ofel 2014 buracas-vilnius

TRANSCRIPT

COMPLEX ASSESSMENT OF ESSENTIAL FINANCIAL INDICATORS

IN CORPORATE GOVERNANCE

A. Buracas, A. Zvirblis, V. Navickas– Lithuania

SUMMARY OF RESEARCH

The study presents the framework for the complex evaluation of

the essential FINANCIAL INDICATORS IN CORPORATE GOVERNANCE:

• based on multiple criteria assessment methodology;

• reflecting its advantage or disadvantage in evaluation of social processes;

• determining the values of so-called indicator pillars &

general measure when the significance of each indicator is

allowed.

The authors applied the Simple Additive Weighting (SAW) method of quantitative evaluation of the governance quality indicators.

2

SYSTEMIC EVALUATION & ANALYTICAL FINDINGS

The theoretic background of the complex evaluation :

• Substantiation of essential financial indicators for manufacturing corporation (as a whole);

• Formalization of interrelations between primary financial indicators and corporate management system;

• Development of multiple criteria evaluation methodology forthe whole of financial indicators;

• Creation of background assessment models by aapplying the Simple Additive Weighting method.

3

MAIN ATTITUDES

For certain companies from the selected industry (their target group), the adequate indicator totality (evaluation criteria system) must be constructed.

It is expedient to detail the purposeful groups(pillars) of these indicators as partially integrated evaluation criteria.

The complex assessment of financial indicators reflecting corporate governance effectiveness was presented for the case of competitive Lithuanian manufacturing corporations to illustrate the application of the analytical research results.

4

COMPLEX EVALUATION METHODOLOGY

The developed multicriteria evaluation methodology is based on:

• formation of the evaluation criteria system;• conceptual provisions of the determination of general

dimension;• expert examination and determination of significances of

primary financial indicators; • establishment of pillar indexes and • determination of the overal index (as a generalized measure)

based on proposed models.

The integrated evaluation system may include several scenarios according to the trend of predicted indicator values.

5

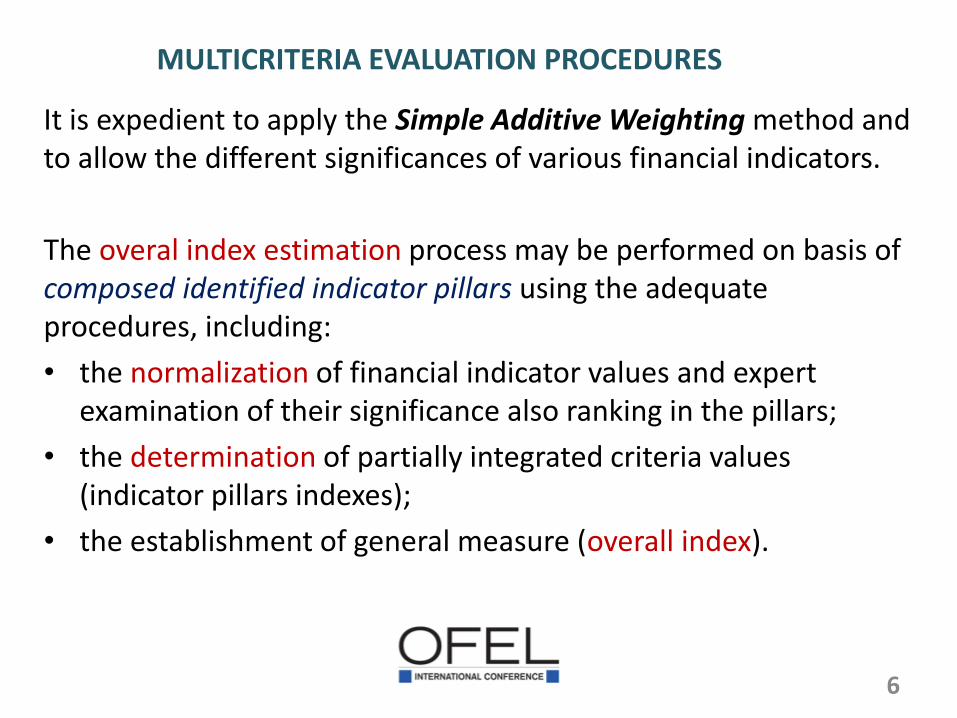

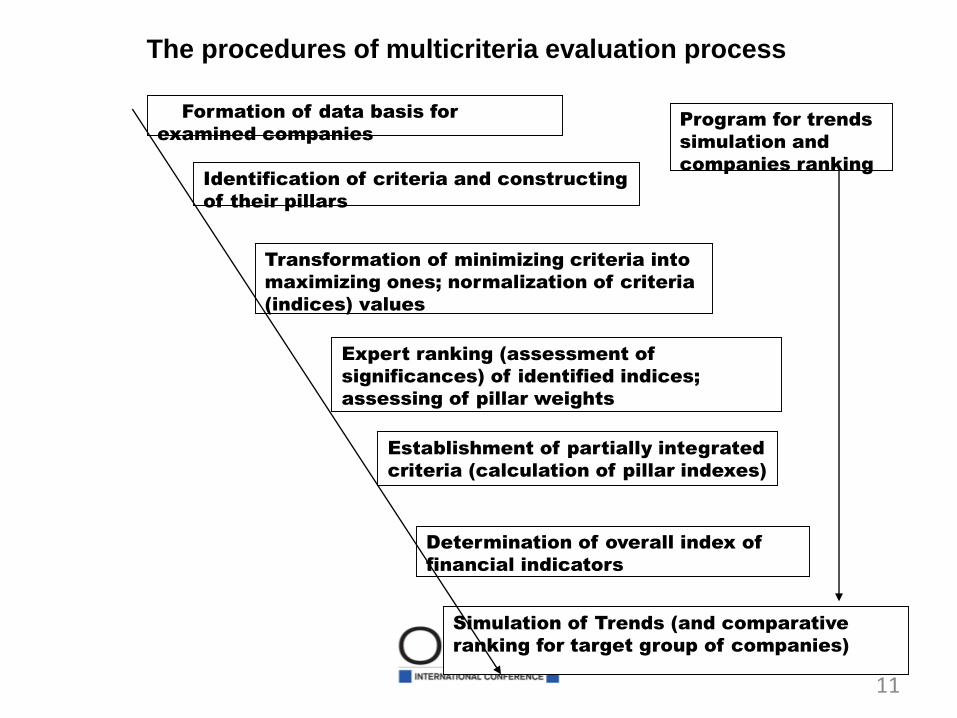

MULTICRITERIA EVALUATION PROCEDURES

6

It is expedient to apply the Simple Additive Weighting method and to allow the different significances of various financial indicators.

The overal index estimation process may be performed on basis of composed identified indicator pillars using the adequate procedures, including:

• the normalization of financial indicator values and expert examination of their significance also ranking in the pillars;

• the determination of partially integrated criteria values (indicator pillars indexes);

• the establishment of general measure (overall index).

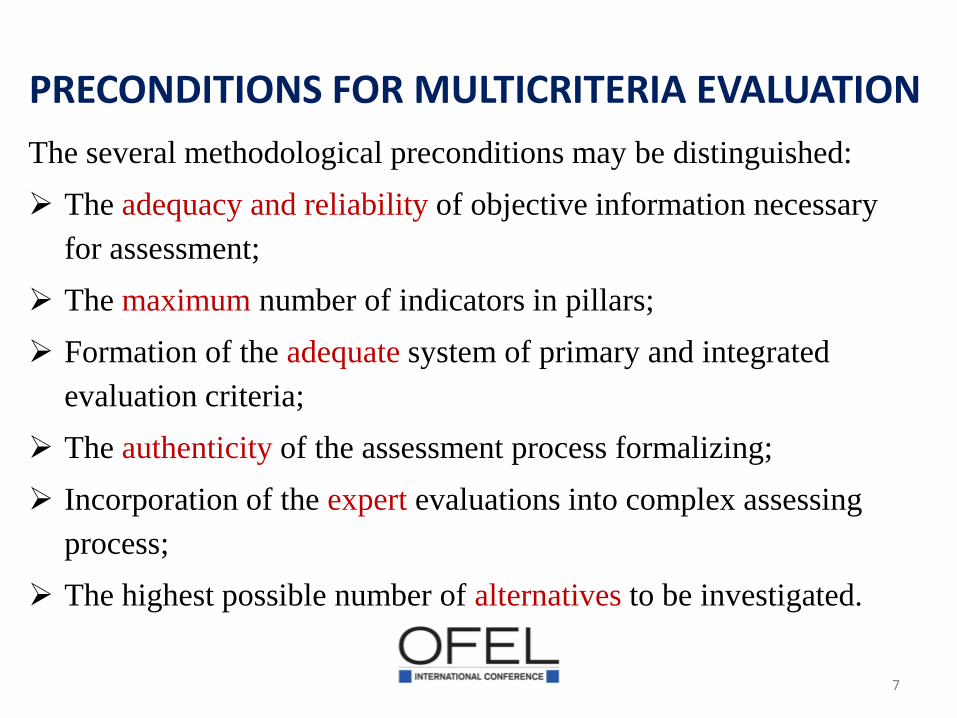

PRECONDITIONS FOR MULTICRITERIA EVALUATION

7

The several methodological preconditions may be distinguished:

The adequacy and reliability of objective information necessary

for assessment;

The maximum number of indicators in pillars;

Formation of the adequate system of primary and integrated

evaluation criteria;

The authenticity of the assessment process formalizing;

Incorporation of the expert evaluations into complex assessing

process;

The highest possible number of alternatives to be investigated.

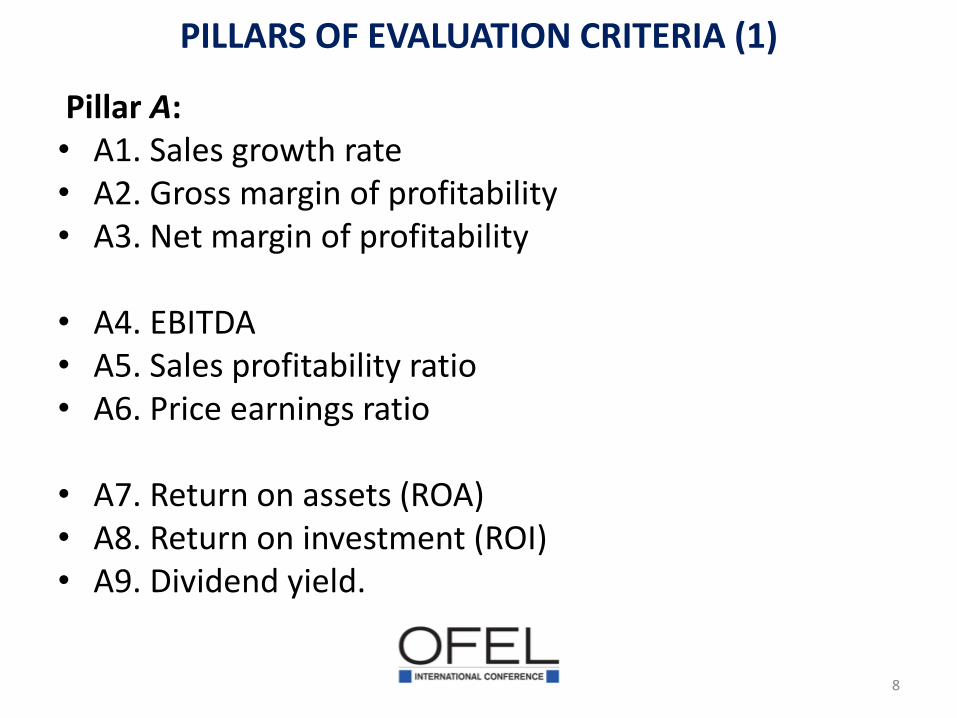

PILLARS OF EVALUATION CRITERIA (1)

Pillar A:• A1. Sales growth rate• A2. Gross margin of profitability • A3. Net margin of profitability

• A4. EBITDA • A5. Sales profitability ratio• A6. Price earnings ratio

• A7. Return on assets (ROA) • A8. Return on investment (ROI)• A9. Dividend yield.

8

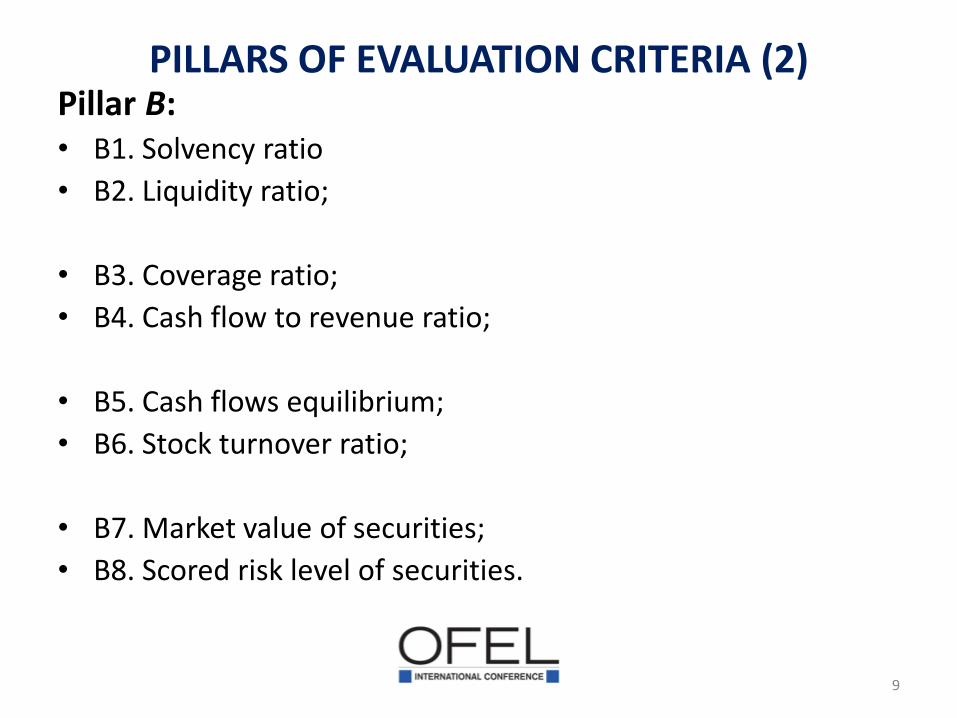

PILLARS OF EVALUATION CRITERIA (2)

9

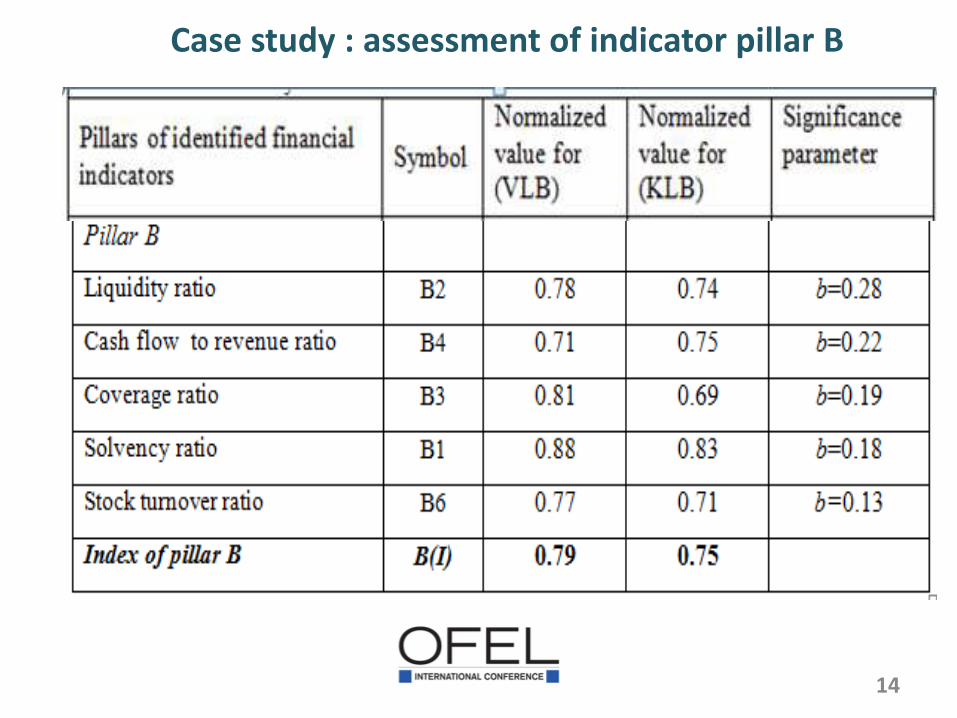

Pillar B:• B1. Solvency ratio

• B2. Liquidity ratio;

• B3. Coverage ratio;

• B4. Cash flow to revenue ratio;

• B5. Cash flows equilibrium;

• B6. Stock turnover ratio;

• B7. Market value of securities;

• B8. Scored risk level of securities.

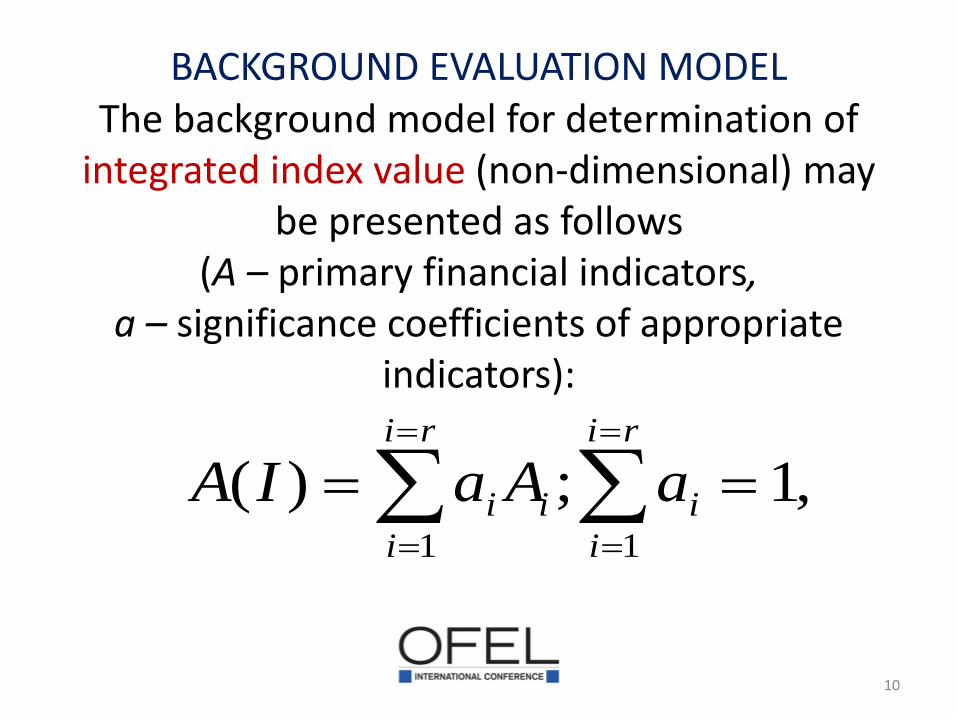

BACKGROUND EVALUATION MODELThe background model for determination of

integrated index value (non-dimensional) may be presented as follows

(A – primary financial indicators,a – significance coefficients of appropriate

indicators):

10

,1;)(11

ri

i

ii

ri

i

i aAaIA

11

The procedures of multicriteria evaluation process

Formation of data basis for

examined companies

Identification of criteria and constructing

of their pillars

Transformation of minimizing criteria into

maximizing ones; normalization of criteria

(indices) values

Expert ranking (assessment of

significances) of identified indices;

assessing of pillar weights

Establishment of partially integrated

criteria (calculation of pillar indexes)

Determination of overall index of

financial indicators

Simulation of Trends (and comparative

ranking for target group of companies)

Program for trends

simulation and

companies ranking

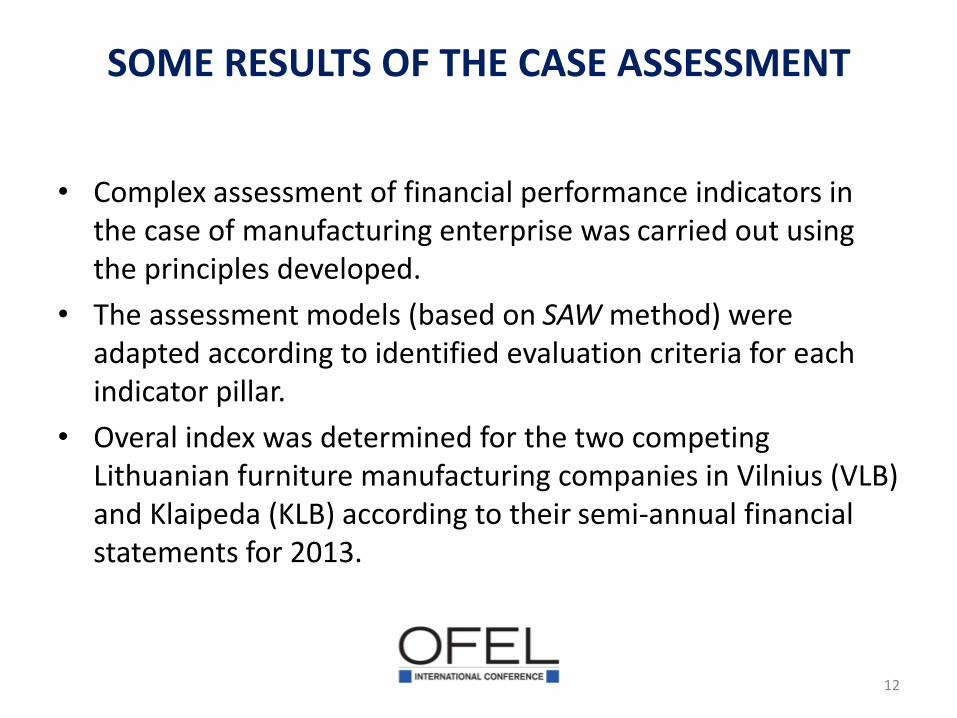

SOME RESULTS OF THE CASE ASSESSMENT

12

• Complex assessment of financial performance indicators in the case of manufacturing enterprise was carried out using the principles developed.

• The assessment models (based on SAW method) were adapted according to identified evaluation criteria for each indicator pillar.

• Overal index was determined for the two competing Lithuanian furniture manufacturing companies in Vilnius (VLB) and Klaipeda (KLB) according to their semi-annual financial statements for 2013.

13

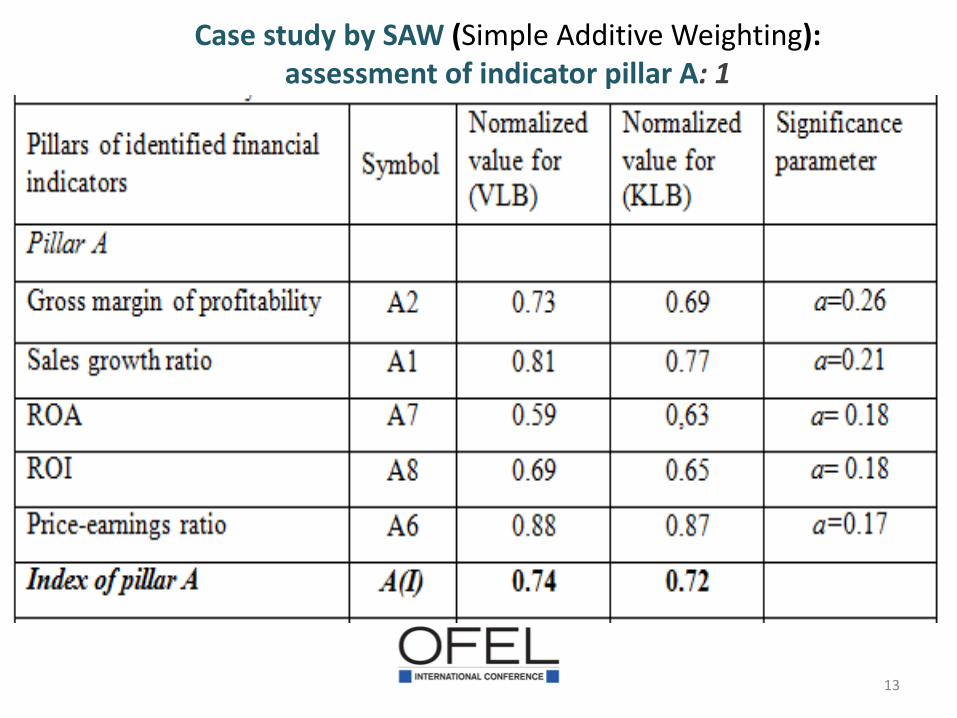

Case study by SAW (Simple Additive Weighting): assessment of indicator pillar A: 1

14

Case study : assessment of indicator pillar B

Conclusions:1

15

The quantitative assessment process is particularly relevant

under conditions of dynamic changes of the surrounding macro

factors affecting corporate management strategy. The

quantitative methodology is still not integrated adequately with

expert evaluations.

It is characterized by adaptability (according to the whole of

evaluation criteria for an assessment in specific conditions);

and it is applicable for the complex investigation of the quality

and effectiveness of corporate governance.

The algorithmic procedures of proposed assessment process may

be incorporated into support system of business management.

Conclusions (2)

16

Authors suggested the complex aggregated evaluation at corporate level – background, modelling and technique.

There are more wide possibilities to implement the Multicriteria Assessment Methodology based on Simple Additive Weighting method when investigating competitive manufacturing corporations & forming more sophisticated algorithms of this process. The proposed models have beenapplied by determining the overal index.

An algorithm of computer-generated assessment process may be recommended to apply when modeling the different trend effects of financial indicators.