october 18, 2006 webinar “asset protection strategies that actually work” mat sorensen, jd...

TRANSCRIPT

October 18, 2006

Webinar“Asset Protection Strategies that Actually Work”

Mat Sorensen, JD

“Important Year-end Tax Strategies”Mark Kohler, CPA, JD

kkolawyers.com856 South Sage Dr., Suite 2, Cedar City, Utah

Telephone 435.586.9366 / Facsimile 435.586.9491

© Kyler Kohler & Ostermiller, LLP 2006

Disclaimer- Although the information contained in this Presentation may be extremely useful and helpful, please understand that the presentation of this information does not constitute an attorney-client relationship. Moreover, the information contained in this Presentation is for general guidance only. It is strongly recommended that each individual or entity obtain their own legal advice, particularly applied to their own set of circumstances, facts and specific situation. Kyler Kohler & Ostermiller, LLP is not responsible or liable for any advice that is taken and applied in a situation without direct consultation and representation specific to that individual’s or company’s needs.

Instructor Notes

© Kyler Kohler & Ostermiller, LLP 2006

Asset Protection Summary1. Protect your personal assets from your business. Corporate veil.

2. Protect your business assets from yourself. Charging order for LP and LLC.

Problems with single member LLC.

3. Protecting personal assets such as cabins, 2nd homes, etc… FLP or irrevocable trusts.

4. Protecting the equity in your Home. Equity stripping.

5. What doesn’t work? Land Trusts and Fraudulent Transfers.

6. Quick and Easy Asset protection. Exemptions and exempt assets (homestead, retirement accounts, tenants by the entirety).

7. What is new in Asset Protection? The Series LLC.

Asset Protection Strategies That Actually Work

© Kyler Kohler & Ostermiller, LLP 2006

Series LLC

Series 1 Series 2 Series 3

Series 4 Series 5

Master LLC

Series LLC Basics

1) Must treat each series as a separate entity. -Hold property and contract in name of the series (e.g, Series 1 of Jones Real Estate, LLC).-Maintain separate accounts and records for each series.

2) States where the Series LLC is recognized. More and more states are considering adopting the Series LLC statute. -Delaware, Illinois, Nevada, Iowa, Oklahoma, Tennessee, and Utah.

© Kyler Kohler & Ostermiller, LLP 2006

Asset Protection Strategies That Actually Work

Benefits and Concerns of the Series LLC

Concerns

• Careful consideration should be used before using the Series LLC in states that do not have a Series LLC statute.

• This is a new area of the law and there is no specific guidance from the IRS on whether one tax return for the mater LLC will be required or whether a separate tax return will be required for each Series within the LLC. The practical approach seems to be to treat each series of the LLC as a wholly owned subsidiary company and thus only do a single LLC tax return for the multiple entities.

• Caution in California. The Franchise Tax Board Revenue Ruling requires that each Series of the LLC pay the minimum $800 franchise tax.

Benefits

• Avoid the problem of having “all of your eggs in one basket”. Each series is treated as a separate entity from the other series so that when a lawsuit occurs in one series the creditor plaintiff can only attack the assets in the series being sued. For example, if you had a lawsuit regarding a property in Series 1, then only the assets in Series 1 would be available to a creditor. The assets in Series 2-5 would be protected from the liability created in Series 1.

• Reduce costs and expenses from setting up multiple entities. Traditional approach to obtain separate treatment is to set up multiple entities.

Asset Protection Strategies That Actually Work

© Kyler Kohler & Ostermiller, LLP 2006

BREAK

1. Start a Small Business2. Pay your Family for Services they Provide

3. Adopt a self-directed Retirement Plan4. Rental Property AND Cost Segregation

5. Properly Deduct Medical Costs6. Purchase a larger vehicle for your business

Important Year-End Tax Strategies

© Kyler Kohler & Ostermiller, LLP 2006

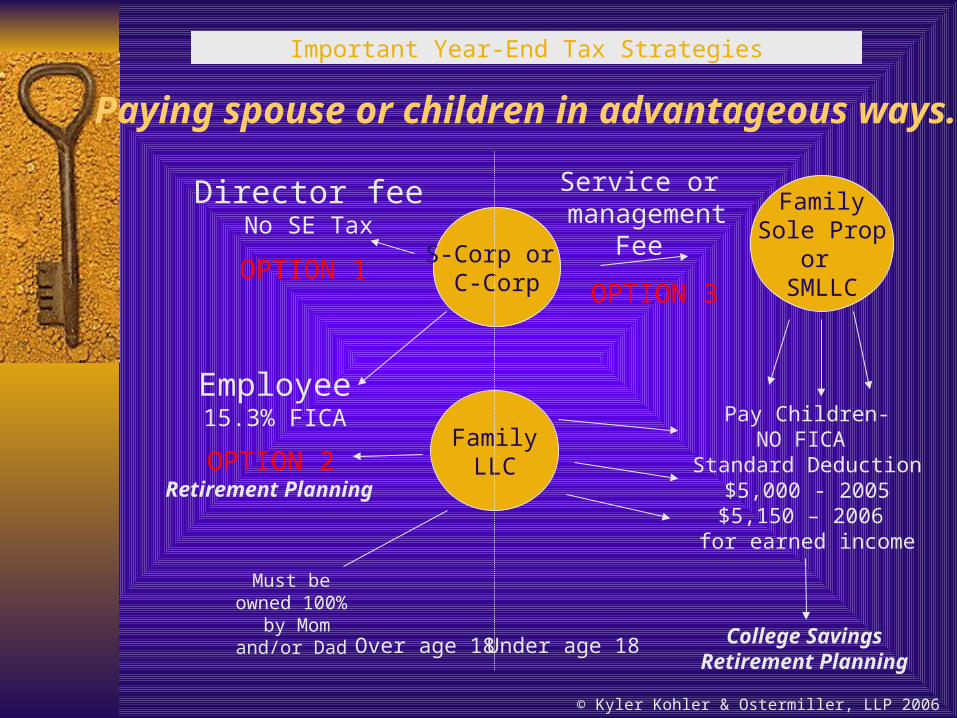

Paying spouse or children in advantageous ways…

S-Corp or C-Corp

Director feeNo SE Tax

Employee15.3% FICA

FamilySole Prop

or SMLLC

Pay Children-NO FICA

Standard Deduction$5,000 - 2005$5,150 – 2006

for earned income

Service or management

Fee

FamilyLLC

Over age 18 Under age 18

Must be owned 100%

by Mom and/or Dad

Retirement Planning

OPTION 1

OPTION 2

OPTION 3

College SavingsRetirement Planning

Important Year-End Tax Strategies

© Kyler Kohler & Ostermiller, LLP 2006

Retirement Plans

Individual Retirement Accounts

Profit Sharing Plans Defined Benefit Plans

- Simple IRA

- Traditional IRA

- Educational IRA

- Simplified Employee Plan IRA

- Roth IRA

- Straight P.S.

- Traditional 401(k)

- Roth 401(k)

- 412 (i)

- Self Directed DB

Government Retirement Plans

- 403 B

- 429

- 457

Important Year-End Tax Strategies

© Kyler Kohler & Ostermiller, LLP 2006

The 4 Most Commonly Used Defined Contribution S.D.R.P.’s

Traditional IRA

Roth IRA

Traditional 401(k)

Roth 401(k)

Important Year-End Tax Strategies

© Kyler Kohler & Ostermiller, LLP 2006

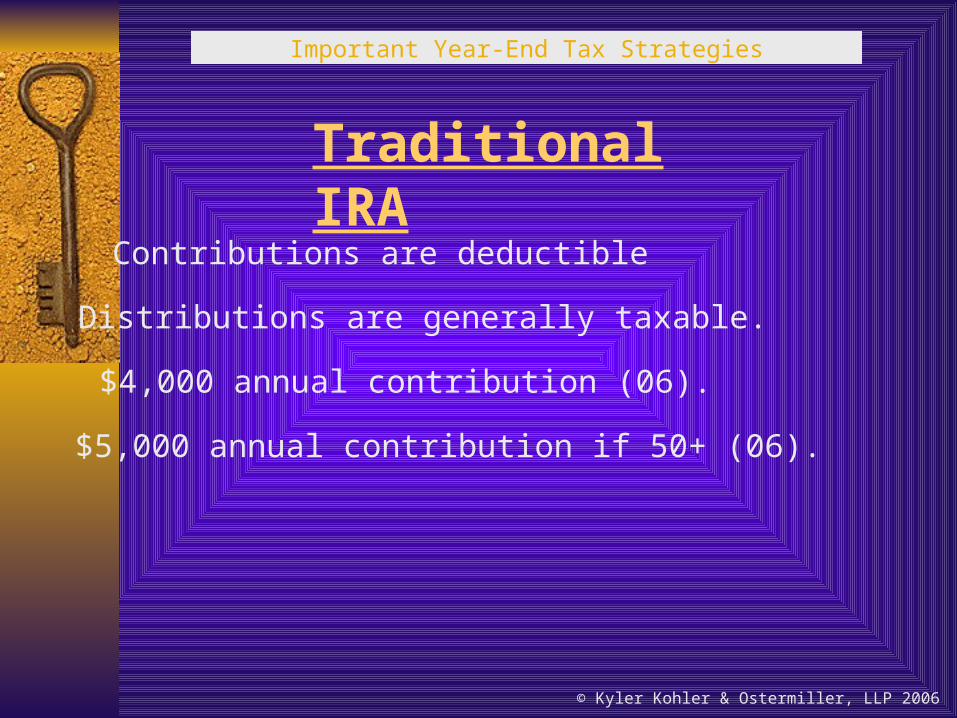

Traditional IRA

Contributions are deductible

$4,000 annual contribution (06).

$5,000 annual contribution if 50+ (06).

Distributions are generally taxable.

Important Year-End Tax Strategies

© Kyler Kohler & Ostermiller, LLP 2006

Roth IRA

Contributions are non-deductible.

$4,000 annual contribution (06).

$5,000 annual contribution if 50+ (06).

Distributions are non-taxable!

Important Year-End Tax Strategies

© Kyler Kohler & Ostermiller, LLP 2006

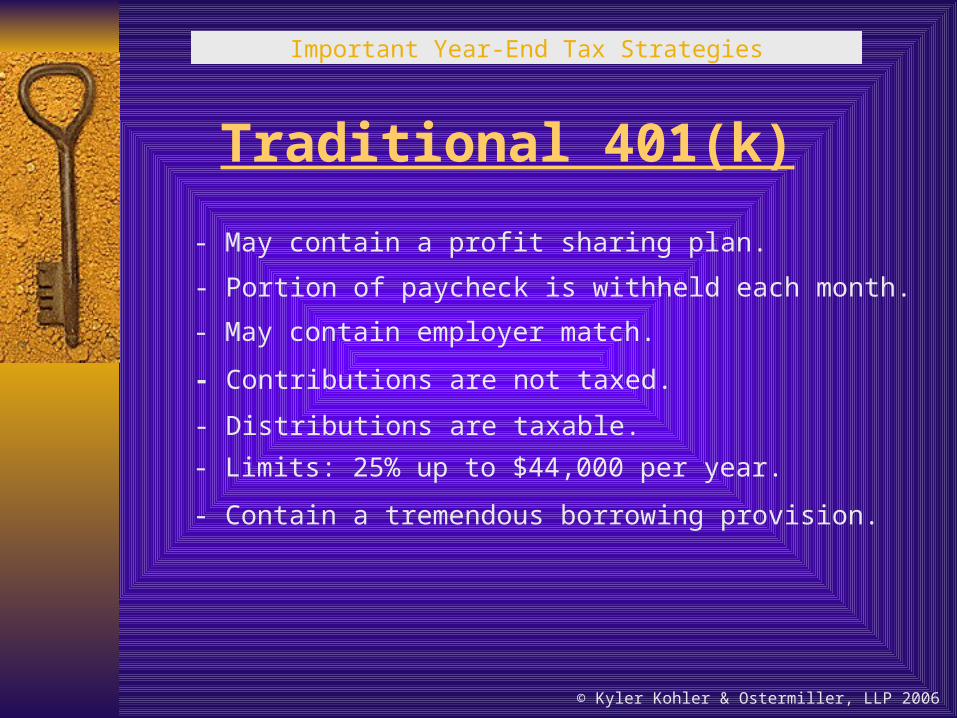

Traditional 401(k)

- Distributions are taxable.

- Limits: 25% up to $44,000 per year.

- Contain a tremendous borrowing provision.

- May contain a profit sharing plan.

- Portion of paycheck is withheld each month.

- Contributions are not taxed.

- May contain employer match.

Important Year-End Tax Strategies

© Kyler Kohler & Ostermiller, LLP 2006

Roth 401(k)

- Distributions will be taxable and non-taxable!

- Limits: 25% up to $44,000 per year.

- Contains a tremendous borrowing provision.

- May contain a profit sharing plan.

- Portion of paycheck is withheld each month.

- Employee contributions are taxable.

- May include employer match.

- Employer contributions non-taxable.

Important Year-End Tax Strategies

© Kyler Kohler & Ostermiller, LLP 2006

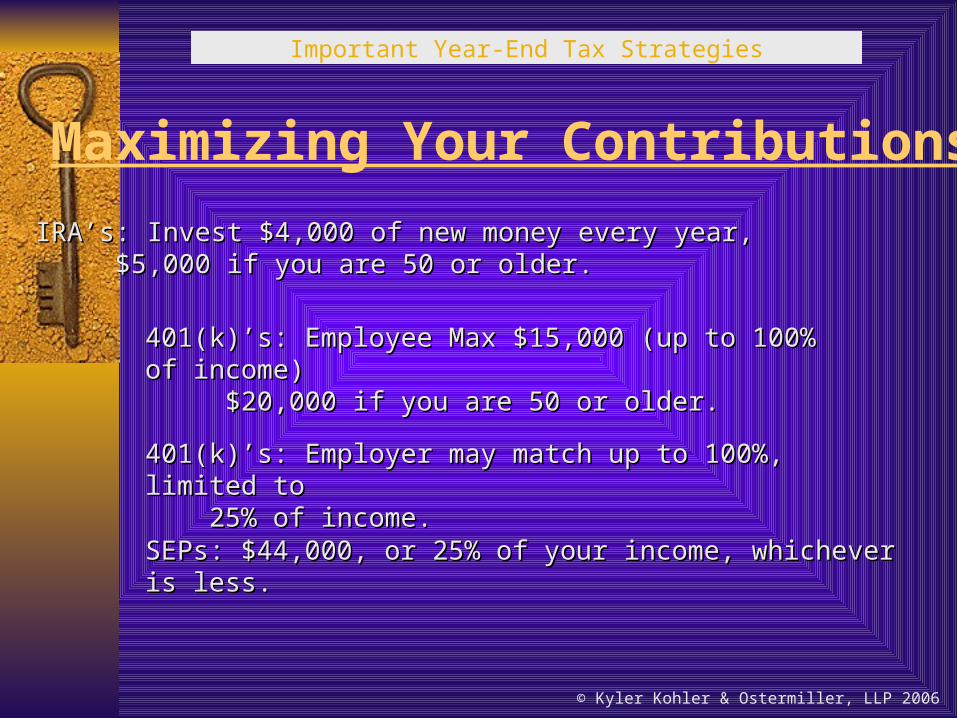

Maximizing Your Contributions

IRA’s: Invest $4,000 of new money every year, IRA’s: Invest $4,000 of new money every year, $5,000 if you are 50 or older.$5,000 if you are 50 or older.

401(k)’s: Employee Max $15,000 (up to 100% of income) 401(k)’s: Employee Max $15,000 (up to 100% of income) $20,000 if you are 50 or older.$20,000 if you are 50 or older.

401(k)’s: Employer may match up to 100%, limited to401(k)’s: Employer may match up to 100%, limited to 25% of income. 25% of income.

SEPs: $44,000, or 25% of your income, whichever is less.SEPs: $44,000, or 25% of your income, whichever is less.

Important Year-End Tax Strategies

© Kyler Kohler & Ostermiller, LLP 2006

Comparing the 401(k) and SEP

Important Year-End Tax Strategies

Salary- 36,000 - FICA cost - $5,508

Salary- 36,000 - FICA cost - $5,508

401(k) SEP

Employee Cont. - $15,000

Company Match - $9,000

Total Deferral - $24,000

Total Deferral- $9,000

In order to obtain a $24,000Deferral, Salary would have To equal $96,000 at a FICACost of $14,465. (diff of $8,957)

To obtain a $44,000 deferralSalary would have to be$176,000 at a FICA costof $16,785.

© Kyler Kohler & Ostermiller, LLP 2006

Thank You!!

Mark J. Kohler, CPA, Attorney at Law

kkolawyers.com856 South Sage Dr., Suite 2, Cedar City, Utah

Telephone 435.586.9366 / Facsimile 435.586.9491

© Mark J. Kohler, CPA, JD, PC, 2006