oil prices and opec

TRANSCRIPT

OPEC and oil pricesHistory, strategy and outlook

JOHN KEMP

REUTERS

8 June 2017

Three key issues for OPEC and other oil producers

Does OPEC have any long-term control over oil prices?

How should OPEC respond to threat from U.S. shale?

What does that mean for the price outlook in 2017/18?

OPEC’s objectives as outlined in its founding statuteAgreed at Caracas in January 1961

Coordination of members’ petroleum policies

Stabilisation of international oil markets

Elimination of harmful and unnecessary fluctuations

Securing a steady income for producers

Efficient, regular and economic supply to consumers

Fair return on capital for investors in the oil industry

OPEC’s priority has always been revenue maximisationBut specific focus has shifted over time

Focus on taxes and royalties 1940s-1960s

Focus on official selling price 1960s-1980s

Focus on ownership of reserves 1960s-1970s

Focus on controlling production 1980s-2010s

Prices have been higher but more volatile in OPEC eraOPEC has not managed to tame the oil industry cycle

Real oil prices have been very volatile (1)Stabilisation has remained elusive

Real oil prices have been very volatile (2)Stabilisation has remained elusive

OPEC has limited impact on oil pricesBig changes in oil market have come from other sources

Supply-side developments

North Sea

Alaska

China

Soviet Union

Deepwater

Megaprojects

Shale

Demand-side developments

Fuel switching

Fuel economy

East Asian Tigers

China

(Electric vehicles?)

OPEC cannot successfully monopolise/cartelise marketMarket share not high enough and cannot prevent new entrants

OPEC is more a price-taker than a price-makerOPEC decisions have marginal impact on evolution of price cycle

OPEC had no identifiable impact on price trend in 2017Prices might have been lower w/o cuts, but so might shale drilling

Oil market showed signs of rebalancing pre-OPEC accordFlat prices and calendar spreads both rising since early 2016

OPEC’s stated ambition: to accelerate rebalancing trendContango has continued to narrow, but no backwardation yet

Putting OPEC in perspective

OPEC has had some limited impact on prices in the very short term

OPEC has little or no impact on prices in the medium and long run

OPEC has not been able to tame the inherent volatility of oil market

OPEC has not been able to prevent market entry

OPEC is more a price-taker than a price-maker

OPEC adapts to rather than shapes market environment

U.S. shale productionBoom, bust and boom again

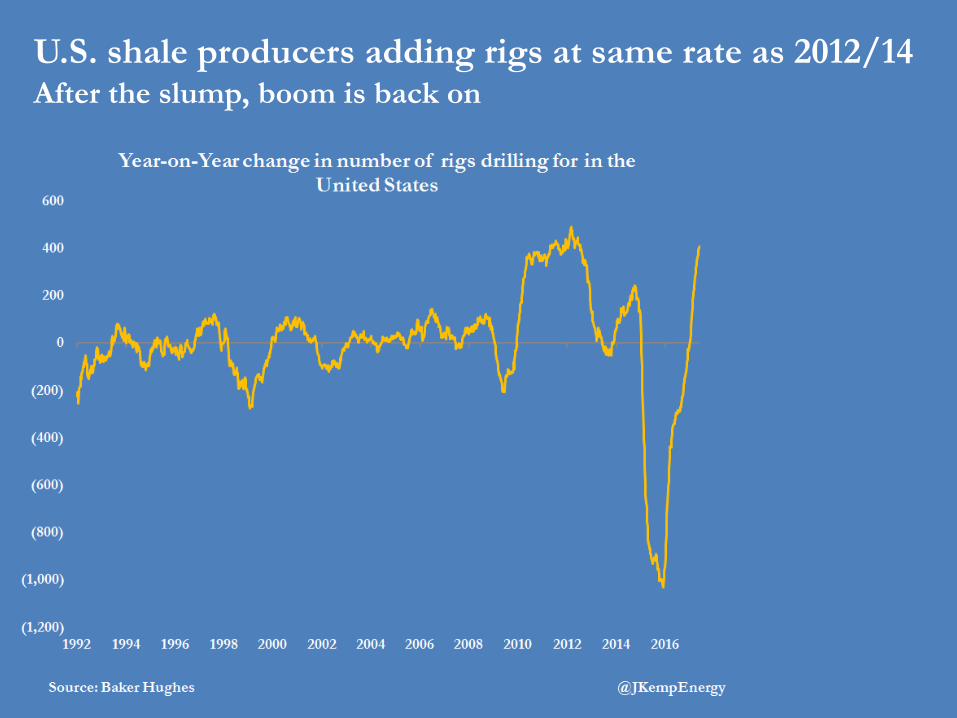

U.S. shale producers adding rigs at same rate as 2012/14After the slump, boom is back on

Rig count follows WTI price with a lag of 15-20 weeks

Current rig count reflects WTI prices in FebruaryPrices have since stalled and fallen

U.S. oil production is rising again (mostly GoM so far)Shale production tends to lag rig count by 6 months

U.S. oil production forecast to rise +460,000 b/d in 2017And another +680,000 b/d in 2018

U.S. oil production forecasts revised upwards repeatedlySurprising speed and strength of drilling boom

U.S. onshore drilling costs have stayed low but set to riseDrilling costs normally follow rig count with 2-3 month lag

Issues for OPEC (and non-OPEC allies)

OPEC delayed planned market rebalancing by its own actions

OPEC made life harder for itself by boosting output pre-agreement

OPEC made life harder for itself by supplying market from own stocks

OPEC may be able to drain global inventories back to 5-year average

But

OPEC faces renewed challenge to market share from shale producers

OPEC’s ability to boost prices constrained by threat from shale

Summary of current situation (1)OPEC is trying to accelerate rebalancing process

Crude oil market has been gradually rebalancing since early 2016

Transition from oversupply in 2014/15 to undersupply in 2018/19

Flat prices and calendar spreads both up significantly pre-OPEC

Compliance with OPEC deal appears good (mostly due to Saudi)

Hedge funds bought into OPEC’s rebalancing narrative

Hedge funds pushed prices and spreads too far, too soon

Summary of current situation (2)Some progress on draining stocks

Crude stocks appear to be falling

Invisible stocks becoming visible

Supply & demand close to balance

Inventory overhang remains large

Rebalancing seems to be happening

Slowly at first, likely to accelerate

Summary of current situation (3)Strategic issues for OPEC

Uncertainty around reactivation of U.S. shale

Higher prices versus protection of market share

Protection of relationships with refiners in Asia

Summary of current situation (4)Key uncertainties in the medium term

Uncertain timing of crude oil market deficit and stock drawdown

Uncertain breakeven price of U.S. shale producers (cyclical costs)

Uncertain breakeven price for oil majors and offshore (costs again)

Uncertain global economic outlook (Trump, Brexit, macro-cycle)

Uncertain recovery in commodity-dependent emerging markets

OPEC compliance and eventual relaxation of output curbs

Concluding thoughts

Traders, analysts and journalists focus heavily on OPEC but other

factors are likely more important in driving prices

OPEC has very little control

OPEC should avoid complicated and probably unworkable market

management schemes

Central planning has always proved unworkable (just ask Gosplan!)

so better to rely on price signal to balance the market

Oil market seems set to remain well supplied even at current prices

for the rest of 2017/18

Price (not OPEC) will move to constrain the growth in shale output

to ensure it grows in line with demand