oipa june 8, 2008. why are we here? “all-climate-all-the-time” policy environment new climate...

TRANSCRIPT

OIPAJune 8, 2008

Why are we here?

“All-Climate-All-The-Time” policy environment New climate policy seems highly likely Assumption that gas is a climate policy winner An “upstream” approach could require natural gas

processors and/or producers to buy billions of dollars of “allowances” for end user emissions

E&P investment and resulting supply effects could be devastating

Why else are we here?

Issue politics – and a need to rethink our energy policy advocacy effectiveness

Senate debate on the Lieberman/Warner – Boxer Substitute cap and trade bill began on June 2.

The Administration now supports a modest legislative program (not Lieberman/Warner that it has threatened to veto).

House legislation will be different….

L/W/Boxer: cap greenhouse gas emissions at 2005 levels in 2012; achieve about 70% emission reductions by 2050.

Obligations can be satisfied one of four ways: 1) acquire allowances; 2) use less carbon intensive fuel; 3) use technology to capture/offset emissions; and 4) improve efficiency.

Estimates of allowance costs vary according to one’s view of these options and allowance markets.

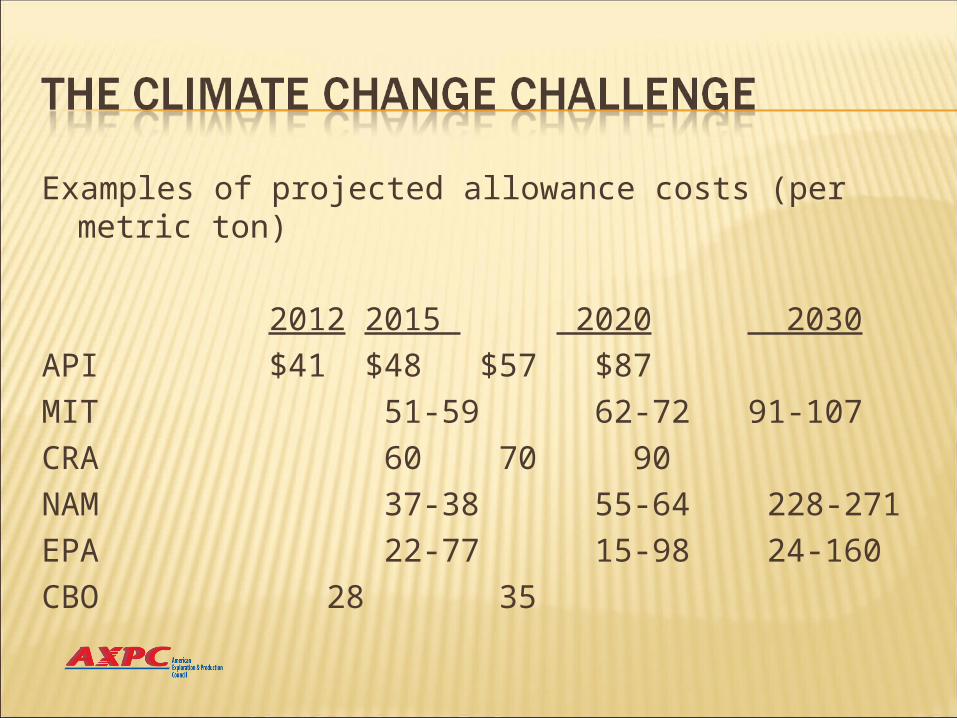

Examples of projected allowance costs (per metric ton)

2012 2015 2020 2030API $41 $48 $57 $87MIT 51-59 62-72 91-107CRA 60 70 90NAM 37-38 55-64 228-271EPA 22-77 15-98 24-160CBO 28 35

Range of Impacts on the Natural Gas Industry(API estimates, in billions)

Costs Producers Processors End Users

$41/ton $5.0 $1.85 $39.6

$57/ton $7.0 $2.2 $59.9

Wood Mackenzie Analysis(on E&P costs of consumer allowances)

Natural gas supply at risk 32% in 2012, 45% in 2017 @ 100% 5% in 2012, 14% in 2017 @ 50% in addition to ICF study facility emission cost effects

Prices “…sharply higher…in response to any threat to US natural gas

supplies.”

Where are we?

AXPC and some others arguing that an upstream approach will distort investment decisions, hurt consumers. Some refiners and others are opposing.

AGA position: downstream coverage of utilities, industrials; residential and small commercial users initially outside cap to continue reductions; LDCs to work with state commissions. Review progress in 2020.

Arguments for: LDC customer emissions already reduced to 1970s levels; home and appliance efficiency programs more effective than price signals.

If the bill isn’t going to pass, why are we so concerned?

All three Presidential candidates are senators who support cap and trade programs.

The next Congress and/or Administration is likely to use L/W/B as the blueprint for it’s program.

Climate change policy can be an early “win” for the next Congress and Administration.

Strong, coordinated, effective advocacy is needed

If past House votes on energy taxes, permitting and new regulatory actions are an indication –

If larger Democrat majorities are possible –

No matter which president we have –

We must do better by getting “back to basics”

Back to BasicsImproving our Policy Effectiveness

_____________________________________________________________

AXPC B2B Good Practices Guidelines Government Relations

Candidate Support Communications

Government Relations: We recognize the importance of building strong relationships with federal elected/appointed officials for the development of sound federal legislation.

Candidate Support: We encourage the formation of company-established political action committees (PACs) which can provide financial support on a bi-partisan basis to pro-business/oil and gas candidates.

Communications: We must share our views with both policymakers and our employees! We should seek active volunteer employee involvement in the political and electoral process through effective communications.

Together we can improve our policy effectiveness!

Thanks!

Questions?