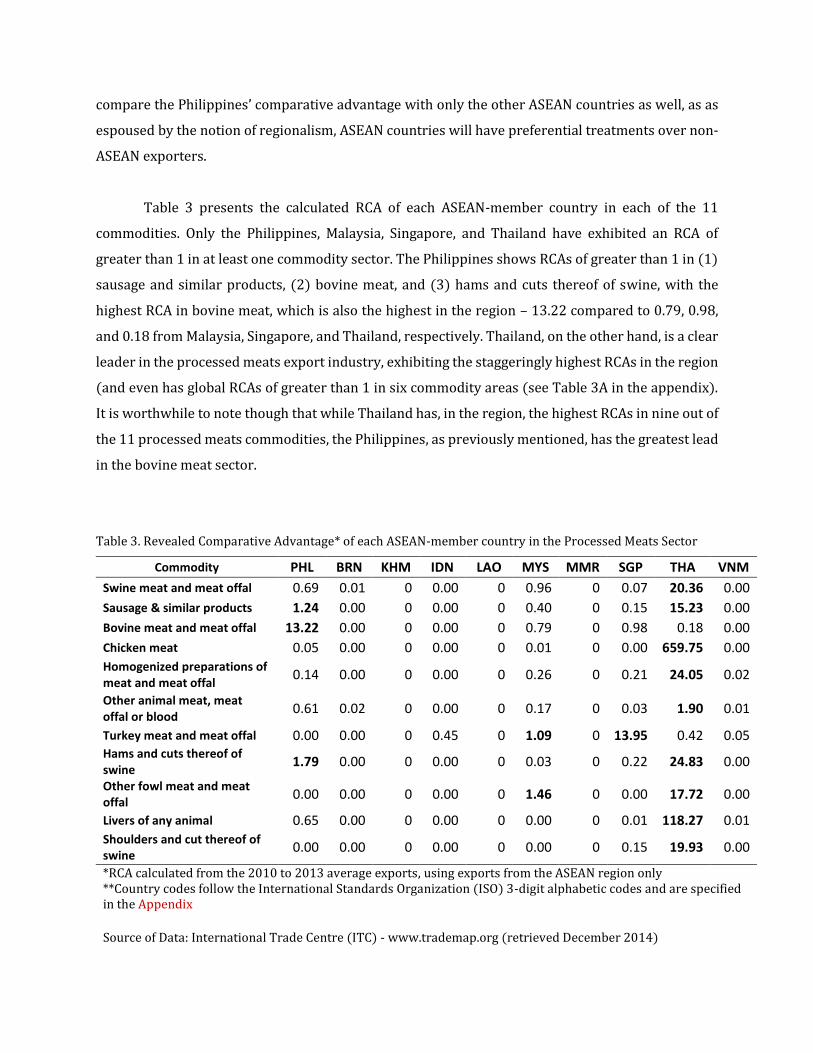

Table 3 presents the calculated RCA of each ASEAN-member country in each of the 11

commodities. Only the Philippines, Malaysia, Singapore, and Thailand have exhibited an RCA of

greater than 1 in at least one commodity sector. The Philippines shows RCAs of greater than 1 in (1)

sausage and similar products, (2) bovine meat, and (3) hams and cuts thereof of swine, with the

highest RCA in bovine meat, which is also the highest in the region – 13.22 compared to 0.79, 0.98,

and 0.18 from Malaysia, Singapore, and Thailand, respectively. Thailand, on the other hand, is a clear

leader in the processed meats export industry, exhibiting the staggeringly highest RCAs in the region

(and even has global RCAs of greater than 1 in six commodity areas (see Table 3A in the appendix).

It is worthwhile to note though that while Thailand has, in the region, the highest RCAs in nine out of

the 11 processed meats commodities, the Philippines, as previously mentioned, has the greatest lead

in the bovine meat sector.

Table 3. Revealed Comparative Advantage* of each ASEAN-member country in the Processed Meats Sector

Commodity PHL BRN KHM IDN LAO MYS MMR SGP THA VNM

Swine meat and meat offal 0.69 0.01 0 0.00 0 0.96 0 0.07 20.36 0.00

Sausage & similar products 1.24 0.00 0 0.00 0 0.40 0 0.15 15.23 0.00

Bovine meat and meat offal 13.22 0.00 0 0.00 0 0.79 0 0.98 0.18 0.00

Chicken meat 0.05 0.00 0 0.00 0 0.01 0 0.00 659.75 0.00

Homogenized preparations of meat and meat offal

0.14 0.00 0 0.00 0 0.26 0 0.21 24.05 0.02

Other animal meat, meat offal or blood

0.61 0.02 0 0.00 0 0.17 0 0.03 1.90 0.01

Turkey meat and meat offal 0.00 0.00 0 0.45 0 1.09 0 13.95 0.42 0.05 Hams and cuts thereof of swine

1.79 0.00 0 0.00 0 0.03 0 0.22 24.83 0.00

Other fowl meat and meat offal

0.00 0.00 0 0.00 0 1.46 0 0.00 17.72 0.00

Livers of any animal 0.65 0.00 0 0.00 0 0.00 0 0.01 118.27 0.01

Shoulders and cut thereof of swine

0.00 0.00 0 0.00 0 0.00 0 0.15 19.93 0.00

*RCA calculated from the 2010 to 2013 average exports, using exports from the ASEAN region only **Country codes follow the International Standards Organization (ISO) 3-digit alphabetic codes and are specified in the Appendix

Source of Data: International Trade Centre (ITC) - www.trademap.org (retrieved December 2014)

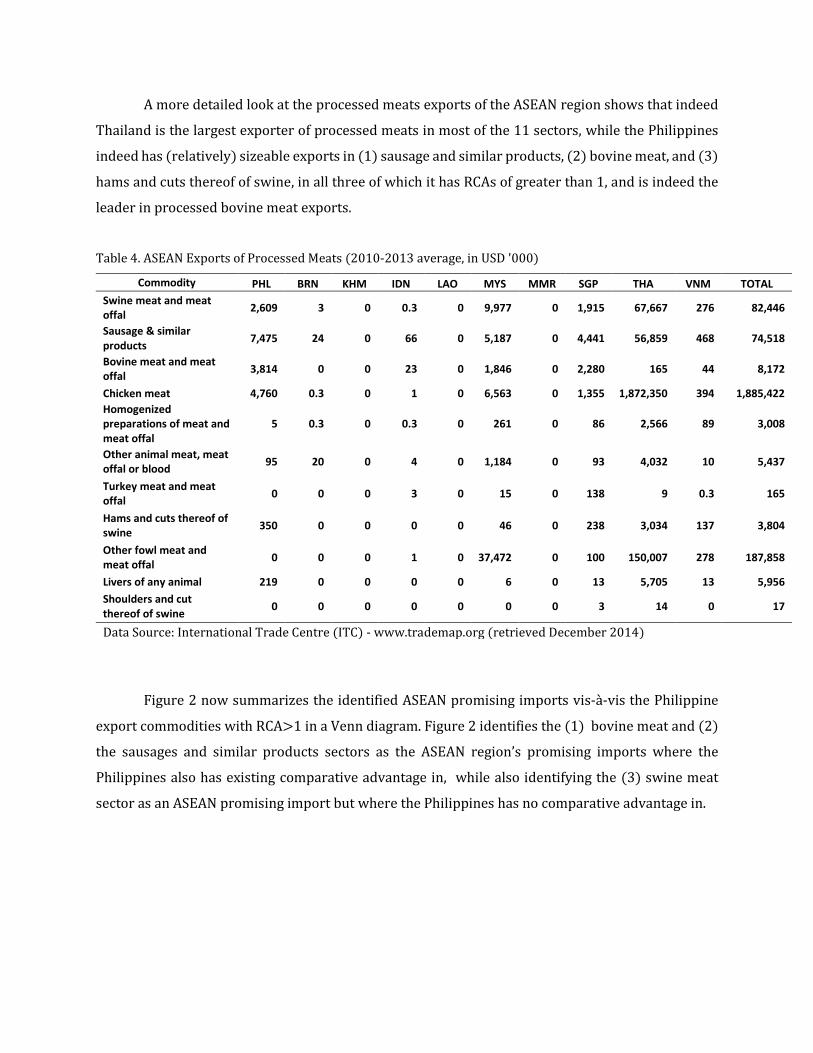

A more detailed look at the processed meats exports of the ASEAN region shows that indeed

Thailand is the largest exporter of processed meats in most of the 11 sectors, while the Philippines

indeed has (relatively) sizeable exports in (1) sausage and similar products, (2) bovine meat, and (3)

hams and cuts thereof of swine, in all three of which it has RCAs of greater than 1, and is indeed the

leader in processed bovine meat exports.

Table 4. ASEAN Exports of Processed Meats (2010-2013 average, in USD '000)

Commodity PHL BRN KHM IDN LAO MYS MMR SGP THA VNM TOTAL

Swine meat and meat offal

2,609 3 0 0.3 0 9,977 0 1,915 67,667 276 82,446

Sausage & similar products

7,475 24 0 66 0 5,187 0 4,441 56,859 468 74,518

Bovine meat and meat offal

3,814 0 0 23 0 1,846 0 2,280 165 44 8,172

Chicken meat 4,760 0.3 0 1 0 6,563 0 1,355 1,872,350 394 1,885,422

Homogenized preparations of meat and meat offal

5 0.3 0 0.3 0 261 0 86 2,566 89 3,008

Other animal meat, meat offal or blood

95 20 0 4 0 1,184 0 93 4,032 10 5,437

Turkey meat and meat offal

0 0 0 3 0 15 0 138 9 0.3 165

Hams and cuts thereof of swine

350 0 0 0 0 46 0 238 3,034 137 3,804

Other fowl meat and meat offal

0 0 0 1 0 37,472 0 100 150,007 278 187,858

Livers of any animal 219 0 0 0 0 6 0 13 5,705 13 5,956

Shoulders and cut thereof of swine

0 0 0 0 0 0 0 3 14 0 17

Data Source: International Trade Centre (ITC) - www.trademap.org (retrieved December 2014)

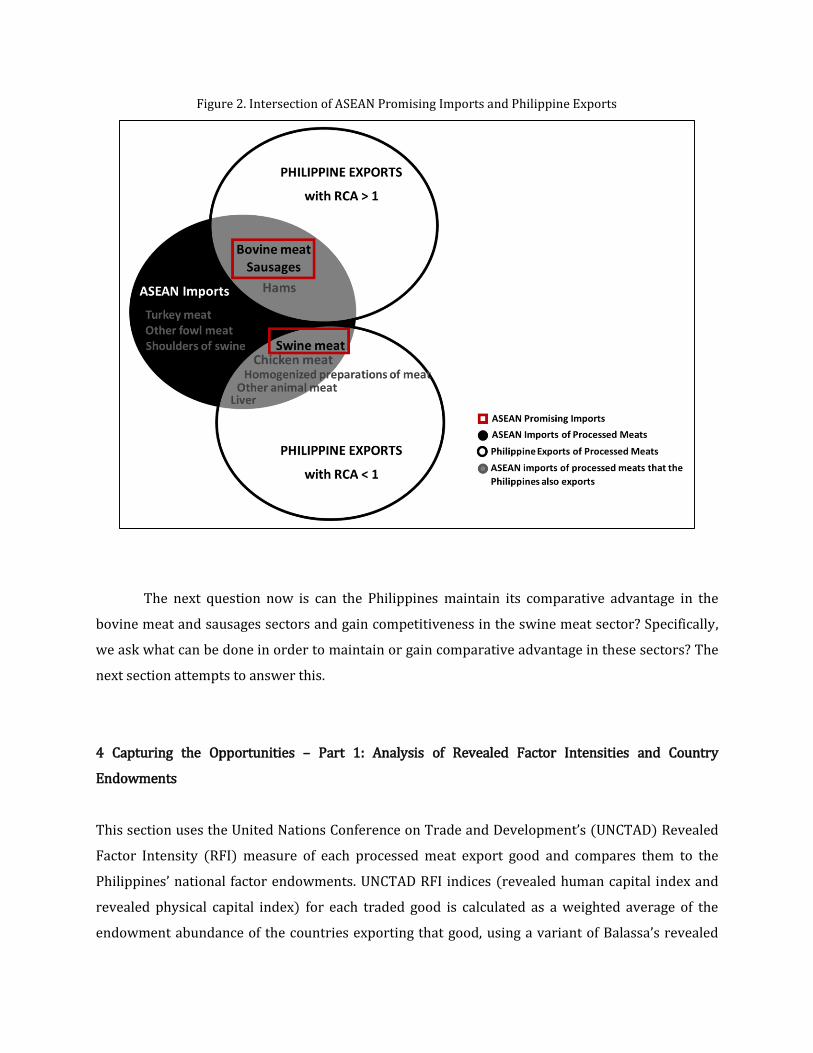

Figure 2 now summarizes the identified ASEAN promising imports vis-à-vis the Philippine

export commodities with RCA>1 in a Venn diagram. Figure 2 identifies the (1) bovine meat and (2)

the sausages and similar products sectors as the ASEAN region’s promising imports where the

Philippines also has existing comparative advantage in, while also identifying the (3) swine meat

sector as an ASEAN promising import but where the Philippines has no comparative advantage in.

Figure 2. Intersection of ASEAN Promising Imports and Philippine Exports

The next question now is can the Philippines maintain its comparative advantage in the

bovine meat and sausages sectors and gain competitiveness in the swine meat sector? Specifically,

we ask what can be done in order to maintain or gain comparative advantage in these sectors? The

next section attempts to answer this.

4 Capturing the Opportunities – Part 1: Analysis of Revealed Factor Intensities and Country

Endowments

This section uses the United Nations Conference on Trade and Development’s (UNCTAD) Revealed

Factor Intensity (RFI) measure of each processed meat export good and compares them to the

Philippines’ national factor endowments. UNCTAD RFI indices (revealed human capital index and

revealed physical capital index) for each traded good is calculated as a weighted average of the

endowment abundance of the countries exporting that good, using a variant of Balassa’s revealed

comparative advantage index as weights. The idea behind the calculation is that a good exported

predominantly – as determined by Balassa’s RCA – by countries that are richly endowed with a

particular factor is “revealed” to be intensive in that factor (Shirotori, Tumurhudur, and Cadot, 2010).

The indices are available on the UNCTAD website.

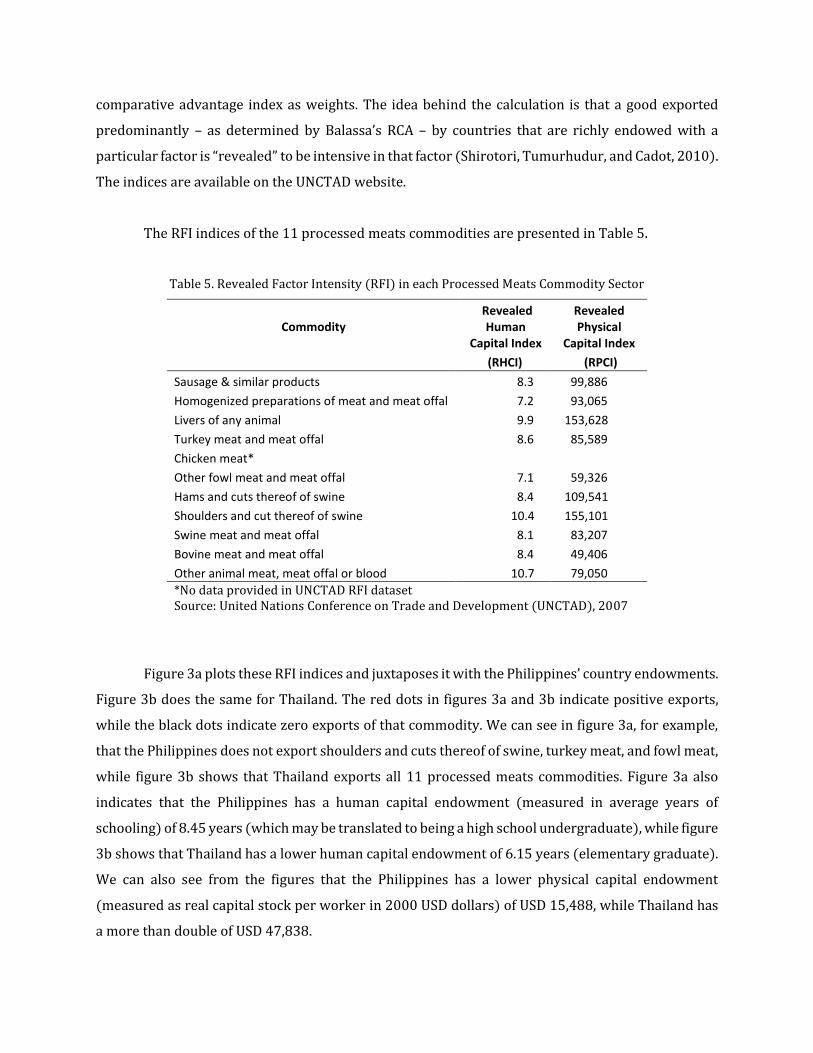

The RFI indices of the 11 processed meats commodities are presented in Table 5.

Table 5. Revealed Factor Intensity (RFI) in each Processed Meats Commodity Sector

Commodity Revealed

Human Capital Index

Revealed Physical

Capital Index

(RHCI) (RPCI)

Sausage & similar products 8.3 99,886

Homogenized preparations of meat and meat offal 7.2 93,065

Livers of any animal 9.9 153,628

Turkey meat and meat offal 8.6 85,589

Chicken meat*

Other fowl meat and meat offal 7.1 59,326

Hams and cuts thereof of swine 8.4 109,541

Shoulders and cut thereof of swine 10.4 155,101

Swine meat and meat offal 8.1 83,207

Bovine meat and meat offal 8.4 49,406

Other animal meat, meat offal or blood 10.7 79,050

*No data provided in UNCTAD RFI dataset Source: United Nations Conference on Trade and Development (UNCTAD), 2007

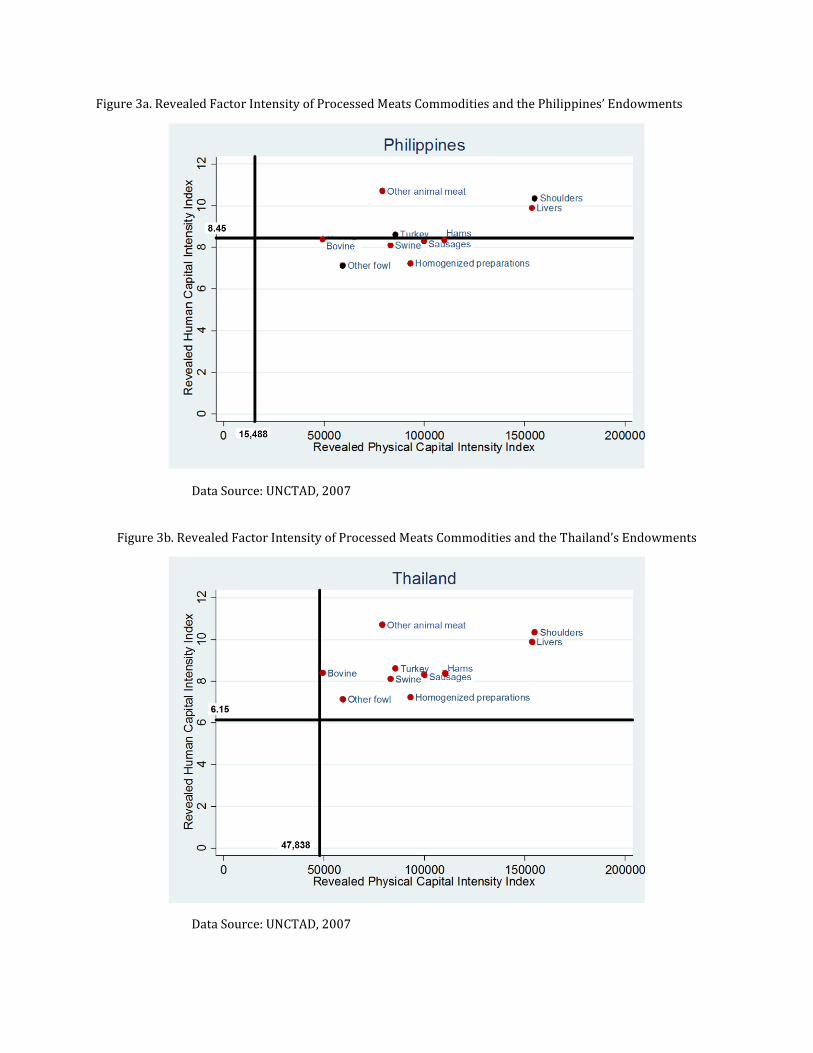

Figure 3a plots these RFI indices and juxtaposes it with the Philippines’ country endowments.

Figure 3b does the same for Thailand. The red dots in figures 3a and 3b indicate positive exports,

while the black dots indicate zero exports of that commodity. We can see in figure 3a, for example,

that the Philippines does not export shoulders and cuts thereof of swine, turkey meat, and fowl meat,

while figure 3b shows that Thailand exports all 11 processed meats commodities. Figure 3a also

indicates that the Philippines has a human capital endowment (measured in average years of

schooling) of 8.45 years (which may be translated to being a high school undergraduate), while figure

3b shows that Thailand has a lower human capital endowment of 6.15 years (elementary graduate).

We can also see from the figures that the Philippines has a lower physical capital endowment

(measured as real capital stock per worker in 2000 USD dollars) of USD 15,488, while Thailand has

a more than double of USD 47,838.

Figure 3a. Revealed Factor Intensity of Processed Meats Commodities and the Philippines’ Endowments

Data Source: UNCTAD, 2007

Figure 3b. Revealed Factor Intensity of Processed Meats Commodities and the Thailand’s Endowments

Data Source: UNCTAD, 2007

We can see from both figures that the Philippines faces no problem in terms of its human

capital since its workers has more average years of schooling than the average Thai worker. The great

difference between the Philippines’ and Thailand’s competitiveness in the processed meats sector

therefore appears to come from the two countries’ great discrepancy in physical capital investments.

Increased (physical) capitalization therefore can give the Philippines comparative advantage or

competitiveness in the processed meats export industry.

Zooming in on the results of figure 3a, we see that (1) bovine meat, (2) swine meat, and (3)

sausages and similar products are among those that require the least amount of (physical)

capitalization and also all require human capital level that is within the 8.45 average years of

schooling of the Philippines. These are excellent results for the Philippines, as these three

commodities are also the very same commodity sectors we have earlier identified to be the ASEAN

region’s promising imports.

It is therefore a major finding of this paper that (1) bovine meat, (2) swine meat, and (3)

sausages and similar products are not only promising imports but sectors where the Philippines can

gain or maintain comparative advantage in, as the human capital endowment of the Philippines

(average years of schooling) more than satisfies the requirements for these commodities and the

capital endowments (real capital per labor) can be feasibly attained by the Philippines as these

commodities require the lowest capitalization. We should also note here that the Philippines already

has an RCA > 1 in the bovine and sausage meat products, and currently has a substantial volume of

swine exports as well (USD 2,609,000 average from 2010-2013 as can be seen in Table 4 under

Section 2).

While this section finds that the Philippines can feasibly capture the potential markets for (1)

bovine meat, (2) swine meat, and (3) sausages and similar products in the ASEAN region by

increasing (physical) capital investments and hence production in this industry, the next section

takes a look at the nontariff barriers that the Philippines faces in this sector in the ASEAN region.

5 Capturing the Opportunities – Part 2: Review of ASEAN import standards and the Philippines’ Current

Compliance

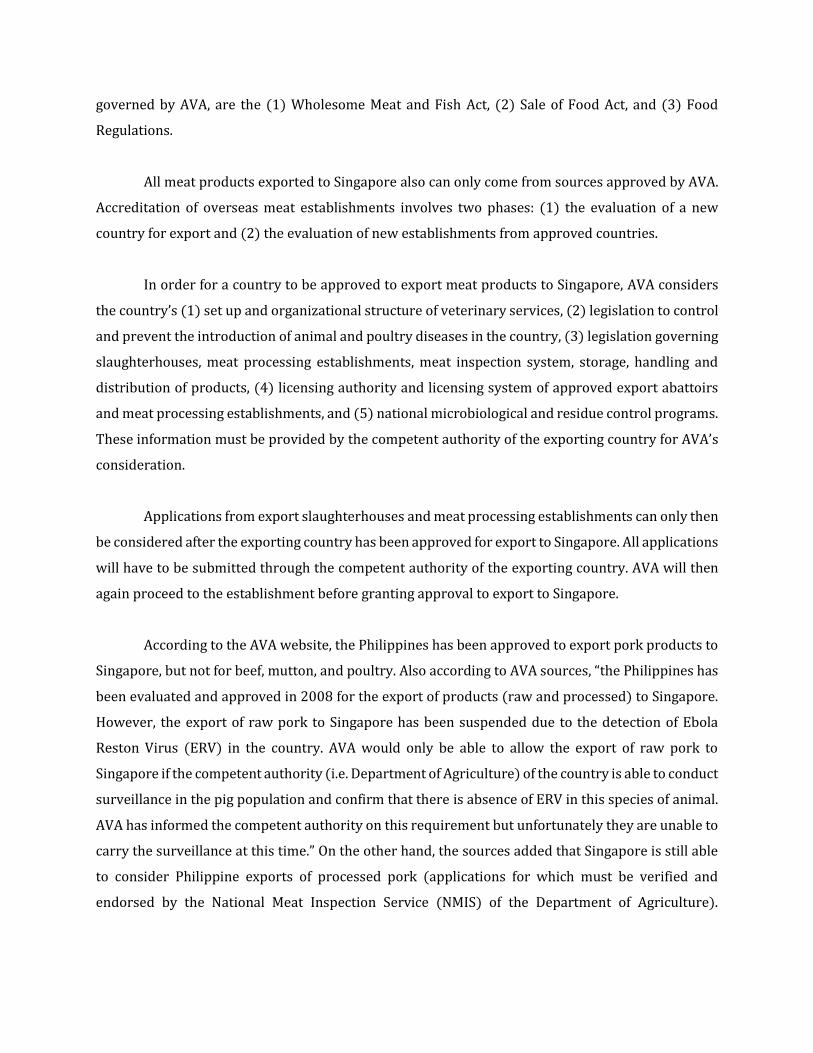

Table 6 shows that Singapore, Malaysia, Indonesia, and Brunei are the ASEAN region’s largest

importers of (1) bovine meat, (2) swine meat, and (3) sausages and similar products (as well as of

the rest of the 11 processed meats commodities). This section thus focuses on the standards for

processed meats imports in these four countries.

Table 6. ASEAN Imports of Processed Meats (2013, in USD '000)

Commodity PHL BRN KHM IDN LAO MYS MMR SGP THA VNM TOTAL

Swine meat and meat offal

3,352 1,390 179 809.0 86 2,105 1,235 24,837 488 861 35,342

Sausage & similar products

823 2,958 604 4,522 202 2,264 702 23,366 3,902 652 39,995

Bovine meat and meat offal

267 572 1 10,943 4 813 49 22,535 3,693 117 38,994

Chicken meat 140 3,401.0 771 112 228 2,390 435 79,683 1,694 2,345 91,199

Homogenized preparations of meat and meat offal

3 524.0 22 9.0 37 5,314 50 1,567 825 117 8,468

Other animal meat, meat offal or blood

58 688 8 1 71 92 200 2,625 10,381 14,124

Turkey meat and meat offal

14 0 0 0 5 13 4,843 33 51.0 4,959

Hams and cuts thereof of swine

390 644 2 63 5 481 19 2,173 398 270 4,445

Other fowl meat and meat offal

13 228 0 670 1 380 714 2,086 422 190 4,704

Livers of any animal 16 2 0 0 0 81 513 229 841

Shoulders and cut thereof of swine

20 3 0 25 2 40 80 12 47 229

Data Source: International Trade Centre (ITC) - www.trademap.org (retrieved December 2014)

Singapore

Singapore currently has no applicable tariffs or duties on food and most beverage products. However,

it implements highly strict sanitary and phytosanitary standards that exporters must comply with.

The Agri-food and Veterinary Authority of Singapore (AVA) is the national authority which ensures

that these standards are met.

As with any country, exporters must first ensure that the food they intend to export complies

with the relevant legislation in Singapore. For meat exports to Singapore, these legislation, which are

governed by AVA, are the (1) Wholesome Meat and Fish Act, (2) Sale of Food Act, and (3) Food

Regulations.

All meat products exported to Singapore also can only come from sources approved by AVA.

Accreditation of overseas meat establishments involves two phases: (1) the evaluation of a new

country for export and (2) the evaluation of new establishments from approved countries.

In order for a country to be approved to export meat products to Singapore, AVA considers

the country’s (1) set up and organizational structure of veterinary services, (2) legislation to control

and prevent the introduction of animal and poultry diseases in the country, (3) legislation governing

slaughterhouses, meat processing establishments, meat inspection system, storage, handling and

distribution of products, (4) licensing authority and licensing system of approved export abattoirs

and meat processing establishments, and (5) national microbiological and residue control programs.

These information must be provided by the competent authority of the exporting country for AVA’s

consideration.

Applications from export slaughterhouses and meat processing establishments can only then

be considered after the exporting country has been approved for export to Singapore. All applications

will have to be submitted through the competent authority of the exporting country. AVA will then

again proceed to the establishment before granting approval to export to Singapore.

According to the AVA website, the Philippines has been approved to export pork products to

Singapore, but not for beef, mutton, and poultry. Also according to AVA sources, “the Philippines has

been evaluated and approved in 2008 for the export of products (raw and processed) to Singapore.

However, the export of raw pork to Singapore has been suspended due to the detection of Ebola

Reston Virus (ERV) in the country. AVA would only be able to allow the export of raw pork to

Singapore if the competent authority (i.e. Department of Agriculture) of the country is able to conduct

surveillance in the pig population and confirm that there is absence of ERV in this species of animal.

AVA has informed the competent authority on this requirement but unfortunately they are unable to

carry the surveillance at this time.” On the other hand, the sources added that Singapore is still able

to consider Philippine exports of processed pork (applications for which must be verified and

endorsed by the National Meat Inspection Service (NMIS) of the Department of Agriculture).

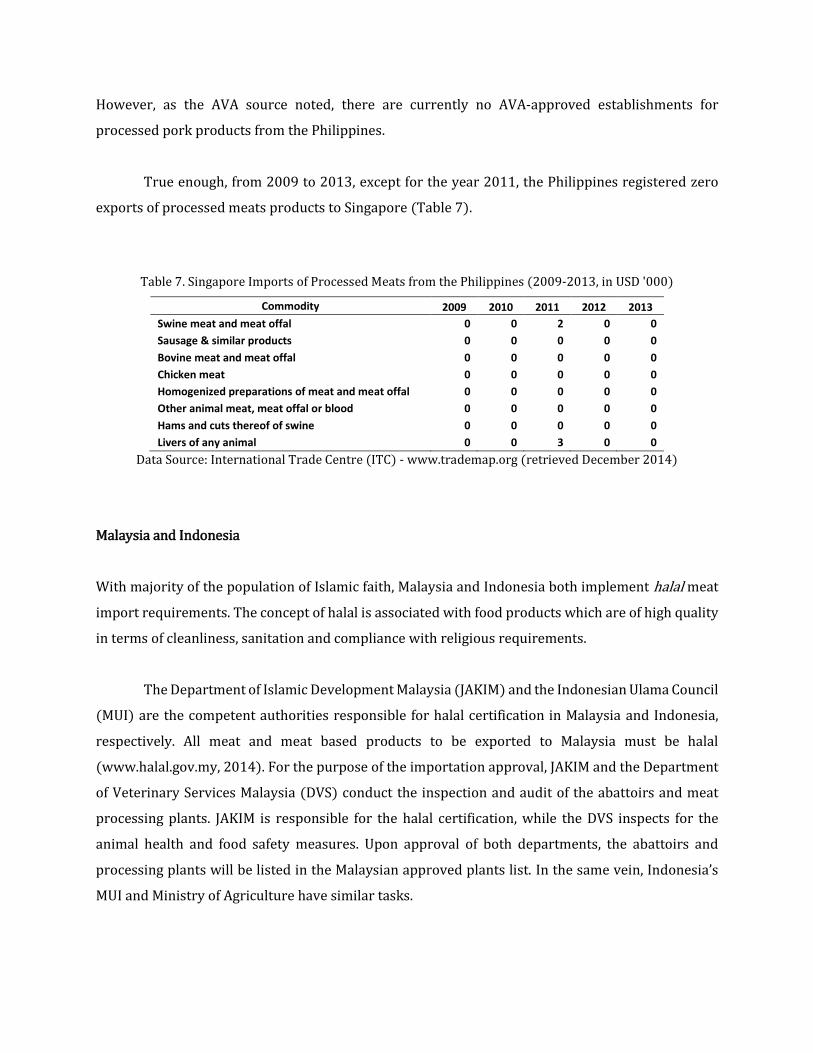

However, as the AVA source noted, there are currently no AVA-approved establishments for

processed pork products from the Philippines.

True enough, from 2009 to 2013, except for the year 2011, the Philippines registered zero

exports of processed meats products to Singapore (Table 7).

Table 7. Singapore Imports of Processed Meats from the Philippines (2009-2013, in USD '000)

Commodity 2009 2010 2011 2012 2013

Swine meat and meat offal 0 0 2 0 0

Sausage & similar products 0 0 0 0 0

Bovine meat and meat offal 0 0 0 0 0

Chicken meat 0 0 0 0 0

Homogenized preparations of meat and meat offal 0 0 0 0 0

Other animal meat, meat offal or blood 0 0 0 0 0

Hams and cuts thereof of swine 0 0 0 0 0

Livers of any animal 0 0 3 0 0

Data Source: International Trade Centre (ITC) - www.trademap.org (retrieved December 2014)

Malaysia and Indonesia

With majority of the population of Islamic faith, Malaysia and Indonesia both implement halal meat

import requirements. The concept of halal is associated with food products which are of high quality

in terms of cleanliness, sanitation and compliance with religious requirements.

The Department of Islamic Development Malaysia (JAKIM) and the Indonesian Ulama Council

(MUI) are the competent authorities responsible for halal certification in Malaysia and Indonesia,

respectively. All meat and meat based products to be exported to Malaysia must be halal

(www.halal.gov.my, 2014). For the purpose of the importation approval, JAKIM and the Department

of Veterinary Services Malaysia (DVS) conduct the inspection and audit of the abattoirs and meat

processing plants. JAKIM is responsible for the halal certification, while the DVS inspects for the

animal health and food safety measures. Upon approval of both departments, the abattoirs and

processing plants will be listed in the Malaysian approved plants list. In the same vein, Indonesia’s

MUI and Ministry of Agriculture have similar tasks.

Both Indonesia and Malaysia also appoint foreign halal certification bodies who shall monitor

and execute a supervisory role in matters of halal at the plant concerned. It should be noted though

that the halal certificate issued by the recognized certification body will only be valid upon approval

from the Malaysian and Indonesian authorities. Malaysia recognizes two halal certification bodies

from the Philippines: the Islamic Da’wah Council of The Philippines (IDCP) and the National

Commission on Muslim Filipinos (NCMF) (www.halal.gov.my, 2014). Indonesia, on the other hand,

recognizes the Office of Muslim Affairs (OMA) (now National Commission for Muslim Filipinos

(NCMF)) (www.halalmui.org, 2014).

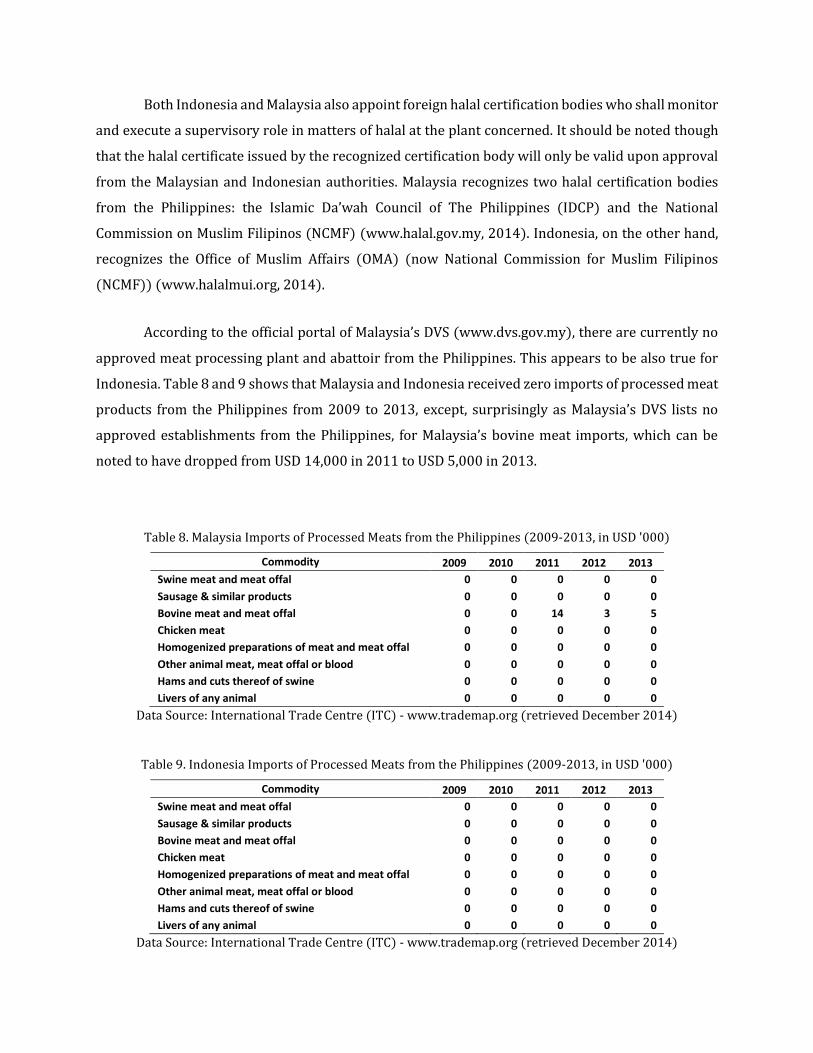

According to the official portal of Malaysia’s DVS (www.dvs.gov.my), there are currently no

approved meat processing plant and abattoir from the Philippines. This appears to be also true for

Indonesia. Table 8 and 9 shows that Malaysia and Indonesia received zero imports of processed meat

products from the Philippines from 2009 to 2013, except, surprisingly as Malaysia’s DVS lists no

approved establishments from the Philippines, for Malaysia’s bovine meat imports, which can be

noted to have dropped from USD 14,000 in 2011 to USD 5,000 in 2013.

Table 8. Malaysia Imports of Processed Meats from the Philippines (2009-2013, in USD '000)

Commodity 2009 2010 2011 2012 2013

Swine meat and meat offal 0 0 0 0 0

Sausage & similar products 0 0 0 0 0

Bovine meat and meat offal 0 0 14 3 5

Chicken meat 0 0 0 0 0

Homogenized preparations of meat and meat offal 0 0 0 0 0

Other animal meat, meat offal or blood 0 0 0 0 0

Hams and cuts thereof of swine 0 0 0 0 0

Livers of any animal 0 0 0 0 0

Data Source: International Trade Centre (ITC) - www.trademap.org (retrieved December 2014)

Table 9. Indonesia Imports of Processed Meats from the Philippines (2009-2013, in USD '000)

Commodity 2009 2010 2011 2012 2013

Swine meat and meat offal 0 0 0 0 0

Sausage & similar products 0 0 0 0 0

Bovine meat and meat offal 0 0 0 0 0

Chicken meat 0 0 0 0 0

Homogenized preparations of meat and meat offal 0 0 0 0 0

Other animal meat, meat offal or blood 0 0 0 0 0

Hams and cuts thereof of swine 0 0 0 0 0

Livers of any animal 0 0 0 0 0

Data Source: International Trade Centre (ITC) - www.trademap.org (retrieved December 2014)

Brunei

Like Malaysia and Indonesia, Brunei, being also a predominantly Muslim country, implements halal

requirements for its food imports. Brunei's national notification authority for sanitary and

phytosanitary measures is the Department of Agriculture in the Ministry of Industry and Primary

Resources. SPS measures are implemented by: the Department of Agriculture for plants and plant

products, live animals, and eggs and other fresh animal (non-halal) products; the Ministry of

Religious Affairs for halal meat products; the Fisheries Department for fish and fisheries products,

and the Forestry Department for forestry products (www.wto.org, retrieved 2014).

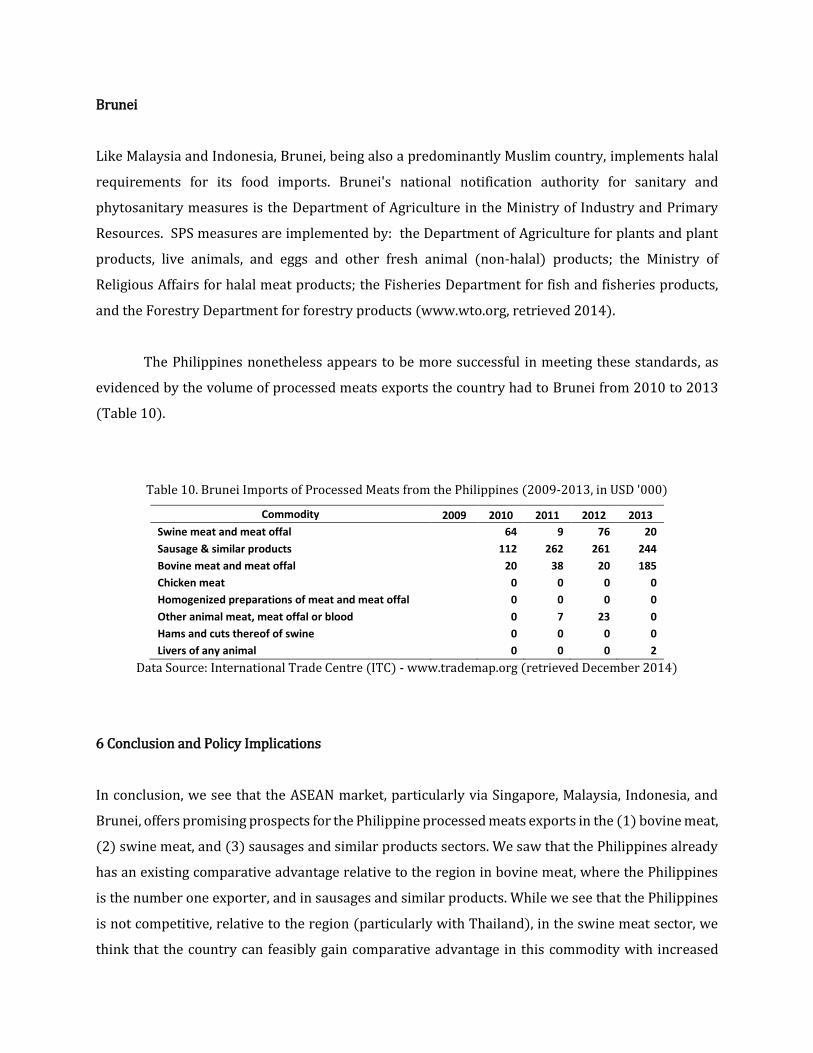

The Philippines nonetheless appears to be more successful in meeting these standards, as

evidenced by the volume of processed meats exports the country had to Brunei from 2010 to 2013

(Table 10).

Table 10. Brunei Imports of Processed Meats from the Philippines (2009-2013, in USD '000)

Commodity 2009 2010 2011 2012 2013

Swine meat and meat offal 64 9 76 20

Sausage & similar products 112 262 261 244

Bovine meat and meat offal 20 38 20 185

Chicken meat 0 0 0 0

Homogenized preparations of meat and meat offal 0 0 0 0

Other animal meat, meat offal or blood 0 7 23 0

Hams and cuts thereof of swine 0 0 0 0

Livers of any animal 0 0 0 2

Data Source: International Trade Centre (ITC) - www.trademap.org (retrieved December 2014)

6 Conclusion and Policy Implications

In conclusion, we see that the ASEAN market, particularly via Singapore, Malaysia, Indonesia, and

Brunei, offers promising prospects for the Philippine processed meats exports in the (1) bovine meat,

(2) swine meat, and (3) sausages and similar products sectors. We saw that the Philippines already

has an existing comparative advantage relative to the region in bovine meat, where the Philippines

is the number one exporter, and in sausages and similar products. While we see that the Philippines

is not competitive, relative to the region (particularly with Thailand), in the swine meat sector, we

think that the country can feasibly gain comparative advantage in this commodity with increased

investments in physical capital, as the country already has the necessary human capital revealed to

be required for this particular commodity. Finally, though, we find that ASEAN non-tariff barriers,

such as Singapore’s strict sanitary and phytosanitary standards and Malaysia’s and Indonesia’s

unique (and strict) halal standards, remain the primary challenge in accessing these countries’

markets.

Government policy and action should thus focus, not only on increasing (physical) capital

investments in these sectors, but also in making relevant institutions more competitive, proactive,

and financially equipped in ensuring that the local industry and qualified producers pass its

promising trade partners’ import standards. In addition, government policy and action geared

towards setting up systems that will strengthen the local industry’s and producers’ compliance with

strict and unique international import standards will also be very helpful in making the export sector

more competitive. It would be worthwhile to note at this point that the Philippine government, for

example, not only sees the potential of the global halal food market for Philippine exporters but has

also been devising plans and making actions in supporting and strengthening the country’s halal food

production. For example, the Philippine government via such agencies as the Department of Trade

and Industry (DTI), the Department of Agriculture (DA), and the National Commission on Muslim

Filipinos (NCMF) has been undertaking wide-ranging initiatives in setting up Mindanao as the

country’s Halal Food Basket, with the Autonomous Region in Muslim Mindanao (ARMM) as the focal

area for the Halal Industry development thrust (www.gov.ph, 2014) (see the Appendix (Philippine

Halal Industry Initiatives) for more interesting details).

As a final word, the ASEAN Economic Community does aim for a single market that removes

barriers to trade. However, we see that there are still important non-tariff barriers that must be

hurdled by the Philippines in order to fully capture the opportunities in the ASEAN market. We

believe though that with stronger and more competent institutions as well as with greater policy and

investment support to the local industry and producers, the Philippines can feasibly capture these

opportunities.

References

Agri-Food & Veterinary Authority of Singapore (http://www.ava.gov.sg/)

“ASEAN Economic Community Blueprint.” (2008). Jakarta: ASEAN Secretariat.

Balassa, B. (1965). “Trade Liberalization and “‘Revealed” Comparative Advantage”. The Manchester

School of Economics and Social Studies, Vol. 33, No. 2, pp. 99-123.

Department of Veterinary Services (Malaysia) (http://www.dvs.gov.my/en/).

Halal Malaysia (Official Portal for the Malaysian Halal Hub) (http://www.halal.gov.my/)

Indonesian Ulama Council (http://www.halalmui.org/)

International Trade Center – Market Analysis and Research (2014). Trade statistics for international

business development. Monthy, quarterly and yearly trade data. Import & export values, volumes,

growth rates, market shares, etc. (TRADE MAP). Retrieved December 2014, from ITC – TRADE MAP database.

http://www.trademap.org/Index.aspx.

“Mainstreaming Food Security.” (2014, February 21,). Official Gazette. (http://www.gov.ph/)

Shirotori, M., Tumurhudur, B., & Cadot, O. (2010). “Revealed Factor Intensity Indices at the Product

Level”. New York and Geneva: United Nations Conference on Trade and Development.

Trade Policy Review (Brunei) (2008). World Trade Organization. (http://www.wto.org/).

United Nations Conference on Trade and Development – Trade Analysis Branch (2007). Revealed

Factor Intensity Indices. Retrieved December 2014, from UNCTAD database. http://r0.unctad.org/ditc/tab/research.shtm

Appendix

Country codes used in this paper

Country Code

Philippines PHL

Brunei BRN

Cambodia KHM

Indonesia IDN

Laos LAO

Malaysia MYS

Myanmar MMR

Singapore SGP

Thailand THA

Vietnam VNM

Table 2. ASEAN (excluding Philippines) Imports of Processed Meats from 2010 to 2013

PRODUCT ASEAN Imports from World

2010 2011 2012 2013 AVE

Swine meat and meat offal 22,662 27,913 32,627 31,990 28,798

Sausage & similar products 24,602 30,643 27,745 39,172 30,541

Bovine meat and meat offal 21,785 27,265 32,580 38,727 30,089

Chicken meat 68,539 77,247 82,543 91,059 79,847 Homogenized preparations of meat and meat offal 2,675 4,386 9,030 8,465 6,139

Turkey meat and meat offal 3,865 4,001 5,011 4,945 4,456

Hams and cuts thereof of swine 1,865 2,665 3,332 4,055 2,979

Other fowl meat and meat offal 2,074 2,353 3,063 4,691 3,045

Livers of any animal 534 765 623 825 687

Shoulders and cut thereof of swine 420 510 281 209 355

Data Source: International Trade Centre (ITC) - www.trademap.org (retrieved December 2014)

Table 3a. Revealed Comparative Advantage* of each ASEAN-member country in the Processed Meats Sector

relative to the world

Commodity PHL BRN KHM IDN LAO MYS MMR SGP THA VNM

Sausage & similar products 0.27 0.00 0 0.001 0 0.10 0 0.05 1.03 0.00 Homogenized preparations of meat and meat offal 0.06 0.00

0 0.001

0 0.11

0 0.12 1.73 0.01

Livers of any animal 0.19 0.00 0 0.000 0 0.00 0 0.00 1.82 0.00

Turkey meat and meat offal 0.00 0.00 0 0.001 0 0.00 0 0.01 0.00 0.00

Chicken meat 0.21 0.00 0 0.000 0 0.07 0 0.01 30.38 0.00

Other fowl meat and meat offal 0.00 0.00

0 0.000

0 4.96

0 0.01 17.46 0.00

Hams and cuts thereof of swine 0.08 0.00

0 0.000

0 0.00

0 0.01 0.30 0.00

Shoulders and cut thereof of swine 0.00 0.00

0 0.000

0 0.00

0 0.00 0.01 0.00

Swine meat and meat offal 0.36 0.00 0 0.000 0 0.54 0 0.05 2.38 0.00

Bovine meat and meat offal 0.38 0.00 0 0.000 0 0.04 0 0.05 0.01 0.00 Other animal meat, meat offal or blood 0.19 0.01

0 0.000

0 0.05

0 0.01 0.18 0.00

*RCA calculated from 2013 exports and entire world exports for the denominator

Source of Data: International Trade Centre (ITC) - www.trademap.org (retrieved December 2014)

Philippine Halal Industry Initiatives

From “Mainstreaming Halal Food Production for Food Security.” (2014, February 21).

(http://www.da.gov.ph/)

In the 2004-2010 Medium Term Philippine Development Plan (MTPDP) crafted by NEDA, Mindanao was

specifically cited as the part of the country where Halal Industry has all the ingredients required to realize

our country’s Halal Food Basket. The plan further mentions the Autonomous Region in Muslim Mindanao,

being the only region with Muslim identity, as the focal area for Halal development thrust.

Our very own Agriculture Secretary Alcala had issued directives to mainstream Halal Food Production

into our national food production effort. In recent years, necessary ground work for Halal Food production

had taken place. The Philippine National Standard (PNS) for Halal Food, the code of Halal Slaughtering

Practices and the protocol for Halal Certification had been generated by a group of national agencies such

as the DTI, DA, and the OMA (now National Commission for Muslim Filipinos). The Autonomous Region

in Muslim Mindanao had also developed its own Halal Food Industry Master Plan and Certification Body

along with related measures undertaken by SOCSARGEN or Region 12, Regions 9 and 11.

Today, the Department of Agriculture, through the Bureau of Animal Industry the National Meat

Inspection Service , the Livestock Devt Council , the Bureau of Agricultural Products Standards and and

the Bureau of Fisheries and Aquatic Resources, have lined up the following Halal support projects: Halal

Slaughterhouses, Halal Goat Production , Halal Organic Fertilizer , Halal Aquaculture and so forth. These

require strategic collaboration of stakeholders so that the Halal Food Industry could finally take off. We

have a lot of catching up to do. And we should be confident that with increasing dynamism in the

agricultural sector, Halal Food Industry in the country would not anymore be treated as an alien concept

but a home-grown production drive forming part of our national food sufficiency effort. President Benigno

S. Aguino III, gave a marching order during the Regional Devt. Council -12 meeting in General Santos City

last April 14, 2011 and I quote: “Accelerate the efforts in making the establishment of Halal Industry a

reality.”

REFERENCE:

Dr. Norodin A. Kuit, DA-Halal Food Industry Development Program National Coordinator