oecd fruit and vegetables scheme · 2019-06-07 · the oecd fruit and vegetables scheme organised...

TRANSCRIPT

OECD Fruit and Vegetables Scheme

Proceedings of the

18th Meeting of the Heads of National Inspection Services

May 9-11, 2018 Seville, Spain

Organised by

OECD

Hosted by

Spanish Ministry of Economy, Industry and Competitiveness

ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT ORGANISATION DE COOPÉRATION ET DÉVELOPPEMENT ÉCONOMIQUE

18TH OECD MEETING OF THE HEADS OF NATIONAL INSPECTION SERVICES │ 3

FOREWORD

The OECD Fruit and Vegetables Scheme organised the 18th OECD Meeting of the Heads of National Inspection Services in Seville, Spain, on 9-11 May 2018, on the invitation of the Spanish Ministry of Economy, Industry and Competitiveness. The Meeting was attended by 34 delegates from 18 Scheme's participating countries as well as one Observer country. The Secretariat of the FAO/WHO Codex Alimentarius Commission was also represented.

The objective of the Meeting of the Heads of National Inspection Services is to facilitate discussions between inspection services on major developments and challenges in the fruit and vegetables sector and quality inspection system. It is also a good possibility for the countries to provide an update on the latest developments in inspection techniques and tools, and to harmonise the application of OECD quality standards.

The Meeting focused on inspection systems, traceability, internet sales of fruit and vegetables, new greenhouse technologies, organic produce, fruit and vegetables pests and citrus markets and trends. Spain gave an overview of their national quality inspection systems. Spain also organised a technical visit to see Peach and nectarine production and inspection.

The debates took place at the Chamber of commerce of Seville.

4 │

18TH OECD MEETING OF THE HEADS OF NATIONAL INSPECTION SERVICES │ 5

EXECUTIVE SUMMARY

The Spanish Ministry of Economy, Industry and Competitiveness hosted the 18th OECD Meeting of the Heads of National Inspection Services in Seville, Spain, on 9-11 May 2018. 34 delegates from 18 Scheme's participating countries as well as one Observer country attended the meeting. The Secretariat of the FAO/WHO Codex Alimentarius Commission was also represented.

The Meeting discussed the Spanish fruit and vegetables sector presented by Subdirección General de Frutas y hortalizas y Vitivinicultura Ministerio de Agricultura y Pesca, Alimentación y Medio Ambiente and the Spanish Inspection System provided by Subdirección General de Inspección, Certificación y Asistencia Técnica de Comercio Exterior.

Delegates also listened to a very interesting presentation by ANIA on new trends and technology for the microbiological control of fruit and vegetables. AINIA is a technology centre established in 1987 as a non-profit organisation. ANIA develops tools to anticipate on risks and focused on their work on risks that may affect fruit and vegetables in the future.

The Spanish private sector made a very comprehensive presentation on the citrus sector and the trends and challenges.

Delegates were also updated on organic fruit and vegetables markets, trends and challenges in Spain as well as on strategies applied in Spain to fight against fungi in the fruit and vegetable production.

Delegates also got a detailed insight into new greenhouse technologies.

Participating Countries also discussed several challenges being faced by inspection services amongst participating countries. In particular they discussed the challenges of conformity checks for fruit and vegetables internet sales (distant selling), the feasibility for OECD to develop operating rules to address internet sales and the other issues that should be considered along with internet sales. Delegates also discussed traceability issues and shared experiences on actions taken at national levels to tackle this challenge.

Spain organised a field trip to visit peaches and nectarines harvest sites as well as packinghouses. Delegates welcomed the opportunity to witness first-hand the production cycle of peaches in Spain. The Andalucía region has unique climate conditions that require extreme attention to water and nutrients of the soil. Therefore, farmers need to make the most of their land using state of the art knowledge and technology.

The recommendations of the Heads of National Inspection Services will be submitted to the 2018 77th Plenary Meeting for discussion.

6 │ 18TH OECD MEETING OF THE HEADS OF NATIONAL INSPECTION SERVICES

TABLE OF CONTENTS

EXECUTIVE SUMMARY ................................................................................................................... 5 OPENING ADDRESSES ...................................................................................................................... 8 SECTION I. PRESENTATIONS OF OTHER ORGANISATIONS .............................................. 14

INFORMATION ON RECENT ACTIVITIES OF THE CODEX ALIMENTARIUS COMMISSION ON THE STANDARDIZATION OF FRESH FRUITS AND VEGETABLES ..... 15

Presentation by Ms. Lingping Lingping Zhang, Codex Secretariat ................................................ 16

SECTION II. FRUIT SECTOR IN SPAIN ....................................................................................... 20 SPANISH FRESH FRUIT AND VEGETABLES SECTOR ............................................................. 21

Presentation by Ms Leonor de Castro, Ministerio de Agricultura y Pesca, Alimentación y Medio Ambiente ............................................................................................................................. 22

SPANISH CITRUS INDUSTRY – PRODUCTION, CHALLENGES AND PERSPECTIVES. ..... 31 Presentation by Ms Immaculada Sanfeliu Felui, Comité de Gestión de Cítricos, Spain ................ 32

SECTION III. STRUCTURE AND ACTIVITIES OF INSPECTION IN COUNTRIES ............. 42 SPANISH FRESH FRUIT AND VEGETABLES CONTROL SYSTEM ........................................ 43

Presentation by Ms Maria de Armas, Ministry of Economic Affairs and Competitiveness .......... 44

SECTION IV. FOCUS ON ORGANIC MARKETS ........................................................................ 54 ORGANIC FRUIT & VEGETABLES SALES. MARKETS, TRENDS AND CHALLENGES. ..... 55

Presentation by Mr José Miguel González Otero, Ministerio de Agricultura y Pesca, Alimentación y Medio Ambiente ................................................................................................... 56

SECTION V. FIELD TRIP ................................................................................................................. 62 SUMMARY OF DISCUSSIONS ON THE FIELD (PEACHES AND NECTARINES) .................. 63

Discussants: Primor Fruit company, RKGROWERS, Associafruit, Spain .................................... 63 SUMMARY OF DISCUSSIONS AT THE PACKING HOUSE ...................................................... 64

Discussants: Primor Fruit company, RKGROWERS, Associafruit, Spain .................................... 64

SECTION VI. NEW TECHNOLOGIES FOR FRUIT AND VEGETABLES PRODUCTION AND INSPECTION ............................................................................................................................. 65

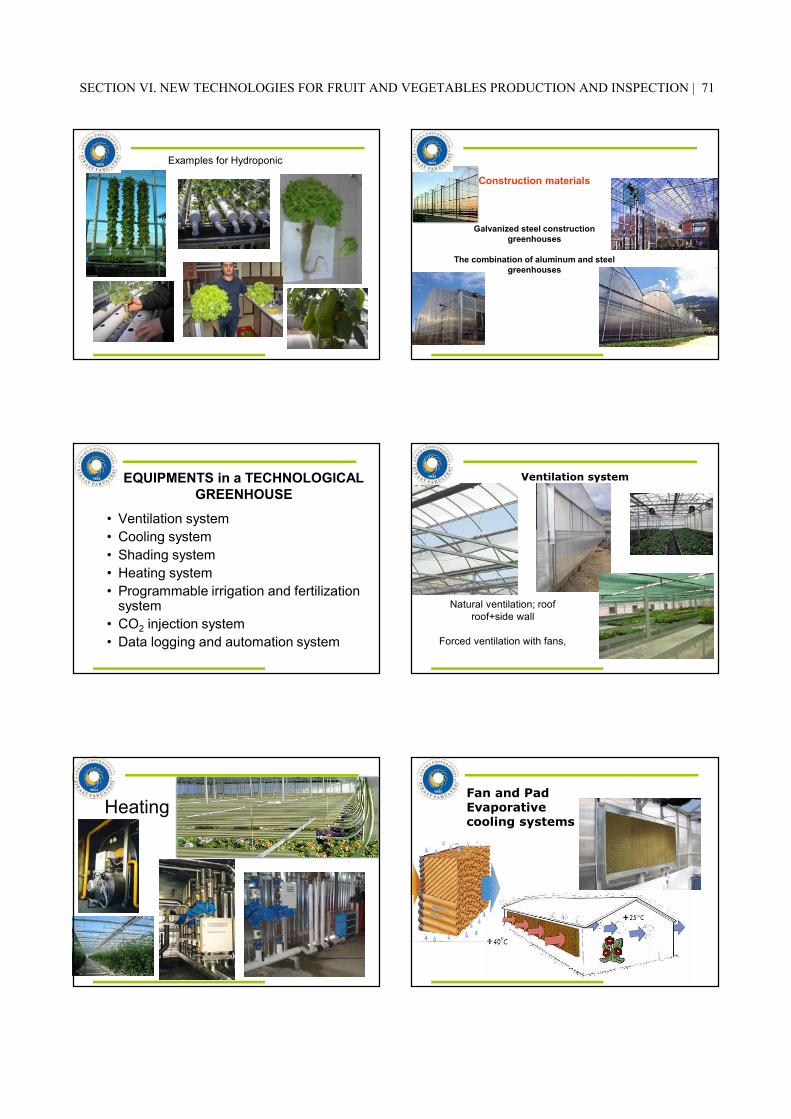

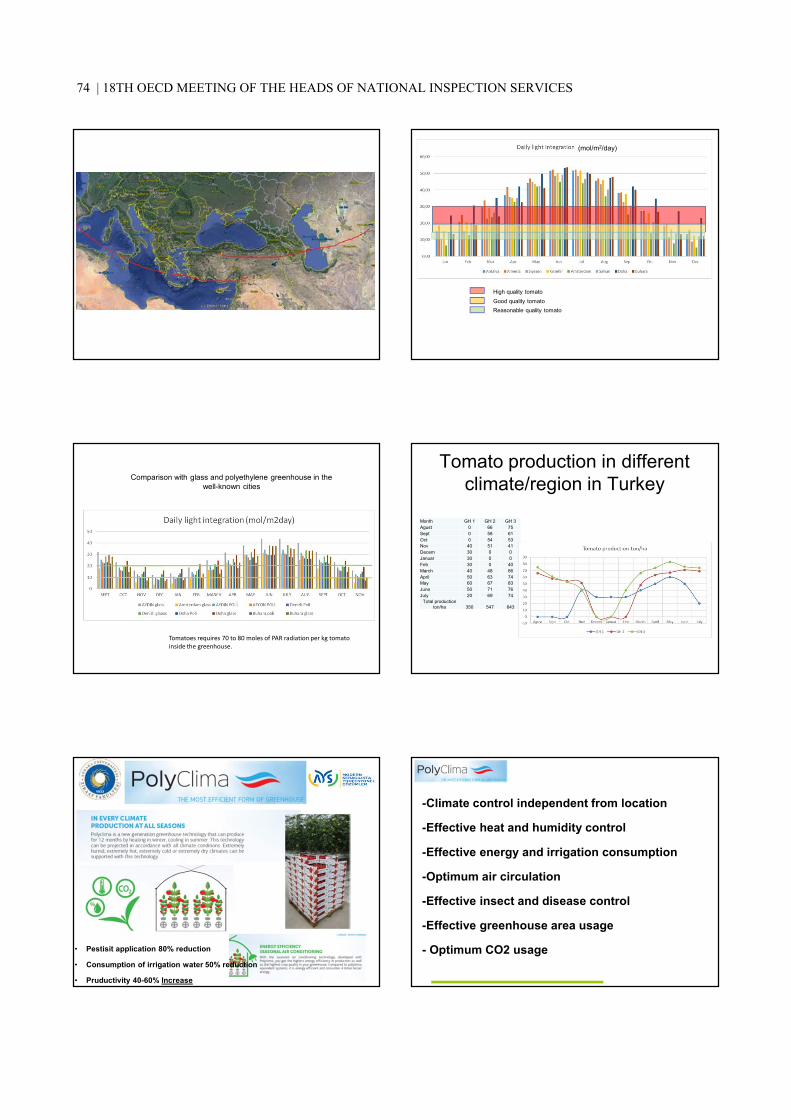

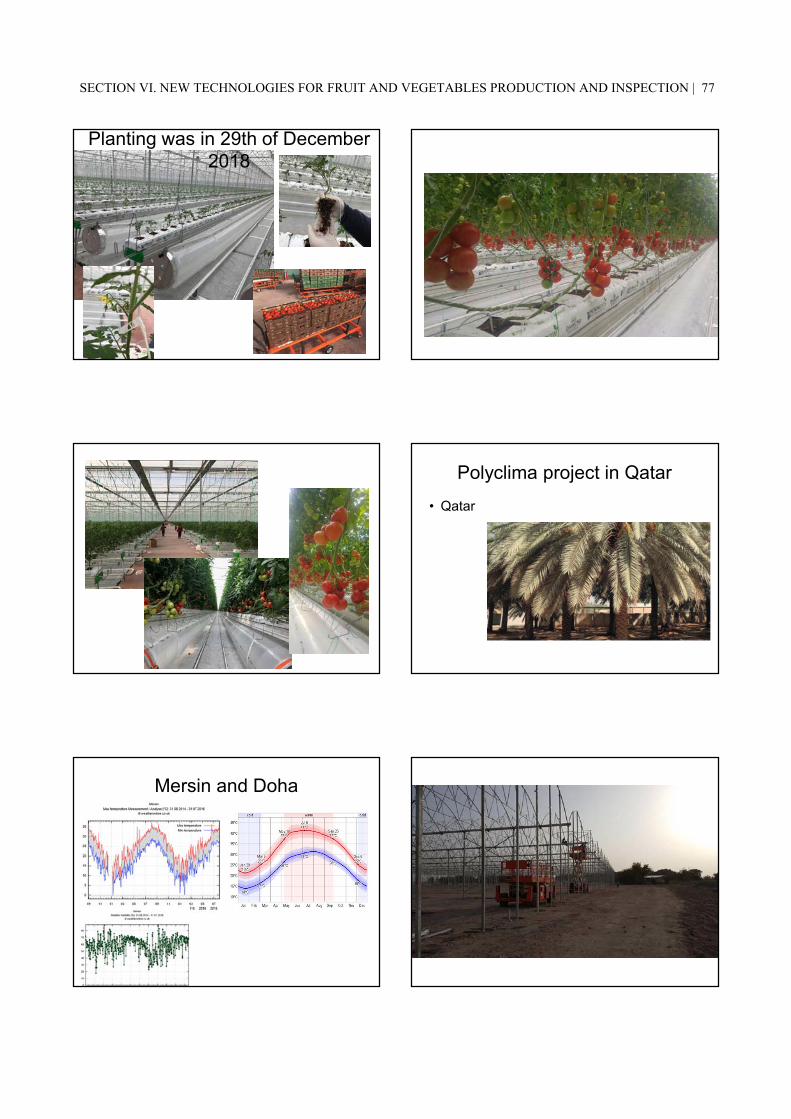

NEW GREENHOUSE TECHNOLOGIES ........................................................................................ 66 Presentation by Pr Hasan Silleli, University of Ankara, Turkey .................................................... 67

NEW MICROBIOLOGICAL ANALYSIS IN FRESH FRUITS AND VEGETABLES .................. 79 Presentation by Ms Amparo de Benito, AINIA .............................................................................. 80

SECTION VII. CHALLENGES FOR INSPECTION SERVICES ................................................. 89 TRACEABILITY ............................................................................................................................... 90

Presentation by the OECD Secretariat ............................................................................................ 91

18TH OECD MEETING OF THE HEADS OF NATIONAL INSPECTION SERVICES │ 7

CONFORMITY CHECKS FOR INTERNET SALES OF FRUIT AND VEGETABLES ............... 93 Presentation by the OECD Secretariat ............................................................................................ 94

SECTION VIII. PHYTOSANITARY AND HEALTH RISKS ....................................................... 98 STRATEGIES AGAINST FUNGI IN THE FRUIT AND VEGETABLE PRODUCTION ............. 99

Presentation by Mr Fernando J. Gonzalez, Frutaria SAT, Spain .................................................. 101

FINAL DISCUSSION AND CONCLUSION .................................................................................. 104 ANNEX I. SOME PHOTOS OF THE EVENT ............................................................................... 105 ANNEX II. DRAFT AGENDA ......................................................................................................... 111 ANNEX III. LIST OF PARTICIPANTS ......................................................................................... 114

8 │ 18TH OECD MEETING OF THE HEADS OF NATIONAL INSPECTION SERVICES

OPENING ADDRESSES

The 18th Meeting of the Heads of National Inspection Services was hosted by the Chamber of Commerce of Seville and locally organised by the Seville Centres of SOIVRE, the Inspection Body of the Territorial and Regional Directorate of Trade, under the coordination of the Deputy Directorate of Inspection Certification and Technical Assistance for Foreign Trade, Ministry of Economic Affairs and Competitiveness.

Presentations on this section :

• Opening address 1 by the President of the Chamber of Commerce of Seville

• Opening address 2 by the Regional Trade Director in Andalucía - ICEX (Director of the SOIVRE Centres in Seville)

OPENING ADDRESSES │ 9

Opening address 1

by Mr Francisco Herrero León, President of the Chamber of Commerce of Seville

Dear delegates of the OECD Scheme of Fruits and Vegetables, ladies and gentlemen.

It is an honour for me, as President of the Chamber of Commerce, to host the OECD Heads of Inspection Services Meeting in our home.

One of the most important activities that we have entrusted the Chambers of Commerce is the promotion of the export activity of Spanish companies; therefore, it is a pleasure to receive the Scheme of the OECD Fruits and Vegetables in the Chamber of Commerce of Seville, which contributes to trade facilitation.

I know that the Spanish Administration, in this case the Ministry of Economy, Industry and Competitiveness, and specifically our friends from the Territorial Directorate of Commerce, and the Subdireccion General de Inspección in Madrid, work to facilitate commercial operations, energizing them, promoting them and reinforcing them. Our house is always open to them, and more in this case, for an aim linked to our own objectives as Chamber of Commerce.

When they explained to me exactly what this forum consists of: progress in the standardization of fruits and vegetables, and in the interpretation of these rules, to achieve a common language among operators in order that distance is not an impediment for commercial operations to occur without problems, I was told that commercial quality standards are a common language for international trade, and that it is a way of communicating between the contracting parties of the commercial operation, thus an essential language. But, they also told me how having a good dictionary is essential for having a good language. And they tell me that you are in charge of editing those dictionaries with their interpretative brochures of the norms.

And, although you will already know, let me remind you of the importance of your meticulous and detailed work, since thanks to the development and elaboration of interpretive brochures and inspection guides, the international trade of fruits and vegetables is enormously possible. Can you imagine the international fruit trade without rules and without regulations? It would be chaotic without a doubt.

According to data from the Ministry of Economy, Industry and Competitiveness of Spain, agricultural food exports accounted for EUR 44 542 million in 2016, that is, they accounted for 17.5% of total exports. Within agri-food exports, fruit and vegetable exports accounted for 22.5%. These data speak for themselves about the great importance of the foreign sector of fruits and vegetables for the Spanish economy. Therefore what you are going to decide here is undoubtedly important at the level of the different sectors involved and many decisions are translated into business figures.

I reiterate my welcome and I trust that you will work well and at ease in our house, that these days is yours as well.

10 │ 18TH OECD MEETING OF THE HEADS OF NATIONAL INSPECTION SERVICES

by Mr Francisco Herrero León, President of the Cámara de Comercio de Sevilla

Estimados delegados del Esquema de la OCDE de Frutas y Hortalizas, señoras y señores.

Es un honor para mí, como Presidente de la Cámara de Comercio , el acoger en nuestra casa el Foro de encuentro de los Jefes de los Servicios de Inspección de la OCDE.

Una de las actividades más importantes que tenemos encomendadas las Cámaras de Comercio es el fomento de la actividad exportadora de las empresas españolas, por ello, es un placer recibir al Esquema de la OCDE Frutas y Hortalizas en la Cámara de Comercio de Sevilla, que tanto contribuye a la facilitación del comercio.

Me consta que la Administración española , en este caso el Ministerio de Economía, Industria y Competitividad, y en concreto nuestros amigos de la Dirección Territorial de Comercio, y de la Subdireccion General de Inspección en Madrid, trabajan en post de facilitar las operaciones comerciales, en dinamizarlas, promoverlas y en reforzarlas. Siempre nuestra casa está abierta para ellos, y más en este caso, para un objetivo tan ligado a nuestros propios objetivos como Cámara de Comercio.

Cuando me han explicado en qué consiste exactamente este foro: el progresar en la normalización de las frutas y hortalizas, y en la interpretación de estas normas, para lograr un lenguaje común entre operadores con la finalidad de que la distancia no sea un impedimento para que las operaciones comerciales se produzcan sin problemas, me comentaban que las normas de calidad comercial son un lenguaje común, para el comercio internacional, y que es una manera de comunicarse entre las partes contratantes de la operación comercial, un lenguaje imprescindible. Pero, me comentaban, que tan importante como el lenguaje es tener un buen diccionario. Y me dicen que Ustedes se encargan de editar esos diccionarios con sus folletos interpretativos de las normas.

Y, aunque ya ustedes lo sabrán déjenme recordarles la importancia de su trabajo minucioso y detallado, ya que gracias al desarrollo y la elaboración de folletos interpretativos y guías de inspección, se hace posible enormemente el comercio internacional de frutas y hortalizas. ¿Imaginan el comercio internacional de frutas sin normas y sin reglas? Sería caótico sin duda.

Según datos del Ministerio de Economía, Industria y Competitividad de España, las exportaciones agroalimentarias supusieron en 2016 fueron de 44.542 millones de euros, es decir, representaron el 17.5% de las exportaciones totales. Dentro de las exportaciones agroalimentarias, las exportaciones de fruta y hortalizas significaron el 22,5%. Los datos hablan por sí solos sobre la gran importancia que tiene el sector exterior de frutas y hortalizas para la economía española. Por lo tanto lo que Vds van a decidir aquí sin duda tiene trascendencia a nivel de los distintos sectores implicados y muchas decisiones se traducen en cifras de negocio.

Reitero mi bienvenida y confío que van a trabajar bien y a gusto en nuestra casa, que estos días es la suya.

OPENING ADDRESSES │ 11

Opening address 2

by José Álvarez Calderón, Regional Trade Director in Andalucía - ICEX

Mr Alvarez Calderon (ICEX) took the floor to welcome delegates. He expressed his satisfaction for having the meeting in Andalusia. He stressed the importance of Spain as a major producer and exporter of fresh fruit and vegetables. Indeed, Andalusia is leader in the production of fresh produce. Their exports target not only the EU but also third countries. As an example, he mentioned that Spain exported EUR 8 300 million of fruits in 2017. He also reminded delegates that Spain is committed to the work of the Scheme and that, back in 2013, the photos for the peach brochure were taken here in Seville. To conclude he wished all delegates a fruitful meeting and unforgettable stay in Seville.

12 │ 18TH OECD MEETING OF THE HEADS OF NATIONAL INSPECTION SERVICES

18TH OECD MEETING OF THE HEADS OF NATIONAL INSPECTION SERVICES │ 13

Section summaries

14 │ 18TH OECD MEETING OF THE HEADS OF NATIONAL INSPECTION SERVICES

SECTION I PRESENTATION OF OTHER ORGANISATIONS

The first section is intended to summarise the latest developments in the Fruit and Vegetables quality inspection systems and standardisation activities at the international level. The representative of the WHO/FAO Codex Alimentarius Commission introduced their activities and the latest developments in their programmes of work.

Presentations in the Section:

• Information on recent activities of the Codex Alimentarius Commission on the Standardization of Fresh Fruits and Vegetables

SECTION I. PRESENTATIONS BY OTHER ORGANISATIONS │ 15

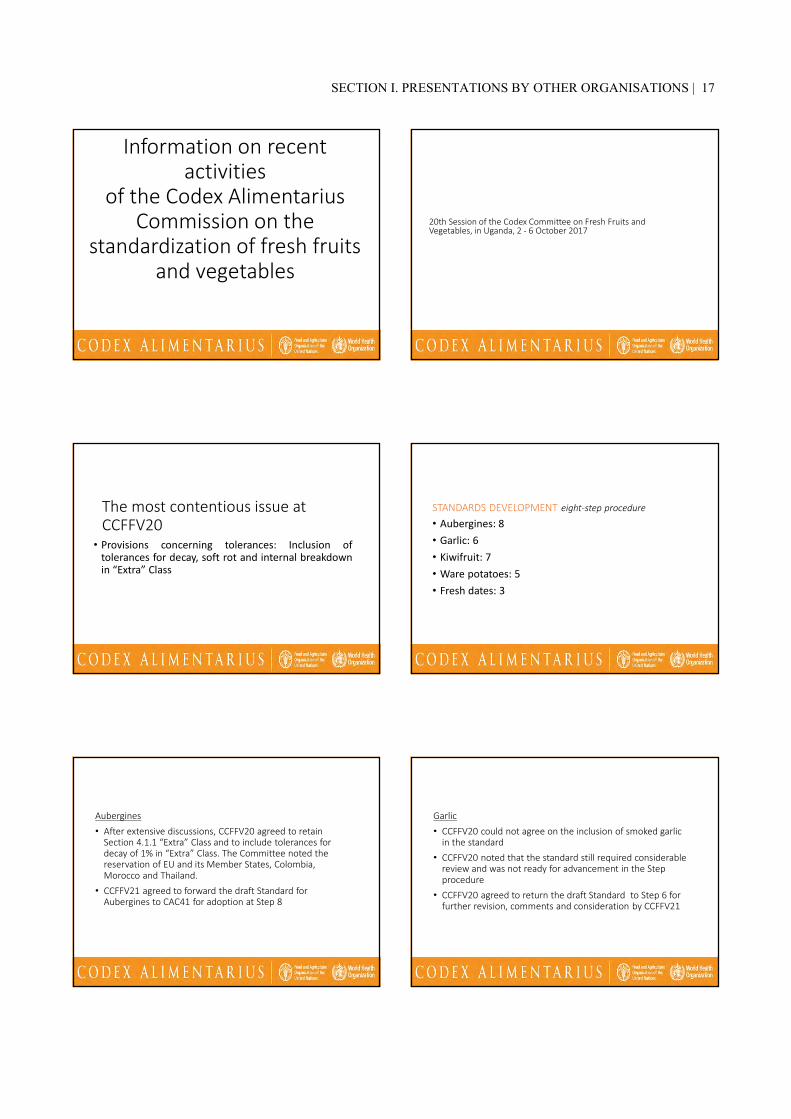

Information on recent activities of the Codex Alimentarius Commission on the standardization of fresh fruits and vegetables

by Ms. Lingping Lingping Zhang, Codex Secretariat

Abstract

Ms. Lingping Zhang from CODEX thanked OECD for the invitation and provided delegates a brief summary of current activities of the CODEX Secretariat; in particular on the outcome of the 20th Session of the Codex Committee on Fresh Fruits and Vegetables held in Uganda on 2-6 October 2017. CODEX also informed delegates of the status of the aubergines, kiwi, garlic, ware potatoes and fresh dates standards. The aubergine standard has been put forward for adoption at step 8, while the other standards is currently at steps 7, 6, 5 and 3 respectively. New work is under development for yam, onions and shallots, and berry fruits.

On other issues, CODEX will be further discussing the glossary of terms associated with the proposed standard layout as well as other terms used in Codex standards for fresh fruits and vegetables. The exact time and venue of the next 21st Session of the Codex Committee on Fresh Fruits and Vegetables will be announced in due course.

16 │ 18TH OECD MEETING OF THE HEADS OF NATIONAL INSPECTION SERVICES

Information on recent activities of the Codex Alimentarius Commission on the standardization of fresh fruits and vegetables

Presentation by Ms. Lingping Lingping Zhang, Codex Secretariat

Information on recent activities

of the Codex Alimentarius Commission on the

standardization of fresh fruits and vegetables

20th Session of the Codex Committee on Fresh Fruits and Vegetables, in Uganda, 2 - 6 October 2017

The most contentious issue at CCFFV20

• Provisions concerning tolerances: Inclusion oftolerances for decay, soft rot and internal breakdownin “Extra” Class

STANDARDS DEVELOPMENT eight-step procedure

• Aubergines: 8• Garlic: 6• Kiwifruit: 7• Ware potatoes: 5• Fresh dates: 3

Aubergines• After extensive discussions, CCFFV20 agreed to retain

Section 4.1.1 “Extra” Class and to include tolerances for decay of 1% in “Extra” Class. The Committee noted the reservation of EU and its Member States, Colombia, Morocco and Thailand.

• CCFFV21 agreed to forward the draft Standard for Aubergines to CAC41 for adoption at Step 8

Garlic• CCFFV20 could not agree on the inclusion of smoked garlic

in the standard• CCFFV20 noted that the standard still required considerable

review and was not ready for advancement in the Step procedure

• CCFFV20 agreed to return the draft Standard to Step 6 for further revision, comments and consideration by CCFFV21

SECTION I. PRESENTATIONS BY OTHER ORGANISATIONS | 17

Kiwifruit• CCFFV20 could not agree on the allowance for tolerance for

decay, soft rot and internal breakdown in Class I and “Extra” Class

• CCFFV20 agreed to hold the standard at Step 7 and that no further comments would be requested nor discussion on the standard would be held at its next session with the exception of the discussion on tolerances for decay, soft rot and internal breakdown

Ware potatoesCCFFV20 agreed although some issues needed to be further discussed, especially minimum requirements and Table of tolerances, substantial progress had been made on the standard; therefore, the document was ready to progress in the Step Procedure.CCFFV20 agreed to forward the proposed draft Standard to CAC for adoption at Step 5

Fresh datesCCFFV20 agreed although some issues needed to be further discussed, especially minimum requirements and Table of tolerances, substantial progress had been made on the standard; therefore, the document was ready to progress in the Step Procedure.CCFFV20 agreed to return the proposed draft Standard to Step 3, for further revision and consideration by CCFFV21

NEW WORK ON STANDARD DEVELOPMENT

CCFFV21 agreed to recommend approval of three proposals on new work i.e. yam, onions and shallots, and berry fruits.

SUPPORTING DOCUMENT FOR STANDARD DEVELOPMENTProposed Standard Layout for Codex Standards for Fresh Fruits and Vegetables:

CCFFV20 noted that the layout was a guidance document to facilitate development and discussion of standards for fresh fruits and vegetables, and did not have any status in Codex (i.e. it was not a Codex text) and thus did not require approval or adoption by CAC but only the agreement of CCFFV.

SUPPORTING DOCUMENT FOR STANDARD DEVELOPMENT

Glossary of Terms:

CCFFV20 agreed to further develop the discussion paper onglossary of terms associated with the proposed standard layout as well as other terms used in Codex standards for fresh fruits and vegetables for consideration at CCFFV21.

18 | 18TH OECD MEETING OF THE HEADS OF NATIONAL INSPECTION SERVICES

OTHERS• Revision of the meeting interval for CCFFV: every 12 months• Post-harvest treatment for fresh fruits and vegetables for referral to

CCFA• Use of effective communicative tools and quality of the simultaneous

translation

The exact time and venue of CCFFV21 would be determined in due course

YT(1

END

SECTION I. PRESENTATIONS BY OTHER ORGANISATIONS | 19

20 │ 18TH OECD MEETING OF THE HEADS OF NATIONAL INSPECTION SERVICES

SECTION II FRUIT SECTOR IN SPAIN

The aim of this section is to leave the host the opportunity to widely present its fruit and vegetables sector.

Presentations in the Section:

• Spanish fresh fruit and vegetables sector

• Spanish Citrus industry – Production, challenges and perspectives

SECTION II. FRUIT SECTOR IN SPAIN │ 21

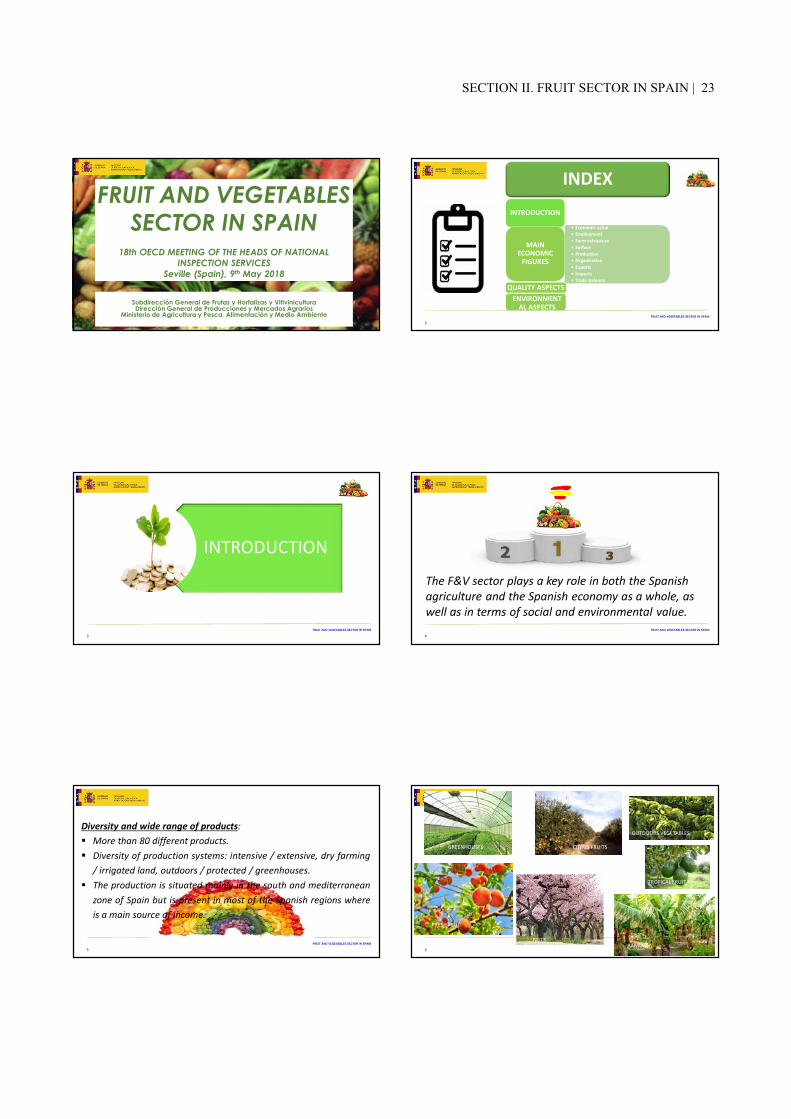

Spanish fresh fruits and vegetables sector

by Ms Leonor de Castro, Subdirección General de Frutas y Hortalizas y Vitivinicultura, Dirección General de Producciones y Mercados Agrarios, Ministerio de Agricultura y

Pesca, Alimentación y Medio Ambiente

Abstract

The fruit and vegetables sector plays a key role in both the Spanish agriculture and the Spanish economy as a whole, as well as in terms of social and environmental value.

Spain produces more than 80 different products. Production uses a wide variety of systems: intensive, extensive, dry farming, irrigated land, outdoors, protected, and greenhouses. Production is located mainly in the south and Mediterranean zones of Spain but can be found in most of the Spanish regions where is a main source of income, generating 100 000 indirect employments related to handling and packaging.

In 2017, production amounted to EUR 14 500 million, with 50% coming from crop production. The sector is continuously increasing its economic value, and Spain is the main fruit and vegetables producer of the European Union and the 5th worldwide (in terms of value).

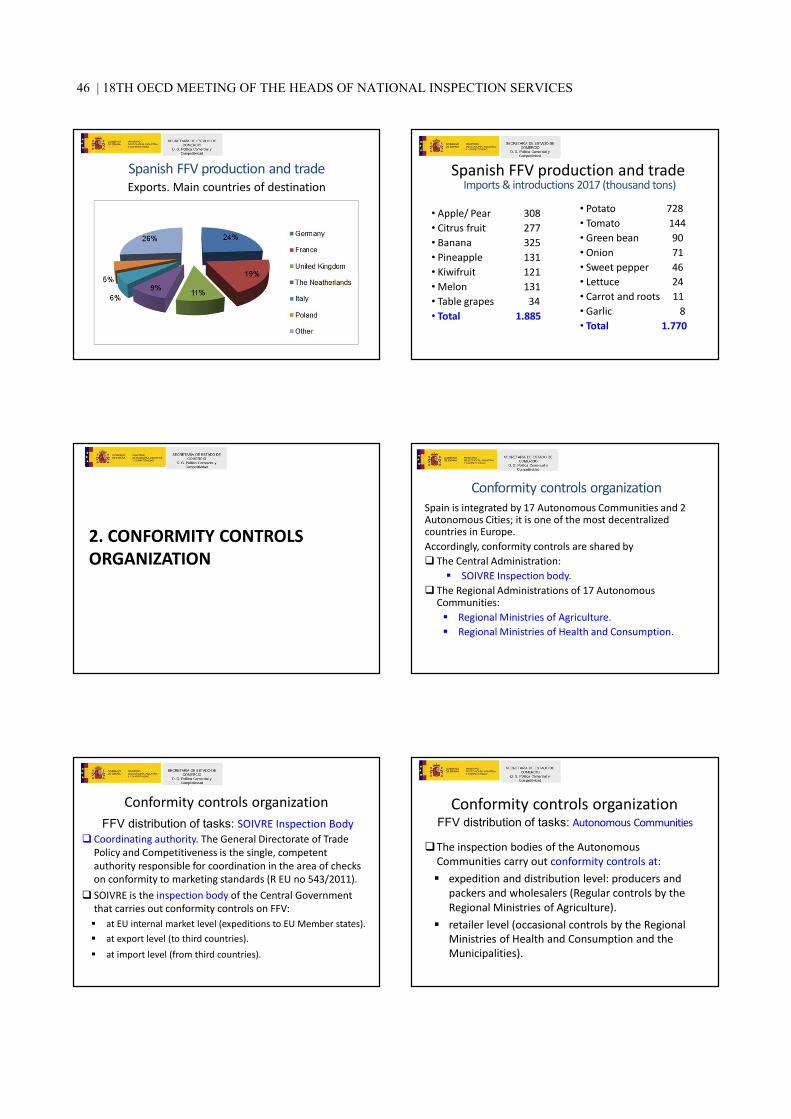

Around 50% of production is exported, but in some particular cases even more than 70% are destined to foreign markets. The main products that are exported are vegetables from greenhouses (tomatoes, pepper and cucumber), citrus fruit, peaches and nectarines. From exports, 93% go to the EU market (Germany, France, United Kingdom and the Netherlands).

Imports are modest, but with an increasing trend. Nowadays, 45% of imports have EU origin (France and Portugal mainly) and 55% come from third countries (Morocco, USA, Mercosur). The main imported products are potatoes, tomatoes, green beans, banana, pineapple and kiwifruit.

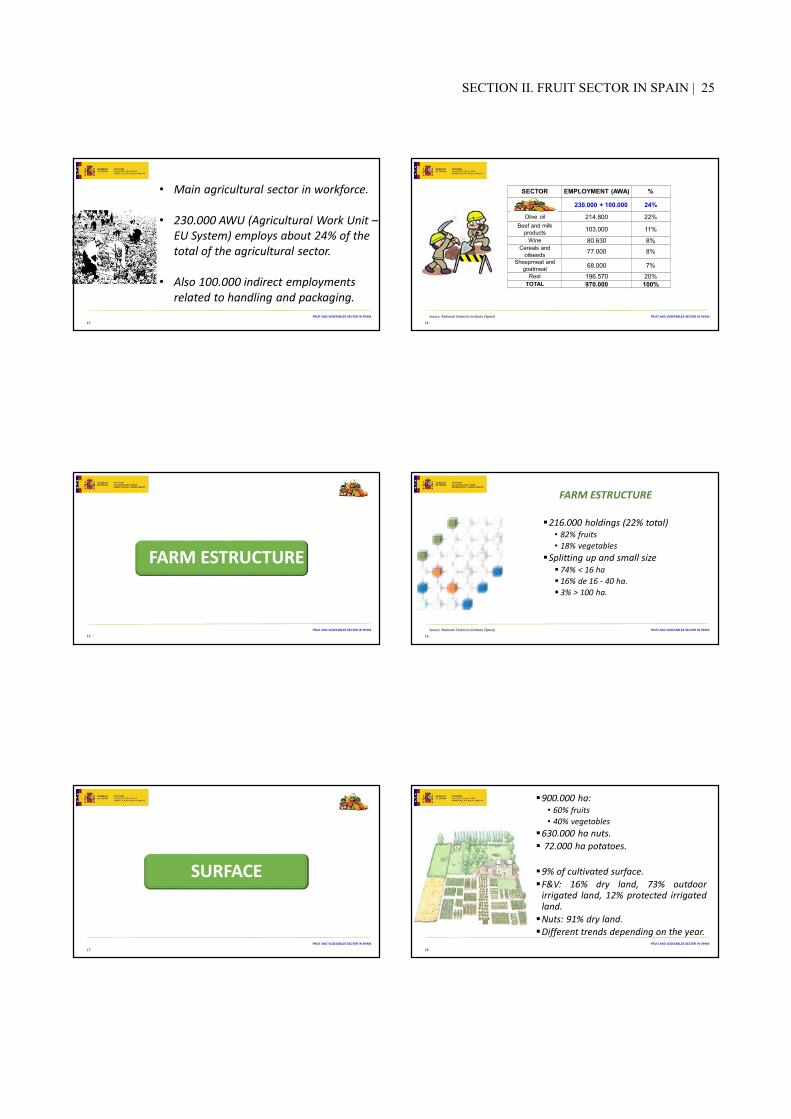

Farm structure in Spain has a total of 216 000 holdings of which 82% focus on fruits and 18% on vegetables. Amongst farms, 74% have less than 16 ha, 16% go from 16 - 40 ha, and only 3% possess more than 100 ha.

In 2016, a total of 896 518 ha were dedicated to the cultivation of citrus fruit, tropical fruit, fresh fruit, table grape sand bananas. Integrated Production covers 119 763 ha (8% of F&V Surface) distributed as follows: Fresh fruit 41%, Citrus fruit 29%, Tropical fruit 18%, Vegetables 11%, Nuts 8%, and Bananas 3%. Another important aspect of the Spanish fruit and vegetable sector is a positive trend on Organic Farming. Currently, 120 694 ha (8% of F&V Surface) are devoted to organic production, distributed as follows: Nuts 78%, Vegetables 10%, Citrus fruit 6%, Fresh fruit 4%, Tropical fruit 2%, and Bananas 2%.

It is also worth highlighting that in Spain, producer members are obliged to market their entire production through the Producers Organisations (POs). Indeed, 50% of production is marketed through POs.

22 │ 18TH OECD MEETING OF THE HEADS OF NATIONAL INSPECTION SERVICES

Spanish fresh fruits and vegetables sector

Presentation by Ms Leonor de Castro, Subdirección General de Frutas y Hortalizas y Vitivinicultura, Dirección General de Producciones y Mercados Agrarios, Ministerio de

Agricultura y Pesca, Alimentación y Medio Ambiente

FRUIT AND VEGETABLES SECTOR IN SPAIN

1

FRUIT AND VEGETABLES SECTOR IN SPAIN

18th OECD MEETING OF THE HEADS OF NATIONAL INSPECTION SERVICES

Seville (Spain), 9th May 2018

Subdirección General de Frutas y Hortalizas y VitiviniculturaDirección General de Producciones y Mercados Agrarios

Ministerio de Agricultura y Pesca, Alimentación y Medio Ambiente FRUIT AND VEGETABLES SECTOR IN SPAIN

2

INDEXINTRODUCTION

• Economic value• Employment• Farm estructure• Surface• Production• Organisation• Exports• Imports• Trade balance

MAIN ECONOMIC

FIGURES

QUALITY ASPECTSENVIRONMENT

AL ASPECTS

FRUIT AND VEGETABLES SECTOR IN SPAIN

3

INTRODUCTION

FRUIT AND VEGETABLES SECTOR IN SPAIN

4

The F&V sector plays a key role in both the Spanish agriculture and the Spanish economy as a whole, as well as in terms of social and environmental value.

FRUIT AND VEGETABLES SECTOR IN SPAIN

5

Diversity and wide range of products:More than 80 different products.Diversity of production systems: intensive / extensive, dry farming/ irrigated land, outdoors / protected / greenhouses.The production is situated mainly in the south and mediterraneanzone of Spain but is present in most of the Spanish regions whereis a main source of income.

FRUIT AND VEGETABLES SECTOR IN SPAIN

6

GREENHOUSES CITRUS FRUITS

FRESH FRUIT

NUTS

TROPICAL FRUIT

BANANA

OUTDOORS VEGETABLES

SECTION II. FRUIT SECTOR IN SPAIN | 23

FRUIT AND VEGETABLES SECTOR IN SPAIN

7

MAIN ECONOMIC

FIGURESFRUIT AND VEGETABLES SECTOR IN SPAIN

8

ECONOMIC VALUE

FRUIT AND VEGETABLES SECTOR IN SPAIN

9

14.500 M€ in 201750% of Crop Production

30% of Agricultural Production (including crop and animal production)

FRUIT AND VEGETABLES SECTOR IN SPAIN

10

Fuente: SG Estadística, MAPAMA y Eurostat

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2010 2011 2012 2013 2014 2015 2016 2017

EVOLUTION OF THE F&V PRODUCTION IN SPAIN (M€)

Vegetables Potatoes Fruits TOTAL

FRUIT AND VEGETABLES SECTOR IN SPAIN

11

With an increasing economic value, SPAIN is the main F&V producer of the European Union and the 5th worldwide (in terms of value).

SPAIN 19%

ITALY 18%

NETHERLANDS16%FRANCE 15%

GERMANY 10%

RESTO 22%

RANKING OF EU MAIN MSs F&V PRODUCERS (value)

TOTAL VALUE UE (2016): 73.386 M€

FRUIT AND VEGETABLES SECTOR IN SPAIN

12

EMPLOYMENT

24 | 18TH OECD MEETING OF THE HEADS OF NATIONAL INSPECTION SERVICES

FRUIT AND VEGETABLES SECTOR IN SPAIN

13

• Main agricultural sector in workforce.

• 230.000 AWU (Agricultural Work Unit –EU System) employs about 24% of the total of the agricultural sector.

• Also 100.000 indirect employments related to handling and packaging.

FRUIT AND VEGETABLES SECTOR IN SPAIN

14

SECTOR EMPLOYMENT (AWA) %FRUTAS Y

HORTALIZAS 230.000 + 100.000 24%

Olive oil 214.800 22%Beef and milk

products 103.000 11%Wine 80.630 8%

Cereals and oilseeds 77.000 8%

Sheepmeat and goatmeat 68.000 7%

Rest 196.570 20%TOTAL 970.000 100%

Source: National Statistics Institute (Spain)

FRUIT AND VEGETABLES SECTOR IN SPAIN

15

FARM ESTRUCTURE

FRUIT AND VEGETABLES SECTOR IN SPAIN

16

216.000 holdings (22% total)• 82% fruits• 18% vegetables

Splitting up and small size74% < 16 ha16% de 16 - 40 ha.3% > 100 ha.

FARM ESTRUCTURE

Source: National Statistics Institute (Spain)

FRUIT AND VEGETABLES SECTOR IN SPAIN

17

SURFACE

FRUIT AND VEGETABLES SECTOR IN SPAIN

18

900.000 ha:• 60% fruits• 40% vegetables

630.000 ha nuts.72.000 ha potatoes.

9% of cultivated surface.F&V: 16% dry land, 73% outdoorirrigated land, 12% protected irrigatedland.Nuts: 91% dry land.Different trends depending on the year.

SECTION II. FRUIT SECTOR IN SPAIN | 25

FRUIT AND VEGETABLES SECTOR IN SPAIN

19Fuente: Anuario de Estadística MAPAMA

2010 2011 2012 2013 2014 2015 2016

Vegetables 363.729 351.145 348.359 348.853 346.262 347.824 359.868

Citrus fruit 319.163 317.605 311.542 306.303 301.124 298.724 295.331

Fresh fruit 198.118 200.673 200.376 200.168 201.640 201.481 201.316

Tropical fruit 18.990 19.106 19.121 19.833 20.101 19.698 17.456

Table grapes 16.226 15.175 14.548 13.742 14.403 14.034 13.507

Banana 9.117 9.144 9.144 9.131 9.130 9.100 9.040

Total 925.343 912.848 903.090 898.030 892.660 890.861 896.518

Nuts 646.026 631.033 630.106 636.148 630.674 657.611 697.736

Potatoes 77.622 79.865 72.023 71.100 76.100 72.100 73.200

TOTAL 1.648.991 1.623.746 1.605.219 1.605.278 1.599.434 1.620.572 1.667.454

SURFACE (has)

FRUIT AND VEGETABLES SECTOR IN SPAIN

20

PRODUCTION

FRUIT AND VEGETABLES SECTOR IN SPAIN

21

Around 27 million tonnes per year.

52% vegetables, 40% fruits, 8% potaoes.

Spain is the main EU F&V producer accountingwith 26% of the total production.

Spain is the 5th main world producer with 3%of world production (after China, India, USAand Turkey).

PRODUCTION

FRUIT AND VEGETABLES SECTOR IN SPAIN

22Fuente: Anuario de Estadística MAPAMA

2011 2012 2013 2014 2015 2016 % 16 / 15

% 16 /11-15

Vegetables 12.972.604 13.282.939 13.201.085 14.174.385 14.337.646 14.943.484 4% 10%Potatoes 2.455.100 2.200.800 2.199.600 2.544.000 2.245.600 2.244.335 0% -4%Citrus fruit 5.736.197 5.567.672 6.330.040 7.047.335 5.970.493 7.085.819 19% 16%Non citrus fruit 2.928.782 2.552.100 2.669.840 3.100.332 3.000.617 2.854.690 -5% 0’2%

Tropical fruit 225.278 178.139 149.956 169.324 164.988 183.521 11% 3%

Table grapes 241.209 254.258 232.965 280.670 251.786 271.602 8% 8%

Banana 346.500 371.200 361.000 363.602 381.983 421.675 10% 16%Nuts 452.410 441.576 386.219 450.504 445.511 438.579 -2% 1%

TOTAL 25.358.080 24.848.684 25.530.705 28.130.152 26.798.624 28.443.705 6% 9%

PRODUCTION (tonnes)

FRUIT AND VEGETABLES SECTOR IN SPAIN

23Fuente: Anuario de Estadística MAPAMA

PRODUCTION

VEGETABLES 52%

POTATOS 9%

CITRUS FRUIT 24%

FRESH FRUIT11%

TROPICAL FRUIT 1%

TABLE GRAPES 1% BANANAS 1%NUTS 2%

MAIN GROUP OF PRODUCTS (%)

Average 2012-2016

FRUIT AND VEGETABLES SECTOR IN SPAIN

24

GEOGRAPHIC DISTRIBUTION OF F&V PRODUCTION (volume)

26 | 18TH OECD MEETING OF THE HEADS OF NATIONAL INSPECTION SERVICES

FRUIT AND VEGETABLES SECTOR IN SPAIN

25

ORGANISATION

FRUIT AND VEGETABLES SECTOR IN SPAIN

26

568 recognised for the F&V sector (EUregulation).

Objectives: concentration of supply,adaptation of production to demand,optimising production costs.

Producer members are obliged to market theirentire production through the PO.

50% of production is marketed through POs.

FRUIT AND VEGETABLES SECTOR IN SPAIN

27

640 633 639 608598 596 596 585 574 569 568

0

50

100

150

200

250

300

350

400

450

500

550

600

650

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

0%

10%

20%

30%

40%

50%

60%

70%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

PRODUCTION MARKETED BY POs

NUMBER OF PRODUCER ORGANISATIONS

FRUIT AND VEGETABLES SECTOR IN SPAIN

28

EXTERNAL TRADE

FRUIT AND VEGETABLES SECTOR IN SPAIN

29

F&V is one of the maineconomic sectors in thetotal spanish exports .

F&V is the agri – food andfisheries spanish exportsleader.

FRUIT AND VEGETABLES SECTOR IN SPAIN

30

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000

MELTING AND STEEL PRODUCTS

TEXTILE

FRUIT AND VEGETABLES

FUELS

CHEMICAL

MOTOR VEHICLES

MAIN SPANISH EXPORTS BY SECTOR (million €)

SECTION II. FRUIT SECTOR IN SPAIN | 27

FRUIT AND VEGETABLES SECTOR IN SPAIN

31

Spain is the main EU exporter and the 3rd world exporter(after China and USA).

Positive trend.

Around 50% of production is exported; more than 70% incertain products such as vegetables from greenhouse,lettuce or lemon.

Main exported product: vegetables from greenhouse(tomatoes, pepper and cucumber), citrus fruit, peachesand nectarines.

EXPORTS

FRUIT AND VEGETABLES SECTOR IN SPAIN

32Fuente: DATACOMEX

EXPORTS

9,649

14,327

6,000

9,000

12,000

15,000

2011 2012 2013 2014 2015 2016 2017

VALUE OF F&V EXPORTS (millIon de €)

FRUIT AND VEGETABLES SECTOR IN SPAIN

33

93% of destination of exports arethe EU market (Germany, France,United Kigdom and theNetherlands)

EXPORTS

FRUIT AND VEGETABLES SECTOR IN SPAIN

34

Average volume (EU): 12,6 million t

EXPORTS

INTRA-EU; 93%

F&V EXPORTS BY DESTINATION (volumen t)

26%

19%

13%

8%

34%

0%

5%

10%

15%

20%

25%

30%

35%

40%

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

GERMANY FRANCE UNITEDKINGDOM

NETHERLANDS REST

F&V EXPORTS TO EU INTERNAL MARKET BY MEMBER STATES

Volume (t) %

FRUIT AND VEGETABLES SECTOR IN SPAIN

35

Imports are less important tan exports.

Incresing trend.

45% of imports have EU origin (France and Portugalmainly) and 55% third countries (Morocco, USA,Mercosur).

Main imported products: potatoes, tomatoes, greenbeans, banana, pineapple and kiwifruit.

IMPORTS

FRUIT AND VEGETABLES SECTOR IN SPAIN

36

IMPORTS

2,444

4,008

-

1,000

2,000

3,000

4,000

2011 2012 2013 2014 2015 2016 2017

VALUE OF F&V IMPORTS (millIon de €)

28 | 18TH OECD MEETING OF THE HEADS OF NATIONAL INSPECTION SERVICES

FRUIT AND VEGETABLES SECTOR IN SPAIN

37

Average of total imports: 3,4 milion t

IMPORTS

INTRA-UE, 55%

F&V IMPORTS BY ORIGIN (volume t)

26%

11%

5% 4%

9% 8%6% 4% 3% 3%

20%

0%

5%

10%

15%

20%

25%

30%

0

200,000

400,000

600,000

800,000

1,000,000

F&V IMPORTS BY ORIGIN

Volume (t) %

FRUIT AND VEGETABLES SECTOR IN SPAIN

38

POSITIVE trade balance (around 10.000 million €);increasing trend.

F&V is the main contributor to the positive balance ofthe agri – food sector: 30% of exports, 8% of imports;358% coverage ratio.

F&V exports means 5% of total spanish exports.

TRADE BALANCE

FRUIT AND VEGETABLES SECTOR IN SPAIN

39

TRADE BALANCE

-

3,000

6,000

9,000

12,000

15,000

EXPORTS

IMPORTS

TRADE BALANCE

14,327

4,008

10,319

F&V TRADE BALANCE (million €)

2011 2012 2013 2014 2015 2016 2017

FRUIT AND VEGETABLES SECTOR IN SPAIN

40

QUALITY ASPECTS

FRUIT AND VEGETABLES SECTOR IN SPAIN

41

Compliance with EU marketing standards (1 general MS + 10specifi MS), CEPE – ONU y Codex Alimentarius.

Innovation to introduce plant selection with allows offeradaptation to new demands of consumers: new products,season enlargement,…

EU Quality Schemes: Protected Designation of Origin (PDO)and Prtected Geographical Origin (PGI): 25 for fruits and 19 forvegetables(24% of total).

FRUIT AND VEGETABLES SECTOR IN SPAIN

42

VEGETABLES

SECTION II. FRUIT SECTOR IN SPAIN | 29

FRUIT AND VEGETABLES SECTOR IN SPAIN

43

FRUITS

FRUIT AND VEGETABLES SECTOR IN SPAIN

44

ENVIRONMENTAL ASPECTS

FRUIT AND VEGETABLES SECTOR IN SPAIN

45

INTEGRATED PRODUCTION: 119.763 Ha (8% of F&V Surface) distributed as follows:Fresh fruit 41%Citrus fruit 29%Tropical fruit 18%Vegetables 11%Nuts 8%Banana 3%

ORGANIC FARMING: 120.694 Ha (8% of F&V Surface) distributed as follows:Nuts 78%Vegetables 10%Citrus fruit 6%Fresh fruit 4%Tropical fruit 2%Banana 2%

POSITIVE TREND

FRUIT AND VEGETABLES SECTOR IN SPAIN

46

ENVIRONMENTALLY FRIENDLY PRODUCTION

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

VEGETABLES CITRUS FRUIT FRESH FRUIT TROPICAL FRUIT BANANA NUTS

% INTEGRATED PRODUCTION / total % ORGANIC FARMING / total

Surface

47

THANK YOU VERY MUCH FOR YOUR

ATTENTIONS.G DE FRUTAS Y HORTALIZAS Y VITIVINICULTURAC/ Almagro, 33, 6ª planta. MADRIDTf: 913476718 E-mail: [email protected]

30 | 18TH OECD MEETING OF THE HEADS OF NATIONAL INSPECTION SERVICES

SECTION II. FRUIT SECTOR IN SPAIN │ 31

Spanish Citrus industry – Production, challenges and perspectives

by Ms Immaculada Sanfeliu Felui, Head of Comité de Gestión de Cítricos

Abstract

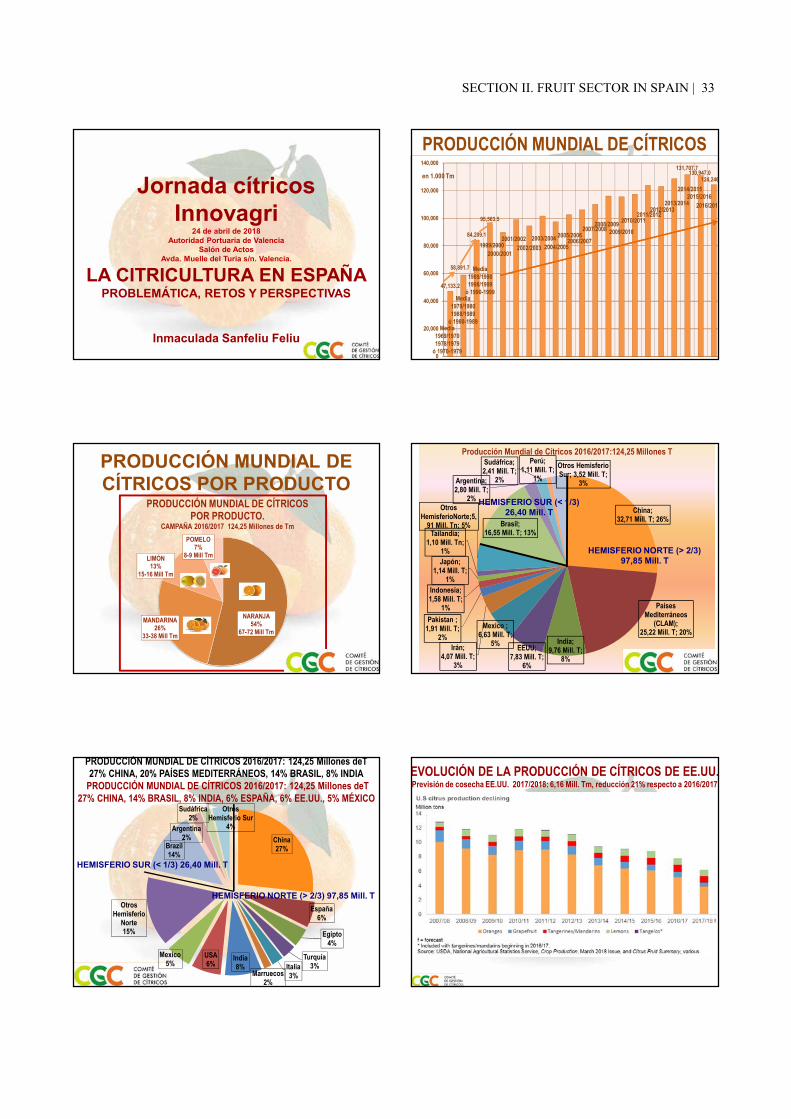

In 2017 the world produced 124.25 million tonnes of citrus. From those, 54% were oranges, 26% tangerines, 13% lemons and 7% grapefruit.

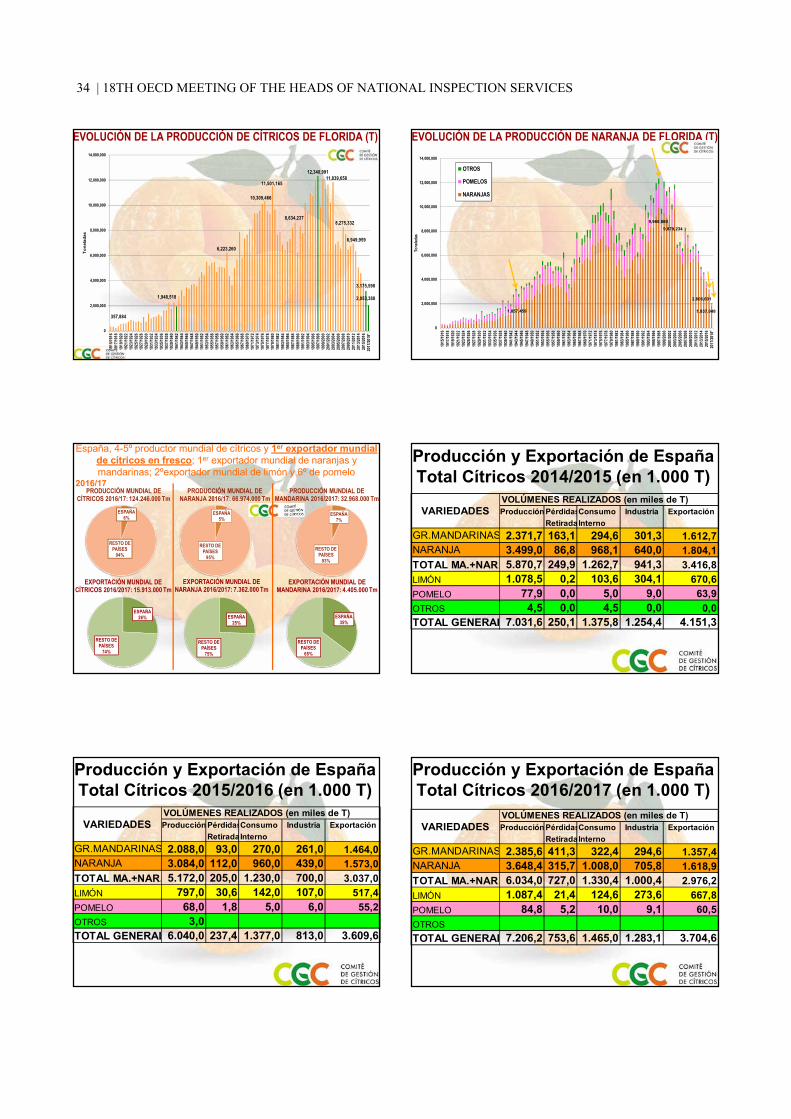

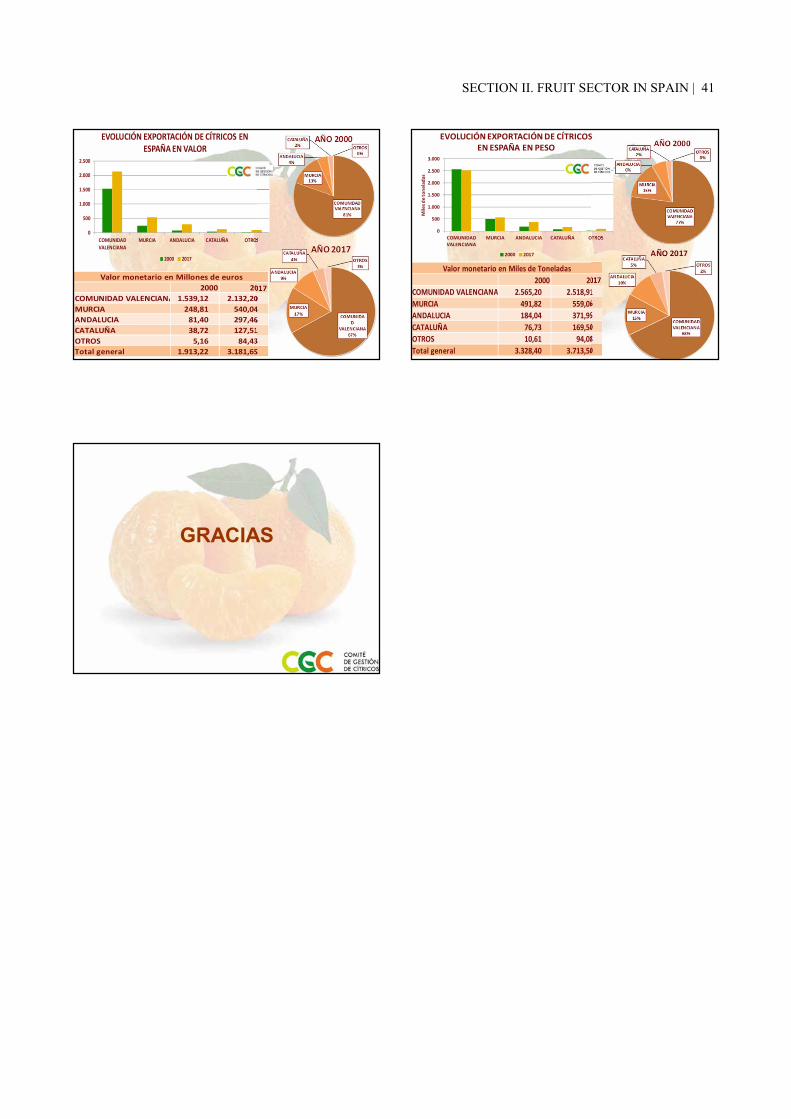

In terms of producing countries, China has the lead generating 27% of all citrus production, followed by Brazil (14%), India (8%) and Spain (6%). This said, the last forecast for 2018 warned of a 21% fall in production with respect to the previous year. Pests and adverse climate situations have contributed to the production shortage around the globe.

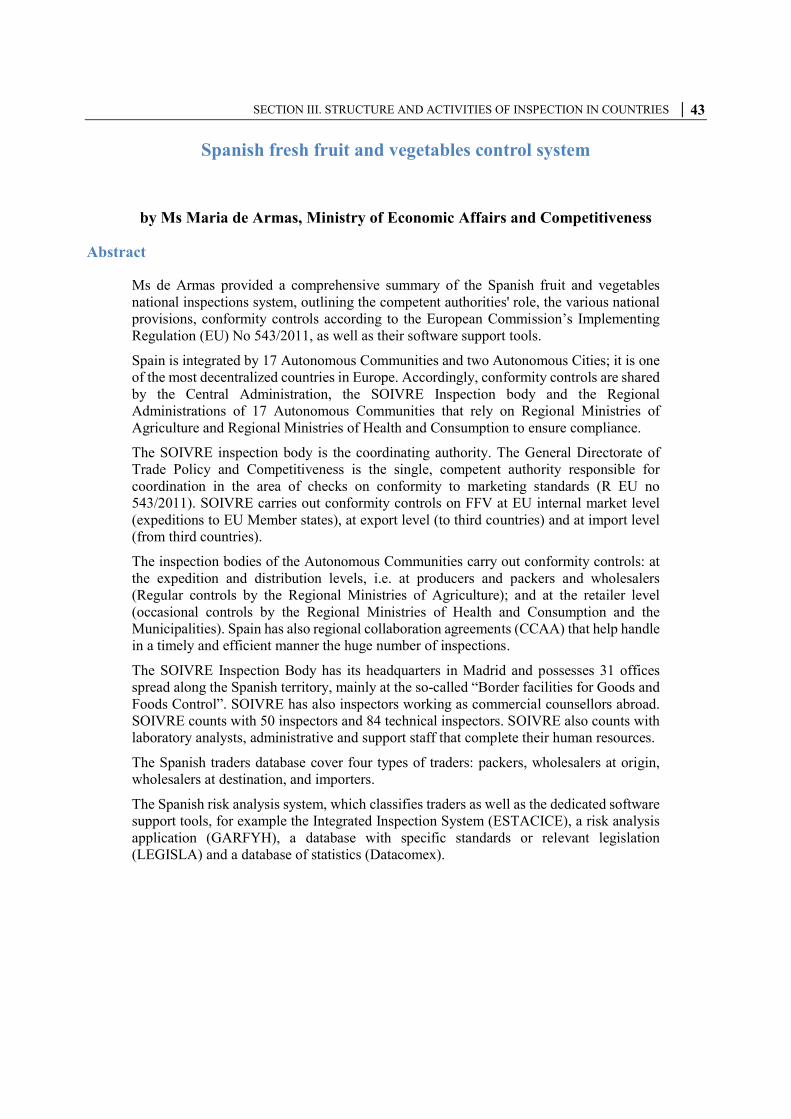

Although Spain is the 4th or 5th global producer, it is the first exporter of oranges and tangerines worldwide. Exporting on average 3 704 000 tonnes in 2017 and dedicating a total of 299 518 ha to cultivate citrus. From those, 50% are used for oranges, 37% to tangerines, and 13% to lemons.

Inside Spain, Valencia produces 54% of all Spanish citrus production, followed by Andalusia (28%), Murcia (14%), Cataluña (4%) and the rest in Baleares and other regions.

In the case of the European Union, Spain supplies 80% of tangerines and 69% of oranges making it the largest supplier of citrus to the continent. The main destination markets are Germany (28%), France (23%), The UK (9%) and the Netherlands (6%).

Outside the EU, Spain’s main destination markets are Switzerland, the US and Canada. The key months for exports go from November to February every year

In monetary terms, citrus exports amounted to EUR 3 181 million last year.

32 │ 18TH OECD MEETING OF THE HEADS OF NATIONAL INSPECTION SERVICES

Spanish Citrus industry – Production, challenges and perspectives

Presentation by Ms Immaculada Sanfeliu Felui, Head of Comité de Gestión de Cítricos

Inmaculada Sanfeliu Feliu

Jornada cítricosInnovagri

24 de abril de 2018Autoridad Portuaria de Valencia

Salón de ActosAvda. Muelle del Turia s/n. Valencia.

LA CITRICULTURA EN ESPAÑAPROBLEMÁTICA, RETOS Y PERSPECTIVAS

47,133.2

58,891.7

84,209.1

95,563.5

131,707.7130,947.0

124,246

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

Media1979/19801988/1989

ó 1980-1989

Media1989/19901998/1999

ó 1990-1999

Media1969/19701978/1979

ó 1970-1979

1999/20002000/2001

2001/20022002/2003

2003/20042004/2005

2005/20062006/2007

2007/20082008/2009

2009/2010

en 1.000 Tm

2010/20112011/2012

2012/20132013/2014

2014/20152015/2016

2016/2017

PRODUCCIÓN MUNDIAL DE CÍTRICOS

PRODUCCIÓN MUNDIAL DE CÍTRICOS POR PRODUCTO

NARANJA54%

67-72 Mill TmMANDARINA

26%33-38 Mill Tm

LIMÓN13%

15-16 Mill Tm

POMELO7%

8-9 Mill Tm

PRODUCCIÓN MUNDIAL DE CÍTRICOS POR PRODUCTO.

CAMPAÑA 2016/2017 124,25 Millones de Tm

China; 32,71 Mill. T; 26%

Países Mediterráneos

(CLAM); 25,22 Mill. T; 20%

India; 9,76 Mill. T;

8%EEUU;

7,83 Mill. T; 6%

Mexico ; 6,63 Mill. T;

5%Irán; 4,07 Mill. T;

3%

Pakistan ; 1,91 Mill. T;

2%

Indonesia; 1,58 Mill. T;

1%

Japón; 1,14 Mill. T;

1%

Tailandia; 1,10 Mill. Tn;

1%

Otros HemisferioNorte;5,

91 Mill. Tn; 5% Brasil; 16,55 Mill. T; 13%

Argentina; 2,80 Mill. T;

2%

Sudáfrica; 2,41 Mill. T;

2%

Perú; 1,11 Mill. T;

1%Otros Hemisferio Sur; 3,52 Mill. T;

3%

Producción Mundial de Cítricos 2016/2017:124,25 Millones T

HEMISFERIO SUR (< 1/3) 26,40 Mill. T

HEMISFERIO NORTE (> 2/3) 97,85 Mill. T

PRODUCCIÓN MUNDIAL DE CÍTRICOS 2016/2017: 124,25 Millones deT27% CHINA, 20% PAÍSES MEDITERRÁNEOS, 14% BRASIL, 8% INDIA

PRODUCCIÓN MUNDIAL DE CÍTRICOS 2016/2017: 124,25 Millones deT27% CHINA, 14% BRASIL, 8% INDIA, 6% ESPAÑA, 6% EE.UU., 5% MÉXICO

China27%

España6%

Egipto4%

Turquía3%Italia

3%Marruecos2%

India8%

USA6%

Mexico 5%

Otros Hemisferio

Norte15%

Brazil14%

Argentina2%

Sudáfrica2%

Otros Hemisferio Sur

4%

HEMISFERIO SUR (< 1/3) 26,40 Mill. T

HEMISFERIO NORTE (> 2/3) 97,85 Mill. T

EVOLUCIÓN DE LA PRODUCCIÓN DE CÍTRICOS DE EE.UU.Previsión de cosecha EE.UU. 2017/2018: 6,16 Mill. Tm, reducción 21% respecto a 2016/2017

SECTION II. FRUIT SECTOR IN SPAIN | 33

EVOLUCIÓN DE LA PRODUCCIÓN DE CÍTRICOS DE FLORIDA (T)

357,884

1,948,518

6,223,260

10,309,466

11,501,165

8,634,237

12,340,99111,839,658

8,275,332

6,949,959

3,175,598

2,053,388

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

1915

/1916

1917

/1918

1919

/1920

1921

/1922

1923

/1924

1925

/1926

1927

/1928

1929

/1930

1931

/1932

1933

/1934

1935

/1936

1937

/1938

1939

/1940

1941

/1942

1943

/1944

1945

/1946

1947

/1948

1949

/1950

1951

/1952

1953

/1954

1955

/1956

1957

/1958

1959

/1960

1961

/1962

1963

/1964

1965

/1966

1967

/1968

1969

/1970

1971

/1972

1973

/1974

1975

/1976

1977

/1978

1979

/1980

1981

/1982

1983

/1984

1985

/1986

1987

/1988

1989

/1990

1991

/1992

1993

/1994

1995

/1996

1997

/1998

1999

/2000

2001

/2002

2003

/2004

2005

/2006

2007

/2008

2009

/2010

2011

/2012

2013

/2014

2015

/2016

2017

/2018

*

Tone

lada

s

EVOLUCIÓN DE LA PRODUCCIÓN DE NARANJA DE FLORIDA (T)

1,857,459

9,960,8809,879,234

2,806,601

1,837,048

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

1915

/1916

1917

/1918

1919

/1920

1921

/1922

1923

/1924

1925

/1926

1927

/1928

1929

/1930

1931

/1932

1933

/1934

1935

/1936

1937

/1938

1939

/1940

1941

/1942

1943

/1944

1945

/1946

1947

/1948

1949

/1950

1951

/1952

1953

/1954

1955

/1956

1957

/1958

1959

/1960

1961

/1962

1963

/1964

1965

/1966

1967

/1968

1969

/1970

1971

/1972

1973

/1974

1975

/1976

1977

/1978

1979

/1980

1981

/1982

1983

/1984

1985

/1986

1987

/1988

1989

/1990

1991

/1992

1993

/1994

1995

/1996

1997

/1998

1999

/2000

2001

/2002

2003

/2004

2005

/2006

2007

/2008

2009

/2010

2011

/2012

2013

/2014

2015

/2016

2017

/2018

*

Tone

ladas

OTROS

POMELOS

NARANJAS

España, 4-5º productor mundial de cítricos y 1er exportador mundial de cítricos en fresco; 1er exportador mundial de naranjas y mandarinas; 2ºexportador mundial de limón y 6º de pomelo

2016/17

ESPAÑA6%

RESTO DE PAÍSES

94%

PRODUCCIÓN MUNDIAL DE CÍTRICOS 2016/17: 124.246.000 Tm

ESPAÑA26%

RESTO DE PAÍSES

74%

EXPORTACIÓN MUNDIAL DE CÍTRICOS 2016/2017: 15.913.000 Tm

ESPAÑA5%

RESTO DE PAÍSES

95%

PRODUCCIÓN MUNDIAL DE NARANJA 2016/17: 66.974.000 Tm

ESPAÑA25%

RESTO DE PAÍSES

75%

EXPORTACIÓN MUNDIAL DE NARANJA 2016/2017: 7.362.000 Tm

ESPAÑA7%

RESTO DE PAÍSES

93%

PRODUCCIÓN MUNDIAL DE MANDARINA 2016/2017: 32.968.000 Tm

ESPAÑA35%

RESTO DE PAÍSES

65%

EXPORTACIÓN MUNDIAL DE MANDARINA 2016/2017: 4.405.000 Tm

Producción y Exportación de EspañaTotal Cítricos 2014/2015 (en 1.000 T)

VOLÚMENES REALIZADOS (en miles de T)PérdidasConsumoRetiradaInterno

GR.MANDARINAS 2.371,7 163,1 294,6 301,3 1.612,7NARANJA 3.499,0 86,8 968,1 640,0 1.804,1TOTAL MA.+NAR. 5.870,7 249,9 1.262,7 941,3 3.416,8LIMÓN 1.078,5 0,2 103,6 304,1 670,6POMELO 77,9 0,0 5,0 9,0 63,9OTROS 4,5 0,0 4,5 0,0 0,0TOTAL GENERAL 7.031,6 250,1 1.375,8 1.254,4 4.151,3

Industria ExportaciónVARIEDADES Producción

Producción y Exportación de EspañaTotal Cítricos 2015/2016 (en 1.000 T)

VOLÚMENES REALIZADOS (en miles de T)PérdidasConsumoRetiradaInterno

GR.MANDARINAS 2.088,0 93,0 270,0 261,0 1.464,0NARANJA 3.084,0 112,0 960,0 439,0 1.573,0TOTAL MA.+NAR. 5.172,0 205,0 1.230,0 700,0 3.037,0LIMÓN 797,0 30,6 142,0 107,0 517,4POMELO 68,0 1,8 5,0 6,0 55,2OTROS 3,0TOTAL GENERAL 6.040,0 237,4 1.377,0 813,0 3.609,6

Industria ExportaciónVARIEDADES Producción

Producción y Exportación de EspañaTotal Cítricos 2016/2017 (en 1.000 T)

VOLÚMENES REALIZADOS (en miles de T)PérdidasConsumoRetiradaInterno

GR.MANDARINAS 2.385,6 411,3 322,4 294,6 1.357,4NARANJA 3.648,4 315,7 1.008,0 705,8 1.618,9TOTAL MA.+NAR. 6.034,0 727,0 1.330,4 1.000,4 2.976,2LIMÓN 1.087,4 21,4 124,6 273,6 667,8POMELO 84,8 5,2 10,0 9,1 60,5OTROSTOTAL GENERAL 7.206,2 753,6 1.465,0 1.283,1 3.704,6

Industria ExportaciónVARIEDADES Producción

34 | 18TH OECD MEETING OF THE HEADS OF NATIONAL INSPECTION SERVICES

3,510.63,867.0

4,543.04,246.0

4,862.94,876.3

4,704.1

5,290.1

4,601.45,128.4

4,679.34,474.8

5,885.5

4,999.7

5,770.05,511.9

5,750.75,935.2

6,280.66,181.3

5,226.0

6,815.4

5,374.8

6,614.1

5,347.6

6,627.0

7,501.3

6,800.77,240.8

7,031.66,040.0

7,206.2

6,231.3

0.0

1,000.0

2,000.0

3,000.0

4,000.0

5,000.0

6,000.0

7,000.0

8,000.0ESPAÑA: EVOLUCIÓN PRODUCCIÓN CÍTRICOS

Campaña 2011/12, Campaña Récord en Producción

en 1.000 Tm

EXPORTACIÓN DE CÍTRICOS DE ESPAÑA ( T )

1,742,622

2,354,6262,579,761

3,177,3093,246,357

3,300,7113,562,980

3,224,868

3,610,4073,369,673

3,644,0003,760,2003,861,700

3,760,500

4.151.300

3,609,6003,704,600

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

en T

Campaña 14/15 Campaña Récord de Exportación

ENCUESTA SOBRE SUPERFICIES Y RENDIMIENTOS DE CULTIVOS EN ESPAÑA (ESYRCE)

RESULTADOS 2004-2016 (Ha)ENCUESTA SOBRE SUPERFICIES Y RENDIMIENTOS DE CULTIVOS EN ESPAÑA (ESYRCE)

RESULTADOS 2004-2017 (ha)Superficie (ha) AñoCultivos y cubiertas del suelo 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 20170a Frutales citricos 305.954 306.557 320.530 332.796 332.626 320.778 314.575 311.584 305.954 303.028 299.478 299.518 297.535 297.0160A010 NARANJO 150.094 148.493 159.805 165.103 166.671 159.395 157.623 159.231 157.592 155.830 152.183 148.777 145.818 144.7060A020 MANDARINO 109.786 113.355 117.209 122.554 120.695 117.545 115.101 112.593 109.386 107.783 107.761 110.177 109.040 107.2490A030 LIMONERO 44.465 42.905 41.573 43.264 43.233 41.816 39.750 38.220 37.068 37.068 36.980 38.105 40.191 41.8230A040 POMELO 1.042 1.029 1.061 1.190 1.432 1.450 1.509 1.290 1.325 1.435 1.466 1.555 1.525 1.8140A050 NARANJO AMARGO 179 66 40 25 48 65 65 64 99 348 120 239 230 2750A060 OTROS CITRICOS 387 710 843 661 547 508 527 186 484 563 968 665 731 1.149

ESPAÑA: SUPERFICIE CITRÍCOLA

NARANJO50%MANDARI

NO37%

LIMONERO13%

POMELO0%

NARANJO AMARGO

0%

OTROS CÍTRICOS

0%

Fuente: Encuesta sobre Superficies y Rendimientos 2015, ESYRCE 2015. Ministerio de Agricultura, Alimentación y Medio Ambiente.

ESPAÑA: ZONAS DE PRODUCCIÓN CITRÍCOLA

CC.AA.SUP (ha)

Com. Valenciana 162.093Andalucía 82.772Murcia 41.078Cataluña 11.157Baleares 1.050Otras CC.AA. 1.368TOTAL 299.518

Com. Valenciana

54%Andalucía

28%

Murcia14%

Cataluña4%

Baleares0%

Otras CCAA

0%

Fuente: Encuesta sobre Superficies y Rendimientos 2015, ESYRCE 2015. Ministerio de Agricultura, Alimentación y Medio Ambiente.

SECTION II. FRUIT SECTOR IN SPAIN | 35

ESPAÑA: ZONAS DE PRODUCCIÓN DE NARANJA

CC.AA.SUP (ha)

Com. Valenciana 73.775Andalucía 60.471Murcia 11.284Cataluña 1.700Baleares 521Otras CC.AA. 1.026TOTAL 148.777

Com. Valenciana

50%

Andalucía41%

Murcia7%

Cataluña1%

Baleares0%

Otras CCAA

1%

Fuente: Encuesta sobre Superficies y Rendimientos 2015, ESYRCE 2015. Ministerio de Agricultura, Alimentación y Medio Ambiente.

ESPAÑA: ZONAS DE PRODUCCIÓN DE MANDARINA

CC.AA.SUP (ha)

Com. Valenciana 77.541Andalucía 16.537Murcia 6.664Cataluña 9.310Baleares 111Otras CC.AA. 14

TOTAL 110.177

Com. Valenciana

70%

Andalucía15%

Murcia6%

Cataluña9%

Baleares0%

Otras CCAA

0%

Fuente: Encuesta sobre Superficies y Rendimientos 2015, ESYRCE 2015. Ministerio de Agricultura, Alimentación y Medio Ambiente.

ESPAÑA: ZONAS DE PRODUCCIÓN DE LIMÓN

CC.AA.SUP (ha)

Com. Valenciana 9.678Andalucía 5.087Murcia 22.608Cataluña 12Baleares 418Otras CC.AA. 302TOTAL 38.105

Com. Valenciana

26%

Andalucía13%Murcia

59%

Cataluña0%

Baleares1%

Otras CCAA

1%

Fuente: Encuesta sobre Superficies y Rendimientos 2015, ESYRCE 2015. Ministerio de Agricultura, Alimentación y Medio Ambiente.

4,151,300

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

1849

1890

1897

1900

1903

1906

1909

1912

1915

1918

1921

1924

1927

1930

1933

1936

/3719

39/40

1942

/4319

45/46

1949

/5019

52/53

1955

/5619

58/59

1961

/6219

64/65

1967

/6819

70/71

1973

/7419

76/77

1981

/8219

84/85

1987

/8819

90/91

1993

/9419

96/97

1999

/0020

02/03

2005

/0620

08/09

2011

/1220

14/15to

nelad

as

Campaña Récord de Exportación, Campaña 2014/2015 con 4.151.300 Tm

exportadas

EXPORTACIÓN DE CÍTRICOS DE ESPAÑA (1849-2016/17)

EXPORTACIÓN DE CÍTRICOS DE ESPAÑA ( T )

1,742,622

2,354,6262,579,761

3,177,3093,246,357

3,300,7113,562,980

3,224,868

3,610,4073,369,673

3,644,0003,760,2003,861,700

3,760,500

4.151.300

3,609,6003,704,600

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

en T

Campaña 14/15 Campaña Récord de ExportaciónProducción y Exportación de EspañaTotal Cítricos 2014/2015 (en 1.000 T)

VOLÚMENES REALIZADOS (en miles de T)PérdidasConsumoRetiradaInterno

GR.MANDARINAS 2.371,7 163,1 294,6 301,3 1.612,7NARANJA 3.499,0 86,8 968,1 640,0 1.804,1TOTAL MA.+NAR. 5.870,7 249,9 1.262,7 941,3 3.416,8LIMÓN 1.078,5 0,2 103,6 304,1 670,6POMELO 77,9 0,0 5,0 9,0 63,9OTROS 4,5 0,0 4,5 0,0 0,0TOTAL GENERAL 7.031,6 250,1 1.375,8 1.254,4 4.151,3

Industria ExportaciónVARIEDADES Producción

36 | 18TH OECD MEETING OF THE HEADS OF NATIONAL INSPECTION SERVICES

Producción y Exportación de EspañaGrupo Mandarinas 2014/2015

(en 1.000 T)VOLÚMENES REALIZADOS (en miles de T)

PérdidasConsumoRetiradaInterno

Satsuma 222,3 59,0 65,0 36,0 62,3Clementina 1.550,9 56,8 178,6 210,0 1.105,5MonrealFortuna y Otras 129,7 11,7 10,0 14,0 94,0WilkingNova 180,5 28,9 33,0 28,0 90,6Diversas(Ortanique y 288,3 6,7 8,0 13,3 260,3TOTALGRUPO MANDARINA

Producción Industria ExportaciónVARIEDADES

2.371,7 1.612,7301,3294,6163,1

Producción y Export.Naranjas 2014/15VOLÚMENES REALIZADOS (en miles de T)

PérdidasConsumoRetiradaInterno

Navelina/Nável 1.322,1 34,7 390,0 150,0 747,4Salustiana 261,8 17,6 50,0 65,0 129,2ShamoutiVarias Blancas FinasBlanca ComúnMoro-TaroccoMaltesaSanguinelliWashington SanguinaVarias Sanguinas FinasSanguina ComúnVerna Sanguina y Ot 10,0 0,1 0,0 0,0 9,9Otras NaranjasNavelate/Lanelate 1.347,7 14,2 363,1 285,0 685,4Valencia Late 545,9 9,7 165,0 140,0 231,2Amargas 11,5 10,5 0,0 0,0 1,0TOTAL NARANJAS 3.499,0 86,8 968,1 640,0 1.804,1

Producción Industria ExportaciónVARIEDADES

EN NARANJAS, EN GENERAL, Y EN NAVELS, EN PARTICULAR, ESPAÑA ES IRREMPLAZABLE

ESPAÑA32%

3.914.200 Tm

GRECIA8%TURQUÍA

11%

ITALIA15%

MARRUECOS8%

EGIPTO21%

OTROS MEDITERRÁ-

NEOS6%

PRODUCCIÓN DE NARANJAS DEL MEDITERRÁNEO 2013/2014: 12.638.000 Tm

ESPAÑA44%

2.997.900 Tm

GRECIA12%

TURQUÍA14%

ITALIA4%

MARRUECOS6%

EGIPTO21%

OTROS MEDITERRÁ-

NEOS1%

PRODUCCIÓN DE NAVELS DEL MEDITERRÁNEO 2013/2014: 7.085.500 Tm

ESPAÑA46%

1.561.200 Tm

GRECIA10%

TURQUÍA10%

ITALIA3%

MARRUECOS3%

EGIPTO30%

OTROS MEDITERRÁ-

NEOS2%

EXPORTACIÓN DE NARANJAS DEL MEDITERRÁNEO 2013/2014: 3.663.500 Tm

ESPAÑA55%

1.247.600 Tm

GRECIA13%

TURQUÍA9%

ITALIA1%

MARRUECOS0%

EGIPTO26%

OTROS MEDITERRÁ-

NEOS0%

EXPORTACIÓN DE NAVELS DEL MEDITERRÁNEO 2013/2014: 2.423.900 Tm

EN NARANJAS Y MANDARINAS, ESPAÑA ES UN PROVEEDOR IRREMPLAZABLE DE LA UE-27

ESPAÑA80%

1.362.900 Tm

GRECIA3%

TURQUÍA3%

ITALIA3%

MARRUECOS6%

EGIPTO0%

OTROS PAISES

MEDITERRÁ-NEOS

5%

CAMPAÑA 2013-2014: MANDARINAS MEDITERRÁNEAS

EXPORTADAS A LA UE-28: 1.718.200 Tm

ESPAÑA69%

1.405.100 Tm

GRECIA13%

TURQUÍA1%

ITALIA4%

MARRUECOS3% EGIPTO

8%

OTROS PAÍSES

MEDITERRÁ-NEOS

2%

CAMPAÑA 2013-2014: NARANJAS MEDITERRÁNEAS

EXPORTADAS A LA UE-28: 2.043.500 Tm

Exportación Cítricos de España 2014/2015 (en 1.000 T) TOTAL TOTAL TOTAL TOTAL TOTAL UE15 UE13 UE28 EUROPA EXPORTAD

OCCIDEN

GR.MANDARINA1.245,9 242,3 1.488,2 39,5 1.527,8 50,0 13,6 21,3 1.612,7NARANJA 1.488,3 191,9 1.680,2 42,3 1.722,6 12,3 7,5 61,7 1.804,1GR.MAND+NAR 2.734,2 434,2 3.168,4 81,8 3.250,4 62,3 21,1 83,0 3.416,8LIMÓN 490,1 125,6 615,7 10,6 626,4 16,0 6,9 21,3 670,6POMELO 48,7 13,1 61,8 0,5 62,3 0,1 0,2 1,3 63,9TOTAL GENERA3.273,0 572,9 3.845,9 92,9 3.939,1 78,4 28,2 105,6 4.151,3

AMÉRICA DEL NO

RTEEURO

PA ORIEN

T. NO UE

RESTO DEL M

UNDOVARIEDADES

NORU

EGA

+SUIZA

+ANDO

R.+ISL

ESPAÑA: EXPORTACIÓN DE CÍTRICOS (en tn)Año 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

EXPORTACIÓN DE CÍTRICOS DE ESPAÑA

3.684.322 3.213.302 3.506.873 3.271.281 3.615.348 3.906.772 3.973.889 3.881.950 4.166.525 3.624.801

PRINCIPALES PAÍSES A LOS QUE EXPORTA ESPAÑAAño 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Alemania 870.192 814.400 807.234 834.778 877.932 944.565 992.193 961.225 1.063.036 975.839Francia 808.303 718.941 888.128 729.296 736.459 819.584 801.387 804.982 860.946 787.282Reino Unido 297.496 245.346 256.279 258.884 300.233 293.622 290.366 307.807 324.718 312.808Países Bajos 281.156 233.220 242.330 238.327 260.820 263.660 274.166 264.614 265.550 247.736Polonia 283.952 247.584 246.583 261.183 288.439 300.268 314.673 270.757 270.384 226.759Italia 171.024 153.308 260.936 116.537 217.270 269.817 296.878 264.431 347.242 188.055Bélgica 122.697 116.920 116.349 121.860 122.725 131.652 118.413 113.234 118.728 112.155Suecia 78.903 78.918 79.512 112.047 95.431 99.636 100.243 81.474 94.199 86.026República Checa 110.245 83.478 82.629 82.078 93.400 102.331 98.868 91.164 105.649 82.839Austria 52.656 49.498 55.923 54.414 75.923 63.402 66.446 60.294 64.115 60.618Suiza 67.582 58.781 69.930 60.663 53.594 57.130 57.194 57.432 62.622 57.282Portugal 32.348 25.560 28.307 30.535 37.338 28.637 41.511 54.665 46.186 49.816Dinamarca 53.686 44.264 46.535 44.925 54.804 56.998 57.339 48.299 51.059 47.028Noruega 46.482 40.825 41.733 41.688 40.860 41.810 45.344 41.111 40.928 40.460Finlandia 28.806 29.365 25.453 31.390 26.588 27.586 32.713 29.746 29.720 34.301OTROS 378.792 272.891 259.013 252.675 333.535 406.073 386.156 430.720 421.441 315.794

SECTION II. FRUIT SECTOR IN SPAIN | 37

ESPAÑA: EXPORTACIÓN DE CÍTRICOS (en participación %)Año 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

EXPORTACIÓN DE CÍTRICOS DE ESPAÑA

100 100 100 100 100 100 100 100 100 100

PRINCIPALES PAÍSES A LOS QUE EXPORTA ESPAÑAAño 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Alemania 22,5 23,5 24,2 25,5 24,8 24,2 25,8 24,9 26,2 27,9Francia 23,6 24 23 23,7 21,3 21,8 21,1 21,7 21,6 22,5Reino Unido 8,3 8 8 8 8,6 7,8 7,9 8,9 8,5 9Países Bajos 7,7 7,5 7,4 7,5 7,1 6,7 6,8 6,5 6,1 6,3Polonia 6,5 7 6,1 6,8 6,6 6,4 6,5 5,9 5,4 5,2Italia 4,6 4,8 7,2 3,7 5,4 6,6 6,7 6,1 7,4 4,9Bélgica 4,1 4,5 4,5 4,1 3,7 3,6 3,3 3,2 3,2 3,3Suecia 2 2,2 2,1 2,9 2,4 2,4 2,2 1,9 2 2,1República Checa 2,5 2,3 2,2 2,1 2,2 2,2 2,2 1,9 2,1 2Suiza 2,2 2,1 2,3 2 1,7 1,7 1,7 1,7 1,8 1,9Austria 1,4 1,5 1,6 1,7 2,6 1,9 1,8 2,1 1,8 1,9Dinamarca 1,4 1,3 1,4 1,3 1,5 1,6 1,4 1,3 1,2 1,2Noruega 1,3 1,2 1,3 1,2 1,2 1,2 1,3 1,2 1,1 1,2Portugal 0,7 0,7 0,8 0,8 0,7 0,6 0,8 0,9 0,8 1Canadá 0,4 0,2 0,1 0,2 0,4 0,7 0,4 1,5 1,2 1OTROS 10,6 8,8 7,6 8 9,5 10,2 9,9 9,8 9,5 8,2

EXPORTACION TOTAL DE CÍTRICOS DE ESPAÑA 2016/2017en Tn CLAUS./

SAT. G.CLEM. COM/WILK FORTUNAS TOTAL

MANDARINAS TOTAL

NARANJASTOTAL

LIMONESTOTAL

POMELOTOTAL

CITRICOS CAMP.15/16 DIFEREN

ALEMANIA 11.479 261.058 41.526 53.341 367.404 415.037 175.107 17.764 975.312 977.365 -2.053FRANCIA 2.585 178.125 29.516 44.749 254.975 377.482 118.150 14.300 764.907 795.660 -30.753REINO UNIDO 15.944 80.227 12.212 41.254 149.637 101.268 68.558 3.773 323.236 298.765 24.471ITALIA 299 48.831 6.376 9.673 65.179 135.137 66.842 2.967 270.125 200.649 69.476PAISES BAJOS 4.127 45.117 7.235 15.753 72.232 140.216 25.441 3.389 241.278 245.347 -4.069POLONIA 390 68.370 15.331 15.056 99.147 72.103 53.822 5.094 230.166 215.690 14.476BELGICA/LUXE 2.930 28.693 1.205 8.479 41.307 53.005 13.285 843 108.440 115.438 -6.998SUECIA 7.748 17.958 2.841 4.340 32.887 40.167 12.377 639 86.070 82.390 3.680REP CHECA 3.829 24.867 3.275 5.119 37.090 21.925 14.744 1.431 75.190 86.789 -11.599AUSTRIA 7.444 11.050 5.290 2.230 26.014 23.178 14.769 1.391 65.352 57.272 8.080PORTUGAL 2 12.508 3.306 1.296 17.112 30.847 12.424 1.054 61.437 45.768 15.669DINAMARCA 94 19.624 577 895 21.190 19.117 5.928 791 47.026 45.836 1.190FINLANDIA 4.829 16.298 525 1.266 22.918 7.438 3.633 37 34.026 30.501 3.525HUNGRIA 64 5.433 2.401 2.735 10.633 5.485 7.306 1.357 24.781 19.949 4.832IRLANDA 503 5.122 991 916 7.532 8.670 3.848 952 21.002 19.857 1.145RUMANIA 65 3.029 574 290 3.958 7.171 8.479 324 19.932 18.351 1.581LITUANIA 341 7.036 1.113 1.266 9.756 4.300 5.031 267 19.354 20.845 -1.491ESLOVAQUIA 981 6.252 941 1.523 9.697 4.087 4.399 646 18.829 24.258 -5.429ESLOVENIA 31 3.755 490 170 4.446 7.337 2.967 51 14.801 13.358 1.443LETONIA 249 8.540 282 767 9.838 1.416 2.519 463 14.236 16.835 -2.599OTROS 360 6.079 291 1.146 7.876 8.738 7.279 471 24.364 24.247 117TOTAL U.E. 64.294 857.972136.298 212.264 1.270.828 1.484.124 626.908 58.004 3.439.864 3.355.170TOTAL P.TERC. 1.877 68.949 0 15.701 86.527 134.745 40.926 2.534 264.732 254.450TOTAL 66.171 926.921136.298 227.965 1.357.355 1.618.869 667.834 60.538 3.704.596 3.609.620CAMP.15/16 69.698 1.041.943183.657 168.713 1.464.011 1.572.987 517.475 55.147 3.609.620

Exportación de Cítricos de España por País Tercero y Variedad 14/15 (en T)en Tm CLAUSE SATSUMG.CLEMENARANJ LIMÓN POMELO TOTAL CAM 13/14VARIACI

SUIZA 1.338 23.175 26.609 8.674 354 60.150 57.738 2.412CANADÁ 6 17.493 12.242 11.110 129 40.980 38.123 2.857ESTADOS UNIDOS 32.520 4.865 37.385 42.193 -4.808NORUEGA 21 14.397 14.758 1.639 63 30.878 39.115 -8.237ARGELIA 2.655 17.305 1.240 21.200 30.444 -9.244ÉMIRATOSÁRABES 6.200 10.620 3.126 158 20.104 18.800 1.304

BRASIL 4.903 11.849 1.780 263 18.795 16.010 2.785ARABIA SAUDÍ 2.130 7.337 3.049 111 12.627 17.225 -4.598BIELORRUSIA 24 7.789 2.304 1.101 66 11.284 14.223 -2.939UCRANIA 23 3.209 1.078 1.275 113 5.698 7.208 -1.510HONG KONG 491 2.058 1.971 53 4.573 2.240 2.333SERBIA 590 1.354 2.238 30 4.212 2.722 1.490KAZAJISTÁN 1.657 229 2.121 28 4.035 1.390 2.645MOLDAVIA 40 1.843 880 956 44 3.763 2.048 1.715JORDANIA 78 268 3.195 3.541 449 3.092CHINA 56 2.959 200 95 3.310 1.141 2.169MALASIA 171 1.288 1.150 23 2.632 2.481 151COREA DEL SUR 10 2.200 2.210 1.203 1.007SUDÁFRICA 603 266 487 286 1.642 861 781MACEDONIA 30 512 1.004 25 1.571 215 1.356OTROS 27 24 3.026 7.599 3.692 314 14.682 70.644 -55.962TOTAL 54 1.449 123.026 123.715 54.873 2.155 305.272

CAMPAÑA 13/14 62 5.039 149.282 155.962 54.908 1.220 366.473

EXPORTACION DE CÍTRICOS DE ESPAÑA A PAÍSES TERCEROS 2016/2017en Tn SATSUMA G.CLEMEN NARANJAS LIMONES POMELOS TOTAL CAMP.15/16 DIFERENCIASUIZA 1.755 22.044 25.782 9.048 346 58.975 57.701 1.274CANADA 12.713 12.947 7.715 384 33.766 27.705 6.061NORUEGA 10.152 13.343 1.960 4 25.459 32.712 -7.253EEUU 16.910 5.263 22.173 25.100 -2.927EMIRATOS A.U 3.276 15.309 1.811 109 20.505 18.150 2.355CHINA 1.154 18.403 6 146 19.709 12.868 6.841ARABIA SAUDI 2.541 16.107 406 1 19.055 13.170 5.885BRASIL 4.644 12.324 1.709 252 18.929 20.345 -1.416BIELORRUSIA 4.275 1.253 1.010 12 6.550 6.325 225ARGENTINA 159 2.614 2.814 519 6.106 3.131 2.975MALASIA 273 1.950 1.357 1 3.581 1.473 2.108COREA DEL SU 2.651 2.651 2.299 352MOLDAVIA 27 860 639 935 99 2.560 2.221 339SUDAFRICA 884 812 144 411 2.251 1.493 758UCRANIA 42 1.006 173 672 50 1.943 2.871 -928SERBIA 363 902 598 1.863 2.147 -284SINGAPUR 281 612 884 45 1.822 1.322 500HONG KONG 164 580 624 19 1.387 2.666 -1.279BAHREIN 133 954 158 7 1.252 428 824COSTA RICA 446 729 45 11 1.231 847 384OTROS 1 2.372 6.661 3.767 118 12.964 19.476 -6.512TOTAL 1.825 84.650 134.745 40.926 2.534 264.732

CAMP.15/16 1.893 105.657 117.061 26.848 2.905 254.450DIFERENCIA -68 -21.007 17.684 14.078 -371 10.282

EXPORTACIÓN DE CÍTRICOS DE ESPAÑA A PAÍSES TERCEROS A 15-04-2018 (en Tn)

SATSUMA G.CLEMEN. NARANJAS LIMONES POMELOS TOTAL CAMP.16/17 DIFERENCIASUIZA 1.212 24.434 20.045 6.443 603 52.737 49.504 3.233CANADA 3 14.568 20.214 11.366 637 46.788 28.981 17.807NORUEGA 9 16.709 14.758 1.705 126 33.307 22.911 10.396CHINA 750 21.704 4 19 22.477 16.644 5.833BRASIL 4.726 14.852 1.813 264 21.655 18.224 3.431EEUU 15.454 3.724 19.178 20.903 -1.725EMIRATOS A.U 1 3.226 6.438 481 1 10.147 17.481 -7.334ARABIA SAUDI 2.907 6.259 195 9.361 14.598 -5.237ARGENTINA 181 5.385 341 268 6.175 6.106 69SUDAFRICA 1.240 768 248 493 2.749 2.251 498COREA DEL SU 2.588 2.588 2.211 377BIELORRUSIA 1.704 836 22 7 2.569 5.698 -3.129QATAR 463 1.625 241 5 2.334 865 1.469UCRANIA 10 1.000 312 28 3 1.353 1.837 -484MOLDAVIA 32 638 433 116 19 1.238 1.864 -626MALASIA 337 596 271 1.204 2.993 -1.789COSTA RICA 490 592 9 10 1.101 1.141 -40URUGUAY 74 585 295 40 994 668 326SINGAPUR 330 518 81 22 951 1.710 -759OMAN 142 652 30 2 826 398 428OTROS 43 3.268 4.551 896 185 8.943 12.048 -3.105 TOTAL 1.310 92.641 123.711 28.309 2.704 248.675CAMP.16/17 1.876 84.119 107.454 33.207 2.380 229.036 DIFERENCIA -566 8.522 16.257 -4.898 324 19.639

3,2707,7114,7485,5268,574

15,84714,377

26,34734,067

45,326

79,35878,978

45,73154,043

69,16461,709

63,68876,717

47,84355,910

45,078

60,71247,56046,976

40,54732,520

23,41716,910

0

14,674

1,003 19

0 0

8

2

16,188

324 62

0

0

0

59 17

19,882

0

46

0

0

22 00

0

0

0

716

1,307

21 5,884857

631 357

4,816

12,601

8,195

8,6624,491

19,8036,685

3,934

8536,779

15,407

141

3,299

605

909

1,577 409

1,646

4,865

1,683

5,263

0

20,000

40,000

60,000

80,000

100,000

120,000

EXPORTACIONES ESPAÑOLAS DE CÍTRICOS A EE.UU. ( en T )

LIMÓN

NARANJA

MANDARINA

(*) Campañas1990/91, 1998/99 & 2006/07: Helada en California

(*) Campaña 2001/02: Embargo a las clementinas de España en EE.UU. desde el 30 de Noviembre de 2001. El embargo a las clementinas de España se levantó el 6 de Octubre de 2002

38 | 18TH OECD MEETING OF THE HEADS OF NATIONAL INSPECTION SERVICES

ESPAÑA: Producción de Cítricos 1991/92-2016/17 (en 1.000 T)

Efectos del frío Enero-Marzo 05

91/92 92/93 93/94 94/95 95/96 96/97 97/98 98/99 99/00 00/01 01/02 02/03 03/04 04/05 05/06 06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14 14/15 15/16 16/17CLAUSELLINA/SATSUMA/MONREAL

406 373 408 365 303 248 355 281 299 300 285 265 257 254 168 280 158 212 164 173 138 180 193 222 187 208CLEMENTINA/CLEMENVILLA O NOVA/HERNANDINA

871 1.027 1.047 1.255 1.139 985 1.402 1.081 1.286 1.223 1.275 1.447 1.461 1.812 1.467 1.860 1.607 1.666 1495 1720 1.788 1.489 1.628 1.731 1.502 1.660TANGERINA/KARA/FORTUNA

66 121 134 171 241 274 342 393 457 297 218 296 357 435 309 361 313 341 341 397 578 505 384 418 399 517TOTAL PETITS FRUITS1.342 1.521 1.589 1.791 1.683 1.507 2.099 1.754 2.042 1.819 1.778 2.009 2.075 2.500 1.945 2.501 2.077 2.219 2.001 2.290 2.503 2.174 2.204 2.372 2.088 2.385NAVEL- NAVELINA/SALUSTIANA/VALENCIA-OTRAS2.721 2.990 2.407 2.739 2.528 2.274 2.772 2.387 2.805 2.703 2.924 2.931 3.100 2.832 2.295 3.393 2.702 3.462 2.622 3.345 3.888 3.723 3.906 3.489 3.067 3.640SANGUINAS/SANGUINELLI

15 13 10 8 8 8 14 5 6 6 5 4 2 3 2 3 2 5 0 0 0 0 9 10 7 8TOTAL ORANGES2.748 3.002 2.417 2.747 2.535 2.282 2.786 2.392 2.811 2.709 2.929 2.935 3.103 2.835 2.297 3.397 2.704 3.466 2.622 3.345 3.888 3.723 3.914 3.499 3.074 3.648TOTAL CITRONS

589 737 570 563 433 666 968 827 893 938 1.018 962 1.071 810 951 879 550 883 673 927 1.051 840 1.057 1.079 797 1.087TOTAL GRAPEFRUITS

25 30 26 28 29 20 32 27 23 25 26 29 33 36 33 39 43 46 52 65 59 64 59 78 68 85TOTAL AGRUMES4.704 5.290 4.601 5.128 4.679 4.475 5.886 5.000 5.770 5.491 5.751 5.935 6.281 6.181 5.226 6.815 5.375 6.614 5.348 6.627 7.501 6.801 7.241 7.032 6.027 7.206

PLANTONES Y PATRONES CERTIFICADOS DE CÍTRICOS COMERCIALIZADOS EN ESPAÑA

(en miles de plantas)VARIEDADES 1.999* 2.000* 2.001* 2.002* 2.003 2.004 2.005 2.006 2.007 2.008 2.009 2.010 2.011 2.012 2.013 2.014 2.015 2.016Naranjos 2.424 2.448 1.775 1.919 2.667 2.855 4.171 4.468 2.462 2.407 2.040 1.808 1.685 1.584 1.637 1.423 1.224 1.477Pomelos 33 49 35 55 73 63 92 77 94 42 54 33 32 43 54 53 40 54Mandarinos 3.613 3.322 3.903 3.137 3.733 3.005 2.333 1.302 807 848 732 1.033 1.274 1.658 1.636 1.373 1.255 1.511Limas 4 2 2 1 4 3 6 7 4 8 9 9 12 19 24 30 57 48Limoneros 546 620 661 399 354 326 209 181 138 166 195 272 335 319 492 617 552 880TOTAL PLANTONES 6.622 6.441 6.376 5.511 6.831 6.252 6.811 6.036 3.505 3.472 3.030 3.154 3.338 3.623 3.843 3.496 3.128 3.972

TOTAL PATR. 515 119 228 60 107 138 59 38 23 32 14 53 52 277 389 215 388 837TOTAL PL. Y PATR. 7.137 6.560 6.604 5.571 6.938 6.390 6.870 6.074 3.527 3.503 3.044 3.207 3.391 3.900 4.232 3.710 3.516 4.809

*Sin datos Cataluña

PLANTONES Y PATRONES CERTIFICADOS DE CÍTRICOS COMERCIALIZADOS EN ESPAÑA

1972-2016 (44 años)183.504.719 árboles

0

1

2

3

4

5

6

7

8

9

1.97

21.

973

1.97

41.

975

1.97

61.

977

1.97

81.

979

1.98

01.

981

1.98

21.

983

1.98

41.

985

1.98

61.

987

1.98

81.

989

1.99

01.

991

1.99

21.

993

1.99

41.

995

1.99

61.

997*

1.99

8*1.

999*

2.00

0*2.

001*

2.00

2*2.

003

2.00

42.

005

2.00

62.

007

2.00

82.

009

2.01

02.

011

2.01

22.

013

2.01

42.

015

2.01

6

Mill

ones

de

árbo

les

* Sin datos Cataluña

PLANTONES Y PATRONES CERTIFICADOS DE CÍTRICOS COMERCIALIZADOS EN ESPAÑA

* Sin datos Cataluña

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

1.97

21.

973

1.97

41.

975

1.97

61.

977

1.97

81.

979

1.98

01.

981

1.98

21.

983

1.98

41.

985

1.98

61.

987

1.98

81.

989

1.99

01.

991

1.99

21.

993

1.99

41.

995

1.99

61.

997*

1.99

8*1.

999*

2.00

0*2.

001*

2.00

2*2.

003

2.00

42.

005

2.00

62.

007

2.00

82.

009

2.01

02.

011

2.01

22.

013

2.01

42.

015

2.01

6

Mile

s de

pla

ntas Patrones

LimonerosLimasMandarinosPomelosNaranjos

COMPARATIVA BALANCE 2016/17 Y AFORO 2017/18 DE CÍTRICOS EN ESPAÑA (en T)

BALANCE 2016/17

AFORO 2017/18

VARIACIÓN %

MANDARINAS 2.385.478 1.946.239 -18,4%

NARANJA DULCE 3.648.485 3.242.140 -11,1%

NARANJA AMARGA 0 0

LIMONES 985.429 957.546 -2,8%POMELOS Y OTROS CÍTRICOS 84.867 85.357 0,6%

TOTAL CÍTRICOS 7.104.259 6.231.282 -12,3%Fuente: Consejerías de Agricultura de las Comunidades Autónomas productoras de cítricos.

COMPARATIVA BALANCE 2016/17 Y AFORO 2017/18 DE CÍTRICOS EN LA COMUNIDAD VALENCIANA (en T)

BALANCE 2016/2017 AFORO 2017/2018 VARIACIÓN %Satsumas tempranas 103.682 68.352 -34,1 %Satsumas tardías 85.484 61.762 -27,8 %SUBGRUPO SATSUMAS 189.166 130.114 -31,2 %

Clementinas tempranas 257.544 197.404 -23,4 %Clementinas media temporada 861.664 592.765 -31,2 %Clementinas tardías 73.992 53.443 -27,8 %SUBGRUPO CLEMENTINAS 1.193.200 843.612 -29,3 %SUBGRUPO MANDARINOS E HÍBRIDOS 391.051 371.718 -4,9 %

TOTAL MANDARINAS 1.773.417 1.345.444 -24,1 %Navel tempranas 718.246 515.276 -28,3 %Navel media temporada 137.444 118.807 -13,6 %Navel tardías 689.077 609.275 -11,6 %SUBGRUPO NAVEL 1.544.767 1.243.358 -19,5 %

Blancas tempranas 64.190 44.947 -30 %Blancas tardías 236.856 233.775 -1,3 %SUBGRUPO BLANCAS 301.046 278.722 -7,4 %SUBGRUPO SANGUINAS 7.848 4.626 -41,1 %

TOTAL NARANJA DULCE 1.853.661 1.526.706 -17,6 %Limón Verna 87.542 44.918 -48,7 %Limón Fino 206.332 201.232 -2,5 %TOTAL LIMONES 293.874 246.150 -16,2 %TOTAL POMELOS 22.261 25.684 15,4 %TOTAL CÍTRICOS 3.943.213 3.143.984 -20,3 %

SECTION II. FRUIT SECTOR IN SPAIN | 39

Calendario de las Exportaciones de España (en 1.000 T)

CAMPAÑAS

Sept/Oct. Nov. Dic. Enero Febr Marzo Abril Mayo Junio Julio/

Agost TOTAL

GRUPOMANDARINAS

2014/15 228 315 369 277 186 124 67 36 10 3 1.6132015/16 212 298 338 248 167 116 54 25 3 3 1.4642016/17 199 321 319 224 147 91 39 13 1 2 1.3572017/18 212 304 321 211 137

NARANJAS 2014/15 55 163 219 243 258 288 254 180 84 60 1.8042015/16 51 192 242 228 229 228 190 117 55 40 1.5732016/17 56 181 225 228 214 246 191 142 76 59 1.6192017/18 61 162 220 216 204

LIMONES

2014/15 70 54 74 61 60 68 68 72 68 78 6712015/16 57 41 59 50 59 63 58 55 35 40 5172016/17 64 50 69 66 68 77 70 72 67 66 6702017/18 72 60 72 60 58

TOTAL GENERAL

2014/15 358 538 669 589 511 489 398 294 164 142 4.1512015/16 327 538 646 534 464 414 308 201 94 83 3.6102016/17 324 560 619 528 438 426 306 230 145 129 3.7072017/18 351 532 618 494 406

ESPAÑA: CALENDARIO DE EXPORTACIÓN DEL GRUPO MANDARINAS 1998/99-2016/17 (en T)

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

SEP/OCT NOV. DEC. ENERO FEBRERO MARZO ABRIL MAYO JUNIO JUL/AGO

98/99

99/00

00/01

01/02

02/03

03/04

04/05

05/06

06/07

07/08

08/09

09/10

10/11

11/12

12/13

13/14

14/15

15/16

16/17

ESPAÑA: CALENDARIO DE EXPORTACIÓN DE NARANJAS 1998/99-2016/17 (en T)

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

SEPT/OCT NOV. DICIEMBR. ENERO FEBRERO MARZO ABRIL MAYO JUNIO JUL/AGO

98/99

99/00

00/01

01/02

02/03

03/04

04/05

05/06

06/07

07/08

08/09

09/10

10/11

11/12

12/13

13/14

14/15

15/16

16/17

ESPAÑA: CALENDARIO DE EXPORTACIÓN DE MANDARINAS + NARANJAS 1998/99-2016/17 (en T)

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

SEPT/OCT NOV. DICIEMB ENERO FEBR MARZO ABRIL MAYO JUNIO JUL/AGO

98/99

99/00

00/01

01/02

02/03

03/04

04/05

05/06

06/07

07/08

08/09

09/10

10/11

11/12

12/13

13/14

14/15

15/16

16/17

1.5391.560

1.8111.8561.7821.6781.679

1.8811.8481.8591.9491.969

2.1092.1642.039

2.2572.1392.132

-

500

1.000

1.500

2.000

2.500

2000 2001 2002 2003 20042005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Millo

nes d

e eur

os

EXPORTACIÓN DE CÍTRICOS DE ESPAÑA EN VALOR

CATALUÑA COMUNIDAD VALENCIANA ANDALUCIA MURCIA OTROS

-

500

1.000

1.500

2.000

2.500

3.000

3.500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Millo

nes d

e eur

os

EXPORTACIÓN DE CÍTRICOS DE ESPAÑA EN VALOR