oecd economic outlook - christian kastrop, oecd

TRANSCRIPT

OECD ECONOMIC OUTLOOK

Senior Budget Officials Meeting

Stockholm, 9-10 June, 2016

Christian Kastrop Director, Economics Department

Key messages

The global economy is stuck in a “low-growth” trap •Growth in advanced economies is low and has declined in many EMEs •Weak trade and sluggish investment continue •Risks: Brexit, high credit growth and debt exposures in EMEs, volatile financial markets

Productivity growth has slowed and inequality has risen •Prolonged demand weakness is damaging long-term growth prospects •Productivity gains are not being widely shared •Wage growth is even lower than productivity growth

Comprehensive and collective action is needed to keep promises •Monetary policy alone cannot break out of low growth trap and may be overburdened • Fiscal space is eased with low interest rates; use public investment to support growth • Structural reform packages needed to boost productivity, wages and equality

2

Global GDP growth is low

Global GDP growth in 2016 projected to be about the same as 2015; 2017 only a little stronger

Growth is flat in advanced economies, slower in many EMEs

Projections Real GDP, Annual percentage changes

1. Moving nominal GDP weights using purchasing power parities. 2. Fiscal years starting in April. Source: OECD June 2016 Economic Outlook database.

GDP growth

2014 2015 2016 2017World1 3.3 3.0 3.0 3.3United States 2.4 2.4 1.8 2.2Euro area 1.0 1.6 1.6 1.7United Kingdom 2.9 2.3 1.7 2.0Japan 0.0 0.6 0.7 0.4China 7.3 6.9 6.5 6.2India2 7.2 7.4 7.4 7.5Brazil 0.1 -3.9 -4.3 -1.7

3

Global trade growth is weak, particularly in Asia

Note: SE Asia includes Chinese Taipei, Hong Kong, Malaysia, the Philippines, Singapore, Thailand and Vietnam. Euro area and SE Asia include intra-regional trade. Source: OECD June 2016 Economic Outlook database; OECD calculations.

Trade in goods and services Real annual growth

A return to pre-crisis trade growth would boost productivity by 1 per cent on average after 5 years

4

Rebalancing and on-shoring in China has contributed to weak trade growth

Note: Manufacturing (secondary) includes construction and utilities. Source: National Bureau of Statistics; General Administration of Customs.

Composition of growth in China The share of China’s processing trade is declining

5

Weak exports and investment are weighing on US growth

Contributions to quarterly US GDP growth

Source: OECD June 2016 Economic Outlook database. 6

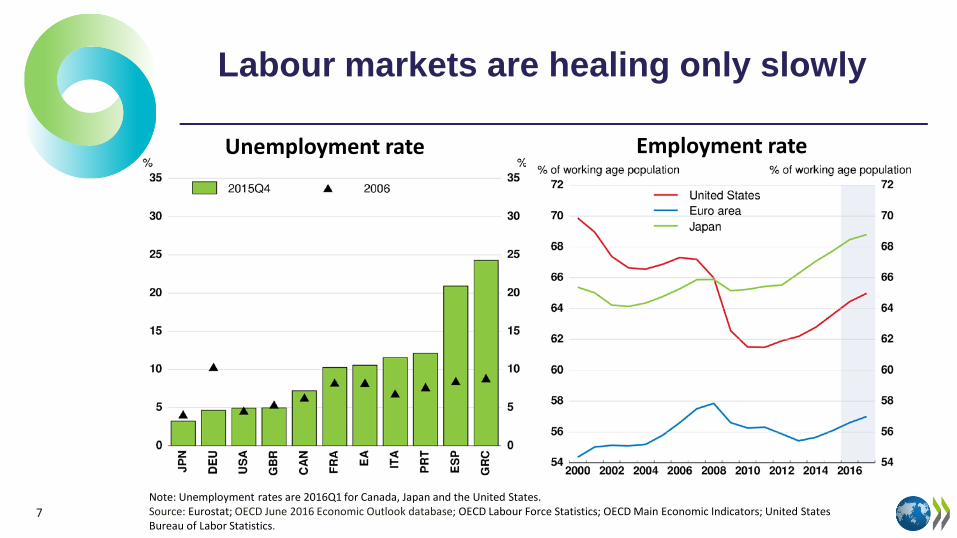

Labour markets are healing only slowly

Employment rate Unemployment rate

Note: Unemployment rates are 2016Q1 for Canada, Japan and the United States. Source: Eurostat; OECD June 2016 Economic Outlook database; OECD Labour Force Statistics; OECD Main Economic Indicators; United States Bureau of Labor Statistics.

7

Risks

8

Some EMEs are vulnerable to exchange rate shocks and high domestic debt

External liabilities Per cent of GDP, 2015 Q3 or latest available

Note: Credit to non-financial corporations. For South Africa, 2008 Q1 instead of 2007. Source: OECD June 2016 Economic Outlook database; BIS; IMF; and OECD calculations.

Credit to corporations has increased Per cent of GDP

9

Financial markets have been volatile

Source: Thomson Reuters.

Recovery only in US equity markets compared with summer 2015

Volatility in asset markets has increased Rolling 3-month standard deviations

10

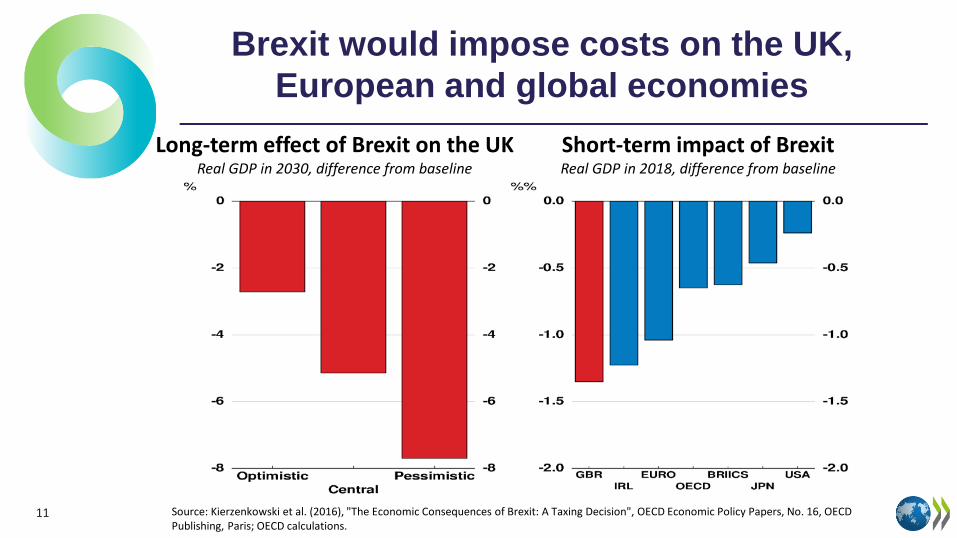

Brexit would impose costs on the UK, European and global economies

Source: Kierzenkowski et al. (2016), "The Economic Consequences of Brexit: A Taxing Decision", OECD Economic Policy Papers, No. 16, OECD Publishing, Paris; OECD calculations.

Long-term effect of Brexit on the UK Real GDP in 2030, difference from baseline

Short-term impact of Brexit Real GDP in 2018, difference from baseline

11

Slowing productivity growth and rising inequality

present significant challenges

12

Declining productivity growth is widespread in advanced economies and some EMEs

Note: Annualised rate. Output per hour worked for OECD economies. For non-OECD economies, measured as output per worker. Brazil is for 1991-2000. Source: OECD National Accounts database; OECD Productivity database.

Labour productivity growth

13

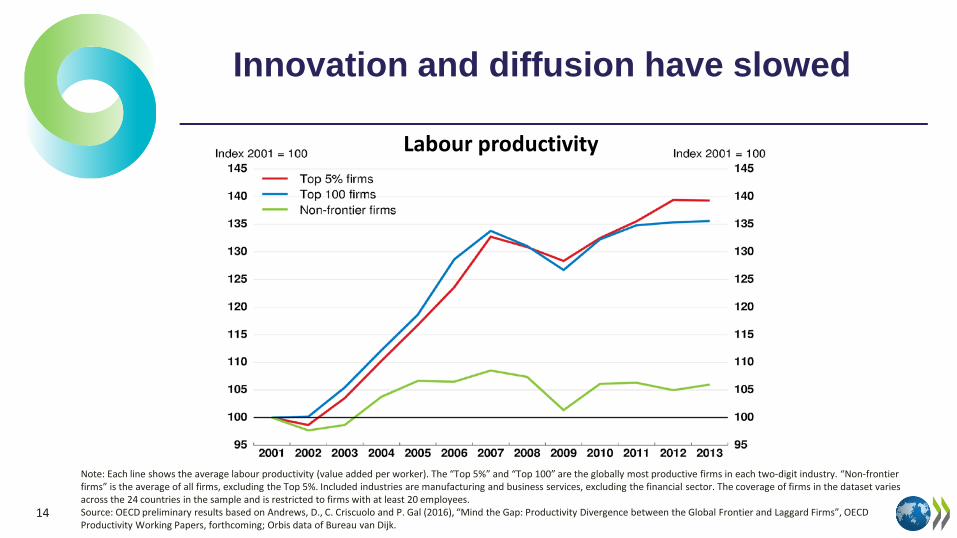

Innovation and diffusion have slowed

Labour productivity

Note: Each line shows the average labour productivity (value added per worker). The “Top 5%” and “Top 100” are the globally most productive firms in each two-digit industry. “Non-frontier firms” is the average of all firms, excluding the Top 5%. Included industries are manufacturing and business services, excluding the financial sector. The coverage of firms in the dataset varies across the 24 countries in the sample and is restricted to firms with at least 20 employees. Source: OECD preliminary results based on Andrews, D., C. Criscuolo and P. Gal (2016), “Mind the Gap: Productivity Divergence between the Global Frontier and Laggard Firms”, OECD Productivity Working Papers, forthcoming; Orbis data of Bureau van Dijk.

14

Incomes are rising very slowly for most workers, increasing inequality

Note: OECD is the unweighted average of the countries for which data are available. Source: OECD estimations based on Kappeler et al. (2016), “Decoupling of Productivity and Median Wage Growth: Macro-Level Evidence”, OECD Economics Department Working Papers, forthcoming; OECD National Accounts database; OECD Earnings database; OECD Income Distribution database; OECD calculations.

Wages growing less than productivity Annualised real growth rates, per hour worked,

1990-2013

15

Inequality in income is increasing Real household disposable income, total population

Productivity differences are correlated with wage inequality

Wage inequality and productivity dispersion across firms

Note: Data are for 2013. OECD is the unweighted average of the countries for which data are available. The P90/P50 ratio is labour income or labour productivity of the firm at the 90th percentile divided by the corresponding value of the firm at the median. Labour income is total compensation including taxes and the employer’s and employee’s social security contributions. Source: OECD estimations based on Saia and Schwellnus (2016), “Decoupling of Productivity and Median Wage Growth: Micro-Level Evidence”, OECD Economics Department Working Papers, forthcoming; Orbis.

Higher wage inequality

Greater productivity dispersion

16

Comprehensive and collective policy action is needed to deliver on promises

17

Failure to get out of the low-growth trap means broken promises to the youth

Note: For LHS, OECD is the unweighted average of 34 OECD countries. 2013 for Chile and the United States. Youth aged 15-24 for Japan. Source: OECD calculations based on national labour force surveys; OECD Short-Term Labour Market Statistics database.

Inactive and unemployed youth Share of all youth (15-29 years old)

Change in OECD employment rate From Q4 2007 to Q4 2015, % pts

Unemployment in the first 10 years of a worker’s career leads to large differences in life-time earnings

18

Keeping promises to older people is more difficult with low returns and low growth

Policy reforms become more urgent, including extending working lives

Falling retirement income for a given contribution

Note: The chart shows the impact of falling interest rates on real incomes in retirement for a defined contribution scheme. Annuity payments calculated for the same hypothetical individual contributing 10% of wages over a 40 year period. The assets are invested in a portfolio comprising 60% of variable income (fixed return of 4.5%) and 40% of fixed income (historical 10 year government bonds yields, kept to maturity) and used at retirement to buy an annuity with a life expectancy of 20 years at age 65 using actual government bond yields for calculating the annuity premium. Constant annual inflation of 2 per cent and productivity growth of 1.5 per cent are assumed. Source: OECD Business and Finance Outlook 2016 (forthcoming).

19

Year of retirement

Monetary policy is in unchartered waters

Negative central bank deposit rates in a number of economies

Source: Thomson Reuters.

Central bank balance sheets

20

Relying on monetary policy alone risks less effectiveness and harmful side effects

Some central banks are the dominant holders of government bonds

Share of total government debt securities

Falling bank share prices Per cent decline over the year to May 2016

Source: Central banks; Thomson Reuters; and OECD calculations.

21

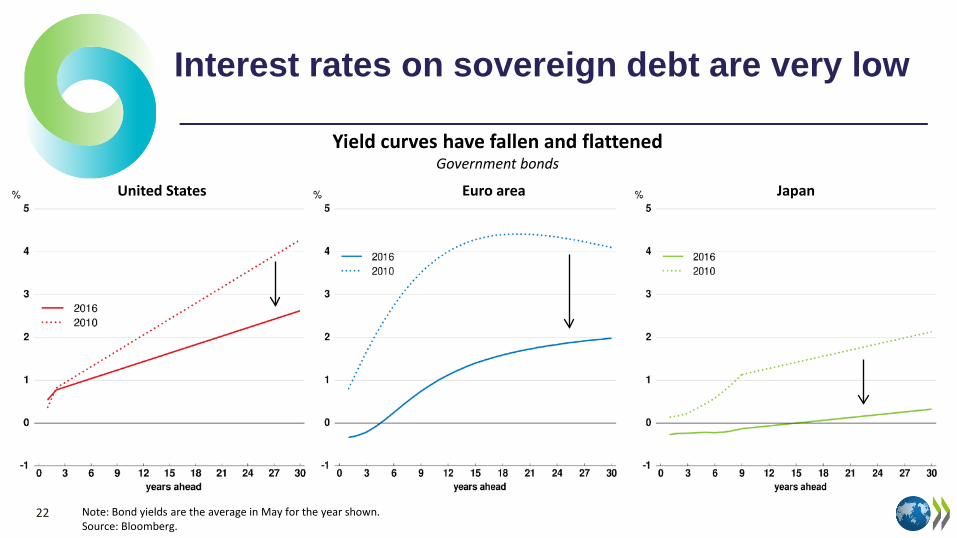

Interest rates on sovereign debt are very low

Yield curves have fallen and flattened Government bonds

Note: Bond yields are the average in May for the year shown. Source: Bloomberg.

22

United States Euro area Japan

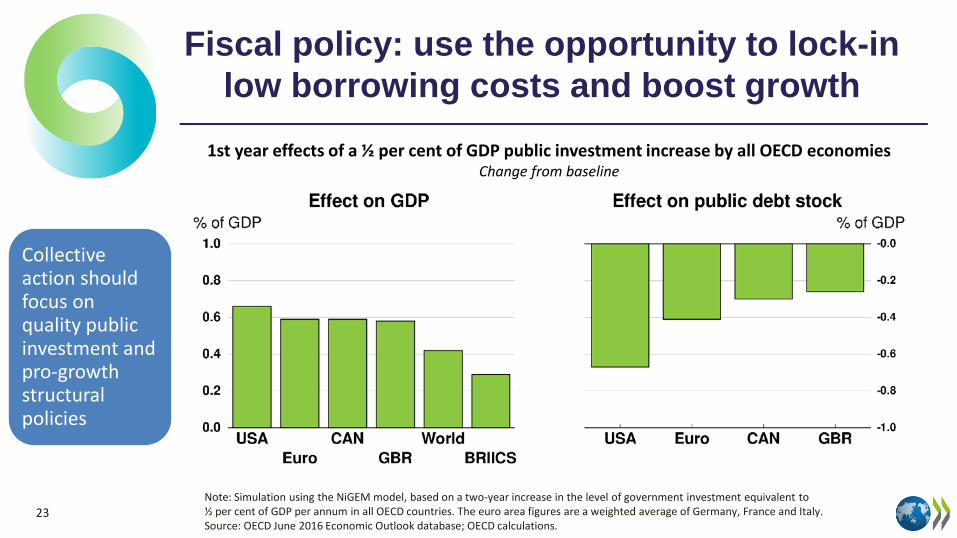

Fiscal policy: use the opportunity to lock-in low borrowing costs and boost growth

Note: Simulation using the NiGEM model, based on a two-year increase in the level of government investment equivalent to ½ per cent of GDP per annum in all OECD countries. The euro area figures are a weighted average of Germany, France and Italy. Source: OECD June 2016 Economic Outlook database; OECD calculations.

Collective action should focus on quality public investment and pro-growth structural policies

1st year effects of a ½ per cent of GDP public investment increase by all OECD economies Change from baseline

23

Structural policies to increase productivity can also boost demand and employment

Note: EMEs include Brazil, Chile, China, Colombia, India, Indonesia, Mexico, Russia, Turkey and South Africa; Mexico and Turkey only prior to 2011. Advanced includes the rest of the OECD. Source: OECD Going for Growth 2016.

Shift the composition of public spending to investment Encourage firm entry and investment in service sectors Reduce barriers to geographic and jobs mobility Package simultaneous labour and product market reforms Improve function of financial system and access to credit

The pace of structural reform has slowed Share of OECD Going for Growth recommendations implemented

Unique package for each country:

24

In the euro area, financial sector reforms are a key priority

Speed up resolution of non-performing loans: prudential tools and asset management companies can help

Complete banking union: set up a common backstop to the Single Resolution Fund and deposit insurance at the European level

25

0

5

10

15

20

25

2010 2011 2012 2013 2014 2015¹

France Germany Italy Spain Ireland Portugal

Non-performing loans (% of total)

1. Average of first three quarters. Source: European Central Bank.

Summary

Diagnosis: Low-growth trap • Subdued investment, trade, employment, wage, and productivity growth

Risks: Substantial downside •Brexit, EME financial vulnerabilities, increased financial market volatility

Consequences: Broken promises to young, old, investors • Slowing productivity, reduced long-term growth prospects, rising inequality

Recommendations: Comprehensive, coherent, collective action •Quality public investment, country-specific structural reforms, reduce

burden on monetary policy

Outcome: A high-growth path that keeps promises • Stronger investment, trade, employment, consumption, productivity, equity 26

Designing the public finances to promote growth and equity

27

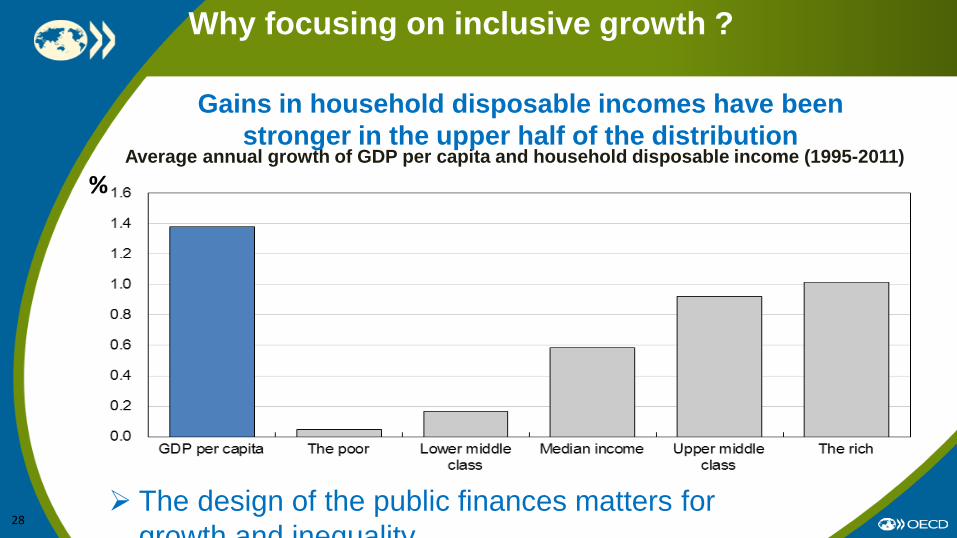

Average annual growth of GDP per capita and household disposable income (1995-2011)

Why focusing on inclusive growth ?

%

Gains in household disposable incomes have been stronger in the upper half of the distribution

The design of the public finances matters for growth and inequality

28

Redistribution mainly occurs via transfers

Reduction in the GINI coefficient due to taxes and transfers, %

Source: OECD Income distribution data base 29

The structure of spending has remained fairly stable

Average across OECD countries, % of potential GDP

Public investment Public investment Public investment

Education EducationEducation

Health HealthHealth

Old-age and survivor pensions

Old-age and survivor pensions

Old-age and survivor pensions

Sickness and disabilitySickness and disability Sickness and disabilityUnemployment benefitsUnemployment benefits Unemployment benefitsFamily and child

Family and child Family and child

Wages and intermediate consumption - other

purposes

Wages and intermediate consumption - other

purposes

Wages and intermediate consumption - other

purposes

SubsidiesSubsidies Subsidies

Other primary expenditureOther primary expenditure Other primary expenditure

0

5

10

15

20

25

30

35

40

45

2001 2007 2013

30

Design of public spending, growth and inequality

Key issue: Sustain long-term growth while addressing inequality. Design of public finance matter as the effect of type of spending

and tax on growth and inequality likely differ.

Empirical set-up: Growth: Neoclassical convergence model Inequality: Empirical framework estimates the impact of the mix of spending along the distribution of household income.

Insights:

• Effect of the size and the mix of public spending on growth and inequality

31

Main results of public spending reforms on growth and inequality

Policy Growth Equity Countries with the most room for growth gains

Decrease in the size of the government

Low to moderate government effectiveness + -

BEL, CZE, FRA, GRC, HUN, ITA, POL, PRT, SVN High government

effectiveness n.s. -

Increasing government effectiveness + + FRA, GRC, HUN, ITA, SVN

Increasing education outcomes + 0/+ CHL, GRC, MEX, PRT, TUR

Increasing public investment + n.s. BEL, DEU, GBR, IRL, ISR, ITA, MEX, TUR

Reducing pension spending + n.s. AUT, DEU, FIN, FRA, GRC, ITA, JPN, POL, PRT, SVN

Increasing family benefits n.s. + CHE, ESP, GRC, PRT

Decreasing public subsidies + - BEL, CHE

32

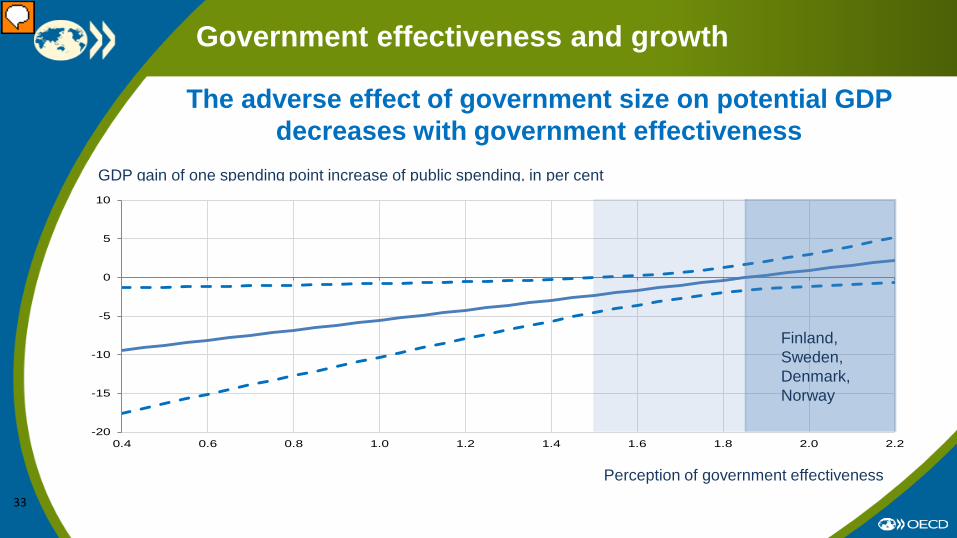

Government effectiveness and growth

The adverse effect of government size on potential GDP decreases with government effectiveness

GDP gain of one spending point increase of public spending, in per cent

Perception of government effectiveness

-20

-15

-10

-5

0

5

10

0.4 0.6 0.8 1.0 1.2 1.4 1.6 1.8 2.0 2.2

Finland, Sweden, Denmark, Norway

33

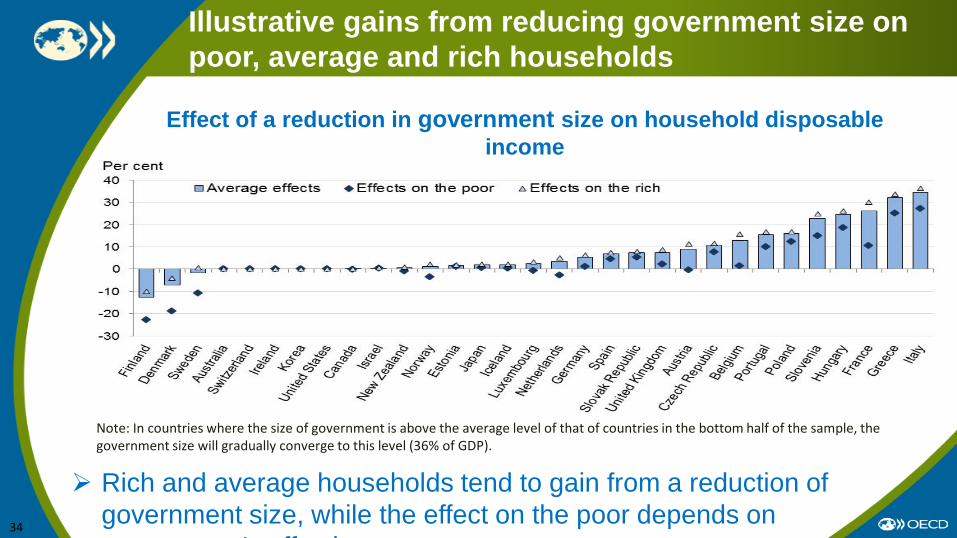

Illustrative gains from reducing government size on poor, average and rich households

Note: In countries where the size of government is above the average level of that of countries in the bottom half of the sample, the government size will gradually converge to this level (36% of GDP).

Rich and average households tend to gain from a reduction of government size, while the effect on the poor depends on

t’ ff ti

Effect of a reduction in government size on household disposable income

34

Decreasing returns to public investment?

The effect of public investment on potential GDP decreases with the level of capital stock

The analysis suggests that all OECD countries, except Japan, have room for additional public investment.

GDP gain of one spending point increase of public investment, in per cent

Public capital stock, per cent of potential GDP

-15

-10

-5

0

5

10

15

20 40 60 80 100 120

United States, Luxembourg, Iceland

Japan

35

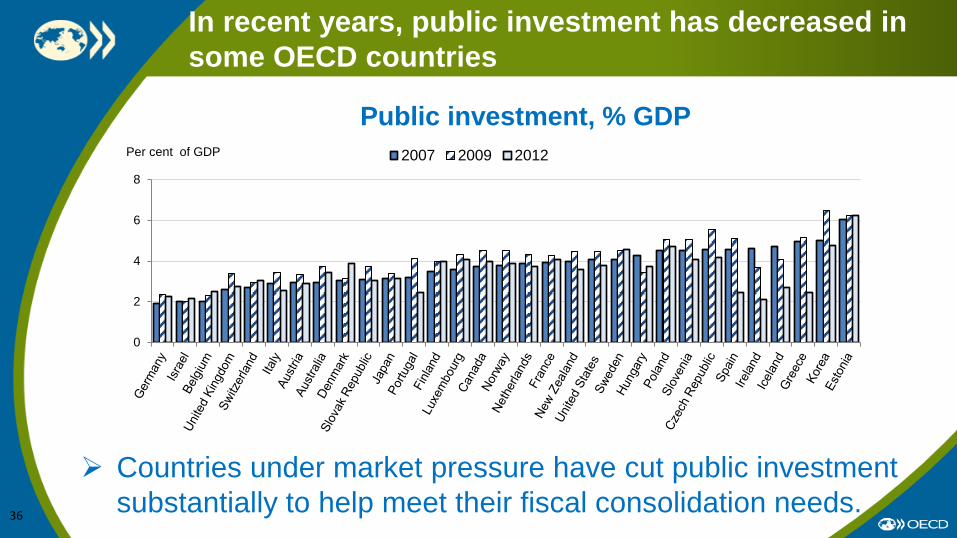

In recent years, public investment has decreased in some OECD countries

Public investment, % GDP

Countries under market pressure have cut public investment substantially to help meet their fiscal consolidation needs.

36

0

2

4

6

8

Per cent of GDP 2007 2009 2012

Thank you

www.oecd.org/economy/economicoutlook.htm

ECOSCOPE blog: oecdecoscope.wordpress.com/