opinion new tricks - total telecom telecom plus/tt...‘digiworld’ revenues–telecoms services...

TRANSCRIPT

1

www.totaltele.com

june 2013Business analysis for telecoms professionals

A round-up of some of the major stories reported in our daily news service www.totaltele.com

Magic Circle: Telcos must take advantage of what they know about customers to launch better offers

Balancing Act: On the record with Mansoor Hanif, who talks about UK operator EE’s LTE rollout plans

Four’s a Crowd: Consolidation on the cards in Sweden and Denmark as mobile operators compete over small populations.

Dates for your diary and details of the must-attend events in the telecoms industry over the coming months.

NEWS & VIEWS tEchNology buSINESS gEography EVENtS

For the most part, users of telecoms services are not looking for any-

thing ground-breaking in their interactions with their service provider; they just want some good, old-fash-ioned customer care.

But providing what seems so simple to the customer is often a complex process for the operator. As our feature on p.8 shows, telcos have a wealth of tools and data at their disposal capable of

telling them where their customers are in the network and what they are trying to achieve, thereby enabling them proactively to solve any problems and to create innovative services and pricing models.

And it’s not just about new technologies. Telcos will also need to change their mindsets and behaviour to give customers the kind of interaction they want. The proverb about teaching an

old dog new tricks immedi-ately springs to mind.

Operators also need to pay close attention to their networks to maintain a good customer experience. On p.12 EE’s director of network integration and LTE Mansoor Hanif explains the steps his company has taken to ensure that refarming 1800-MHz spectrum for LTE has a minimal impact on 2G services running in the same frequency.

It is clear that as telecom offerings become more sophisticated, there will be little room for sleight of hand in customer service.

Mary Lennighan, editor [email protected] @TelecomEditor

There is no room for sleight of hand when it comes to ensuring a good customer experience

new tricksopinion

MAGic

circLeTelcos are look-ing to create a virtuous circle that makes their investment more efficient and the customer lifecycle more profitable

feAture

A round-up of the major stories in telecoms in the past month, as reported in our daily news service www.totaltele.com

in brief AnALysis

3

www.totaltele.com

2 – 3 July 2013ETC Venues St Paul’s, London

Book your place today at www.totaltele.com/network For sponsorship information contact us at [email protected]

Profiting through the network

spot tHe DifferenceThe fortunes of Europe’s biggest telcos stand in stark contrast with those of their US cousins. Average European operator revenues decreased by 4%-5% in 2011-2012, while growth in the US was around 4%, according to IDATE’s DigiWorld Yearbook 2013. “Europe’s still a bit of a cause for concern,” admits Steve Durbin, chairman of the think tank’s London institute. Europe’s share of the €3.17 trillion 2012 ‘DigiWorld’ revenues–telecoms services and equipment, software, computer hardware, TV, and consumer electronics–has fallen by 1.5pp over two years to 27%.

But “things may be about to change”, IDATE says, noting that T-Mobile’s acquisition of MetroPCS and the ongoing battle for Sprint could lead to greater competition in the US, which could eat into AT&T and Verizon’s profit margins. “If this trend continues, it would not be surprising to see North American operators return to Europe,” IDATE says.

t itALiA spins off network Telecom Italia will spin off its fixed network into a separate entity, pledging to guarantee equal access to all competing operators.

VeriZon wireLess pAyout Verizon Wireless will pay a $7 billion dividend to 55%/45% owners Verizon Communications and Vodafone, but indicated that there may be no more payouts this year.

cArrier serVices Vodafone has brought together Cable & Wireless Worldwide and the carrier services businesses of its various operating units to create Vodafone Carrier Services, a unit of Vodafone Group Enterprise.

spAin Lte LAuncHYoigo said it will be the first operator in Spain to provide a commercial LTE service when its network goes live in July.

turnoVer cHAnGe 2011-2012

usA eu-5

Source: IDATE

10%8%6%4%2%0%

-2%-4%-6%

10%8%6%4%2%0%

-2%-4%-6%

perc

enta

ge c

hang

e

perc

enta

ge c

hang

e

n Verizon n At&t n sprint n t-Mobile usA

n t-Mobile (Germany)* n orange (france) n Movistar (spain) n tiM (italy) n Vodafone (uk)

*At the level of income from services alone, the turnover of T-Mobile in Germany dropped by 1.5% in 2012

in brief

profiLe

4

www.totaltele.com

$3.7trillion 2013 it & teLecoMs serVices spenDinG

(IDC)

MoVers AnD sHAkers

fcc cHAirMAn-eLect toM wHeeLer Must LeAVe tHe trAppinGs of His forMer Life beHinD

tHe future’s orAnGe France Telecom shareholders approved a formal name change: from 1 July the company will be known as Orange and its share ticker will become ‘ORA’.

spectruM Auction in oZAustralia raised A$2bn from the sale of 700-MHz and 2.5-GHz spectrum. Telstra and Optus won spectrum in both bands, paying A$1.3 billion and A$650 million respectively. TPG Internet paid a small sum for 2.5-GHz airwaves.

Dt Looks eAst Deutsche Telekom is reportedly in talks to acquire GTS Central Europe for around €600 million. The German incumbent may also take full control of T-Mobile Czech Republic.

VoDAfone sues inDiA Vodafone’s Indian unit has begun court proceedings against the country’s Department of Telecoms (DoT) over its refusal to extend the telco’s operating licences in three cities.

cHArLier tAkes on sfrVivendi executive Jean-Yves Charlier was named as the new CEO of SFR as the French mobile op-erator splits its chairman and chief executive roles. Stephane Roussel remains as chairman.

new LeADer for kceLLAli Agan takes over as the new chief executive of Kazakhstan’s Kcell from June. He replaces Veysel Aral.

MAxis seeks A cHief Malaysia’s Maxis is looking for a new CEO after John Dennelind, the man due to take over on 1 July, declined the post for family reasons.

teLe2 russiA’s new boss Former Rostelecom CEO Alexander Provotorov has reportedly been named as the new head of Tele2 Russia, triggering talk of increased cooperation between the telcos.

Lobbyist becoMes LobbieDTom Wheeler, who spent years lobbying the US government on behalf of telcos and cable companies before settling into venture capitalism, has been nominated to take over from Julius Genachowski as chairman of the FCC. “Tom has been at the forefront of some of the very dramatic changes that we’ve seen in the way we communicate and how we live our lives,” said president Barack Obama last month.

But before Wheeler gets down to the serious business of keeping the industry’s most powerful players–AT&T, Verizon and Comcast–in line, he must leave the trappings of his former life behind. Reuters reported recently that Wheeler has agreed to step down from his role at Core Capital Partners and divest holdings in 78 companies, including AT&T, Verizon, Sprint, and Deutsche Telekom. He also owns shares in Apple, Microsoft, Time Warner Cable and others.

“I will divest these assets within 90 days of my confirma-tion and will invest the proceeds in non-conflicting assets,” Wheeler wrote in a letter to the Office of Government Ethics. The government is expected to confirm his nomina-tion this month.

5

www.totaltele.com

stAtistics

reGuLAtionbeyonD borDersIt is no secret that from a telecoms point of view Europe is lagging behind the US. IDATE’s latest numbers (p.3) show the differences in fortunes between some of the biggest operators, while the GSMA has also warned that without policy change Europe will fall further behind; the industry body published a joint study with Navigant Economics that shows mobile connec-tion speeds in the US are 75% faster than in Europe and LTE accounts for a significantly higher proportion of mobile subscribers. “EU regulatory policies have resulted in a fragmented market structure that prevents operators from capturing beneficial economies of scale and scope and inhibits the growth of the mobile ecosystem,” says Jeffrey Eisenach, managing director at Navigant Economics.

Enter Neelie Kroes. The digital agenda commissioner last month pledged to end roaming charges altogether within the 27-member bloc and guarantee net neutrality as part of a proposal aimed at moving towards a single European telecoms market. As it stands, there are few details; Kroes will present her full regulatory package around Easter next year, she told the European parliament. Kroes admitted to members she is “not promising a single market package that gives you everything you dreamed of,” but she did promise “growth stimulated by breaking down barriers.”

sAMsunG’s siZeAbLe sHAreThe global Android smartphone segment generated operating profits of $5.3 billion in the first quarter of this year, with Samsung accounting for a massive 95% of the total, according to Strategy Analytics. Domestic rival LG claimed the next highest share with 2.5%.

210 million smartphone units were sold to end-users in Q1, 64.7 million–or 30.8%–of which were Samsung devices, Gartner reports. Apple came in second with an 18.2% market share, followed by LG with 4.8%.

A rose by Any otHer nAMe...AT&T has a brand value of $75.5 billion, up 10% year-on-year, making it the world’s most valuable telecoms operator brand, according to the Millward Brown Optimor BrandZ 2013 ranking. China Mobile comes in at number two, its brand value having risen by 18% to $55.4 billion.

The pair are the only two telcos in the global top 10, which is headed by Apple, whose brand value comes in at a staggering $185.1 billion. In this year’s ranking Google edged out IBM for second place, their brand values coming in at $113.7 billion and $112.5 billion respectively. BrandZ describes Google as “a serious challenger for the number one spot.”Focused

briefings, key topics

Join us for breakfast in 2013

View the event line-up at www.totaltele.com/

breakfast

in brief

6

www.totaltele.com

biG news

nuts AnD boLtsoss tie-upEricsson, Huawei and Nokia Siemens Networks signed a memorandum of understanding that will see them work together to improve interoperability between OSS systems.

biLLinG firM bouGHtA consortium led by CITIC Capital Holdings agreed to pay US$12 per share–around $890 million–for China’s AsiaInfo-Linkage.

cisco Gets enerGiseDCisco Systems agreed to pay $107 million for energy management specialist JouleX,

ericsson winDs up cAbLeEricsson announced the closure of its copper cable manufacturing operations in Sweden, noting that production has not been at full capacity for a long time and the business has struggled with profit-ability. 354 jobs will go.

VectoreD VDsL DeALs Deutsche Telekom inked a deal to enable Vodafone Germany to use its vectored VDSL network, once it launches. DT also announced a similar agreement with Telefonica.

orAscoM sAys ‘no’Egypt’s Orascom Telecom advised shareholders to reject a US$0.70-per-share offer from Baskindale, noting that advisors have valued the company at $0.86 per share. The deal was not completed as just 15.9% of the telco’s shares were tendered.

cAribbeAn network JV Cable & Wireless Comms and Columbus Networks will combine their subsea networks in Central America and the Caribbean into a JV that will be 72.5%-owned by Columbus.

buLGAriA DeAL Telenor agreed to pay €717 million for Bulgarian mobile operator Globul and its retail partner Germanos.

$1 biLLion bLoG Yahoo will acquire blogging service Tumblr for $1.1 billion in cash.

AM snAps up stArtAmerica Movil agreed to acquire US MVNO Start Wireless and its 1.4 million customers via its own US virtual operator Tracfone.

DisH ups cLeArwire biDAs we were going to press, Dish Network increased its offer for Clearwire to $4.40 per share, a full $1 higher than that already tabled by the mobile broadband operator’s majority owner Sprint Nextel, which is itself the subject of a takeover bid from Dish. The move adds further complication to the web of buyout bids surrounding Sprint; earlier the telco’s proposed acquisition by Japan’s Softbank–Dish’s rival suitor–got the green light from US foreign investment watchdog CFIUS. Keep up with the twists and turns at www.totaltele.com.

europe-cHinA reLAtions The European Commission announced an anti-dumping and anti-subsidy investigation to ascertain whether Chinese mobile network equipment makers have been supplying kit into Europe at below cost or with the backing of state subsidies, enabling them to keep costs low. However, the probe is on hold to allow time for negotiations with Chinese authorities aimed at reaching an amicable solution.

swALLoweD upCanada’s Telus has agreed to acquire smaller rival Mobilicity for C$380 million. Toronto-based Mobilicity launched mobile services in 2010 but failed to gain much ground on the market’s bigger players; Mobilicity has 250,000 customers to Telus’ 7.7 million. Mobilicity is currently undergoing a court-supervised restructuring as it seeks to avoid bankrupt-cy protection. Debtholders and the Ontario Superior Court have approved the Telus acquisition plan.

2 – 3 July 2013ETC Venues St Paul’s, London

Book your place today at

www.totaltele.com/network

For sponsorship information

contact us at

The Business Strategy

Day one Tuesday 2 July 2013

Book your place todayFree attendance for telecom operators!

Quote WDBR when prompted to receive your discount.*

Total Telecom Network Management ShowAgenda highlights:

08:00 Registration and Networking

08:20 Partner Breakfast Briefing: Working group to address challenges posed by growing volumes of mobile video traffic

Matt Stagg, Senior Manager of Network Strategy, Architecture and Design, EE Senior representative from Equinix

09:30 Welcome from the Chair Pieter Veenstra, Architect, KPN

09:40 Panel Discussion: Why network management is THE big issue for operators and enterprises today

Moderator: Pieter Veenstra, Architect, KPN Yusuf Kıraç, Network Director, Türk Telekom Philip Marnick, CTO, UK Broadband Javan Erfanian, Distinguished Member of Technical Staff, Bell Mobility

10:10 New Network Business Models: Best practices for the 21st century Samer Salameh, CEO, Azteca Telecom with Grupo Salinas and CE, TotalMovie

10:40 Network Sharing: Reducing costs, and promoting competition and investment

Eduardo Martinez Rivero, Head of Unit, Antitrust Telecoms Unit, Competition Directorate-General, European Commission

11:10 Speed Networking & Morning Coffee

Profitingthrough the

network

8

www.totaltele.com

8

www.totaltele.com

“We know how to make people pay for things,” said

Gervais Pellissier, Orange’s CEO-in-waiting, at May’s Management World event.

At the time, Pellissier was trying to make a case for the upside of the telco future, but the line also contrasted with an underlying worry for many in his audience: that telcos are in fact losing the knack of making people pay for things. Accordingly, there is widespread under-standing that if the customer relationship is a key strategic advantage, then finding ways to deepen and widen that relationship is a must.

One way operators have tried to do this is to imple-ment the much-referenced and sometimes-hyped customer experience management (CEM) strategy. This model points all of a telco’s guns at the same target–understanding an individual customer’s context and overall service experi-ence–so that the network and operations teams on one hand, and the customer service and marketing teams on the other, have the best information at hand to make aligned decisions.

“You hear a lot of hype about CEM, but most of what

people are really doing is still fixing faults,” says Steve Buck, head of marketing and OSS at Amdocs. “What’s more interesting is looking at the complete experience and understanding when to give better bandwidth, when to send a campaign, when to apologise, [and] what to say in customer service when someone rings up.”

Before telcos can hope to understand and respond appropriately according to an individual customer’s experience, they must first understand what is happen-ing in their networks.

But that is easier said than done. Doug Fantuzzi, VP and general manager of product marketing for service assurance company JDSU, says that it is theoretically

possible to put probes everywhere throughout the network, ideally as close to the customer, as possible.

“The closer you can get to the user, the more accurate you can be, but this is clearly not a cost-effective approach, so telcos must select what data they want to extract,” he says. “That means not duplicating data collection and deploying tools to sift through data to determine what is of value and what is not.”

custoMer inequALityHowever much data is collected, using it as part of a drive to serve the customer better means the way an operator thinks about its network operations must change.

Telcos must take advantage of what they know about customers to launch better offers and ensure their networks are optimised to support them.

MAGic circLeserVinG tHe custoMer

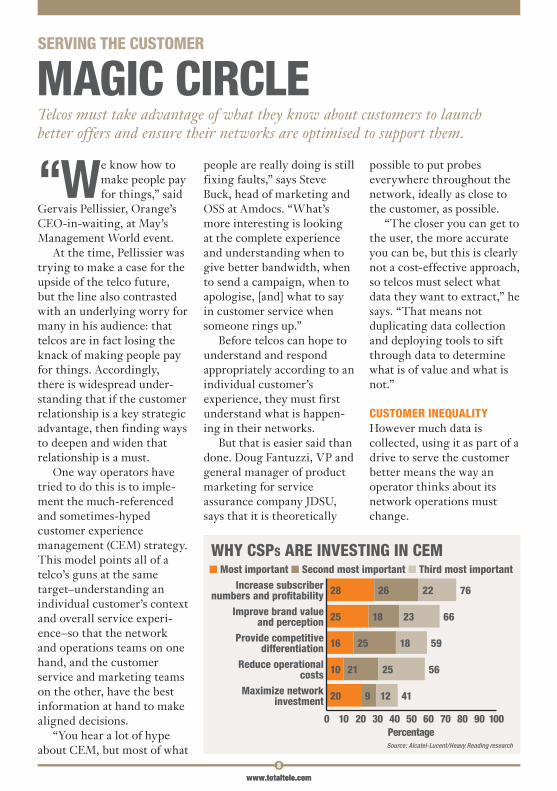

wHy csps Are inVestinG in ceM

0 10 20 30 40 50 60 70 80 90 100

20 9 12 41

10 21 25 56

16 25 18 59

25 18 23 66

28 26 22 76increase subscriber numbers and profitability

improve brand value and perception

provide competitive differentiation

reduce operational costs

Maximize network investment

Source: Alcatel-Lucent/Heavy Reading research

n Most important n second most important n third most important

percentage

9

www.totaltele.com

For Fantuzzi, operators must establish what data to collect “based on the user, device, application, time and location, because every customer is not equal”. For example, by knowing the value of a customer within a traffic hotspot where throughput is clearly an issue, and knowing what the customer is trying to achieve, an operator can ascertain whether it needs to invest in more capacity or an offload strategy for that hotspot. Fantuzzi points to MTN in South Africa as having taken this approach, aligning its capacity investment with the value of its subscribers.

Telcos need to develop “systempathy”; that is, systems with a greater awareness of what a subscrib-er is trying to achieve when they access the network, advised Birger Thorburn, CIO of Cable & Wireless Communications, at April’s Breakfast with Total

Telecom event. “We need to add context to our interac-tion” with the customer, he says.

Attaining this level of understanding is not easy though. “Our surveys of customers have said the problem is not so much collecting the data but correlating it into something meaningful,” says Amdocs’ Buck. “Something like overall cell throughput is a lot easier to see than [it is] to understand who within that cell is getting a reasonable experience but is a high value customer and would benefit from the delivery of a better-than-reasonable experience at certain times,” he says. “This is why people are focussing on faults.”

For Buck, correlating all that data is the key to bringing the operational and business systems of a telco together. “The network provides really valuable information that can be

connected to the care agent, or bill, or campaigns, and the other way round is true as well, which is that customer information helps you direct where you want your network,” he says.

Meanwhile, C&W’s Thorbun believes that over-the-top (OTT) players are showing the way when it comes to engaging with customers. “They have built an experience around being connected and their interac-tions are all very public,” he says. Telcos need to be less transactional about how they communicate with custom-ers, he adds. “It will require quite a culture change about how we interact.”

stArt witH tHe enD in MinDOne telco that has recently invested in a CEM strategy that tries to go beyond fault management and do some of the difficult correlation Buck talks about is Zain Kuwait.

Zain’s manager of information planning and development, Almuhanna Jaber, says that working with Nokia Siemens Networks the operator has segmented its subscriber base in a more granular way, and taken a more intelligent approach to the offers and campaigns it brings to market.

“For example, it was noticed that there were some subscribers who started using high end devices prior to their being available in our market,” he explains. “Users of these smartphones were some of our highest

tHe probLeM is not so MucH coLLectinG DAtA but correLAtinG it

cHAnGes to csps’ ceM buDGets 2013

Source: Alcatel-Lucent/Heavy Reading research

increase 67% no change 24%Decrease 3%Don’t know/not sure 6%

67%3%

24%

6%

10

www.totaltele.com

data and voice users. Now we can send out promotions for the newest devices and advanced services to this group and get a better hit rate for the campaigns because we know they are early adopters.”

Jaber says Zain embarked upon its CEM strategy with three goals in mind: to deliver superior voice service experiences to customers; to have proactive care and problem resolution; and to be able to measure an individual customer’s level of satisfaction.

“The journey began with improvements in the core network KPIs using real-time monitoring, then it evolved towards service monitoring and customer experience monitoring,” he says. “There was a wealth of customer data to be sorted, but the strategy was to use the right data for the right conclusions rather than trying to use everything available.”

Zain started each implementation exercise by asking “what is the end result we want?” Jaber says. “Building from there was a tremendous help in over-coming challenges of integration and correlation because everything was started with the end result in mind.”

pLAnneD pricinGMany telcos are also building on this intelligent network approach by using their increased awareness of customer segmentation to

innovate with pricing. Martin Morgan, marketing manager at Openet, makes it his business to track these approaches, as many of them are built upon the policy and real-time charging engines that his company, amongst many others, provides.

“We are seeing networks as a marketing tool and an enabler of new service bundles, and the main catalyst is speed,” he says, listing Sweden’s Telia, which prices on volume and speed, and Swisscom, which prices on speed tiers, as examples.

However, many telcos are also using real-time charging capabilities to enable per-day or per-month packages allied to specific applications-based charging, enabled by policy control. Turkcell has launched a Facebook data plan and social network package for $2 per month that drove a 17% ARPU gain from users who signed up, claims Morgan. Malaysian operator Digi offers prepaid customers five days’ unlim-ited access to messaging service WhatsApp for $1.64, while Orange Slovakia has around 40 individual data tariffs built around different content packages. Kuwait’s Wataniya uses a similar approach for its data roaming bundles, offering a daily pass of 20MB for $17.50.

Such pricing models have achieved a measure of success. Orange France says it has seen its Origami offer, which includes access to music streaming service

Deezer, reduce churn amongst those users by 50%. Israel’s Pelephone claims its policy of upselling volume and double-speed add-ons on top of a basic data plan has driven a 25% data ARPU increase and reduced the churn rate of subscribers to its cloud services by 25%. Meanwhile Canadian telco Rogers Wireless offers a data pass aimed at infrequent data users, and claims that by providing those users with a clearer picture of how much data they are using, it has converted 5% of them to a postpaid data plan.

The key for Morgan is that these innovative pricing arrangements are not static but are built on the correla-tion between customer information and a real-time outbound marketing system that can trigger, if applicable, a context-sensitive marketing offer to be sent to the customer’s device.

Going forward, will telcos be able to maintain that crucial advantage spelled out by Orange’s Pellissier, namely their ability to “make people pay”? If telcos can take advantage of what they truly know about the customer then they can not only make better customer offers, but they can also ensure their networks are optimised to support these offers, creating a virtuous circle that makes the telco’s investment more efficient and the customer lifecycle more profitable.

By Keith Dyer

9 - 10 October 2013, Grand Connaught Rooms, London

Understanding the business of telecoms

2 day, leading telecoms finance and investment conference for telecoms

executives and the financial community

Book now to save up to £300! www.totaltele.com/financesummit

12

www.totaltele.com

12

www.totaltele.com

12

www.totaltele.com

in April EE announced it will refarm another 10 MHz of 1800-MHz

spectrum to double the speed of its UK LTE network, and revealed plans to trial LTE-Advanced Carrier Aggregation (CA). Mansoor Hanif, EE’s director of network integra-tion and LTE, talks to Total Telecom assistant editor Nick Wood about spectrum, small cells, and maintaining legacy networks.

EE acquired a large amount of 2.6-GHz spectrum in the recent auction. How you are going to use it?We’ve announced that we are going to double speeds on 1800-MHz, and we’ve already got a strategy in place for the next five-to-10 years, including the next carriers we’re going to use. We can’t reveal that [strategy], but we have revealed that we will be experimenting with carrier aggregation (CA) – the first step of LTE-Advanced. We can’t say too much about which frequency band we’ll use, but we will have field trials later this year.

In terms of 2600-MHz, it’s a fantastic acquisition. It secures our long-term strategy and future for many years to come.

Did EE look at acquiring any of the unpaired spectrum on offer at the auction?We looked at it but we didn’t see it as a high priority. The TDD ecosystem is still very far behind [FDD]. We looked at the roaming implications around the world and saw that TDD is not a dominat-ing technology.

TDD spectrum is good for some niche operators and would be good for some kind of backhaul solution. It could also be very good for broadcasters, so I totally get why BT went for it. If they are going to give away football matches for free they’re going to need some bandwidth so they can do it over wireless in local areas.

How do you ensure that refarming 1800-MHz spectrum for LTE has a minimal impact on 2G services running in the same frequency?It’s not easy. We spent a lot of time, effort and money to prepare the re-farming

months in advance on a city-by-city basis. We do extensive capacity analysis [and] we also align with the commercial and marketing teams to understand the mix of 2G handsets in the area. Then we take corrective actions all the time to shift traffic up and down from the 3G layer. We do a lot of work to make sure we get the right mix in the right area because the traffic on our network is not homogeneous.

It’s a very dynamic atmosphere. If you plan ahead six months, by the time you come to the next phase, you’ve got to re-check everything from the beginning because things have moved.

For example, the iPhone 5 launch changed the whole traffic pattern on 3G, because a lot of iPhone 4S apps used WiFi by default, but the iPhone 5 uses cellular by default, so all the networks in the UK saw a big step change.

Mansoor Hanif describes how EE is driving forward with its LTE plans while continuing to serve customers on its 2G network

bALAncinG Acton tHe recorD

we tAke correctiVe Actions to sHift trAffic up AnD Down froM tHe 3G LAyer

13

www.totaltele.com

13

www.totaltele.com

13

www.totaltele.com

EE is also rolling out DC-HSPA. Why is that important?When an LTE customer makes a voice call they fall back to 3G. If you use data during a call, or use data when you’ve finished a voice call, you would notice a really slow data experience, which we don’t want.

We cover about 75% of the population [with DC-HSPA]. It means that in 50% of the UK we’ve got 4G coverage, and in all the areas where we don’t, we have the best of 3G. Right from the beginning we made it clear to our suppliers that we wanted all our 4G handsets to have 42 Mbps (peak DC-HSPA speed) capability as well [as LTE].

Our competitors try to make a big noise about [DC-HSPA] being like 4G, but it’s not. It’s a good technology but it’s not as stable or pervasive as 4G.

How do metro small cells fit into EE’s roadmap?I love the whole concept of small cells, especially the metro coverage. We’ve got a lot of people lobbying us to work with them on it, and we’re talking to several partners for trials but we’re not yet convinced that this is the way forward for us.

There will be some areas where it would make sense to do it, in other areas it wouldn’t. It’s down to the overall cost of ownership, and the overall opex.

The small cell roadmap is behind the macro cell

[roadmap], which is a struggle for us, but if we have partners coming to us with ground-breaking small cells that can keep pace with our macro network, then why not?

What infrastructure, besides the access and backhaul, needs upgrading before you can offer the really fast mobile broadband speeds?We’re living in a TCP/IP world – the Internet world. The protocols were designed to work over not very reliable networks, so they are resilient, but they weren’t designed for speeds of 80 Mbps and above, especially over wireless.

If you want loads of people using speeds that high or above, the whole ecosystem needs to adapt: the application world; the operating system world; the FTP servers; the Internet servers; even WiFi. People used to say ‘we’ll just offload to WiFi’, but now the industry is going beyond WiFi speed.

You need to push the ecosystem. It will start off in some high-tech areas and in sectors like finance. I think it will take around the same time as it took IPv6 to roll out, so a transition period of about five years.

In the device field, the biggest challenge is heat management. A small device, at that type of speed, burns your device; it just gets hot. You need to manage heat dissipation.

How have you optimised the network to deliver video?There are a number of different areas. One is caching. If you can get the video closer to the user, it offers a massive improve-ment in performance and you don’t need to spend quite so much on the backhaul, so we’re interested in that.

Another is compression. When you’re on a mobile and moving quickly, the radio environment is variable: you might get 20 Mbps one second, which would enable HD video streaming, but the next it might drop to 5 Mbps and then to 2 Mbps. What we’re interested in is making the most of the bandwidth available, and automatically making the system fit the right video quality to the pipe. With GPRS and 3G you used to start off with the lowest bitrate and then step it up, because you assumed there was very little band-width. We don’t like that. We want to use the maxi-mum we’re confident with and step down only when needed.

We’re also looking at video broadcast. If you have 500 users in a cell and you want to let them all watch a TV channel it takes a lot of bandwidth. But with technology like eMBMS (evolved multimedia broadcast multicast services) they can all tune into the same channel, which optimises the bandwidth usage.

14

www.totaltele.com

GeoGrApHy: scAnDinAViA

four’s A crowD

wAtcH tHis spAcePeder Ramel, CEO of 3 Scandinavia, told Swedish newspaper Dagens Industri last month that consolidation will come in the Swedish and Danish mobile markets, and that his company will be a willing partici-pant, as a buyer. Tele2 is seen as a likely target, but a merger between 3 and Telenor in Sweden has also been mooted, while TeliaSonera is having a tough time in Denmark.

wAr ZonesWith the number of mobile subscribers well exceeding the populations in Sweden and Denmark, operators are having to fight hard for market share. LTE is the next big battleground and analysts are already warning of a price war in Denmark.

MobiLe MArket sHAres (enD-2012)

Source: operators, Statistics Sweden, denmark.dk

Consolidation on the cards in Sweden and Denmark where mobile operators are battling for their share of a small population

5.4m MobiLe

broADbAnD subs in DenMArk in 2H 2012

(Danish Business Authority)

62% sMArtpHone

penetrAtion in sweDen(ADL/Exane BNP Paribas)

operAtors HAVe sAiD DenMArk’s four-pLAyer structure is unsustAinAbLe(aDl/Exane bNp paribas)

teliasonera 46% telenor 17%tele2 26% 3 11%

46%11%26%

17%

teliasonera 23% telenor 31%3 13% tDc 33%

13%

23%33%

31%

DenMArktotAL: 6.45MpopuLAtion:

5.58M

sweDentotAL: 14.28MpopuLAtion:

9.57M

15

www.totaltele.com

15

www.totaltele.com

coMMunicAsiA18-21 June 2013Marina Bay Sands, Singapore www.communic asia.com

network MAnAGeMent sHow2-3 July 2013ETC Venues St Pauls, London, UKwww.totaltele.com/network

ipx suMMitAutumn 2013

cALenDAr contActs

© 2013. All rights reserved. Terrapinn Holdings Ltd registered office: 4th Floor Welken House, 10-11 Charterhouse Square, London EC1M 6EH

eDitoriAL4th Floor, Welken House, 10-11 Charterhouse Square, London EC1M 6EH +44 (0)20 7608 7030; [email protected]

editor Mary Lennighanmary.lennighan @totaltele.comT +44 (0) 20 7608 7069 Assistant editor Nick Woodnick.wood @totaltele.comT +44 (0) 20 7608 7046Art editor Michelle [email protected] +44 (0) 7956 946374 ADVertisinGManaging Director and publisher Rob Chambersrob.chambers @totaltele.comT +44 (0) 20 7608 7077

business Development Manager Charles Georgioucharles.georgiou @totaltele.comT +44 (0) 20 7608 7071business Development Manager Claudia [email protected] +44 (0)20 7608 7027business Development Manager Sarah Abdelaalsarah.abdelaal @totaltele.comT +44 (0)20 7608 7065sales Manager Oliver Chandleroliver.chandler @totaltele.comT +44 (0)20 7608 7041

usA east contactKaren C. Smith-Kernc KCS [email protected] +1 717 397 7100

west & canada contactAlan A, Kernc KCS [email protected] +1 717 397 7100F +1 717 397 7800

eVentsconference DirectorMatthew Seckermatthew.secker @totaltele.comT +44 (0)20 7608 7039

MArketinGMarketing Director Tally Judgetally.judge @totaltele.comT +44 (0) 20 7608 7076

custoMer serVice customer services ManagerAleisha Bryantaleisha.bryant @totaltele.comT +44 (0)20 7608 7042

London, UKrob.chambers @totaltele.com

teLecoMs worLD MiDDLe eAst30 Sept-2 Oct 2013Jumeriah Beach Hotel, Dubaiwww.terrapinn.com

totAL teLecoM finAnce suMMit 9-10 Oct 2013Grand Connaught Rooms, London, UKwww.totaltele.com/ financesummit

cArriers worLD 15-16 October 2013 Jumeirah Carlton Tower, London, UK www.totaltele.com/carriersworld

Personal touch

World Communication Awards 2013

World Communication AwardsFor global communications providers

3 December 2013Lancaster Hotel, Londonwww.worldcommsawards.com

ENTRIES NOW OPENVisit www.worldcommsawards.com for the full list of award categories and the entry form

Closing date: Friday 5 July 2013

For sponsorship opportunities callOliver Chandler +44 (0)207 608 7023

Organised by:Sponsored by:

AsiA coMMunicAtion

AwArDs20 June, Singapore

BOOK YOUR TABLEwww.asiacomms

awards.com