oecd work on institutional investors and long- term

TRANSCRIPT

___________________________________________________________________________

2015/FMP/WKSP2/022 Session 5.1

OECD Work on Institutional Investors and Long-Term Financing - Expanding the Role of Pension Funds and Insurers As Investors in Asia-Pacific

Capital Markets

Submitted by: OECD

Workshop on Infrastructure Financing and Capital Market Development

Iloilo, Philippines23-24 July 2015

OECD WORK ON INSTITUTIONAL

INVESTORS AND LONG-TERM

FINANCING

Stephen A. Lumpkin

Senior Economist

Financial Affairs Division - OECD

1. Expanding the role of pension funds and insurers as investors in Asia-Pacific capital markets

2.Appendix

2

Contents

Expanding the role of institutional investors

in Asia-Pacific capital markets

Matching Supply and Demand for long-term finance

3

Categories of investors in capital

markets

Four categories of “investors” in OECD capital markets

• Fundamental investors: traditional long-term investors. Maintain

open positions and are typically not leveraged

• Hedgers: in the market to limit exposure in funding markets or to

off-lay other particular risks

• Arbitrageurs: assess the value of financial instruments on a

relative, versus absolute, basis. Compare current market values with

historic norms to identify opportunities for mean reversions

• Speculators: traditional contrarians.

Where are the institutional investors?

4

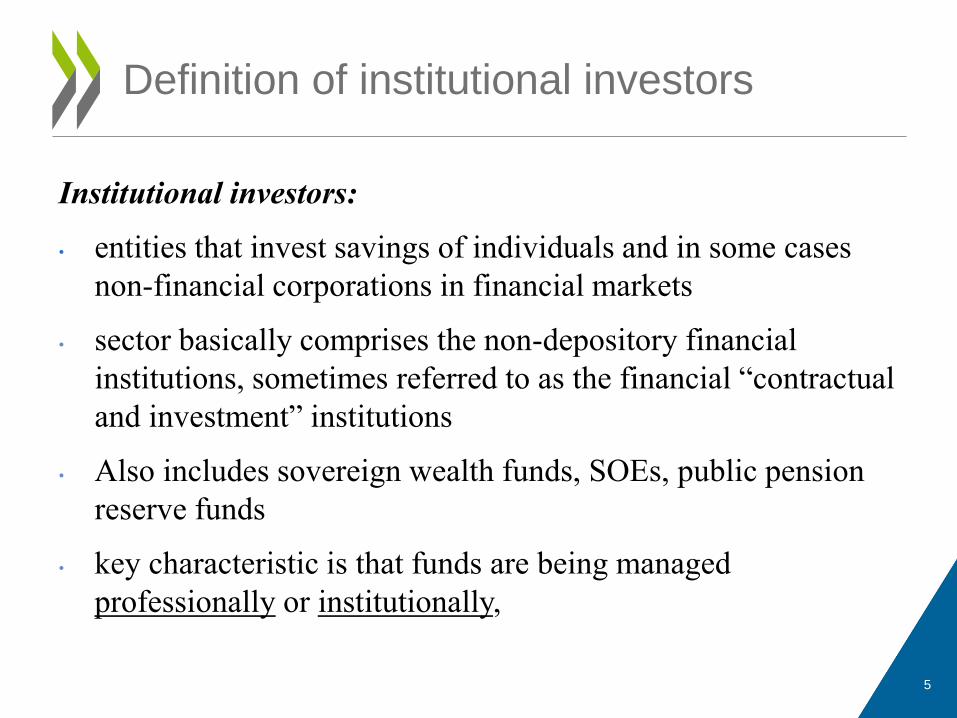

Definition of institutional investors

Institutional investors:

• entities that invest savings of individuals and in some cases

non-financial corporations in financial markets

• sector basically comprises the non-depository financial

institutions, sometimes referred to as the financial “contractual

and investment” institutions

• Also includes sovereign wealth funds, SOEs, public pension

reserve funds

• key characteristic is that funds are being managed

professionally or institutionally,

5

Common Characteristics of Institutional

Investors

• Long-term savings vehicles

Managed professionally

Special Regulatory Regime

• Fiduciary duty to investors supported by

Law and regulation

Market competition

• Other features

Differing liability for future payments

Tax status

Execution of investment strategy

6

Reasons to promote institutional

investors

• To provide increased retirement income for an ageing population, thereby relieving pressures on budgets associated with state-financed pay-as-you-go systems;

• To promote the development of an equity culture

• To make risk capital available to new or innovative enterprises

• To increase the range of choices available to investors and firms

• To develop more efficient financial intermediation and more effective systems of corporate governance

7

Investment strategies of institutional

investors

• Institutional investors operate on the basis of well-

defined risk-return criteria.

• Some institutions are highly risk averse;

• others invest in riskier assets with higher expected

returns.

• Myriad investment strategies exist in practise,

stretched across numerous asset dimensions: fixed-

income versus equity, mature versus emerging

market, domestic versus international, etc.

8

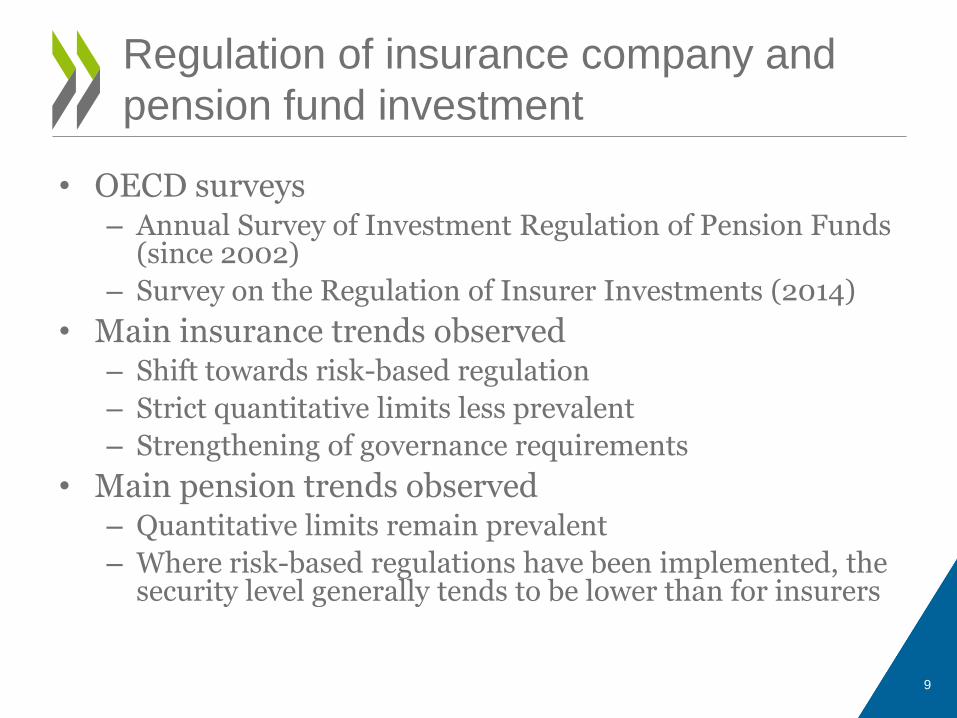

• OECD surveys– Annual Survey of Investment Regulation of Pension Funds

(since 2002)

– Survey on the Regulation of Insurer Investments (2014)

• Main insurance trends observed– Shift towards risk-based regulation

– Strict quantitative limits less prevalent

– Strengthening of governance requirements

• Main pension trends observed– Quantitative limits remain prevalent

– Where risk-based regulations have been implemented, the security level generally tends to be lower than for insurers

Regulation of insurance company and

pension fund investment

9

• Limits on investment in certain instruments

– Limits on certain asset classes (e.g. equities) or types of instruments (e.g. unlisted or non-investment grade)

• Limits on investment in the vehicle with which the instrument is accessed

– Limits on indirect investment in retail or private funds (e.g. mutual funds, REITs, private equity, hedge funds, etc.)

• Limits on the jurisdiction in which investment originates

– Geographical limits (e.g. OECD only), foreign currency limits, or limits on market-based elements (e.g. non-regulated markets)

• Limits on the concentration of exposure to single counterparties

– Limits to investment with a single entity, in a single investment, self-investment or ownership in an entity

• Limits on the nature of the investment transaction

– Limits on speculation (e.g. short selling, derivative use), securities financing transactions (e.g. securities lending) or borrowing and lending activities

Quantitative investment limits:

Conceptual framework

10

• Risk based regulation:

– requires a higher capital requirement for investment in higher risk asset classes, making explicit the trade-off between capital requirements and risk/return of investment

– alternative to strict quantitative limits, though quantitative limits may still be imposed as a complement

– increasingly based on market-consistent valuation

• Main qualitative/governance requirements:

– prudent person standards

– fiduciary duty

– clearly stating the roles and responsibilities for relevant decisions

– drawing up an written policy on investment or risk management, which may include setting internal limits on the level of risks

– ensuring that risk management structures are instituted, and the board(s) are informed and responsible for decisions

– when a non-routine investment is being planned, appropriate discussion and risk management is carried out

Risk-based regulation and qualitative

requirements

11

Considerations on investment regulations and

investment strategies (1/2)

12

• Value of quantitative investment regulation vs. alternative risk return policies of pension funds

– Simple quantitative limits have some advantage over risk-based regulation, and could achieve the same results as more complicated regulatory approaches (e.g., minimum returns with a certain security level), but only in the case that the model is validated by real events

– Long contribution/accumulation periods may allow for a larger share of riskier assets/higher replacement rates but also higher risk of shortfall

• Policies impacting the long-term investment of insurers

– Risk-based capital requirements can account for the interaction between assets and liabilities and thus encourage investment in assets with a duration in line with the liabilities

– Other government policies may also influence investment

• Japan: fiscal loan and investment program bonds to finance SMEs and large-scale, long-term projects

• Netherlands: Dutch Investment Institution (NLII) and private-sector initiated SME fund was established to facilitate the financing of the real economy

Considerations on investment regulations and

investment strategies (2/2)

13

• Counter-cyclical measures under risk-based regulation– Designed to prevent pro-cyclical investment when insurers or pension

funds with long-term liabilities are exposed to short-term volatility• Adjust the calculation of required capital: e.g. equity dampener (adjusts the risk-

charge), matching and volatility adjustments (adjusts the liability discount rate)

• Adjust the target requirement: e.g. dynamic minimum investment return

• Allowing amortised cost accounting of assets backing technical provisions

• Admissibility of assets to cover technical provisions– Conditions to allow certain types of assets to count towards covering

technical provisions• Treatment of infrastructure project bonds as corporate bonds

• Allowance for the use of proxy ratings for unrated bonds and loans

• Recognition of collateral for risk-reduction

• Asset traded on a liquid market

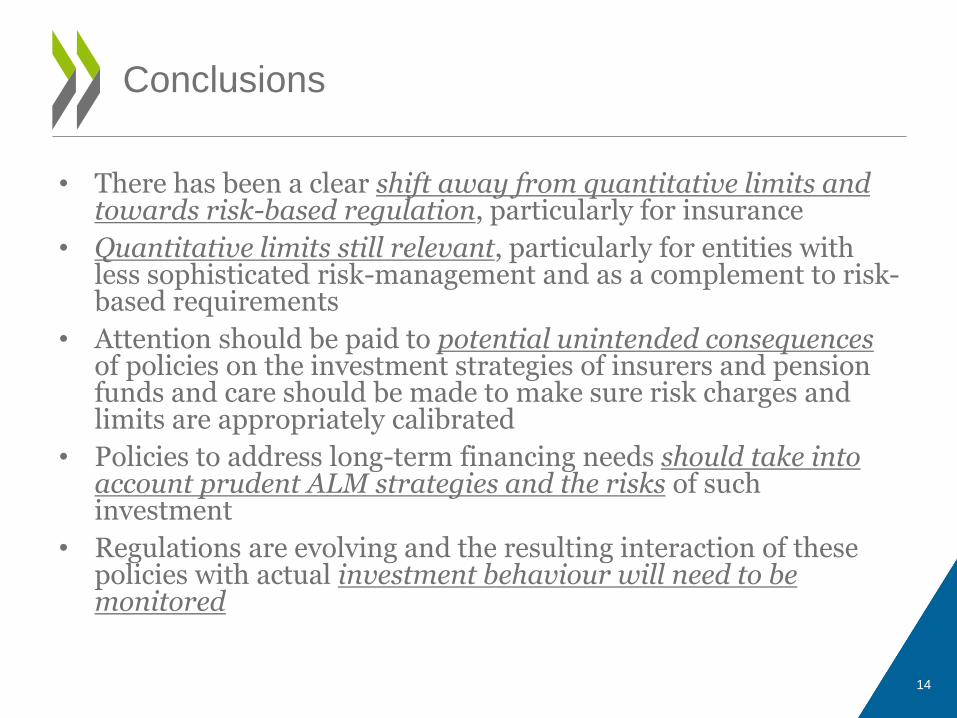

Conclusions

14

• There has been a clear shift away from quantitative limits and towards risk-based regulation, particularly for insurance

• Quantitative limits still relevant, particularly for entities with less sophisticated risk-management and as a complement to risk-based requirements

• Attention should be paid to potential unintended consequences of policies on the investment strategies of insurers and pension funds and care should be made to make sure risk charges and limits are appropriately calibrated

• Policies to address long-term financing needs should take into account prudent ALM strategies and the risks of such investment

• Regulations are evolving and the resulting interaction of these policies with actual investment behaviour will need to be monitored

Appendix

15

Institutional investors and long-term investment project

www.oecd.org/finance/lti

• Focusing on “Patient”,“Engaged”,“Productive” capital

• Large Network of LTI Investors (>3,000 members)

G20-OECD work on long-term financing

http://www.oecd.org/finance/private-pensions/g20-oecd-long-term-financing.htm

• High Level Principles for Institutional Investors and LTI (2013)

• the G20/OECD Task Force on Long-term Investment Financing by Institutional Investors

• the OECD is developing further work with the new Turkish presidency of the G20

16

Recent OECD work on long-term investment

The OECD has been developing a vast program of work on LTI for the G20

Appendix - OECD work on long-term

investment

• “Patient”,“Engaged”,“Productive” capital

• LTI investors/LT assets

• NB: Short Term not bad

• OECD, APEC & G20 relevance

• Network of LTI Investors (new Advisory Board)

17

What does long-term investment mean and why does it matter?

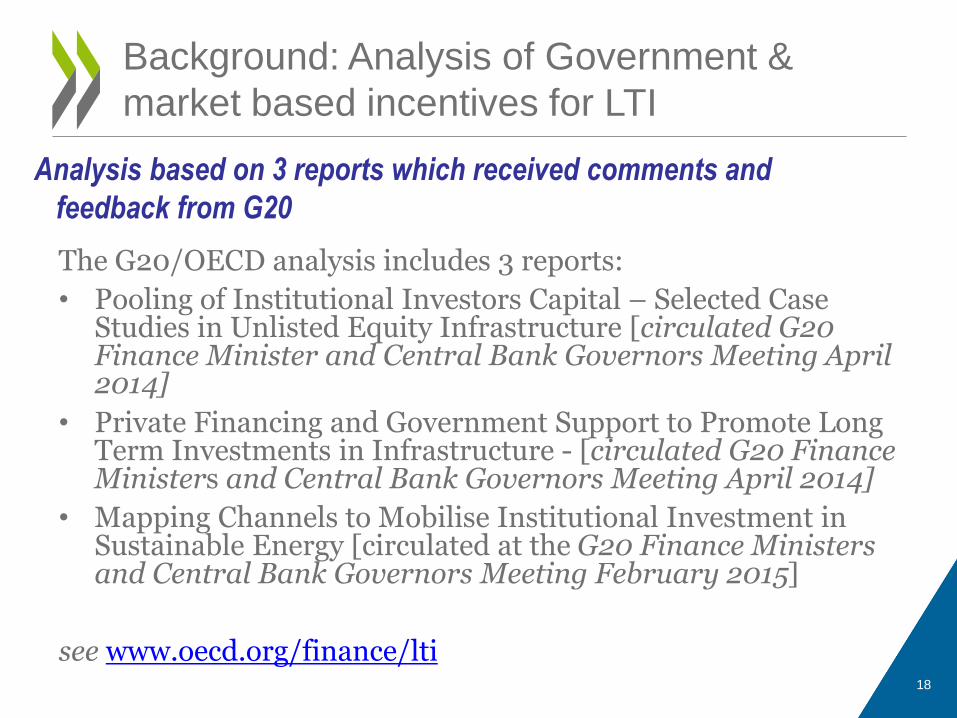

Background: Analysis of Government &

market based incentives for LTI

The G20/OECD analysis includes 3 reports:

• Pooling of Institutional Investors Capital – Selected Case Studies in Unlisted Equity Infrastructure [circulated G20 Finance Minister and Central Bank Governors Meeting April 2014]

• Private Financing and Government Support to Promote Long Term Investments in Infrastructure - [circulated G20 Finance Ministers and Central Bank Governors Meeting April 2014]

• Mapping Channels to Mobilise Institutional Investment in Sustainable Energy [circulated at the G20 Finance Ministers and Central Bank Governors Meeting February 2015]

see www.oecd.org/finance/lti18

Analysis based on 3 reports which received comments and

feedback from G20