office of school finance update texas education agency dawn-fisher... · office of school finance...

TRANSCRIPT

Office of School Finance Update

Texas Education Agency

Great Expectations for New School Finance Legislation 22nd Annual Public School Finance Conference

Education Service Center X June 11, 2015

Office of School Finance Texas Education Agency

1

Rule Regarding Audit Firm

Office of School Finance Texas Education Agency

2

Rule Regarding Audit Firm

• 19 Texas Administrative Code §109.23

• The district or other educational entity must hire at its own expense an independent auditor to conduct an independent audit of its financial statements and provide an opinion on its annual financial report.

• The independent auditor must: – Be associated with a certified public accountancy (CPA) firm that has a

current valid license issued by the Texas State Board of Public Accountancy (TSBPA)

– Be a CPA with a current valid license issued by the TSBPA as required under the Texas Education Code, §44.008; and

– Adhere to the generally accepted auditing standards (GAAS), adopted by the American Institute of CPAs (AICPA), as amended, and the generally accepted government auditing standards (GAGAS), adopted by the US Government Accountability Office, as amended.

EXTERNAL AUDITORS

Office of School Finance Texas Education Agency

3

• The CPA firm must:

– Be a member of the AICPA Governmental Audit Quality Center

(GAQC);

– Adhere to GAQC's membership requirements; and

– Collectively have the knowledge, skills, and experience to be

competent for the audit being conducted, including thorough

knowledge of the government auditing requirements and: • Texas public school district environment; or

• Public sector; or

• Nonprofit sector.

EXTERNAL AUDITORS

Rule Regarding Audit Firm

Office of School Finance Texas Education Agency

4

UPDATES TO THE TEXAS ADMINISTRATIVE CODE (TAC)

• If at any time the TEA division responsible for financial

compliance reviews an audit firm's working papers and finds

that the firm or the quality of the work does not meet the

required standards, the division may require the district or

other educational entity to change its audit firm.

• There is NO requirement for mandatory rotation.

EXTERNAL AUDITORS

Rule Regarding Audit Firm

Office of School Finance Texas Education Agency

5

Special Allotment Reviews

Office of School Finance Texas Education Agency

6

Special Allotment Reviews

• TEC Chapter 42, Subchapter C, Special Allotments:

– Special Education

– Compensatory Education

– Bilingual Education

– Career and Technology Education

– Gifted and Talented

– High School

Office of School Finance Texas Education Agency

7

Special Allotment Reviews

• Risk Assessment based on:

– 3 consecutive years of financial data reported in the FSP (revenue) and PEIMS systems (expenditures)

– Findings in the Annual Financial Report (AFR)

– Findings in a Legislative Budget Board Management and Performance Review

– Concerns raised by program areas or complaints

Office of School Finance Texas Education Agency

8

Special Allotment Reviews

• Types of reviews:

– Desk or on-site review (in-depth review) triggered by risk assessment

– Audit Follow-Up and Financial Management Reviews

– Student Attendance Compliance Reviews – transaction testing for accuracy in coding, allowability, and timeliness.

– AFR reviews

– CPA workpaper reviews

Office of School Finance Texas Education Agency

9

Special Allotment Reviews

• Some areas we will look at:

– Compliance with direct expenditure requirements

– Appropriate expenditures on direct services

• For example, bilingual funds may be spent on a stipend but may not be used to fund a teacher’s entire salary

– Compliance with the requirement to prioritize state compensatory education spending on students who failed end-of-course exams

Office of School Finance Texas Education Agency

10

Special Allotment Reviews

• Potential results:

– Letter directing the district or charter to take required actions.

– Requirement to submit corrective action plans

– Potential loss of state funds

Office of School Finance Texas Education Agency

11

Financial Integrity Rating System of

Texas (FIRST)

Office of School Finance Texas Education Agency

12

Proposed FIRST

• 19 Texas Administrative Code (TAC) §109.1001 • School FIRST or Charter FIRST • Legislative mandate to combine FIRST and Financial Solvency into one system • Proposed seven indicators for the rating year 2014–2015 based on financial

data of 2014 (30 points) • Proposed fifteen indicators for rating years 2015–2016 and 2016–2017 (phase

in of passing standard) • Open for public comment May 22, 2015 - June 22, 2015 • Public hearing: June 17, 2015, 9 am – 12 noon at Travis Building, Room 1-104 • Web address:

http://tea.texas.gov/About_TEA/Laws_and_Rules/Commissioner_Rules_(TAC)/Proposed_Commissioner_of_Education_Rules/

Office of School Finance Texas Education Agency

13

Proposed FIRST – 2014–2015

• Indicator 1:

– Was the complete annual financial report (AFR) and ISD or charter school financial data submitted to TEA within 30 days of the November 27 or January 28 deadline depending on the ISD or charter school’s fiscal year end date of June 30 or August 31, respectively?

– Critical Indicator

– Source: AFR

Office of School Finance Texas Education Agency

14

Proposed FIRST – 2014–2015

• Indicator 2:

– Was there an unmodified opinion in the AFR on the financial statements as a whole? The American Institute of Certified Public Accountants (AICPA) defines unmodified opinion. The external independent auditor determines if there was an unmodified opinion

– Critical Indicator

– Source: AFR

Office of School Finance Texas Education Agency

15

Proposed FIRST – 2014–2015

• Indicator 3:

– Was the ISD or charter school in compliance with the payment terms of all debt agreements at fiscal year end?

– Critical Indicator

– Source: AFR

Office of School Finance Texas Education Agency

16

Proposed FIRST – 2014–2015

• Indicator 4: – ISD - Was the total unrestricted net asset balance (Net of the

accretion of interest for capital appreciation bonds) in the governmental activities column in the Statement of Net Assets greater than zero? • (If the district's 5 year percent change in students in membership was 10 percent or

more, then the district passes this indicator).

– Charter School - Was the total net asset balance in the Statement of Financial Position for the charter school greater than zero? • (If the charter school’s membership of students increased by 10 percent or more

over the past 5 years, then the charter school passes this indicator).

– Critical Indicator

– Source: AFR and PEIMS

Office of School Finance Texas Education Agency

17

Proposed FIRST – 2014–2015

• Indicator 5:

– Was the ISD or charter school administrative cost ratio equal to or less than the threshold ratio?

– 10 point scale

– Source: AFR and FSP

Office of School Finance Texas Education Agency

18

Proposed FIRST – 2014–2015

• Indicator 5:

ISD

ADA Threshold 10 8 6 4 2

10,000 0.046 0.053 0.061 0.069 0.076

5,000 0.05 0.066 0.083 0.099 0.116

1,000 0.068 0.079 0.091 0.102 0.126

500 0.079 0.093 0.107 0.121 0.135

Less than 500 0.108 0.139 0.169 0.199 0.23

Sparse 0.153 0.191 0.229 0.268 0.306

CHARTER

ADA Threshold 10 8 6 4 2

1,000 0.087 0.142 0.191 0.239 0.288

500 0.090 0.152 0.214 0.276 0.330

0 0.094 0.163 0.238 0.314 0.390

Office of School Finance Texas Education Agency

19

Proposed FIRST – 2014–2015

• Indicator 6:

– Did the comparison of Public Education Information Management System (PEIMS) data to like information in the district’s AFR result in an aggregate variance of less than 3 percent of all expenditures per fund type?

– 0 or 10 points

– Source: AFR and PEIMS

Office of School Finance Texas Education Agency

20

Proposed FIRST – 2014–2015

• Indicator 7:

– Was the AFR free of any instance(s) of material weaknesses in internal controls over financial reporting and compliance for local, state, or federal funds? The AICPA defines material weakness. The external independent auditor determines if there are any instances of material weakness.

– 0 or 10 points

– Source: AFR

Office of School Finance Texas Education Agency

21

Proposed FIRST – Future years

• Proposed future indicators – Make timely payments of payroll taxes to TRS, TWC, IRS

• (Critical)

– Days cash on hand, General Fund • ISDs = 90+ • Charters = 60+

– Current assets to current liabilities • ISDs = 3+ • Charters = 2+

– Long-term liability to long-term asset ratio • ISDs and charters = 0.6

– Revenues >= expenses (General Fund) or 60 days cash on hand

Office of School Finance Texas Education Agency

22

Proposed FIRST – 2014–2015

• Proposed future indicators – Debt service coverage

• Measures ability of district or charter to meet debt requirements • Ratio for ISDs and charters = 1.2

– Student to total staff ratio • Based on prior three years of enrollment • If no decline in enrollment over past three years = automatic pass • If enrollment declines by 15% or more, ratio should be maintained (through

reduction in staff) or lose 10 points

– FSP adjustment based on a financial hardship • No hardship adjustment = 10 points • Hardship adjustment = 0 points

Office of School Finance Texas Education Agency

23

Proposed FIRST

• REMINDER: Your district or charter must prepare, distribute, and hold a public meeting to discuss the Annual Financial Management Report within two months of the final FIRST rating. The report must include: – The FIRST rating and how it performed on each indicator for the

current and previous year – The superintendent’s contract or other written documentation to

report the total compensation paid to the superintendent unless the superintendent’s contract is posted on the school’s website

– A summary schedule of expenditures paid to and on behalf of the superintendent and each board member

Office of School Finance Texas Education Agency

24

Proposed FIRST

• REMINDER (cont’d) – A summary schedule for the fiscal year of the total dollar amount by

the executive officers and board members of gifts that had an economic value of $250 or more in the aggregate in the fiscal year (only gifts from outside entity)

– A summary schedule for the fiscal year of the dollar amount by board member for the aggregate amount of business transactions with the school district or open-enrollment charter school,

– Any other information the board of trustees determines to be useful – Retained for three years – Applies to both ISDs and Charters

Office of School Finance Texas Education Agency

25

DEPOSITORY CONTRACTS

Office of School Finance Texas Education Agency

26

Depository Contracts

• 19 Texas Administrative Code §§ 109.51, 109.52

• The district must use the following forms: – Bid Form for Depository Services

– Proposal Form for Depository Services

• The district must keep the selected bid or proposal form in the district and make it available to the Texas Education Agency upon request.

Office of School Finance Texas Education Agency

27

Depository Contracts

• Documents must be submitted to TEA electronically.

• Please do not mail or email the documents.

– Depository Contract for Funds of Independent School Districts under the Texas Education Code, Chapter 45, Subchapter G, School District Depositories

– Texas School Depository Surety Bond Form

• Applies to both ISDs and charter schools

Office of School Finance Texas Education Agency

28

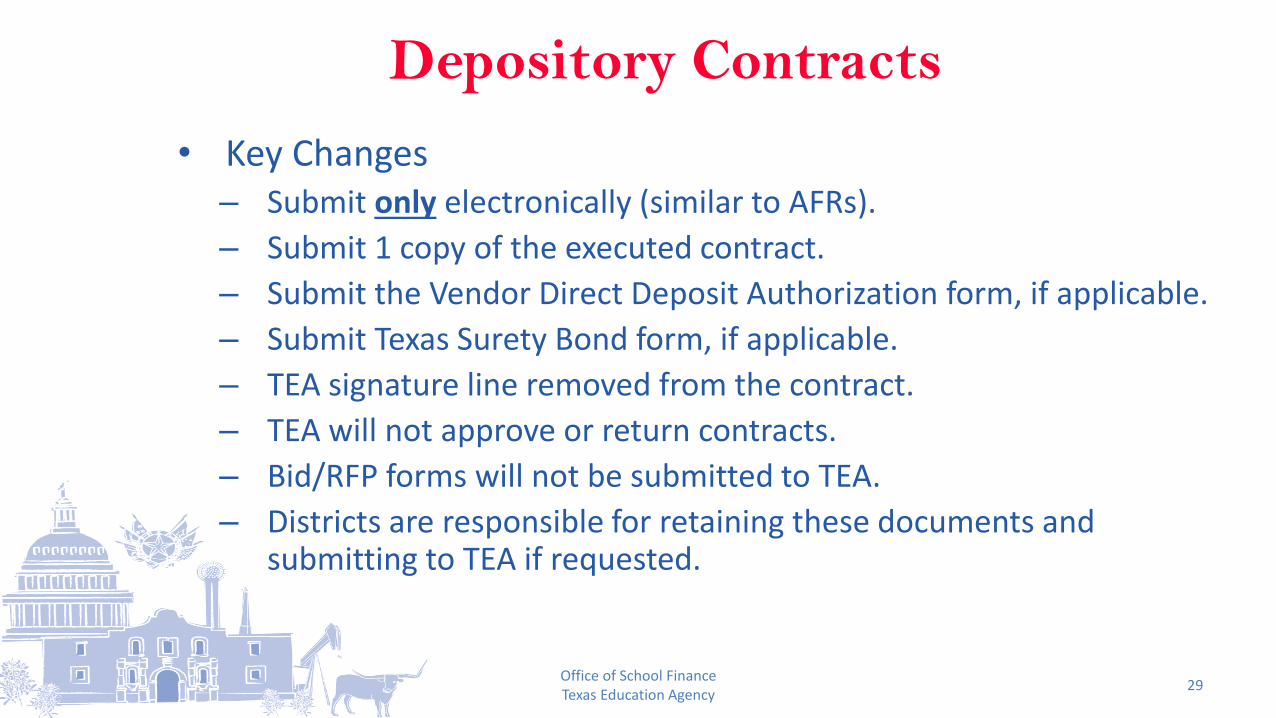

Depository Contracts

• Key Changes – Submit only electronically (similar to AFRs).

– Submit 1 copy of the executed contract.

– Submit the Vendor Direct Deposit Authorization form, if applicable.

– Submit Texas Surety Bond form, if applicable.

– TEA signature line removed from the contract.

– TEA will not approve or return contracts.

– Bid/RFP forms will not be submitted to TEA.

– Districts are responsible for retaining these documents and submitting to TEA if requested.

Office of School Finance Texas Education Agency

29

OVERVIEW OF LEGISLATIVE SESSION

SCHOOL FINANCE CHANGES

Office of School Finance Texas Education Agency 30

Overview of Legislative Session

• We are still reviewing legislation, so this is a very preliminary analysis, subject to change!

• Nothing is final until after the veto period (June 21)

Office of School Finance Texas Education Agency

31

House Bill 1: Base Funding Elements

2014-2015 2015-2016 2016-2017

Basic Allotment $5,040 $5,140 $5,140

Equalized Wealth Level (Tier I) $504,000 $514,000 $514,000

Guaranteed Yield (Austin Pennies) $61.86 $74.28 $77.53

Guaranteed Yield (Copper Pennies) $31.95 $31.95 $31.95

Equalized Wealth Level (Copper Pennies) $319,500 $319,500 $319,500

Office of School Finance Texas Education Agency

32

House Bill 1

• New Instructional Facilities Allotment

– $23.75 million in each year of the biennium

– Will provide for $250 per ADA in a new campus, up to appropriations limit

– Since the program was not funded last year, no campuses are currently in second year status

– Districts must submit an online application by July 15 to be eligible for funding

– NIFA module is now open!

Office of School Finance Texas Education Agency

33

House Bill 1

• Instructional Facilities Allotment (IFA)

– Appropriation of $55.5 million in fiscal year 2017

– Will provide for a new round of IFA

– IFA is a program to provide property poor school districts assistance in repaying bonded debt on instructional facilities

– IFA is not the same thing as NIFA!

– Information coming soon regarding how to apply

Office of School Finance Texas Education Agency

34

House Bill 1

• Supplemental Funding for Prekindergarten

– $15 million in each year of the biennium

– Funded on the basis of eligible prekindergarten ADA

– In the past, this has been worth about $148 per pre-k ADA

Office of School Finance Texas Education Agency

35

House Bill 1

• Rider 71 funding, related to TRS contributions, is not continued

Office of School Finance Texas Education Agency

36

House Bill 1

• Contingency Riders

– Homestead Exemption Hold-Harmless

• $1.2 billion for the biennium is allocated for an additional $10,000 homestead exemption

• Contingent on SB 1 and SJR 1 passing as well as the constitutional amendment receiving popular vote

Office of School Finance Texas Education Agency

37

House Bill 1

• Contingency Riders

– Maintenance and operations tax rate conversion (fractional funding)

• $200 million for the biennium is allocated contingent on legislation passing that would allow districts with compressed tax rates below $1.00 to convert copper pennies to basic allotment pennies

• Legislation allowing tax rate conversion included in House Bill 7

Office of School Finance Texas Education Agency

38

Senate Bill 1

• Increases the mandatory homestead exemption from $15,000 to $25,000 • Contingent on SJR 1 • Begins in tax year 2015 (2015-2016 school year) • Optional homestead exemptions may not be repealed or reduced before January

1, 2020 • The Property Tax Assistance Division (PTAD) state funding value for recapture and

state aid will be recalculated as if the exemption went into effect in 2014 • PTAD values going forward will reflect reduced value

Office of School Finance Texas Education Agency

39

Senate Bill 1

• The recalculation of the PTAD will:

– Reduce the local share and increase the state share of Tier I

– Reduce the local share and increase the state share of Tier II

– Reduce the local share and increase the state share of the Existing Debt Allotment (EDA) and IFA

– Reduce recapture

• The recalculation of tax collections will:

– Increase ASATR for those districts that receive it

Office of School Finance Texas Education Agency

40

Senate Bill 1

• Districts held harmless to the state and local maintenance and operations revenue that would have been available:

– without exemption,

– under 2015-2016 school finance formulas,

– excluding any increased maintenance and operations tax rates.

Office of School Finance Texas Education Agency

41

Senate Bill 1

• Districts held harmless to the state and local Interest and Sinking revenue that would have been available

– Without the exemption,

– Using 2015-2016 eligible debt

Office of School Finance Texas Education Agency

42

House Bill 7

• Allows districts that had tax rates below $1.50 in 2005 and so have compressed tax rates below $1.00 to increase compressed tax rates.

– Districts must have a current tax rate greater than their original compressed tax rate plus $0.06;

– For the 2015-2016 and 2016-2017 school years, districts must request the conversion

Office of School Finance Texas Education Agency

43

House Bill 7

• If tax rate conversion occurs:

– tax effort will be shifted out of the zone of Tier II that is equalized at $31.95 per penny of tax effort to Tier 1

– tax effort will be shifted out of the zone of recapture governed by the equalized wealth level of $319,500 and to the zone governed by the equalized wealth level of $514,000

– For districts that receive ASATR, tax effort will be shifted under the ASATR umbrella, out of Tier 2

Office of School Finance Texas Education Agency

44

Yield per Penny of Tax Effort in School Finance

System

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

$70.00

$80.00

Tier I Austin Copper

Office of School Finance Texas Education Agency

45

House Bill 7 Example

Without Conversion With Conversion

2005 tax rate $1.35 $1.35

Current Adopted Rate 1.04 1.04

Compressed tax rate 90 98

Pennies allocated to Austin Yield 6 6

Pennies allocated to Copper Yield 8 0

Office of School Finance Texas Education Agency

46

House Bill 7

• Will tax rate conversion help my district?

– Districts that do not receive ASATR should benefit from tax rate conversion because low yield pennies are shifted to Tier I, which has a higher yield.

– Districts that receive ASATR may not benefit since Tier 2 is outside the ASATR umbrella and so revenue is shifted from outside to within the ASATR portion of the formula.

Office of School Finance Texas Education Agency

47

House Bill 7 Example

Without Conversion With Conversion Difference

Compressed Tax Rate .8614 1.00

Adopted M&O Tax Rate $1.17 $1.17

District Basic Allotment $4,426 $5,140

Total Tier I Allotment $107,175,373 $124,003,449

Local Fund Assignment ($58,422,277) ($67,830,326)

Tier I State Aid $48,753,096 $56,173,103 $7,420,007

Total Tier II Entitlement $29,562,927 $18,996,995

Total Tier II Local Share ($21,990,598) ($12,107,717)

Tier II State Aid $7,572,329 $6,889,278 -$683,051

ASATR $5,004,636 0 -$5,004,636

Total State Aid $61,330,061 $63,062,381 $1,732,320

Office of School Finance Texas Education Agency

48

House Bill 7

• TEA will post information soon related to how to notify us of your district’s decision as well as how to evaluate the impact of the decision

Office of School Finance Texas Education Agency

49

Other Legislation with Financial Implications

• House Bill 4

– Up to $1,500 per student available for districts that implement a high quality prekindergarten program;

– Appropriation of $59 million in each year of the biennium is provided in HB 1

Office of School Finance Texas Education Agency

50

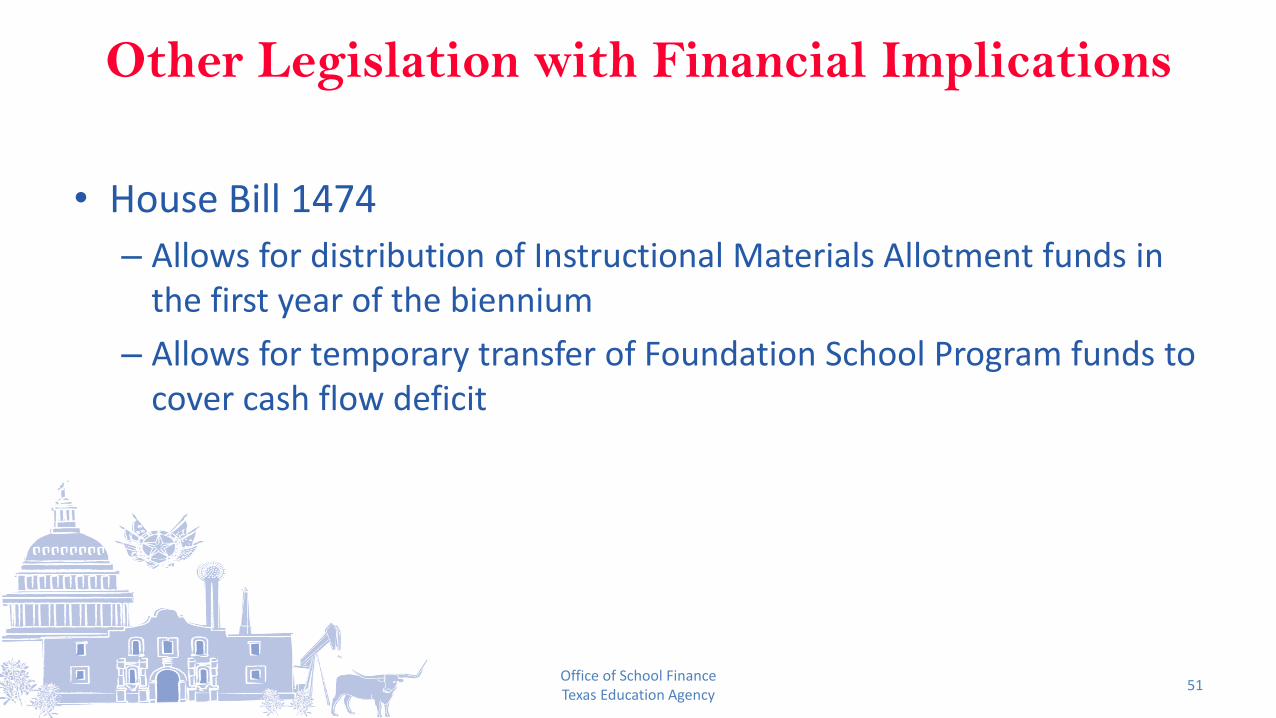

Other Legislation with Financial Implications

• House Bill 1474

– Allows for distribution of Instructional Materials Allotment funds in the first year of the biennium

– Allows for temporary transfer of Foundation School Program funds to cover cash flow deficit

Office of School Finance Texas Education Agency

51

Other Legislation with Financial Implications

• House Bill 2251 – Allows charter schools with enrollment growth of more than 10

percent from prior year to request FSP payment acceleration

• House Bill 2660 / Senate Bill 496 – Allows use of two or four hour rule for Optional Flexible School Day

program

– Allows expanded use of Optional Flexible School Day program without application process––will still require local board approval

– Allows use of state compensatory education funds for childcare expenses for at-risk students

Office of School Finance Texas Education Agency

52

Other Legislation with Financial Implications

• House Bill 1305

– Allows locally funded program for provision of free or reduced-priced breakfast;

– Allows alternative reporting for compensatory education on one or more campuses in a district;

– Requires a detailed plan for use of compensatory education funds if a virtual campus intends to make use of this provision

Office of School Finance Texas Education Agency

53

OTHER UPDATES FROM STATE

FUNDING

Office of School Finance Texas Education Agency 54

Closing Out 2013-2014

• Final summary of finances (SOFs) for the 2013–2014 school year are posted. These SOFs incorporate:

– Transportation module data if the district submitted!

– Staff salary data if the district submitted!

– EYS student counts, and

– Final tax collection data from the J-1 schedule.

• Positive balances will be paid and adjustments rolled to 2014–2015.

Office of School Finance Texas Education Agency

55

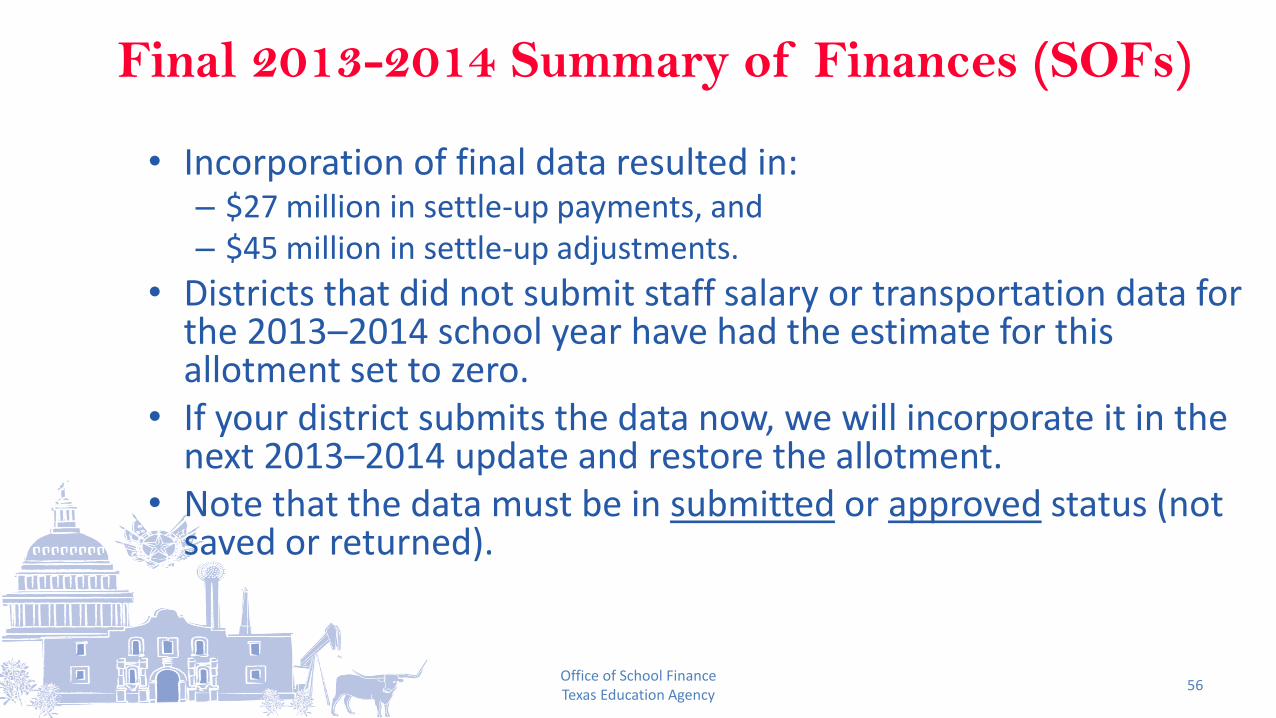

Final 2013-2014 Summary of Finances (SOFs)

• Incorporation of final data resulted in: – $27 million in settle-up payments, and – $45 million in settle-up adjustments.

• Districts that did not submit staff salary or transportation data for the 2013–2014 school year have had the estimate for this allotment set to zero.

• If your district submits the data now, we will incorporate it in the next 2013–2014 update and restore the allotment.

• Note that the data must be in submitted or approved status (not saved or returned).

Office of School Finance Texas Education Agency

56

Updates to the 2014-2015 SOF

• Legislative Payment Estimates (LPE) now incorporate:

– Current tax rates from Comptroller’s Self Report, and

– Updated state compensatory education counts (with two months of CEP data for those districts participating).

• District Planning Estimates (DPE) now incorporate:

– Updated ADA estimates (DPE running 27,800 lower than LPE), and

– Updated tax collections (DPE running $548 million higher than LPE).

Office of School Finance Texas Education Agency

57

State Compensatory Education Detail Report

Office of School Finance Texas Education Agency

58

Updates to the 2014-2015 SOF

• The Tax Information Survey is open. Submissions of 2014–2015 tax collections due August 31.

• The Transportation module is open. Submissions of 2014–2015 route services reports due August 3.

• The staff salary module is open. Submission of 2014–2015 data due August 31 for inclusion in Near Final SOF.

Office of School Finance Texas Education Agency

59

Preliminary 2015-2016 SOF

• Preliminary 2015–2016 SOFs are posted and incorporate:

– Revised basic allotment, equalized wealth level, guaranteed yield

– Revised ASF rate (estimated at $284)

– Student counts submitted through pupil projections

– 2014 preliminary values

– Maintenance and operations tax collections increased by 4.56 percent from 2014 budget

Office of School Finance Texas Education Agency

60

Preliminary 2015-2016 SOF

• After voter authorization of constitutional amendment related to homestead exemption SOFs will be revised to include:

– Revised property values and tax collections, and

– Calculation of homestead exemption hold-harmless

• This fall, SOFs updated to include fractional funding adjustments

Office of School Finance Texas Education Agency

61

QUESTIONS??

Lisa Dawn-Fisher

(512) 463-9179

Amanda Brownson

(512) 463-0986

Office of School Finance Texas Education Agency

62