on - lamprell/media/files/l/lamprell-v3/... · 2019-09-19 · strengthen position in core markets...

TRANSCRIPT

l a m p r e l l . c o m

Mo

ray E

ast

fab

ricati

on

Half yearresults 2019

19 September 2019

Disclaimer

2

This presentation contains certain forward-looking statements relating to the business,

financial performance and results of the Company and/ or the industry in which it operates.

Forward-looking statements concern future circumstances and results and other

statements that are not historical facts, sometimes identified by the words “believes”,

“expects, “predicts”, ”intends”, “projects”, “plans” “estimates”, “aims”, “foresees”,

anticipates”, “targets” and similar expressions. The forward-looking statements, contained

in this document, including assumptions, opinions and views of the Company or cited from

third party sources are solely opinions and forecasts which are uncertain and subject to

risks. A multitude of factors can cause actual events to differ significantly from any

anticipated development. Neither the Company nor any of its officers or employees

guarantees that the assumptions underlying such forward-looking statements are free from

errors nor does any of the foregoing accept any responsibility for the future accuracy of the

opinions expressed in this document or the actual occurrence of the forecasted

developments.

No representation or warranty (express or implied) is made as to, and no reliance should

be placed on, any information, including projections, estimates, targets and opinions,

contained herein, and no liability whatsoever is accepted as to any errors, omissions or

misstatements contained herein, and, accordingly, neither the Company nor any of its

subsidiary undertakings nor any such person’s officers or employees accepts any liability

whatsoever arising directly or indirectly from the use of this document.

Highlights

Operational review

Strategy

Financial review

Outlook

Appendices

123456

Agenda

3

HighlightsChristopher McDonald

CEO

l a m p r e l l . c o m

Mo

ray E

ast

weld

ing

HighlightsFoundations for growth

5

▪ Excellent safety performance – TRIR 0.16*

▪ East Anglia One operationally completed, Moray

East progressing to schedule

▪ Strong bid pipeline across oil and gas and

renewables: progressing closer to awards

▪ Net cash reduced, but expected to improve in 2H

▪ Operational improvements ahead of major work

returning to yards$6.3bnBid Pipeline

$441.0mBacklog

$50.2mNet Cash

$106.4mRevenue

$(51.9)mNet loss

* Total recordable injury rate

OperationalreviewChristopher McDonald

CEO

l a m p r e l l . c o m

Com

pact

Dri

ller

7

Moray East:

▪ Project on time and on budget

▪ Yard set up improved for throughput and

efficiency of fabricating serial jackets

▪ Fabrication peaks in Q4 2019 with final

deliveries early Q3 2020

Rig refurbishment:

▪ 9 completed YTD

▪ 12 stacked

▪ Scopes continue to be below strong market

levels but improving

East Anglia One:

▪ All jackets installed by client

▪ Contractual close out progressing

Operational reviewMoray East ramping up to peak activity

8

IMI Maritime Yard

▪ Dredging and site preparation works

completed

▪ Construction work commenced

▪ On schedule for full commissioning in

2022

IMI sub-contract work

▪ LOI for first two new build jackup rigs

extended

▪ Detailed technical discussions with

client continue

Saudi Aramco LTA programme

▪ Bidding volumes as anticipated

▪ Multiple packages submitted

▪ Several bids in final stages of

preparation

Strategic initiatives in Saudi ArabiaExposure to transformational opportunities

9

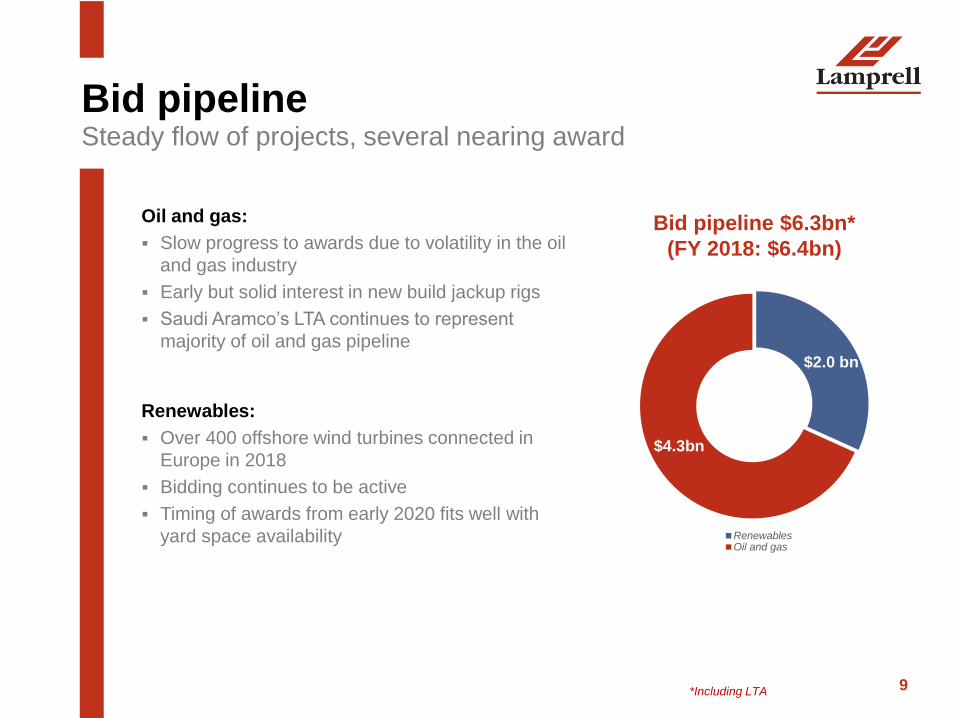

Renewables:

▪ Over 400 offshore wind turbines connected in

Europe in 2018

▪ Bidding continues to be active

▪ Timing of awards from early 2020 fits well with

yard space availability

Oil and gas:

▪ Slow progress to awards due to volatility in the oil

and gas industry

▪ Early but solid interest in new build jackup rigs

▪ Saudi Aramco’s LTA continues to represent

majority of oil and gas pipeline

Bid pipeline $6.3bn*

(FY 2018: $6.4bn)

*Including LTA

$2.0 bn

$4.3bn

RenewablesOil and gas

Bid pipelineSteady flow of projects, several nearing award

Strategy updateChristopher McDonald

CEO

l a m p r e l l . c o m

Sta

cked

rig

s -

Ham

riyah

Strengthen position in core markets

▪ New build jackup market severely challenged

but new opportunities begin to arise

Implement EPC(i) strategy

▪ Saudi Aramco LTA programme to open up

projects higher up the value chain

Expand into new markets and geographies

▪ Strong foothold in European offshore wind

market

▪ Multiple projects due for award from early 2020

▪ Focus on strategic presence in Saudi Arabia

Delivering on our strategyGaining a stronger foothold in new markets

11

FinancialreviewTony Wright

CFO

l a m p r e l l . c o m

Mo

ray E

ast pro

ject

constr

uctio

n in

Ham

riyah

Fa

cili

ty

▪ Revenue in line with forecast, to ramp up in 2H 2019 as per project scheduling

▪ Loss driven by cost pressures at low revenue levels

▪ Net cash reducing in line with working capital requirements and will improve in 2H

2019

▪ Total overheads $48.8 million, operational overheads $19.0 million, G&A $29.3 million

▪ Debt facility extended until December 2019 as new facility negotiations progress

Income statement

($m, unless stated otherwise)HY 2019 HY 2018

Revenue 106.4 155.1

EBITDA (29.6) (6.2)

EBITDA margin (27.8)% (4.0)%

Loss from continuing operations after

income tax(51.9) (21.9)

Reported diluted loss per share (US

cents)(15.20) (6.42)

Balance sheet

($m)HY 2019 FY2018

Net cash as at 30 June 50.2 80.0

Tangible net assets 314.7 363.0

Revenue by

segmentHY2019$m HY2018$m

Rigs 13.2 52.0

EPC(I) 61.9 74.7

Contracting

services31.3

28.4

13

Key FinancialsBalance sheet supports business through downturn

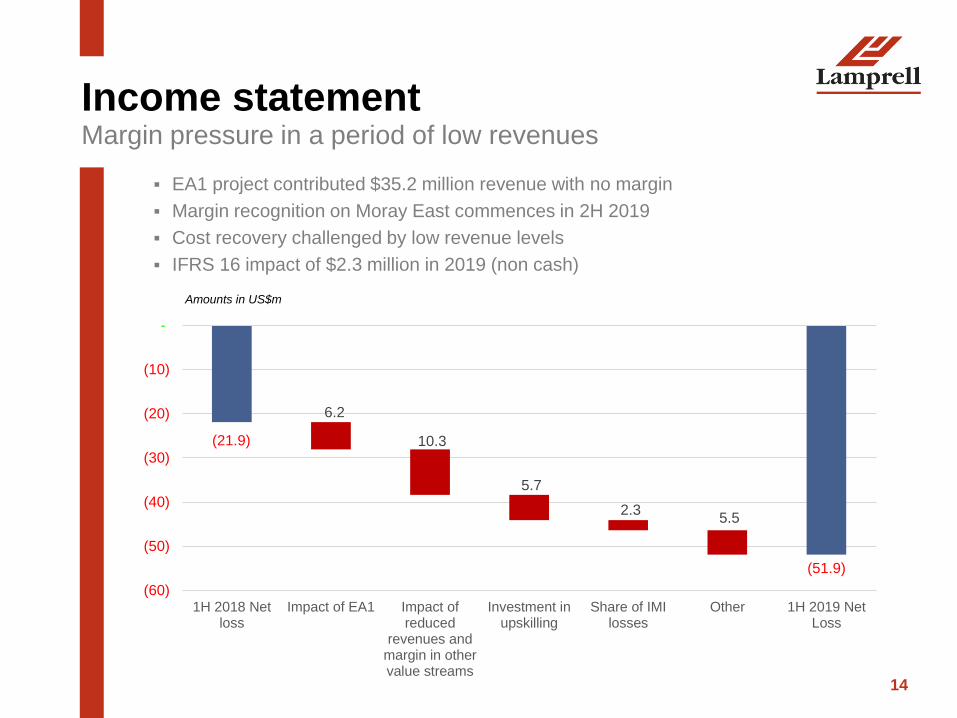

▪ EA1 project contributed $35.2 million revenue with no margin

▪ Margin recognition on Moray East commences in 2H 2019

▪ Cost recovery challenged by low revenue levels

▪ IFRS 16 impact of $2.3 million in 2019 (non cash)

14

Income statementMargin pressure in a period of low revenues

Amounts in US$m

(21.9)

(51.9)

6.2

10.3

5.7

2.3 5.5

(60)

(50)

(40)

(30)

(20)

(10)

-

1H 2018 Netloss

Impact of EA1 Impact ofreduced

revenues andmargin in othervalue streams

Investment inupskilling

Share of IMIlosses

Other 1H 2019 NetLoss

▪ Net cash reduction driven by Moray East working capital requirements, minor

yard investment and operational losses

15

Net cash$50.2m in line with forecast

Amounts in US$m

80.0 7.7 22.4

9.6

5.5

50.2

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

Net Cash as at 31stDecember 2018

Movement inworking capital

Operating cash flows Asset additions Other Net Cash as at 30thJune 2019

▪ Sufficient headroom for medium term working

capital requirements

▪ Focus on monetising inventory on the

balance sheet

▪ $37m restricted cash

▪ Negotiations for new debt facility at an

advanced stage

Debt packageHY19

$m

FY18

$m

Term loan - 20

Working capital facility 40 50

Revolver - -

Total funded facilities 40 70

Committed bonding - -

16

Balance sheetSecuring sufficient headroom for growth

Balance sheetHY19

$m

FY18

$m

Strategic investments 176.4 175.4

Hamriyah yard

improvements 38.9 34.8

New pipe shop 24.8 23.0

Rig kit inventory 69.1 69.1

IMI capital 43.6 48.5

Other Assets 305.6 281.2

Gross Cash 90.5 99.8

Total Assets 572.5 556.4

Tangible Net Assets 314.7 363.0

▪ Financial performance in 1H 2019 in line

with expectations

▪ Focus on cost remains

▪ Incremental investment to sustain

operational capability

▪ Net cash will improve moderately in 2H 2019

17

Financial outlookProfitability remains challenged in 2019

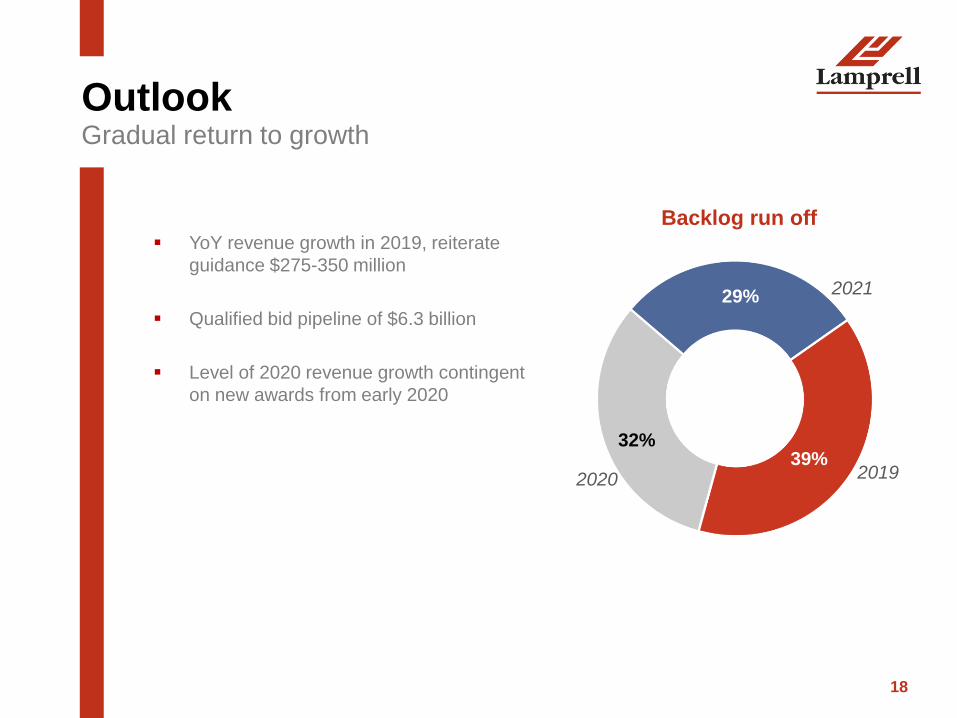

▪ YoY revenue growth in 2019, reiterate

guidance $275-350 million

▪ Qualified bid pipeline of $6.3 billion

▪ Level of 2020 revenue growth contingent

on new awards from early 2020

18

OutlookGradual return to growth

39%32%

29%

2020 2019

Backlog run off

2021

Appendix

l a m p r e l l . c o m

Mo

ray E

ast pro

ject

constr

uctio

n in

Sharja

h F

acili

ty

20

Financial summary

Amounts in $mHY 2019, $m

Underlying/ Reported

HY 2018 $m

Underlying/ Reported

Revenue 106.4 155.1

Cost of sales (119.4) (147.9)

Gross (loss) / profit (13.0) 7.2

Gross margin % (12.2%) 4.6%

G&A (29.3) (22.7)

Operating loss (41.7) (15.7)

Finance costs - net* (4.1) (1.8)

Share of loss in investments accounted using

the equity method (6.1) (3.3)

Loss before income tax (51.9) (20.9)

Income tax expense (0.01) (1.1)

Loss for the period (51.9) (21.9)

Total loss attributable to equity holders (51.9) (21.9)

* Represents the net balance of finance costs and finance income

21

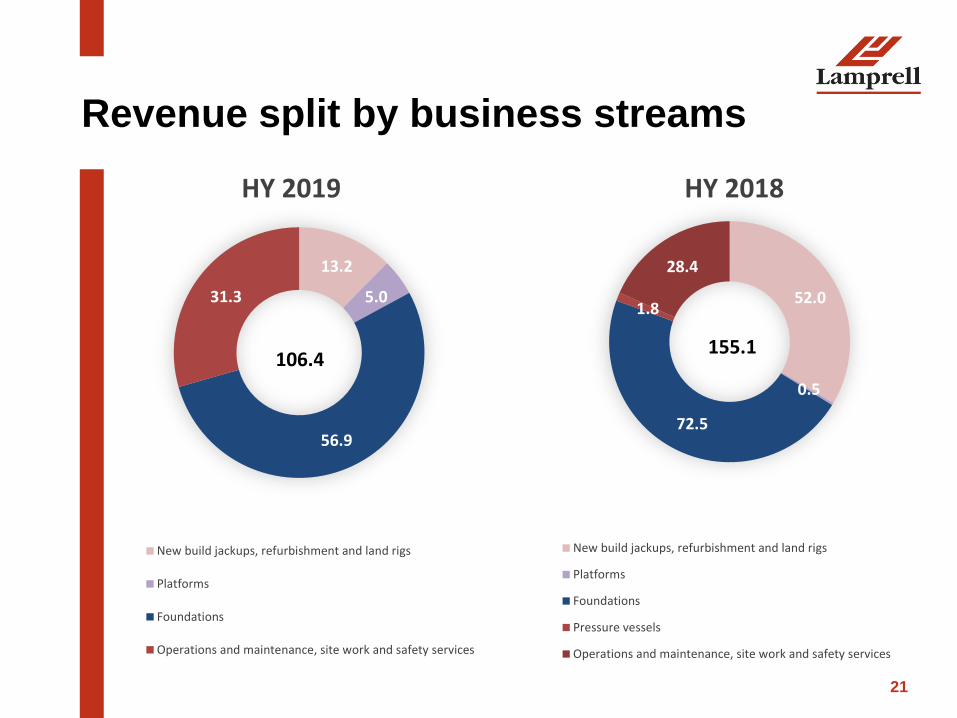

Revenue split by business streams

13.2

5.0

56.9

31.3

HY 2019

New build jackups, refurbishment and land rigs

Platforms

Foundations

Operations and maintenance, site work and safety services

106.4

52.0

0.5

72.5

1.8

28.4

HY 2018

New build jackups, refurbishment and land rigs

Platforms

Foundations

Pressure vessels

Operations and maintenance, site work and safety services

155.1

22

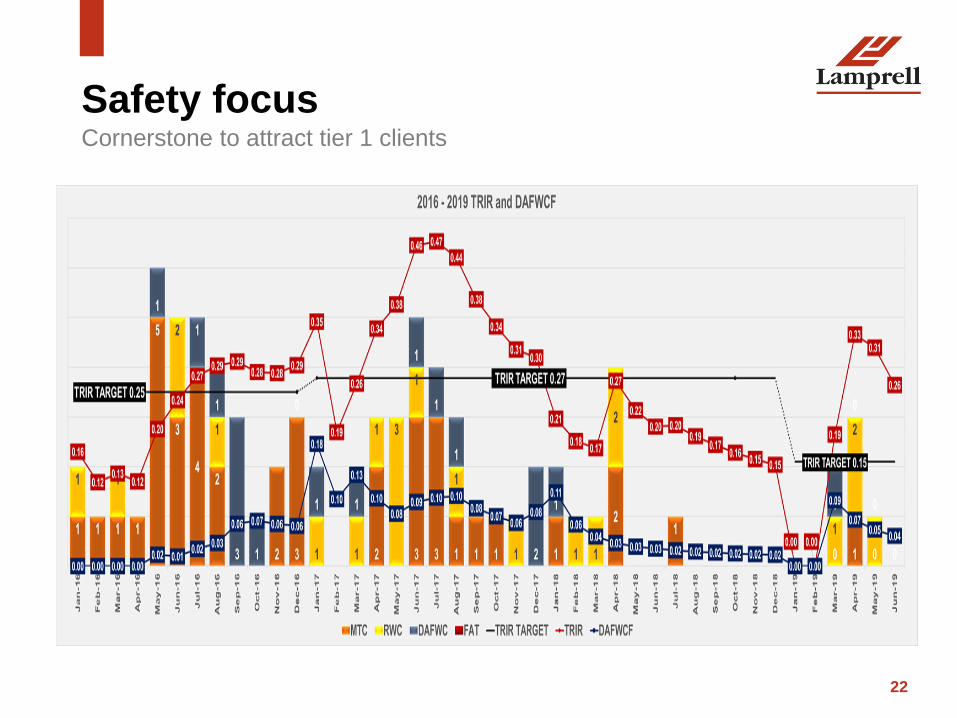

Safety focusCornerstone to attract tier 1 clients