oikos pri finance academy 2015: unpacking the black box

TRANSCRIPT

UNPACKING THE BLACK BOX:

An investigation into the decision-making processes of

South African institutional investors

1

Colin HabbertonOikos PRI AcademyHenley, Reading, UK

1-4 June 2015

2

Overview

1. Introduction2. Motivation3. Research Methodology4. Findings5. Conclusions6. Limitations & Alternative

Explanations

(Source: USB)

Cape Town, South Africa

(Source: Wikipedia)

Stellenbosch

Introduction

Adapted from: Piketty (2014) in Cassidy (2014)

Introduction

Introduction

(Source: Google Images, 2015)

Introduction

(Source: Google Images, 2015)

9

Overview

1. Introduction2. Motivation3. Research Methodology4. Findings5. Conceptual Model6. Limitations & Alternatives

10

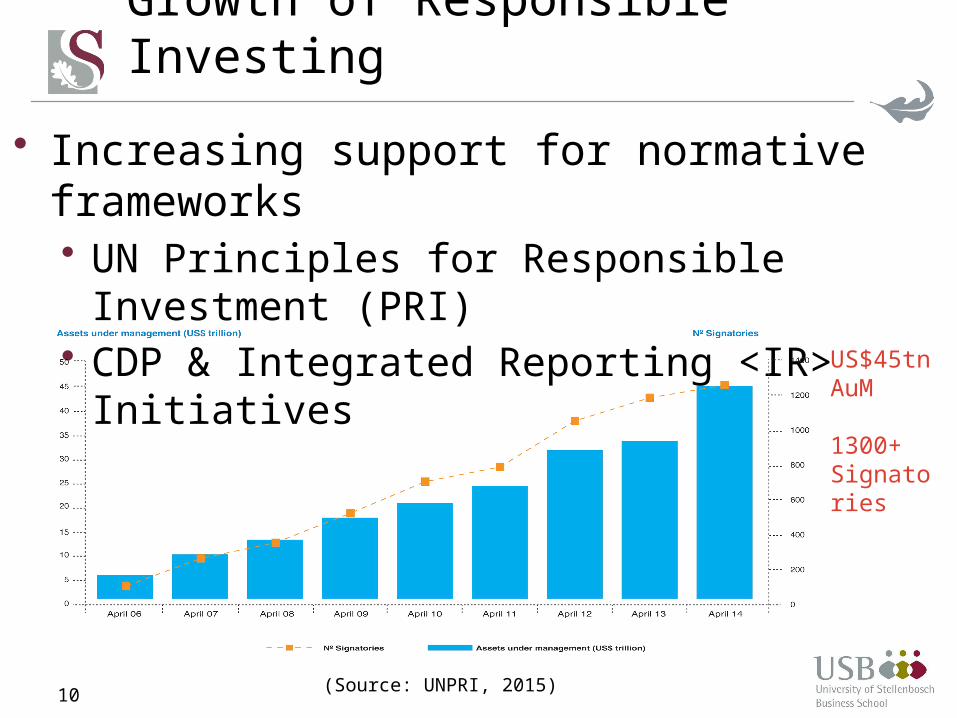

• Increasing support for normative frameworks • UN Principles for Responsible

Investment (PRI)• CDP & Integrated Reporting <IR>

Initiatives

Growth of Responsible Investing

(Source: UNPRI, 2015)

US$45tn AuM

1300+Signatories

11

“All retirement funds, long term insurers, collective investment scheme (CIS)

management companies are treated as institutional investors…” (SARB, 2013)

• Asset Owners• Public Sector: GEPF, Transnet, Eskom,

parastatals• Private Sector: Over 4800 funds FSB

registered• Asset Managers

• Public Sector: Public Investment Corporation

• Over 200 Retirement Funds & CIS companies

• Over 100 Insurers

Institutional Investors in South Africa

12

• Comparative Analysis:• ASISA Membership Base• UNPRI/CDP/<IR> Signatories• SA Reserve Bank & FSB Registration

• Interim Findings:• Of the 45 South African UNPRI

Signatories• 5 of 4800+ Asset Owners, just 1

Private Sector• 34 of 200+ Asset Managers• Role of Asset Consultants in the

process

Institutional Investors in South Africa

13

• Analysis of 20 top asset managers in RSA: • Top 10 managers account for the

management of >75% of private sector AuM

• Top 20 for >95% of AuM • Comparison to the PRI listing:

• All of the Top 10 are PRI signatories • 15 out of the top 20 asset

managers • Yet, the growth in RI funds and PRI

signatories, especially asset owners, has stagnated in recent years (Viviers 2014; PRI, 2015)

A Local Dilemma

14

Research Questions

• What are the barriers that are limiting the growth of responsible investing in South Africa?

• What factors influence the decision-making process of institutional investors towards responsible investing?

15

Barriers, drivers and enablers to RI

(Source: The State of Responsible Investing in South Africa, 2007; van der Ahee & Schulschenk; IODSA , 2013)

16

• Strong corporate culture of corporate governance developed over 20 years: • King Reports & Institute of Directors“…how a company has, both positively or negatively, impacted on the economic life of the community in

which it operated…” (IODSA, 2009).

• Localised ‘apply or explain’ version of PRI • Code for Responsible Investing in SA

(2011)• New commercial & pension fund

legislation• Companies Act of 2008• Regulation 28 of 2011

The legal & regulatory environment in SA

17

• 60% were PRI signatories (n=47)

• 40% disclosed their investment policies

• >10% of asset owners make mandates publicly available.

• >11% disclose their activities or indeed any progress made regarding CRISA disclosure

CRISA/PRI Signatory Compliance

• 30% of asset owners that provide any form of information relating to CRISA compliance,

• 90% delegated their disclosure requirements to asset managers.

• No details on how the principles are applied by any asset consultants

CRISA compliance research summary (IODSA, 2013)

South African institutional investors exhibit a “passive and selective approach” to the practice of

RI

Principles for Responsible Investing

18

(Source: UNPRI, 2014)

19

Research Questions

• What factors influence the decision-making process of institutional investors towards responsible investing?

• What are the barriers that are limiting the growth of responsible investing in South Africa?

20

Overview

1. Introduction2. Motivation3. Research Methodology4. Findings5. Conceptual Model6. Limitations and Alternatives

Research design and methodology

21

Research Problem, Questions & Objectives

Research Paradigm

Phenomenological

Research Methods

Semi-Structured Interviews

PRI Sample

Non-PRI Control Group

Data Analysis

Grounded Theory

Coding

Memos

Research Types

Qualitative

Descriptive, Exploratory

Inductive

Research methodology

• The analysis of the existing data sets of the South African investment industry provided a quantitative departure point for the paper.

• Secondary literature research provided the theoretical foundation to inform the concepts, population & sample frame for interviews.

• The consequent understanding of the theory and industry information was integrated into the design and execution of semi-structured interviews with industry experts.

22

23

Institutional Investors• Blume, M. E. & Keim, D. B. 2012. Institutional Investors

and Stock Market Liquidity: Trends and Relationships. SSRN

• Gifford, E.J.M. 2010. Effective Shareholder Engagement: The Factors that Contribute to Shareholder Salience. Journal of Business Ethics. 92:79-97.

• Piotroski, J. D. 2004. The Influence of Analysts, Institutional Investors, and Insiders on the Incorporation of Market, Industry, and Firm-Specific Information into Stock Prices. The Accounting Review, 79(4):1119-1151.

Decision-making• Bazerman, M.H. & Moore, D.A. 2009. Judgement in

Managerial Decision Making. 7th ed. Hoboken: Wiley. • Tversky, A., & Kahneman, D. 1974. Judgment under

uncertainty: Heuristics and biases. Science.185(4157): 1124-1131.

• Langley A, Mintzberg H, Pitcher P, Posada E, Saint-Macary J. 1995. Opening up Decision Making: The View from the Black Stool. Organization Science. 6(3):260-279.

Literature

24

• Miller, S. J., Hickson, D. J., & Wilson, D. C. 1996. Decision-making in organizations. In Clegg, S.R., Hardy, C. & Nord, W.R. Handbook of Organization Studies. London: Sage.

• Glanville, R. 2009, Black Boxes. Cybernetics and Human Knowing. pp153-167

Institutional Structure • Clarke, G.L. 2000. The functional and spatial structure of the

investment management industry. Geoforum, 31(1):71-86.Responsible Investing in South Africa• IODSA. 2013. CRISA disclosure by institutional investors and

their service providers. Sandton: IODSA• Van der Ahee, G & Schulschenk, J. 2013. The State of RI in

South Africa:. Climate Change and Sustainability Services: E&Y Africa.

• Viviers, S., Eccles, N.S., de Jong, D., Bosch, J.K., Smit, E. v.d.M & Buijs, A. 2008. Responsible investing in South Africa. Investment Analysts Journal. 69(1):3-16.

• Viviers, S. 2014. 21 years of responsible investing in South Africa: key investment strategies and criteria. Journal of Economic and Financial Sciences. 7(3):737-774.

Literature

25

“…the essence of ultimate decision remains impenetrable to the observer – often, indeed,

to the decider himself…” John F. Kennedy

• The Decision• What is a decision?

• The Decision-maker• Economic Man (Mill, Ricardo)• Onto Administrative Man (Simon)• Now, Insightful Man (Allison, Nonaka)• Possible argument for Relational Man

Decision-making theory (Langley et al)

26

Decision-making processes

(Source: Langley et al, 1995:263-275)

27

Stakeholder decision-making system

(Source: Clark, 2000)

Research sample

28

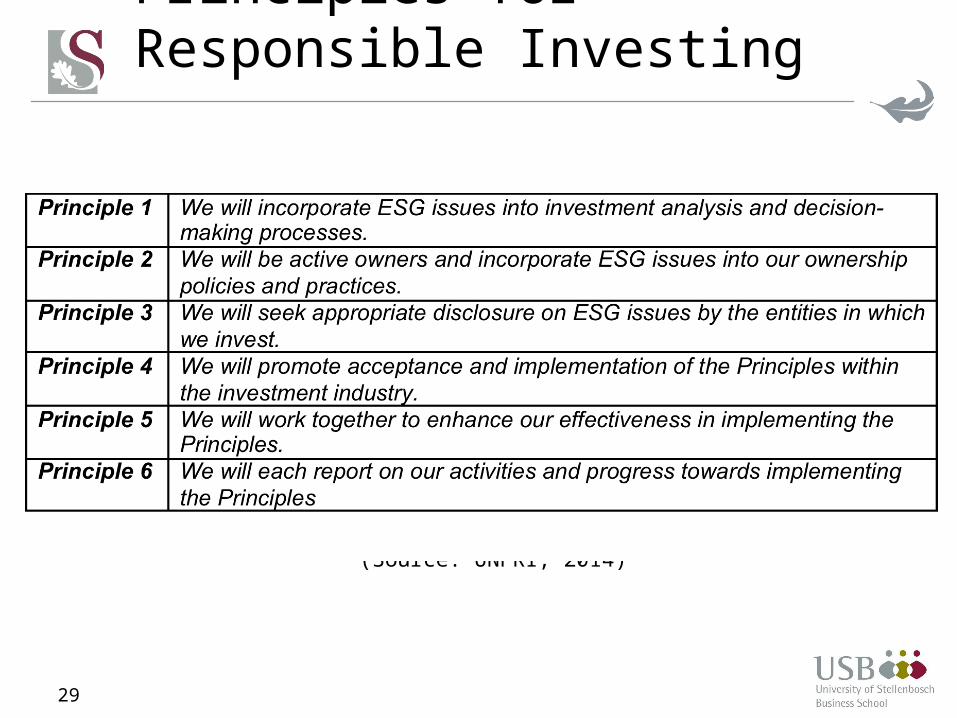

Principles for Responsible Investing

29

(Source: UNPRI, 2014)

30

Overview

1. Introduction2. Motivation3. Research Methodology4. Findings5. Conceptual Model6. Alternative Explanations

31

• Institutional PRI/CRISA participation• Perception of institutional ‘window-

dressing’• Unanimous acceptance of importance of

ESG• Investment decision-making

• Delegation of decision-making to skilled specialists

• Influence of unregulated asset consultants

• Fee structures heavily geared towards benchmarks

• Responsibility• Different perspectives on definition of

responsibility• Maximisation of return overriding intent• Evidence of ‘change agents’ and

awareness

Findings: Institutional Investor Interviews

32

• Accountability & Transparency• Resistance to concept by the

professionals• Requires additional resources and time• Potential disregard for analysis and

depth• Inefficient, chaotic driven by

sentiment• Lack of investor literacy and

prudence• Increase institutional investor

accountability to ownership responsibilities

• Highlight the importance of ESG decision-making

• Increased demand may enhance choice

Findings: Institutional Investor Interviews

33

Overview

1. Introduction2. Motivation3. Research Methodology4. Findings5. Conceptual Model6. Limitations & Alternatives

34

Observed Behaviours & Drivers?

• What factors influence the decision-making process of institutional investors towards responsible investing?

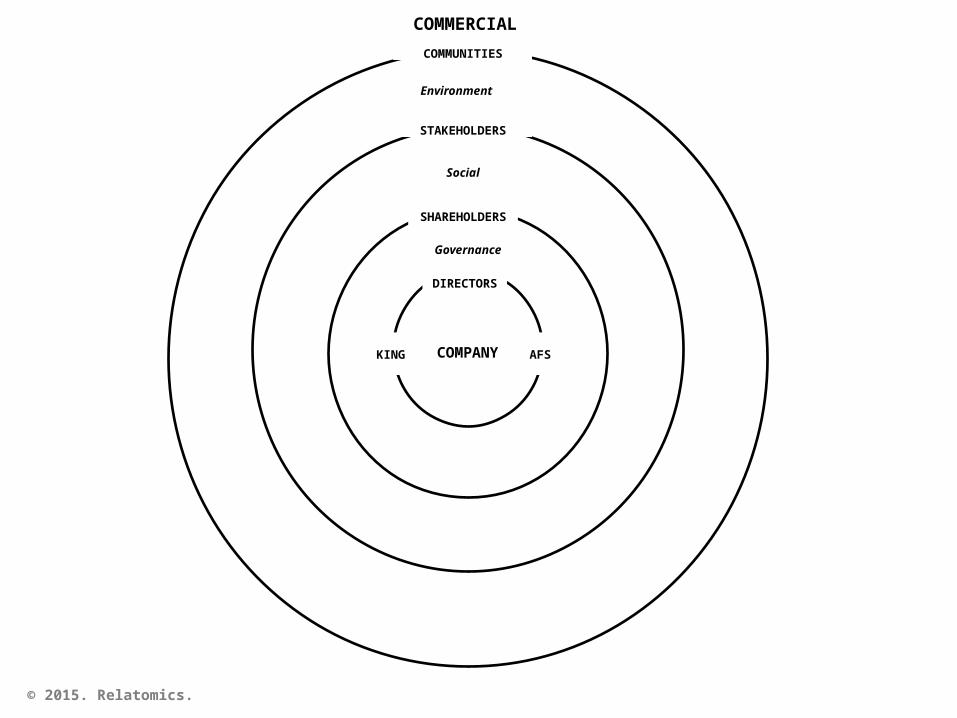

© 2015. Relatomics.

DIRECTORS

AFSCOMPANYKING

COMMERCIAL

INVESTORS

© 2015. Relatomics.

DIRECTORS

AFSCOMPANYKING

COMMERCIAL

Governance

INVESTORS

© 2015. Relatomics.

DIRECTORS

AFSCOMPANYKING

COMMERCIAL

Social

Governance

INVESTORS

© 2015. Relatomics.

DIRECTORS

AFSCOMPANYKING

COMMERCIAL

Environment

Social

Governance

INVESTORS

© 2015. Relatomics.

Environment

Social

Governance

SHAREHOLDERS

DIRECTORS

STAKEHOLDERS

AFSCOMPANY

COMMUNITIES

KING

COMMERCIAL

© 2015. Relatomics.

Environment

Social

Governance

SHAREHOLDERS

DIRECTORS

STAKEHOLDERS

CONTRIBUTORS

ASSET OWNERS

ASSET MANAGERS

BENEFICIARIES

AFSCOMPANY/

ASSET

COMMUNITIES

KING

FINANCIAL

COMMERCIAL

© 2015. Relatomics.

Environment

Social

Governance

SHAREHOLDERS

DIRECTORS

STAKEHOLDERS

CONTRIBUTORS

ASSET OWNERS

ASSET MANAGERS

BENEFICIARIES

AFSCOMPANY/

ASSET

COMMUNITIES

KING

FINANCIAL

COMMERCIAL

© 2015. Relatomics.

Environment

Social

Governance

SHAREHOLDERS

DIRECTORS

STAKEHOLDERS

CONTRIBUTORS

ASSET OWNERS

ASSET MANAGERS

BENEFICIARIES

AFSCOMPANY/

ASSET

COMMUNITIES

KINGETHICAL

FINANCIAL

ANALYTICAL

COMMERCIAL

Environment

Social

Governance

SHAREHOLDERS

DIRECTORS

STAKEHOLDERS

CONTRIBUTORS

ASSET OWNERS

ASSET MANAGERS

BENEFICIARIES

AFS <IR> SR GRICOMPANY/

ASSET

COMMUNITIES

KINGPRI

CRISACR

CSVUNGCETHICAL

FINANCIAL

ANALYTICAL

COMMERCIAL

Environment

Social

Governance

SHAREHOLDERS

DIRECTORS

STAKEHOLDERS

CONTRIBUTORS

ASSET OWNERS

ASSET MANAGERS

BENEFICIARIES

AFS <IR> SR GRICOMPANY/

ASSET

COMMUNITIES

KINGPRI

CRISACR

CSVUNGC

ACCOUNTABILITY

TRANSPARENCYRESPONSIBILITY

PARTICIPATION

ETHICAL

FINANCIAL

ANALYTICAL

COMMERCIAL

Environment

Social

Governance

SHAREHOLDERS

DIRECTORS

STAKEHOLDERS

CONTRIBUTORS

ASSET OWNERS

ASSET MANAGERS

BENEFICIARIES

AFS <IR> SR GRICOMPANY/

ASSET

COMMUNITIES

KINGPRI

CRISACR

CSVUNGC

Power

Acces

s

Value

Info

rmat

ion

Time

ACCOUNTABILITY

TRANSPARENCYRESPONSIBILITY

PARTICIPATION

Return

RiskReputation

ETHICAL

FINANCIAL

ANALYTICAL

COMMERCIAL

Environment

Social

Governance

SHAREHOLDERS

DIRECTORS

STAKEHOLDERS

CONTRIBUTORS

ASSET OWNERS

ASSET MANAGERS

BENEFICIARIES

AFS <IR> SR GRICOMPANY/

ASSET

COMMUNITIES

KINGPRI

CRISACR

CSVUNGC

Power

Acces

s

Value

Info

rmat

ion

TimeCITIZENSHIP

ACCOUNTABILITY

TRANSPARENCY

ACTIVITY

RESPONSIBILITY

PARTICIPATION

ENGAGEMENT

NORMS

DISCLOSURE

METRICS

OWNERSHIP

IMPACT

Return

RiskReputation

ETHICAL

FINANCIAL

ANALYTICAL

COMMERCIAL

47

Unpacking the Black Box…

48

Overview

1. Introduction2. Motivation3. Research Methodology4. Findings5. Conceptual Model6. Limitations & Alternatives

49

• Small sample• Robustness of the framework• Justification of ‘proximity horizon’• Missing factors and behaviours• Test the validity of the model• Applicability to contexts outside South

Africa• Limited data due to access to information,

transparency in decision-making processes• Compare interview findings to quantitative

evidence

Limitations & Alternatives

50

Final Word

“We don't know who discovered water, but we know it wasn't the fish.”

Marshall McLuhan