october 2000 ccefm doctoral program - …info.tuwien.ac.at/ccefm/outlines02/notes.pdf · literal...

TRANSCRIPT

Financial Markets and Instruments

Stefan Pichler

CCEFM Doctoral Program

October 2000

CCEFM Doctoral Program, Stefan Pichler

2

Overview

1 Money Markets and Instruments

2 Foreign Exchange Markets and Instruments

3 Bond Markets and Instruments

4 Swap Markets and Instruments

5 The Term Structure of Interest Rates

6 Financial Futures

7 Options

8 A First Look at the Fundamental Theorem of Asset Pricing

CCEFM Doctoral Program, Stefan Pichler

3

1 Money Markets and Instruments

¬ Borrowing and lending of time deposits.

¬ Money market instruments form basic building block of financial pricing models.

¬ Trading takes place only over-the-counter (OTC) and between financial intermediaries.

¬ Current supply and demand is quoted via data vendors.

CCEFM Doctoral Program, Stefan Pichler

4

RIC Bid Ask Source Time EUROND= 4.53 4.63 RLBL 14:41 EURTND= 4.53 4.63 GBBR 12:49 EURSND= 4.55 4.61 10:09 EURSWD= 4.57 4.63 14:15 EUR2WD= 4.57 4.67 AABI 11:56 EUR1MD= 4.62 4.72 RABQ 14:24 EUR2MD= 4.67 4.79 CDCE 14:34 EUR3MD= 4.74 4.86 CDCE 14:37 EUR4MD= 4.89 4.95 14:35 EUR5MD= 4.90 5.00 RLBL 14:41 EUR6MD= 4.96 5.08 CDCE 14:41 EUR9MD= 5.08 5.20 CDCE 14:41 EUR1YD= 5.19 5.25 14:36

Euro-Deposits on Sep 5, 2000. Source: Reuters.

CCEFM Doctoral Program, Stefan Pichler

5

¬ Banks usually quote for standard maturities.

¬ Settlement period for most trades is two days (except „OverNight“ and „Tomorrow/Next“).

¬ Marketmakers quote two-way prices with a bid/ask spread (bid/offer spread).

¬ Quoted rates are money market yields (MMY) with linear compounding.

Example: A bank borrows EUR 100,000 from CDCE for six months.

After six months the bank has to pay back 100,000](1+0.5]0.0508) =EUR 102,540

assuming six months are exactly equal to 0.5 years.

CCEFM Doctoral Program, Stefan Pichler

6

AFT � 1 � RT ]T PT �1

1 � RT ]T

AFT � (1 � RT)T PT � (1 � RT)�T

Accrual factor and discount factor

AFT accrual factor for maturity T

PT discount factor for maturity T

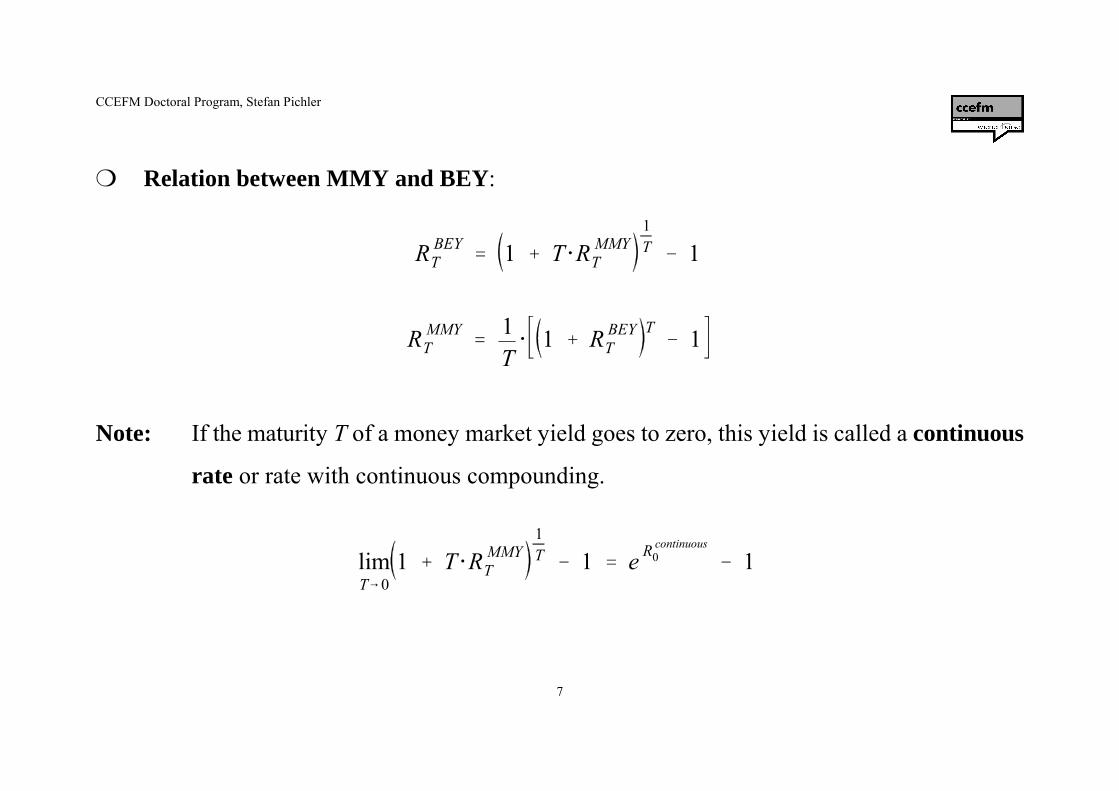

¬ If rates were quoted with annual compounding (bond equivalent yield, BEY), the following

would apply:

CCEFM Doctoral Program, Stefan Pichler

7

R BEYT � 1 � T ]R MMY

T

1T� 1

R MMYT �

1T] 1 � R BEY

TT� 1

limTS0

1 � T ]R MMYT

1T� 1 � e R continuous

0� 1

¬ Relation between MMY and BEY:

Note: If the maturity T of a money market yield goes to zero, this yield is called a continuous

rate or rate with continuous compounding.

CCEFM Doctoral Program, Stefan Pichler

8

T �number of days to maturitynumber of days in the year

¬ Determination of maturity T

The maturity T measures the time between two dates as a fraction of a year.

USD and EUR convention: actual/360

Literal number of calendar days between two dates divided by 360.

Alternatives: 30/360 (Eurobonds), actual/365 (GBP, CAD, GRD, some Asian

currencies), actual/actual (USD-TBills).

CCEFM Doctoral Program, Stefan Pichler

9

¬ Legal basis for money market transactions:

S ISDA (International Swaps and Derivatives Association) sets standards.

S Master agreements between banks and other financial intermediaries.

S 1992 ISDA Master Agreements.

S 2000 ISDA Definitions and Guidebooks.

S Reference: http://www.isda.org

CCEFM Doctoral Program, Stefan Pichler

10

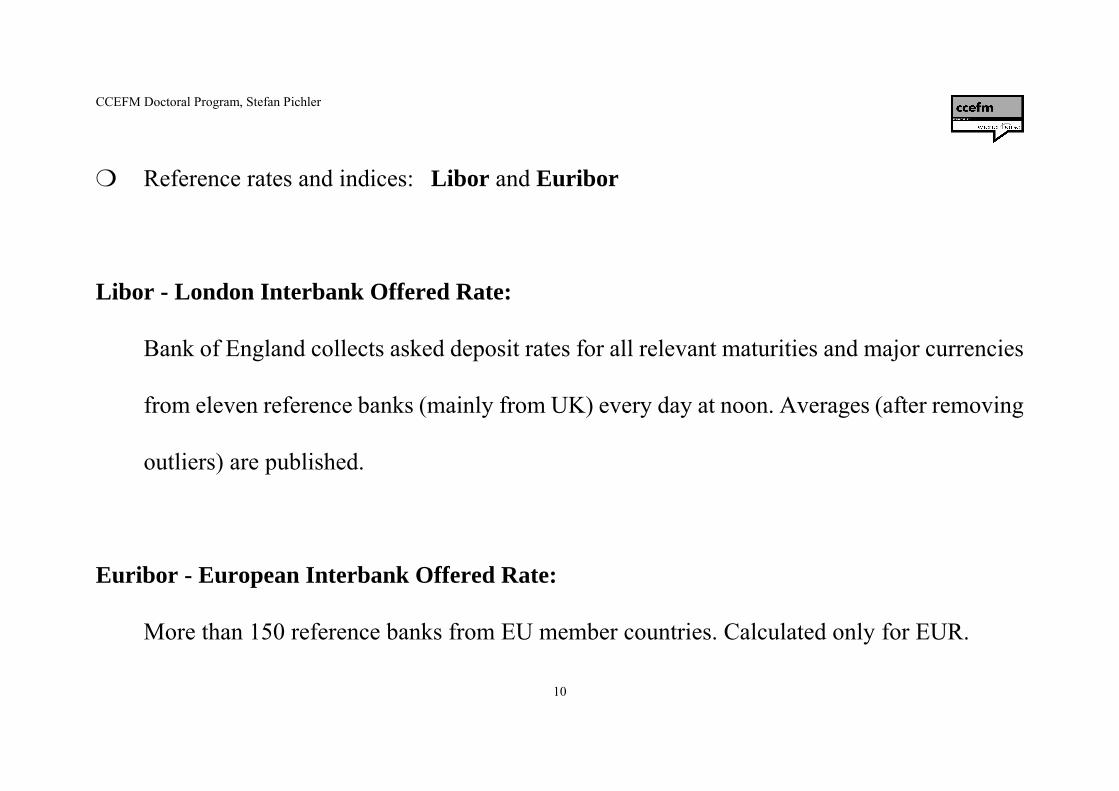

¬ Reference rates and indices: Libor and Euribor

Libor - London Interbank Offered Rate:

Bank of England collects asked deposit rates for all relevant maturities and major currencies

from eleven reference banks (mainly from UK) every day at noon. Averages (after removing

outliers) are published.

Euribor - European Interbank Offered Rate:

More than 150 reference banks from EU member countries. Calculated only for EUR.

CCEFM Doctoral Program, Stefan Pichler

11

¬ Money market securities:

S Short term zerobonds issued by governments: US Treasury Bills (T-Bills), British

short-term gilts, German Bundesschatzscheine, etc.

S Short term zerobonds issued by banks and corporates: Certificates of deposits (CDs),

Banker‘s acceptances (BAs), etc.

S Short term zerobonds issued by central banks.

CCEFM Doctoral Program, Stefan Pichler

12

¬ Basis pricing relationship: No-arbitrage principle

Example: 1M-Rate is quoted at 4.00%, Zerobond with one month to maturity and face value

of 100 is traded. What is the arbitrage-free price of the zerobond?

Pricing by Replication 0 1M

long zerobond - Price 100

long money market deposit -99.67 100

Note: 99.67 ] (1 �112

]0.04) � 100

¬ The price of the zerobond must equal 99.67. Otherwise arbitrage opportunities exist.

CCEFM Doctoral Program, Stefan Pichler

13

¬ Discount factor is the key pricing tool for money market instruments.

From the quoted deposit rate we know that ,P1M �1

1 �112

]0.04� 0.9967

hence the discount factor PT may be interpreted as the current price of a zerobond with unit face

value maturing at time T.

¬ A mapping P(T) can be seen as the discount function. It determines the present value of one

unit of currency paid T periods of time in the future.

¬ The discount function is an unambiguous representation of the time value of money.

CCEFM Doctoral Program, Stefan Pichler

14

¬ Basic properties of an arbitrage-free discount function:

(1) For one maturity T there is only one PT. (Otherwise direct arbitrage is possible).

(2) P0 = 1. (One Euro today is worth one Euro).

(3) PQ S 0. (The present value of one Euro in the distant future converges to zero).

(4) PT @ 1. (One Euro in the future is worth less than one Euro today).

(5) PT > 0. (The present value of one Euro is always positive).

(6) PT @ PS, if T>S. (The more distant a payment is in the future the smaller is its present value).

Note: (4) and (6) follow from the existence of cash positions. (3) does not strictly follow from

no-arbitrage.

CCEFM Doctoral Program, Stefan Pichler

15

¬ Money market deposits and zerobonds are cash instruments.

¬ There are markets for deposits and zerobonds settled in a future period of time. Those markets

are called forward markets.

¬ Basic no-arbitrage pricing of a forward contract on a traded asset with price S:

0 T

long forward 0 - Forward Price + ST

long asset - S0 + ST

short money market deposit + S0 - S0 / PT

total 0 - S0 / PT + ST

CCEFM Doctoral Program, Stefan Pichler

16

F �

S0

PT

¬ The forward price F of a traded asset is the accrued price of the underlying asset.

¬ Forward prices can be seen as relative prices, ie price of underlying asset divided by price of

zerobond.

¬ Forward contracts on short-term zerobonds are not actively traded in the markets.

CCEFM Doctoral Program, Stefan Pichler

17

f(T,T�h) �1h]

PT

PT�h

� 1

¬ Deposit rates fixed in advance for a future time period are called forward rates.

0 T T+h

long forward deposit 0 -1 1 + h]f(T,T+h)

short T-deposit + PT -1 0

long T+h-deposit - PT + PT / PT+h

sum 0 -1 + PT / PT+h

¬ The following must hold for the arbitrage-free forward rate fixed from T to T+h:

CCEFM Doctoral Program, Stefan Pichler

18

¬ Forward rates are actively quoted in the markets for forward rate agreements (FRAs).

¬ Typically, start and termination period are quoted in months, eg 6x9 means interest period

beginning six months from now and terminating nine months from now.

¬ Counterparties usually do not enter physical deposit positions. Contracts are settled in cash

at the beginning of the FRA period (time T).

¬ „Long“ and „short“ are seen from the position of debtors. To „buy“ a FRA means to bet on

rising rates.

CCEFM Doctoral Program, Stefan Pichler

19

Cash amount (buyer pays seller) � �1 �1 � h ] f(T,T�h)1 � h ]r(T,T�h)

� h ] f(T,T�h) � r(T,T�h)1 � h ]r(T,T�h)

¬ Cash settlement seen from the short position in a FRA (long position in time deposit) given

a money market rate r(T,T+h) prevailing at time T.

¬ A position in a FRA can be replicated by a position in two zerobonds or deposits. The

present value of the FRA position is thus determined by the value of its replicating

portfolio.

CCEFM Doctoral Program, Stefan Pichler

20

Term Bid Ask Source 1X4 5.05 5.07 TULLIB 2X5 5.13 5.14 TULLIB 3X6 5.21 5.22 TULLIB 4X7 5.14 5.15 TULLIB 5X8 5.19 5.2 TULLIB 6X9 5.23 5.26 NBP 7X10 5.27 5.28 TULLIB 8X11 5.28 5.3 TULLIB 9X12 5.29 5.32 SOC.GENERALE 1X7 5.13 5.15 TULLIB 2X8 5.19 5.21 TULLIB 3X9 5.245 5.275 SOC.GENERALE 4X10 5.24 5.26 TULLIB 5X11 5.28 5.29 TULLIB 6X12 5.295 5.325 SOC.GENERALE 9X15 5.34 5.37 SOC.GENERALE 12X18 5.405 5.435 SOC.GENERALE 18X24 5.44 5.46 TULLIB

Euro-FRAs on Sep 13, 2000. Source: Reuters.

CCEFM Doctoral Program, Stefan Pichler

21

Example: Bank buys 9x12 FRA from Societe Generale at the quoted rate on Sep 13, 2000. On

Jun 13, 2001 the relevant 3M-money market rate is 5.52%. The notional principal

of the transaction is EUR 1m. What is the amount the bank receives from Societe

Generale?

Day-count-fraction h: 92 days between Jun 13 and Sep 13, 2001. .h �92

360� 0.2555

Amount received: 0.2555 ] 0.0532 � 0.05521 � 0.2555 ]0.0552

]1m � EUR 504.00

CCEFM Doctoral Program, Stefan Pichler

22

2 Foreign Exchange Markets and Instruments

¬ Spot and forward transactions in tradable currencies.

¬ A certain amount of a currency is traded against a certain amount of an other currency

(reference currency). Prices refer to currency pairs.

¬ Trading takes place only over-the-counter (OTC) and between financial intermediaries.

¬ Current supply and demand is quoted via data vendors.

CCEFM Doctoral Program, Stefan Pichler

23

¬ FX trades are settled by transferring a bank deposit in the relevant currency.

¬ Settlement takes place two business days after the trading date. The settlement location is the

home of the traded currency.

¬ The exchange of currencies takes place using electronic message services like SWIFT

(international) or CHIPS and Fedwire (US).

¬ Major dealing centers are London, New York, and Tokyo. Other relevant loctions are

Singapore, Hong Kong, Zürich, and Frankfurt.

¬ Major currencys are USD, EUR, JPY, GBP, CHF, CAD, AUD.

CCEFM Doctoral Program, Stefan Pichler

24

Printed By Reuters : Unknown Thursday, 14 September 2000 11:35:02

RIC Bid/Ask Contributor Loc Srce Deal Time High Low

FX= WORLD SPOTS

ATS= 15.8001/92 REUTERS RTR RTRS 10:31 16.0582 15.7784

AUD= 0.5523/28 WESTPAC LON WBCL WBCL 10:29 0.5545 0.5483

AWG= 1.7650/ STANDCHART GFX 09:26

BBD= 1.985/ HSBC BANKPLC LON EM03 HKEK 07:55

BDT= 53.85/4.15 B'DESH BK DHA BKBG 04:07 53.85 54.15

BEF= 46.320/346 REUTERS RTR RTRS 10:31 47.077 46.256

BGN= 2.2341/57 RAIFFEISENBK SOF RBBS RZBS 10:31 2.2712 2.2278

BHD= 0.37696/7701 BNP BAHRAIN BAH BNPB BNPB 10:31 0.37700 0.37701

BIF= 757.463/122 TRADITION LON TRDM TRDZ 15:28

BMD= 0.995/ HSBC BANKPLC LON EM03 HKEK 08:44

BND= 1.7389/99 REUTERS LON RTRL RTRS 10:00

BOB= 6.25/ HSBC BANKPLC LON EM06 HKEK 07:54

Printed By Reuters : Unknown Thursday, 14 September 2000 11:36:55

CCEFM Doctoral Program, Stefan Pichler

25

RIC Bid/Ask Contributor Loc Srce Deal Time High Low

FX= WORLD SPOTS

EUR= 0.8693/98 BC ARABE MAD AREX AREX 10:33 0.8738 0.8569

FIM= 6.8365/97 REUTERS RTR RTRS 10:33 6.9387 6.8177

FJD= 0.4500/50 BARCLAYS LON BARL BBIL 08:04

FKP= 1.42735/ RRU LON EXOF 15:13

FRF= 7.5423/58 REUTERS RTR RTRS 10:33 7.6550 7.5216

GBP= 1.4164/74 BARCLAYS GFX BGFX 10:33 1.4215 1.4032

GHC= 6970/7270 STD BANK JHB SBIC SBSJ 07:04

GIP= 1.42735/ RRU LON EXOF 15:13

GMD= 13.00/4.50 STANDCHART GFX SCB1 ------ 09:58

GNF= 1735.00/ TRADITION LDN TRDM TRDZ 11:19

GRD= 388.81/9.34 NT BK GREECE ATH NBGX NBGX 10:33 394.85 388.21

GTQ= 7.78/ HSBC BANKPLC LON EM06 HKEK 07:55

Printed By Reuters : Unknown Thursday, 14 September 2000 11:38:36

RIC Bid Ask Srce Time RIC Bid Ask Srce Time

CCEFM Doctoral Program, Stefan Pichler

26

WX= MAJOR CROSSES

EUR= 0.8690 0.8692 SGOX 10:34 JPY= 107.20 107.23 ALFN 10:34

EURGBP=R 0.6136 0.6140 10:33 JPYGBP=R 0.6579 0.6584 10:34

EURJPY=R 93.23 93.30 10:34 JPYCHF=R 1.6385 1.6397 10:34

EURCHF=R 1.5283 1.5291 10:34 CHF= 1.7583 1.7588 NBP1 10:34

DEM= 2.2489 2.2499 RTRS 10:34 CHFGBP=R 0.4011 0.4014 10:33

DEMGBP=R 0.3136 0.3140 10:33 CHFJPY=R 60.99 61.04 10:34

DEMJPY=R 47.65 47.68 10:33 FRF= 7.5423 7.5458 RTRS 10:34

DEMCHF=R 0.7813 0.7816 10:34 FRFJPY=R 14.21 14.22 10:33

GBP= 1.4162 1.4165 AIBM 10:34 FRFGBP=R 0.0935 0.0936 10:33

GBPJPY=R 151.86 151.98 10:34 FRFCHF=R 23.30 23.30 10:34

GBPCHF=R 2.4888 2.4913 10:34

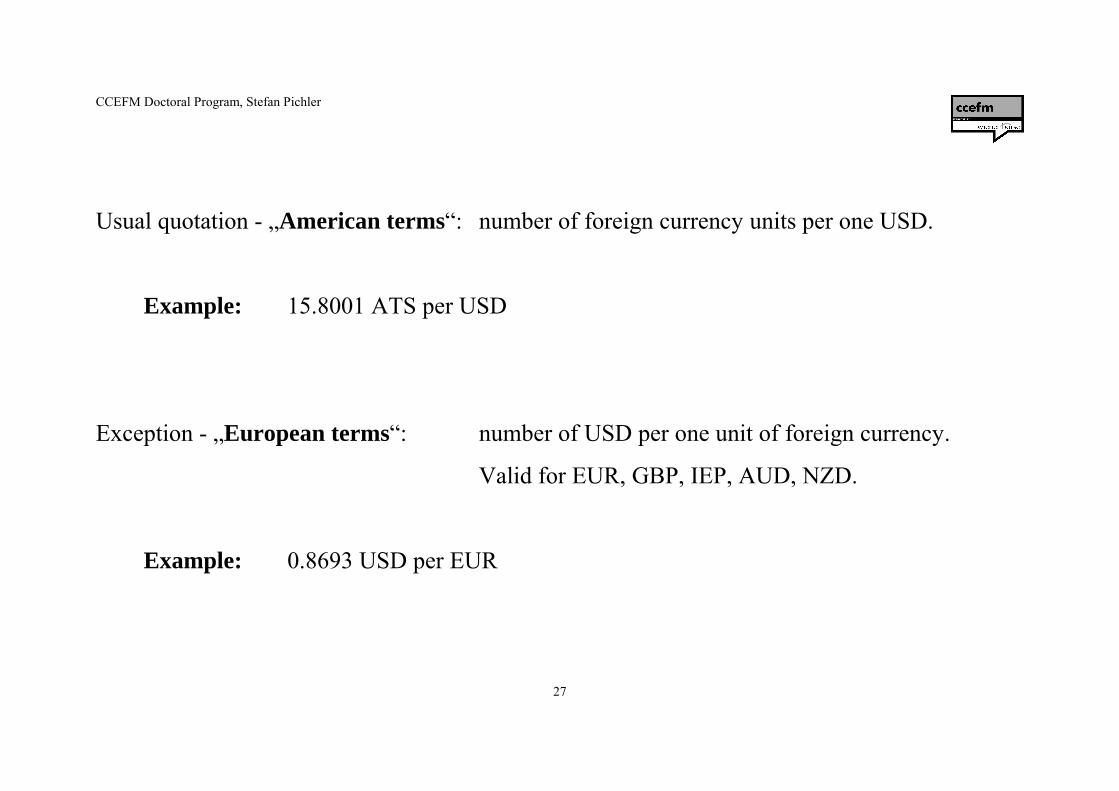

¬ Reference currency when quote is against USD:

CCEFM Doctoral Program, Stefan Pichler

27

Usual quotation - „American terms“: number of foreign currency units per one USD.

Example: 15.8001 ATS per USD

Exception - „European terms“: number of USD per one unit of foreign currency.

Valid for EUR, GBP, IEP, AUD, NZD.

Example: 0.8693 USD per EUR

CCEFM Doctoral Program, Stefan Pichler

28

¬ FX forward markets have increasing importance.

¬ A transaction where a currency is bought or sold at fixed price but settled at a future date is

called outright forward.

¬ A position in a FX forward can be replicated by a spot transaction and two money market

transactions.

¬ The forward price of the target currency is the price of a deposit in the target currency

accrued by the reference currency deposit rate.

CCEFM Doctoral Program, Stefan Pichler

29

Notation: St time t reference currency price of one unit of target currency

PTTAR discount factor in target currency

PTREF discount factor in reference currency

F0(T) forward price of one unit of target currency

Replication 0 T

long forward 0 - F0(T) [REF] + 1 [TAR]

long deposit in TAR - PTTAR [TAR] 1 [TAR]

spot transaction (buy TAR) + PTTAR [TAR]

- S0 PTTAR [REF]

short deposit in REF + S0 PTTAR [REF] - S0 PT

TAR / PTREF [REF]

sum 0 - S0 PTTAR / PT

REF [REF] + 1 [TAR]

CCEFM Doctoral Program, Stefan Pichler

30

F0(T) � S0 ]P TAR

T

P REFT

¬ Formula for arbitrage-free forward price:

¬ Forward price depends on the rate differential. The higher the deposit rate of the target

currency the lower its forward price.

¬ This is a version of the interest parity theorem.

CCEFM Doctoral Program, Stefan Pichler

31

¬ A spot sale of a currency with a simultaneous agreement to repurchase it at a fixed price some

date in the future (or a spot purchase with a resell agreement) is called a currency swap.

¬ The arbitrage-free repurchase price equals the relevant forward price.

¬ Typically, the difference between sale and repurchase price, ie the difference between

spot and forward price are quoted in the markets.

¬ This difference is called the FX swap rate. Swap rates are quoted in number of ticks. The

direction is forward price minus spot price.

CCEFM Doctoral Program, Stefan Pichler

32

Printed By Reuters : Unknown Thursday, 14 September 2000 13:50:54RIC Bid Ask Srce Time RIC Bid Ask Srce TimeEURF= EUR Deps & FwdsEUR= 0.8679 0.8681 SGOX 12:47EUROND= 4.45 4.55 NOLL 12:03 EURON= 0.44 0.49 LOYM 08:25EURTND= 4.45 4.55 NOLL 11:48 EURTN= 1.46 1.51 RLBL 12:12EURSND= 4.46 4.57 09:47 EURSN= 0.46 0.51 LOYM 09:45EURSWD= 4.48 4.58 SELY 12:12 EURSW= 3.35 3.42 GBBR 12:43EUR2WD= 4.53 4.65 CDCE 11:43 EUR2W= 6.65 6.75 AABX 11:39EUR1MD= 4.60 4.72 SUMO 12:20 EUR1M= 13.78 13.98 SELY 12:42EUR2MD= 4.68 4.80 CDCE 12:45 EUR2M= 27.98 28.28 SELY 12:42EUR3MD= 4.75 4.87 CDCE 12:45 EUR3M= 39 41 12:43EUR4MD= 4.91 4.96 TIBB 12:45 EUR4M= 49.00 55.00 11:52EUR5MD= 4.96 5.02 BCIX 12:04 EUR5M= 62.50 68.50 11:52EUR6MD= 4.95 5.07 CDCE 12:45 EUR6M= 73.3 75.0 DBFX 12:46EUR9MD= 5.06 5.18 CDCE 12:46 EUR9M= 103.65 105.15 SELY 12:42EUR1YD= 5.15 5.27 CDCE 12:46 EUR1Y= 133.8 136.0 DBFX 12:46EUR2YD= 5.38 5.48 11:51 EUR2Y= 254 268 DBFX 12:33EUR3YD= 5.45 5.55 11:51 EUR3Y= 362 382 DBFX 12:43EUR4YD= 5.54 5.64 11:51 EUR4Y= 464 504 DBFX 12:37EUR5YD= 5.60 5.70 11:51 EUR5Y= 560 650 CHNY 12:19

CCEFM Doctoral Program, Stefan Pichler

33

Printed By Reuters : Unknown Thursday, 14 September 2000 13:54:43

RIC Bid Ask Srce Time RIC Bid Ask Srce Time

DM= Deposits-Majors

USDOND= 6.41 6.53 ABCZ 12:31

USDTND= 6.55 6.65 RLBL 12:32

USDSND= 6.50 6.58 HALI 12:45

USDSWD= 6.52 6.58 NMRM 12:50

USD1MD= 6.50 6.62 ABCZ 12:32

USD2MD= 6.58 6.64 NMRM 12:50

USD3MD= 6.60 6.66 NMRM 12:50

USD6MD= 6.68 6.74 NMRM 12:50

USD9MD= 6.65 6.77 SGOX 12:44

USD1YD= 6.70 6.82 SGOX 12:44

CCEFM Doctoral Program, Stefan Pichler

34

F0(T) � 0.8681 ] 0.988140.98344

� 0.8722

Example: A bank wants to replicate a long position in the USD/EUR 3M forward. Does

the quote - 41 ticks - correspond to its arbitrage-free value?

Trades will be settled on Sep 18. The day count fraction for three months is 91/360 = 0.25277.

Target currency: EUR Reference currency: USD

EUR deposit rate at bid: 4.75% P3MTAR = 0.98814

USD deposit rate at ask: 6.66% P3MREF = 0.98344

USD/EUR at ask: S0 = 0.8681 [USD]

Difference is 0.8722 - 0.8681 = 0.0041. This equals exactly the quote!

CCEFM Doctoral Program, Stefan Pichler

35

3 Bond Markets and Instruments

¬ A bond is a security issued by a debtor to its creditors (investors) which guarantees a certain

repayment structure.

¬ Primary markets: Initial sale of bonds by their issuers.

¬ Secondary markets: Trading of portions of already issued bonds among market participants.

¬ Reference point for all features of a bond is its notional principal. All items are measured in

percent of the notional principal.

CCEFM Doctoral Program, Stefan Pichler

36

Example: 5-year-bond over a notional principal of 100,000 issued by the Realm of

Vertania.The bond pays a 8% coupon on an annual basis. The face value is 100%.

The Realm of Vertania guarantees

100,000.--payable on Oct 14, 2005 at Bank Vertania

8,000.--Oct 14, 2001

8,000.--Oct 14, 2002

8,000.--Oct 14, 2003

8,000.--Oct 14, 2004

8,000.--Oct 14, 2005

CCEFM Doctoral Program, Stefan Pichler

37

¬ Face value: Usually 100% of notional principal.

¬ Repayment: Typically the face value is paid in one amount at the maturity of the

bond.

¬ Coupon rate: Straight bonds have a fixed coupon rate (eg, US Treasury Bonds, German

Bunds). Coupons of floating rate notes (FRNs) are reset periodically

depending on a reference rate or index (eg, Libor, Euribor).

¬ Coupon basis: Annual basis for most EUR denominated issues, semiannual basis for

most USD issues, quarterly basis for many floating rate notes.

CCEFM Doctoral Program, Stefan Pichler

38

Accrued interest � C ]d

¬ Additional features: Call or prepayment features, conversion features, ....

¬ Determination of market prices:

To smooth price behaviour bonds are typically quoted without taking the next coupon

payment into account. Nevertheless, the accrued value of the coupon payment (accrued

interest) has to be paid to the seller of the bond.

C Annual coupon rate

d Time since last coupon date in years (usually measured actual/365; in some markets

30/360 apply).

CCEFM Doctoral Program, Stefan Pichler

39

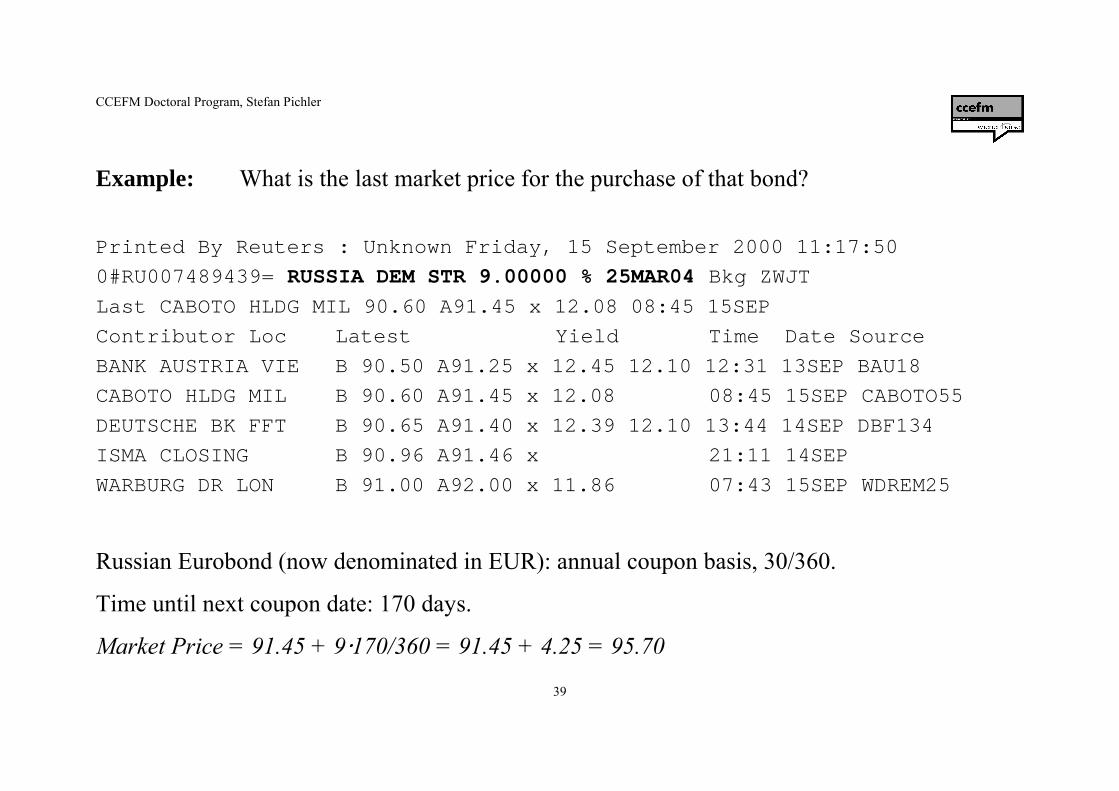

Example: What is the last market price for the purchase of that bond?

Printed By Reuters : Unknown Friday, 15 September 2000 11:17:50

0#RU007489439= RUSSIA DEM STR 9.00000 % 25MAR04 Bkg ZWJT

Last CABOTO HLDG MIL 90.60 A91.45 x 12.08 08:45 15SEP

Contributor Loc Latest Yield Time Date Source

BANK AUSTRIA VIE B 90.50 A91.25 x 12.45 12.10 12:31 13SEP BAU18

CABOTO HLDG MIL B 90.60 A91.45 x 12.08 08:45 15SEP CABOTO55

DEUTSCHE BK FFT B 90.65 A91.40 x 12.39 12.10 13:44 14SEP DBF134

ISMA CLOSING B 90.96 A91.46 x 21:11 14SEP

WARBURG DR LON B 91.00 A92.00 x 11.86 07:43 15SEP WDREM25

Russian Eurobond (now denominated in EUR): annual coupon basis, 30/360.

Time until next coupon date: 170 days.

Market Price = 91.45 + 9]170/360 = 91.45 + 4.25 = 95.70

CCEFM Doctoral Program, Stefan Pichler

40

¬ Domestic bond markets

S Government bonds issued in local currency are the most important segment.

S Bonds issued by financial intermediaries form the second important group.

S The third group with increasing importance are corporate bonds.

S Bonds issued by special agencies (mortgage bonds, Pfandbriefe) form relevant

submarkets.

S Although most issues are listed at exchanges, most trading takes place OTC.

CCEFM Doctoral Program, Stefan Pichler

41

¬ Foreign bond and Eurobond markets

S Foreign bonds are bonds that are issued by foreign borrowers in a nation‘s domestic

market and are denominated in the nation‘s domestic currency.

S Examples for large foreign bond markets are Yankee bonds, Samurai bonds, CHF-

denominated bonds, Brady bonds.

S Eurobonds denominated in a particular currency (USD, EUR, GBP, CHF, JPY) are

issued simultaneously in the markets of several nations.

S Eurobonds are traded exclusively OTC.

CCEFM Doctoral Program, Stefan Pichler

42

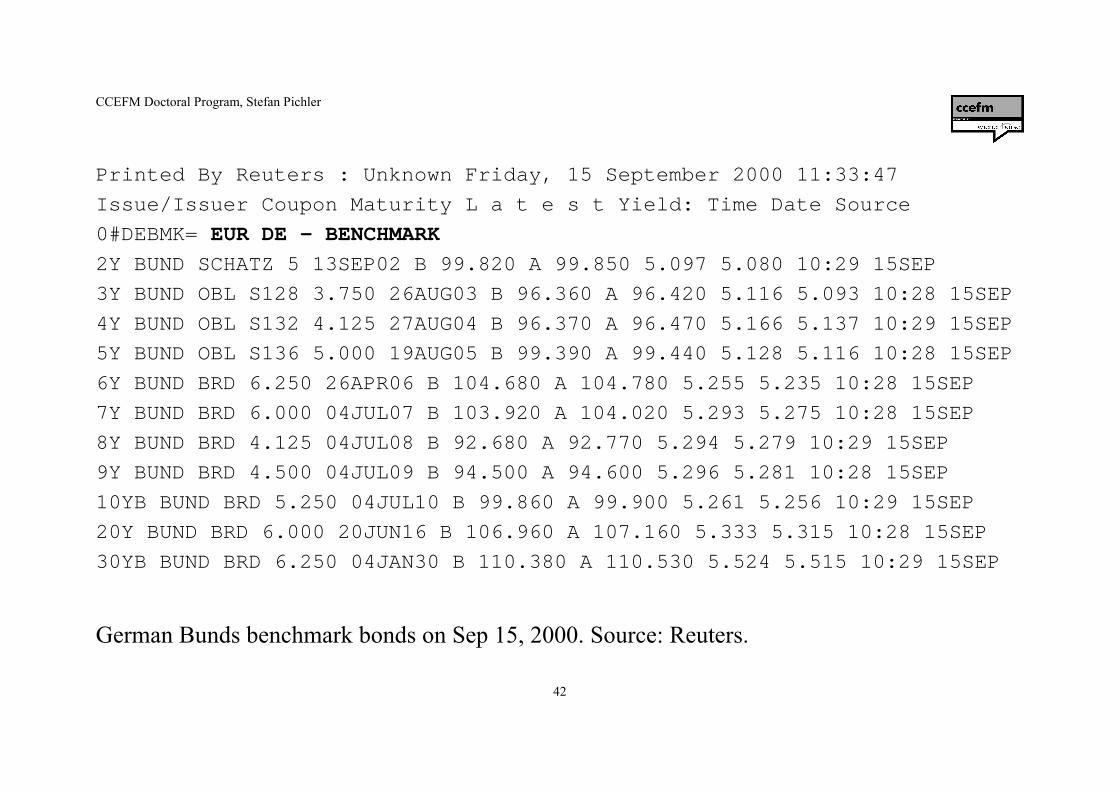

Printed By Reuters : Unknown Friday, 15 September 2000 11:33:47

Issue/Issuer Coupon Maturity L a t e s t Yield: Time Date Source

0#DEBMK= EUR DE - BENCHMARK

2Y BUND SCHATZ 5 13SEP02 B 99.820 A 99.850 5.097 5.080 10:29 15SEP

3Y BUND OBL S128 3.750 26AUG03 B 96.360 A 96.420 5.116 5.093 10:28 15SEP

4Y BUND OBL S132 4.125 27AUG04 B 96.370 A 96.470 5.166 5.137 10:29 15SEP

5Y BUND OBL S136 5.000 19AUG05 B 99.390 A 99.440 5.128 5.116 10:28 15SEP

6Y BUND BRD 6.250 26APR06 B 104.680 A 104.780 5.255 5.235 10:28 15SEP

7Y BUND BRD 6.000 04JUL07 B 103.920 A 104.020 5.293 5.275 10:28 15SEP

8Y BUND BRD 4.125 04JUL08 B 92.680 A 92.770 5.294 5.279 10:29 15SEP

9Y BUND BRD 4.500 04JUL09 B 94.500 A 94.600 5.296 5.281 10:28 15SEP

10YB BUND BRD 5.250 04JUL10 B 99.860 A 99.900 5.261 5.256 10:29 15SEP

20Y BUND BRD 6.000 20JUN16 B 106.960 A 107.160 5.333 5.315 10:28 15SEP

30YB BUND BRD 6.250 04JAN30 B 110.380 A 110.530 5.524 5.515 10:29 15SEP

German Bunds benchmark bonds on Sep 15, 2000. Source: Reuters.

CCEFM Doctoral Program, Stefan Pichler

43

MV � ˆJ

j�1Zj ] (1 � YTM)�Tj

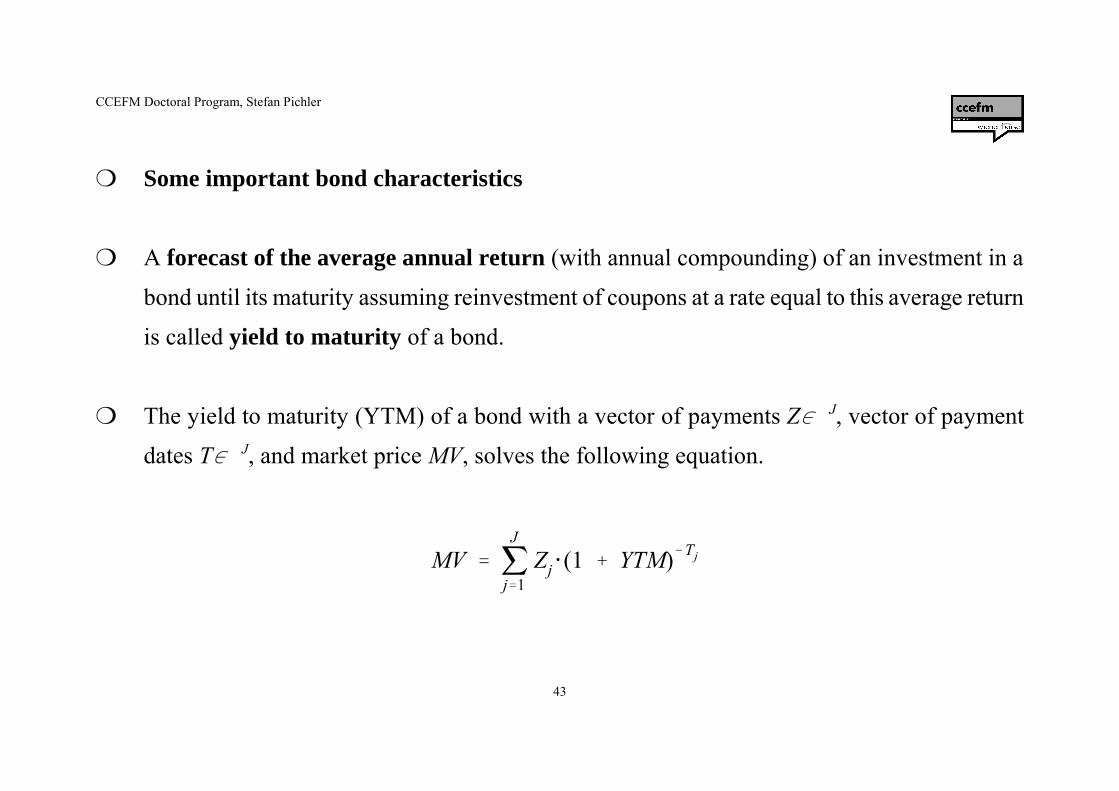

¬ Some important bond characteristics

¬ A forecast of the average annual return (with annual compounding) of an investment in a

bond until its maturity assuming reinvestment of coupons at a rate equal to this average return

is called yield to maturity of a bond.

¬ The yield to maturity (YTM) of a bond with a vector of payments Zc J, vector of payment

dates Tc J, and market price MV, solves the following equation.

CCEFM Doctoral Program, Stefan Pichler

44

DD � �1

1 � YTM]ˆ

J

j�1Tj ]Zj ] (1 � YTM)�Tj

¬ The first derivative of the market value of a bond with respect to its YTM is called dollar

duration (DD) of a bond. It measures the dollar sensitivity of a bond price to changes of its

yield.

¬ The dollar sensitivity of a bond price to a one basis point change of its yield is called price

value of a basis point (PVBP). PVBP = DD / 10,000.

¬ The percentage sensitivity of a bond price to changes of its yield is calles modified duration

(MD). MD = DD / MV.

CCEFM Doctoral Program, Stefan Pichler

45

Example: Calculate the characteristics of the 6Y-Benchmark Bund.

The market price including accrued interest is 107.21.

YTM is given by a numerical solution. YTM = 5.237.

T Z P Z*P T*Z*P0.6110 6.25 0.96930 6.06 3.701.6110 6.25 0.92106 5.76 9.272.6110 6.25 0.87523 5.47 14.283.6110 6.25 0.83167 5.20 18.774.6110 6.25 0.79029 4.94 22.775.6110 106.25 0.75096 79.79 447.69

total: 107.21 516.50

DD =490.80, PVBP = 0.0491, MD = 4.58.

CCEFM Doctoral Program, Stefan Pichler

46

8.00 8.00 8.00 8.00

108.00

0.0020.0040.0060.0080.00

100.00120.00

1 2 3 4 5

Payment dates

Cash Flow Mapping: 5Y- 8%-Coupon Bond

Cash Flow

¬ Valuation of straight bonds: Replication by zerobonds.

CCEFM Doctoral Program, Stefan Pichler

47

Example: In the Pokemon bond market discount factors (ie zerobond prices) are

1Y-0.96154 2Y-0.92456 3Y-0.88900 4Y-0.85480 5Y-0.82193

(note that these discount factors correspond to a 4% annual interest rate).

Derive the arbitrage-free price of the Pikachu bond.

Solution I: Calculate the value of each individual zerobond and take the sum.

8] 0.96154 + 8] 0.92456 + 8] 0.88900 + 8] 0.85480 + 108] 0.82193 = 117.81

Solution II: Form a vector of cash flows Z´ = (8,8,8,8,108) and a vector of discount factors d´

= 0.96154, 0.92456, 0.88900, 0.85480, 0.82193). Then the inner product of those

vectors yields the price. Z´] d = 117.81.

CCEFM Doctoral Program, Stefan Pichler

48

¬ Valuation of floating rate notes (floaters) is more complicated in some cases.

¬ Exact knowledge of coupon fixing and additional features is important.

¬ Reference rate: money market rate (Libor), capital market rate (CMT)

The maturity of the reference rate corresponds to the length of the coupon or reset period

(natural time lag).

¬ Reset date: in advance (usually), in arrears, averaging periods

¬ Additional features: margin, roundoff, cap, floor, drop-lock, conversion

CCEFM Doctoral Program, Stefan Pichler

49

¬ A floater indexed to a money market rate with natural time lag which is reset in advance and

has no additional features is called perfectly indexed.

¬ A perfectly indexed floater can easily be replicated by a revolving money market strategy.

0 1 2 ... 9 10

Long floater - price Libor(0) Libor(1) ... Libor(8) 1 + Libor(9)

Replication

strategy

- 1 1 + Libor(0)

- 1

1 + Libor(1)

-1

... 1 + Libor(8)

-1

1 + Libor(9)

¬ The amount necessary to initiate the replicating strategy equals exactly the notional principal

of the floater. Hence, at a reset date the arbitrage-free price of a floater equals 100%.

CCEFM Doctoral Program, Stefan Pichler

50

PV � (1 � c0 ) ]PT

¬ Between two reset dates the current coupon c0 is a known quantity. At the next coupon/reset

date the arbitrage-free value of the remaining stream of cash flows is again 100%.

¬ The arbitrage-free value PV of a floater with T years to the next coupon date is given by

¬ A perfectly indexed floater can always be mapped into a zerobond with maturity until the

next reset date.

CCEFM Doctoral Program, Stefan Pichler

51

PV � P(T) ] (1 � c0 ) � Margin ]ˆN�1

i�1P(T� ih)

¬ If the floater pays a margin (eg, Libor + 50 bp) the valuation is done by separating the

margin (ie stream of fixed payments) from the perfectly indexed part of the floater (ie

zerobond).

¬ With N payment dates outstanding and a length of the coupon period h the value of a floater

is given by

CCEFM Doctoral Program, Stefan Pichler

52

Z � h ]Libor (T�h)

h ]Libor (T�h) �1

PT�h(h)� 1

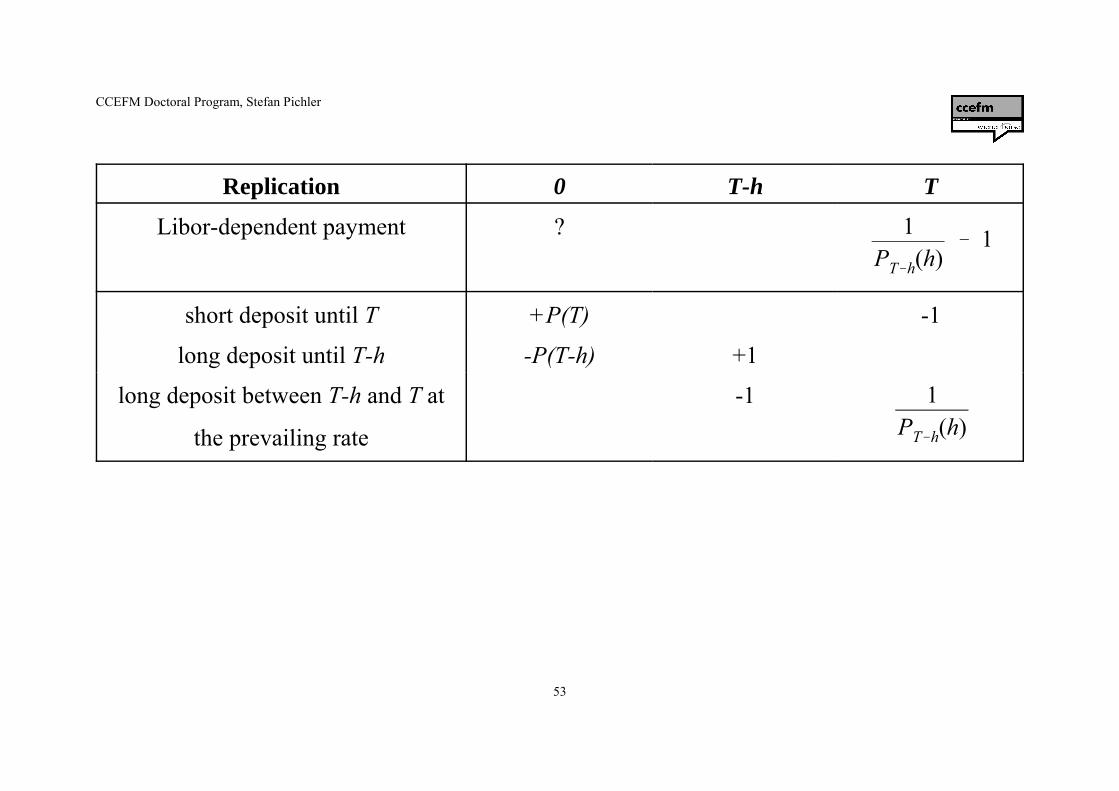

¬ Replication of a single Libor-dependent payment:

The payoff of a single Libor-dependent coupon paid at time T (natural time lag, reset in advance)

is given by

where h denotes the length of the coupon period. Rewriting Libor in terms of discount factors

prevailing at time T-h yields

CCEFM Doctoral Program, Stefan Pichler

53

Replication 0 T-h T

Libor-dependent payment ? 1PT�h(h)

� 1

short deposit until T +P(T) -1

long deposit until T-h -P(T-h) +1

long deposit between T-h and T at

the prevailing rate

-1 1PT�h(h)

CCEFM Doctoral Program, Stefan Pichler

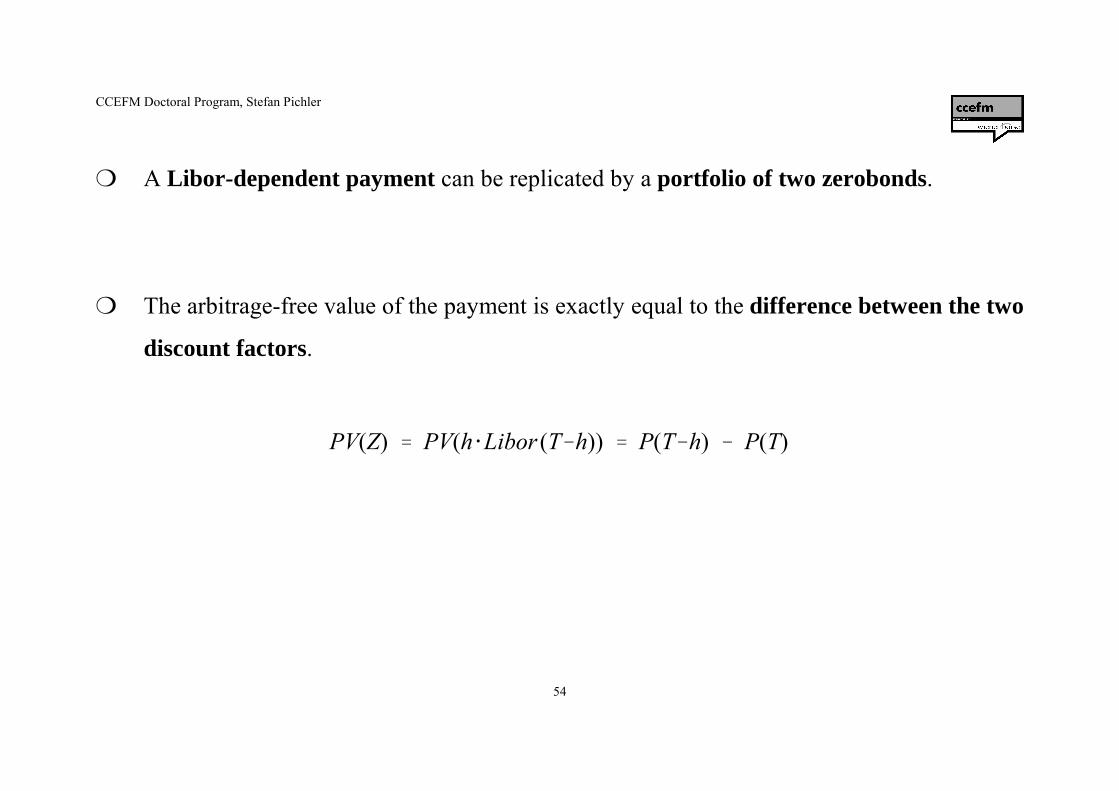

54

PV(Z) � PV(h ]Libor (T�h)) � P(T�h) � P(T)

¬ A Libor-dependent payment can be replicated by a portfolio of two zerobonds.

¬ The arbitrage-free value of the payment is exactly equal to the difference between the two

discount factors.

CCEFM Doctoral Program, Stefan Pichler

55

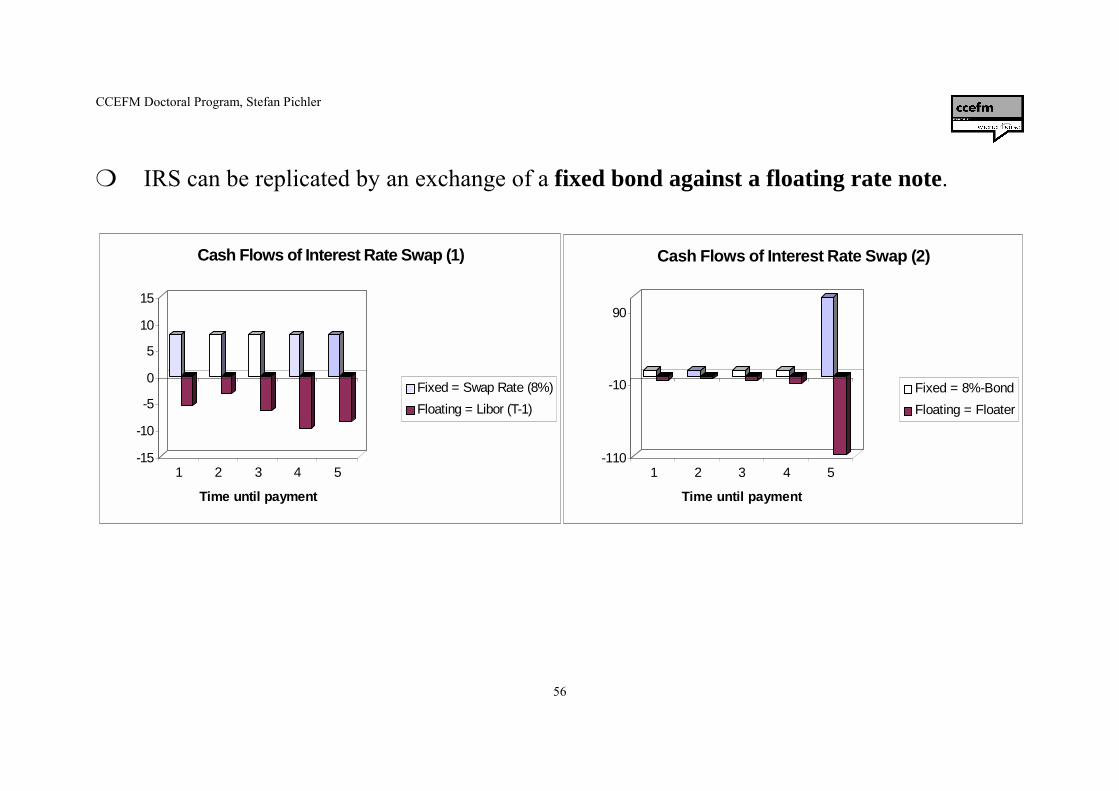

4 Swap Markets and Instruments

¬ This chapter is focused on interest rate swaps (IRS).

¬ IRS is an agreement beween two parties to exchange fixed against floating payments.

¬ Usually, there are no up-front payments. At the time of initiation, the value of the fixed leg

equals the value of the floating leg.

CCEFM Doctoral Program, Stefan Pichler

56

-15

-10

-5

0

5

10

15

1 2 3 4 5

Time until payment

Cash Flows of Interest Rate Swap (1)

Fixed = Swap Rate (8%)Floating = Libor (T-1)

-110

-10

90

1 2 3 4 5

Time until payment

Cash Flows of Interest Rate Swap (2)

Fixed = 8%-BondFloating = Floater

¬ IRS can be replicated by an exchange of a fixed bond against a floating rate note.

CCEFM Doctoral Program, Stefan Pichler

57

-110

-10

90

1 2 3 4 5

Time until payment

Cash Flows of Interest Rate Swap (3)

Fixed = 8%-BondFloating = 1Y-Zerobond

¬ Since a floater can be replicated by a zerobond, the following portfolio of zerobonds is the

exact replication of an IRS.

CCEFM Doctoral Program, Stefan Pichler

58

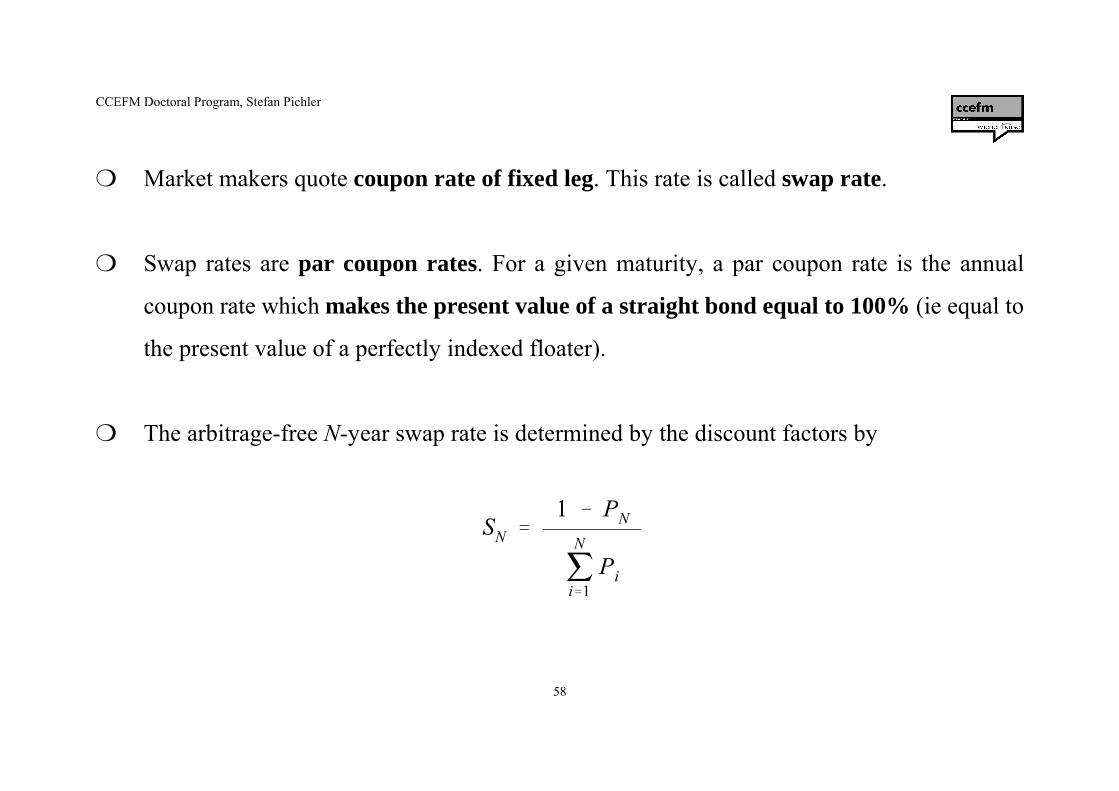

SN �

1 � PN

ˆN

i�1Pi

¬ Market makers quote coupon rate of fixed leg. This rate is called swap rate.

¬ Swap rates are par coupon rates. For a given maturity, a par coupon rate is the annual

coupon rate which makes the present value of a straight bond equal to 100% (ie equal to

the present value of a perfectly indexed floater).

¬ The arbitrage-free N-year swap rate is determined by the discount factors by

CCEFM Doctoral Program, Stefan Pichler

59

¬ If a party enters a IRS and receives fixed payments (and pays floating), it enters a receiverswap.

¬ If a party enters a IRS and pays fixed payments (and receives floating), it enters a payerswap.

¬ Reference rate is usually 3M or 6M Libor/Euribor.

¬ EUR-IRS pay annual coupons, USD-IRS pay semi-annual coupons.

CCEFM Doctoral Program, Stefan Pichler

60

Printed By Reuters : Unknown Thursday, 21 September 2000 16:57:12EUR IRS FOCUS EURIRS LINKED DISPLAYS MONEYEUR AB/6M EURIBOR DEALING1Y 5.2100 5.2400 HVB GERMANY MUN HVBG 15:522Y 5.3275 5.3575 HVB GERMANY MUN HVBG 15:523Y 5.4350 5.4650 HVB GERMANY MUN HVBG 15:524Y 5.523 5.553 ABN AMRO AMS 15:525Y 5.601 5.631 ABN AMRO AMS 15:526Y 5.6800 5.7100 RABOBANK AMS 15:527Y 5.7575 5.7875 RABOBANK AMS 15:528Y 5.815 5.845 BANK AMERICA LON 15:539Y 5.8700 5.8900 TRADITION LON 15:5310Y 5.9050 5.9250 TRADITION LON 15:5312Y 5.9575 5.9975 TRADITION LON 15:5315Y 6.0400 6.0800 TRADITION LON 15:5320Y 6.1175 6.1575 TRADITION LON 15:5325Y 6.1400 6.1800 TRADITION LON 15:5330Y 6.1300 6.1700 TRADITION LON 15:53

CCEFM Doctoral Program, Stefan Pichler

61

Example: A bank enters a 5Y-payer swap with ABN-AMRO on Sep 21, 2000. Assume thaton Mar 21, 2001 the 6M-Euribor is fixed at 5.12%. What is the cash flow betweenthe bank and ABN-AMRO on Sep 21, 2001?

Fixed leg: On each Sep 21 the bank is obliged to pay 5.631% of notional principal.

Floating leg: On each Mar 21 and Sep 21 the bank receives h] 6M-Euribor, where h denotes therelevant daycount fraction and 6M-Euribor denotes the Euribor observed at thebeginning of the coupon period. On Sep 21, 2001 the bank receives (184/365)]5.12% = 2.581% of notional principal.

On Sep 25, 2001 (two business days later) a payment of 5.631% - 2.581% = 3.05% of notionalprincipal is settled, ie has to be paid by the bank to ABN-AMRO.

CCEFM Doctoral Program, Stefan Pichler

62

¬ The standard type of IRS are fixed against floating swaps.

¬ Basis swaps are agreements to exchange floating payments tied to different reference (=basis)rates, eg, 3M-Libor against 6M-Libor.

¬ Yield curve swaps are agreements to exchange floating rate payments tied to a long termzero-coupon yield (or YTM of a specific bond) against Libor/Euribor.

¬ Constant maturity swaps are agreements to exchange floating rate payments tied to a parcoupon rate (swap rate or constant maturity treasury rate) against Libor/Euribor.

¬ Callable Swaps are IRS where on each reset date one party has the right to cancel the swapwithout any payment. This option is called Bermudan Swaption.

CCEFM Doctoral Program, Stefan Pichler

63

-1.5

-1

-0.5

0

0.5

1

1 2 3 4 5 6 7Maturity

Mapped Cash Flows of a Forward Payer Swap

FlaotingFix

¬ A forward starting swap (FSS) is an agreement between two parties to enter a prespecifiedIRS at some fixed date in the future.

CCEFM Doctoral Program, Stefan Pichler

64

PV(Float) � PV(Fix)

P(t,T) � P(t,T�N) � FSRt ] ˆT�N

i�T�1P(t,i)

v FSRt �P(t,T) � P(t,T�N)

Ht(T,N), Ht(T,N) � ˆ

T�N

i�T�1P(t,i)

¬ Determination of the forward swap rate of an N-year FSS starting at time T:

FSRt Forward swap rate at time t P(t,T) Discount factor for maturity T seen at time tP(t,T+N) Discount factor for maturity T+N seen at time tHt(T,N) Present value of portfolio of zerobonds with maturities corresponding to the

payment dates of the underlying swap

CCEFM Doctoral Program, Stefan Pichler

65

t � 0, T � 1 , N � 3:

Ht(T,N) � ˆT�N

i�T�1P(t,i) � ˆ

4

i�2P(0,i) � 0.94292 � 0.90854 � 0.87239 � 2.72385

FSRt �P(t,T) � P(t,T�N)

Ht

�P(0,1) � P(0,4)

Ht

�0.97393 � 0.87239

2.72385� 3.728%

Example: Determine the arbitrage-free forward swap rate for a 3Y-FSS starting in one yeargiven the following discount factors:

1Y-0.97393 2Y-0.94292 3Y-0.90854 4Y-0.87239

CCEFM Doctoral Program, Stefan Pichler

66

5 The Term Structure of Interest Rates

¬ The basic relationship between present value and maturity of future payments is called theterm structure of interest rates.

¬ Discount factors and zero-coupon rates are equivalent representations.

¬ Discount function (discrete / continuous) is the key instrument for valuation.

¬ Where does the discount function come from?

CCEFM Doctoral Program, Stefan Pichler

67

¬ Direct observation: Quotes of money market deposits or prices of zerobonds.

¬ At least for longer maturities too little information.

¬ Indirect observation: Calculation/estimation of discount factors implied by prices ofarbitrary fixed income instruments (eg, swaps, coupon bonds).

¬ Term structure estimation crucially depends on market completeness.

CCEFM Doctoral Program, Stefan Pichler

68

Zi1 PT1� Zi2 PT2

� ... � ZiJ PTJ� MVi

¬ Informal definition of market completeness:

„A market where sufficiently many fixed instruments are traded with sufficientliquidity such that discount factors for all relevant maturities are uniquely implied byno-arbitrage is called complete.“

¬ Assume that the fixed income market is free of arbitrage. Then discount factors aredetermined by the following system of equations:

Zij , MVi Cash flows and market value of instrument iTj Arbitrary payment date in the market (independent of i).

CCEFM Doctoral Program, Stefan Pichler

69

¬ Matrix notation: MV = Z] d, MV c I, d c J, Z c I×J, I denotes number of fixed income instruments.

¬ This system of equations has an unique solution iff

S Rank(Z) W J

S Market is arbitrage-free.

¬ Rank(Z) = J is a necessary and sufficient condition for market completeness. There must beat least as many traded instruments as there are distinct payment dates in the market.

CCEFM Doctoral Program, Stefan Pichler

70

Formal proof:

¬ Let x c I denote a trading strategy or portfolio vector. The element xi denotes the notionalprincipal invested in instrument i. Negative elements correspond to a short position in thatinstrument.

¬ Let G(x) = MV´] x denote the price of a trading strategy or portfolio.

¬ A market is called arbitrage-free iff Z´] x W 0 � G(x) = MV´] x W 0.

¬ From Farkas´ lemma we know that MV = Z ] d iff Z´] x W 0 � MV´] x W 0, for a uniqueand nonnegative d c J. QED.

CCEFM Doctoral Program, Stefan Pichler

71

H M(J�1)×J: Hrs �

�1 r�s1 r�s�10 other

.

¬ Farkas´ lemma tells us the conditions for a unique and nonnegative vector of discount factorsd. What about monotonically declining discount factors less or equal to one?

¬ To proof this property we formally introduce the existence of cash positions.

¬ Let E denote the J×J identity matrix, 1 a J×1 vector of ones, 0n a n×1 vector of zeros, and

CCEFM Doctoral Program, Stefan Pichler

72

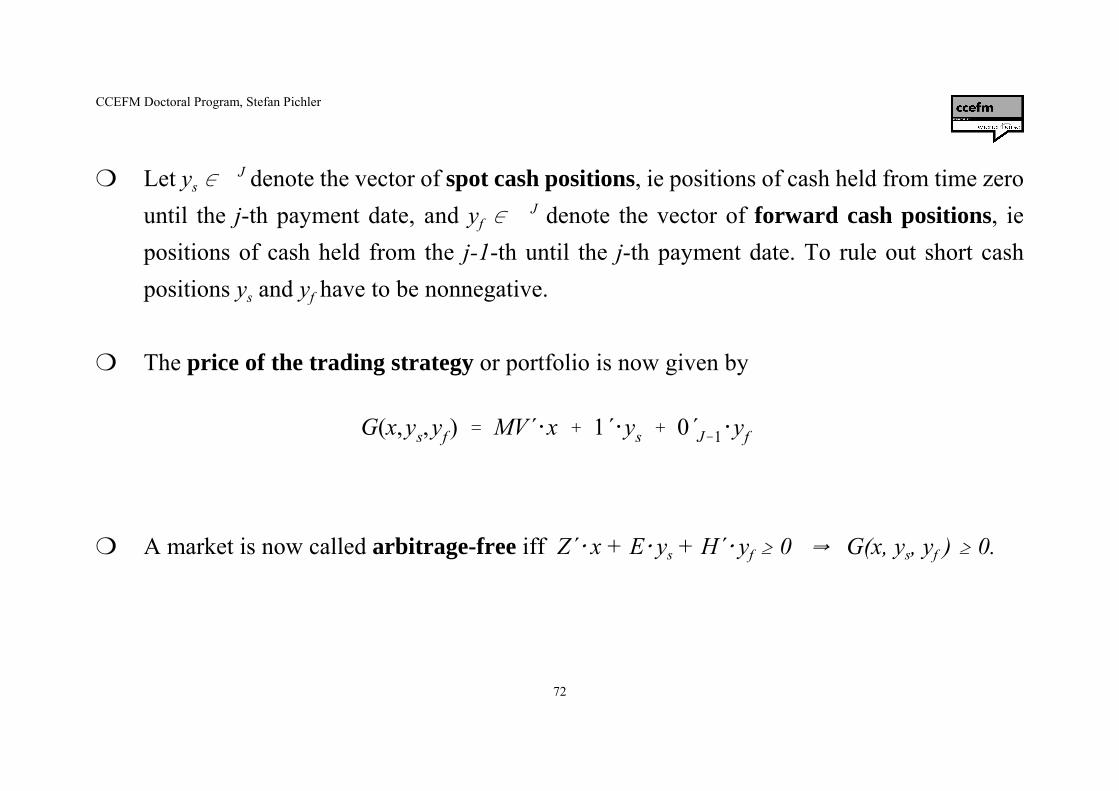

G(x,ys,yf ) � MV´ ]x � 1´ ]ys � 0´J�1 ]yf

¬ Let ys c J denote the vector of spot cash positions, ie positions of cash held from time zerountil the j-th payment date, and yf c J denote the vector of forward cash positions, iepositions of cash held from the j-1-th until the j-th payment date. To rule out short cashpositions ys and yf have to be nonnegative.

¬ The price of the trading strategy or portfolio is now given by

¬ A market is now called arbitrage-free iff Z´] x + E] ys + H´] yf W 0 � G(x, ys, yf ) W 0.

CCEFM Doctoral Program, Stefan Pichler

73

Pr: G(x,ys,yf ) � MV´ ]x � 1´ ]ys � 0´J�1 ]yf i Min!

s. t. Z´ ]x � E ]ys � H´ ]yf W 0J

x MI, ys W 0, yf W 0

Theorem: A market is complete and arbitrage-free in the above definition iff there exists aunique vector of discount factors 0@ d@ 1, with ds@ dr Ð Ts > Tr , which solvesMV = Z] d.

Proof: Consider the following (primal) LP.

(Note that to minimize a price maximizes a possible arbitrage profit.)

CCEFM Doctoral Program, Stefan Pichler

74

Du: Q(d) � 0J´ ]d i Max!

s. t. Z ]d � MV, E ]d V 1, H ]d V 0J�1

d W 0

The dual program is

Implication: The set of solutions of Pr is bounded by the absence of arbitrage and non-empty (x = 0, ys = 0, yf = 0 is a trivial solution). Hence Pr possesses anoptimal solution and so does Du. Therefore, there exists at least one d whichsolves Z] d = MV (equality in Du) and for which 0@ d@ 1 (first inequality inDu) and ds@ dr Ð Ts > Tr (second inequality in Du). Since Rank(Z) = J(completeness), d is unique.

CCEFM Doctoral Program, Stefan Pichler

75

Reverse: The existence of a unique vector d with 0@ d@ 1 and ds@ dr Ð Ts > Tr impliesthe existence of a unique solution of Du. Since d is unique Q*(d) W 0 is theoptimal solution to Du. Finally, duality implies that Pr also possesses anoptimal solution G*(x, ys, yf ) W 0. QED.

¬ Market completeness is crucial for the uniqueness of d. In incomplete markets the arbitrage-free discount function is not unique.

¬ Note that the primal LP is also useful to detect arbitrage opportunities in real markets.

CCEFM Doctoral Program, Stefan Pichler

76

S1 ]P1 � P1 � 1

¬ In a complete and arbitrage-free market the term structure of interest rates is „estimated“ bysimple matrix inversion.

¬ Usually, instruments with standardized coupon dates (eg, Treasury bonds, IRS) are used asan input. Use of IRS leads to a simple recursive „bootstrapping“ algorithm.

¬ Let Si , i = 1, 2, ...., N denote quoted swap rates for consecutive maturities. Then the follwoingalgorithm yields the discount factors for those maturities:

Step 1: Determine P1 using S1.

CCEFM Doctoral Program, Stefan Pichler

77

S2 ]P1 � S2 ]P2 � 100 ]P2 � 100

P2 �

100 � S2 ]P1

100 � S2

Pn �

100 � Sn ]ˆn�1

i�1Pi

100 � Sn

Step 2: Determine P2 using P1 and S2.

and

Genral recursive formula for Pn:

CCEFM Doctoral Program, Stefan Pichler

78

P2 �100 � 5.35 ]0.94841

105.35� 0.90105, R2 � 5.348%

P3 �100 � 5.27 ] (0.94841 � 0.90105)

105.27� 0.85735, R3 � 5.264%

Example: The following swap rates are quoted in a market: 1Y-5.44, 2Y-5.35, 3Y-5.27.

Discount factors: P1 �100

105.44� 0.94841, R1 � 5.440%

CCEFM Doctoral Program, Stefan Pichler

79

MV � Z ]d � …, … MI

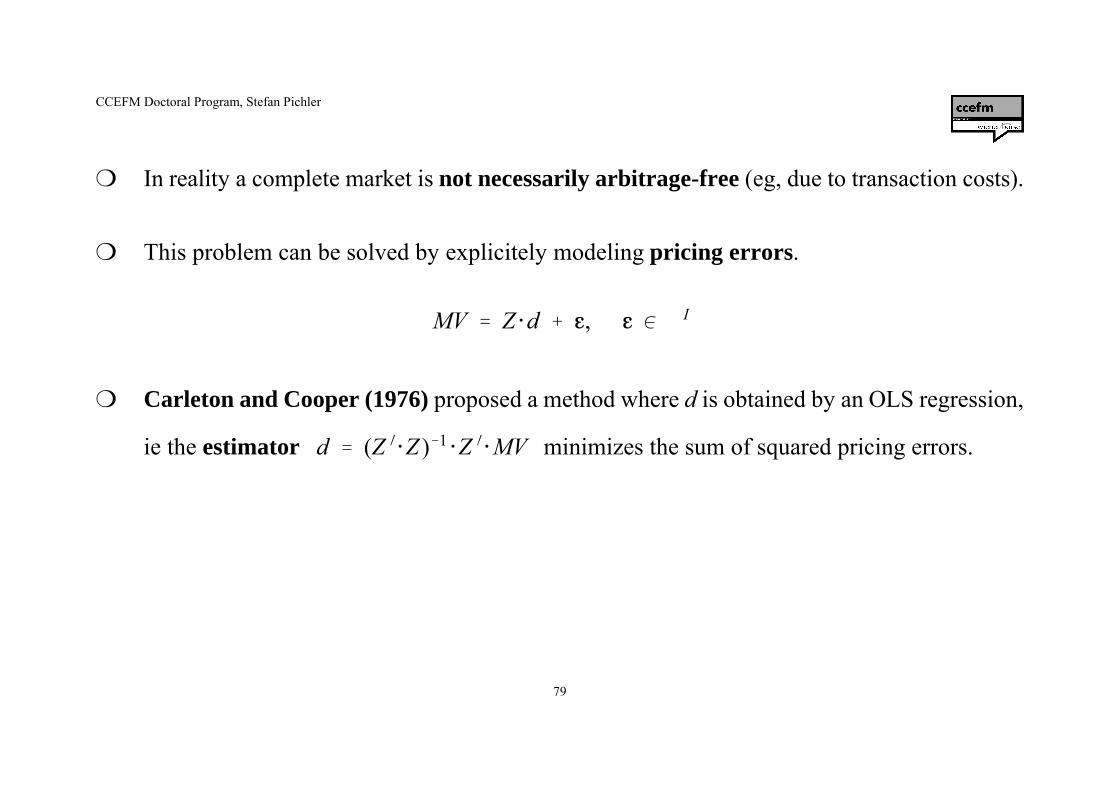

¬ In reality a complete market is not necessarily arbitrage-free (eg, due to transaction costs).

¬ This problem can be solved by explicitely modeling pricing errors.

¬ Carleton and Cooper (1976) proposed a method where d is obtained by an OLS regression,

ie the estimator minimizes the sum of squared pricing errors.d � (Z �]Z )�1

]Z �]MV

CCEFM Doctoral Program, Stefan Pichler

80

dj � ˆK

k�0ak ] fk (Tj)

¬ If the market is incomplete missing information has to be substituted by additionalassumptions.

¬ Most frequently, a specific functional form for either the discount function or the zero-rate-curve (in some cases the forward rate curve) is assumed.

¬ In the simplest case the discount function is then again obtained by OLS.

¬ Let the discount factors dj be defined as linear combinations of K+1 component functions(eg, polynomials, splines) fk (T).

CCEFM Doctoral Program, Stefan Pichler

81

MVi � ˆJ

j�1Zij ]ˆ

K

k�0ak ] fk (Tij) � ˆ

K

k�0ak ]ˆ

J

j�1Zij ] fk (Tij) � ˆ

K

k�0ak ]Xik

¬ Substitution for dj in the pricing equation yields

¬ The elements of the auxiliary matrix X can easily be calculated. The coefficients ak areobtained by OLS.

¬ Most popular are methods using cubic splines (McCulloch (1971, 1975), B-splines(Langetieg and Smoot (1989), Steeley (1991), or extended Laguerre functionals (Nelsonand Siegel (1987), Svensson (1997)). These methods, however, do not guarantee nonnegativediscount factors.

CCEFM Doctoral Program, Stefan Pichler

82

fk (T) � ˆK�k

r�0(�1)r�1

]K�k

r ]T k�r

k � rÐ k � 1, .... ,KÐ 0 V T V 1

¬ Schaefer (1981) proposed a method based on Bernstein polynomials which overcomes thisdrawback.

¬ For all 0 @ T @ 1 the component functions are defined as f0(T) = 1 and

¬ Bernstein polynomials are monotonically decreasing in T. To ensure that the discountfunction is also monotonically decreasing the linear restriction ak W 0 must hold. To ensure

that 0 @ dj @ 1 the linear restrictions a0 = 1 and must hold. ˆK

k�0ak ] fk (1) W 0

CCEFM Doctoral Program, Stefan Pichler

83

¬ Maturities are standardized by dividing all maturities by the maximum maturity in the market.

¬ Minimization of pricing errors is done by an all-purpose nonlinear optimization routine orby a standard quadratic programming algorithm.

¬ Degree of polynomial typically is set to K=5 or K=7, respectively.

CCEFM Doctoral Program, Stefan Pichler

84

¬ Choice of estimation procedure might be important.

¬ Mean absolute pricing error (MAE) measures quality of procedure.

¬ MAE is expected to be of the size of the average bid/ask spread.

¬ Choice of data input is more important.

¬ MAE is below five to ten basis points when liquid instruments (eg, benchmark bonds) areused. MAE might be up to 30-40 basis points when illiquid instruments are included.

¬ Size of bid/ask spread, validity of quotes, and time accuracy are crucial criteria.

CCEFM Doctoral Program, Stefan Pichler

85

Example: Quotes of German Benchmark Bunds are used as input. Estimate the discountfunction using cubic splines (knots at 4Y, 7Y, 10Y) and Schaefer (K=5). Calculatepricing errors and compare the results.

Coupon Maturity QuoteBund 2Y 5.000 13.09.02 99.80Bund 3Y 3.750 26.08.03 96.38Bund 4Y 4.125 27.08.04 96.43Bund 5Y 5.000 19.08.05 99.51Bund 6Y 6.250 26.04.06 104.71Bund 7Y 6.000 04.07.07 103.99Bund 8Y 4.125 04.07.08 92.67Bund 9Y 4.500 04.07.09 94.53

Bund 10Y 5.250 04.07.10 99.76

CCEFM Doctoral Program, Stefan Pichler

86

4.95

5.00

5.05

5.10

5.15

5.20

5.25

5.30

5.35

1 2 3 4 5 6 7 8 9 10

SchaeferSplines

Estimated term structures:

CCEFM Doctoral Program, Stefan Pichler

87

Model prices and pricing errors:

Benchmark Market Value Splines AE in bp Schaefer AE in bp2Y 99.96 99.94 2.0 99.97 0.23Y 96.69 96.74 5.7 96.65 3.44Y 96.75 96.89 14.2 96.72 3.15Y 100.00 99.78 22.8 99.65 35.76Y 107.30 107.47 17.6 107.41 11.87Y 105.34 105.38 4.0 105.41 7.68Y 93.59 93.59 0.8 93.59 0.09Y 95.53 95.56 2.8 95.47 6.1

10Y 100.93 100.95 2.8 100.93 0.4MAE 8.1 7.6

CCEFM Doctoral Program, Stefan Pichler

88

6 Financial Futures

¬ Financial futures are exchange traded forward contracts where temporary profits and lossesare settled on a daily basis (daily settlement).

¬ At the initiation of the contract a party (buyer or seller) has to transfer a margin (5-10% ofcontract volume) to a margin account. This account is used by the exchange or clearinghouse for settlement.

¬ At maturity of the contract the underlying has to be delivered physically (physical delivery)or cash settlement takes place.

CCEFM Doctoral Program, Stefan Pichler

89

¬ The most important underlyings for financial futures are money market deposits,government bonds, stock indices, and currencies.

Turnover in millions of contracts

Exchange Country 1998 1999

EUREX GER, CH 248.2 379.2

CBOT USA 281.2 254.6

CME USA 226.6 200.7

MATIF FRA 103.8 185.6

LIFFE UK 186.6 119.9

NYMEX USA 95.0 109.5

The most important futures exchanges by the end of 1999.

CCEFM Doctoral Program, Stefan Pichler

90

EDSP �� F �

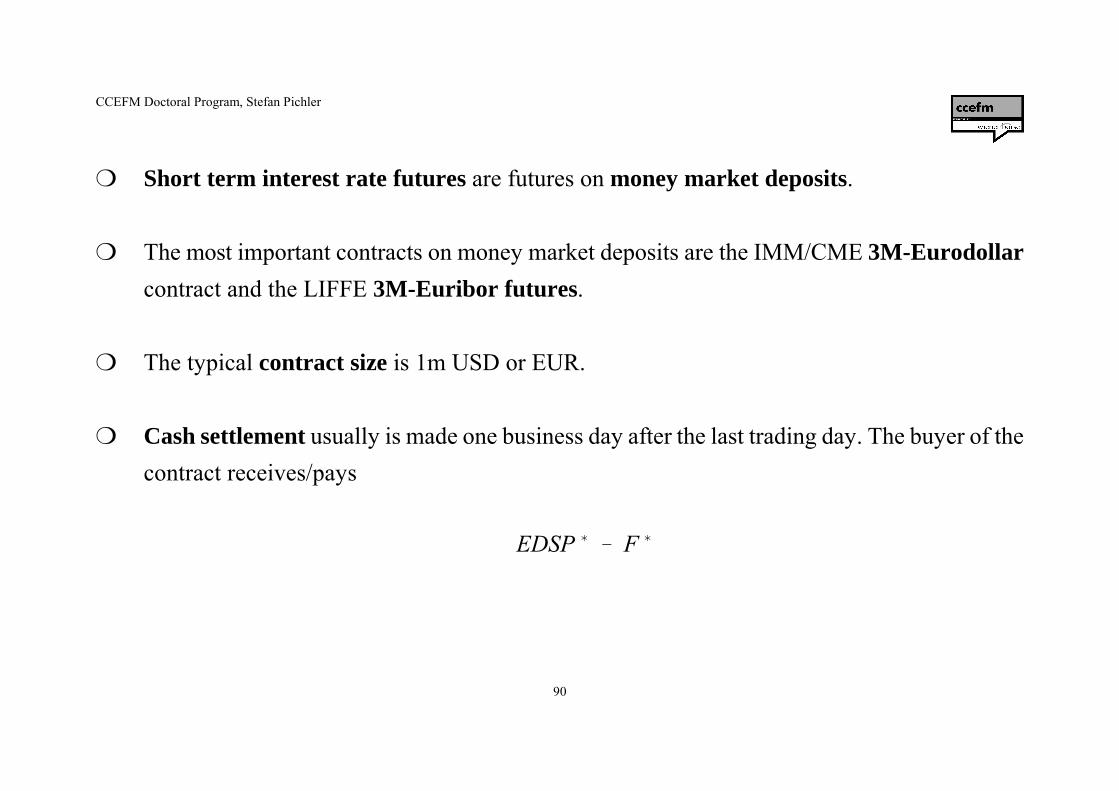

¬ Short term interest rate futures are futures on money market deposits.

¬ The most important contracts on money market deposits are the IMM/CME 3M-Eurodollarcontract and the LIFFE 3M-Euribor futures.

¬ The typical contract size is 1m USD or EUR.

¬ Cash settlement usually is made one business day after the last trading day. The buyer of thecontract receives/pays

CCEFM Doctoral Program, Stefan Pichler

91

EDSP ��

contract size100

] 100 � h ] (100 � EDSP)

F ��

contract size100

] 100 � h ] (100 � F)

¬ EDSP denotes the exchange delivery settlement price, which is determined by the exchangethrough the simple relation EDSP = 100 - Libor/Euribor.

¬ EDSP* denotes the EDSP contract value and is calculated by

¬ F* denotes the futures contract value based on the closing price and is calculated by

where F denotes the quoted futures price.

CCEFM Doctoral Program, Stefan Pichler

92

¬ Since the daycount fraction h is approximately equal to 0.25, one tick (basis point) is worth 25USD or EUR.

Example: The 3M-Eurodollar contract closes at 93.295. On the following business day the3M-Libor rate is at 8%. Determine the amount the buyer has to pay the sellerassuming h=0.25.

EDSP = 100 - 8 = 92 EDSP* = 10,000] (100 - 0.25] (100 - 92)) = 980,000.00F = 93.295 F* = 10,000] (100 - 0.25] (100 - 93.295)) = 983,237.50Payment: 3,237.50 USD

Note, that F corresponds to a 3M-rate of 6.705%. In analogy to zerobonds the buyer suffers a losswith rising interest rates.

CCEFM Doctoral Program, Stefan Pichler

93

0.25 ] 0.06705 � 0.081 � 0.25 ]0.08

]1m � USD 3,174.02

¬ A long position in a short term interest futures corresponds approximately to a shortposition in a FRA.

¬ The loss of the corresponding FRA position would be

¬ Due to the linear compounding assumption used by the exchanges there is a small differencebetween positions in FRAs and short term interest rate futures. This difference is determinedby the relation Futures-amount = FRA-amount] (1 + h]Libor), ie in the futures markets thedifference in interest rates is paid without discounting.

CCEFM Doctoral Program, Stefan Pichler

94

¬ Long term interest rate futures are contracts on government bonds.

¬ The most important contracts on government bonds are the EUREX Euro Bund Futurescontract and the CBOT US-Treasury Bond Futures (followed by their medium-term andshort-term counterparts).

¬ The underlying is a synthetic coupon bond with a certain maturity and a given notionalprincipal per contract (typically 100,000 USD or EUR).

¬ To settle a contract (physical delivery) the seller has the right to choose a bond to deliverout of a prespecified set of deliverable bonds.

CCEFM Doctoral Program, Stefan Pichler

95

Contract Deliverable Bonds

Euro Bund FuturesEuro Bobl Futures

Euro Schatz FuturesUS Treasury Bond Futures

10Y-US Treasury Note Futures5Y-US Treasury Note Futures2Y-US Treasury Note Futures

8.5Y-10.5Y German Bunds4.5Y-5.5Y German Bunds1.75-2.25 German BundsA15Y Treasury Bonds

6.5Y-10Y Treasury Notes4.25Y-5.25Y Treasury Notes

1.75Y-2Y Treasury Notes

Deliverable bonds for several government bond futures.

¬ Differences between the present values of the synthetic underlying and the market values ofthe deliverable bonds are partly balanced by exchange determined conversion factors.

CCEFM Doctoral Program, Stefan Pichler

96

¬ Conversion factors are calculated as the ratio of the present value of the deliverable bondand the synthetic bond under a specific term structure, which is set by the exchange.

¬ Exchanges use a hypothetic flat term structure which makes the present value of thesynthetic bond equal to 100%, ie 6% at EUREX, 7% at CBOT.

¬ Since conversion factors do not totally equalize differences in present values betweendeliverable bonds, there exists one bond which is cheapest-to-deliver (CTD) seen from theview of the short position.

¬ The seller (short position) has the right to choose the CTD bond (delivery option). CurrentCTD bond is seen as ‚underlying‘ by market participants.

CCEFM Doctoral Program, Stefan Pichler

97

¬ The seller receives in exchange for delivering the CTD bond the invoice amount.

Invoice amount = EDSP ] notional principal] conversion factor + accrued interest(CTD)

¬ The exchange delivery settlement price (EDSP) is the volume-weighted average of the last(eg, last ten trades, last minute of trading) futures prices of the last trading day.

¬ The seller maximizes invoice amount - price(CTD) incl. accrued interest. This equivalent tochoosing the bond with minimal ratio price / conversion factor.

CCEFM Doctoral Program, Stefan Pichler

98

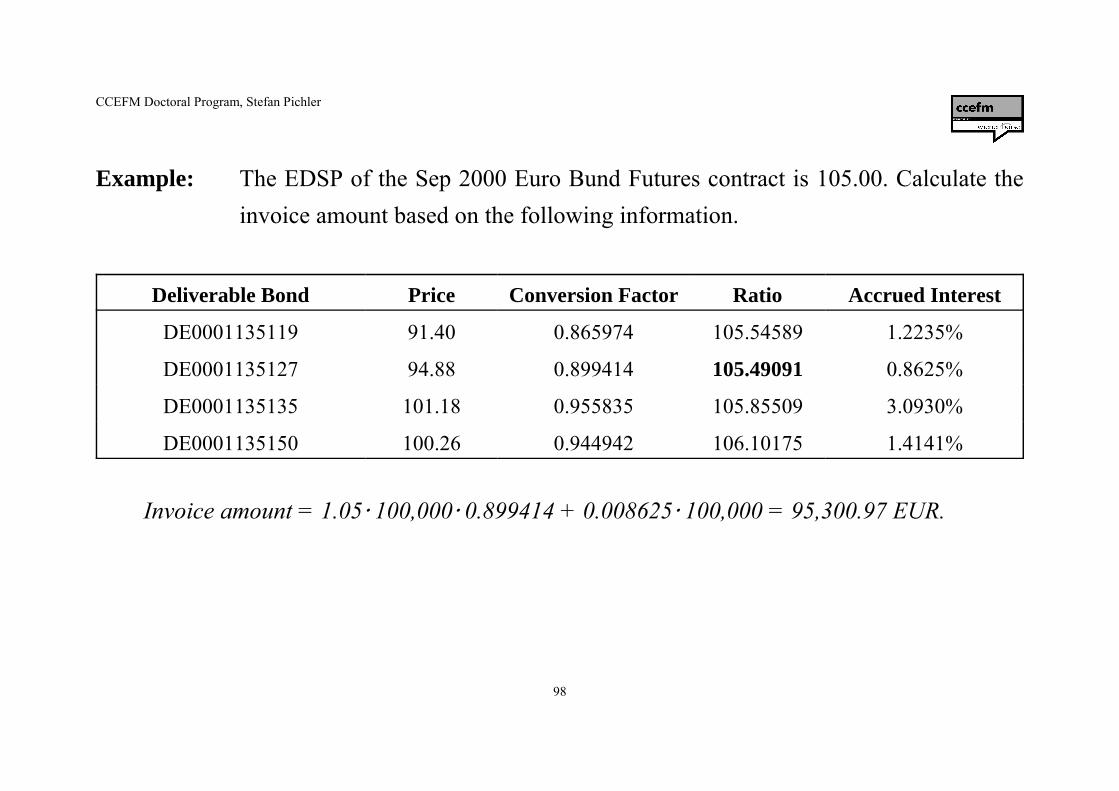

Example: The EDSP of the Sep 2000 Euro Bund Futures contract is 105.00. Calculate theinvoice amount based on the following information.

Deliverable Bond Price Conversion Factor Ratio Accrued Interest

DE0001135119 91.40 0.865974 105.54589 1.2235%

DE0001135127 94.88 0.899414 105.49091 0.8625%

DE0001135135 101.18 0.955835 105.85509 3.0930%

DE0001135150 100.26 0.944942 106.10175 1.4141%

Invoice amount = 1.05] 100,000] 0.899414 + 0.008625] 100,000 = 95,300.97 EUR.

CCEFM Doctoral Program, Stefan Pichler

99

¬ Stock index futures are contracts on stock portfolios represented by stock indices.

¬ The most important index futures contracts are the S&P 500 contract (CME), the CAC 40contract (MATIF), the DAX contract (EUREX), and the FTSE 100 contract (LIFFE).

¬ The underlying is a synthetic position in the index portfolio with a fixed value of one indexpoint (eg, USD 250 for the S&P 500 contract).

¬ For stock index futures contracts cash settlement takes place.

CCEFM Doctoral Program, Stefan Pichler

100

¬ For pricing and hedging purposes the underlying indices have to be replicable.

¬ Only capital weighted indices are replicable. Note, that the DJIA is not replicable.

¬ Most indices do not take dividends into account. Therefore, the index portfolio outperformsthe index. Transaction costs might outweigh this effect.

¬ Performance indices (eg, DAX) take dividends into account. However, in the case of theDAX, the hypothetical reinvestment of dividends is based on a questionable assumption.

CCEFM Doctoral Program, Stefan Pichler

101

7 Options

¬ Options are financial contracts which give one party the right but not the obligation to dosomething.

¬ The buyer of the option possesses the right, the seller (writer) of the contract is obliged tofulfill the terms of the contract.

¬ The buyer pays the seller the price of the option (option premium). Her risk is limited by thesize of the premium.

¬ The writer receives the premium. Her risk depends on the terms of the contract and is perhapsunlimited.

CCEFM Doctoral Program, Stefan Pichler

102

¬ Usually, options give the right to buy (call options) or sell (put options) an underlyingfinancial instrument at prespecified terms some time in the future.

Summary of important underlyings for option markets:

Underlying Currency Fixed Income Instrument Equity Other

FX (OTC)FX (exchange)FX futures

Money market futuresLibor rates (Caps)Swaps (Swaptions)Bond futuresIndividual bonds

Stock indicesStock index futuresIndividual stocks

Commodity futuresCommoditiesInsurance typeinstruments

(Ordered by estimated importance).

CCEFM Doctoral Program, Stefan Pichler

103

¬ Options are either traded individually (on exchanges or OTC) or embedded in otherfinancial instruments (Callable bonds/swaps, convertibles, capped FRNs, etc).

¬ For many contracts the buyer of the option has to exercise her right physically (physicaldelivery). In some cases only a cash settlement takes place.

¬ Options (like other derivatives) are described by their payoff function.

¬ Exact knowledge of the payoff is essential for valuation. Legal terms are very importantespecially for exotics and structured instruments.

CCEFM Doctoral Program, Stefan Pichler

104

CT � ST � K

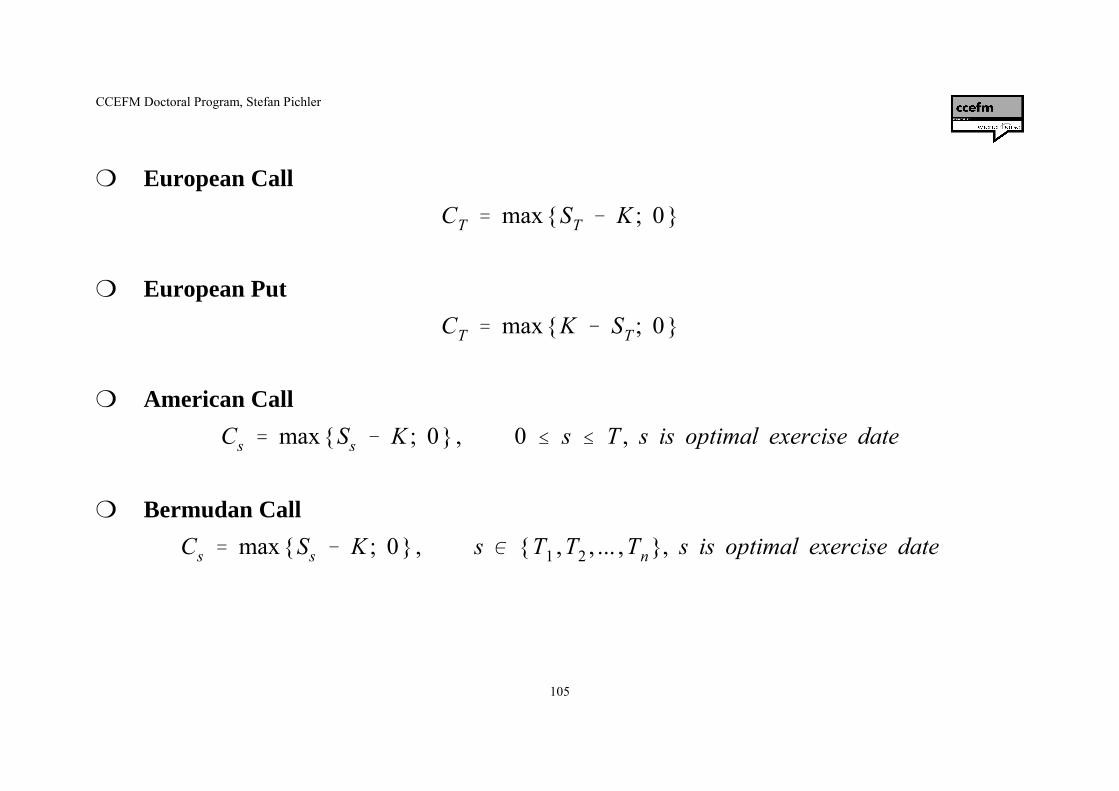

« Some important payoff functions:

Notation: St value of underlying at time tCt option value at time t t=0 valuation datet=T maturity of options payment date (if not equal to T)K, H constants known at initiation of the contract (strike/exercise price,

barrier)

¬ Forward (of course not an option)

CCEFM Doctoral Program, Stefan Pichler

105

CT � max{ST � K ; 0}

CT � max{K � ST ; 0}

Cs � max{Ss � K ; 0} , 0 V s V T , s is optimal exercise date

Cs � max{Ss � K ; 0} , s M {T1 ,T2 , ... ,Tn }, s is optimal exercise date

¬ European Call

¬ European Put

¬ American Call

¬ Bermudan Call

CCEFM Doctoral Program, Stefan Pichler

106

Type Strike Expiry Last Date/Time Bid Ask High Low Open Interest Volume C 1180 20.10.2000 10.50 22.09.2000 17:12 9.00 10.00 10.50 10.50 740 20

Market information from Wiener Börse on Sep 22, 2000. European options on ATX.

Example: Bank A buys 20 contracts from bank B. What happens on Sep 22 and on Oct 20?

Sep 22: One contract is good for five ATX points. Thus, bank A has to pay a premium of20]5]10.50 = 1,050 EUR.

Oct 20: Assume the ATX is 1,320. Cash settlement takes place and bank A receives20]5](1,320 - 1,180) = 14,000 EUR from bank B. If the ATX is below 1,180, bankA will receive nothing.

CCEFM Doctoral Program, Stefan Pichler

107

CT � max{Saverage � K ; 0}

CT � max{ST � Saverage ; 0}

CT � 1St > H ]max{ST � K ; 0} , 0 V t V T

CT � 1St A H ]max{K � ST ; 0}, 0 V t V T

Some exotics:

¬ Asian Call

¬ Average Strike Call

¬ Down-and-out Call

¬ Up-and-in Put

CCEFM Doctoral Program, Stefan Pichler

108

CT � max{ST � K ; 0} � K ]ST ]max 1K

�1ST

; 0

¬ FX-Option (European call as an example)

ST is the time T price of one unit target currency expressed in units of reference currency. Thestrike price K is also expressed in units of reference currency. Note, that in the USD/EUR optionmarket USD is the reference currency!

Using the fact that 1/ST is the time T price of one unit of reference currency expressed in units oftarget currency we can deduce that a call on one unit of target currency with strike price K isequivalent to K puts on one unit of reference currency with strike price 1/K.

CCEFM Doctoral Program, Stefan Pichler

109

CT � min(ST ;K ) � ST � max(ST � K ;0) � ST � CapletT

CapletT � max(PT�h � PT � K ;0 )

CapletT � maxPT�h � PT

PT

� K ;0 � max h ] f (T�h ,T) � K ;0

¬ Caplet

ST denotes the index rate reset at date T-h and K is the strike rate. Substituting ST = PT-h - PT yields

Using the fact that the forward price of an asset equals its spot price at maturity yields

CCEFM Doctoral Program, Stefan Pichler

110

PST � max PV(Float) � PV(Fix) ; 0 � max 1 � P(T,T�N) � K ]HT(T,N) ; 0 �

� HT(T,N) ]max P(T,T) � P(T,T�N)HT(T,N)

� K; 0 � HT(T,N) ]max FSRT � K; 0

¬ Payer Swaption (with strike rate K)

A payer swaption, which gives the right to enter a payer swap, can be seen as a call on theforward swap rate, a receiver swaption, which gives the right to enter a receiver swap, can beseen as a put on the forward swap rate.

CCEFM Doctoral Program, Stefan Pichler

111

¬ Put-Call Parity

It is possible to replicate a European call by a portfolio consisting of long positions in theunderlying and a European put (with identical strike price and maturity) and a short position ina money market deposit.

Position Heute S @@@@ K S > K

long call - call 0 S - K

long underlying - S + S + S

long put - put K - S 0

short money market deposit + PT]K - K - K

¬ call + deposit = underlying + put

CCEFM Doctoral Program, Stefan Pichler

112

8 A First Look at the Fundamental Theorem of Asset Pricing

¬ The Fundamental Theorem of Asset Pricing is the most important tool for pricing financialinstruments.

¬ The theorem delivers a general valuation formula for all financial instruments based on theno-arbitrage assumption.

¬ This chapter provides an intuitive introduction and not a mathematical derivation.

CCEFM Doctoral Program, Stefan Pichler

113

Fundamental Theorem of Asset Pricing

¬ The prices of all financial instruments traded in a market free of arbitrage are determined bytheir expected payoffs under a certain probability measure.

¬ Under this probability measure all relative price processes are martingales.

¬ If the market is complete, this measure is unique.

CCEFM Doctoral Program, Stefan Pichler

114

E(ST) � pS upT � (1 � p)S down

T

S upT � 110 , S down

T � 100 , p � 0.7 v E (ST) � 0.7 ]110 � 0.3 ]100 � 107

What does that mean?

¬ A probability measure describes the probability law under which the expected value iscalculated.

Example: In the Cox-Ross-Rubinstein binomial model p denotes the probability of an up-move, (1 - p) is the probability of a down-move. The expected value is given by

CCEFM Doctoral Program, Stefan Pichler

115

S̃t �St

Bt

S̃t �St

Pt (T)

¬ A relative price process describes the value of a certain financial instrument relative to thevalue of a ‚basis‘ asset (numeraire). The pricing of derivatives is based on the replication bya position in the underlying combined with a position in the numeraire.

Examples: The continuously compounded money market deposit with time t value Bt is usedas the numeraire. The relative price of an asset with current price St is then given by

A zerobond with maturity T and price Pt(T) is used as the numeriare. The relativeprice of the asset is then

CCEFM Doctoral Program, Stefan Pichler

116

EPST

BT

�SB

� EPST

BT

�1001

� 0.5 1401.1

� 0.5 901.1

� 100 � 4.55

EQST

BT

�SB

� EQST

BT

�1001

� 0.4 1401.1

� 0.6 901.1

� 100 � 0

¬ A (relative) price process is a martingale, if its expected changes are zero.

Example: Asset: S = 100 Sup = 140 Sdown = 90Deposit (R = 10%): B = 1 Bup = Bdown = 1.1

For the probability measures P: p = 0.5 und Q: p = 0.4 the expected changes are given by

CCEFM Doctoral Program, Stefan Pichler

117

EQ�ST

PT

�SP

� EQ�ST

PT

�100

0.8264� 0.3787 140

0.9259� 0.6213 90

0.8772� 121 � 0

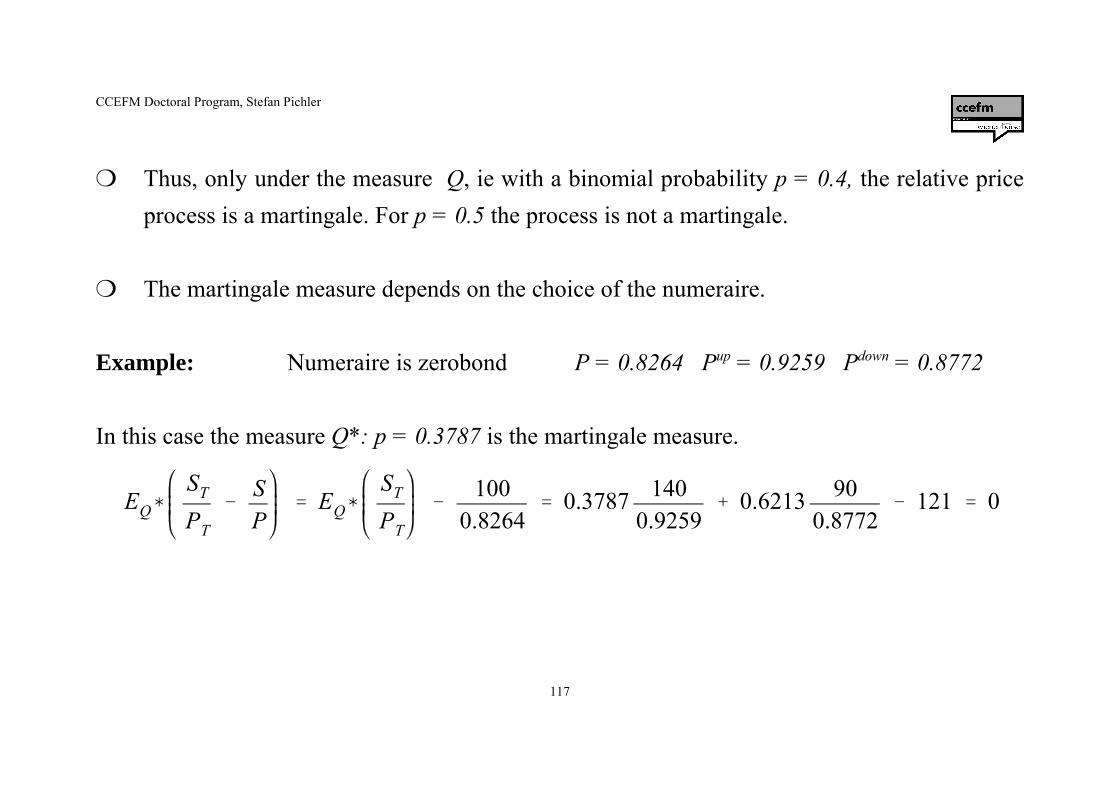

¬ Thus, only under the measure Q, ie with a binomial probability p = 0.4, the relative priceprocess is a martingale. For p = 0.5 the process is not a martingale.

¬ The martingale measure depends on the choice of the numeraire.

Example: Numeraire is zerobond P = 0.8264 Pup = 0.9259 Pdown = 0.8772

In this case the measure Q*: p = 0.3787 is the martingale measure.

CCEFM Doctoral Program, Stefan Pichler

118

¬ A market is complete if all financial instruments are replicable. In the binomial model this isthe case.

Example:

Instrument Price State 1 State 2

Deposit 1 1.1 1.1

Asset 100 140 90

Call 30 0

European Call with exercise price K = 110.

CCEFM Doctoral Program, Stefan Pichler

119

Action t=0 S = 140 S = 90

buy call - C 30 0

buy H assets - 100H + 140H + 90H

‚sell‘ G deposits = money market loan + G - 1.1G - 1.1G

An exact replication implies the following:

(1) 140H - 1.1G = 30 sowie (2) 90H - 1.1G = 0

Solution: H = 0.6 G = 49.09

CCEFM Doctoral Program, Stefan Pichler

120

Action t=0 S = 140 S = 90

buy call - C 30 0

buy 0.6 assets - 60 + 84 + 54

sell deposit with 49.09 + 49.09 - 54 - 54

Total - 10.91 30 0

The price of the replicating portfolio is 10.91. This is the arbitrage-free price of the call option. Forthe determination of the arbitrage-free price the knowledge of the actual or empirical probabilitiesof state 1 and state 2 is not necessary!

General formula for the hedge ratio H in the binomial model:

CCEFM Doctoral Program, Stefan Pichler

121

H �C̃ up

� C̃ down

S̃ up� S̃ down

�

301.1

� 0

1401.1

�901.1

� 0.6

H �∆C∆S

adCdS

� δ v ∆C a δ ]∆S

First interpretation of hedge ratio as delta of the option:

CCEFM Doctoral Program, Stefan Pichler

122

C � H ]S � G ]B � 0.6 ]100 � 49.09 ]1 � 10.91

G �S down

B downT

]H �C down

B downT

�90 ]0.6

1.1� 0 � 49.09

General formula for the price of the call:

General formula for the size of the money market position G:

CCEFM Doctoral Program, Stefan Pichler

123

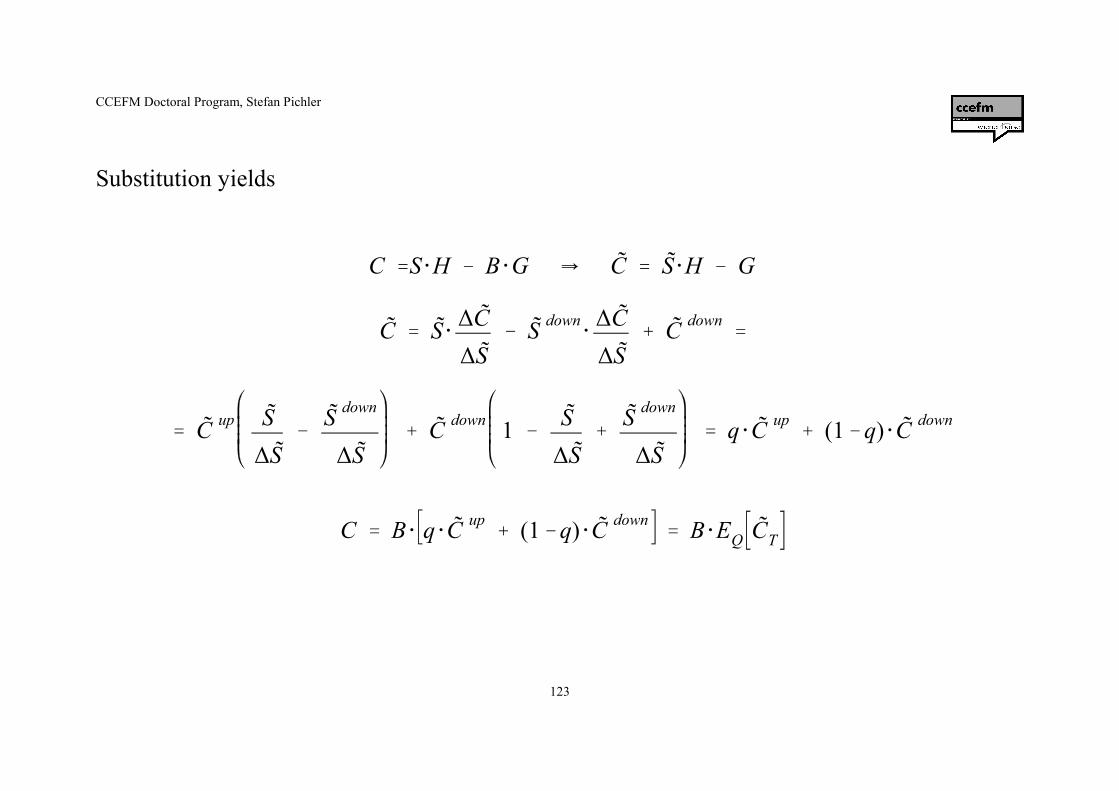

C �S ]H � B ]G v C̃ � S̃ ]H � G

C̃ � S̃ ] ∆C̃∆S̃

� S̃ down]∆C̃∆S̃

� C̃ down�

� C̃ up S̃∆S̃

�S̃ down

∆S̃� C̃ down 1 �

S̃∆S̃

�S̃ down

∆S̃� q ] C̃ up

� (1�q) ] C̃ down

C � B ] q ] C̃ up� (1�q) ] C̃ down

� B ]EQ C̃T

Substitution yields

CCEFM Doctoral Program, Stefan Pichler

124

C � B ] q ] C̃ up� (1�q) ] C̃ down

� 1 ] q ] C up

1�R� (1�q) ] C down

1�R�

�q ]C up

� (1�q) ]C down

1�R�

EQ CT

1�R

q �S̃ � S̃ down

S̃ up� S̃ down

�

1001

�901.1

1401.1

�901.1

� 0.4

If a deposit with interest rate R is used as the numeraire, this expression can be simplified to

General formula for the binomial probability q:

CCEFM Doctoral Program, Stefan Pichler

125

This probability is exactly the martingale probability!

¬ The valuation of a financial instruments by construction of a replicating portfolio impliesthat the relative price of the instrument equals the expected relative price at expiry.

¬ If a money market deposit is used as the numeraire, the arbitrage-free value of theinstrument equals the discounted expected payoff.

CCEFM Doctoral Program, Stefan Pichler

126

EQ S̃T� S̃ � S̃ up S̃ � S̃ down

S̃ up� S̃ down

� S̃ down 1 �S̃ � S̃ down

S̃ up� S̃ down

� S̃ �

�1

S̃ up� S̃ down

] S̃ up S̃� S̃ up S̃ down� S̃ up S̃ down

� S̃ down S̃ down� S̃ down S̃� S̃ down S̃ down

� S̃ up S̃� S̃ down S̃ � 0

¬ Only the use of martingale probabilities for taking the expectation yields the arbitrage-freevalue.

CCEFM Doctoral Program, Stefan Pichler

127

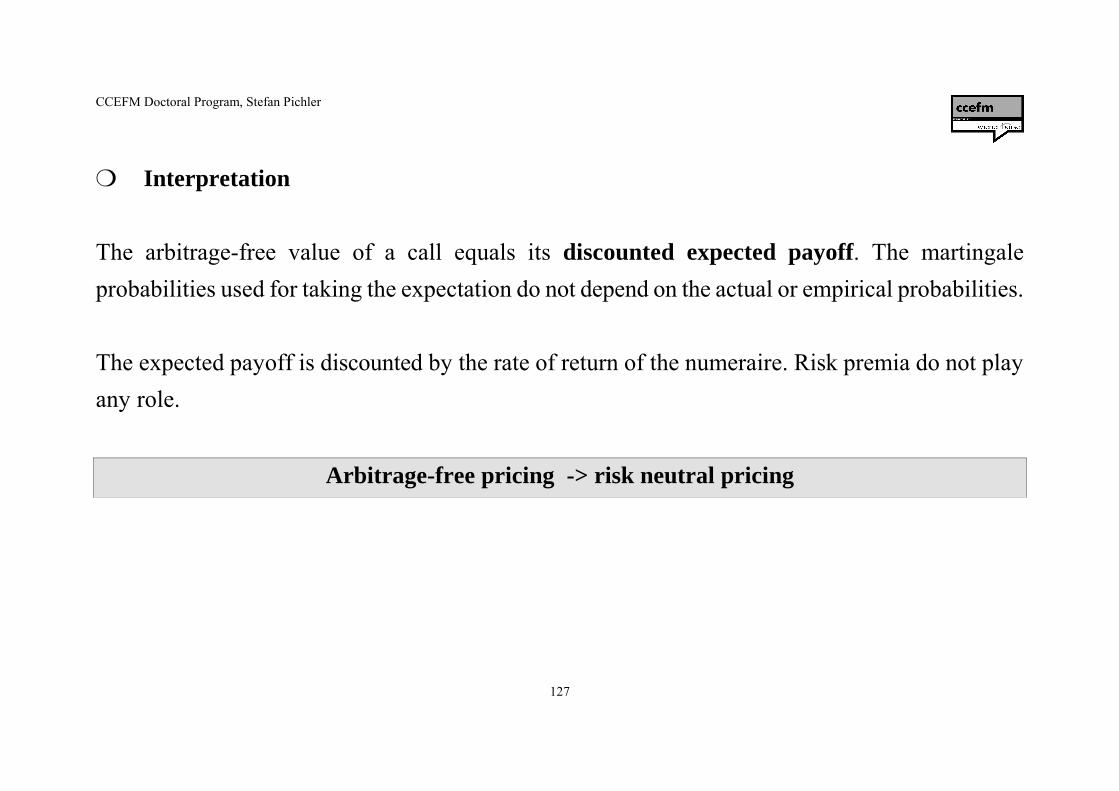

¬ Interpretation

The arbitrage-free value of a call equals its discounted expected payoff. The martingaleprobabilities used for taking the expectation do not depend on the actual or empirical probabilities.

The expected payoff is discounted by the rate of return of the numeraire. Risk premia do not playany role.

Arbitrage-free pricing -> risk neutral pricing

CCEFM Doctoral Program, Stefan Pichler

128

¬ The price of a financial instrument is independent of risk preferences which might beincorporated in risk premia.

¬ The price of a financial instrument is independent of empirical probabilities.

¬ In a risk neutral world the expected return of all assets is identical to the return of thenumeraire.

¬ This is exactly the case if all relative price processes are martingales.

CCEFM Doctoral Program, Stefan Pichler

129

risk neutrality: E ∆SS

� E ∆BB

E ST � S �SB

E BT � B

E ST �SB

E BT

EST

BT

�SB

v martingale property

Assume that S and B are independent.

CCEFM Doctoral Program, Stefan Pichler

130

EQST

BT

�SB

v S � B ]EQST

BT

¬ General valuation principle

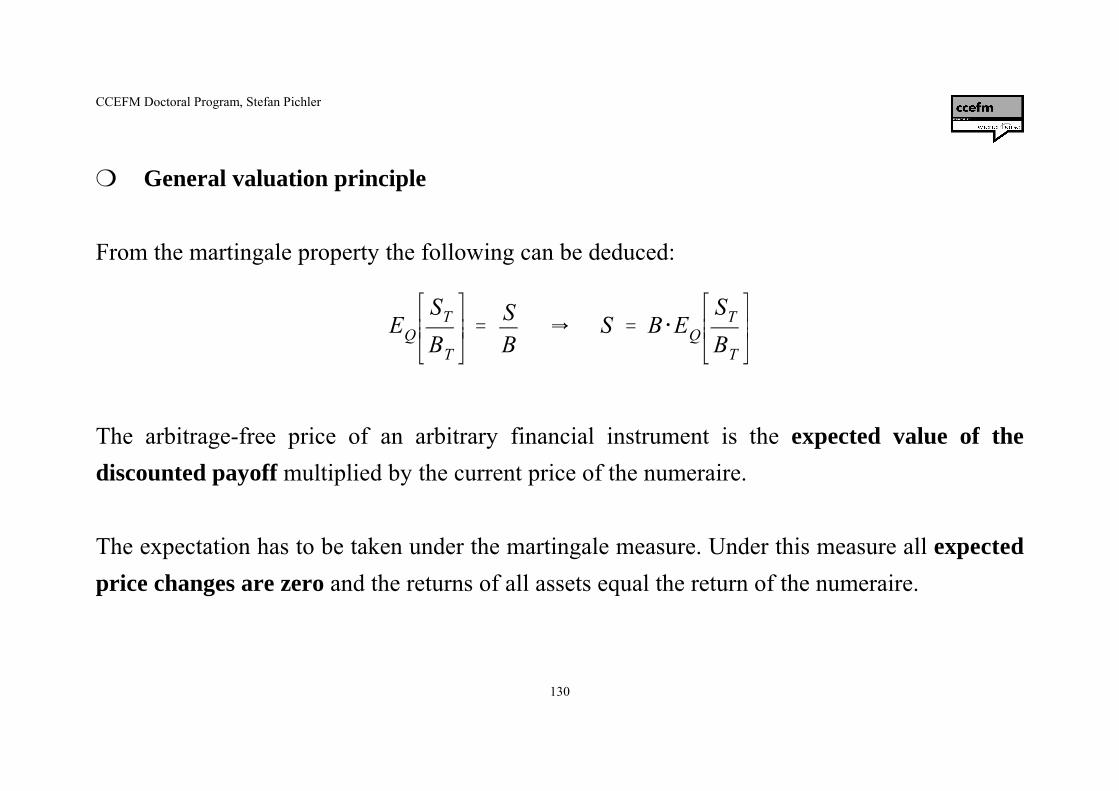

From the martingale property the following can be deduced:

The arbitrage-free price of an arbitrary financial instrument is the expected value of thediscounted payoff multiplied by the current price of the numeraire.

The expectation has to be taken under the martingale measure. Under this measure all expectedprice changes are zero and the returns of all assets equal the return of the numeraire.

CCEFM Doctoral Program, Stefan Pichler

131

S � B ]EQST

BT

v S � EQST

1 � R

¬ Valuation with stochastic interest rates

Money market deposit as numeraire

Note, that 1+R is now a random variable. Taking expectations of the ratio might be inconvenient(Vasicek, Cox-Ingersoll-Ross).

Frequently, R is assumed to be constant (Black-Scholes, Cox-Ross-Rubinstein, Rubinstein-Reiner). For interest rate and FX derivatives this assumption is questionable.

CCEFM Doctoral Program, Stefan Pichler

132

S � B ]EQST

BT

v S � P(T) ]EQST

1

Zerobond with maturity T as numeraire

¬ Since the price of the numeraire at expiry is known in advance, the expected payoff issimply multiplied (discounted) by the price of the zerobond.

¬ This method is standard market practice for valuation of interest rate sensitive derivatives.

CCEFM Doctoral Program, Stefan Pichler

133

¬ This probability measure is known as forward measure for maturity T.

¬ Note, that St / Pt (T) is the forward price of the asset.

¬ Under the forward measure all forward prices are martingales.

CCEFM Doctoral Program, Stefan Pichler

134

First application of the Fundamental Theorem of Asset Pricing:

¬ Continuously compunded money market deposit with annual rate r used as numeraire.

¬ r assumed to be constant.

¬ Distribution of ST given S0 is assumed to be lognormal with variance σ2T for all T > 0.

¬ Multi-period extension of the one-period binomial model.

CCEFM Doctoral Program, Stefan Pichler

135

u � e σ ] stepsize

¬ Let St+1 be uSt in the up-step and dSt in the down-step.

¬ d = 1/u is a sufficient and necessary condition for a binomial lattice (recombining tree).

¬ Cox, Ross, and Rubinstein (1979) showed that in a binomial lattice the condition

ensures that the distribution of ST converges to a lognormal with variance σ2T for very smallstepsizes.

¬ In the CRR model the martingale probability is given by q �e r ]stepsize

� u �1

u � u �1.

CCEFM Doctoral Program, Stefan Pichler

136

Example:The current price of a non-dividend paying stock is 100 and its volatility is 20%p.a. Thecontinuous deposit rate is 5% p.a. Calculate the value of a six-months call with strike price 100.Use a four-step binomial lattice.

Stepsize: 0.5 / 4 = 0.125 yearsVolatility per step: 0.2 ] B0.125 = 0.0707Discount factor per step: e-0.125]0.05 = 0.99377Accrual factor per step: 1/0.99377 = 1.00627Multiplier u: e0.0707 = 1.0733

CCEFM Doctoral Program, Stefan Pichler

137

1. Step:Sup = 100]1.0733 = 107.33 Sdown = 100 / 1.0733 = 93.17

2. Step:Sup,up = 107.33]1.0733 = 115.19 Sdown,down = 93.17 / 1.0733 = 86.81Sup.down = Sdown,up = 107.33 / 1.0733 = 93.17]1.0733 = 100

.....

CCEFM Doctoral Program, Stefan Pichler

138

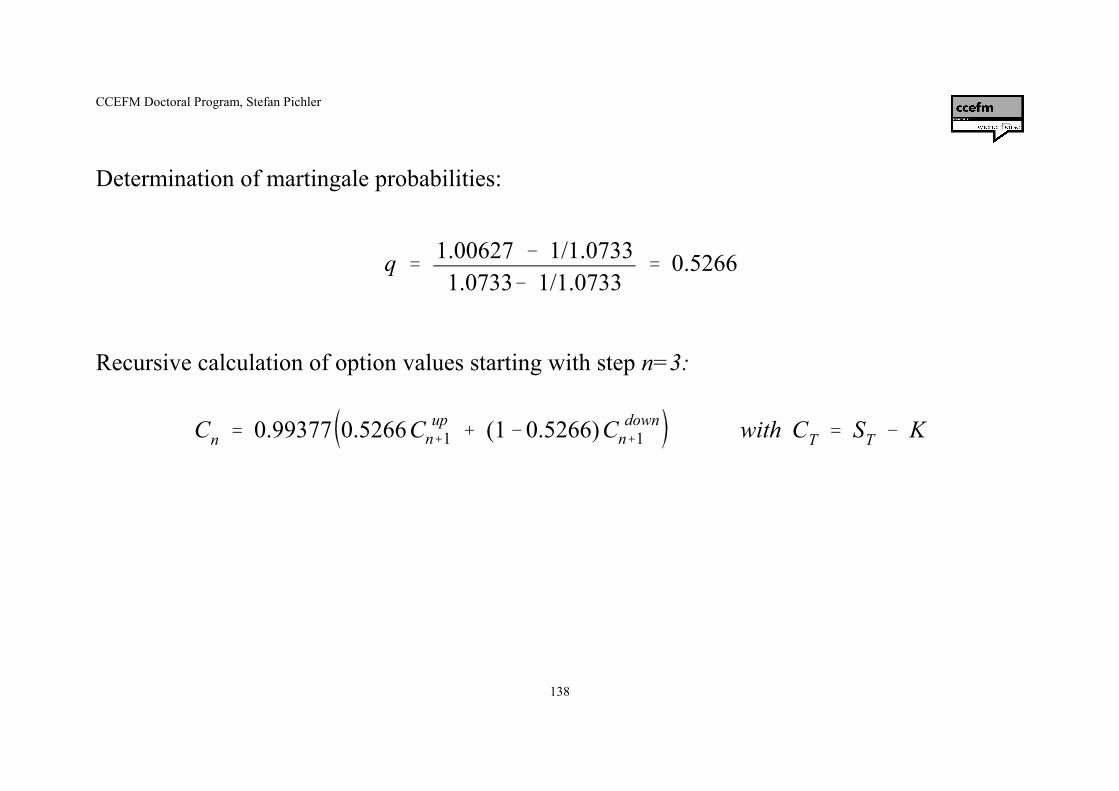

q �1.00627 � 1/1.07331.0733� 1/1.0733

� 0.5266

Cn � 0.99377 0.5266C upn�1 � (1�0.5266)C down

n�1 with CT � ST � K

Determination of martingale probabilities:

Recursive calculation of option values starting with step n=3:

CCEFM Doctoral Program, Stefan Pichler

139

Underlying 132.69Call 123.63 32.69

115.19 24.2516.43 115.19

107.33 107.33 15.1910.56 7.95

100.00 100.00 100.006.55 4.16 0.00

93.17 93.172.18 0.00 86.81

86.81 0.000.00 80.89

0.00 75.360.00

n=0 n=1 n=2 n=3 n=4

CCEFM Doctoral Program, Stefan Pichler

140

C � B ]EQCT

BT

� e �r ]T]EQ CT

Further applications of the Fundamental Theorem of Asset Pricing:

¬ Assumptions as in the CRR model (constant r, lognormality with constant variance).

¬ Direct application of the general valuation principle.

¬ Under these assumptions the arbitrage-free value of a financial instrument C is given by

CCEFM Doctoral Program, Stefan Pichler

141

C � e �rT]‹Q

K

(ST � K) ] f (ST) ]dST

¬ For a European call option this problem reduces to

where f(.) denotes the lognormal density function under the martingale measure.

¬ Problem: What are the correct parameters under the martingale measure?

¬ Answer: Given by Girsanov‘s theorem. The variance parameter equals the empiricalvariance σ2T, the expected value equals E[ST] = S] erT , ie the expected assetprice is independent of the empirically estimated growth rate.

CCEFM Doctoral Program, Stefan Pichler

142

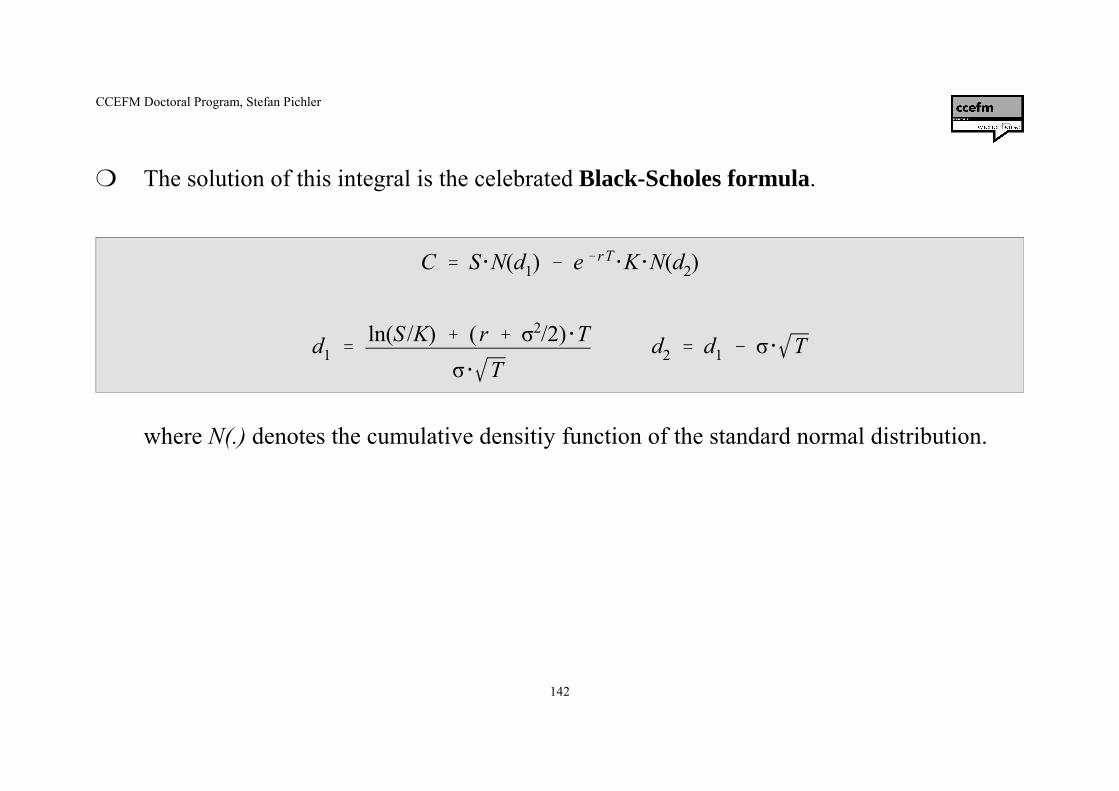

C � S ]N(d1) � e �rT]K ]N(d2)

d1 �ln(S /K) � (r � σ2/2) ]T

σ ] Td2 � d1 � σ ] T

¬ The solution of this integral is the celebrated Black-Scholes formula.

where N(.) denotes the cumulative densitiy function of the standard normal distribution.

CCEFM Doctoral Program, Stefan Pichler

143

d1 �ln(120/130) � (0.05 � 0.22/2) ]0.5

0.2 ] 0.5� �0.3185

d2 � �0.4599

C � 120 ]0.3751 � e �0.05 ]0.5]130 ]0.3228 � 4.08

Example: Calculate the arbitrage-free value of a European call option under the Black-Scholes model given the following inputs.

S = 120, K = 130, σ = 20% p.a., r = 5% p.a., T = 6M

CCEFM Doctoral Program, Stefan Pichler

144

C � PT ]‹Q

K

(FT � K) ] f (FT) ]dFT

C � B ]EQCT

BT

� PT ]EQ CT

¬ Using a zerobond with maturity until expiry as the numeraire and again assuminglognormality the arbitrage-free value of a financial instrument C is given by

¬ The integral to solve is now

where we make use of the fact that the forward price F of the underlying asset equals the spotprice S at expiry.

CCEFM Doctoral Program, Stefan Pichler

145

C � PT ] F ]N(d1) � K ]N(d2)

d1 �

ln(F /K) � σ2F /2 ]T

σF ] Td2 � d1 � σF ] T

¬ The solution of this integral is the Black (1976) formula.

¬ What has changed? The forward price is now assumed to be lognormal with volatilityparameter σF, and there are no assumptions made about a constant continuous interest rate.

¬ The Black formula is the market standard for the valuation of interest dependent options.