one global car company in the making - fca group global car company in the making . ... chrysler...

TRANSCRIPT

20 Novembre, 2010

One global car company in the making

Sergio Marchionne

Sanford C. Bernstein - Strategic Decisions Conference

London - September 20, 2011

September 20, 2011 Sanford C. Bernstein – Strategic Decisions Conference 2

Safe Harbor Statement

Cer ta i n i n fo rmat i on i n c l uded i n t h i s

p resen ta t i on , i n c l ud i ng , w i t hou t l im i ta t i on ,

any f o recas t s i n c l uded here i n , i s f o rwa rd

l ook i ng and i s sub j ec t t o impor tan t r i sks and

uncer t a i n t i es t ha t cou l d cause ac tua l resu l t s

t o d i f f e r ma te r i a l l y . The Group ‟ s bus i nesses

i nc l ude i t s au tomot i ve , au tomot i ve- re l a t ed and

o ther sec t o rs , and i t s ou t l ook i s p redominan t l y

based on i t s i n t e rp re ta t i on o f what i t

cons i de rs t o be the key economi c f a c t o r s

a f f ec t i ng these bus i nesses . Fo rward - l ook i ng

s t a t emen t s w i th rega rd t o t he Group ' s

bus i nesses i nvo l ve a number o f impor tan t

fa c t o r s t ha t a re sub j ec t t o change , i n c l ud i ng ,

bu t no t l im i t ed t o: t he many i n t e r re l a t ed

fa c to r s t ha t a f f ec t consumer con f i dence and

wor l dw ide demand fo r au tomot i ve and

au tomot i ve - re l a t ed p roduc t s ; governmen ta l

p rog rams; genera l economi c cond i t i ons i n each

o f t he Group ' s marke t s ; l eg i s l a t i on ,

pa r t i cu l a r l y t ha t re l a t i ng t o au tomot i ve-

re l a t ed i s sues , t he env i ronmen t , t rade and

commerce and i n f ra s t ru c tu re deve l opmen t ;

a c t i ons o f compet i t o r s i n t he va r i ous

i ndus t r i es i n wh i ch the Group competes ;

produc t i on d i f f i cu l t i e s , i n c l ud i ng capac i ty and

supp l y cons t ra i n t s and excess i nven to ry

l eve l s ; l abo r re l a t i ons ; i n t e res t ra t es and

cu r rency exchange ra t es ; po l i t i ca l and c i v i l

un res t ; ea r thquakes and o ther r i sks and

uncer t a i n t i es . Any o f the assumpt i ons

under l y i ng t h i s p resen ta t i on o r any o f the

c i r cumstances o r da ta men t i oned i n t h i s

p resen ta t i on may change . Any f o rward - l ook i ng

s t a t emen t s con ta i ned i n t h i s p resen ta t i on

speak on l y a s o f t he da te o f t h i s p resen ta t i on .

F i a t does assume and exp ress l y d i s c l a ims any

ob l i ga t i on t o upda te t hese f o rward - l ook i ng

s t a t emen t s . F i a t does no t a ssume and

express l y d i s c l a ims any l i ab i l i t y i n connec t i on

w i th any i naccu rac i es i n any o f t hese f o rward -

l ook i ng s ta t emen t s o r i n connec t i on w i t h any

u se by any th i rd par t y o f su ch f o rward - l ook i ng

s ta temen t s . Th i s p resen ta t i on does no t

rep resen t i nves tmen t adv i ce o r a

recommenda t i on f o r t he pu rchase o r sa l e o f

f i nanc i a l p roduc t s and/o r o f any k i nd o f

f i nanc i a l se rv i ces . F i na l l y , t h i s p resen ta t i on

does no t rep resen t an i nves tmen t so l i c i t a t i on

i n I t a l y , pu rsuan t t o Sec t i on 1 , l e t t e r ( t ) o f

Leg i s l a t i ve Dec ree no . 58 o f Februa ry 24 ,

1998 , a s amended, nor does i t r ep resen t a

s im i l a r so l i c i t a t i on a s con temp la ted by the

l aws i n any other count ry or s ta te .

September 20, 2011 Sanford C. Bernstein – Strategic Decisions Conference 3

The creation of a global automaker Milestones in the integration of Fiat & Chrysler

2009 June: 20% initial ownership interest in Chrysler Group LLC

2011 January: achievement of 1st Performance Event by Chrysler Group LLC

April: achievement of 2nd Performance Event by Chrysler Group LLC

May: exercise of Incremental Equity Call Option by Fiat

July: purchase of ownership interest in Chrysler Group LLC from UST and Canada by Fiat plus UST rights under Equity Recapture Agreement

By year-end: expected achievement of 3rd

Performance Event, moving Fiat‟s interest in Chrysler Group LLC up to 58.5% from current 53.5%

From July 1st, 2012 until June 30th, 2016: Fiat has the option to purchase 40% of VEBA‟s original interest in Chrysler. Option is exercisable not in excess of 20% of Covered Interest in any 6 month period. Before an IPO, exercise price is based on a market multiple not to exceed Fiat‟s multiple applied to Chrysler reported LTM EBITDA less net industrial debt and following an IPO based on trading price of common stock

In addition to above option, under Equity Recapture Agreement: i) Fiat may purchase any remaining membership interest held by VEBA at a specified threshold ($4.25bn plus 9% p.a. compounded annually from Jan 1, 2010), and ii) Fiat receives all proceeds from Chrysler ownership interest held by VEBA over the above threshold (and once such threshold is reached, any remaining shares are turned over to holder)

VEBA 41.5% FIAT

58.5%

Chrysler pro-forma shareholder structure

(on a fully diluted basis)

September 20, 2011 Sanford C. Bernstein – Strategic Decisions Conference 4

Better geographic diversification

North America

3%

Europe 60%

RoW 9%

Mercosur 28%

North America

47% Europe 32%

Mercosur 17%

RoW 4%

* 12-month contribution by Chrysler

September 20, 2011 Sanford C. Bernstein – Strategic Decisions Conference 5

EMEA Gianni Coda

Asia Michael Manley

Mopar Pietro Gorlier

Systems & Castings

Riccardo Tarantini

Components Eugenio Razelli

LATAM Cledorvino Belini

CHIEF OPERATING

OFFICERS

BRAND LEADERS

INDUSTRIAL PROCESS LEADERS

CEO

Sergio

Marchionne

NAFTA Sergio Marchionne

SUPPORT PROCESS LEADERS

Fiat Professional

Lorenzo Sistino

Lancia

Chrysler Saad Chehab

Chief

Marketing Officer

Olivier François

Dodge Reid Bigland

Alfa

Romeo

Abarth

Maserati Harald Wester

Fiat Olivier François

Design Lorenzo Ramaciotti

Group Purchasing

Vilmar Fistarol

Quality Doug Betts

Product Portfolio

Mark Chernoby

Powertrain Coordinator

Bob Lee

Chief

Manufacturing

Officer Stefan Ketter

Chief Technical

Officer Harald Wester

Business Development

Alfredo Altavilla

Chief Human

Resources Officer

Linda Knoll

Chief

Financial Officer

Richard Palmer

Fiat Services

& Holdings

Alessandro Baldi

Jeep Michael Manley

The leadership team

September 20, 2011 Sanford C. Bernstein – Strategic Decisions Conference 6

Overhaul of stand-alone companies in 2009

• Inadequate European business model

• Portfolio heavily skewed to A & B segments

• Heavy reliance for profitability on LCVs

• Under utilization of manufacturing infrastructure preventing full exploitation of operational efficiency

• Suboptimal volumes for Alfa Romeo & Lancia to support stand alone brand

• Low presence in major developing markets (China, Russia, India)

• Unique mass market brands with Fiat having the most solid position, Alfa Romeo with internationally recognized strong heritage

• A leading position for LCVs

• Leadership in CO2 emissions

• Strong positioning in Latin America

• Best-in-class time-to-market from design freeze

• Ferrari & Maserati unique iconic and profitable assets

Negative Positive Weaknesses Strengths

• Customer trust and confidence

• Heavy reliance on NAFTA markets

• Less than optimal product line-up

• Incomplete offering in C- & D-segment

• Gap in perceived quality and reliability vs. competition

• Brands with strong heritage in North America, Jeep globally recognized

• US distribution network re-sized

• Experienced and talented workforce, albeit demoralized

• Competitive labor rates and significantly restructured OPEB liabilities

• Sufficient liquidity to launch a credible business plan with speed being of the essence

Negative Positive Weaknesses Strengths

September 20, 2011 Sanford C. Bernstein – Strategic Decisions Conference 7

Inextricably intertwined entity leveraging on partners‟ core strengths

Sharing of best practices in the

areas of WCM, engineering and

design, quality and

management with significant

cost synergies, particularly in

purchasing and engineering

Optimized allocation of

production capacity at both

organizations

Full integration of Fiat &

Chrysler product portfolios

Strong joint geographic

coverage, Asia excepted

Critical mass target of ~6mn

units by 2014

September 20, 2011 Sanford C. Bernstein – Strategic Decisions Conference 8

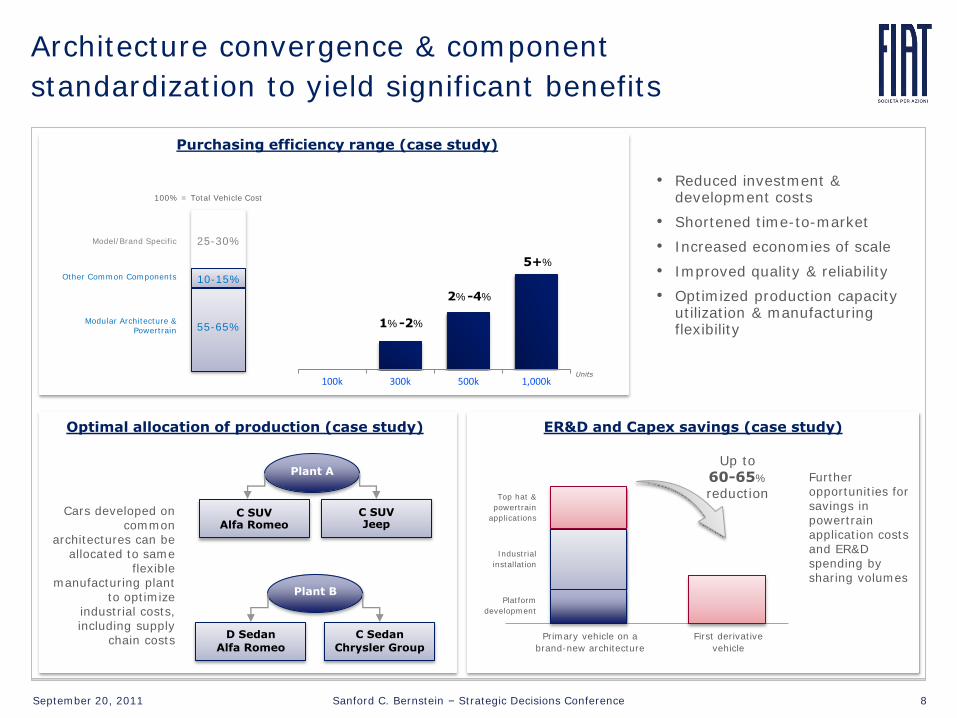

Architecture convergence & component

standardization to yield significant benefits

100k 300k 500k 1,000k

1%-2%

2%-4%

5+%

Purchasing efficiency range (case study)

25-30%

10-15%

Model/Brand Specific

Modular Architecture & Powertrain

Other Common Components

100% = Total Vehicle Cost

• Reduced investment & development costs

• Shortened time-to-market

• Increased economies of scale

• Improved quality & reliability

• Optimized production capacity utilization & manufacturing flexibility

C SUV Alfa Romeo

C SUV Jeep

Plant A

D Sedan

Alfa Romeo

C Sedan

Chrysler Group

Plant B

Cars developed on common

architectures can be allocated to same

flexible manufacturing plant

to optimize industrial costs, including supply

chain costs

Units

ER&D and Capex savings (case study)

Top hat &

powertrain

applications

Industrial

installation

Platform

development

Up to

60-65%

reduction

55-65%

Further opportunities for savings in powertrain application costs and ER&D spending by sharing volumes

First derivative

vehicle

Primary vehicle on a

brand-new architecture

Optimal allocation of production (case study)

September 20, 2011 Sanford C. Bernstein – Strategic Decisions Conference 9

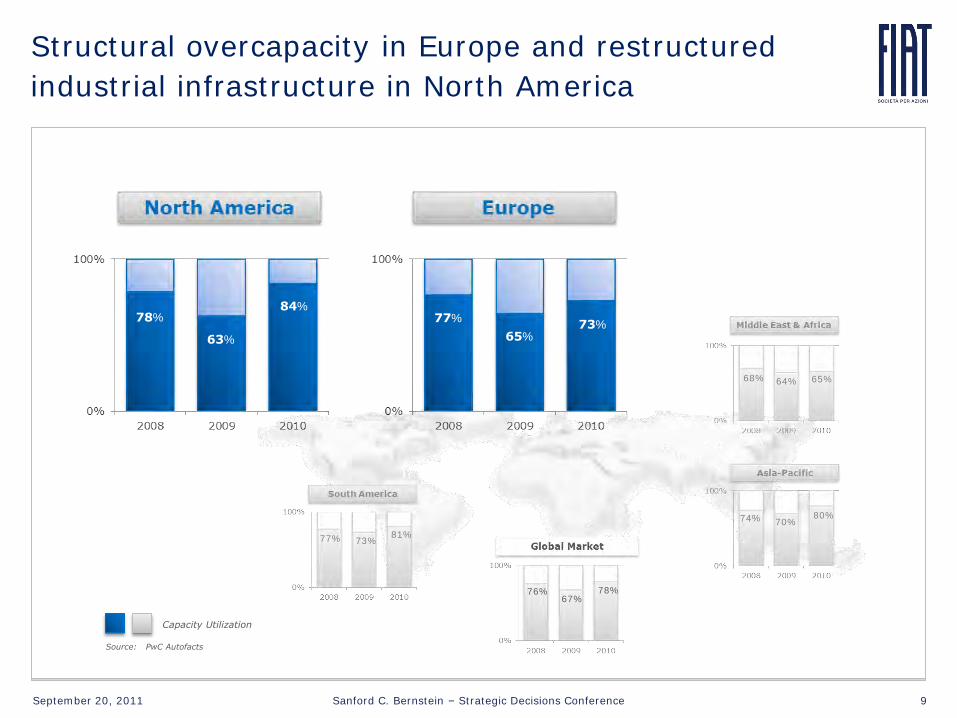

Structural overcapacity in Europe and restructured

industrial infrastructure in North America

Source: PwC Autofacts

Capacity Utilization

78%

63%

84% 77%

65% 73%

68% 64% 65%

74% 70% 80%

77% 73% 81%

76% 67%

78%

September 20, 2011 Sanford C. Bernstein – Strategic Decisions Conference 2011 10

0

20

40

60

80

100

120

140

160

0

50

100

150

200

250

300

350

400

450

500

0

5

10

15

20

25

30

35

40

45

50

0

50

100

150

200

250

300

350

400

78%

37%

126%

54%

H1 2010

73%

33%

118%

49%

H1 2011

Rest of Europe2

Italy1

1 Italy: Cassino, Melfi, Mirafiori, Pomigliano d’Arco & Termini Imerese (ceasing production by 2001 year-end) 2 Tycky (Pol), Kragujevac (Ser), Bursa (Tur, including vehicles supplied to Opel in force of Nov 2010 agreement)

Capacity utilization at FGA (Passenger car plants)

Rest of Europe2

Italy1

Harbour definition

(235 days per annum/

16 hours per day)

Technical definition

(280 days per annum/

3 shifts per day)

Cassino

Termini Imerese (end of car production in 2011)

Melfi

90%

2010 2014E

0

50

100

150

200

250

300

350

0

50

100

150

200

250

300

350

400

450

500

Pomigliano d’Arco

Mirafiori

2010 2014E

2010 2014E

2010 2014E

2010 2014E 2010 2014E

HARBOUR DEFINITION

Officine Automobilistiche Grugliasco

TECHNICAL HARBOUR DEFINITION

TECHNICAL

HARBOUR DEFINITION

TECHNICAL

HARBOUR DEFINITION

TECHNICAL HARBOUR DEFINITION

TECHNICAL

HARBOUR DEFINITION

TECHNICAL HARBOUR DEFINITION

TECHNICAL HARBOUR DEFINITION

TECHNICAL

HARBOUR DEFINITION

TECHNICAL HARBOUR DEFINITION

TECHNICAL

Reconstructing a sustainable industrial system with

ultimate goal of European ops at break-even by 2014

Capacity

(k units)

Production

(k units)

September 20, 2011 Sanford C. Bernstein – Strategic Decisions Conference 2011 11

An intense product rejuvenation underway in Europe

Major modification

• Re-launch of Alfa Romeo brand, including strong European push

• Return to North American market through Chrysler network

• Major focus on core A,B,C segments

• Full integration of Chrysler with Lancia

• Comprehensive product line leveraging on Chrysler nameplates

2011 2012 2013 2014

• Maintaining strong position in EU & Latin America

• Leveraging on Chrysler opportunities

• Consolidating strong industrial and R&D partnerships

• Strengthening body-builder business

• Revitalizing an American icon

2010

New model

• Continue building on sporty image

September 20, 2011 Sanford C. Bernstein – Strategic Decisions Conference 2011 12

2011 2012 2013 2014

70th Anniversary

Commemorative

product actions

across all

nameplates

• Elegant sedans & premium minivans

• Enhanced offering with high-performance SRT versions

• Revitalizing an American icon on a global basis

• Enhanced offering with high-performance SRT versions

• Focus on pick-up trucks

• Full-line passenger cars, CUVs & minivans

• Enhanced offering with high-performance SRT versions

• Small cars

2010

Major modification

New model

Commitment to enhance product portfolio at Chrysler

September 20, 2011 Sanford C. Bernstein – Strategic Decisions Conference 2011 13

• First FGA vehicle to come out of partnership with Chrysler

Initially available in FWD, powered by 2.0 140 & 170hp MultiJet II produced and developed by Fiat Powertrain

Rounding out powertrain offerings in H2

Chrysler V6 Pentastar gas engine in Q3

Diesel version equipped with automatic transmission and AWD capabilities available in latter part of the year

• Successful launch in June across Europe, with very good initial reception by market

Bringing new customers to the brand (60% new to Fiat)

• FY 2011 target of 20+k units

• Fiat‟s historical leadership in European A-segment…

More than 6 million Pandas manufactured since early 80‟s

More than 2.6 million Panda units in operation in Europe at the end of 2010

• …to continue in a steadily recovering segment post eco-incentive boom with the introduction of New Panda

The “Magic Box” since the ‟80s

A unique city-car offering simple yet ingenious solutions to everyday mobility needs

State-of-the-art safety, versatility, comfort and efficiency

Cars hitting showrooms in December in Italy; sales to start in January in Italy, then across Europe in February and later on in more than 40 countries outside Europe

0.8

1.2

1.7

1.2

1.6

2000 2008 2009 2011E 2014E

A-segment in EU27+EFTA

(million units)

Fiat: 2011 key product launches Renovating portfolio

September 20, 2011 Sanford C. Bernstein – Strategic Decisions Conference 2011 14

• Successfully launched in mid June across key European markets with 20k orders taken to date

• FY target of ~120k units, 45-50k shipments expected in 2011

• Sales potential doubled vs. predecessor models thanks to first-time 5-door concept, leveraging also on strong customer base (1.5+mn car park)

• Competitive fuel-efficient powertrain offering

A true icon in MPV category with 13mn units sold in its history

• Based on significantly refreshed Chrysler Town & Country

• The most advanced safety systems in market today and the most advanced entertainment system in its class

• To be launched in Q4 in Europe

First global flagship, a RWD equipped with segment leading standards

• Derived from all-new Chrysler 300

• On sale from October in all European dealerships

• Elegance and dynamism in perfect tune with Italian style

• Based on significantly refreshed Chrysler 200

• On sale in 2012

Lancia/Chrysler: key product launches Transformation into a full-liner underway

September 20, 2011 Sanford C. Bernstein – Strategic Decisions Conference 2011 15

Alfa Romeo Giulietta: Entered best-in-class club in C-Segment in 2011

• Best-in-class features in C-segment…

Handling & dynamic performance

Comfort

Safety

Quality

CO2 emissions in C-segment

121g/Km of CO2 for 1.4 MultiAir 170hp gas engine coupled with “Alfa TCT”

• …making Alfa Romeo Giulietta among best-in-class players in all main EU countries

• ~61k orders (100+k since launch in May 2010) to date

• ~58k shipments, fully in line with FY target of 90-100k units

~90% shipments with high trim level

• Share of 3% in EU27+EFTA in C-segment, the highest level ever for Alfa Romeo

• Fuel-efficient MultiAir technology

• Competitive diesel MultiJet II

• Dual Dry Clutch Transmission “Alfa TCT”, available in market starting H2

• Powertrains available across model range with best torque/power ratio compared to emissions

Alfa Romeo

Giulietta

Competitor

A

Competitor

B

Competitor

C

Competitor

D

Competitor

E

Competitor

F

September 20, 2011 Sanford C. Bernstein – Strategic Decisions Conference 2011 16

Jeep New & refreshed vehicles gaining traction in Europe

Total Jeep up 41% to ~15K units

Year-over-year registrations increase largely due to performance of Wrangler and Compass

Compass: 4x last year levels

Wrangler: +66%

Several key markets experienced strong performance

Italy: +91%

Germany: +67%

France: +95%

Spain: +20%

Switzerland: +31%

Several product actions introduced to market in the quarter

Refreshed Compass launched in late April equipped with 2.2 CRD diesel engine ranging 136-163hp

Available with 2WD & AWD

2011 Grand Cherokee (the most awarded SUV ever) available with a new diesel engine since June

3.0 CRD available with 190hp & 241hp

Introduction of Laredo & Limited trims

Introduction of the 70th Anniversary package (April)

Available on Wrangler, Wrangler Unlimited & Compass

Package includes unique exterior badging and special interior trim

September 20, 2011 Sanford C. Bernstein – Strategic Decisions Conference 2011 17

H1 „09 H1 „10 H1 „11

The shift in portfolio – The first evidence in H1 2011 (EU27+EFTA passenger cars)

• FGA gradually reducing dependence from smaller segments on the back of new product launches…

Alfa Romeo Giulietta contributing the most, with 220 bps share gain vs. prior year in C-segment

Strong pace for Jeep branded products resulting in greater presence in SUV segment (up 31% over same period in 2010)

• …while consolidating presence in lower spectrum of market…

Fiat 500 gaining 140 bps share in A-segment

Share gain of 20 bps by Punto in B-segment

…in expectation of full- quarter contribution of newly-launched Freemont & Ypsilon

42%

37%

7%6%

3%

1% 1%3%

0%

43%

35%

6%5%

3%

1% 2%

5%

0%

39%

34%

12%

3%2%

0%

4%4%

0%

Mini Small Compact Large MPV

Compact MPV &

MPV Large SUV LCV

derivatives

Others

12%

28%

22%

12%

4%

8% 8%

2%

5%

11%

28%

21%

11%

4%

9% 10%

2%

5%9%

25%

20%

12%

4%

9%

13%

2%

6%

September 20, 2011 Sanford C. Bernstein – Strategic Decisions Conference 2011 18

• The most updated and complete product offerings of any EU producer

• Fiat Professional best in class in CO2 emissions and the widest CNG range in LCV market

• Strong distribution network

• Launched in May, a best-selling van whose 5 generations have received international awards and 2.2+ million units sold since 1981

Enhanced versatility to serve independent workers in various sectors, large fleets, convertible recreational vehicles and specialist transportation

Well structured and diversified product offering with ~2,000 different combinations of chassis, engine and mechanics

• Record-low consumption and CO2 emission levels (~15% reduction compared with Euro4 engines)

A step further with an extended range of Euro5 diesel engines ranging 115-177hp, also available in CNG version

Light Commercial Vehicles: Fiat Professional

September 20, 2011 Sanford C. Bernstein – Strategic Decisions Conference 2011 19

Industry Units (000s)

Chrysler Group performance (H1 2011 vs. H1 2010)

Sales Market share

Key Messages (year-over-year)

+21% 9.9%

(up 70 bps)

+15%

14.8% (up 160 bps)

5,703

6,449

H1 2010 H1 2011

798 822

H1 2010 H1 2011

• Retail sales (excluding fleet) increased 43%

• Retail of retail market share* increased to 8.6%, up 160 bps

• Fleet mix at 31%, down from 42%

• Key performers included: • Jeep Grand Cherokee (+114%) • Jeep Compass / Patriot (+89%) • Chrysler 200 (32k vehicles sold) • Dodge Durango (24k vehicles sold)

• Retail sales (excluding fleet) increased 20%

• Retail of retail market share* increased to 12.9%, up 190 bps

• Key performers included: • Jeep Grand Cherokee (+130%) • Jeep Wrangler (+34%) • Dodge Journey (+53%)

* Company calculation; retail sales (excluding fleet) versus industry retail sales (excluding fleet)

Chrysler: sales in US & Canada outpace industry

September 20, 2011 Sanford C. Bernstein – Strategic Decisions Conference 2011 20

Q1 Q2

+64% +196%

Q1 Q2

+19%

+13%

Q1 Q2 Q1 Q22010 2011

15k

8k

23k

10k

Q1 Q2

+64%

+112%

Key new vehicle contributors in US market New and redesigned vehicles launched in 2010 driving increased sales

September 20, 2011 Sanford C. Bernstein – Strategic Decisions Conference 2011 21

1.5

2.3

0.6

0.3

0.4

0.1 0.1 0.1 (0.0) 0.0

0.4 0.0 0.0

0.2 0.1

0.1

0.2

0.2 0.1 0.1 (0.0)

0.1 (0.0) 0.0

0.7

0.3

0.8

0.1

0.4

0.4

0.8

0.3

0.4

0.4

0.5

2010 MarketDrivengrowth

Marketsharegain

NewMarkets

MarketDrivengrowth

Marketsharegain

NewMarkets

MarketDrivengrowth

Marketsharegain

NewMarkets

MarketDrivengrowth

Marketsharegain

NewMarkets

MarketDrivengrowth

Marketsharegain

NewMarkets

MarketDrivengrowth

Marketsharegain

NewMarkets

MarketDrivengrowth

Marketsharegain

NewMarkets

2014ETotal

growth

0.6

1.2

0.5

2.3

3.6

5.9

Market driven growth

Market share gain

New Market

0.8

0.1

0.5

0.3

0.4

0.1

0.1

(millions of units – Excl. JVs)

Critical mass, greater geographic diversification

Fiat & Chrysler combined volumes

September 20, 2011 Sanford C. Bernstein – Strategic Decisions Conference 2011 22

The iconic assets

• Increase product differentiation to target new customers in the high-end sport cars segment

• Keep innovating with a new model every year to sustain turnover and reinforce brand

• Selectively exploit Special Series to target high-end customers and collectors

• Continuing search for opportunities in emerging markets, maintaining exclusivity in mature ones

• Personalization, one-off program, spare parts and after sales services improvement

• New generation of Quattroporte

• Extend luxury market coverage by entering high-end E and I segments

• Maintain and sustain GranTurismo and GranCabrio products in H segment

• Increase global market shares in all segments

• Dealer network improvement to support volume growth

• Production efficiencies and fixed cost optimization

September 20, 2011 Sanford C. Bernstein – Strategic Decisions Conference 2011 23

Net profit (€mn)

Net industrial debt

(€mn)

Liquidity (€bn)

Fiat ex Chrysler improving €391mn before €881mn (US$1,268mn) paid to Chrysler for an incremental 16% ownership interest (on a fully diluted basis)

• Strong cash flow from operating activities

• Capex at €794mn, in line with FY guidance

• Dividend payments of €172mn

Revenues

(€bn)

Trading profit (€mn)

Trading margin

• Chrysler contributed €3.3bn for June

• FGA up 2.7%

• Double-digit growth for Luxury brands and Components

• Chrysler contributed €150mn for June

• Ex Chrysler, €68mn increase despite difficult trading conditions in Europe

• Strong performance at Components and Luxury & Performance brands

• FGA holding trading profit despite continued weak demand for passenger car in most European markets

• Fiat ex-Chrysler €0.9bn below Mar-end level, mainly reflecting disbursement for 16% stake in Chrysler

• Quarter-end position not inclusive of proceeds from recent €1.5bn bond issuances (settled on July 8, 2011) and disbursements for UST & Canada ownership stakes and UST rights under Equity Recapture Agreement

Q2 ‟11 highlights Significant improvements across the board, with and ex Chrysler

Note: Q2 ’10 figures are provided herein on a pro-forma basis to reflect a carve-out of Fiat operations from the historical Fiat Group financial statements

• FGA: 2.5%

• Ferrari: 13.9%

• Maserati: 5.4%

• Components & Production Systems: 3.4%

• Reported net profit reflects measurement of ownership interest in Chrysler upon consolidation, net of unusual charges, for €1,058mn

• Ex one-off items and related tax impacts, net profit of €156mn (ex Chrysler €76mn, up €68mn over Q2 „10)

(17)

489

13.1

9.4

307

3.3%

Q2 „10 Q2 „10

Mar-end „11

Mar-end „11

Q2 „10

Q2 „10

+6.5%

+22.1%

10.0

375

3.8%

Ex Chrysler

+40.2%

+71.0%

13.2

525

4.0%

Reported

Q2 „11

Ex Chrysler Reported

Q2 „11

Ex Chrysler Reported

Q2 „11

1,380

979

12.2

Ex Chrysler

1,237

3,407

19.2

Reported

Q2 „11

Ex Chrysler Reported

Jun-end „11

Ex Chrysler Reported

Jun-end „11

September 20, 2011 Sanford C. Bernstein – Strategic Decisions Conference 2011 24

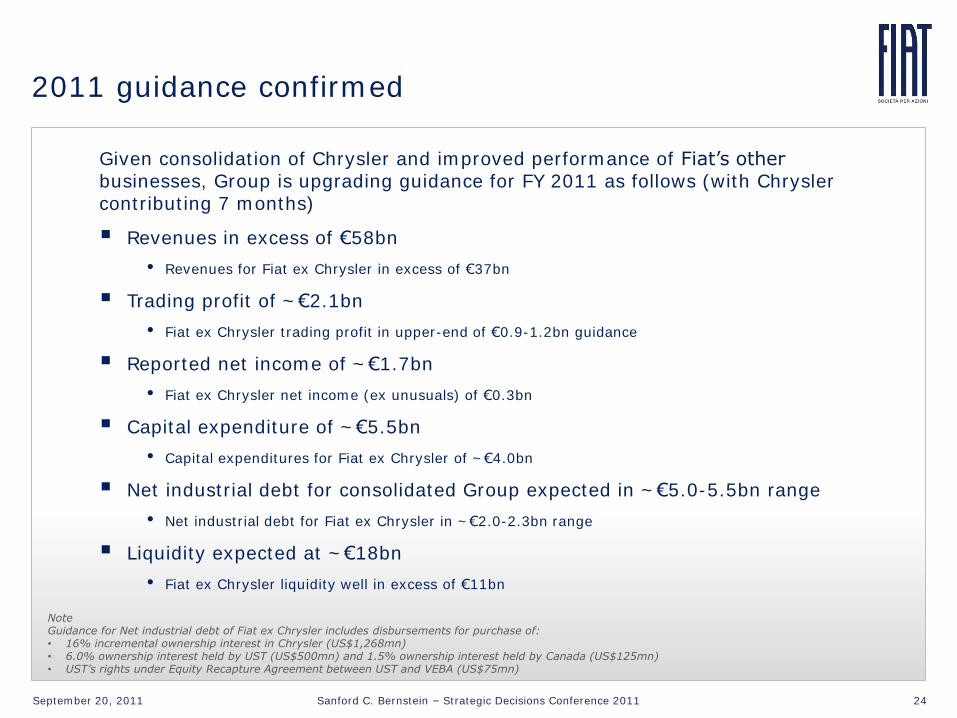

Given consolidation of Chrysler and improved performance of Fiat‟s other businesses, Group is upgrading guidance for FY 2011 as follows (with Chrysler contributing 7 months)

Revenues in excess of €58bn

• Revenues for Fiat ex Chrysler in excess of €37bn

Trading profit of ~€2.1bn

• Fiat ex Chrysler trading profit in upper-end of €0.9-1.2bn guidance

Reported net income of ~€1.7bn

• Fiat ex Chrysler net income (ex unusuals) of €0.3bn

Capital expenditure of ~€5.5bn

• Capital expenditures for Fiat ex Chrysler of ~€4.0bn

Net industrial debt for consolidated Group expected in ~€5.0-5.5bn range

• Net industrial debt for Fiat ex Chrysler in ~€2.0-2.3bn range

Liquidity expected at ~€18bn

• Fiat ex Chrysler liquidity well in excess of €11bn

2011 guidance confirmed

Note Guidance for Net industrial debt of Fiat ex Chrysler includes disbursements for purchase of: • 16% incremental ownership interest in Chrysler (US$1,268mn) • 6.0% ownership interest held by UST (US$500mn) and 1.5% ownership interest held by Canada (US$125mn) • UST’s rights under Equity Recapture Agreement between UST and VEBA (US$75mn)

September 20, 2011 Sanford C. Bernstein – Strategic Decisions Conference 2011 25

A reminder of April 2010 Investor Day Fiat & Chrysler 2010-14 financial targets (pro-forma combined from 2010)

>32

37 45 57 64

32

41

45

48

52

>64

76

85

97

104

2.0%

4.0%

5.4%

6.3%

7.2%

2.2%

4.8%

6.2%

7.1%

8.0%

0%

2%

4%

6%

8%

10%

12%

14%

-12

8

28

48

68

88

108

128

2010E 2011E 2012E 2013E 2014E

Tradin

g m

argin

Net R

even

ues (

€bn

)

Fiat Chrysler Eliminations Trading margin range - Low Trading margin range - High

(IFRS) CAGR 2010-14 = 12%

September 20, 2011 Sanford C. Bernstein – Strategic Decisions Conference 2011 26

What is the future of Fiat-Chrysler?

Totally shared • Architectures

• Powertrains

• Manufacturing strategies

Multi-brand

Multi-national

Multi-ethnic

"Halfway to heaven and just a mile out of hell” (Bruce Springsteen)

How will the automotive industry look going forward?

Two key truths of this industry

• Very capital intensive

• Highly sensitive to operating leverage

Consequence

• Limited number of players

- 5 or 6 global with 6+ million vehicles

• Highly-efficient industrially but with a keen sense of markets & brands

• Geographically diversified

• Ready to tackle Chinese threat

September 20, 2011 Sanford C. Bernstein – Strategic Decisions Conference 2011 27

Contacts

Marco Auriemma +39-011-006-3290 Vice President

Alexandra Deschner +39-011-006-2308

Paolo Mosole +39-011-006-1064

Sara Nicola +39-011-006-2572

Maristella Borotto +39-011-006-2709

fax: +39-011-006-3796

email: [email protected]

website: www.fiatspa.com