october 2016 spotlight on africa: a diverse frontier … hotels research... · understand the...

TRANSCRIPT

Spotlight on Africa: A Diverse Frontier An Overview of Hotel Real Estate in Sub-Saharan Africa

October 2016

2 Spotlight on Africa: A Diverse Frontier2 Spotlight on Africa: A Diverse Frontier

ContentsIntroduction 3

Macro-economic context 4

Global and regional capital flows 8

Hotel market overview 10

Emerging hotel markets 12

Regional investor focus 14

Investment hotspots 16

Barriers to investment 18

Transparency watch 20

Evolving debt markets 22

Looking forward 26

Kigali, Rwanda

JLL 3

The long-term outlook for hotel investment in Sub-Saharan Africa remains positive despite the recent slowdown in many of the region’s economies. The investment case is set by fundamentals such as comparatively high economic growth, increasing economic and political stability, favourable demographic trends, diversification of export revenues and infrastructure investment. This in turn underpins growth in demand for hotels. There is, however, no doubt that the slowdown in numerous economies dependent on resource revenue has reduced hotel trading performance and, consequently, investors and lenders are more cautious about investing in the region.

The emergence of new markets and the saturation of others are leading to an increased divergence in investment opportunities in hotel markets across the region. In this changing environment, which is largely driven by local and regional capital, it is critical to have a deep understanding of what investors and lenders seek to achieve in Sub-Saharan Africa. Recent global market uncertainty and currency fluctuation have placed local and regional capital in a better position to capitalise on hotel investment opportunities. The gradual upturn in the global commodity cycle in 2016 will undoubtedly translate into improved investment conditions in these resource intensive markets.

Given the corporate centric nature of hotel demand in Sub-Saharan Africa, there is a clear link between economic growth, capital investment and foreign corporate entry to demand for hotel beds. The medium-term outlook for acceleration in growth is positive and we forecast demand growth of 3% to 5% during the coming three years.

From an investment perspective, we forecast USD1.7 billion to be invested in hotels in Sub-Saharan Africa in 2017 and a further acceleration to USD1.9 billion in 2018. The supply pipeline will continue to grow as a result, with increasing efficiencies in realising new developments.

This 2016 Sub-Saharan Africa hotel investment overview aims to reflect the current investor and lender sentiment for the region. The aim of the research is to map out these fundamentals and to highlight trends facing the hotel real estate sector in Sub-Saharan Africa. The diverse set of fundamentals in each market is becoming integral to the way in which investors and lenders approach the sector, with a region-wide approach becoming increasingly challenging. The hope is that this research will assist in bringing further transparency to the hotel sector and promote the view that investors should embrace the diversity that these markets bring, but most importantly to understand the variety and nuances of these markets.

Introduction

4 Spotlight on Africa: A Diverse Frontier

The reduction in global commodity prices has led to a slowdown in the regional economic growth rate from 2014. Certain economies overexposed to commodity income for foreign exchange earnings and government income have been particularly hard hit.

For 2016, the GDP growth forecast for the region has slowed to 3.0% from an average between 2010 to 2015 of 6.0%. This is expected to accelerate to 4.1% in 2017 and 2018 driven by the large regional markets. The challenging economic climate in West Africa led by the challenges in Nigeria and Angola have shifted the economic growth center towards East Africa. The top three markets for economic growth between 2016 and 2018 are expected to be Côte d’Ivoire,Tanzania and Senegal which shows the geographic diversity of growth withinthe region.

Demand in the hotel sector is driven by economic activity in each market as hotels are largely dependent on corporate guests. Aside from base economic growth, other key factors in increasing hotel demand are economic participation, regional integration, foreign direct investment, infrastructure investment and corporate entry. The medium-term outlook for all of these factors is positive, yet their impact on each hotel market varies significantly.

Currency volatility and access to foreign currency has been a major challenge in the region in the recent past and it is clear from discussions with lenders and investors that this is seen as a key risk area for them. The fact that most hotel markets in Sub-Saharan Africa continue to trade in US Dollars provides a significant currency hedge and a competitive advantage for the hotel sector over other real estate asset classes.

Macro-economic context

JLL 5

Note: Nominal GDP forecasts for Liberia are estimated because of data shortages. Sierra Leone has been excluded from the chart given its highly unusual economic dynamics following an economic collapse causedby the Ebola pandemic© 2016 Frontier Strategy Group | www.frontierstrategygroup.com | Sub-Saharan Africa Regional Outlook for 2017 | August 2016

Angola

BeninBotswana

Burkina Faso

Burundi

Cameroon

Cape Verde

Central African Republic

Chad

Comoros

Congo

Congo (DRC)

Cote d'Ivoire

Equatorial Guinea

Eritrea

Ethiopia

GabonGambia

Ghana

GuineaGuinea-Bissau

Kenya

Lesotho

Liberia

Madagascar Malawi

Mali

Mauritania

Mozambique Namibia

Niger

Nigeria

Rwanda

Sao Tome and Principe

Senegal

Seychelles

Sierra Leone

South AfricaSwaziland

Tanzania

Togo

Uganda

Zambia

Zimbabwe

-3%

-1%

1%

3%

5%

7%

9%

30 35 40 45 50 55 60 65 70 75 80

Thre

e-6102 ht

worg PDG egareva raey–2

018

Resilience to external shocks

High growth, low resilience

Low growth, low resilience Low growth, high resilience

High growth, high resilience

Bubble size = 2018 nominal GDP, US $ billions

Sub-Saharan Africa Resilience Index

6 Spotlight on Africa: A Diverse Frontier

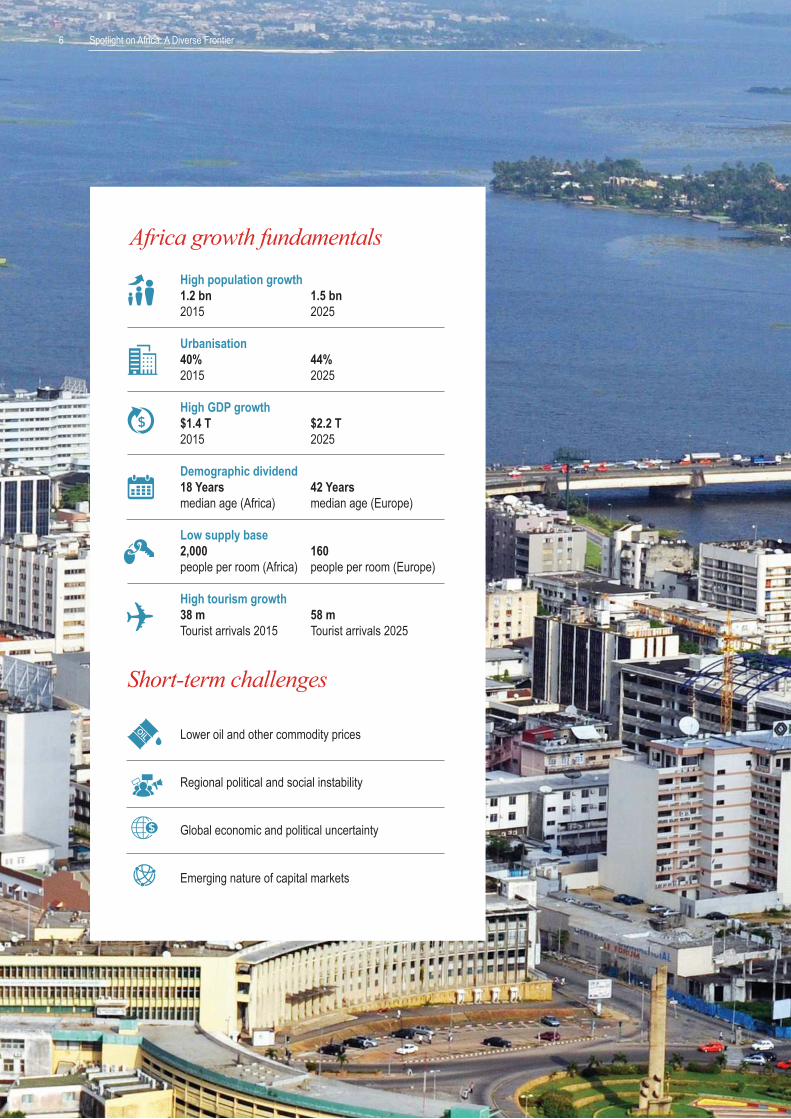

High population growth1.2 bn 1.5 bn2015 2025

Urbanisation40% 44% 2015 2025

High GDP growth$1.4 T $2.2 T2015 2025

Demographic dividend18 Years 42 Yearsmedian age (Africa) median age (Europe)

Low supply base2,000 160people per room (Africa) people per room (Europe)

High tourism growth38 m 58 mTourist arrivals 2015 Tourist arrivals 2025

Africa growth fundamentals

Lower oil and other commodity prices

Regional political and social instability

Global economic and political uncertainty

Emerging nature of capital markets

Short-term challenges

6 Spotlight on Africa: A Diverse Frontier

JLL 7JLL 7

Abidjan, Ivory Coast

8 Spotlight on Africa: A Diverse Frontier

In 2016 we are seeing global transaction volumes decline from their high of USD85 billion in 2015, with investors demonstrating a more measured approach to the sector. Cross-border capital is expected to remain steady year-on-year, after some USD30 billion in capital was deployed into hotels across national borders during 2015. So while overall transaction volumes are anticipated to taper, cross-border investment will be more resilient.

Private equity funds still have large amounts of cash and have a need to deploy, a trend motivating the continued momentum in the sector. For funds raised prior to the current cycle, there will be an increase in pressure for the capital to be spent during the funds’ investment horizon. Private equity groups in the US and Western Europe are expected to lead this trend, with assets in secondary markets in the US, UK, Germany, Spain, and Japan the primary targets.

There is a large pool of global capital looking for new hotel frontiers and at the moment Sub-Saharan Africa has a very limited share of this global capital. This is largely driven by the perceived higher risk of investing in the region and subsequent higher return requirements, as well as the lack of liquidity and access to investment grade hotel assets. Even in South Africa, Kenya and Mauritius, which are some of the most mature markets in the region, assets remain tightly held. As liquidity improves during the coming years we should see an increasing appetite from global capital for the region.

In the medium-term, hotel investment in Sub-Saharan Africa will continue to be driven by local and regional private capital. With the exception of a few regional owner operators, the majority of investment is driven by first-time hotel investors with diverse portfolios of other business interest. Over time, we expect that this will result in increased liquidity, consolidation and further sector specialisation with certain markets already seeing this maturation in hotel investment

Global and regional capital flows

We also saw the highest ever volume of single asset transactions at USD47 billion in 2015 and the highest ever levels of cross border investment (USD30 billion).

Cross-border activity will remain relatively strong in 2016 and the big targets will be assets in Japan and across Western Europe.

We expect to see more mergers and acquisitions in 2016.

Consolidation is set to continue, with single assets and secondary markets to be the big stories.

Global hotel transactions rose nearly 50% to USD85 billion in 2015 - the second-highest year ever.

JLL 9JLL 9JLL 9

Johannesburg, South Africa

10 Spotlight on Africa: A Diverse Frontier

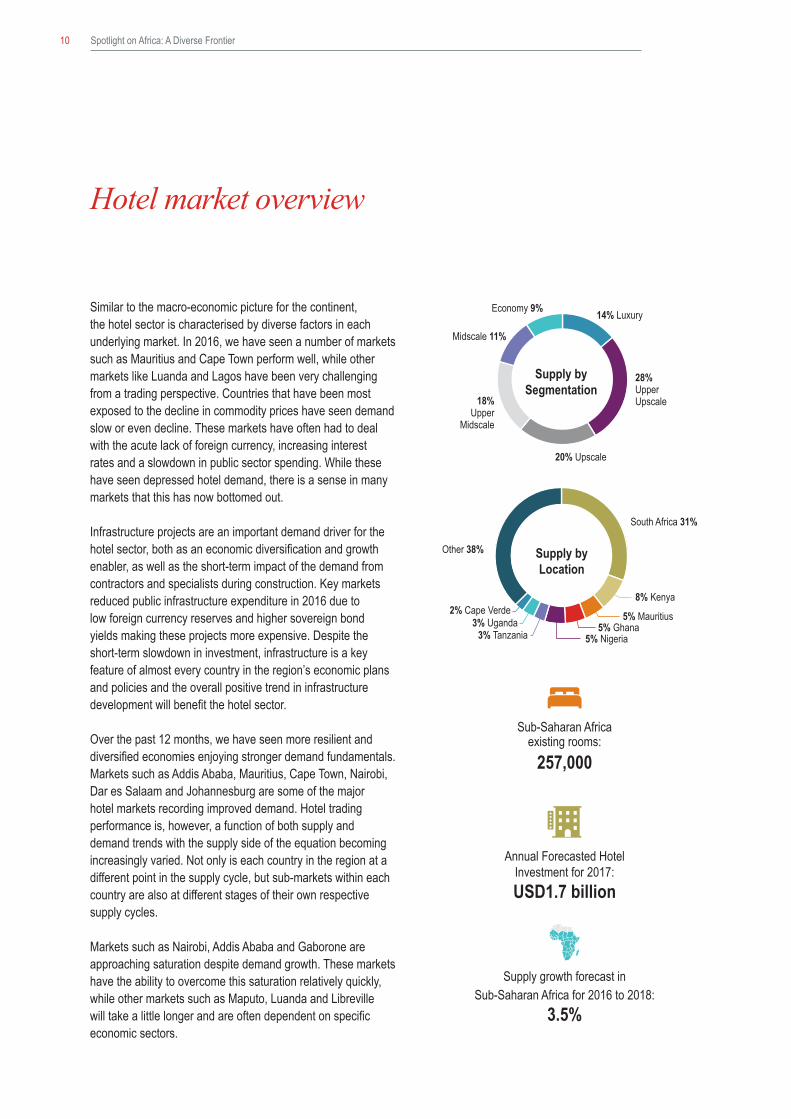

Similar to the macro-economic picture for the continent, the hotel sector is characterised by diverse factors in each underlying market. In 2016, we have seen a number of markets such as Mauritius and Cape Town perform well, while other markets like Luanda and Lagos have been very challenging from a trading perspective. Countries that have been most exposed to the decline in commodity prices have seen demand slow or even decline. These markets have often had to deal with the acute lack of foreign currency, increasing interest rates and a slowdown in public sector spending. While these have seen depressed hotel demand, there is a sense in many markets that this has now bottomed out. Infrastructure projects are an important demand driver for the hotel sector, both as an economic diversification and growth enabler, as well as the short-term impact of the demand from contractors and specialists during construction. Key markets reduced public infrastructure expenditure in 2016 due to low foreign currency reserves and higher sovereign bond yields making these projects more expensive. Despite the short-term slowdown in investment, infrastructure is a key feature of almost every country in the region’s economic plans and policies and the overall positive trend in infrastructure development will benefit the hotel sector.

Over the past 12 months, we have seen more resilient and diversified economies enjoying stronger demand fundamentals. Markets such as Addis Ababa, Mauritius, Cape Town, Nairobi, Dar es Salaam and Johannesburg are some of the major hotel markets recording improved demand. Hotel trading performance is, however, a function of both supply and demand trends with the supply side of the equation becoming increasingly varied. Not only is each country in the region at a different point in the supply cycle, but sub-markets within each country are also at different stages of their own respective supply cycles.

Markets such as Nairobi, Addis Ababa and Gaborone are approaching saturation despite demand growth. These markets have the ability to overcome this saturation relatively quickly, while other markets such as Maputo, Luanda and Libreville will take a little longer and are often dependent on specific economic sectors.

Hotel market overview

Annual Forecasted Hotel Investment for 2017:USD1.7 billion

Sub-Saharan Africa existing rooms:

257,000

Supply growth forecast in Sub-Saharan Africa for 2016 to 2018:

3.5%

Supply by Segmentation

14% Luxury

28% Upper Upscale

20% Upscale

18% Upper

Midscale

Midscale 11%

Economy 9%

Supply by Location

South Africa 31%

8% Kenya

Other 38%

3% Tanzania

5% Mauritius 3% Uganda 2% Cape Verde

5% Nigeria 5% Ghana

JLL 11

> 30,000 keys

10,000 - 30,000 keys

5,000 - 10,000 keys

0 - 5,000 keys

In 2015, we reported that there were 250,000 hotel rooms in Sub-Saharan Africa. This is estimated to grow to 257,000 in 2016, with room supply expected to increase by 2.8% over the period. A number of investors and operators are however looking to the midscale segment for opportunities, particularly to attract domestic demand.

We estimate that USD1.4 billion was invested in hotel real estate in Sub-Saharan Africa in 2015. In 2016, we forecast that the recovery in the region’s economy will see this increase to USD1.7 billion in 2017 and USD1.9 billion in 2018. Further to this, we expect an improvement in liquidity in the region which should exceed USD500 million in 2016 depending on some high value transactions in South Africa.

> 30,000 keys

10,000 - 30,000 keys

5,000 - 10,000 keys

0 - 5,000 keys

12 Spotlight on Africa: A Diverse Frontier

The past decade has seen the emergence of a number of new hotel markets in Sub-Saharan Africa. This supply growth was largely necessitated by the growth demand from the business segment, followed by government, diplomats, NGOs and leisure. High supply growth markets in 2016 included Nairobi, Addis Ababa and Kigali.

South Africa remains the largest hotel market in Sub-Saharan Africa and accounts for 30% of the room supply in the region. The market is particularly mature in a regional context and key nodes such as Johannesburg, Cape Town and Durban are again entering their Hotel development supply cycles subsequent to the saturation of 2009 and 2010. The following maps give some perspective to the relative supply growth per country since 2008. Off a low base, West and Central Africa have experienced the largest room supply growth of 8% and 9% per annum respectively since 2008, while East and Southern Africa have grown at 5% and 4% respectively.

Emerging hotel markets

Africa Room Supply 2008 Africa Room Supply 2016

Note: Bubble size represents size of country room supply. Source: JLL & STR Global, 2016

JLL 13JLL 13JLL 13

Antananarivo, Madagascar

14 Spotlight on Africa: A Diverse Frontier

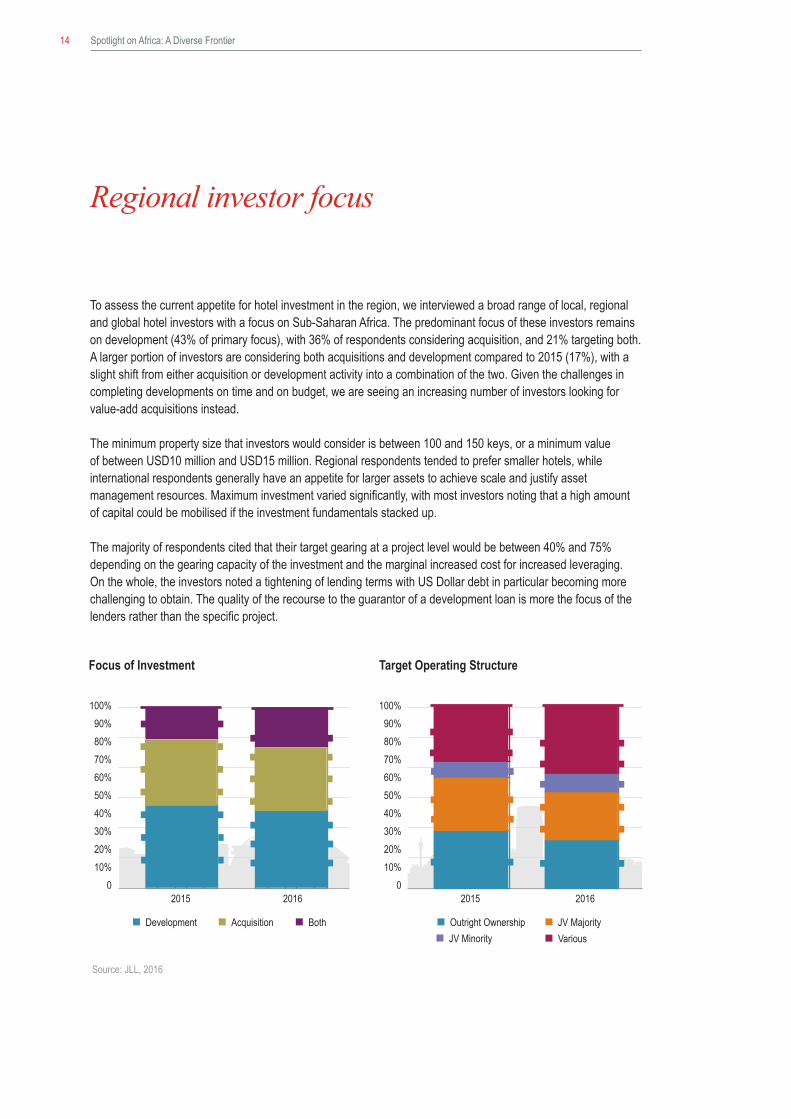

To assess the current appetite for hotel investment in the region, we interviewed a broad range of local, regional and global hotel investors with a focus on Sub-Saharan Africa. The predominant focus of these investors remains on development (43% of primary focus), with 36% of respondents considering acquisition, and 21% targeting both. A larger portion of investors are considering both acquisitions and development compared to 2015 (17%), with a slight shift from either acquisition or development activity into a combination of the two. Given the challenges in completing developments on time and on budget, we are seeing an increasing number of investors looking for value-add acquisitions instead.

The minimum property size that investors would consider is between 100 and 150 keys, or a minimum value of between USD10 million and USD15 million. Regional respondents tended to prefer smaller hotels, while international respondents generally have an appetite for larger assets to achieve scale and justify asset management resources. Maximum investment varied significantly, with most investors noting that a high amount of capital could be mobilised if the investment fundamentals stacked up.

The majority of respondents cited that their target gearing at a project level would be between 40% and 75% depending on the gearing capacity of the investment and the marginal increased cost for increased leveraging. On the whole, the investors noted a tightening of lending terms with US Dollar debt in particular becoming more challenging to obtain. The quality of the recourse to the guarantor of a development loan is more the focus of the lenders rather than the specific project.

Regional investor focus

Focus of Investment

100%90%80%70%60%50%40%30%20%10%

02015

Development Acquisition

2016

17% 21%

37% 36%

46% 43%

Both

Target Operating Structure

100%90%80%70%60%50%40%30%20%10%

02015

Outright Ownership JV Majority

2016

JV Minority Various

9%29%

31%

30%

11%26%

26%

37%

Source: JLL, 2016

JLL 15

0 10

Long-termShort-term

Real Estate Investment Trust

High-Net-Worth

Developer

Owner Operator

Investment Fund

17% Franchise

Target Tenure Types

17% Fixed Lease 17%

Owner Operate

28% Management

Agreement

22% Variable Lease

Investment Interest in the Short and Long-term

Investors are taking an increasingly flexible approach to the target grading level of assets to invest in, with an increasing portion of investors looking at the midscale and serviced apartment sectors over the upscale and upper upscale sectors. The interest from investors in certain market segments or grading levels appears to be increasingly market driven rather than mandate or brand preference driven.

Hotel management agreements remained the strongest preference for most investors (28%), a trend borne out of the strong preference for these from operators in the region.

JLL 15

Source: JLL, 2016

16 Spotlight on Africa: A Diverse Frontier

As the transparency of real estate in Sub-Saharan Africa improves, investors are better equipped to understand (and price) risks, and are able to adjust their investment hurdles accordingly. Investors that we interviewed targeted leveraged IRRs of between 14% and 18% in mature markets like South Africa and Mauritius, while emerging markets such as Kenya, Tanzania and Ghana require a return of between 16% and 22%. Higher risk markets are still actively being pursued by investors, yet return expectations consistently exceed 20%. It should be noted that beyond these professional investors there are projects that will be funded for other reasons, often strategic or emotional, where investors will be comfortable with lower returns. Further to this, local investors are often better able to assess the local risk (or have less cross-border risk) and therefore accept lower returns.

The JLL Property ClockTM presents our view on the relative position of a number of regional markets within their supply cycle. As liquidity increases in Sub-Saharan Africa during the next five years, there will be increasing transactional evidence to support the development of the investment cycle in different markets. We currently see the highest investor interest in Cape Town, Abidjan, Dar es Salaam and Seychelles.

Investment hotspots

Source: JLL, 2016

Investor Interest Growing

Stron

g Inve

stor Interest Investor Interest Falling

Low Investor In

teres

t

Kigali

Durban Mauritius

Seychelles

Johannesburg

Addis Ababa

Nairobi

Cape Town

Abidjan

Lagos

Luanda

Dar es Salaam

Kampala

Antananarivo

Maputo

Accra

Kinshasa Gaborone

Property clock

JLL 17JLL 17

18 Spotlight on Africa: A Diverse Frontier

Barriers to investment

The higher yielding opportunities that are presented in the region carry inherently challenges for investors to navigate, due to the emerging nature of the sector. The extent to which these challenges exist vary from market-to-market, yet an overarching trend emerges when we look at the broader region.

The primary challenge that investors are facing is finding projects that meet their minimum return threshold and this remains in pole position as it was in 2015. It appears that there is a high amount of capital available, yet investors search for projects with the right level of returns. This is not to say that projects in the market are incorrectly configured or priced, but investors may be finding that there is a lack of suitable leveraging in the market to achieve their required equity returns, or they may be pricing in excessive risk.

Lack of political stability again ranked second in 2016, with this clearly being an important risk factor in long-term investments such as real estate. There appears to be a continued positive shift towards inclusive and democratic rule, yet investors need to take into account that changes in political power can impact on economic policy and economic alignment.

7Lack of investment grade properties

Projects not meeting my returns

1

6Lack of suitable local equity partners

9Opportunity cost of my land against other uses

2Lack of political stability

3High development costs

4Lack of foreign currency

8Lack of access to quality development professionals

5Lack of clear exit opportunities at the end of my asset-holding period

JLL 19

Lack of foreign currency was ranked the same as 2015, remaining at fourth place, as investors are struggling to deal with currency pricing uncertainty and access to hard currency. Certainty of delivery was anecdotally cited as improving, due to the development and construction sector becoming more experienced in delivering projects.

High development costs remain a key challenge for investors in the region, ranking third on the list of concerns. High development costs for new builds when compared to mature markets are driven by a longer development period, less experienced building professionals and contractors, increasing land prices, high development finance costs, and higher import duties and taxes in certain countries. This barrier in turn has a significant impact on the ability for investors to secure projects with suitable investment returns.

The reduction of these barriers of entry in markets in the region will see an increase in the flow of capital into new projects and existing assets. When looking at the current primary hotel investment markets in the region (such as South Africa and Kenya), they will rank significantly lower in terms of each of these barriers than most frontier markets and be in a better position to attract capital.

Goree Island, Senegal

20 Spotlight on Africa: A Diverse Frontier

Transparency watch

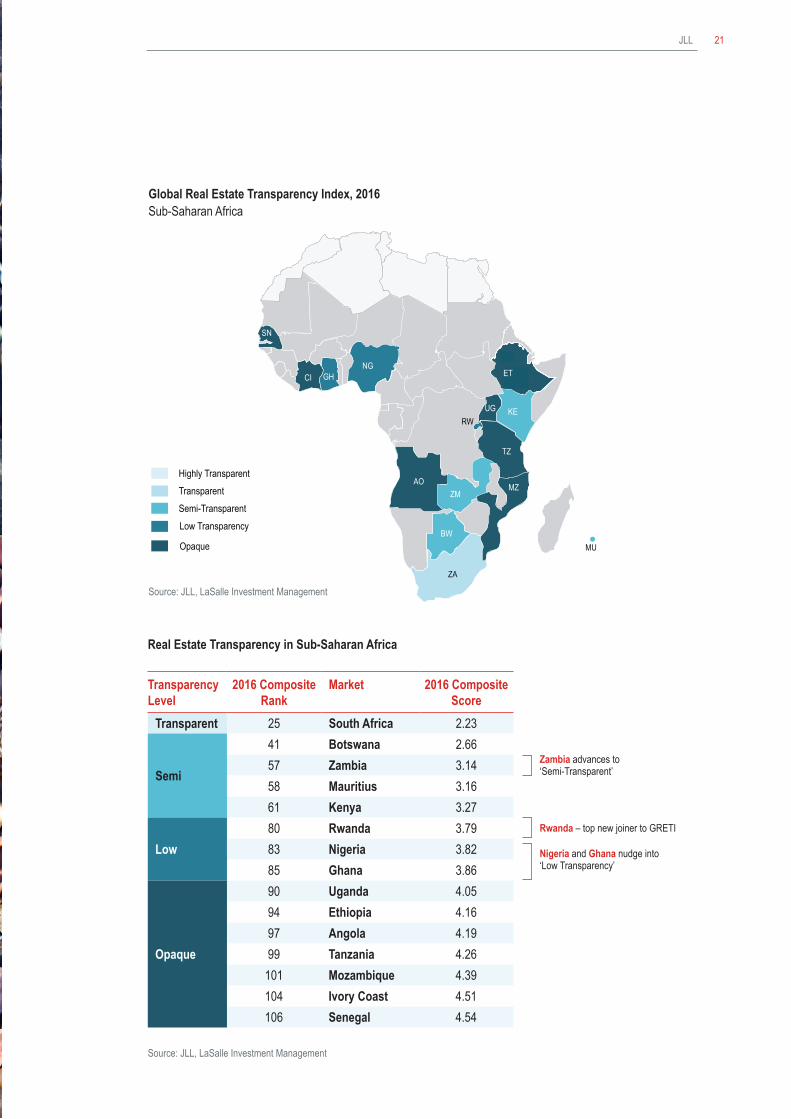

Transparency levels remain a focus for hotel investors in Sub-Saharan Africa, as is the case with real estate investors across the region. JLL’s 2016 Global Real Estate Transparency Index reveals that Sub-Saharan Africa has continued to make advances in real estate transparency over the last several years, although progress has been mixed.

Of the 12 markets in the region included in the 2014 index, six (Botswana, Zambia, Ethiopia, Nigeria, Angola and Ghana) have recorded progress in transparency with the remaining six either stagnating or regressing. Advances in the ”Market Fundamentals”, ”Performance Measurement” and ”Governance of Listed Vehicles” sub-indices have supported the overall regional improvement, as greater involvement by international real estate consultancies and local data providers elevates the level of access to information about real estate markets. South Africa remains the only country ranked as “Transparent”, while Botswana, Zambia, Mauritius and Kenya are all now classified as “Semi Transparent”.

20 Spotlight on Africa: A Diverse Frontier

JLL 21

Highly Transparent Transparent Semi-Transparent Low Transparency

Opaque

EG

SD

ZA

BW

KE

ZM

GH

AO

NG ET

MZ

SN

UG RW

CI

TZ

MU

Real Estate Transparency in Sub-Saharan Africa

Transparency Level

2016 Composite Rank

Market 2016 Composite Score

Transparent 25 South Africa 2.23

Semi

41 Botswana 2.6657 Zambia 3.1458 Mauritius 3.1661 Kenya 3.27

Low80 Rwanda 3.7983 Nigeria 3.8285 Ghana 3.86

Opaque

90 Uganda 4.0594 Ethiopia 4.1697 Angola 4.1999 Tanzania 4.26

101 Mozambique 4.39104 Ivory Coast 4.51106 Senegal 4.54

Source: JLL, LaSalle Investment Management

Zambia advances to ‘Semi-Transparent’

Rwanda – top new joiner to GRETI

Nigeria and Ghana nudge into ‘Low Transparency’

Source: JLL, LaSalle Investment Management

Global Real Estate Transparency Index, 2016Sub-Saharan Africa

Highly Transparent Transparent Semi-Transparent Low Transparency

Opaque

EG

SD

ZA

BW

KE

ZM

GH

AO

NG ET

MZ

SN

UG RW

CI

TZ

MU

22 Spotlight on Africa: A Diverse Frontier

Evolving debt markets

Given the critical role of debt in completing the capital stack and providing leveraged return on equity, we extended the research into hotel debt markets in Sub-Saharan Africa. For analysis purposes, we interviewed the leading hotel lenders focused on the region to understand their lending strategy and where they see opportunities and challenges.

Lender OverviewDebt funding in Sub-Saharan Africa’s hotel sector remains in its infancy across the region, primarily due to the perceived risks surrounding the variability of underlying cash flow of hotel operations. The majority of bankers interviewed are proceeding with caution in the sector, with a select few respondents steering clear of lending for hotels entirely. This confirms the sentiment expressed by investors that the ease of access to funding remains a challenge.

The higher level of uncertainty of the underlying cash flows for hotels in Sub-Saharan Africa, paired with the banks not having specific hotel lending teams, results in a hesitation of the commercial banks to take on development lending or single asset finance. The broader balance sheet of the project or deal sponsor and the recourse to other cash flows is generally the deciding factor in lending in many of the markets in the region. The added complexity to this is that certain markets like Kenya, South Africa and Mauritius have competitive local debt markets while others such as Ethiopia and Angola do not.

In the region, management agreements are the primary form of operating contracts and by their nature, the operating risk remains with the real estate owner rather than the operator in the case of leases. Our interviews confirmed an overwhelming preference for leases from lenders, with a number of respondents citing that it is the deciding factor as to whether they would consider hospitality lending. In addition to this, the opaque nature of a number of markets means that there is also a lack of information to access risks, meaning that without external recourse, direct owner surety or an operator performance guarantee, it is challenging for lending institutions to commit to hotel projects.

That being said, selective local, regional and international banks are discerningly lending to developers and long-term investors in the hotel sector, including both commercial and development banks. Each jurisdiction poses unique obstacles for lenders in terms of country risk, capital allocation, country lending limits and their house views for the sector. Development banks expressed less sensitivity to short-term economic and political adjustments, with an appetite for longer terms where a developmental agenda was in play. In this context, hotels are seen as an enabler of economic activity and as an employment creator in frontier markets, which is an important feature for development funding institutions.

Local banks throughout the region tend to have more limited access to capital, due to their balance sheets often being constrained by central bank regulations, particularly when it comes to providing foreign currency loans. This is challenging for hotel real estate as the sector tends to be capital intensive and driven by hard currency. Most of the large international banking groups remain very cautious when considering opportunities in the region as their experience in these local real estate markets is more limited. This often results in them being uncompetitive with risk adjusted lending terms.

22 Spotlight on Africa: A Diverse Frontier

JLL 23

The South Africa banking groups also have an ever increasing presence in Sub-Saharan Africa, supported by the establishment of regional hubs in East and West Africa, a clear sign of their intention to move strongly into these markets. A few South African banks have adopted the alternative strategy of expanding organically by following their South African client base into the region, yet their real estate lending continues to be focused on retail and commercial asset classes with underlying leases.

Lending criteria The track record of the investor and the operator are key considerations in a bank’s lending criteria. Banks will typically require security in the form of a registered first mortgage bond over the asset or require a pledge of shares in the special purpose vehicle. Unless the hotel has a lease agreement in place, or has reached stabilisation with a strong track record, most banks will require additional external recourse in the form of direct owner surety or by way of a performance guarantee from the operator. This external security can be reduced as the loan to asset value (LTV) decreases and cash flows strengthen after stabilisation. Respondents indicated that they take more comfort when the hotel operator has real skin in the game and is further aligned with the capital contributors through providing guarantees, equity participation or key money.

Loans terms The majority of commercial and development banks alike have a maximum threshold on income-producing assets of 50% LTV, whereas development projects come in at a similar level, albeit that these are assessed on a loan to cost (LTC) basis. There are certain exceptions to this rule, for example, the presence of a lease with strong covenants or external security can increase the LTV to 60% and above. South African respondents expressed comfort with increasing their exposure on occasions within South Africa based on the covenant of the borrower.

Preferred Form of Operator Guarantee

40% Operator fixed

lease/guarantee

60%Direct ownership surety

Hotel Loans Required

to be Fully Amortizing

40% No

60%Yes

Source: JLL, 2016

24 Spotlight on Africa: A Diverse Frontier

Local Currency vs. US Dollar Terms

Sub-Saharan Africa (including South Africa)

Sub-Saharan Africa (excluding South Africa)

When looking at development finance, these loans are more expensive and of a shorter duration. They tend to be capitalised as a project cost which is then refinanced or repaid on exit. The standard maximum loan term for stabilised hotels tends to be around seven years from a commercial bank, and up to ten years for development banks. Without corporate guarantees in place, commercial banks generally require that loans on income producing hotels be fully amortised over the term. Certain development banks are more flexible and may consider interest only loans, particularly during the first years of operation. We expect banks to reduce their amortisation requirements as liquidity improves and evidence of successful exits increases.

Cost of debtThe majority of hotel developments and transactions outside of South Africa are funded in US Dollar terms to align the capital structure with the predominantly US Dollar based cash flows. US Dollar denominated debt facilities are generally linked to LIBOR. The typical margin range over US Dollar LIBOR is between 4.0% and 7.5% for operational hotels and between 7.0% and 9.0% for development projects. This margin is dependent on the risk attached to the project, jurisdiction of the loan and capital available to the bank, with internal and external factors considered. Local and regional banks often lend in local currency and, due to high inflation, it is not uncommon for the interest rates to range between 18% and 25%. Certain commercial banks take a more competitive view on pricing, a strategy to secure ensuing transactional banking once the hotel begins trading.

0% 100%10% 30% 50% 70%20% 40% 60% 80% 90%

Local Currency US Dollars

Source: JLL, 2016

JLL 25

Lender All-in Pricing Range

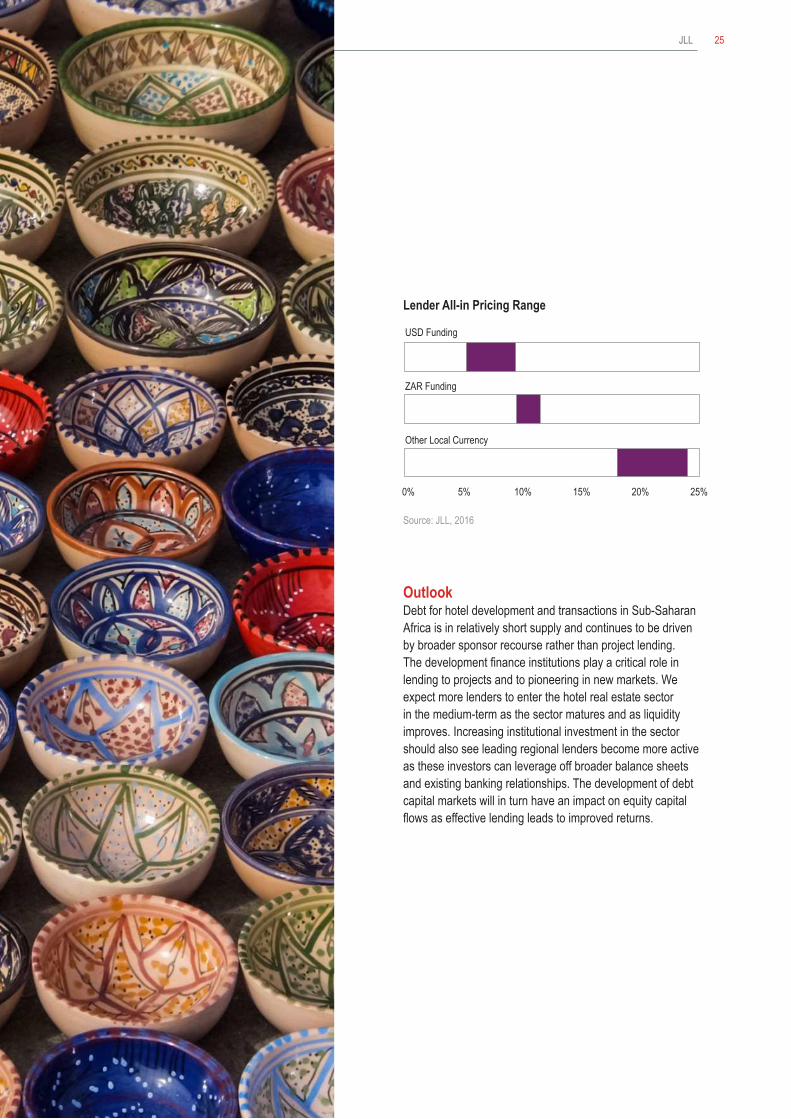

OutlookDebt for hotel development and transactions in Sub-Saharan Africa is in relatively short supply and continues to be driven by broader sponsor recourse rather than project lending. The development finance institutions play a critical role in lending to projects and to pioneering in new markets. We expect more lenders to enter the hotel real estate sector in the medium-term as the sector matures and as liquidity improves. Increasing institutional investment in the sector should also see leading regional lenders become more active as these investors can leverage off broader balance sheets and existing banking relationships. The development of debt capital markets will in turn have an impact on equity capital flows as effective lending leads to improved returns.

USD Funding

ZAR Funding

Other Local Currency

0% 25%5% 10% 15% 20%

Source: JLL, 2016

26 Spotlight on Africa: A Diverse Frontier

Sub-Saharan Africa offers a uniquely diverse set of hotel real estate markets with a broad range of opportunities and challenges, as well as risk and reward. From the perspective of global capital searching for investment opportunities, the region can be a challenging one to navigate. Investors and lenders alike are recognising this and while regional players continue to leverage their first mover advantage to entrench their presence in the sector, global capital markets are likely to increasingly flow into the region as markets mature and transparency increases.

The demand for hotel beds in Sub-Saharan Africa is underpinned by positive economic, demographic and tourism trends which should ensure that demand growth will be one of highest out of any region in the world. Hotel developers and operators are increasingly understanding how to tap into this demand and offering a broader hospitality offering best suited for each market and client base. This demand growth, paired with the more effective matching of supply to this demand, sets a good foundation for investment.

Hotel investors in the region are discerning in their investment decisions as hotel projects often compete for capital with other real estate asset classes and industries. The increase in political, economic and currency stability will see a reduction in the risk premium placed on hotel investment in the region which will in turn increase capital flows. Development costs should reduce further in the medium term as development professionals, owners and lenders gain further experience in the region. As the pipeline of new projects is more effectively implemented, liquidity will increase and exit options will improve.

Lenders are more cautious towards the hotel sector than their clients in the region and are challenged with underwriting operational cash flows in what is seen as an emerging sector. For the foreseeable future we expect commercial bank lending to be determined on the basis of recourse to the sponsor, while the development banks will play a critical role in pioneering new frontiers. As institutional investment increases, we expect lending to become more readily available at improved terms which will in turn provide better leverage returns on equity for investors.

Long-term investment fundamentals for the region remain positive despite the short-term challenges that have impacted the hotel sector in Sub-Saharan Africa in the past two years. Macro-economic development and government policy towards tourism, investment and economic growth remain critical in a corporate demand led sector. Hotel investors who carefully consider the supply and demand variables of the markets in which they develop and transact are well placed to generate high risk adjusted returns. Those who are able to establish platforms with scale should be increasingly well placed to attract external capital or become an acquisition prospect for larger global players. With such a wide range of opportunities and challenges in the region, this will continue to be a divergent region in which to invest.

Looking ahead

JLL 27JLL 27JLL 27

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. This report has been prepared solely for information purposes and does not necessarily purport to be a complete analysis of the topics discussed, which are inherently unpredictable. It has been based on sources we believe to be reliable, but we have not independently verified those sources and we do not guarantee that the information in the report is accurate or complete. Any views expressed in the report reflect our judgment at this date and are subject to change without notice. Statements that are forward-looking involve known and unknown risks and uncertainties that may cause future realities to be materially different from those implied by such forward-looking statements. Advice we give to clients in particular situations may differ from the views expressed in this report. No investment or other business decisions should be made based solely on the views expressed in this report.

JLL Regional Headquarters:

Chicago200 East Randolph DriveChicago, IL 60601USA+1 312 782 5800

London30 Warwick StreetLondon W1B 5NHUnited Kingdom+44 20 7493 4933

Singapore9 Raffles Place#39-00 Republic PlazaSingapore 048619+65 6220 3888

JLL Sub-Saharan Africa Offices:

JohannesburgOffice 303, 3rd Floor, The FirsCnr Biermann and Cradock AveRosebank, 2196+27 11 507 2200

LagosRoom 112, Mulliner Towers39 Alfred Rewane RoadLagos, Nigeria+234 1 448 9261

To find out how JLL can assist you in making real estate decisions in Africa, contact:

Jonathan HubbardHead of Investor ServicesHotels & Hospitality GroupEurope, Middle East and Africa+44 20 7399 [email protected]

Craig HeanManaging DirectorSub-Saharan Africa+27 11 507 [email protected]

Xander NijnensSenior Vice PresidentHotels & Hospitality GroupSub-Saharan Africa+27 11 507 [email protected]

Nairobi6th Floor, Delta TowerChiromo RoadNairobi, Kenya+254 7301 12024

Contributing Authors:

Wayne GodwinAssociateHotels & Hospitality GroupSub-Saharan Africa+27 11 507 [email protected]

James NathanAssociateHotels & Hospitality GroupSub-Saharan Africa+27 11 507 [email protected]