one theme, multiple opportunities · pdf fileone theme, multiple opportunities* please refer...

TRANSCRIPT

One theme, multiple opportunities*

Please refer page 22 for product labelling*For complete details on investment strategy, please refer to SID/KIM

October 2017

Introducing HDFC Housing Opportunities Fund

Demand for Housing in India

Source: Census of India, Ministry of Statistics & Programme Implementation (MoSPI), National Sample Survey Office (NSSO),CLSA , Report of the Technical Group on Urban Housing Shortage (2012-17), Working Group on Rural Housing for XII Five Year Plan. 2

Ÿ Total incremental demand for housing 1 Cr+ paŸ Total opportunity over the next 3 years expected to be ~ 7 Cr houses

Ÿ Estimated housing shortage - ~ 4 Cr houses (urban & rural)Ÿ In addition, the following growth drivers contribute to incremental need for housing

Current population growth @ 1.3% pa

Ongoing nuclearisation@ 0.9% pa

Rising income/aspirations -per-capita GDP growthat 9-10% pa nominal

Demand for 34 lakhhouses pa

Demand for 25 lakhhouses pa

Demand for 40-50 lakh houses pa

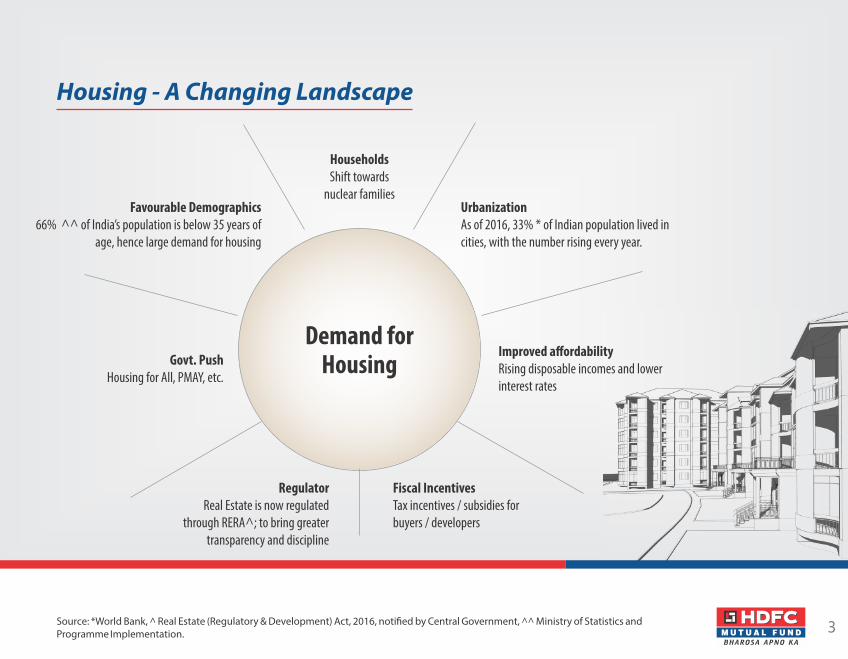

Source: *World Bank, ̂ Real Estate (Regulatory & Development) Act, 2016, noti�ed by Central Government, ̂ ^ Ministry of Statistics and Programme Implementation. 3

HouseholdsShift towards

nuclear families

Housing - A Changing Landscape

UrbanizationAs of 2016, 33% * of Indian population lived in cities, with the number rising every year.

Favourable Demographics66% ^^ of India’s population is below 35 years of

age, hence large demand for housing

Improved affordabilityRising disposable incomes and lower interest rates

Govt. PushHousing for All, PMAY, etc.

Fiscal IncentivesTax incentives / subsidies for buyers / developers

RegulatorReal Estate is now regulated

through RERA^; to bring greater transparency and discipline

Demand for Housing

A Simple Quiz

4

“2017 has been a watershed year for housing. The last Union Budget will go down as the ‘Affordable Housing Budget’. ” - Deepak Parekh - Chairman, HDFC Ltd

A.�Luxury�Segment

B.�Penthouses

C.�Affordable�Segment

D.�Vacation�Homes

Which segment of housing in India is expected to see strong demand and supply in the next 3 to 6 years?

thSource: Economic Times, 26 September 2017

The snapshot of news articles above is public information shown for illustration purposes. 5

thLive Mint, 24 October, 2017 Times of India, 19th October 2017

thLive Mint, 10 May 2017

Housing in the News

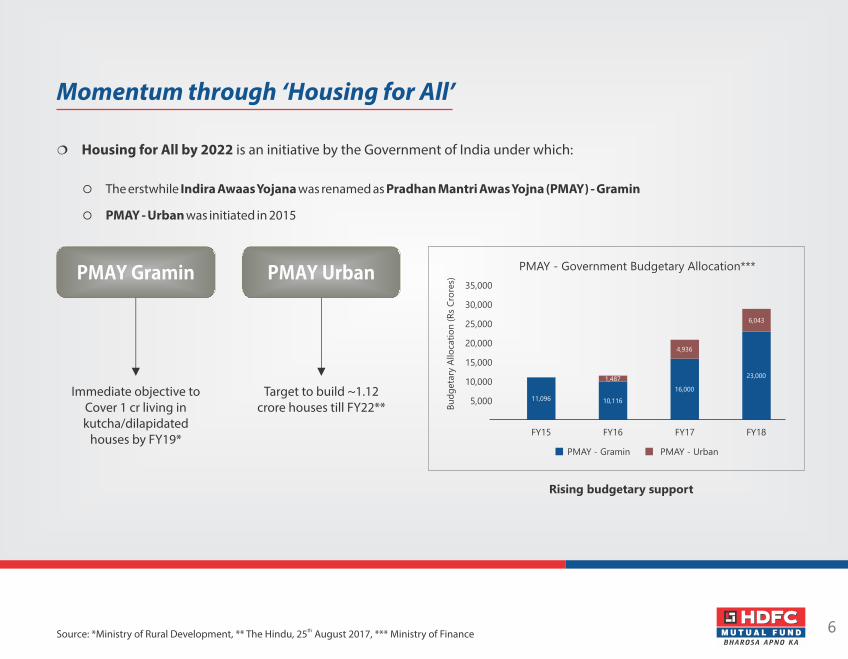

thSource: *Ministry of Rural Development, ** The Hindu, 25 August 2017, *** Ministry of Finance 6

Momentum through ‘Housing for All’

¦ Housing for All by 2022 is an initiative by the Government of India under which:

¡ The erstwhile Indira Awaas Yojana was renamed as Pradhan Mantri Awas Yojna (PMAY) - Gramin

¡ PMAY - Urban was initiated in 2015

PMAY�Gramin PMAY�Urban

Immediate objective to Cover 1 cr living in kutcha/dilapidated

houses by FY19*

Target to build ~1.12 crore houses till FY22**

Rising budgetary support

FY15 FY16 FY17 FY18

PMAY - Gramin PMAY - Urban

PMAY - Government Budgetary Allocation***

35,000

30,000

25,000

20,000

15,000

10,000

5,000

Bu

dg

eta

ry A

lloca

tio

n (

Rs

Cro

res)

11,096 10,116

16,000

23,000

6,043

4,936

1,487

Source: *PMAY Gramin and PIB Government of India, **incometaxindia.gov.in ^ Ministry of Housing and Urban Affairs, ^^ EPFO noti�cation dated 19th May, 2017. 7

‘Housing for All by 2022' - Building the future

¡ Strong political will under Government’s ‘Housing for All’¡ Target to build 5 cr homes* over �ve years under Pradhan Mantri Awaas Yojana -

Urban and GraminPolitical Will

¡ Direct funding from Central and State Governments¡ Ensuring active participation by private sector through various incentives

Action Plan

¡ Interest subsidy provided to low and mid income group^¡ Affordable housing is the only segment in housing sector to get 100% tax exemption

for developers**¡ 90% of govt run pension fund EPFO can be withdrawn for home purchase^^

Incentives

8

Housing Opportunity - Shaping Next Leg of Growth

Source: CLSALIG-Lower Income Group, MIG-Middle Income Group.

Total houses to be

constructed FY 18-24 (lakh)

Total amount to be spent

(Rs. lakh crore)

PMAY (Gramin & Urban) 315 13.5

Rs. 5-10 lakh - Rural 123 9.8

Rs 10-20 lakh - Rural / LIG 95 14.5

Rs 20-50 lakh - MIG 53 21.7

Rs 50 lakh+ 21 23.5

Total 605 83.1

¡ Over 6 cr houses are expected to be built in the next 7 years¡ Over Rs 80 lakh crore is expected to be spent on constructing new houses in the next 7 years

46% expected to be spent on low-cost housing

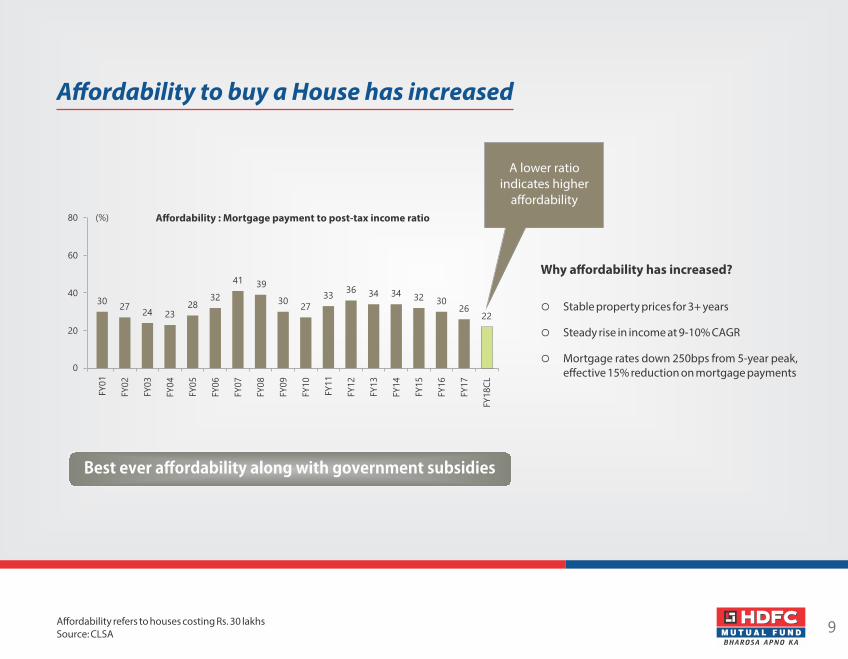

Affordability to buy a House has increased

9Affordability refers to houses costing Rs. 30 lakhsSource: CLSA

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18C

L

80

60

40

20

0

Best�ever�affordability�along�with�government�subsidies

(%)

3027

24 2328

32

41 39

3027

3336 34 34 32 30

2622

¡ Stable property prices for 3+ years

¡ Steady rise in income at 9-10% CAGR

¡ Mortgage rates down 250bps from 5-year peak, effective 15% reduction on mortgage payments

Why affordability has increased?

Affordability : Mortgage payment to post-tax income ratio

A lower ratio indicates higher

affordability

10

What Has Changed?

¡ Affordable housing segment is at the beginning of a high growth phase¡ Government push is evident

Earlier Now

High Interest Rates Lower Interest Rates

Not a major focus area Housing - On top of Government’s agenda

No infrastructure statusInfrastructure status for affordable housing,

thereby enabling easier institutional credit

Not a regulated industry RERA in place

Relatively slower approval / clearances Faster clearances

Fewer tax incentives for developers 100% tax exemption on affordable housing

Fewer incentives for buyers Enhanced interest subsidies, tax benefits, etc.

Lower affordability for buying a house Best ever affordability

Policy change

11

Housing Opportunity - Wide Economic Linkages

Source: Ministry of Housing and Urban Poverty Alleviation, * National Council of Applied Economic Research, ̂ Indian Brand Equity Foundation (IBEF)

th¦ Housing sector – 4 largest employment provider in India*

¦ Housing sector to aid government’s push for economic growth

¦ Housing sector accounts for ~ 5 % of GDP^

¦ Revival of capex cycle

¦ Opportunity to propel rural and urban economic activity

¦ Construction and allied sectors to be major bene�ciaries

¦ Overall upliftment of standard of living

¦ Hence, Government expected to show full commitment

Housing Demand to Boost Various Industries

Names of entities/industries mentioned are currently part of the benchmark and provided for illustration purposes only, to depict the diversi�ed nature of the opportunity and does neither, in any manner, re�ect the nature of the actual portfolio, nor are stock recommendations made by HDFC AMC. Stocks/Sectors referred above are illustrative and not recommendations made by HDFC Mutual Fund /AMC .The above segregation of sectors is based on the broad thematic assessment of the businesses covered under the housing theme and its allied businesses. The fund may or may not have any present or future positions in these industries. HDFC Mutual Fund/AMC is not guaranteeing any returns on investments made in the scheme . 12

Presenting�a�great�investment�opportunity

Wooden Panels

Greenply, Century

Light Electricals

Havells, Crompton Greaves

Paints

Asian Paints, Nerolac, Berger

Adhesives and Chemicals

Akzo Nobel

Steel

Tata Steel, SAILTiles

Kajaria

Cement

UltraTech, Ambuja

Sanitaryware

Cera, HSIL

Construction

DLF, NBCC

Engineering

L&T, Engineers India, Sadhbhav

Home Appliances

Voltas, Whirlpool, Symphony

Home Loans

HDFC Ltd, HDFC Bank, ICICI Bank, SBI

Housing Opportunity - Deep Sectoral/Macro Links

Source: CLSA-Housing Linked demand for FY17 converted from USD to INR @ 1 USD = Rs 65. 13

Construction�of��6�crore�units�over�FY�18-24Total�spend�on�housing�over�7�years:�Over�Rs�80�lakh�crore

Multiple�Sector�Linkages

Industry Cement Steel Paints WoodPanel

Tiles PlasticPipes

LightElectricals

Adhesives &Construction

Chemicals

Rs. 91,000 cr Rs. 78,000 cr Rs. 29,250 cr Rs. 24,050 cr Rs. 22,750 cr Rs. 13,650 cr Rs. 13,650 cr Rs. 7,150 cr

3% NIL 30% 60% 50% 40% 30% 25%

Demandlinked to

housing (FY17)

Share ofUnorganized

players

Implementation of GST to aid transformation of businesses from unorganized to organized sector.

Overview of HDFC Housing Opportunities Fund - Series 1

14

HDFC HOF - I - 1140D November 2017 (1)(Close Ended Thematic Equity Scheme)

Investment Strategy

15

Positioned�as�thematic�equity�offering,

the�focus�will�be�on

For complete details on investment strategy (Including illustrations on derivative strategies refer SID/KIM available on the website www.hdfcfund.com or with Distributor) *Indicative Allocation at the time of initial portfolio construction, post closure of NFO. HDFC Mutual Fund/AMC is not guaranteeing returns on investments made in this scheme. The portfolio allocation is subject to change depending on the market conditions in line with theme of the scheme ,** For risks associated with derivatives strategy, refer slide titled “Fund suitability and risk factors”.

Equities�of�housing�and�allied�businesses�

(~80-85%)*

Debt�and�Money�Market�Instruments�

(~15-20%)*

Downside�protection�using�derivatives**Depending�on�market�conditions,�the�Fund�may�purchase�Put�

Options�to�de-risk�the�portfolio/lock�gains�closer�to�the�maturity

Underlying�of�Put�Options:�NIFTY50/individual�stocks

For�managing�volatility�vis-a-vis�equities

For�portfolio�risk�mitigation

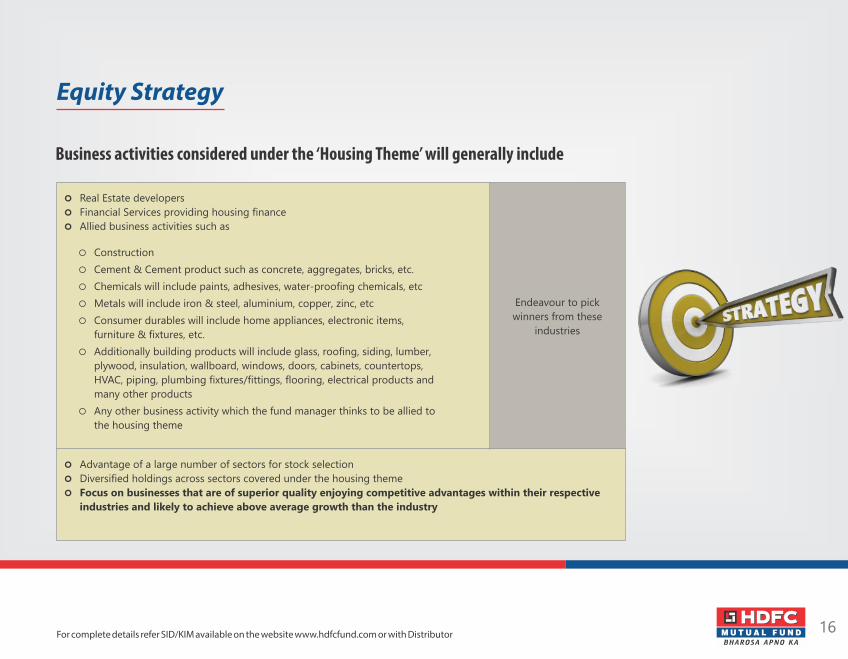

Equity Strategy

16

¢ Real Estate developers

¢ Financial Services providing housing finance

¢ Allied business activities such as

Endeavour to pick

winners from these

industries

¢ Advantage of a large number of sectors for stock selection

¢ Diversified holdings across sectors covered under the housing theme

¢ Focus on businesses that are of superior quality enjoying competitive advantages within their respective

industries and likely to achieve above average growth than the industry

Business activities considered under the ‘Housing Theme’ will generally include

¡ Construction

¡ Cement & Cement product such as concrete, aggregates, bricks, etc.

¡ Chemicals will include paints, adhesives, water-proofing chemicals, etc

¡ Metals will include iron & steel, aluminium, copper, zinc, etc

¡ Consumer durables will include home appliances, electronic items,

furniture & fixtures, etc.

¡ Additionally building products will include glass, roofing, siding, lumber,

plywood, insulation, wallboard, windows, doors, cabinets, countertops,

HVAC, piping, plumbing fixtures/fittings, flooring, electrical products and

many other products

¡ Any other business activity which the fund manager thinks to be allied to

the housing theme

For complete details refer SID/KIM available on the website www.hdfcfund.com or with Distributor

Summary

17

¦ Acute housing shortage in India

¦ Changing landscape provides a conducive environment for the growth of housing sector

¦ Government’s focus on affordable housing could lead to maximum activity in this segment

¦ Affordability has increased over the last decade

¦ Multiple macro-economic linkages to foster growth in allied industries, thereby boosting economic growth

¦ HDFC Housing Opportunities Fund to focus on businesses that would bene�t from the expected growth in housing

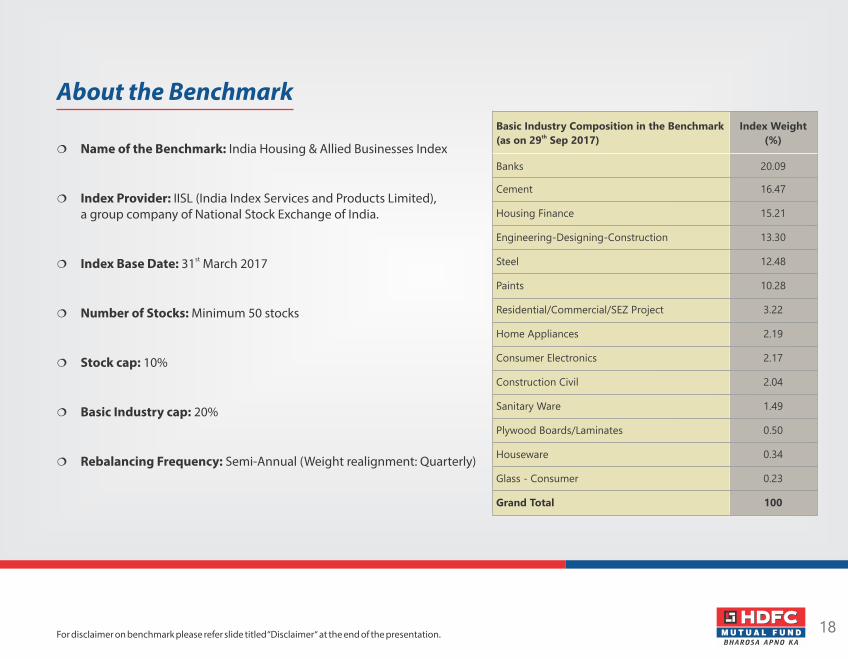

About the Benchmark

18

¦ Name of the Benchmark: India Housing & Allied Businesses Index

¦ Index Provider: IISL (India Index Services and Products Limited),a group company of National Stock Exchange of India.

st¦ Index Base Date: 31 March 2017

¦ Number of Stocks: Minimum 50 stocks

¦ Stock cap: 10%

¦ Basic Industry cap: 20%

¦ Rebalancing Frequency: Semi-Annual (Weight realignment: Quarterly)

Basic Industry Composition in the Benchmark th(as on 29 Sep 2017)

Index Weight

(%)

Banks 20.09

Cement 16.47

Housing Finance 15.21

Engineering-Designing-Construction 13.30

Steel 12.48

Paints 10.28

Residential/Commercial/SEZ Project 3.22

Home Appliances 2.19

Consumer Electronics 2.17

Construction Civil 2.04

Sanitary Ware 1.49

Plywood Boards/Laminates 0.50

Houseware 0.34

Glass - Consumer 0.23

Grand Total 100

For disclaimer on benchmark please refer slide titled “Disclaimer“ at the end of the presentation.

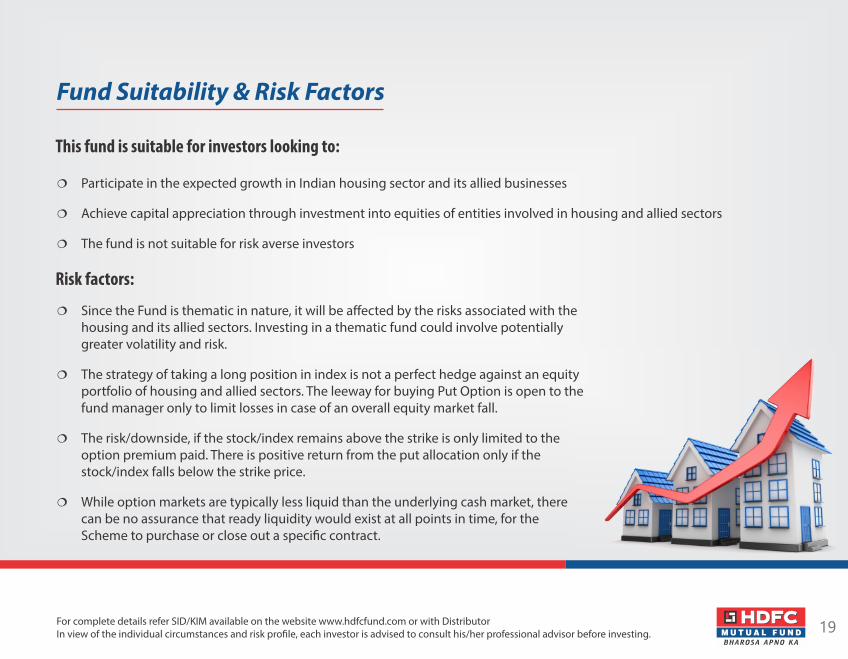

Fund Suitability & Risk Factors

19

¦ Participate in the expected growth in Indian housing sector and its allied businesses

¦ Achieve capital appreciation through investment into equities of entities involved in housing and allied sectors

¦ The fund is not suitable for risk averse investors

This fund is suitable for investors looking to:

¦ Since the Fund is thematic in nature, it will be affected by the risks associated with the housing and its allied sectors. Investing in a thematic fund could involve potentially greater volatility and risk.

¦ The strategy of taking a long position in index is not a perfect hedge against an equity portfolio of housing and allied sectors. The leeway for buying Put Option is open to the fund manager only to limit losses in case of an overall equity market fall.

¦ The risk/downside, if the stock/index remains above the strike is only limited to the option premium paid. There is positive return from the put allocation only if the stock/index falls below the strike price.

¦ While option markets are typically less liquid than the underlying cash market, there can be no assurance that ready liquidity would exist at all points in time, for the Scheme to purchase or close out a speci�c contract.

Risk factors:

For complete details refer SID/KIM available on the website www.hdfcfund.com or with DistributorIn view of the individual circumstances and risk pro�le, each investor is advised to consult his/her professional advisor before investing.

20For complete details refer SID/KIM available on the website www.hdfcfund.com or with Distributor$ Overseas Fund Manager for the scheme-Mr Rakesh Vyas

Fund Facts

Scheme Name HDFC Housing Opportunities Fund - Series 1

Scheme Type Closed Ended Thematic Equity Scheme

Investment Manager HDFC Asset Management Company Limited

Product Labelling High Risk (Refer Page 22 of the presentation)

Tenure 1140 days

NFO Periodth th16 November 2017 to 30 November 2017

$Fund Manager Mr. Srinivas Rao Ravuri

Investment Objective

To provide long-term capital appreciation by investing predominantly in equity and equity related instruments of entities engaged in

and/or expected to benefit from the growth in housing and its allied business activities.

There is no assurance that the investment objective of the Scheme will be realized.

Exit LoadNot applicable. The Units under the Plan cannot be directly redeemed with the Fund as the Units will be listed on the stock

exchange(s).

Benchmark India Housing and Allied Businesses Index

Minimum Application

Amount/Number of UnitsPurchase: Rs. 5,000 and in multiple of Rs. 10 thereafter.

21

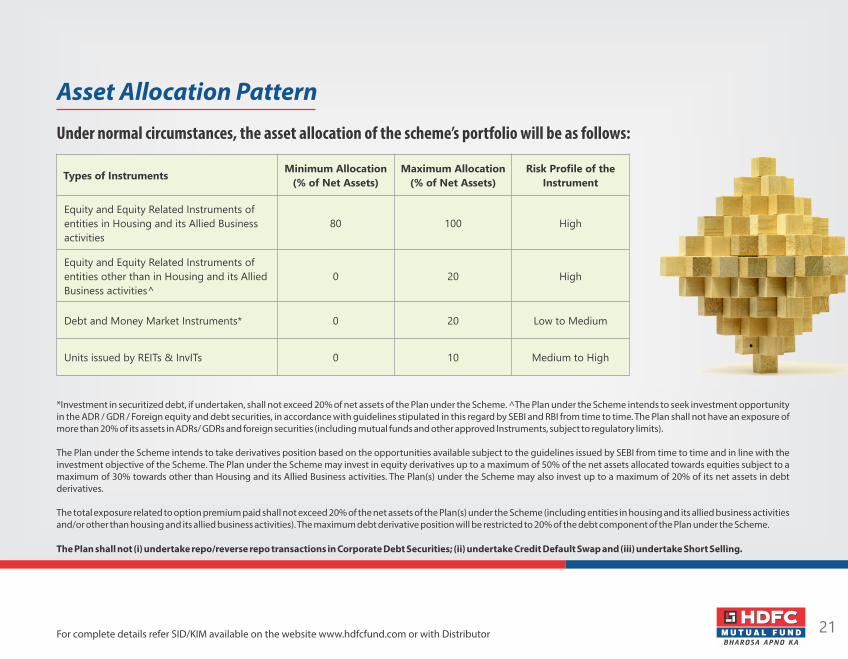

Asset Allocation Pattern

*Investment in securitized debt, if undertaken, shall not exceed 20% of net assets of the Plan under the Scheme. ̂ The Plan under the Scheme intends to seek investment opportunity in the ADR / GDR / Foreign equity and debt securities, in accordance with guidelines stipulated in this regard by SEBI and RBI from time to time. The Plan shall not have an exposure of more than 20% of its assets in ADRs/ GDRs and foreign securities (including mutual funds and other approved Instruments, subject to regulatory limits).

The Plan under the Scheme intends to take derivatives position based on the opportunities available subject to the guidelines issued by SEBI from time to time and in line with the investment objective of the Scheme. The Plan under the Scheme may invest in equity derivatives up to a maximum of 50% of the net assets allocated towards equities subject to a maximum of 30% towards other than Housing and its Allied Business activities. The Plan(s) under the Scheme may also invest up to a maximum of 20% of its net assets in debt derivatives.

The total exposure related to option premium paid shall not exceed 20% of the net assets of the Plan(s) under the Scheme (including entities in housing and its allied business activities and/or other than housing and its allied business activities). The maximum debt derivative position will be restricted to 20% of the debt component of the Plan under the Scheme.

The Plan shall not (i) undertake repo/reverse repo transactions in Corporate Debt Securities; (ii) undertake Credit Default Swap and (iii) undertake Short Selling.

Under normal circumstances, the asset allocation of the scheme’s portfolio will be as follows:

Types of InstrumentsMinimum Allocation

(% of Net Assets)

Maximum Allocation

(% of Net Assets)

Risk Profile of the

Instrument

Equity and Equity Related Instruments of

entities in Housing and its Allied Business

activities

80 100 High

Equity and Equity Related Instruments of

entities other than in Housing and its Allied

Business activities^

0 20 High

Debt and Money Market Instruments* 0 20 Low to Medium

Units issued by REITs & InvITs 0 10 Medium to High

For complete details refer SID/KIM available on the website www.hdfcfund.com or with Distributor

* Investors should consult their financial advisers if in doubt about whether the product is suitable for them.

This product is suitable for investors who are seeking*

Ÿ Capital appreciation over 1140 days (tenure of the Plan)

Ÿ Investment predominantly in equity and equity related instruments of entities engaged

in and/or expected to benefit from the growth in housing and its allied business activities

Product Labelling

22

Riskometer

23

Disclaimerth

The presentation is dated 27 October 2017 and has been prepared by HDFC Asset Management Company Limited (HDFC AMC) based on internal data, publicly

available information and other sources believed to be reliable. Any calculations made are approximations, meant as guidelines only, which you must confirm before

relying on them. The information contained in this document is for general purposes only. The document is given in summary form and does not purport to be

complete. The document does not have regard to specific investment objectives, financial situation and the particular needs of any specific person who may receive

this document. The information/ data herein alone are not sufficient and should not be used for the development or implementation of an investment strategy. The same should

not be construed as investment advice to any party. The statements contained herein are based on our current views and involve known and unknown risks and uncertainties that

could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Neither HDFC Asset Management Company (HDFC

AMC) and HDFC Mutual Fund (the Fund) nor any person connected with them, accepts any liability arising from the use of this document.

HDFC Mutual Fund/AMC is not guaranteeing returns on investments made in this scheme. The recipient(s) before acting on any information herein should make

his/her/their own investigation and seek appropriate professional advice and shall alone be fully responsible / liable for any decision taken on the basis of information contained

herein. Past performance may not be sustained in the future.

The HDFC Housing Opportunities Fund-Series 1 is not sponsored, endorsed, sold or promoted by India Index Services & Products Limited ("IISL"). IISL does not make any

representation or warranty, express or implied, to the owners of the HDFC Housing Opportunities Fund-Series 1 or any member of the public regarding the advisability of

investing in securities generally or in the HDFC Housing Opportunities Fund-Series 1 particularly or the ability of HDFC Asset Management Company Ltd. to track general stock

market performance in India. The relationship of IISL to the Issuer is only in respect of the licensing of the Indices and certain trademarks and trade names associated with such

Indices which is determined, composed and calculated by IISL without regard to the Issuer or the HDFC Housing Opportunities Fund-Series 1. IISL does not have any obligation to

take the needs of the Issuer or the owners of the HDFC Housing Opportunities Fund-Series 1 into consideration in determining, composing or calculating the India Housing and

Allied Businesses Index. IISL is not responsible for or has participated in the determination of the timing of, prices at, or quantities of the HDFC Housing Opportunities Fund-Series

1 to be issued or in the determination or calculation of the equation by which the HDFC Housing Opportunities Fund-Series 1 is to be converted into cash. IISL has no obligation or

liability in connection with the administration, marketing or trading of the HDFC Housing Opportunities Fund-Series 1.

IISL do not guarantee the accuracy and/or the completeness of this document or any data included therein and IISL shall have not have any responsibility or liability for any errors,

omissions, or interruptions therein. IISL does not make any warranty, express or implied, as to results to be obtained by the Issuer, owners of the HDFC Housing Opportunities

Fund-Series 1, or any other person or entity from the use of the presentation or any data included therein. IISL makes no express or implied warranties, and expressly disclaim all

warranties of merchantability or fitness for a particular purpose or use with respect to the index or any data included therein. Without limiting any of the foregoing, IISL expressly

disclaim any and all liability for any claims ,damages or losses arising out of or related to the Products, including any and all direct, special, punitive, indirect, or consequential

damages (including lost profits), even if notified of the possibility of such damages.

An investor, by subscribing or purchasing an interest in the HDFC Housing Opportunities Fund-Series 1, will be regarded as having acknowledged, understood and accepted the

disclaimer referred to in Clauses above and will be bound by it.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Disclaimer of India Housing & Allied Businesses Index