oilvoice magazine | may 2012

DESCRIPTION

Edition 2 of the OilVoice MagazineTRANSCRIPT

Edition Two - May 2012

The big 6 challenges for an oil and gas translator

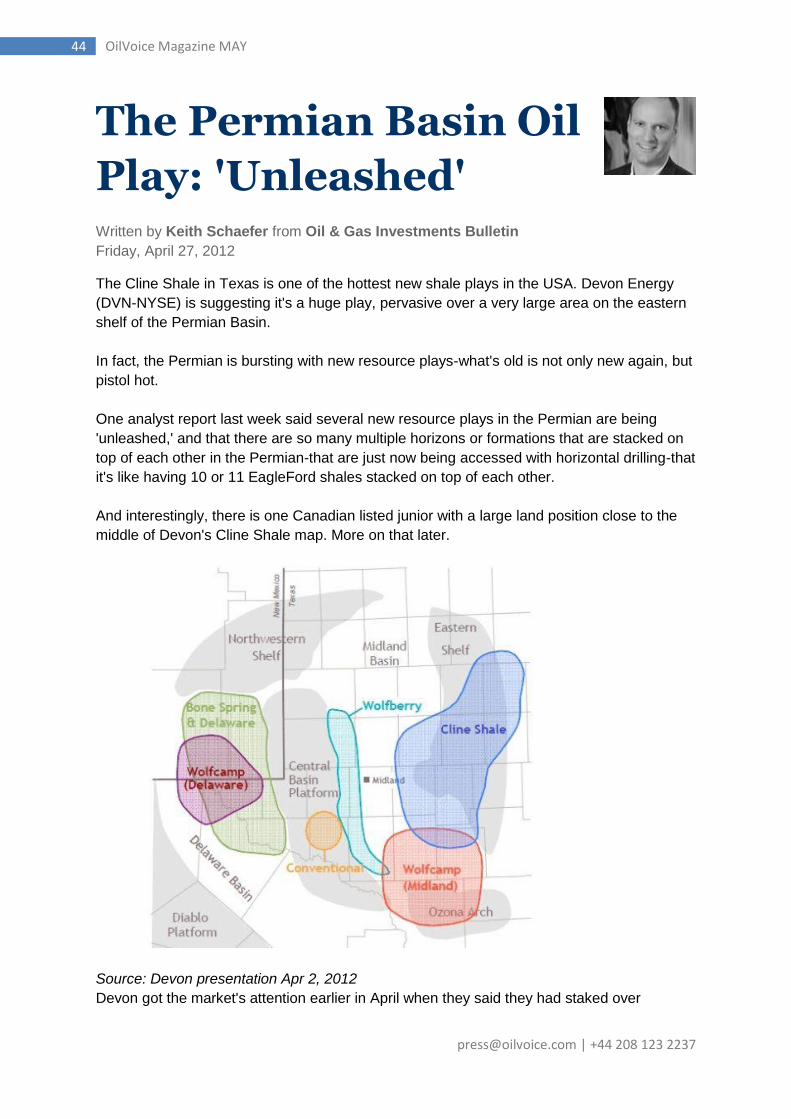

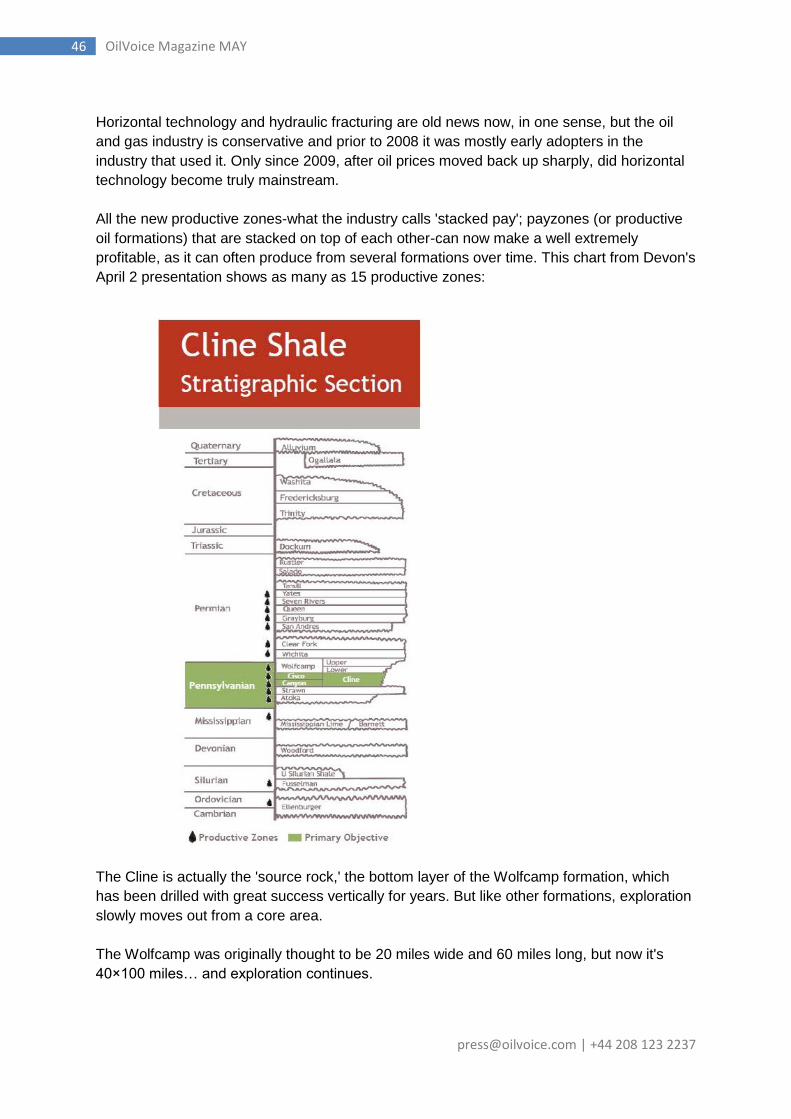

The Permian Basin Oil Play: 'Unleashed'

[email protected] | +44 208 123 2237

1 OilVoice Magazine MAY

Adam Marmaras Manager, Technical Director

Welcome to the second edition of the OilVoice

Magazine. We were very pleased with the

download numbers of the first edition and

thought it a project worth continuing. Thanks for

all your feedback on the first issue as well. We've

removed the traditional column format of a

magazine, and gone for full page text. It works a

lot better on iPads and other devices. Please

keep the feedback coming, we always read it.

This month we have some new great

contributors - Keith Schaefer from Oil & Gas

Investments Bulletin, Raj Ladwa from Contract

Jobs and Chris Wilson from Evaluate Energy. Be

sure to take a look at what they've read, and

visit their sites. If you'd like to reach the oil and

gas community and have something to say, then

get in touch.

Thanks for reading!

Issue 2 – May 2012

OilVoice

Acorn House

381 Midsummer Blvd

Milton Keynes

MK9 3HP

Tel: +44 208 123 2237

Email: [email protected]

Skype: oilvoicetalk

Editor

James Allen

Email: [email protected]

Advertising/Sponsorship

Adam Marmaras

Email: [email protected]

Tel: +44 208 123 2237

Social Network

Facebook: https://www.facebook.com/oilvoice Twitter: http://www.twitter.com/oilvoice

Google+: https://plus.google.com/118419367014120616513/

Linked In:

http://www.linkedin.com/groups/Oil

Voice-3162868

Read on your iPad

You can open PDF documents, such

as a PDF attached to an email, with

iBooks. When you view a PDF email

attachment, simply tap "Open in

iBooks," located in the upper-right

corner of the screen. iBooks will

open and you'll be able to view your

PDF using the iBooks app.

[email protected] | +44 208 123 2237

2 OilVoice Magazine MAY

Contents

May’s Featured Authors Biographies of this months featured authors. 3 Watching World Energy: Flying on a solar impulse By Eric Watkins 6 Watching World Energy: The turn of a friendly card By Eric Watkins 8 Featured University: University of Aberdeen This month we are featuring University of Aberdeen 11 How exporting LNG could bring serious wealth to the U.S. By Keith Schaefer 13 Watching World Energy: Bottling up Canada's oil exports By Eric Watkins 17 Obama pushes Iran sanction to breaking point By Hanife Mehmet 19 Exploration: Explorers be good... By David Bamford 20 Iran halts oil sales to EU By Raj Ladwa 24 The big 6 challenges for an oil and gas translator By Camilo Muñoz 25 Exploration: Explorers be good or be lucky... By David Bamford 27 Greenhouse Gas Emissions: In Situ oil sands producers drive efficiencies, but integrated operations take a step back By Chris Wilson

32

OilEdge: Know your customers By David Bamford 35 Review: Argentina - Under the spotlight By David Bamford 40 Recently added companies An overview of the recent companies added to the OilVoice database 42 The Permian Basin Oil Play: 'Unleashed' By Keith Schaefer 44 EnQuest to expand North Sea oil projects An overview of the recent companies added to the OilVoice database. 47

[email protected] | +44 208 123 2237

3 OilVoice Magazine MAY

Featured Authors

OilVoice is always on the lookout for quality, original content. We receive submissions

from people in the industry on a regular basis, who in turn benefit from our large user

base. You get a chance to broadcast to the industry and spread the word, and we get

fantastic original content. Get in touch for more details!

Hanife Mehmet

Contract Jobs

Hanife Mehmet is a copywriter working for contractjobs.com, the contract only job board and news resource for freelance professionals. The site provides information for professional temporary workers from all leading industry sectors including the oil and gas sector.

Keith Schaefer

Oil & Gas Investments Bulletin

Keith Schaefer, editor and publisher of the Oil & Gas Investments Bulletin.

David Bamford

OilEdge

David Bamford is non-executive director of Tullow Oil, and a past head of exploration, West Africa and geophysics with BP.

Eric Watkins

Oil Diplomacy

Oil Diplomacy produces news, analyses, commentary and tailored research concerning the global oil and gas industry. Watching World Energy, which appears daily, comments on current events in the energy industry

Raj Ladwa

Contract Jobs

Raj Ladwa, a Journalism graduate, is currently a copywriter for Contract Jobs, providing Oil & Gas contractors with the latest industry news.

Camilo Muñoz

Translation Source

Translation Source helps companies communicate worldwide by offering comprehensive multilingual solutions based upon client needs. Our solutions are developed in more than 140 languages and include a full range of language translation and localization services, international training and e-learning development, interpretation, instruction, bilingual

staffing and other supporting linguistic services.

[email protected] | +44 208 123 2237

4 OilVoice Magazine MAY

Chris Wilson

Evaluate Energy

Chris joined Evaluate Energy in December 2007, gaining significant experience in Canadian company financial and operating data, specialising in unconventional energy.

Make the most of OilVoice

Jobs The is fast becoming the place candidates look for their next move in OilVoice Jobs boardthe industry. Featuring adverts from top draw recruiters, CV upload capability, and an easy application process. New jobs are appearing every day, so be sure to bookmark it. Company Directory

3330 company profiles, 5208 offices and 10765 people - all searchable by keyword and location. You can even export your results as an excel file. So the next time you are searching for a company or person, be sure to . give it a try

Advertise

OilVoice traffic numbers continue to climb and climb. If you'd like to reach a global audience of oil and gas professionals then it's easy to run an advert with us. We have solutions for every budget, so with us to discuss how we can help promote get in touchyour business now. Events

Let's face it, there are a lot of events in the oil and gas industry. It can be hard to keep track. The OilVoice Events Board contains hundreds of upcoming events, complete with descriptions and calendar bookmark functionality. Training Courses

You can never stop learning about the oil and gas industry. How do you find the course that's right for you? By visiting our . Training Courses section Free Membership Over the past ten years we've grown to 29653 members (let's call it 30,000). If you're not

a member then you should , it only takes a second. Then you'll be free to post start nowjob adverts, events and press releases.

[email protected] | +44 208 123 2237

6 OilVoice Magazine MAY

Watching World

Energy: Flying on a

solar impulse

Written by Eric Watkins from Oil Diplomacy

Tuesday, April 03, 2012

A team of two pilots plans to fly a solar-powered aircraft from Switzerland to Morocco in a

couple of weeks, calling it a rehearsal in the run-up to the plane's round-the-world flight in

2014.

'Flying as far as this, powered only by solar energy will be excellent training for the round-

the-world trip,' said Andre Borschberg, co-founder and chief executive of Solar Impulse, the

company behind the plan and the plane.

The Solar Impulse HB-SIA is the first aircraft that can fly day and night without fuel or

polluting emissions, demonstrating the potential of new technologies in terms of energy

reduction and the production of renewable energy.

The carbon fiber aircraft, which has the 63.4-meter wingspan of an Airbus A-340 and the

weight of an average family car at 1,600 kg, is the result of what its backers say are 'seven

intense years of work, calculations, simulations and tests.'

The pending flight will also enable the mission team do some necessary prepping in

procedures of coordinating with airports, integrating their plane into air traffic and providing

the logistics for servicing the aircraft.

MORE THAN A FLIGHT

The venture, though, is more than just a flight and it's even more than just a dress rehearsal

for the longer mission in 2014. The coming air journey to Morocco will also serve to

showcase that country's new solar industry.

'The Kingdom of Morocco will welcome Solar Impulse in the spring of this year,' said an

announcement issued by the Moroccan Agency for Solar Energy, also known as MASEN.

In case you haven't heard of it, MASEN is in charge of the implementation of the integrated

Moroccan Solar Plan, which aims at developing a minimum power capacity of 2,000 MW by

2020.

By 2020, Morocco intends to build five solar complexes, not only generating the 2000 MW,

[email protected] | +44 208 123 2237

7 OilVoice Magazine MAY

but also eventually preventing the emission 3.7 million tons of CO2.

All of that could be a real boost to the economy of Morocco, which currently imports 97% of

its energy needs.

The solar-thermal power plant in the region of Ouarzazate, which will have a capacity of 160

MW, is part of the solar complex, housing a range of solar installations which, by 2015, will

generate a total of 500 MW.

DESTINATION 'FITS THE PLAN'

Borschberg and fellow pilot Bertrand Piccard say their destination in Morocco fits their flight

plans as well as the environmental aspirations expressed in their solar-powered flight.

'This destination corresponds fully with the goals we had set ourselves, in terms of distance

and flight duration,' said Borschberg, adding that the pair did not have 'a moment's hesitation

in accepting the idea of working with Morocco.'

Picard said the two fliers are full of admiration for the vision of Morocco's King Mohammed

VI and the 'intelligent energy policy' adopted by his country.

'We are delighted to support it,' Piccard said. 'Theirs is a pioneering project, which clearly

demonstrates that the clean technologies we are promoting with Solar Impulse also have a

role to play in everyday life.'

Piccard and Borschberg are not the only ones supporting King Mohammed and his solar

plan. Even the World Bank is behind it, approving $297 million in loans to Morocco to help

finance the solar project at Ouarzazate.

World Bank Group President Robert B. Zoellick said that Ouarzazate demonstrates

Morocco's commitment to low-carbon growth and could demonstrate the enormous potential

of solar power in the Middle East and North Africa.

A MULTIPLE WINNER

'This solar project could advance the potential of the technology, create many new jobs

across the region, assist the European Union to meet its low-carbon energy targets, and

deepen economic and energy integration in the Mediterranean,' said Zoellick, calling the

project 'a multiple winner.'

The 500 MW Ouarzazate solar complex will be among the largest Concentrated Solar Power

plants in the world, and international observers say it is 'an important step' in Morocco's

national plan to deploy 2000 MW of solar power generation capacity by 2020.

The United Nations agrees, and sees Morocco's project as a good role model for other

countries to follow.

[email protected] | +44 208 123 2237

8 OilVoice Magazine MAY

'The inauguration of its initial phase costing $200 million by the World Bank, and $97 million

from the Clean Technology Fund has placed Morocco in good stead to a realize an energy

future which could show the way for other countries struggling to honor their commitment to

climate change,' the UN said.

So, the Solar Impulse will be doing a little more than just making an historical flight when it

lands at Ouarzazate in a few weeks' time. It also will be showcasing the potential of a whole

new industry for Morocco, North Africa and the wider world.

View more quality content from

Oil Diplomacy

Watching World

Energy: The turn of a

friendly card

Written by Eric Watkins from Oil Diplomacy

Wednesday, April 04, 2012

So far, India has not been following the US lead when it comes to weaning itself off Iran's oil.

But that could soon change given the card played by the US in the sanctions game this

week.

That card came in the form of a $10 million reward offer by the US for 'information leading to

the arrest or conviction' of Hafiz Mohammad Saeed, leader of the Pakistan-based Lashkar-

e-Tayyiba terrorist organization.

'Saeed participated in the planning of the 4-day-long terrorist assault on Mumbai in

November 2008 that left 166 individuals dead, including six US citizens,' said the US

Department of State.

'Saeed and his organization continue to spread ideology advocating terrorism, as well as

virulent rhetoric condemning the United States, India, Israel, and other perceived enemies,' it

said.

[email protected] | +44 208 123 2237

9 OilVoice Magazine MAY

INDIA PLEASED

New Delhi could not have been more pleased, and it said so.

'India welcomes this new initiative of the government of the United States,' said External

Affairs Minister S.M. Krishna, adding that, 'In recent years, India and the United States have

moved much closer than ever before in our common endeavor of fighting terrorists.'

That view was underlined a few weeks ago when US Pacific Commander Admiral Robert

Willard told a Congressional hearing that India was one of several countries where US

special forces assist teams were operating.

'We have currently special forces assist teams - Pacific assist teams is the term - laid down

in Nepal, Bangladesh, Sri Lanka, Maldives, as well as India,' Adm Willard told the

Congressional hearing.

Adm Willard said Lashkar-e-Tayyiba is a 'very dangerous organization … so it is a very

important threat, and we're working very closely with the nations in the region to help contain

it.'

AFFILIATED WITH AL-QAEDA

He said Lashkar-e-Tayyiba 'is headquartered in Pakistan, affiliated with al-Qaeda… and

contributes to terrorist operations in Afghanistan and aspires to operate against Asia, Europe

and North America.'

That sounds like Iran, too, especially after the recent rant by on senior official.

'In the face of any attack, we will have a crushing response. In that case, we will not only act

in the boundaries of the Middle East and the Persian Gulf, no place in America will be safe

from our attacks,' said Massoud Jazayeri, a senior Republican Guards Commander.

'America, the Zionists and reactionary Arabs should pay attention that we will seriously

confront them wherever the Islamic Republic's interests are threatened,' Jazayeri said.

What guarantee does anyone have that Lashkar would not do the bidding of Teheran? That

alone may have prompted Washington's decision to put a price on Saeed's head - a decision

that could not have sounded any sweeter to India, Pakistan's arch enemy.

However, it also should be noted that the State Department announcement of a bounty on

Saeed's head coincided with a visit to India by US Undersecretary of State for Political

Affairs, Wendy Sherman, a visit that emphasized oil sanctions.

In a televised broadcast, Sherman said that India knows that relying on crude oil from Iran is

risky and that it may seek to diversify its energy sources for the sake of its energy security.

Sherman said that countries face numerous risks in importing crude oil from Iran, including a

[email protected] | +44 208 123 2237

10 OilVoice Magazine MAY

lack of insurance cover for ships as well as the inability of banking channels to transmit

money in the face of US sanctions.

These sound like curtain raisers to a change in India's recent policy on sanctions against

Iran.

IRAN'S POTENTIAL FEARED

Sherman met with Indian Foreign Secretary Ranjan Mathai on a range of issues, including

the agenda for the forthcoming meeting between Foreign Minister S.M. Krishna and

Secretary of State Hillary Clinton.

Indian news media cited sources as saying India's government expressed concerns over the

US sanctions, particularly the possibility that Iran has the potential to undermine the energy

security of India, which daily imports 340,000 barrels of oil from Iran.

Up until now, India has been saying it would adhere to UN sanctions against Iran but not

unilateral sanctions imposed by any country. However, that position could soon be changing

- especially given the bounty on Saeed.

In Saeed, Obama had a useful card up his sleeve, and played it well with India. It was the

turn of a very friendly card indeed, showing New Delhi that Washington understands its

concerns.

NO REASON TO BUY IRAN'S OIL

Still, much depends on the coming visit of Hilary Clinton, as well as on further US efforts to

assure India of the availability of alternative sources of oil in the event that it decides to

forego supplies from Iran.

On that score, Obama has been more than clear in recent days, telling world leaders that

there is sufficient oil available and that there is no reason for anyone to keep buying Iran's.

Some say it remains to be seen whether that message has been heard and understood in

New Delhi. Others say it is in the cards.

View more quality content from

Oil Diplomacy

[email protected] | +44 208 123 2237

11 OilVoice Magazine MAY

Featured University – University of Aberdeen

Contact

Geology & Petroleum Geology

School of Geosciences

University of Aberdeen

Meston Building

Aberdeen

AB24 3UE

Tel: +44 (0)1224 273433

Fax: +44 (0)1224 272785

Located at the heart of Europe’s energy capital, we

are a leading centre of geological training and

research. Working in partnership with industry we

build on their data and methods to understand

fundamental processes in the Earth System with

specific reference to the World’s sedimentary

basins. Our portfolio of training ranges from

undergraduate level BSc honours degrees, through

the full range of graduate programmes to

professional training for industry.

Suncor are proud to be an OilVoice Sponsor for University of Aberdeen

In 1967, we pioneered commercial development of Canada's oil

sands — one of the largest petroleum resource basins in the world.

Since then, Suncor has grown to become a globally competitive

integrated energy company with a balanced portfolio of high-quality

assets, a strong balance sheet and significant growth prospects. Across our operations,

we intend to achieve production of one million barrels of oil equivalent per day by

2020.

Want to Sponsor a University? OilVoice has created an opportunity for companies to

help students gain a valuable insight into the industry from a worldwide perspective by

sponsoring unrestricted OilVoice access to a university of their choice. Read more

The University of Aberdeen is today at the forefront of teaching,

learning and discovery, as it has been for 500 years. As the 'global

university of the north', we have consistently sent pioneers and

ideas outward to every part of the world. We are an ambitious,

research-driven university with a global outlook, committed to excellence in everything

we do.

rpsgroup.com/energy

Health, Safety, Environment and Risk Management

RPS Energy is a global multi-disciplinary consultancy, providing integrated technical, commercial and project management support services in the fields of geoscience, engineering and HS&E.

ContactJames Blanchard T +44 (0) 20 7280 3200 E [email protected]

[email protected] | +44 208 123 2237

13 OilVoice Magazine MAY

How exporting LNG

could bring serious

wealth to the U.S.

Written by Keith Schaefer from Oil & Gas Investments Bulletin

Thursday, April 05, 2012

Where will the wealth created by the fast growing Liquid Natural Gas (LNG) market be

concentrated in the coming years?

In a word-Australia. It's the #4 exporter of LNG in the world already, and seven new plants

are in various stages of planning and development, which would require $200 billion in

capital investment-and lots of jobs.

By comparison, America, which produces massive amounts of natural gas, sends a

shockingly small amount of the resource abroad.

Both are close to markets - Australia is closer to Asia, which imports vast quantities of LNG,

but the U.S. is also relatively close to these markets and closer to Europe, which holds some

major LNG consumers, like Spain and France. Both also have robust natural gas production.

And yet Australia is light years ahead of America in sending LNG overseas. How far? about

800 billion cubic feet (bcf) per year.

Now before we explore that gap further, here's a short-version background on LNG…

LNG is created by cooling natural gas to minus 256 degrees Fahrenheit, which transforms

the gas into a liquid. This liquid has about 1/600th the volume of natural gas, making its

transport over long distances much simpler -and much more economic.

While turning a gas into a liquid may seem to be the stuff of science fiction, it has its roots in

the 19th century when Carl Von Linde, an engineer in Munich, built the first practical

compressor refrigeration machine. The first LNG plant was built roughly a century ago in

West Virginia.

Is This 'New' Bakken Play Ready To Boom?

It's not the Bakken most investors have come to know.

But I expect that all to change, especially now that one small company operating here has

just hit TWICE on a HUGE new play-validating thousands of acres.

[email protected] | +44 208 123 2237

14 OilVoice Magazine MAY

That's why company insiders have been loading up on shares… AND why brokerage firms

have price targets 50% to 100% higher than today's share price.

As an OGIB reader, you can get the full update on this high-potential growth play - here in

my new findings. Go here for free access.

Of course, large-scale users of natural gas prefer to deal with the regular kind-not liquid and

frozen. Since gas is easier to move and doesn't need to be refrigerated, companies had to

then develop ways to reverse the process. So you have to liquefy the gas to move it, and

then 're-gasify' the natural gas to use it. That's a lot of work and means large infrastructure

investments are required.

The gas is converted to liquid at liquefaction plants (LNG export terminals.) It is then

transported in special ships that use auto-refrigeration. These LNG ocean tankers actually

use a small amount of the LNG - 3%-4% during an average voyage-to power the ships.

These tankers can carry around 135,000 cubic meters of liquid natural gas, which works out

to about 3 billion cubic feet of warm natural gas.

To give you an idea of how much gas that is, 23 ships a day could feed ALL the US demand

for natural gas. There are now roughly 375 ships in service worldwide.

The ships then go to an LNG import, or regasification, terminal where the LNG is converted

back to a gaseous state and then either stored in tanks or sent through pipelines.

The Asian market is a major destination for LNG exporters. Japan is by far the world's

largest importer of LNG, bringing in nearly 71 million tons (8.52 bcf/d)-or almost 31 percent

of all global LNG imports, according to Unit Economics.

South Korea is #2 at 34.5 million tons (4.14 bcf/d), or roughly 15 percent of global imports.

Taiwan (11.3 million tons/1.36 bcf/d) and China (9.7 million tons/1.16 bcf/d) also account for

a significant portion of LNG imports.

Asia isn't the only major LNG import market, though. Europe brings in large amounts as well.

Spain is the third largest importer of LNG with 27.3 million tons (3.28 bcf/d) coming in during

2010. The United Kingdom and France are also major importers, bringing in 13.4 million tons

(1.60 bcf/d) and 10.2 million tons (1.22 bcf/d) in 2010, respectively.

According to the U.S. Energy Information Administration (EIA), the U.K. received 55 percent

of its LNG exports from Qatar in 2009. That same year significant quantities of the

hydrocarbon entered the U.K. from Trindad and Tobago (a surprisingly robust LNG exporter

with 15.4 million tons (1.85 bcf/d) sent abroad in 2010), Algeria, Egypt and Australia.

Now that we've covered the basics of LNG, we can dive into the LNG industry in Australia to

see what the U.S. might learn from the Land Down Under.

Australia only trails Qatar, Indonesia and Malaysia in LNG exports. In 2010, Australia sent

872 billion cubic feet (about 19 million tons) abroad, which was a substantial improvement

over the 714 BCF exported in 2009, says the EIA.

[email protected] | +44 208 123 2237

15 OilVoice Magazine MAY

That's just over 8% of the world's LNG exports. By comparison, Qatar does 25% of all LNG

exports. Unit Economics states that Australia could contend with the Middle Eastern country

for top spot as early as 2016.

Not surprisingly, most of Australia's LNG exports go to the Top 4 importing countries-all in

the Far East. Japan gets about 70% of Australia's LNG exports, China gets 21%, South

Korea 5% and Taiwan 4%.

There are only two LNG liquefaction plants in Australia right now, but seven additional export

facilities are under construction, and four more are planned. Unit Economics reports that if all

of these facilities come on line and produce their projected capacities, Australia will send a

staggering 95.7 million tons (11.5 bcf/d) of natural gas abroad per year, versus the 19 million

tons (2.28 bcf/d) it is exporting now-a five-fold increase!

The capital investments-and the jobs created by it-are enormous. The Australian major

Santos Ltd., along with Petroliam Nasional Bhd., are planning on shelling out $45 billion to

create three LNG export facilities that would be able to convert 20.8 million tons of coal

seam gas into LNG each year, reports the Wall Street Journal.

Other prominent players in Australian LNG are the BG Group PLC and the Australia Pacific

LNG consortium, which is led by ConocoPhillips and Origin Energy Ltd.

'LNG is simply in high demand. and it's not just the consequence of Fukushima,' Jon Skule

Storheill, chief executive officer of Awilco LNG, told Reuters, referencing the nuclear disaster

in Japan that has prompted the country to rely more heavily on LNG. 'There's Korea, there's

Taiwan, this market is just strong. Gas is clean, it's available and it's cheap.'

America, on the other hand, has only two export terminals. The terminal in Kenai, Alaska,

which was built in the 1960s, was idled in November of last year. (At the time,

ConocoPhillips' spokeswoman Natalie Lowman told The Associated Press the plant will be

in preservation mode until spring 2012, at which time the company will re-examine the

facility.)

The other is Cheniere Energy's Sabine Pass LNG Terminal, near the border of Texas and

Louisiana. This station has 4 billion cubic feet per day of capacity.

Overall, the US exported 0.2 bcf/d of LNG in 2011, according to the EIA-a total of 71.5 bcf.

Australia almost does that in just one month. The U.S. sends most of its LNG exports to

Brazil, China, Japan and South Korea.

So How Does the US Get In On the Global LNG Action?

The LNG market is growing, and its future looks bright.

Some industry analysts predict demand for LNG globally will increase 40% in the five-year

period from 2010 to 2015. This would make the annual market for LNG roughly 300 million

tons.

[email protected] | +44 208 123 2237

16 OilVoice Magazine MAY

The U.S. has the fifth-highest amount of natural gas reserves in the world, with the EIA

putting the number at 273 trillion cubic feet. By comparison Australia has the 12th-highest

natural gas reserves, with 'only' 110 trillion cubic feet. But, as stated above, Australia was

able to ship more than 12 times as much LNG overseas in 2010 than the U.S.

The largest obstacle the U.S. faces in the LNG market is its lack of export/liquefaction

terminals. With the Kenai facility going idle, the Sabine Pass terminal is the only facility in

America even close to being able to regularly send LNG overseas. And even that could still

be a few years away.

Now what about building LNG liquefaction plants? Unit Economics says it can cost $3 billion

for each million tons of annual capacity for the entire liquefaction supply chain, which

includes production, pipelines, the port and the facility itself.

The Wall Street Journal reports there are seven additional projects seeking approval from

the Department of Energy to ship LNG to most foreign nations. If all of these projects gain

approval they could handle about 25 percent of U.S. gas production. However, the news

source reports that approval for all of the facilities is unlikely.

An additional hurdle to the LNG market in the U.S. is political opposition to sending the

energy source overseas. The American Chemistry Council has warned the U.S. government

that it 'should not undermine the availability of domestic natural gas,' but is not necessarily

against exporting the substance.

The Sierra Club is concerned that exporting more natural gas will cause companies to

increase their fracking operations. While there has been little to no evidence that fracking

itself harms the environment, a groundswell of opposition to the practice has emerged,

making investing in greater production difficult for the industry.

Still, for all the hurdles in exporting LNG, the U.S. also many opportunities.

In mid-March Japanese officials planned to meet with a delegation headed by Deputy

Energy Secretary Daniel Poneman to reportedly request LNG exports to Japan. This

appears to be a major step, as Japan had previously shied away from American LNG due to

uncertainty over whether Washington would allow it to be exported.

As mentioned, Japan's thirst for LNG is insatiable, and it will only grow stronger as the

country scales back on its use of nuclear power following last year's Fukushima Daiichi

nuclear disaster. (Before the disaster, nuclear power accounted for about 30 percent of

Japan's energy production. That's a large hole Japan will need to fill.)

Other markets that could be exploited by the U.S. are the U.K., France and Spain, all three

of which are among the largest importers of LNG in the world. While Australia does send

some LNG to these European countries, most of the U.S. competition will come from African

countries like Nigeria and Algeria, as well as Qatar.

Another positive sign for U.S. LNG exports is that they appear to have the support of Energy

[email protected] | +44 208 123 2237

17 OilVoice Magazine MAY

Secretary Steven Chu, who has stated that sending the hydrocarbon overseas would allow

America to cut into its trade deficit.

'Exporting natural gas means wealth comes into the United States,' he said, reports The Wall

Street Journal.

There is much work to be done in the U.S. LNG industry to help it catch Australia-but the

economics are powerful if it can. The gears appear to be moving in the right direction, as

both international markets are opening up, domestic production increases and LNG

liquefaction facilities gain approval and come on line.

View more quality content from

Oil & Gas Investments Bulletin

Watching World

Energy: Bottling up

Canada's oil exports

Written by Eric Watkins from Oil Diplomacy

Thursday, April 05, 2012

Canada's government, frustrated by the US decision to delay construction of Transcanada's

proposed Keystone XL pipeline, has been stepping up efforts to find alternative routes and

markets for its oil. But even these redoubled efforts are facing domestic opposition.

One proposal is Enbridge's Northern Gateway Project, which involves a twin pipeline system

running between Edmonton, Alberta, and a marine terminal at Kitimat in British Columbia.

One of the lines would export 525,000 b/d of Alberta oil sands crude to Asia-Pacific, while

the other would import 193,000 b/d of condensate.

Another proposal comes from Kinder Morgan, which is considering plans to double the

capacity of its Trans Mountain pipeline which currently delivers 300,000 b/d of crude oil and

products 1,500 kilometers from Edmonton to the Burnaby terminal on Canada's Pacific

coast.

[email protected] | +44 208 123 2237

18 OilVoice Magazine MAY

BOOST TO EXPORT POTENTIAL

These two pipelines would boost Canada's export potential, and ease concerns in Asia-

Pacific over scarce supplies. Shipping additional supplies across the Pacific would also

create supply chain diversity and reduce tensions along the main energy supply route

through the Indian Ocean to markets in South and East Asia.

The Northern Gateway project has met with considerable opposition from the public,

especially since Canada's government said it would retroactively shorten the regulatory

review to 24 months from 42 months in an effort to start exports as soon as possible.

However, Grand Chief Stewart Phillip, president of the Union of British Columbia Indian

Chiefs, said that Ottawa's shortening the review process was an 'incredibly stupid' move

which serves only 'to expedite the battle in the courts and on the land itself.'

VOLATILE MOOD

Phillip said the mood between the Canadian and British Columbia governments and the First

Nations was 'volatile' and he asserted that 'our communities will do everything they can to

stop this project.'

The First Nations made good on their word on April 1 when they surrounded a vehicle

carrying officials for a public hearing on the project, and lined the road from the airport to the

village of Bella Bella, 240 km south of the pipeline's planned tanker terminal at Kitimat.

The vehicle was carrying the three members of the National Energy Board and Canadian

Environmental Assessment Agency who later canceled the April 2 hearing, the first of four

planned for the remote region.

SURVEY SHOWS PUBLIC SPLIT

Meanwhile, according to a survey conducted by the Mustel Group, opinions concerning

increased tanker traffic transiting Vancouver Harbor were split down the middle: 44%

supported traffic of up to 300 additional oil tankers, 44% were opposed, and 12% were

undecided,

'Without having much information, people are split about 50-50,' said MP Kennedy Stewart.

'It will be a real battle for Kinder Morgan and opponents like First Nations to win over public

opinion,' he said.

'We want to see a line on a map,' said Stewart, who serves as natural resources critic for the

NDP, which is waiting to see Kinder Morgan's application before it decides to support the

project or not.

'If the expansion goes ahead, land would have to be expropriated. The route crosses 15

First Nations,' Stewart said. 'The company's right-of-way would have to be expanded to the

width of a four-lane highway,' he said.

[email protected] | +44 208 123 2237

19 OilVoice Magazine MAY

Canada's government clearly has a considerable amount of pipeline diplomacy ahead if it is

to get the public on board with the nation's energy policy. Meanwhile, much to the chagrin of

Ottawa, Canada's oil exports will simply languish.

View more quality content from

Oil Diplomacy

Obama pushes Iran

sanction to breaking

point

Written by Hanife Mehmet from Contract Jobs

Thursday, April 05, 2012

Last week, US president Barack Obama tightened the reign even further on Iran oil exports,

which may threaten to increase fuel prices even further as well as intensifying tensions

already in place. The sanctions, which were passed by congress in December of last year,

will enable the US to take further action against countries which do not comply with the

reduction of oil import intake from Iran.

Obama's decision was reportedly based on the fact that there are enough non-Iranian oil

exporters to see the world through supply and demand, despite the current shortage and

staggering fuel prices. Not only is Obama being met with criticism over the coming re-

election, but has been blamed for heightening the chance of a nuclear weapons capability in

Iran, a fact that Tehran has adamantly denied however.

Despite this, Obama stated: "Nonetheless, there currently appears to be sufficient supply of

non-Iranian oil to permit foreign countries to significantly reduce their import of Iranian oil."

In spite of the negativity surrounding the report, the US government have pointed out that

many past Iranian export buyers have significantly reduced its spend with the country and

were seeking supplies from elsewhere. Oil and gas contract jobs in other locations around

[email protected] | +44 208 123 2237

20 OilVoice Magazine MAY

the world may strive without competition from Iran or crumble under the pressure to meet

expectations in the current tough oil and gas market.

View more quality content from

Contract Jobs

Exploration: Explorers

be good...

Written by David Bamford from OilEdge

Tuesday, April 10, 2012

In the field of observation, chance favors only the prepared mind.

Louis Pasteur, lecture 1854

French biologist & bacteriologist (1822 - 1895)

Yes, ma'am, the more I practice, the luckier I get!

Gary Player, golfer, in response to a lady who said

'that was a lucky shot!'

A couple of stories...

The first comes from nearly 25 years ago when I was working in Houston and had the

opportunity to read a review of the then century-long exploration history of every play in

every basin in USA. What I noticed then was that in each example, there were no more than

two or three real 'Winners' who claimed a large, disproportionate, share of the discovered

volumes and a very large number of 'Losers' who (literally and metaphorically?!) 'made up

the numbers' and drilled a large, disproportionate, share of the dry holes. I have noticed this

in more recent campaigns; consider how for example ExxonMobil, Total and BP - the early

entrants - have dominated deep water Angola.

The second is really an example of hubris, in which I played a part. Following BP's merger

with Amoco at the end of 1998, when our exploration portfolio more or less doubled and - as

oil prices began to rise - we were able to drill some wells which had been postponed for a

couple of years, we enjoyed two years of unprecedented exploration success, drilling major

discoveries in the Gulf of Mexico, the Northern Caspian, enjoying continued success in

[email protected] | +44 208 123 2237

21 OilVoice Magazine MAY

Angola, with an overall success rate of something like 2 out of 3. To us this all seemed to

follow from really getting a grip on the exploration process - applying technology (regional 3D

seismic etc), building and ranking a prospect inventory, drilling only the 'best' - and as

'Winners' we were willing to share our wisdom with anybody who would listen (anybody who

was in the audience at the 2001 Bath meeting of the Petroleum Group of the Geological

Society might remember this!). Of course what happened next was that the wheels fell off

and in the next two years our overall exploration success rate plummeted and we drilled dry

holes where none were imagined - in Angola, West of the Shetlands, the Gulf of Mexico...

In trying to figure out what separates exploration 'Winners' from 'Losers', I have been

somewhat bemused by these experiences and so have been collecting stories about

exploration successes, especially those from relatively early in the history of our business.

I'm not going to recount them here as to do so would step across the lines of confidentiality -

owed to both companies and more especially to individuals - and some of them are truly

anecdotal. However, what these stories all seem to imply is that our predecessors were

smart...but not perhaps as smart as they thought! Indeed, the layperson might well conclude

that serendipity, good old 'luck', played a much larger role in exploration than some old

explorers would ever want to admit.

The first step in being 'good' is to answer the question...

Where shall we explore?

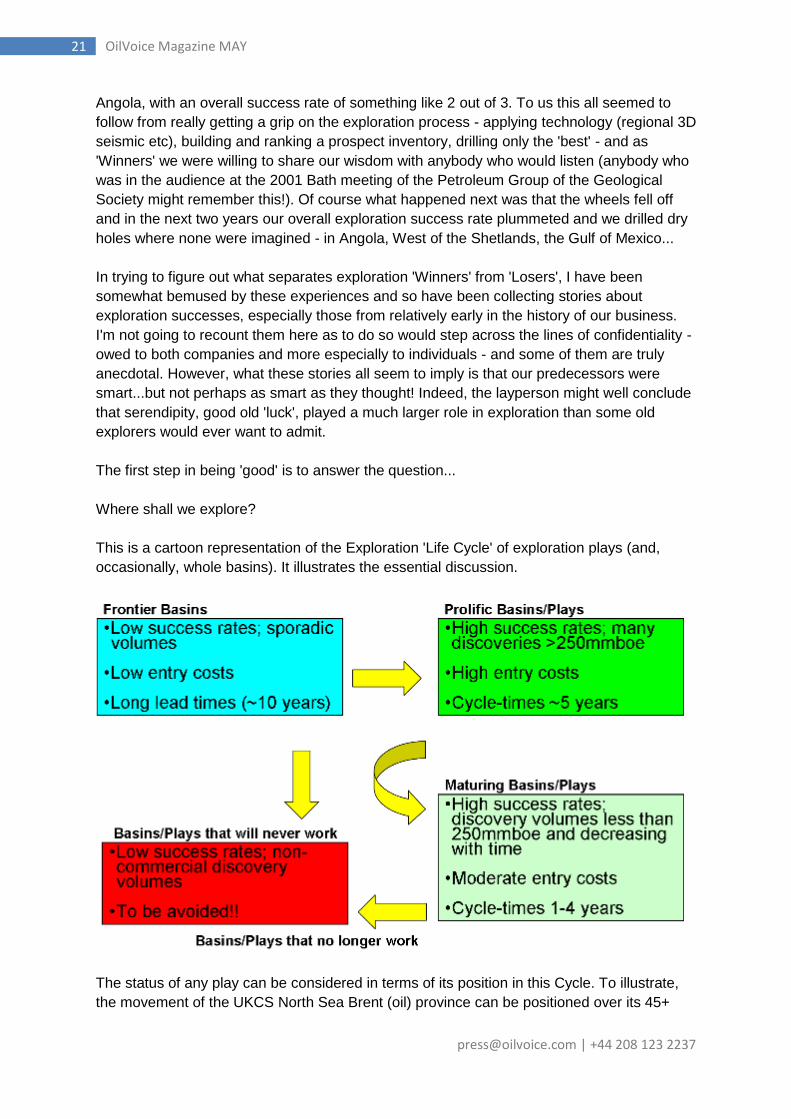

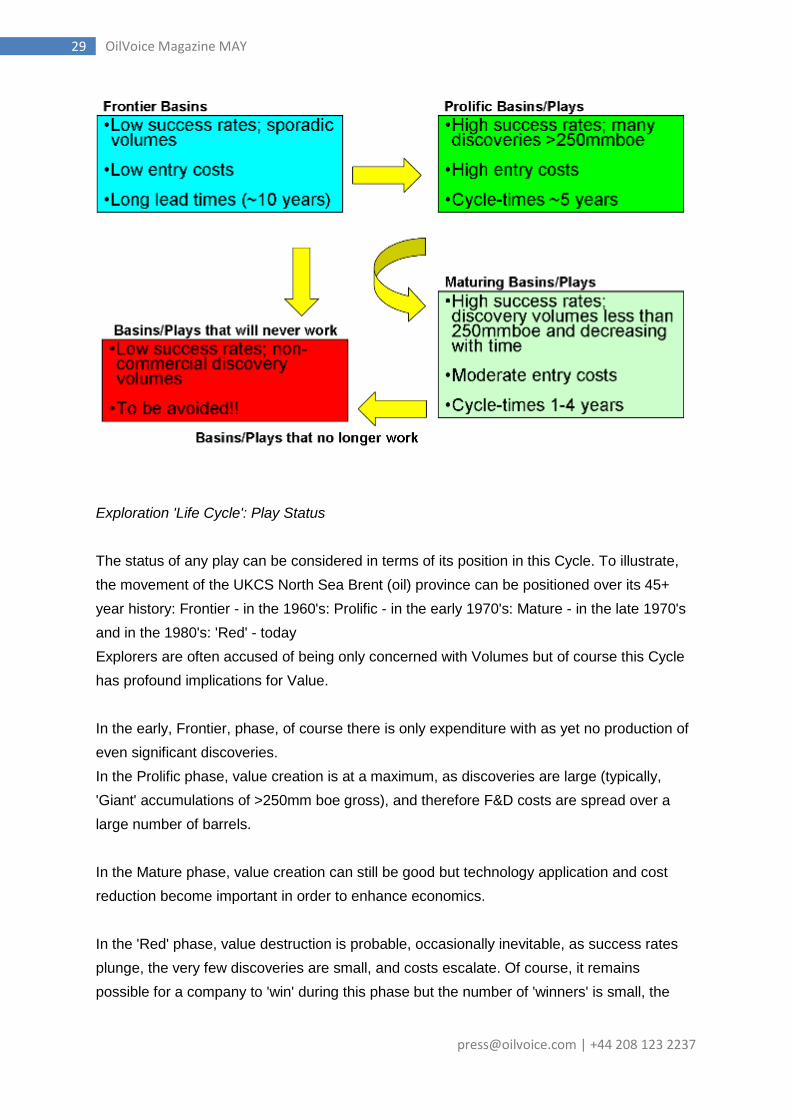

This is a cartoon representation of the Exploration 'Life Cycle' of exploration plays (and,

occasionally, whole basins). It illustrates the essential discussion.

The status of any play can be considered in terms of its position in this Cycle. To illustrate,

the movement of the UKCS North Sea Brent (oil) province can be positioned over its 45+

[email protected] | +44 208 123 2237

22 OilVoice Magazine MAY

year history: Frontier - in the 1960's: Prolific - in the early 1970's: Mature - in the late 1970's

and in the 1980's: 'Red' - today

Explorers are often accused of being only concerned with Volumes but of course this Cycle

has profound implications for Value.

In the early, Frontier, phase, of course there is only expenditure with as yet no production of

even significant discoveries.

In the Prolific phase, value creation is at a maximum, as discoveries are large (typically,

'Giant' accumulations of >250mm boe gross), and therefore F&D costs are spread over a

large number of barrels.

In the Mature phase, value creation can still be good but technology application and cost

reduction become important in order to enhance economics.

In the 'Red' phase, value destruction is probable, occasionally inevitable, as success rates

plunge, the very few discoveries are small, and costs escalate. Of course, it remains

possible for a company to 'win' during this phase but the number of 'winners' is small, the

number of 'losers' very high!

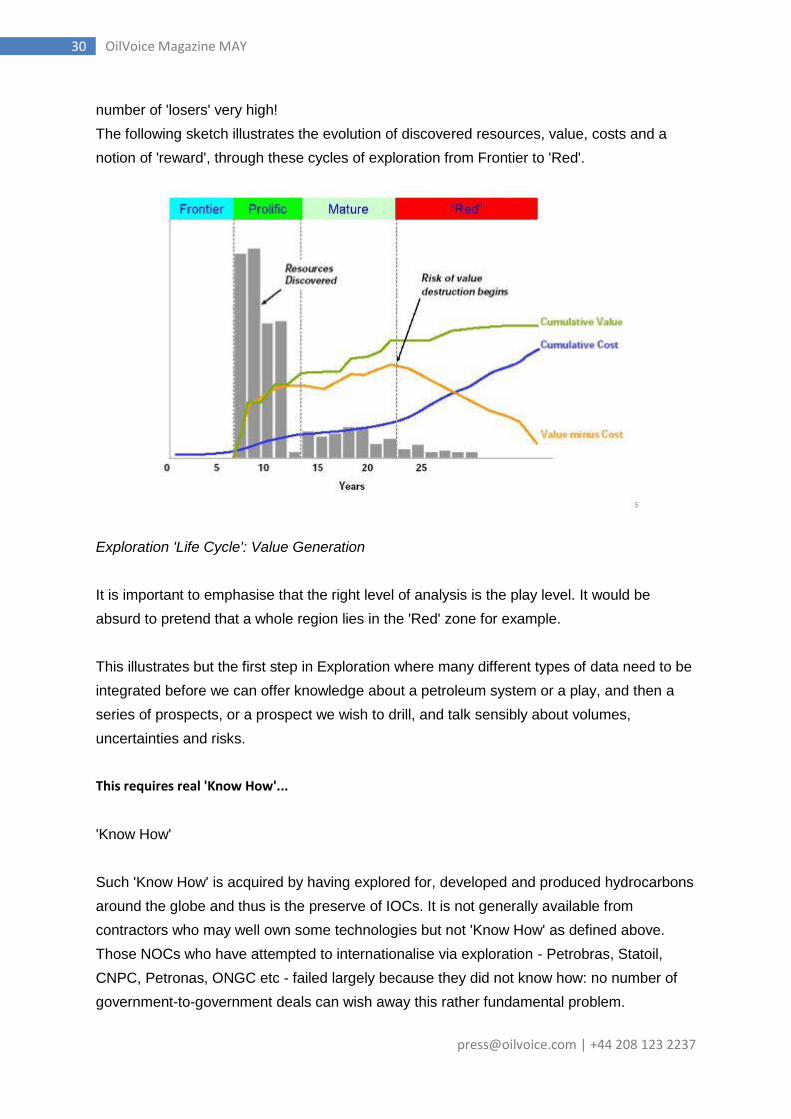

The following sketch illustrates the evolution of discovered resources, value, costs and a

notion of 'reward', through these cycles of exploration from Frontier to 'Red'.

It is important to emphasise that the right level of analysis is the play level. It would be

absurd to pretend that a whole region lies in the 'Red' zone for example.

This illustrates but the first step in Exploration where many different types of data need to be

integrated before we can offer knowledge about a petroleum system or a play, and then a

series of prospects, or a prospect we wish to drill, and talk sensibly about volumes,

uncertainties and risks.

View more quality content from

OilEdge

[email protected] | +44 208 123 2237

24 OilVoice Magazine MAY

Iran halts oil sales to

EU

Written by Raj Ladwa from Contract Jobs

Friday, April 13, 2012

The EU could be facing an oil shortage as Iran retaliates to sanctions placed on them by the

US and EU.

As the fallout continues from Iranian nuclear activity, Tehran has continued to implement its

own sanctions in the face of EU and US sanctions banning the import of Iranian Oil.

Iran has already hit Britain and France with a pre-emptive strike, an attempt to stop them

importing Iranian oil before they can find alternative suppliers.

This week has seen a few more names being added to the list as Iran continues its

retaliation. Iranian President, Mahmoud Ahmadinejad has placed embargoes on Greece,

Spain and Germany according to an Iranian television network with Italy also set to be

placed on the list. However, there are also suggestions Mr Ahmadinejad is considering

cutting oil supplies to over a hundred European countries.

The latest reports may spur European countries to act faster in reducing their reliance on

Iranian oil as many countries risk being cut off from the US financial system.

A report by the International Energy Agency (IEA) has predicted oil production in Iran could

fall by up to a million barrels per day by July as nations restrict Iranian imports and find

alternative supplies to avoid the risk of being hit US sanctions.

However, as the oil flow from one of the world's largest oil producers stems, this could see

oil prices rocket as Europe looks for alternative suppliers.

Talks between Iran and the UN Security Council are set to reconvene in Istanbul regarding

Iran's nuclear activity. Any positive results could lead to sanctions against Iran being eased.

View more quality content from

Contract Jobs

[email protected] | +44 208 123 2237

25 OilVoice Magazine MAY

The big 6 challenges

for an oil and gas

translator

Written by Camilo Muñoz from Translation Source

Monday, April 23, 2012

As a multi-billion dollar industry, the oil and gas sector operates on a global scale. It's a big

business. The implications for an oil and gas translator to make the wrong decision when it

comes to localizing the content are usually magnified.

When there are so many technical translators out there, how do you make sure your oil and

gas translation is up to scratch? We have compiled the 5 main challenges of oil and gas

translation:

1. Timeline Requirements

The energy industry as a whole is extremely time-sensitive. It's never acceptable to miss a

deadline for an oil and gas translator. Having an idle rig for one day alone, for instance, can

cost an oil company $650,000 and that doesn't include the millions lost by not producing oil.

Three minutes late could mean $3 million lost.

2. Industry Specific Vocabulary

How many of these expressions do you know?

a) PSA [1]

b) Gone to Water

c) Gunk squeeze

d) Sour Corrosion

e) Gas Cut mud

f) Sidetrack

g) Pipe ram preventer

These are just a few examples of technical terms that an oil and gas translator may

encounter and that may need to communicate succinctly and effectively in another language.

Most linguists, even if professionally trained, won't know the definitions of these words

unless they have industry-specific knowledge. Extensive knowledge of highly technical and

specific terms is vital in order to provide accurate high-quality translations.

3. 'Translating' regulations

[email protected] | +44 208 123 2237

26 OilVoice Magazine MAY

Each nation has specific codes and standards that must be adhered to. Russia, for example,

has the world's strictest regulations on offshore oil production and has introduced new

regulations on how foreign assistance missions are to approach Russian authorities when

sending in expertise and equipment. Oil and gas translators are responsible for being aware

of these and ensuring the translations they produce comply with them.

Failing to budget for good translations that comply with the requirements of target countries

can lead to them being rejected (and having to be retranslated). Why not get it right first

time?

4. Keeping up with industry social and environmental requirements

Like many industries, the oil and gas sector is under increasing pressure to improve their

social and environmental impact. The Environmental Impact Assessment (EIA) and Social

Impact Assessment (SIA) are used to assess the sustainability of their approach. The

requirements for these open to public review and are imposed on a national level by treaties,

national laws, oil and gas industry guidelines, and are imposed as conditions of lending and

assistance by international financial organizations (e.g. the World Bank). It is a lengthy

procedure that demands a good knowledge of legal and financial terminology. As a result of

this constant transnational flow of documents translators should also be familiar with the

procedures and documents involved that will be referred to in the process. They should be

able to update and amend documents efficiently so they can be approved.

5. DTP requirements

Due to the highly technical nature of many oil and gas translations, specialized desktop

publishing tools such as AutoCAD may be required in order to incorporate technical

diagrams. Oil and gas translators must know how to manipulate annotations using these

tools. It is easy to leave things out without review.

6. Project Specific Multilingual Communication

To date there have been US$ 53.43 billion invested in the pre-salt, with an overall $400

billion expected over the next ten years, including foreign investment from Petrobras

partners British Gas and from investment from Chile. There are currently 688 sources of

foreign investment in the pre salt project, a figure which not only demonstrates the demand

for multi-lingual translations but also shows how, when centered on one project, a

streamlined approach is vital to insure that even though they are written in different

languages they are 'talking the same language' using the same terminology.

Do you consider the impact of your translation choices when you are choosing a translation

provider?

[1]

a) Pressure Setting Assembly - A tool used to set permanent tools on wireline using

explosive force

b) Describes a well in which water production is increasing

[email protected] | +44 208 123 2237

27 OilVoice Magazine MAY

c) A bentonite and diesel oil mixture that is pumped down the drill pipe and into the annulus

to mix with drilling mud.

d) Embrittlement and subsequent wearing away of metal caused by contact of the metal with

hydrogen sulfide.

e) A drilling mud that contains entrained formation gas, giving the mud a characteristically

fluffy texture.

f) To use a whipstock, turbodrill, or other mud motor to drill around broken drill pipe or casing

that has become lodged permanently in the hole.

g) A blowout preventer that uses pipe rams as the closing elements.

View more quality content from

Translation Source

Exploration: Explorers

be good or be lucky...

Written by David Bamford from OilEdge

Monday, April 23, 2012

In the field of observation, chance favors only the prepared mind.

Louis Pasteur, lecture 1854

French biologist & bacteriologist (1822 - 1895)

Yes, ma'am, the more I practice, the luckier I get!

Gary Player, golfer, in response to a lady who said

'that was a lucky shot!'

A couple of stories…..

The first comes from nearly twentyfive years ago when I was working in Houston and had

the opportunity to read a review of the then century-long exploration history of every play in

every basin in USA. What I noticed then was that in each example, there were no more than

two or three real 'Winners' who claimed a large, disproportionate, share of the discovered

[email protected] | +44 208 123 2237

28 OilVoice Magazine MAY

volumes and a very large number of 'Losers' who (literally and metaphorically?!) 'made up

the numbers' and drilled a large, disproportionate, share of the dry holes. I have noticed this

in more recent campaigns; consider how for example ExxonMobil, Total and BP - the early

entrants - have dominated deep water Angola.

The second is really an example of hubris, in which I played a part. Following BP's merger

with Amoco at the end of 1998, when our exploration portfolio more or less doubled and - as

oil prices began to rise - we were able to drill some wells which had been postponed for a

couple of years, we enjoyed two years of unprecedented exploration success, drilling major

discoveries in the Gulf of Mexico, the Northern Caspian, enjoying continued success in

Angola, with an overall success rate of something like 2 out of 3. To us this all seemed to

follow from really getting a grip on the exploration process - applying technology (regional 3D

seismic etc), building and ranking a prospect inventory, drilling only the 'best' - and as

'Winners' we were willing to share our wisdom with anybody who would listen (anybody who

was in the audience at the 2001 Bath meeting of the Petroleum Group of the Geological

Society might remember this!). Of course what happened next was that the wheels fell off

and in the next two years our overall exploration success rate plummeted and we drilled dry

holes where none were imagined - in Angola, West of the Shetlands, the Gulf of

Mexico………

In trying to figure out what separates exploration 'Winners' from 'Losers', I have been

somewhat bemused by these experiences and so have been collecting stories about

exploration successes, especially those from relatively early in the history of our business.

I'm not going to recount them here as to do so would step across the lines of confidentiality -

owed to both companies and more especially to individuals - and some of them are truly

anecdotal. However, what these stories all seem to imply is that our predecessors were

smart….but not perhaps as smart as they thought! Indeed, the layperson might well

conclude that serendipity, good old 'luck', played a much larger role in exploration than some

old explorers would ever want to admit.

The first step in being 'good' is to answer the question...

Where shall we explore?

This is a cartoon representation of the Exploration 'Life Cycle' of exploration plays (and,

occasionally, whole basins). It illustrates the essential discussion.

[email protected] | +44 208 123 2237

29 OilVoice Magazine MAY

Exploration 'Life Cycle': Play Status

The status of any play can be considered in terms of its position in this Cycle. To illustrate,

the movement of the UKCS North Sea Brent (oil) province can be positioned over its 45+

year history: Frontier - in the 1960's: Prolific - in the early 1970's: Mature - in the late 1970's

and in the 1980's: 'Red' - today

Explorers are often accused of being only concerned with Volumes but of course this Cycle

has profound implications for Value.

In the early, Frontier, phase, of course there is only expenditure with as yet no production of

even significant discoveries.

In the Prolific phase, value creation is at a maximum, as discoveries are large (typically,

'Giant' accumulations of >250mm boe gross), and therefore F&D costs are spread over a

large number of barrels.

In the Mature phase, value creation can still be good but technology application and cost

reduction become important in order to enhance economics.

In the 'Red' phase, value destruction is probable, occasionally inevitable, as success rates

plunge, the very few discoveries are small, and costs escalate. Of course, it remains

possible for a company to 'win' during this phase but the number of 'winners' is small, the

[email protected] | +44 208 123 2237

30 OilVoice Magazine MAY

number of 'losers' very high!

The following sketch illustrates the evolution of discovered resources, value, costs and a

notion of 'reward', through these cycles of exploration from Frontier to 'Red'.

Exploration 'Life Cycle': Value Generation

It is important to emphasise that the right level of analysis is the play level. It would be

absurd to pretend that a whole region lies in the 'Red' zone for example.

This illustrates but the first step in Exploration where many different types of data need to be

integrated before we can offer knowledge about a petroleum system or a play, and then a

series of prospects, or a prospect we wish to drill, and talk sensibly about volumes,

uncertainties and risks.

This requires real 'Know How'...

'Know How'

Such 'Know How' is acquired by having explored for, developed and produced hydrocarbons

around the globe and thus is the preserve of IOCs. It is not generally available from

contractors who may well own some technologies but not 'Know How' as defined above.

Those NOCs who have attempted to internationalise via exploration - Petrobras, Statoil,

CNPC, Petronas, ONGC etc - failed largely because they did not know how: no number of

government-to-government deals can wish away this rather fundamental problem.

[email protected] | +44 208 123 2237

31 OilVoice Magazine MAY

Another way of saying all this is that Exploration is knowledge-based, that is, dependent on

people.

The 'Winners' in exploration will guard their 'Know How' carefully, cosseting the staff who

embody this knowledge. They will pursue long lists of potentially hydrocarbon bearing basins

and plays (and, similarly, prospects) in the manner described above. They will be 'good

explorers'.

The 'Losers' will depend on 'luck', or believe they can. I'm sure there are many ways to

lose….but here are just three:

1. For a Major, with plenty of staff and 'Know How', nonetheless rely on an 'Exploration

Supremo' who selects two or three opportunities and says 'one of these will wok!

2. Be a small company, with no/few staff and little 'Know How', and rely on one play, or

a small number of prospects, 'working'.

3. Be an investor in several small companies (all with executive packages, corporate

jets etc to pay for) in the belief that a 'portfolio effect' will somehow get "luck" on your

side!

View more quality content from

OilEdge

[email protected] | +44 208 123 2237

32 OilVoice Magazine MAY

Greenhouse Gas

Emissions: In Situ oil

sands producers drive

efficiencies, but

integrated operations

take a step back

Written by Chris Wilson from Evaluate Energy

Tuesday, April 24, 2012

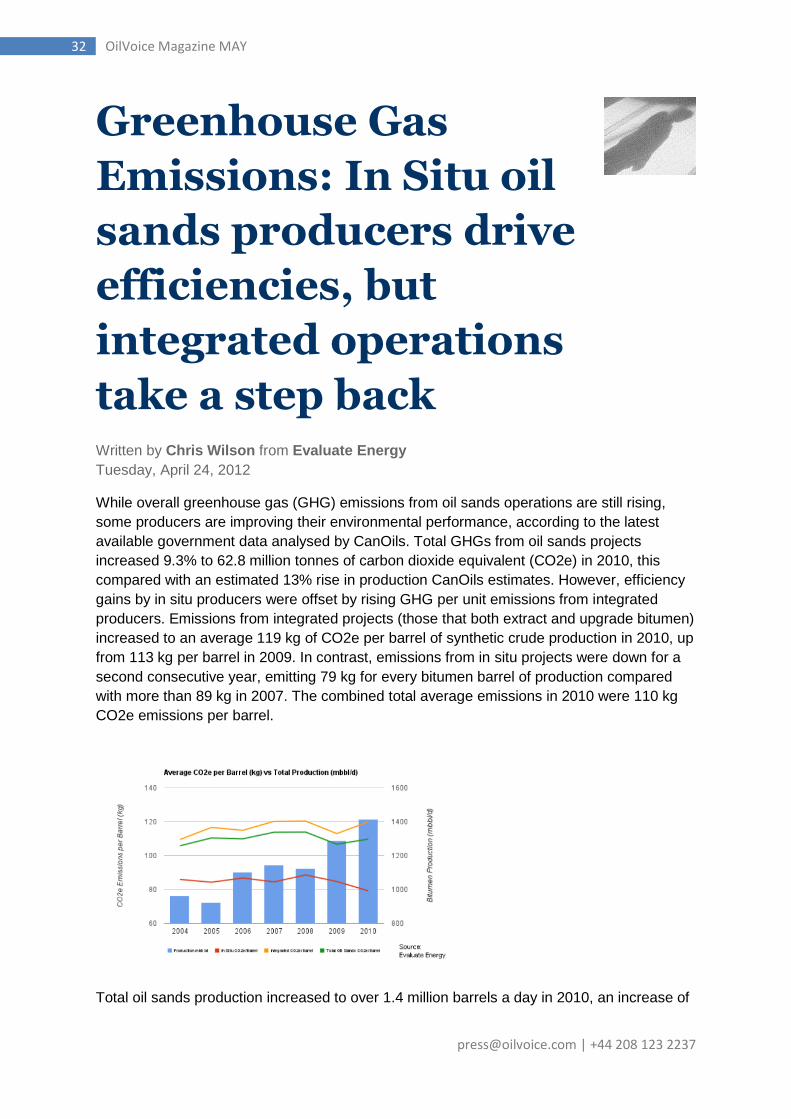

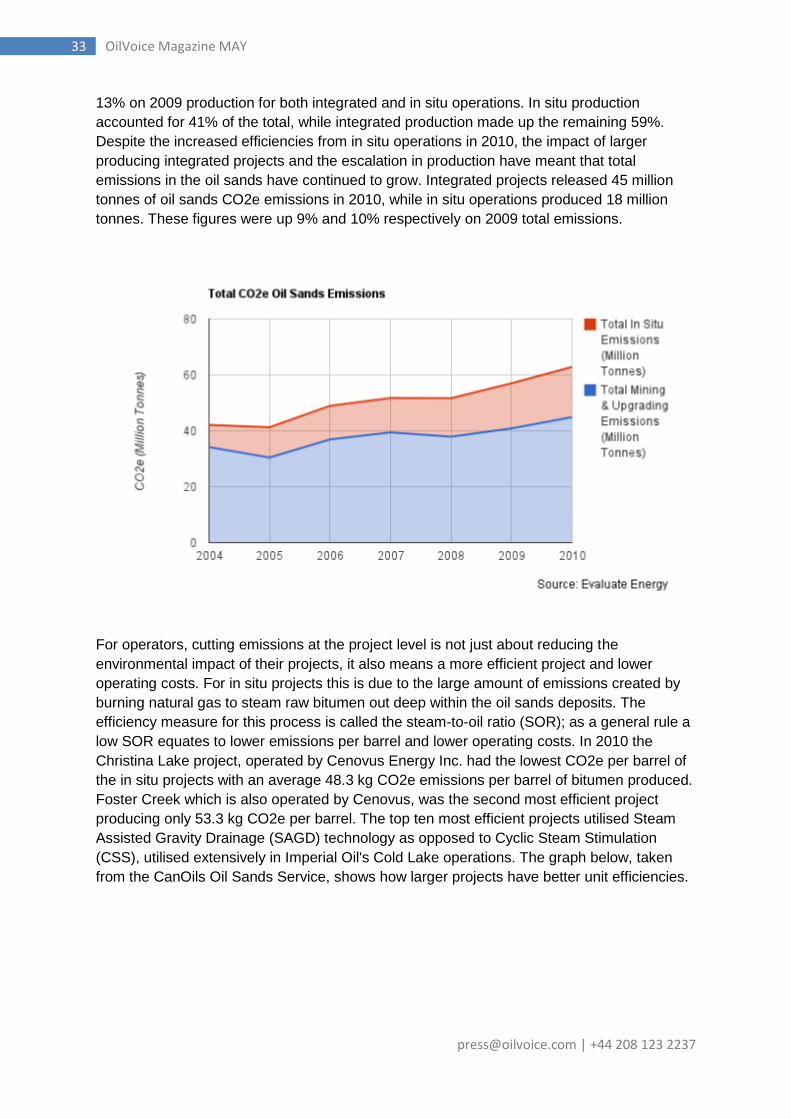

While overall greenhouse gas (GHG) emissions from oil sands operations are still rising,

some producers are improving their environmental performance, according to the latest

available government data analysed by CanOils. Total GHGs from oil sands projects

increased 9.3% to 62.8 million tonnes of carbon dioxide equivalent (CO2e) in 2010, this

compared with an estimated 13% rise in production CanOils estimates. However, efficiency

gains by in situ producers were offset by rising GHG per unit emissions from integrated

producers. Emissions from integrated projects (those that both extract and upgrade bitumen)

increased to an average 119 kg of CO2e per barrel of synthetic crude production in 2010, up

from 113 kg per barrel in 2009. In contrast, emissions from in situ projects were down for a

second consecutive year, emitting 79 kg for every bitumen barrel of production compared

with more than 89 kg in 2007. The combined total average emissions in 2010 were 110 kg

CO2e emissions per barrel.

Total oil sands production increased to over 1.4 million barrels a day in 2010, an increase of

[email protected] | +44 208 123 2237

33 OilVoice Magazine MAY

13% on 2009 production for both integrated and in situ operations. In situ production

accounted for 41% of the total, while integrated production made up the remaining 59%.

Despite the increased efficiencies from in situ operations in 2010, the impact of larger

producing integrated projects and the escalation in production have meant that total

emissions in the oil sands have continued to grow. Integrated projects released 45 million

tonnes of oil sands CO2e emissions in 2010, while in situ operations produced 18 million

tonnes. These figures were up 9% and 10% respectively on 2009 total emissions.

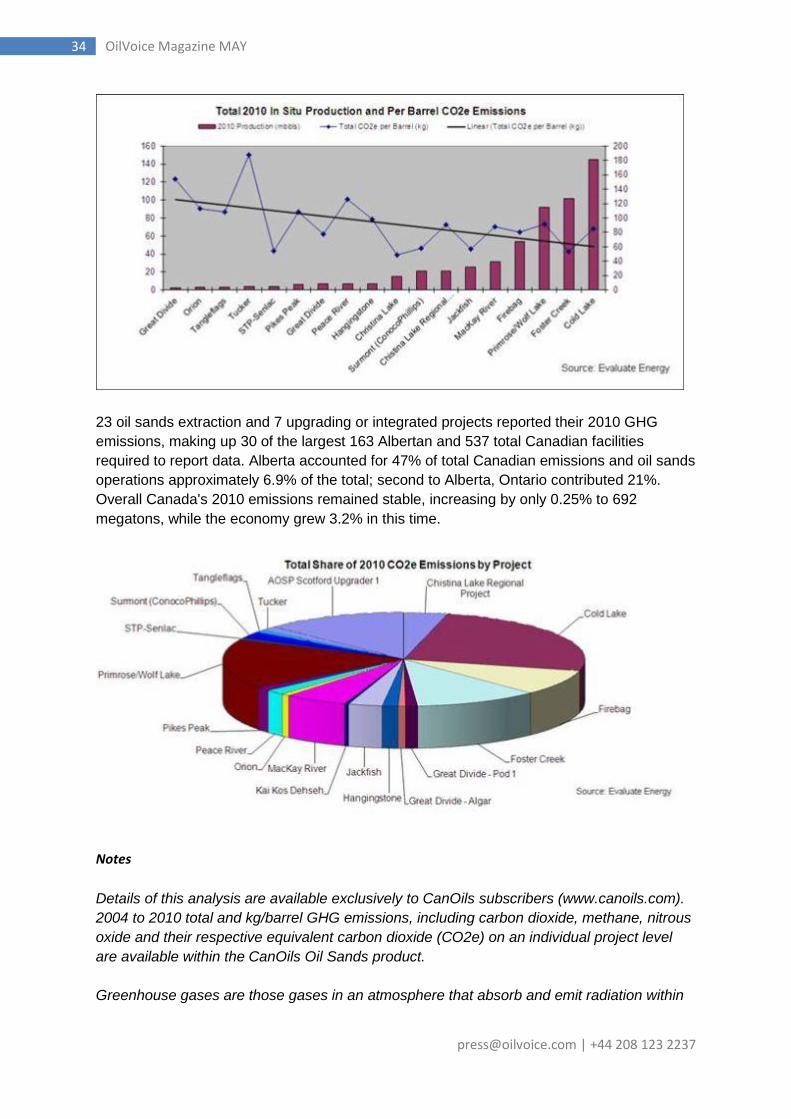

For operators, cutting emissions at the project level is not just about reducing the

environmental impact of their projects, it also means a more efficient project and lower

operating costs. For in situ projects this is due to the large amount of emissions created by

burning natural gas to steam raw bitumen out deep within the oil sands deposits. The

efficiency measure for this process is called the steam-to-oil ratio (SOR); as a general rule a

low SOR equates to lower emissions per barrel and lower operating costs. In 2010 the

Christina Lake project, operated by Cenovus Energy Inc. had the lowest CO2e per barrel of

the in situ projects with an average 48.3 kg CO2e emissions per barrel of bitumen produced.

Foster Creek which is also operated by Cenovus, was the second most efficient project

producing only 53.3 kg CO2e per barrel. The top ten most efficient projects utilised Steam

Assisted Gravity Drainage (SAGD) technology as opposed to Cyclic Steam Stimulation

(CSS), utilised extensively in Imperial Oil's Cold Lake operations. The graph below, taken

from the CanOils Oil Sands Service, shows how larger projects have better unit efficiencies.

[email protected] | +44 208 123 2237

34 OilVoice Magazine MAY

23 oil sands extraction and 7 upgrading or integrated projects reported their 2010 GHG

emissions, making up 30 of the largest 163 Albertan and 537 total Canadian facilities

required to report data. Alberta accounted for 47% of total Canadian emissions and oil sands

operations approximately 6.9% of the total; second to Alberta, Ontario contributed 21%.

Overall Canada's 2010 emissions remained stable, increasing by only 0.25% to 692

megatons, while the economy grew 3.2% in this time.

Notes

Details of this analysis are available exclusively to CanOils subscribers (www.canoils.com).

2004 to 2010 total and kg/barrel GHG emissions, including carbon dioxide, methane, nitrous

oxide and their respective equivalent carbon dioxide (CO2e) on an individual project level

are available within the CanOils Oil Sands product.

Greenhouse gases are those gases in an atmosphere that absorb and emit radiation within

[email protected] | +44 208 123 2237

35 OilVoice Magazine MAY

the thermal infrared range. The main greenhouse gases in the Earth's atmosphere are water

vapour, carbon dioxide, methane, nitrous oxide and ozone. CanOils tracks carbon dioxide,

methane, nitrous oxide and their respective equivalent carbon dioxide (CO2e) release per

barrel and by total for every oil sands project. In the CanOils database, methane, nitrous

oxide and ozone emissions are converted to CO2 equivalent based on the US

Environmental Protection Agency Global Warming Potential (GWP) factors under which CO2

has a GWP of 1, methane a GWP of 21 and Nitrous oxide a GWP of 310.

Syncrude is raw produced bitumen that has been upgraded to synthetic crude oil.

Air pollutant emissions data were compiled in collaboration with provincial, territorial and

regional environmental agencies by Environment Canada, National Pollutant Release

Inventory (NPRI). Facilities report their own pollutant release and transfer data to

Environment Canada. Only facilities emitting the equivalent of 50,000 tonnes are reported

and therefore pilot projects are not included. Total oil sands emissions data refers to total

project coverage in the CanOils database.

There are two main ways of extracting oil sands - mining, in which the bitumen is located

within 80-100 meters of the surface and in situ whereby the bitumen is located in deeper

reservoirs and is produced using steam injection or other enhanced recovery methods.

View more quality content from

Evaluate Energy

OilEdge: Know your

customers

Written by David Bamford from OilEdge

Wednesday, April 25, 2012

Perhaps for an oil field service company knowing who your suppliers and customers are - where

you sit in the supply chain - is relatively easy.

For example, a seismic contractor supply a proprietary 3D seismic survey over an oil field sits

between the manufacturer of cables, airguns, recording equipment and the seismic operations

specialists of the client oil company.

[email protected] | +44 208 123 2237

36 OilVoice Magazine MAY

The same specialists sit in the supply chain between the seismic contractor and the geoscientists in

the field's reservoir management team.

Less obviously, the reservoir management's team has the asset manager as a customer and,

ultimately, the oil company that owns the asset has the host government as a customer.

Often as managers with responsibility for people, we only consider ourselves responsible for

the people in our team. The truth is, to make the organisation work effectively we need to

consider relationships more widely.

Regularly we focus on the areas for which we are responsible, forgetting the 'bigger picture'

and how our 'bit' fits in with other parts in order to make a complete whole. I will refer to

'context' throughout this article. For me the context is the end goal which is the delivery of

something to a consumer or customer.

It is concerning that many people do not look at the ultimate relationship; that with an end

consumer or user, a customer. It is also concerning that not many people in an organisation

look upon others within the organisation as potential customers. The latter, where identified

are referred to as 'Internal Customers'. Internal customer is not a new concept but is one

which does not seem to have taken on a great significance.

There is often a difference between the way we treat colleagues and customers, so the

attitude of thinking of internal customer can improve the relationship or the 'service' we

provide to those internal customers.

External Customers

In some circumstances it is easy to identify external customers and some functions in the

organisation have a direct relationship or interface with them. Others are more remote and

therefore perhaps more inclined to be inward focussed. One concept I was introduced to

was 'if you are not serving the customer, serve someone who is'. I have interpreted this and

include it in my big picture awareness.

I believe this is important both in operational, practical terms and in the way in which we

engage our team. It is true that some may not be truly interested, but having a context will

often provide us as managers with a great tool to use either as a managerial or controlling

mechanism.

With exploration for example it is easy to see that as an end in itself, but in the context of the

various customers (road users, aircraft, shipping, plastics manufacturers, energy suppliers,

oilfield service comapnies, even host governments, for example) we can see that it has a

real purpose, use and value and needs to be controlled (especially cost) effectively as

ultimately we are all 'users' or consumers.

In production, again, it is again an end in itself but again the context of the customers and

their use of the oil or gas produced will again be useful as a real purpose.

[email protected] | +44 208 123 2237

37 OilVoice Magazine MAY

For some the end user or customer may be too remote and, although it could be a useful

context, something more immediate is needed.

Internal Customer

Many organisations have adopted an approach where they have the notion of customer

within the organisation rather than merely colleagues. This is far from universal but where it

really and truly exists the relationships within the organisation are different from where it is

the view that internal folk are colleagues alone.

We may be respectful of colleagues but somehow the notion of a customer prompts greater

accuracy, timeliness or quality in our outputs.

Outputs are perhaps the result of a process, 'what we do'. Possibly a customer approach is

one that makes us think more in terms of outcomes….not just the result of a process but the

effect it has too.

This becomes more important in the larger picture as well as the immediate customer

relationship when we consider how our outputs and outcomes will be used by others. What

this implies is that as a manager of a team we need to be right on top of the 'how' our

outcomes will be utilised by our customer.

The first thing we need to be aware of is who is our customer? Identifying the customer has

to be an initial activity so that we have an idea of where our outcomes will go. Next we need

to understand how the customer will use these outcomes in their part of the journey towards

the ultimate customer.

This further implies that we as managers need to have the bigger picture in mind as we think

of the ultimate or end user. We can share as much or as little of this with the team as is

appropriate. The ultimate goal is not a secret and in my view should be shared anyway;

some team members may respond to this more than others which is the nature of human

beings and where the art of management comes in….how well do we know the individuals in

our team and what motivates and excites or even interests them?

The relationships

This may be the part that needs work as we build and manage relationships with our internal

customers. This is where openness and open questions are of fundamental importance. It

may also be a time for us to have a thick skin and a degree of realism or practicality in our

response to the answers we receive.

Again, knowing the personality we are dealing with and their angle or perspective on life.

Some people may have greater and unfair expectations of our outcomes than we can or

maybe should provide. This is where a dose of reality is important and gradually the internal

customer becomes educated in how we will respond and what we can fairly provide.

Nonetheless it is valuable to ask of our internal customer what they expect and what they

feel or think about the outcomes we provide them with at present.

[email protected] | +44 208 123 2237

38 OilVoice Magazine MAY

Generally organisations are structured in such a way that we have separate departments

and functions which collectively produce the ultimate outcome for the end user. This has to

be the ultimate purpose of any organisation. What then usually happens is that organisations

set up processes which deliver that ultimate outcome. Often organisations expect individual

functions to operate their processes effectively and efficiently and to 'own' or control them. I

have seen examples where the bigger picture is lost altogether and individual departments

have wonderfully efficient processes but they do not fit in with the 'up stream' or 'down

stream' processes of other functions.

In discussing or asking what other functions require of us it is important to keep the overall

context in mind. We need to have that picture in our own mind and there is no harm in

asking a fellow customer centric colleague (internal customer) how their process works

towards the ultimate customer goal. We may consider this as holding both our and their feet

to the flame and keeping everything in context.

The approach

Where the concept of internal customer is truly embedded the approach is expected and is a

normal conversation. It may be that internal customer surveys are conducted that prompt the

conversations or it may be that the conversations happen anyway.

Where this is not the norm, it is still possible to make the approach but at first it may need to

be more tentative. Again the value of knowing the person you are dealing with will help. You

don't need to be bosom buddies but understanding what makes them 'tick' and likely

responses will be advantageous.

When one suggests tentative approaches this does not mean being on the back foot. It is

quite possible to be assertive in style whilst seeking the information in a tentative or

exploratory way. Possibly exploratory is a better word to use.

'X, what I'd like to explore with you is the value and quality of our outputs and outcomes that

you then use as part of your inputs.'

We may end up with some ideas along the lines of 'this is what we need less of, please keep

doing this and we need more of that'. Some you can respond to, some may be unrealistic

and some may be unfair expectations. However, having sought the feedback you do need to

do something with it and to 'report' back to the internal customer on what you are doing and

the changes you may be making.

I have seen that treating a colleague as a customer improves focus on outcomes rather than

focus on my own process and the nature of the conversation being outcome led also

improves the quality and the relationship.

Suppliers (both internal and external)

If we adopt a customer centric view there is benefit in creating good relationships with

suppliers too. Being proactive may be advantageous. However we probably want to avoid

[email protected] | +44 208 123 2237

39 OilVoice Magazine MAY

being a whinging moaner: 'This is not right, that's wrong' and so on. Starting from a position

of positives helps and allows us to then point to the things that may be improved.

It is, as with customers, to form good, open, trusting relationships. If we are seen as a

moaner then we are unlikely to get any response, but if we have reasonable expectations we

can often realise a great improvement in the service we are provided by both internal and

external suppliers. This may seem common sense but sadly it does not appear to be that

common.

Too often I have witnessed a dissatisfied customer ranting and raving at the supplier or

conversely meekly accepting poor quality outcomes or service. Neither of these is a

satisfactory state and the importance of establishing a decent relationship is again

emphasised. It may be that as individuals we need help in relating and possibly in being

assertive (as opposed to being aggressive).

The important elements are to have an idea of the bigger picture and know what you

contribute as a team. Then looking at customers and suppliers and ensuring that your

outcomes and outputs are appropriate in the context. Relationships are so important in

making this work and it probably resides with us a managers although there is no harm in

fostering positive relationships between teams. My concern here would be that as manager I

would need to own the 'official' relationship with other teams, or all sorts of promises and

expectations may be created!

Emotional intelligence

I will cover this in more detail in a later article but for now let's say that awareness of others

and how you can manage yourself to relate to that person and their behaviours will stand

you in good stead. The basis of emotional intelligence is precisely that awareness and then

responding appropriately.

Summary and activity

It is worth considering: who are your suppliers? Who are your customers? Which of your

suppliers causes you the most problems? What are you going to do about it? Few of us are

without some form of supplier and customer and not every one of them is perfect. It is worth

considering and responding appropriately.

View more quality content from

OilEdge

[email protected] | +44 208 123 2237

40 OilVoice Magazine MAY

Review: Argentina -

Under the spotlight

Written by David Bamford from OilEdge

Thursday, April 26, 2012

It is hard to avoid stories about the Argentine oil industry at present. In light of three key issues,

namely:

1) the battle for control of YPF

2) the ongoing search for oil in the Falklands; and

3) a series of downgrades by Moody's for firms operating in the country, Argentina is the talk of

the global oil industry

- but for all the wrong reasons.

For some time now Argentina has been regarded as something of an underperformer in the

oil sector - especially among emerging market nations - and this is something the incumbent

administration of President Cristina Kirchner is acutely aware of.

1. Eager to turn the tide, the Argentine government has made moves to expand state

control over the oil sector in recent weeks, and a rumoured nationalisation of YPF

(the former national oil and gas company, in which Spanish major Repsol now has a