˘ˇˆ˙˝˛˚˜˘ˇˆ˙˝˛˚˜ ˚!"#$% vehicle makers are challenged by chinese automakers...

TRANSCRIPT

���������� ��� ���� ��������

����� ����� �!"#$%���

0%

1%

2%

3%

4%

5%

6%

7%

0

10

20

30

40

50

60

70

2009 2010 2011 2012 2013 2014 2015 2016

(1,000 units)

�4%

�2%

0%

2%

4%

6%

8%

10%

� 20

� 10

0

10

20

30

40

50

2009 2010 2011 2012 2013 2014 2015 2016

(1,000 units)

0%

2%

4%

6%

8%

10%

12%

0

2

4

6

8

10

12

2009 2010 2011 2012 2013 2014 2015 2016

(1,000 units)

0%

1%

2%

3%

4%

5%

6%

7%

8%

0

100

200

300

400

500

600

700

800

2009 2010 2011 2012 2013 2014 2015 2016

(Units)

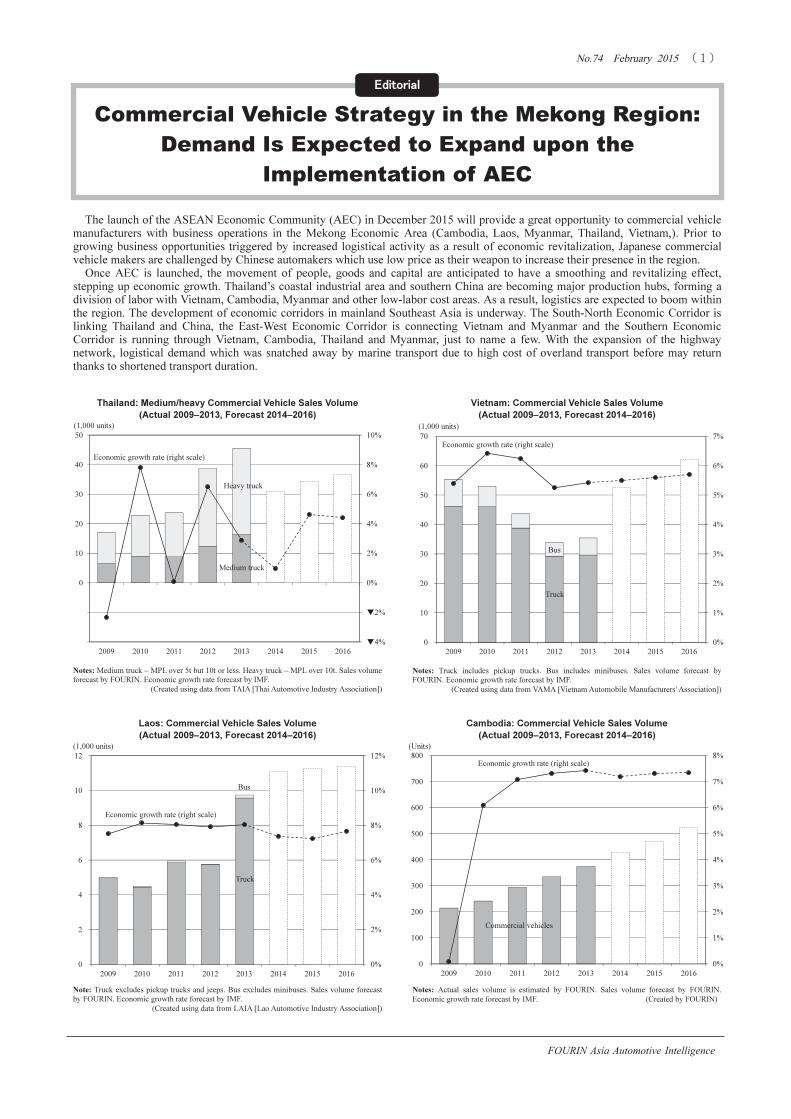

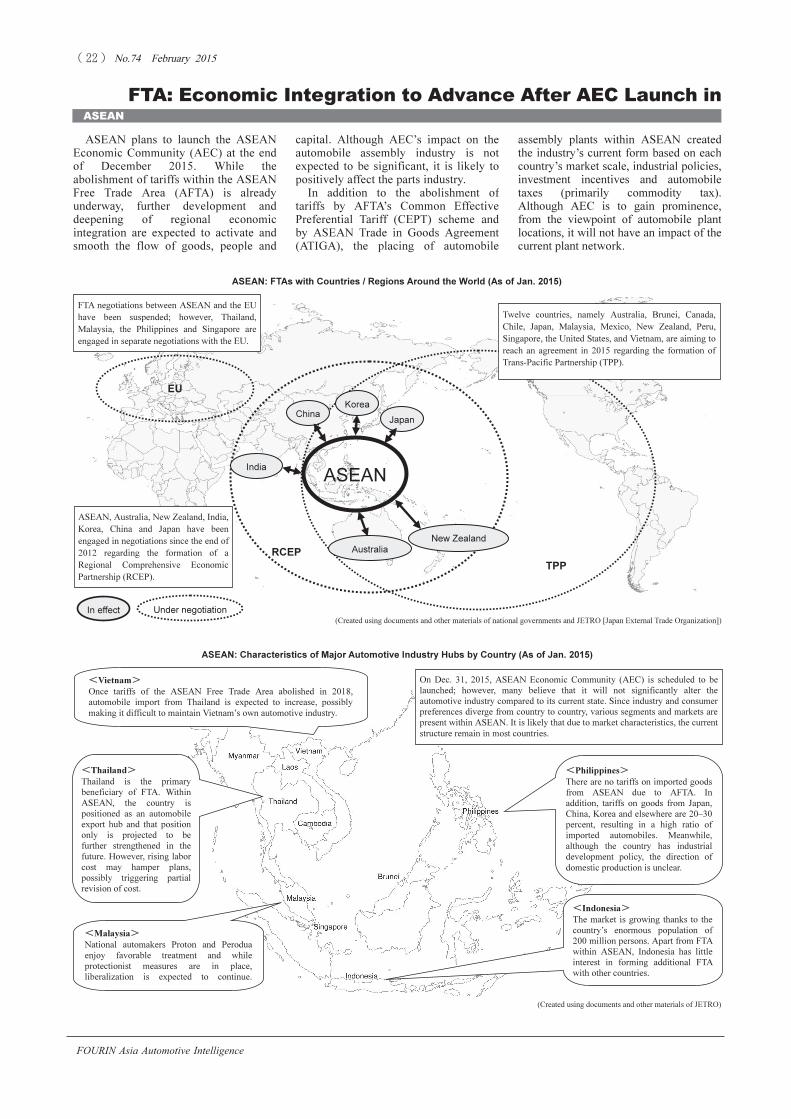

Commercial Vehicle Strategy in the Mekong Region:

Demand Is Expected to Expand upon the

Implementation of AEC

The launch of the ASEAN Economic Community (AEC) in December 2015 will provide a great opportunity to commercial vehicle

manufacturers with business operations in the Mekong Economic Area (Cambodia, Laos, Myanmar, Thailand, Vietnam,). Prior to

growing business opportunities triggered by increased logistical activity as a result of economic revitalization, Japanese commercial

vehicle makers are challenged by Chinese automakers which use low price as their weapon to increase their presence in the region.

Once AEC is launched, the movement of people, goods and capital are anticipated to have a smoothing and revitalizing effect,

stepping up economic growth. Thailand’s coastal industrial area and southern China are becoming major production hubs, forming a

division of labor with Vietnam, Cambodia, Myanmar and other low-labor cost areas. As a result, logistics are expected to boom within

the region. The development of economic corridors in mainland Southeast Asia is underway. The South-North Economic Corridor is

linking Thailand and China, the East-West Economic Corridor is connecting Vietnam and Myanmar and the Southern Economic

Corridor is running through Vietnam, Cambodia, Thailand and Myanmar, just to name a few. With the expansion of the highway

network, logistical demand which was snatched away by marine transport due to high cost of overland transport before may return

thanks to shortened transport duration.

��������

Thailand: Medium/heavy Commercial Vehicle Sales Volume

(Actual 2009–2013, Forecast 2014–2016)

Vietnam: Commercial Vehicle Sales Volume

(Actual 2009–2013, Forecast 2014–2016)

Laos: Commercial Vehicle Sales Volume

(Actual 2009–2013, Forecast 2014–2016)

Cambodia: Commercial Vehicle Sales Volume

(Actual 2009–2013, Forecast 2014–2016)

Medium truck

Heavy truck

Notes: Medium truck – MPL over 5t but 10t or less. Heavy truck – MPL over 10t. Sales volume

forecast by FOURIN. Economic growth rate forecast by IMF.

(Created using data from TAIA [Thai Automotive Industry Association])

Economic growth rate (right scale)

Truck

Bus

Economic growth rate (right scale)

Notes: Truck includes pickup trucks. Bus includes minibuses. Sales volume forecast by

FOURIN. Economic growth rate forecast by IMF.

(Created using data from VAMA [Vietnam Automobile Manufacturers' Association])

Note: Truck excludes pickup trucks and jeeps. Bus excludes minibuses. Sales volume forecast

by FOURIN. Economic growth rate forecast by IMF.

(Created using data from LAIA [Lao Automotive Industry Association])

Truck

Bus

Economic growth rate (right scale)

Economic growth rate (right scale)

Notes: Actual sales volume is estimated by FOURIN. Sales volume forecast by FOURIN.

Economic growth rate forecast by IMF. (Created by FOURIN)

Commercial vehicles

���������� ��� ���� ��������

����� ����� �!"#$%���

0

20

40

60

80

100

120

140

160

0

200

400

600

800

1,000

1,200

1,400

1,600

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

(1,000 units)(Billion USD)

Myanmar

Cambodia

Laos

Vietnam

Thailand

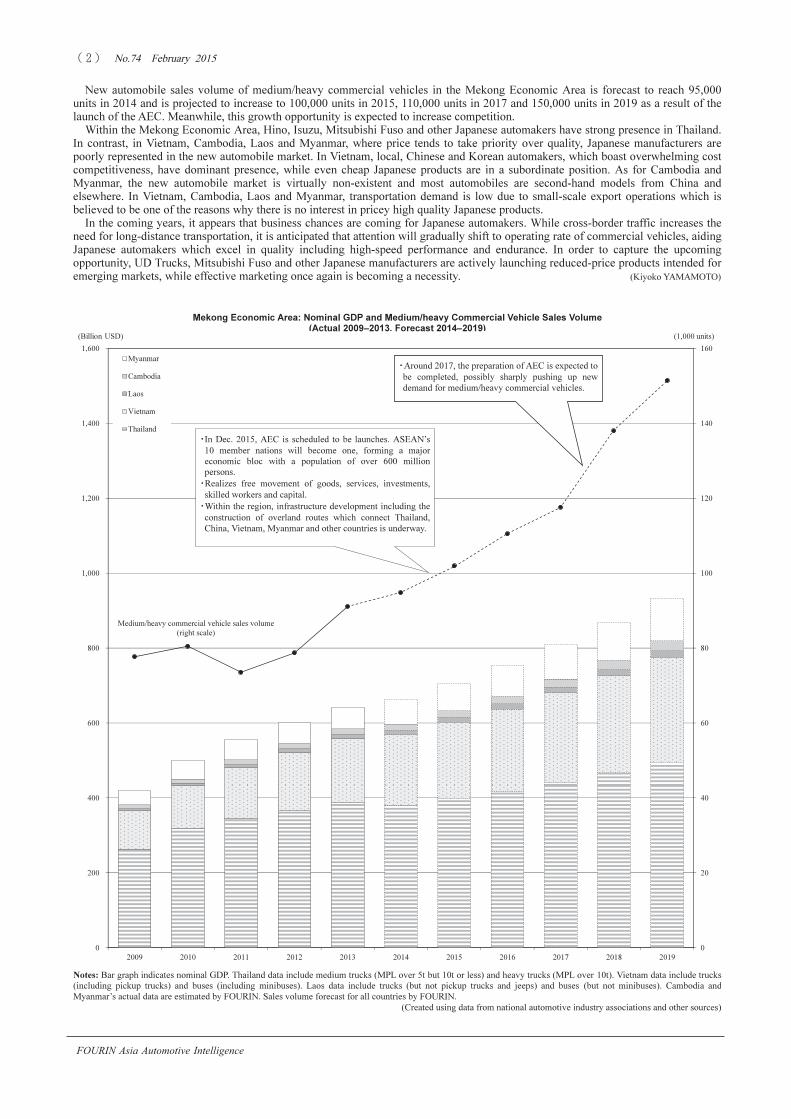

New automobile sales volume of medium/heavy commercial vehicles in the Mekong Economic Area is forecast to reach 95,000

units in 2014 and is projected to increase to 100,000 units in 2015, 110,000 units in 2017 and 150,000 units in 2019 as a result of the

launch of the AEC. Meanwhile, this growth opportunity is expected to increase competition.

Within the Mekong Economic Area, Hino, Isuzu, Mitsubishi Fuso and other Japanese automakers have strong presence in Thailand.

In contrast, in Vietnam, Cambodia, Laos and Myanmar, where price tends to take priority over quality, Japanese manufacturers are

poorly represented in the new automobile market. In Vietnam, local, Chinese and Korean automakers, which boast overwhelming cost

competitiveness, have dominant presence, while even cheap Japanese products are in a subordinate position. As for Cambodia and

Myanmar, the new automobile market is virtually non-existent and most automobiles are second-hand models from China and

elsewhere. In Vietnam, Cambodia, Laos and Myanmar, transportation demand is low due to small-scale export operations which is

believed to be one of the reasons why there is no interest in pricey high quality Japanese products.

In the coming years, it appears that business chances are coming for Japanese automakers. While cross-border traffic increases the

need for long-distance transportation, it is anticipated that attention will gradually shift to operating rate of commercial vehicles, aiding

Japanese automakers which excel in quality including high-speed performance and endurance. In order to capture the upcoming

opportunity, UD Trucks, Mitsubishi Fuso and other Japanese manufacturers are actively launching reduced-price products intended for

emerging markets, while effective marketing once again is becoming a necessity. (Kiyoko YAMAMOTO)

Mekong Economic Area: Nominal GDP and Medium/heavy Commercial Vehicle Sales Volume

(Actual 2009–2013, Forecast 2014–2019)

Medium/heavy commercial vehicle sales volume

(right scale)

�In Dec. 2015, AEC is scheduled to be launches. ASEAN’s

10 member nations will become one, forming a major

economic bloc with a population of over 600 million

persons.

�Realizes free movement of goods, services, investments,

skilled workers and capital.

�Within the region, infrastructure development including the

construction of overland routes which connect Thailand,

China, Vietnam, Myanmar and other countries is underway.

�Around 2017, the preparation of AEC is expected to

be completed, possibly sharply pushing up new

demand for medium/heavy commercial vehicles.�

Notes: Bar graph indicates nominal GDP. Thailand data include medium trucks (MPL over 5t but 10t or less) and heavy trucks (MPL over 10t). Vietnam data include trucks

(including pickup trucks) and buses (including minibuses). Laos data include trucks (but not pickup trucks and jeeps) and buses (but not minibuses). Cambodia and

Myanmar’s actual data are estimated by FOURIN. Sales volume forecast for all countries by FOURIN.

(Created using data from national automotive industry associations and other sources)

���������� ��� ���� ��������

����� ����� �!"#$%���

Note: Indicates major border areas with mutual vehicle entry points.

(Created using documents of the GMS-CBTA [Greater Mekong Subregion Cross-Border Transport Agreement] and other sources)

Mekong Economic Area: Major Border Areas with Mutual Vehicle Entry Points

Jun. 2012: Thailand and Cambodia agreed to allow

mutual entry at Aranyaprathet on the Thai side and at

Poipet on the Cambodian side. Trucks and buses

can now travel between Bangkok and Siem Reap,

and between Bangkok and Phnom Penh.�

Mutual entry was allowed at five locations

along the Vietnam-Cambodia border including

between Cambodia’s Bavet and Vietnam’s

Moc Bai as of 2013.�

2005: Laos and Vietnam concluded an

agreement to regarding the trial

implementation of single-stop inspection (SSI)

at Lao-Bao on the Laotian side and at

Dansavanh on the Vietnamese side. As a

result, customs time dropped from 90 minutes

to 29 minutes.�

Aug. 2012: At three locations, trucks and

buses are now allowed to make mutual entry

along the Vietnam–China border. As a result,

cargo can moved from Hanoi toward

Guangzhou and elsewhere without having to

be reloaded.�

May 2013: China and Laos agreed to

increase mutual-entry quota for trucks

and buses to 20,000 units each.

Implemented in 2013.�

The East-West Economic Corridor is a trunk

road that crosses Vietnam, Laos and Thailand.

Although triple license is necessary when

three countries are crossed, it was limited to

traffic area between Vietnam’s Danang and

Thailand’s Khon Kaen as of 2012.�

Northern Economic Corridor

Western Economic Corridor

South-North Economic Corridor

Eastern Economic Corridor

Central Economic Corridor

Southern Coastal Economic

Corridor

Southern Economic Corridor

East-West Economic Corridor

North-East Economic Corridor

���������� ��� ���� ��������

����� ����� �!"#$%���

FOURIN Asia Automotive Intelligence

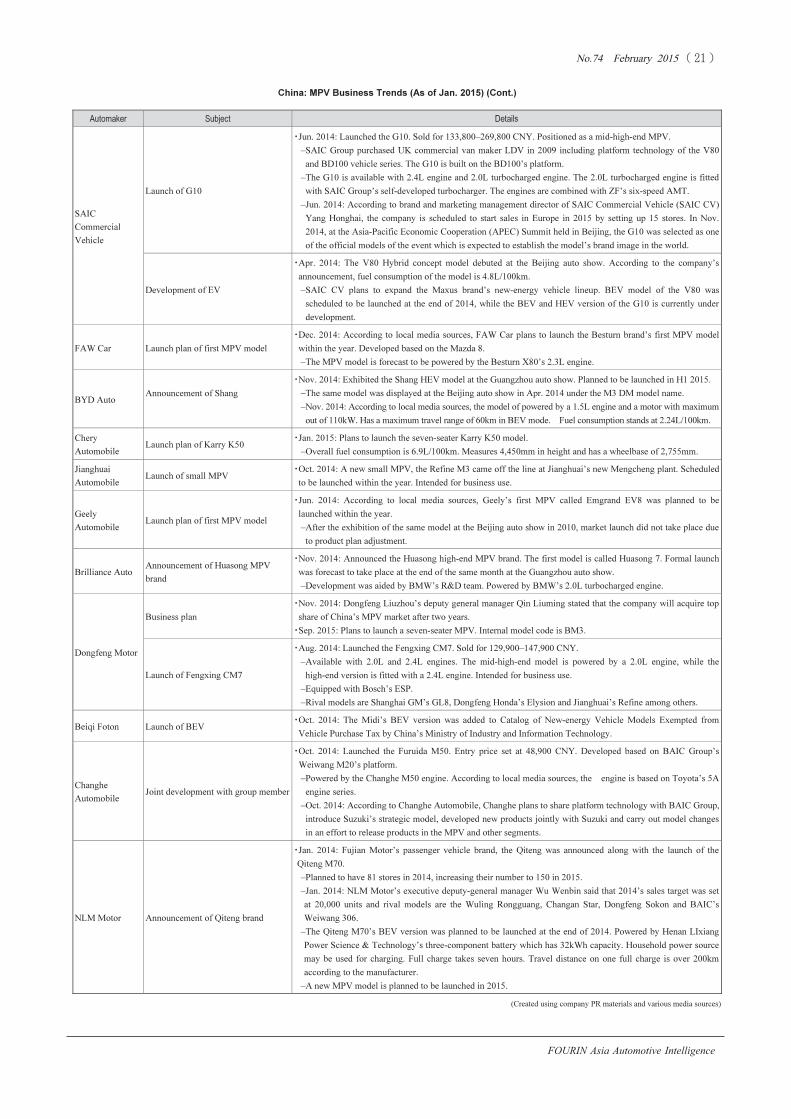

Proton Interview:

Launches the Iriz Powered by New VVT Engine;

Aims to Revive Sales by Stressing Safety

10%

15%

20%

25%

30%

0

50

100

150

200

2009 2010 2011 2012 2013 2014

Market share (right scale)

Passenger car

sales volume

(left scale)

MPV etc.

(1,000 units)

Malaysia’s national car maker Proton is

aiming to strengthen product

competitiveness, improve sales and

aftersales service network productivity

and enhance marketing in pursuit of

reviving share. Looking at products, the

in-house developed new hatchback Iriz

designed new models. After the launch of

the Prevé sedan in 2012, the Suprima S

hatchback was released in August 2013.

Meanwhile, in response to consumer

needs, Proton is forging ties with other

companies to be able to offer a wider

range of automobiles and powertrains.

went on sale in September 2014. With

enhanced safety, the Iriz is expected to

reclaim share. In addition, built on the

Iriz’s platform, the B segment’s lineup is

planned to be revamped and expanded. In

the C segment, Proton has expanded

product lineup with the launch of in-house

(Created using data from MAA)

Proton: Automobile Sales Volume by Type and Market Share in

Malaysia (2009–2014)

Proton: Automobile Production Volume Composition

by Model in Malaysia (2014)

(Created using data from MAA/Malaysian Automotive Association)

Proton: Automobile Sales Volume by Type in Malaysia (2009–2014)

(Created using data from MAA)

Proton: Automobile Production Volume by Model in Malaysia (2009–2014)

(Created using data from MAA)

Saga

49.7%

Persona

20.9%

Exora

11.2%

Prevé

8.3%

Iriz

7.4%

Others

2.5%

(Units)

Type 2009 2010 2011 2012 2013 2014 Year-on-year

Passenger car 129,293 130,173 137,535 117,004 115,770 100,431 ▼13.2%

MPV 18,451 26,787 21,064 24,113 22,983 15,352 ▼33.2%

Van - - 2 3 - - -

Pickup truck 287 314 56 1 - - -

Automobile sales volume 148,031 157,274 158,657 141,121 138,753 115,783 ▼16.6%

Automobile market share 27.6% 26.0% 26.4% 22.5% 21.2% 17.4% ▼3.8pp

(Units)

Platform Model 2009 2010 2011 2012 2013 2014

Period-on-

period

Saga (second-gen) 69,164 72,252 78,732 70,025 70,025 55,613 ▼20.6%

Persona 44,071 49,884 47,370 28,831 17,032 23,352 37.1%

Iriz - - - - - 8,272 -

Satria Neo�

4,301 4,921 2,865 414 1,916 596 ▼68.9%

Gen.2 3,051 4,248 981 1,148 1,489 245 ▼83.5%

Savvy 4,586 2,751 887 - - - -

Waja 3,139 5,304 1,462 - - - -

Exora 23,224 28,074 23,644 30,711 24,376 12,506 ▼48.7%

Prevé - - - 26,303 18,403 9,282 ▼49.6%

Suprima S - - - - 4,289 712 ▼83.4%

Inspira - 2,144 10,288 3,980 2,552 1,262 ▼50.5%

Others 2,445 1,030 - - - - -

Automobile production total 153,981 170,608 166,229 161,412 140,082 111,840 ▼20.2%

In-house developed

C segment

In-house developed

B segment

Mitsubishi Lancer etc.

���������� ��� ���� ��������

����� ����� �!"#$%���

FOURIN Asia Automotive Intelligence

Searching for ways to revive sales as

domestic demand falls below 20 percent

In the Malaysian vehicle market,

where the two national automakers

Proton and Perodua have a commanding

presence, non-national competitors are

enhancing product lineup in recent years

in an aim to capture a stable demand of

600,000–700,000 units annually. As a

result, Proton’s market share has dropped

over 10 percentage points in the past 10

years. In 2014, market share fell below

20 percent, continuing to face severe

market conditions.

Seeing the urgent need of rebuilding

“effective implementation of integrated

marketing.” More concretely, in order to

improve product competitiveness, the

automaker has been focusing on areas

such as quality, pricing, safety and fuel

efficiency. Regarding the Iriz, the results

of these efforts have come to fruition.

However, in order to make sure that

consumers recognize these positive

results, it is necessary to implement

effective marketing. As for the

automaker’s sales and aftersales service

network which covers nearly all of

Malaysia, Proton intends to efficiently

locate dealerships, improve product

production and sales, Proton put forth a

five-year business plan set in 2013 in an

effort to revive share at home and seize

growth opportunities overseas. Although

the actual target figures of this five-year

plan are not revealed, in November 2014

FOURIN interviewed Proton’s General

Manager of Corporate Strategy Yusri

Yusuf who said that “In general, the plan

remains. Nonetheless, we have some

reviews on several target settings…”

Mr. Yusri explained that the present

business policy is concentrating on three

areas namely “product range,”

“strengthening network efficiency” and

Q: I would like you to explain the 5-year Business Plan.

A: In general, the plan remains. Nonetheless we have some reviews on

several target settings to align with the progression of market condition,

both in domestic and international markets. This review will cover

both operational aspects as well as the business approach in order to

enable us attaining the targets set.

A: At the same time, we will continue to pursue our intention in

maximizing the potentials of the existing product range and powertrain

family, especially in terms of fuel efficiency, performance and the

overall package. These activities are spearheaded by Research &

Development team based in Shah Alam and supported by Lotus

Engineering team in the United Kingdom.

A: In terms of manufacturing, our aim is to optimize the available

production capacities at our plants in Shah Alam and Tanjung Malim,

covering the complete manufacturing processes of iron casting,

machining, engine assembly, body assembly, stamping, hot press

forming, painting and vehicle assembly, supported by quality

management, logistics and supply chain management.

Q: What is your strategy to revive market share?

A: Long-term strategies are set to align with the vision and mission of the

company. In order to enable the trajectory towards achieving those

targets, specific focus areas have been identified which include:

A: 1. Enhancing product range and aligning to consumers’ expectations,

particularly in the aspects of quality, features and price positioning.

A: 2. Strengthening network efficiency in terms of coverage and productivity

of sales and after-sale services. From the vast number of outlets in the

country, we are more looking at how to leverage on the coverage and

improving our operations, such as product knowledge, soft-skills,

customer service level etc. These areas will eventually be measured in

the aspects of customer satisfaction level, covering products, sales and

services.

A: 3. Effective implementation of integrated marketing programs is also

an important area to enable our effort to communicate our strengths and

product benefits, and more importantly relaying the useful information

to our consumers.

Q: Would you tell me your product strategy and plan? You have just

launched the Iriz. And you are working on the Irox, aren’t you?

A: Today we have our own platforms as the base for models in the B

segment and C segment. The Proton Iriz which was launched in

September 2014 has received commendable feedback from the market

and recently awarded with pinnacle recognitions of Maybank-NST Car

of The Year 2014 in two categories, namely Compact Hatchback and

People’s Choice Award. We will now work on how to maximize the

Iriz platform to push into other variants.

A: Other active models of Saga, Persona, Exora, Prevé and Suprima S

continue to provide significant contributions towards fulfilling market

requirements, both in domestic and export markets. We will continue

working on these models to enhance them and put better proposition.

This is our focus for now.

�PROTON Centre of Excellence�

Interview with Perusahaan Otomobil Nasional Sdn. Bhd. (PROTON�

General Manager, Corporate Strategy Mr. Yusri Yusuf

On November 20, 2014, at PROTON Centre of Excellence (main office) in Shah Alam, Selangor, Malaysia

Proton: Aiming to Revive Share Centered on Products, Network and Marketing

���������� ��� ���� ��������

����� ����� �!"#$%���

FOURIN Asia Automotive Intelligence

knowledge of sales staff, advance

aftersales service techniques and boost

customer satisfaction.

New Iriz is to become the core platform

of the next-gen B segment

In order to revive market share, the

most important thing is to improve

product competitiveness. For Proton,

which is looking for growth

opportunities in export markets, it is

indispensable to strengthen and expand

its lineup through in-house development.

Accordingly, new model development in

the core B and C segment is underway.

However, with an annual production

scale of some 150,000 units, Proton is

unable to independently develop various

lineups. As a result, the automaker

intends to continue partnership and

cooperation with other manufacturers in

the areas of automobiles and

powertrains.

In September 2014, Proton began

sales of the new hatchback Iriz in

Malaysia. The Iriz is the first model

which is fitted with the Campro series’

VVT engine (1.3L/1.6L) and also

features electronic stability control and

other vehicle dynamics control

technologies. In an effort to strengthen

vehicle body structure, Proton

introduced hot-pressed parts and

high-strength steel, earning the five stars

on the ASEAN NCAP’s collision safety

evaluation. For the Iriz, which is

�Proton Iriz�

Q: Is the Iriz fully developed by Proton? Is the platform newly developed

from scratch? Let me know about your own R&D capability?

A: Waja was the first model fully developed by Proton, in which the

development activities started in 1996 and eventually launched in 2000.

The platform was further optimized through the introduction of the

stylish hatchback Proton Gen.2 in 2004, powered by our own Campro

engine and manufactured in the new state-of-the-art plant in Tanjung

Malim. The platform was further spun�off with the introduction of

Persona in 2007, leveraging on the existing parts bin. Satria Neo,

launched earlier in 2006, has also adopted a significant level of

commonality from the same platform.

A: The compact hatchback Savvy was another model designed and

developed ground-up by PROTON. The platform was further enhanced

through the introduction of the new Saga in 2008.

A: Later in 2009, the Exora was launched as PROTON’s first 7-seater

multi-purpose vehicle. Based on this platform, the Prevé and

Suprima S was introduced to the market in 2012 and 2013

respectively, providing a high level of occupant safety and drivability

performance to consumers.

A: The Iriz is developed on a totally new platform as a replacement to

B-segment vehicles. We are now studying the potential of the

platform in terms of spinning it off to produce other models.

A: In terms of engine, PROTON introduced the first version of Campro

1.3-litre and 1.6-litre in 2004. The engine was further enhanced with

the CPS version that features additional 10% of power output.

Subsequently, a more refined performance and fuel efficient IAFM and

IAFM+ engine variants were introduced, followed by the 1.6-litre

CFE Turbo engine in 2011. Based on the technologies and learnings

from the CFE and IAFM+, the 1.3-litre and 1.6-litre VVT engines were

introduced on the Iriz, emphasizing on fuel efficiency.

A: Concurrently, collaborative opportunities will continue to be explored to

fulfill market needs.

Q: The Iriz comes with a 1.6L engine. Do you think this is too big for a B

segment car? In the meantime, the Malaysia government is

promoting fuel efficient vehicles. Due to this policy, smaller engine

displacement seems to match. What is your strategy to catch up with

those trends and issues?

A: In terms of body size, the Iriz fits well in providing the needs and

preferences of its customer group of B-segment hatch, either as first

car, additional car or replacement car purchase. While 1.3-litre VVT

engine provides the expected needs to the target customer group, the

1.6-litre VVT engine offers the customers with a high performance

option with respectable fuel efficiency. Nonetheless, it is also natural

for consumers to make comparisons in other areas of interest.

A: In other segments, PROTON is represented by the Persona, Prevé and

�Proton Iriz�

Proton: Aiming to Revive Share Centered on Products, Network and Marketing (Cont.)�

���������� ��� ���� ��������

����� ����� �!"#$%���

FOURIN Asia Automotive Intelligence

anticipated to have a leading role in

reviving share, improved safety

performance is lending a special appeal.

With a base price of 42,438 MYR, it is

set nearly on the same level as its rival

the Perodua Myvi (1.3L only).

The Iriz platform is used as the

platform of new in-house designed B

segment cars and models are to be

positioned as the successors of the

Savvy/Saga series. Proton intends to

maximize the use of the Iriz platform by

launching two variant models or more in

the future. Based on this platform,

product lineup in the B segment is

planned to be revamped and expanded.

According to local media sources, the

next-gen Saga (small sedan) seems to be

built on this platform.

As for the EEV (Energy Efficient

Vehicle) policy, which is introduced by

the Malaysian government, Perodua’s first

EEV-compliant model the Axia small

hatchback was released in September

2014, while Proton is yet to launch its

own EEV product. Proton considers the

EEV policy very important, and so the

automaker is focusing on powertrain

improvement, as well as conducting EV

and HEV product development and

marketing research in cooperation with

major suppliers. Although Mr. Yusri

declined to confirm it, local media

sources say that Proton may enter the EV

or HEV market in the second half of

2016 or later. (Toru NAKATA)

�Proton Iriz�

Suprima S as well as the Exora, in which these models have different

sets of competition and expectations in the market.

Q: What is sales target for the Iriz? Do you disclose this kind of figures?

A: It is always natural for any company to achieve the best results possible.

Q: I find the design of the Iriz iimpressive. What are the features of the

Iriz?

A: The Iriz is designed with emphasis on style and comfort, equipped with

various advanced features.

A: On top of its various features on convenience and practicality, the Iriz

has the highest level of occupant safety in its class, awarded with the

5-star ASEAN NCAP safety rating. On top of its reinforced safety

structure built with ultra-high strength steel (UHSS) and hot-press

forming (HPF) components, the Iriz is equipped with Vehicle Dynamic

Control system that provides a complete package of active safety, as

well as various features on passive safety. The new VVT engine and

superb ride-and-handling characteristics further enhance the overall

performance of the vehicle.

A: With these product strengths, effective marketing activities will enable

us to provide the right message and confidence to people.

Q: When did you start working on hot press and safety features?

A: PROTON started hot press forming production since 2012 for the

Prevé, followed by the Suprima S and now the Iriz. The technology is

adopted from a renowned origin from Europe and operated by our

subsidiary, Miyazu (Malaysia).

Q: Let me know about your R&D activity.

A: We have about 800 engineers & technical staff in R&D, mainly to cover

core areas from product planning, right down to design, vehicle

engineering, powertrain, engineering services and prototyping,

homologation and testing. In addition to our R&D center in Malaysia,

we also work together with Lotus Engineering in the UK especially in

their areas of expertise such as chassis and powertrain development.

Lotus has about 1,500 employees.

Q: What is your intention regarding the EEV policy?

A: EEV is a very important policy for PROTON as well as for the local

automotive industry. We have been working hard towards complying

with EEV requirements, particularly in the areas of engine (turbo and

non-turbo), transmission (manual, automatic and CVT) and vehicle

engineering.

Q: Let me know about your HEV and EV strategy. I thought your initial

plan was to launch EV and/or HEV by 2014-2015.

A: We are still in the research stage and at the same time, assessing all

requirements towards commercialization.

A: We are also assessing the infrastructure requirements with various parties

involved and will continue to monitor the dynamic of EV and hybrid

requirements by consumers.

Q: Are the EV and hybrid systems fully developed by Proton?

A: We have a dedicated in-house team who are also working closely with

key component suppliers. The important aspects are integration

activities to ensure consumers’ expectations are met, technically and

commercially.

Q: What is your perspective of the EV market in Malaysia?

A: The development of EV is important to PROTON and the local industry,

both in terms of vehicle and infrastructure. Our aim is to ensure that

customers’ expectations are fulfilled in all aspects, especially on

technical reliability and commercial viability.

(FOURIN)

Proton: Aiming to Revive Share Centered on Products, Network and Marketing (Cont.)�

���������� ��� ���� ��������

����� ����� �!"#$%���

FOURIN Asia Automotive Intelligence

Proton: Overview of Main Products (As of Dec. 2014)

Proton: Overview of the New Hatchback Iriz

MT CVT MT CVT MT CVT MT CVT

Price (MYR) 42,888 45,888 46,888 49,888 53,888 56,888 59,888 62,888

Occupant capacity (seating)

Length×width×height

Wheelbase

Ground clearance

Truck capacity

Engine

Maximum output

Maximum torque

Transmission 5-speed MT CVT 5-speed MT CVT 5-speed MT CVT 5-speed MT CVT

Vehicle body weight 1,130kg 1,150kg 1,138kg 1,158kg 1,150kg 1,170kg 1,165kg 1,185kg

Maximum speed 165km/h 160km/h 165km/h 160km/h 175km/h 170km/h 175km/h 170km/h

Minimum turning radius

Steering

Suspension

Brake

Keyless entry

Push-button start

Vehicle dynamics control (VDC)

Seatbelt pretensioner

Airbag

Parking assist

Collision safety evaluation

Infotainment

5 persons

Inline-4 1,597cc VVT gasolineInline-4 1,332cc VVT gasoline

3,920×1,722×1,554mm

Radio/CD, MP3 player, USB, AUX port, Bluetooth 6.2-inch LCD, DVD player, DSP, USB, AUX port, Bluetooth, Wi-Fi

1.6L1.3L

ExecutiveStandardExecutiveStandard

215L/270L

No

Front: Ventilated disc. Rear: Leading/trailing drum brake

5 stars (ASEAN NCAP)

No

Parking space displayed on monitor

(rearview camera + reverse sensor)

Yes

ABS with EBD, brake assist (BA), electronic stability control (ESC), traction control (TC), hill-hold assist (HHA)

6 airbags

(front, side, curtain)

YesNo

2,555mm

155mm

Front only

70kW (5,750rpm) 80kW (5,750rpm)

120Nm (4,000rpm) 150Nm (4,000rpm)

Electronic power steering (EPS)

5.0m

Yes

Front: Mcpherson strut / stabilizer bar. Rear: Torsion beam axle.

Model Type Model Source Market Launch Length Engine Transmission Base Price (MYR) Notes

Saga

(second-gen)

B segment,

sedan

In-house

development

Jan. 2008 4,278mm IAFM 1.3L/1.6L

5-speed MT,

CVT

33,488

Saga SE (launched in Jul. 2009), Saga

FLX (Jul. 2011), Saga FLX SE (Nov.

2011), Saga SV value edition (Jun.

2013), etc.

Iriz

B segment,

hatchback

In-house

development

Sep. 2014 3,920mm VVT 1.3L/1.6L

5-speed MT,

CVT

42,438

Rival model is the Perodua Myvi

among others. Apparently, it will be

exported to Europe and elsewhere.

Persona

B segment,

sedan

In-house

development

Aug. 2007 4,477mm IAFM 1.6L MT, AT 45,021

Sedan version of the Gen.2 which

was launched in 2004.

Satria Neo

B segment,

hatchback

In-house

development

2006 3,898mm CPS 1.6L MT, AT 50,515

The Waja and Gen.2 shares parts, but

their platform is different.

Prevé

C segment,

sedan

In-house

development

Apr. 2012 4,543mm

IAFM+ 1.6L,

CFE 1.6L

5-speed MT,

CVT (6-speed),

CVT (7-speed)

58,531

Developed based on the Exora.

Adopted hot-press parts to improve

body strength. Development cost was

540 million MYR.

Suprima S

C segment,

hatchback

In-house

development

Aug. 2013 4,436mm CFE 1.6L CVT 76,398

Variant model of the Prevé.

Apparently, development cost was

200 million MYR. Received five stars

on the ASEAN NCAP.

Inspira

C segment,

sedan

Mitsubishi

Lancer

Nov. 2010 4,570mm MIVEC 1.8L/2.0L

5-speed MT,

CVT

78,566

Positioned as the successor model of

the Waja.

Perdana

(second-gen)

D segment,

sedan

Honda Accord Dec. 2013 N.A. 2.0L/2.4L 5-speed AT N.A.

Began to be supplied as government

vehicle at the end of 2013. Not to be

sold to general customers.

Manufactured by Honda's plant.

Exora

C segment,

MPV

In-house

development

Apr. 2009 4,592mm

CPS 1.6L,

CFE 1.6L

5-speed MT,

CVT

59,995.5

Achieved local content of 90 percent.

Also has a luxury version called

Exora Prime.

���������� ��� ���� ��������

����� ����� �!"#$%���

FOURIN Asia Automotive Intelligence

Proton: In-house Development of Automobiles and Engines

(Created using Proton’s PR materials and FOURIN interview)

B segment

C segment

Platform

sharing

VariantGen.2 is the first model fitted with the in-

house developed Campro engine (Since the

Gen.2, all in-house developed models are

powered by the Campro engine)

2011: Production discontinuedWaja Campro

(2006)

Platform

extension

Savvy's sedan version

2010: Production discontinued

Plans to launch

variant modelsSavvy/Saga platform is planned to be used

for the Iriz series

2011: Sales discontinued in Malaysia

Gen.2's sedan version

Proton's first in-house developed MPV

Variant

Variant

Switch to Iriz platform?

Waja

(2000)

Gen.2

(2004)

Persona

(2007)

Savvy

(2005)

New Saga

(2008)

Iriz

(2014)

New models

(2015 or after)

Exora

(2009)

Prevé

(2012)

Suprima S

(2013)

Campro

series

engine

Exora was the first model fitted with CFE.

Preve and Suprima S also equipped with the

same engine.

Improved output

10 percent

Improved fuel

efficiency

Improved fuel

efficiency

Converted to turbo

Saga FLX was the first model fitted with IAFM+.

Preve also equipped with the same engine.

Iriz was the first model fitted with

VVT. Planned to be used for

additional models.

Waja was the first model fitted with CPS.

As of 2014, Exora and Satria Neo were equipped with CPS.

Compatible with 5-speed MT/

4-speed AT.

Available in 1.3L/1.6L.

Compatible with 5-speed MT/CVT.

Available in 1.6L only.

Combined with CVT.

Available in 1.3L/1.6L.

Compatible with 5-speed MT/CVT.

Waja was the first model fitted with IAFM.

As of 2014, Persona was equipped with IAFM.

Gen.2 was the first model fitted with the in-house developed

Campro engine . The Waja and Satria Neo were equipped

with the same engine. 2010: Discontinued use.

Campro

(2004)

IAFM

(2007)

CFE

(2011)

CPS

(2007)

IAFM+

(2007)

VVT

(2014)

Includes technology and knowhow from IAFM+ and CFE.

���������� ��� ���� ��������

����� ����� �!"#$%����

FOURIN Asia Automotive Intelligence

EECS Use in China:

Stricter Emission Regulations Force Weaker Suppliers

to Exit the Market

Beijing launched China 5 emission

standards that regulate passenger vehicle

emissions in March 2013 ahead of its

nationwide introduction in January 2018.

The evaporative emission control system

(EECS), a device which prevents the

emission of gasoline vapor into the

atmosphere, will become subject to

regulation with the introduction of China

5 emission standards.

FOURIN has compiled a list of

emission standard-compliant

automobiles announced by China’s

Ministry of Environmental Protection

with VW, GM and Ford. Meanwhile,

Mahle, Delphi and other Western

suppliers are engaged in securing new

orders in an effort to boost share. As for,

Japanese components makers, they

continue to supply affiliated Japanese

automakers. In the next fuel efficiency

regulation, which is currently under

review, on-board refueling vapor

recovery (ORVR) system is scheduled to

be introduced. After the launch of the

ORVR system, more suppliers are

forecast to drop out while competition is

expected to intensify.

and combined it with new passenger

vehicle registration data to create a

database on EECS use broken down to

supplier. As for Chinese suppliers, which

account for over half of all EECS supply,

some manufacturers exited the market

due to lack of technology needed for

switching from China 4 to China 5

emission standards, resulting in a drop in

Chinese share. Under these

circumstances, the largest local supplier

Langfang Hua’an Automotive

Equipment is maintaining share by

stepping up technological cooperation

China: EECS Volume by Supplier Origin and Supplier (2012–2013, YTD Sep. 2014)

Notes: Tentative calculation from new automobile registration data and EECS supply data. Unknown includes automobiles with diesel engine and with unknown supplier origin. Utility vehicles are not

included. (Created using data from China’s MEP [Ministry of Environmental Protection] and new automobile registration data)

� (Created using data from table below) (Created using data from table below)

China: EECS Share by Supplier Origin (2012–2013, YTD Sep. 2014) China: EECS Share by Supplier (2012–2013, YTD Sep. 2014)

(Units)

Volume Share Volume Share Share Change Volume Share Share Change

China 6,534,203 54.4% 7,810,257 56.2% 1.8pp 6,339,374 54.7% ▼1.5pp

Japan 2,035,068 17.0% 2,298,707 16.5% ▼0.4pp 1,855,618 16.0% ▼0.5pp

EU 1,640,908 13.7% 1,589,227 11.4% ▼2.2pp 1,522,593 13.1% 1.7pp

Korea 1,169,995 9.7% 1,433,251 10.3% 0.6pp 1,175,129 10.1% ▼0.2pp

US 473,108 3.9% 612,931 4.4% 0.5pp 588,306 5.1% 0.7pp

Unknown 149,377 1.2% 153,553 1.1% ▼0.1pp 105,794 0.9% ▼0.2pp

Langfang Hua'an 3,737,237 31.1% 4,752,547 34.2% 3.1pp 3,948,991 34.1% ▼0.1pp

Mahle 1,363,515 11.4% 1,317,212 9.5% ▼1.9pp 1,309,159 11.3% 1.8pp

Greenleaf (Hunan) 991,569 8.3% 1,066,638 7.7% ▼0.6pp 863,189 7.4% ▼0.2pp

Aisan 790,155 6.6% 879,555 6.3% ▼0.3pp 717,949 6.2% ▼0.1pp

KFTC 620,862 5.2% 792,802 5.7% 0.5pp 702,013 6.1% 0.4pp

Roki 661,210 5.5% 828,043 6.0% 0.4pp 688,661 5.9% ▼0.0pp

Delphi 455,148 3.8% 608,274 4.4% 0.6pp 588,187 5.1% 0.7pp

Futaba 439,073 3.7% 494,432 3.6% ▼0.1pp 394,791 3.4% ▼0.2pp

Other 2,943,890 24.5% 3,158,423 22.7% ▼1.8pp 2,373,874 20.5% ▼2.2pp

12,002,659 100.0% 13,897,926 100.0% 11,586,814 100.0%Total

2012 2013 YTD Sep. 2014

Mak

er O

rigin

Supplier

3.9% 4.4% US 5.1%

9.7% 10.3% Korea 10.1%

13.7% 11.4%EU 13.1%

17.0%16.5%

Japan 16.0%

54.4%56.2%

China 54.7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 YTD Sep. 2014

24.5%22.7%

Other 20.5%

3.7%

3.6%

Futaba 3.4%

3.8%4.4%

Delphi 5.1%

5.5%6.0%

Roki 5.9%

5.2% 5.7%KFTC 6.1%

6.6% 6.3%Aisan 6.2%

8.3%7.7% Greenleaf

(Hunan) 7.4%

11.4%

9.5%Mahle 11.3%

31.1%34.2%

Langfang

Hua'an 34.1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 YTD Sep. 2014

���������� ��� ���� ��������

����� ����� �!"#$%����

FOURIN Asia Automotive Intelligence

Stepped up emission regulations force

Chinese suppliers to drop out of

competition

FOURIN has compiled a list of

automobiles which comply with China 3,

China 4 and China 5 emission regulations

announced by China’s Ministry of

Environmental Protection to produce a

database on supplier-specific EECS use.

Based on a list of over 110,000 models,

with the introduction of China 5 emission

effective volume and butane working

capacity (BWC) of EECS charcoal

canisters as well as added BWC

inspection to production consistency

inspection. After the introduction of China

6 emission regulations, which is currently

under study, ORVR system, a device

which collects fuel vapors during fueling,

is planned to be added to the list of

inspection items, which is expected to

force even more suppliers out of business.

regulations, while foreign EECS suppliers

are maintaining their existing clientele,

smaller Chinese manufacturers are

dropping out of competition, increasing

supplier concentration. Since 2014, when

the certification of China 5-compliant

models began, the products of 16 Chinese

suppliers passed new emission regulations

out of over 40 companies, allowing them

to supply EECS to automakers. China 5

certification brought about the testing of

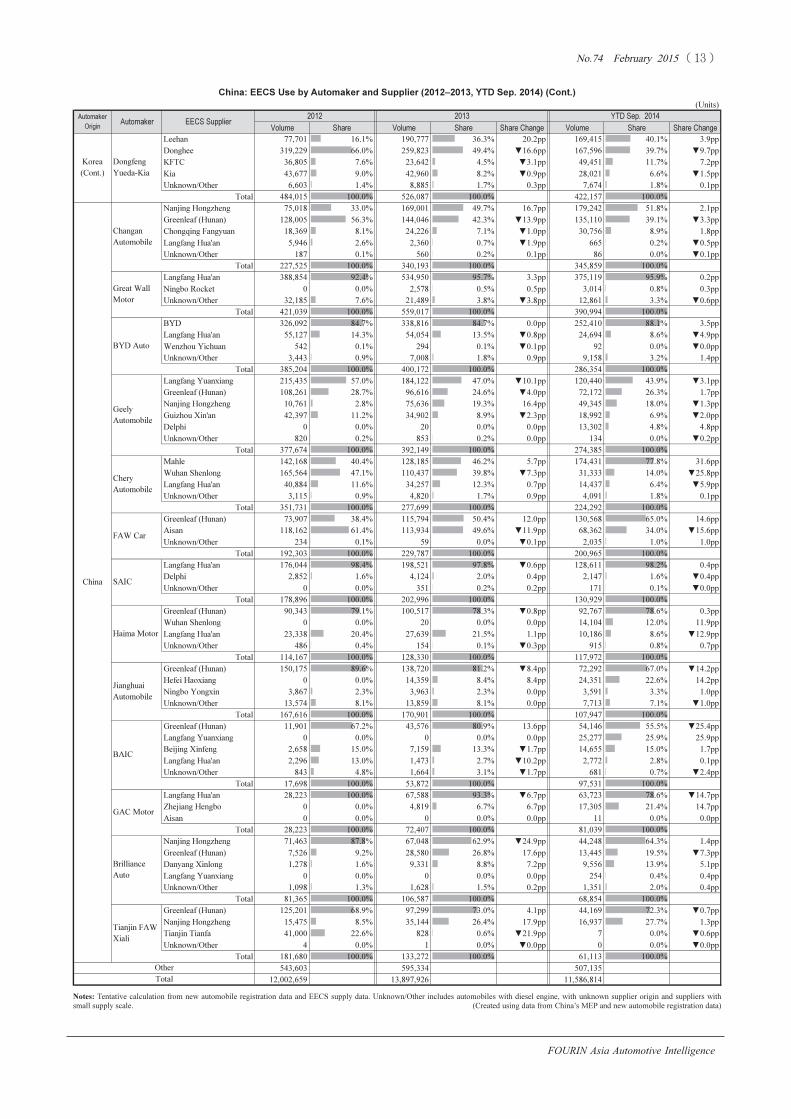

China: EECS Use by Automaker and Supplier (2012–2013, YTD Sep. 2014)

China: EECS Use by Supplier and Emission Standard Level

Notes: Created based on MEP7’s official announcements of emission regulation-compliant gasoline-powered light automobiles until Sep. 30, 2014. Each model designation is counted as one model.

Covers light automobiles with GVW of 3,500kg or less. If the EECS maker is an automaker, then it is supposed that the automaker assembles canisters and other procured parts in house.

(Created using data from China’s MEP)

Notes: Tentative calculation from new automobile registration data and EECS supply data. Unknown/Other includes automobiles with diesel engine, with unknown supplier origin and suppliers with

small supply scale. � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � (Created using data from China’s MEP and new automobile registration data)

Supplier Origin Supplier China 3 China 4 China 5 Supplier Origin Supplier China 3 China 4 China 5

Greenleaf (Hunan) High-Tech Materials 11,241 19,651 2,654 Mahle 663 1,674 774

Langfang Hua'an Automotive Equipment 4,475 8,275 1,670 Kayser 109 78 60

Nanjing Hongzheng Electromechanical Manufacturing 1,947 4,052 1,488 Dayco 298 256 52

Langfang Yuanxiang Automobile Fittings 1,272 4,949 643 Daimler 18 90 36

Xiamen Sentec E&E 807 1,531 285 VW 255 317 0

Wuhan Shenlong Automobile Plastic Products 2,620 3,777 270 BMW 5 0 0

BYD 90 436 249 Hutchinson 8 7 0

Ningbo Rocket Automobile Parts 0 1,220 190 Total 1,356 2,422 922

Chongqing Fangyuan Industry & Trade 7,463 10,136 140 Aisan 519 880 333

Liuzhou Shunzeer Auto Parts 0 2,282 98 Roki 253 378 241

Ningbo Yongxin Auto Components Manufacturing 543 514 76 Futaba 103 162 116

Guizhou Xin'an Aviation Machinery 85 906 56 Denso 76 73 36

Beijing Xinfeng Tianji Science & Technology 0 36 38 Toyo Roki 13 0 0

Zhejiang Hengbo Filter 0 479 34 Total 964 1,493 726

Shanghai Lianyi Automobile Tractor Industry & Trade 23 72 14 KFTC 285 325 277

Hefei Haoxiang Automobile Parts 0 386 12 Leehan 8 158 123

Nanjing Zhongshan Automobile Matching Parts Factory 834 1,804 0 Donghee 4 48 0

Tianjin Tianfa Automobile Fittings 157 24 0 Kia 86 16 0

Tianjin Shenzhou Auto Parts 46 312 0 Hyundai 33 0 0

Huanghua Xiangyu Auto Parts 83 232 0 Total 416 547 400

Shanghai Dazhong Lianxiang Automotive Components 47 22 0 Delphi 122 264 221

Chongqing Oubiao Science & Technology 0 168 0 Visteon 23 79 0

Other 1,388 1,722 0 Total 145 343 221

Total 33,121 62,986 7,917 36,002 67,791 10,186

(Number of models)

China

Total

EU

US

Korea

Japan

(Units)

Volume Share Volume Share Share Change Volume Share Share Change

Langfang Hua'an 1,202,714 95.2% 1,435,964 96.5% 1.3pp 1,251,316 97.9% 1.4pp

Dayco 21,987 1.7% 20,771 1.4% ▼0.3pp 14,236 1.1% ▼0.3pp

Unknown/Other 38,536 3.1% 30,553 2.1% ▼1.0pp 12,023 0.9% ▼1.1pp

Total 1,263,237 100.0% 1,487,288 100.0% 1,277,575 100.0%

Langfang Hua'an 1,020,017 80.3% 1,391,006 94.4% 14.1pp 1,252,597 97.2% 2.8pp

Mahle 176,934 13.9% 62,170 4.2% ▼9.7pp 34,642 2.7% ▼1.5pp

Kayser 20,932 1.6% 799 0.1% ▼1.6pp 125 0.0% ▼0.0pp

Visteon 17,960 1.4% 4,657 0.3% ▼1.1pp 119 0.0% ▼0.3pp

Unknown/Other 33,965 2.7% 14,967 1.0% ▼1.7pp 1,623 0.1% ▼0.9pp

Total 1,269,808 100.0% 1,473,599 100.0% 1,289,106 100.0%

Mahle 261,666 62.0% 332,230 63.4% 1.5pp 445,506 88.4% 24.9pp

Wuhan Shenlong 144,314 34.2% 171,230 32.7% ▼1.5pp 44,105 8.7% ▼24.0pp

Unknown/Other 16,285 3.9% 20,155 3.8% ▼0.0pp 14,498 2.9% ▼1.0pp

Total 422,265 100.0% 523,615 100.0% 504,109 100.0%

Kayser 98,318 72.2% 120,686 61.6% ▼10.5pp 99,009 50.9% ▼10.8pp

Delphi 37,903 27.8% 75,091 38.4% 10.5pp 95,511 49.1% 10.7pp

Unknown/Other 34 0.0% 23 0.0% ▼0.0pp 52 0.0% 0.0pp

Total 136,255 100.0% 195,800 100.0% 194,572 100.0%

Daimler 93,287 100.0% 110,862 100.0% 0.0pp 91,347 86.5% ▼13.5pp

Mahle 0 0.0% 0 0.0% 0.0pp 12,220 11.6% 11.6pp

Kayser 0 0.0% 0 0.0% 0.0pp 2,028 1.9% 1.9pp

Unknown/Other 2 0.0% 2 0.0% ▼0.0pp 9 0.0% 0.0pp

Total 93,289 100.0% 110,864 100.0% 105,604 100.0%

Mahle 7,055 99.9% 6,894 99.1% ▼0.8pp 4,872 97.5% ▼1.7pp

Unknown/Other 4 0.1% 61 0.9% 0.8pp 127 2.5% 1.7pp

Total 7,059 100.0% 6,955 100.0% 4,999 100.0%

GAC Fiat Zhejiang Hengbo 4,791 100.0% 39,453 100.0% 0.0pp 45,420 100.0% 0.0pp

Automaker

Origin

Automaker EECS Supplier

Fujian Benz

Shanghai

VW

FAW-VW

Dongfeng

Peugeot

Citroën

Brilliance

BMW

Beijing Benz

EU

2012 2013 YTD Sep. 2014

���������� ��� ���� ��������

����� ����� �!"#$%����

FOURIN Asia Automotive Intelligence

China’s Hua’an dominates the market

while Mahle strengthens sales promotion

In China’s EECS sector, since Chinese

suppliers supply not only Chinese

automakers, but also Western manufacturers,

Chinese share exceeds 50 percent. Of which,

the two largest Chinese suppliers Langfang

Hua’an and Greenleaf (Hunan) High-Tech

Materials supply EECS to over 90 percent

of new Shanghai VW and FAW-VW

models, over 40 percent of new Shanghai

GM models and over 60 percent of new

Ford models, controlling a dominant market

position. Out of China’s newly-registered

automobile volume of 13.9 million units,

4.75 million units are supplied by Langfang

Hua’an distantly followed by German

component maker Mahle with over 3

million units.

As for supply relations, taking advantage

of the introduction of China 5 emission

standards, Mahle charged ahead in the

Chinese market supplying not only Western

automakers, but also Japan’s Nissan and

China’s Jiangling, Great Wall and Chery. In

contrast, the three major Japanese suppliers

Aisan, Futaba and Roki supply only

Japanese automakers as before. As a result,

they cannot enjoy the benefits of a larger

clientele base and as Japanese automakers

are struggling with sluggish sales, Japanese

suppliers inevitably face declining market

share. (Jincheng ZHOU)

China: EECS Use by Automaker and Supplier (2012–2013, YTD Sep. 2014) (Cont.)�

Notes: Tentative calculation from new automobile registration data and EECS supply data. Unknown/Other includes automobiles with diesel engine, with unknown supplier origin and suppliers with

small supply scale.� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � (Created using data from China’s MEP and new automobile registration data)

(Units)

Volume Share Volume Share Share Change Volume Share Share Change

Langfang Hua'an 555,589 44.9% 575,675 40.2% ▼4.7pp 423,725 37.0% ▼3.3pp

Mahle 392,882 31.8% 443,081 31.0% ▼0.8pp 351,913 30.7% ▼0.3pp

Delphi 211,110 17.1% 284,358 19.9% 2.8pp 244,273 21.3% 1.4pp

KFTC 77,486 6.3% 127,421 8.9% 2.6pp 125,719 11.0% 2.1pp

Kayser 0 0.0% 0 0.0% 0.0pp 855 0.1% 0.1pp

Unknown/Other 4 0.0% 76 0.0% 0.0pp 16 0.0% ▼0.0pp

Total 1,237,071 100.0% 1,430,611 100.0% 1,146,501 100.0%

Greenleaf (Hunan) 88,823 84.2% 84,651 83.8% ▼0.4pp 46,380 55.7% ▼28.1pp

Liuzhou Shunzeer 0 0.0% 0 0.0% 0.0pp 22,999 27.6% 27.6pp

Shanghai Lianyi 16,611 15.8% 16,342 16.2% 0.4pp 13,929 16.7% 0.5pp

Unknown/Other 10 0.0% 5 0.0% ▼0.0pp 3 0.0% ▼0.0pp

Total 105,444 100.0% 100,998 100.0% 83,311 100.0%

Langfang Hua'an 189,900 47.1% 385,863 59.1% 12.0pp 378,626 64.8% 5.7pp

Xiamen Sentec 151,430 37.6% 165,507 25.4% ▼12.2pp 96,761 16.6% ▼8.8pp

Delphi 6,429 1.6% 52,232 8.0% 6.4pp 61,951 10.6% 2.6pp

Aisan 52,205 13.0% 48,948 7.5% ▼5.5pp 46,714 8.0% 0.5pp

Unknown/Other 3,007 0.7% 37 0.0% ▼0.7pp 5 0.0% ▼0.0pp

Total 402,971 100.0% 652,587 100.0% 584,057 100.0%

Aisan 348,246 70.7% 417,383 81.2% 10.5pp 354,337 86.7% 5.5pp

Denso 144,616 29.3% 96,671 18.8% ▼10.5pp 54,215 13.3% ▼5.5pp

Unknown/Other 3 0.0% 2 0.0% ▼0.0pp 2 0.0% 0.0pp

Total 492,865 100.0% 514,056 100.0% 408,554 100.0%

GAC Toyota Aisan 261,671 100.0% 293,963 100.0% 0.0pp 246,885 100.0% 0.0pp

Roki 379,033 50.3% 510,092 60.3% 9.9pp 400,668 59.2% ▼1.0pp

Mahle 373,859 49.7% 336,386 39.7% ▼9.9pp 272,270 40.2% 0.5pp

Greenleaf (Hunan) 0 0.0% 0 0.0% 0.0pp 3,465 0.5% 0.5pp

Unknown/Other 15 0.0% 134 0.0% 0.0pp 149 0.0% 0.0pp

Total 752,907 100.0% 846,612 100.0% 676,552 100.0%

Xiamen Sentec 27,064 52.1% 30,285 56.5% 4.4pp 21,285 55.8% ▼0.7pp

Roki 15,495 29.8% 16,010 29.9% 0.0pp 13,720 36.0% 6.1pp

Mahle 8,210 15.8% 6,732 12.6% ▼3.3pp 2,887 7.6% ▼5.0pp

Unknown/Other 1,142 2.2% 581 1.1% ▼1.1pp 232 0.6% ▼0.5pp

Total 51,911 100.0% 53,608 100.0% 38,124 100.0%

Dongfeng Honda Futaba 269,738 100.0% 304,015 100.0% 0.0pp 235,575 100.0% 0.0pp

Roki 165,223 49.4% 216,537 57.0% 7.6pp 199,056 62.4% 5.4pp

Futaba 169,262 50.6% 163,673 43.0% ▼7.6pp 120,182 37.6% ▼5.4pp

Unknown/Other 4 0.0% 8 0.0% 0.0pp 0 0.0% ▼0.0pp

Total 334,489 100.0% 380,218 100.0% 319,238 100.0%

Greenleaf (Hunan) 74,072 95.5% 77,436 98.8% 3.3pp 51,974 79.6% ▼19.2pp

Langfang Yuanxiang 3,133 4.0% 767 1.0% ▼3.1pp 13,097 20.0% 19.1pp

Roki 364 0.5% 188 0.2% ▼0.2pp 254 0.4% 0.1pp

Unknown/Other 24 0.0% 5 0.0% ▼0.0pp 3 0.0% ▼0.0pp

Total 77,593 100.0% 78,396 100.0% 65,328 100.0%

Greenleaf (Hunan) 75,832 42.9% 80,474 55.7% 12.8pp 67,022 53.3% ▼2.4pp

Roki 96,606 54.6% 61,496 42.5% ▼12.1pp 56,308 44.8% 2.2pp

Unknown/Other 4,525 2.6% 2,607 1.8% ▼0.8pp 2,436 1.9% 0.1pp

Total 176,963 100.0% 144,577 100.0% 125,766 100.0%

Greenleaf (Hunan) 0 0.0% 14,715 24.0% 24.0pp 54,750 76.7% 52.7pp

Xiamen Sentec 69,184 94.3% 44,516 72.7% ▼21.6pp 15,902 22.3% ▼50.4pp

Aisan 4,189 5.7% 1,998 3.3% ▼2.4pp 744 1.0% ▼2.2pp

Total 73,373 100.0% 61,229 100.0% 71,396 100.0%

Futaba 73 1.7% 26,739 100.0% 98.3pp 39,032 98.7% ▼1.3pp

Aisan 4,218 98.3% 0 0.0% ▼98.3pp 503 1.3% 1.3pp

Unknown/Other 2 0.0% 0 0.0% ▼0.0pp 1 0.0% 0.0pp

Total 4,293 100.0% 26,739 100.0% 39,536 100.0%

KFTC 506,571 62.4% 641,739 65.2% 2.8pp 526,843 65.3% 0.1pp

Delphi 196,837 24.2% 192,444 19.6% ▼4.7pp 171,000 21.2% 1.6pp

Leehan 108,515 13.4% 146,884 14.9% 1.6pp 108,084 13.4% ▼1.5pp

Unknown/Other 4 0.0% 2,873 0.3% 0.3pp 1,153 0.1% ▼0.1pp

Total 811,927 100.0% 983,940 100.0% 807,080 100.0%

Korea

US

Japan

Dongfeng

Nissan

Zhengzhou

Nissan

Guangqi

Honda

Changhe

Suzuki

Changan

Suzuki

Changan

Mazda

Shanghai GM

SAIC-GM-

Wuling

Changan Ford

FAW Toyota

Automaker

Origin

Automaker EECS Supplier

2012

GAC

Mitsubishi

Beijing

Hyundai

2013 YTD Sep. 2014

���������� ��� ���� ��������

����� ����� �!"#$%����

FOURIN Asia Automotive Intelligence

China: EECS Use by Automaker and Supplier (2012–2013, YTD Sep. 2014) (Cont.)�

Notes: Tentative calculation from new automobile registration data and EECS supply data. Unknown/Other includes automobiles with diesel engine, with unknown supplier origin and suppliers with

small supply scale. � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � (Created using data from China’s MEP and new automobile registration data)

(Units)

Volume Share Volume Share Share Change Volume Share Share Change

Leehan 77,701 16.1% 190,777 36.3% 20.2pp 169,415 40.1% 3.9pp

Donghee 319,229 66.0% 259,823 49.4% ▼16.6pp 167,596 39.7% ▼9.7pp

KFTC 36,805 7.6% 23,642 4.5% ▼3.1pp 49,451 11.7% 7.2pp

Kia 43,677 9.0% 42,960 8.2% ▼0.9pp 28,021 6.6% ▼1.5pp

Unknown/Other 6,603 1.4% 8,885 1.7% 0.3pp 7,674 1.8% 0.1pp

Total 484,015 100.0% 526,087 100.0% 422,157 100.0%

Nanjing Hongzheng 75,018 33.0% 169,001 49.7% 16.7pp 179,242 51.8% 2.1pp

Greenleaf (Hunan) 128,005 56.3% 144,046 42.3% ▼13.9pp 135,110 39.1% ▼3.3pp

Chongqing Fangyuan 18,369 8.1% 24,226 7.1% ▼1.0pp 30,756 8.9% 1.8pp

Langfang Hua'an 5,946 2.6% 2,360 0.7% ▼1.9pp 665 0.2% ▼0.5pp

Unknown/Other 187 0.1% 560 0.2% 0.1pp 86 0.0% ▼0.1pp

Total 227,525 100.0% 340,193 100.0% 345,859 100.0%

Langfang Hua'an 388,854 92.4% 534,950 95.7% 3.3pp 375,119 95.9% 0.2pp

Ningbo Rocket 0 0.0% 2,578 0.5% 0.5pp 3,014 0.8% 0.3pp

Unknown/Other 32,185 7.6% 21,489 3.8% ▼3.8pp 12,861 3.3% ▼0.6pp

Total 421,039 100.0% 559,017 100.0% 390,994 100.0%

BYD 326,092 84.7% 338,816 84.7% 0.0pp 252,410 88.1% 3.5pp

Langfang Hua'an 55,127 14.3% 54,054 13.5% ▼0.8pp 24,694 8.6% ▼4.9pp

Wenzhou Yichuan 542 0.1% 294 0.1% ▼0.1pp 92 0.0% ▼0.0pp

Unknown/Other 3,443 0.9% 7,008 1.8% 0.9pp 9,158 3.2% 1.4pp

Total 385,204 100.0% 400,172 100.0% 286,354 100.0%

Langfang Yuanxiang 215,435 57.0% 184,122 47.0% ▼10.1pp 120,440 43.9% ▼3.1pp

Greenleaf (Hunan) 108,261 28.7% 96,616 24.6% ▼4.0pp 72,172 26.3% 1.7pp

Nanjing Hongzheng 10,761 2.8% 75,636 19.3% 16.4pp 49,345 18.0% ▼1.3pp

Guizhou Xin'an 42,397 11.2% 34,902 8.9% ▼2.3pp 18,992 6.9% ▼2.0pp

Delphi 0 0.0% 20 0.0% 0.0pp 13,302 4.8% 4.8pp

Unknown/Other 820 0.2% 853 0.2% 0.0pp 134 0.0% ▼0.2pp

Total 377,674 100.0% 392,149 100.0% 274,385 100.0%

Mahle 142,168 40.4% 128,185 46.2% 5.7pp 174,431 77.8% 31.6pp

Wuhan Shenlong 165,564 47.1% 110,437 39.8% ▼7.3pp 31,333 14.0% ▼25.8pp

Langfang Hua'an 40,884 11.6% 34,257 12.3% 0.7pp 14,437 6.4% ▼5.9pp

Unknown/Other 3,115 0.9% 4,820 1.7% 0.9pp 4,091 1.8% 0.1pp

Total 351,731 100.0% 277,699 100.0% 224,292 100.0%

Greenleaf (Hunan) 73,907 38.4% 115,794 50.4% 12.0pp 130,568 65.0% 14.6pp

Aisan 118,162 61.4% 113,934 49.6% ▼11.9pp 68,362 34.0% ▼15.6pp

Unknown/Other 234 0.1% 59 0.0% ▼0.1pp 2,035 1.0% 1.0pp

Total 192,303 100.0% 229,787 100.0% 200,965 100.0%

Langfang Hua'an 176,044 98.4% 198,521 97.8% ▼0.6pp 128,611 98.2% 0.4pp

Delphi 2,852 1.6% 4,124 2.0% 0.4pp 2,147 1.6% ▼0.4pp

Unknown/Other 0 0.0% 351 0.2% 0.2pp 171 0.1% ▼0.0pp

Total 178,896 100.0% 202,996 100.0% 130,929 100.0%

Greenleaf (Hunan) 90,343 79.1% 100,517 78.3% ▼0.8pp 92,767 78.6% 0.3pp

Wuhan Shenlong 0 0.0% 20 0.0% 0.0pp 14,104 12.0% 11.9pp

Langfang Hua'an 23,338 20.4% 27,639 21.5% 1.1pp 10,186 8.6% ▼12.9pp

Unknown/Other 486 0.4% 154 0.1% ▼0.3pp 915 0.8% 0.7pp

Total 114,167 100.0% 128,330 100.0% 117,972 100.0%

Greenleaf (Hunan) 150,175 89.6% 138,720 81.2% ▼8.4pp 72,292 67.0% ▼14.2pp

Hefei Haoxiang 0 0.0% 14,359 8.4% 8.4pp 24,351 22.6% 14.2pp

Ningbo Yongxin 3,867 2.3% 3,963 2.3% 0.0pp 3,591 3.3% 1.0pp

Unknown/Other 13,574 8.1% 13,859 8.1% 0.0pp 7,713 7.1% ▼1.0pp

Total 167,616 100.0% 170,901 100.0% 107,947 100.0%

Greenleaf (Hunan) 11,901 67.2% 43,576 80.9% 13.6pp 54,146 55.5% ▼25.4pp

Langfang Yuanxiang 0 0.0% 0 0.0% 0.0pp 25,277 25.9% 25.9pp

Beijing Xinfeng 2,658 15.0% 7,159 13.3% ▼1.7pp 14,655 15.0% 1.7pp

Langfang Hua'an 2,296 13.0% 1,473 2.7% ▼10.2pp 2,772 2.8% 0.1pp

Unknown/Other 843 4.8% 1,664 3.1% ▼1.7pp 681 0.7% ▼2.4pp

Total 17,698 100.0% 53,872 100.0% 97,531 100.0%

Langfang Hua'an 28,223 100.0% 67,588 93.3% ▼6.7pp 63,723 78.6% ▼14.7pp

Zhejiang Hengbo 0 0.0% 4,819 6.7% 6.7pp 17,305 21.4% 14.7pp

Aisan 0 0.0% 0 0.0% 0.0pp 11 0.0% 0.0pp

Total 28,223 100.0% 72,407 100.0% 81,039 100.0%

Nanjing Hongzheng 71,463 87.8% 67,048 62.9% ▼24.9pp 44,248 64.3% 1.4pp

Greenleaf (Hunan) 7,526 9.2% 28,580 26.8% 17.6pp 13,445 19.5% ▼7.3pp

Danyang Xinlong 1,278 1.6% 9,331 8.8% 7.2pp 9,556 13.9% 5.1pp

Langfang Yuanxiang 0 0.0% 0 0.0% 0.0pp 254 0.4% 0.4pp

Unknown/Other 1,098 1.3% 1,628 1.5% 0.2pp 1,351 2.0% 0.4pp

Total 81,365 100.0% 106,587 100.0% 68,854 100.0%

Greenleaf (Hunan) 125,201 68.9% 97,299 73.0% 4.1pp 44,169 72.3% ▼0.7pp

Nanjing Hongzheng 15,475 8.5% 35,144 26.4% 17.9pp 16,937 27.7% 1.3pp

Tianjin Tianfa 41,000 22.6% 828 0.6% ▼21.9pp 7 0.0% ▼0.6pp

Unknown/Other 4 0.0% 1 0.0% ▼0.0pp 0 0.0% ▼0.0pp

Total 181,680 100.0% 133,272 100.0% 61,113 100.0%

543,603 595,334 507,135

12,002,659 13,897,926 11,586,814

Korea

(Cont.)

China

Total

Other

Haima Motor

Chery

Automobile

Jianghuai

Automobile

GAC Motor

Brilliance

Auto

BAIC

Great Wall

Motor

BYD Auto

Geely

Automobile

Dongfeng

Yueda-Kia

SAIC

FAW Car

Tianjin FAW

Xiali

Automaker

Origin

EECS Supplier

2012

Changan

Automobile

Automaker

2013 YTD Sep. 2014

���������� ��� ���� ��������

����� ����� �!"#$%����

FOURIN Asia Automotive Intelligence

China: China 5-compliant EECS Supply to Top 40 Automakers

Note: Each model designation is counted as one model. (Created using data from China’s MEP)

Shanghai V

W

FA

W-V

W

Dongfe

ng

Peugeot C

itroën

Brilliance B

MW

Beijin

g B

enz

Fujian B

enz

GA

C F

iat

Shanghai G

M

SA

IC

-G

M-W

uling

Changan F

ord

FA

W T

oyota

GA

C T

oyota

Dongfeng N

issan

Zhengzhou N

issan

Do

ng

fen

g H

on

da

Guangqi H

onda

Changhe S

uzuki

Changan S

uzuki

Changan M

azda

GA

C M

itsubis

hi

195 3 2 68 32

505 250 80 33

49

14 20

106

18

4

Total 505 250 49 18 80 305 33 3 14 2 68 52

Mahle (Shanghai) 42 149 73

Mahle (Import) 18 42 68

Mahle (China) 14 79

Mahle (Japan)

Total 42 149 18 14 0 79 115 68

Kayser (Import) 53 4

Kayser (Changchun) 5

Total 53 4 5

Dayco Dayco (Italy) 52

Daimler Daimler (Import) 36

Total 52 42 149 53 58 14 84 115 68

Aisan (Tianjin) 9 163 29 25

Aisan (Import) 34 18

Aisan (Foshan) 35

Total 9 197 82 25

Roki Roki (Suzhou) 108 12 40 68 15

Futaba (Dongguan) 69 32

Futaba (Import) 24

Futaba (Japan) 2

Total 69 32 26

Denso Denso (Tianjin) 36

Total 9 233 82 108 12 69 72 68 25 41

KFTC (Beijing) 107

KFTC (Import) 32

Total 139

(Leehan (Suzhou)

Leehan (Import)

Total

Total 139

Delphi (Shanghai) 81

Delphi (Import) 61 6

Delphi (Luxemburg)

Delphi (India) 6

Delphi (Mexico) 2

Total 61 83 12

557 292 198 114 58 14 18 386 305 54 233 82 226 94 69 72 2 136 77 41

Zhejiang Hengbo Filter

Hefei Haoxiang Automobile Parts

Shanghai Lianyi Automobile Tractor Industry & Trade

Chongqing Fangyuan Industry & Trade

Liuzhou Shunzeer Auto Parts

Guizhou Xin'an Aviation Machinery

Beijing Xinfeng Tianji Science & Technology

Ningbo Yongxin Auto Components Manufacturing

Nanjing Hongzheng Electromechanical Manufacturing

Wuhan Shenlong Automobile Plastic Products

Xiamen Sentec E&E

BYD

Ningbo Rocket Automobile Parts

China

EU

Mahle

Kayser

Total

Japan

Aisan

Futaba

Korea

KFTC

Leehan

US Delphi

Greenleaf (Hunan) High-Tech Materials

Langfang Hua'an Automotive Equipment

Langfang Yuanxiang Automobile Fittings

Supplier O

rig

in

Supplier

EU US Japan

���������� ��� ���� ��������

����� ����� �!"#$%����

FOURIN Asia Automotive Intelligence

China: China 5-compliant EECS Supply to Top 40 Automakers (Cont.)�

Note: Each model designation is counted as one model. (Created using data from China’s MEP)

Beijin

g H

yu

nd

ai

Do

ngfe

ng

Yue

da

-K

ia

SA

IC

FA

W C

ar

Ha

ima M

oto

r

Tia

njin F

AW

Xia

li

Don

gfe

ng

Pa

sse

ng

er

Cha

ng

an

Au

tom

ob

ile

Jia

ng

ling

Mo

tors

BA

IC

Beiq

i F

oto

n

Gre

at W

all M

oto

r

BY

D

Geely

Au

tom

ob

ile

Ch

ery

Au

tom

ob

ile

Jia

nghu

ai

Au

tom

ob

ile

Sou

th E

ast

(F

ujian

) M

oto

r

GA

C M

oto

r

Brillian

ce

Auto

Lifa

n A

uto

mob

ile

45 75 5 792 73 144 423 16 521 2,394

118 41 4 8 19 502 46 48 1,654

9 206 668 589 10 1,482

6 672 3 681

58 173 280

217 251

249 249

190 190

115 1 116

106

56 56

54 54

46 46

16 34

20 20

4

Total 118 45 116 18 58 1,113 8 146 196 692 249 1,819 219 36 217 64 1,111 13 7,617

Mahle (Shanghai) 40 42 76 422

Mahle (Import) 128

Mahle (China) 93

Mahle (Japan) 1 1

Total 1 40 42 76 644

Kayser (Import) 57

Kayser (Changchun) 5

Total 62

Dayco Dayco (Italy) 52

Daimler Daimler (Import) 36

Total 1 40 42 76 794

Aisan (Tianjin) 226

Aisan (Import) 14 66

Aisan (Foshan) 35

Total 14 327

Roki Roki (Suzhou) 243

Futaba (Dongguan) 101

Futaba (Import) 24

Futaba (Japan) 2

Total 127

Denso Denso (Tianjin) 36

Total 14 733

KFTC (Beijing) 73 16 196

KFTC (Import) 61 93

Total 134 16 289

(Leehan (Suzhou) 103 103

Leehan (Import) 24 24

Total 24 103 127

Total 158 119 416

Delphi (Shanghai) 28 26 135

Delphi (Import) 67

Delphi (Luxemburg) 16 16

Delphi (India) 6

Delphi (Mexico) 2

Total 28 26 16 226

186 119 144 60 116 18 58 1,113 48 146 196 734 249 1,835 295 36 217 64 1,111 13 9,786

US Delphi

Total

Korea

KFTC

Leehan

Japan

Aisan

Futaba

Shanghai Lianyi Automobile Tractor Industry & Trade

EU

Mahle

Kayser

Ningbo Yongxin Auto Components Manufacturing

Zhejiang Hengbo Filter

Hefei Haoxiang Automobile Parts

Liuzhou Shunzeer Auto Parts

Guizhou Xin'an Aviation Machinery

Beijing Xinfeng Tianji Science & Technology

BYD

Ningbo Rocket Automobile Parts

Chongqing Fangyuan Industry & Trade

Nanjing Hongzheng Electromechanical Manufacturing

Langfang Yuanxiang Automobile Fittings

Wuhan Shenlong Automobile Plastic Products

Xiamen Sentec E&E

China

Total

China

Greenleaf (Hunan) High-Tech Materials

Langfang Hua'an Automotive Equipment

Sup

plie

r O

rig

in

Supplier

Korea

���������� ��� ���� ��������

����� ����� �!"#$%����

FOURIN Asia Automotive Intelligence

China MPV Market:

Chinese Low-price Business-oriented

Models Dominate the Market

�150%

�120%

�90%

�60%

�30%

0%

30%

60%

90%

120%

150%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 YTD

Nov. 2013

YTD

Nov. 2014

(1,000 units)

MPV C-MPV B-MPV

China’s MPV market (including

B-MPVs and C-MPVs) increased 8.8

percent in the first 11 months of 2014 to 3

million units (factory shipment data).

Compared to 2013’s 4.9 percent growth

rate, 2014’s increase is high. Looking at

data by segment, while B-MPVs went up

only by a single digit, C-MPVs rose 33.5

percent, registering the highest growth by

surpassing even SUV growth of 32.7

percent. MPVs went up 19.1 percent,

becoming the third growth segment after

C-MPVs and SUVs. In the second half of

2014, while economic downturn slowed

down passenger vehicle sales, the MPV

automakers which use low cost as their

weapon of choice. Since foreign

automakers are unable to compete with

Chinese manufacturers due to low product

price, they focus on the launch of

high-end models; however, their market

share remains well below 10 percent.

Among foreign automakers, only US

manufacturers realized positive growth

thanks to brisk sales of GM’s high-end

business model the Buick GL8. However,

the family-oriented MPV market is

anticipated to expand, prompting Honda

and Toyota among others to step up local

product launches.

market, whose products are intended for

both business and family use greatly

expanded compared to other segments,

drawing attention as a segment that is

anticipated to see further demand in the

future.

Looking at data by brand origin,

Chinese share stood at 89.9 percent in the

first 11 months of 2014, nearly

monopolizing the MPV market. B-MPVs,

which are sold for an entry price of

around 50,000 CNY and intended for

business use, account for 77.3 percent of

the MPV market, highlighting the

overwhelming domination of Chinese

China: MPV Factory Shipment Volume by Segment (2003–2013, YTD Nov. 2013/2014)

China: MPV Factory Shipment Volume by Segment (2003–2013, YTD Nov. 2013/2014)

(Created using data from CAAM)

Since 2008, demand expanded in the suburbs primarily aiding the growth of

B-MPVs; however, starting from 2012, MPV growth rate became the highest, factory

shipment volume going up 27.3 percent in 2013. Meanwhile, in YTD Nov. 2014,

C-MPVs went up 33.5 percent driven by the launch of the Baojun 730 in Jul. 2014.�

Following the implementation of the “Vehicles to the Countryside”

policy in 2008, factory shipment volume of B-MPVs spiked in 2009.

China: Passenger Vehicle Factory Shipment Volume by Segment (2003–2013, YTD Nov. 2013/2014)

(Created using data from CAAM)

(Created using data from CAAM [China Association of Automobile Manufacturers])

B-MPV

C-MPV

MPV

Growth rate(right scale)

Factory shipment

volume

(left scale)

(Units)

Segment 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Year-on-

year

Share

YTD Nov.

2013

YTD Nov.

2014

Period-on-

period

Share

MPV 67,979 91,594 118,780 144,512 180,242 158,841 187,060 278,502 315,677 327,989 417,643 27.3% 13.6% 370,520 441,321 19.1% 14.7%

C-MPV 34,899 27,204 28,839 37,680 86,077 97,471 135,165 217,523 223,496 219,474 193,825 ▼11.7% 6.3% 181,341 242,097 33.5% 8.1%

B-MPV 732,235 779,518 873,177 965,764 1,040,401 1,130,216 2,070,250 2,642,455 2,369,013 2,374,856 2,453,732 3.3% 80.1% 2,208,627 2,321,208 5.1% 77.3%

Total 835,113 898,316 1,020,796 1,147,956 1,306,720 1,386,528 2,392,475 3,138,480 2,908,186 2,922,319 3,065,200 4.9% 100.0% 2,760,488 3,004,626 8.8% 100.0%

(Units)

Segment 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Year-on-

year

Share

YTD Nov.

2013

YTD Nov.

2014

Period-

on-period

Share

E2 57,578 54,945 83,331 122,854 162,147 169,291 184,586 117,561 271,698 320,468 361,912 12.9% 2.0% 333,243 383,056 14.9% 2.2%

E1 8,173 15,841 17,152 28,685 40,352 41,956 73,537 116,567 186,370 189,872 259,589 36.7% 1.4% 236,567 266,757 12.8% 1.5%

D 428,895 411,511 516,874 733,753 935,562 965,586 1,226,179 1,459,635 1,526,908 1,652,842 1,911,863 15.7% 10.7% 1,738,381 1,820,283 4.7% 10.3%

C 687,607 876,356 1,076,680 1,597,470 2,266,169 2,476,574 3,960,278 4,982,370 5,339,622 5,845,878 6,903,222 18.1% 38.5% 6,333,065 6,649,399 5.0% 37.7%

B 624,120 686,601 801,173 1,010,773 937,533 946,896 1,373,342 1,848,060 2,019,192 2,052,588 1,977,499 ▼3.7% 11.0% 1,666,405 1,640,457 ▼1.6% 9.3%

A 133,318 172,645 269,990 294,748 291,362 320,636 464,852 607,778 547,477 468,356 406,821 ▼13.1% 2.3% 368,671 272,747 ▼26.0% 1.5%

Sports 0 0 3,550 3,670 2,143 1,743 1,027 939 126 0 0 - 0.0% 0 0 - 0.0%

MPV 67,979 91,594 118,780 144,512 180,242 158,841 187,060 278,502 315,677 327,989 417,643 27.3% 2.3% 370,520 441,321 19.1% 2.5%

C-MPV 34,899 27,204 28,839 37,680 86,077 97,471 135,165 217,523 223,496 219,474 193,825 ▼11.7% 1.1% 181,341 242,097 33.5% 1.4%

B-MPV 732,235 779,518 873,177 965,764 1,040,401 1,130,216 2,070,250 2,642,455 2,369,013 2,374,856 2,453,732 3.3% 13.7% 2,208,627 2,321,208 5.1% 13.2%

SUV 74,703 128,190 191,252 235,510 355,545 446,399 655,039 1,165,885 1,459,435 2,042,917 3,042,752 48.9% 17.0% 2,713,962 3,602,349 32.7% 20.4%

Total 2,849,507 3,244,405 3,980,798 5,175,419 6,297,533 6,755,609 10,331,315 13,437,275 14,259,014 15,495,240 17,928,858 15.7% 100.0% 16,150,782 17,639,674 9.2% 100.0%

���������� ��� ���� ��������

����� ����� �!"#$%����

FOURIN Asia Automotive Intelligence

Wuling Hongguang

Wuling Rongguang

Wuling Sunshine

Fengxing

Honor

Changan Star II

Baojun 730

Sokon K Series

Buick GL8

Sokon Fengguang

Weiwang M20

Refine

Weiwang 306

Wagon R+

Livina

Lifan Fengshun

Jinbei minibuses

New Changan Star

Ouliwei

Golf Touran

Changan Star I

Taurus

Odyssey

Succe

Sokon C Series

Starlight 4500

Weiwang 205

Furuida

Xenia M80

NV200

0

5

10

15

20

25

30

35

2,300 2,500 2,700 2,900 3,100 3,300 3,500

(Wheelbase: mm)

(Price: 1,000 CNY)

The MPV market began to see rapid

growth in 2008 when China’s “Vehicles

to the Countryside” policy was

implemented which supported vehicle

dissemination in rural areas with

incentives. As a result, especially

business-type B-MPVs realized drastic

sales increase. These models have an

entry price of 50,000 CNY or less and are

used for cargo transport or as company

vehicles. In the B-MPV segment,

SAIC-GM-Wuling’s Wuling brand enjoys

the highest share. In the first 11 months of

2014, the top three models were those of

the Wuling brand. The best-selling model

Wuling Hongguang succeeded in

capturing strong demand thanks to its low

price and family-oriented design concept.

While in the past B-MPV models were

intended primarily for business use and

had a typical box-like design, the

Hongguang’s design resembles to that of a

passenger vehicle with an aim to capture

demand of family vehicle buyers.

SAIC-GM-Wuling released its seven-seat

/ three-row C-MPV the Baojun 730 in

recent years. BAIC opened a flagship

store on a Chinese online retail website

Tmall.com, selling limited-edition models

and offering special discounts among

other activities in an aim to explore new

sales opportunities.

In contrast to active product launches

by Chinese automakers, foreign entry

into the MPV market is lagging behind.

Since low-price models dominate the

market, there is little demand for

relatively expensive family-oriented

MPVs. The best-selling model among

foreign products is GM’s Buick GL8

whose entry price is set at a high level of

289,900 CNY and is sold as a high-end

business-use model. The GL8 succeeded

in capturing demand from corporate users

who have a taste for high-end products.

The model was ninth based on data of the

first 11 months of 2014, having a

50,000-unit lead on the Honda Odyssey

which is also sold for over 200,000 CNY.

As for Japanese models, although

Changan Suzuki’s Beidouxing and

Dongfeng Nissan’s Livina ranked 14th

July 2014, expanding its product lineup

from FR-layout models to FF-layout

products. With an entry price of 69,800

CNY, the Baojun 730 is somewhat more

expensive than most B-MPV models.

However, it has superior cost performance

considering that it has fuel consumption

of 7.1L/100km which is on par with that

of the segment-leader Hongguang and is

equipped with electronic stability control

(ESC). In the first four months after its

launch, the Baojun sold 89,000 units, over

30,000 units more than Nissan’s global

strategic model Livina in the same

C-MPV segment. Since Changan

Automobile, which has a rich lineup of

B-MPV products, made a late start in

launching family-use models, the

automaker dropped behind compared to

SAIC-GM-Wuling. Changan Automobile’s

Honor model, which was designed based

on the same business/family dual-use

concept as the Hongguang, sold some

500,000 units less than the Hongguang.

Meanwhile, BAIC is boosting its share by

emphasizing online sales promotion in

China: Product Structure and Price Range Distribution of the MPV Market (YTD Nov. 2014, Top 30 Models)

Main foreign models are located far away

from the product concentration area due to

their high price. Although they have few

rivals, their sales volume is also low.�

Product concentration area within the MPV

market. Especially, products in the

2,500–2,700mm / 50,000 CNY area sell

well. Includes some high-end models, but

they are foreign brands.�

Notes: Includes B-MPV and C-MPV models. Size of the bubbles is in proportion to sales volume. Grey bubbles indicate Chinese models. Dotted bubbles indicate foreign models. Fengxing is

represented by Lingzhi V3. Sokon K Series is represented by new K7. Sokon Fengguang is represented by Fengguang 360. Entry price of some models are from autohome.com.cn.

(Created using data from company PR materials and CAAM)

���������� ��� ���� ��������

����� ����� �!"#$%����

FOURIN Asia Automotive Intelligence

and 15th, they are low-price models sold

for less than 100,000 CNY. Guangqi

Honda’s Odyssey with an entry price of

229,800 CNY was 23rd while GAC

Toyota’s E’Z with an entry price of

152,800 CNY stood at 32nd place,

indicating that models sold for over

100,000 CNY are fighting an uphill battle.

Although low-price business-oriented

models maintain an overwhelming share in

the MPV market, some Chinese

manufacturers are strengthening

development of medium/high-end models

sold for 100,000 CNY or more. Brilliance

Auto announced the Huasong high-end

MPV model in July 2014. The Huasong’s

product power is enhanced by BMW’s

2.0L turbocharged engine. After UK van

maker LDV’s purchase by SAIC Group in

2009, SAIC Commercial Vehicle began

manufacturing products based on

technology from UK van maker LDV,

reviving the Maxus high-end commercial

vehicle brand and starting full-scale

production of Maxus brand products from

2012. The launch of the Maxus brand is

intended to compete with foreign

automakers in the high-end MPV market.

Meanwhile, family-oriented MPVs, which

resemble in design to passenger cars, began

to alter the market by capturing share from

business-use MPVs. This change is seen as

a business opportunity for Japanese

automakers which have rich experience in

family-use MPV development. Upcoming

challenges for Japanese automakers are the

launch of new models tailored to local

needs and the establishment of brand