oceanagold fact book 2014 · 2 oceanagold corporation fact book 2014 cautionary statement regarding...

TRANSCRIPT

1Section title

OceanaGold Fact Book 2014Innovation Performance Growth

2 OceanaGold Corporation Fact Book 2014

Cautionary Statement Regarding Forward Looking Information

This Fact Book contains “forward-looking statements and information” within the meaning of applicable securities laws which may include, but is not limited to, statements with respect to the future financial and operating performance of the Company, its subsidiaries and affiliated companies, its mining projects, the future price of commodities, the estimation of Mineral Reserves and Mineral Resources, the realisation of Mineral Reserve and resource estimates, costs of production, estimates of initial capital, sustaining capital, operating and exploration expenditures, costs and timing of the development of new deposits, costs and timing of the development of new mines, costs and timing of future exploration and drilling programs, timing of filing of updated technical information, anticipated production amounts, requirements for additional capital, governmental regulation of mining operations and exploration operations, timing and receipt of approvals, consents and permits under applicable mineral legislation, environmental risks, title disputes or claims, limitations of insurance coverage and the timing and possible outcome of pending litigation and regulatory matters. Often, but not always, forward-looking statements and information can be identified by the use of words such as “plans”, “expects”, “is expected”, “predicts”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “targets”, “aims”, “anticipates” or “believes” or variations (including negative variations) of such words and phrases, or may be identified by statements to the effect that certain actions, events or results “may”, “could”, “would”, “should”, “might” or “will” be taken, occur or be achieved. Forward-looking information or statements contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Company and/or its subsidiaries and/or its affiliated companies to be materially different. For a list of risk factors, please refer to the Company’s Annual Information Form in respect of its fiscal year-ended December 31, 2013, which is available on SEDAR at www.sedar.com under the Company’s name. Forward-looking statements and information contained herein are made as of the date of this document and, subject to applicable securities laws, the Company disclaims any obligation to update any forward looking statements and information, whether as a result of new information, future events or results or otherwise. Readers should not place undue reliance on forward-looking statements and information due to the inherent uncertainty therein. All forward-looking statements and information made herein are qualified by this cautionary statement.

Cautionary Notes Regarding Technical Information

Standards: This Fact Book includes disclosure of scientific and technical information, as well as information in relation to the calculation of reserves and resources, with respect to OceanaGold’s mineral projects. OceanaGold’s disclosure of Mineral Reserve and Mineral Resource information is governed by National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”) under the guidelines set out in the Canadian Institute of Mining, Metallurgy and Petroleum (the “CIM”) Standards on Mineral Resources and Mineral Reserves, adopted by the CIM Council, as may be amended from time to time by the CIM (“CIM Standards”). The disclosure of Mineral Reserve and Mineral Resource information relating to OceanaGold’s properties is also presented in accordance with the reporting requirements of the 2012 Edition of the “Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves” (“JORC Code”). Estimates of Mineral Resources and Mineral Reserves prepared in accordance with the JORC Code would not be materially different if prepared in accordance with the CIM definitions applicable under NI 43-101. There can be no assurance that those portions of Mineral Resources that are not Mineral Reserves will ultimately be converted into Mineral Reserves. Mineral Resources are not Mineral Reserves and do not have demonstrated economic viability. This Fact Book uses the terms “Measured”, “Indicated” and “Inferred” resources. U.S. persons are advised that while such terms are recognized and required by Canadian regulations, the Securities and Exchange Commission does not recognize them. U.S. persons are cautioned not to assume that all or any part of Measured or Indicated Resources will ever be converted into reserves. U.S. persons are also cautioned not to assume that all or any part of an Inferred Mineral Resource exists, or is economically or legally mineable.

Technical Reports: For further information regarding OceanaGold’s properties, reference should be made to the following NI 43-101 technical reports that have been filed and are available at www.sedar.com under the Company’s name: (a) “Technical Report for the Macraes Project located in the Province of Otago, New Zealand” dated February 12, 2010, prepared by R. Redden and J. G. Moore, both of Oceana Gold (New Zealand) Limited; (b) “Technical Report for the Reefton Project located in the Province of Westland, New Zealand” dated May 24, 2013, prepared by K. Madambi, Technical Services Manager and J. G. Moore Chief Geologist, both of Oceana Gold (New Zealand) Limited (the “Reefton Technical Report”; and (c) “Technical Report for the Didipio Project located in Luzon, Philippines” dated July 29, 2011, prepared by R. Redden and J. Moore of Oceana Gold (New Zealand) Limited (the “Didipio Technical Report”).

R. Redden was a full-time employee of the Company’s subsidiary, Oceana Gold (New Zealand) Limited at the time of writing, and K. Madambi and J. G. Moore were, and remain, full-time employees of Oceana Gold (New Zealand) Limited. The Technical Reports have been filed with the Canadian securities regulatory authorities and are available for review at www.sedar.com under the Company’s profile.

For further information regarding the El Dorado property, formerly owned by Pacific Rim Mining Corp. (“Pacific Rim”), reference should be made to the following NI 43-101 technical report which has been filed and is available at www.sedar.com under Pacific Rim’s name: “Technical Report Update on the El Dorado Project Gold and Silver Resources, Department of Cabañas, Republic of El Salvador” dated March 3, 2008, prepared by Steven Ristorcelli and Peter A. Ronning of Mine Development Associates.

The El Dorado resource estimate referred to herein was prepared by Mr. Steven Ristorcelli, C.P.G., of Mine Development Associates, Reno, Nevada (who is an independent Qualified Person as defined in NI 43-101) and conforms to current CIM Standards on Mineral Resources and Reserves. Where the Mineral Reserve and Mineral Resource estimates of the Company’s Reefton, Macraes and Didipio Projects set out in this Fact Book differ from those set out in the Technical Report for the relevant property, such differences arise from updates to such Mineral Reserve and Mineral Resource estimates as a result of depletion through production, additional exploration activities or revised economic assumptions.

The latest updates of Mineral Reserves for each of the Company’s New Zealand projects were prepared by, or under the supervision of, K. Madambi, while the Mineral Reserves for the Didipio Project were prepared under the supervision of R. Corbett. The updates of Mineral Resources for Didipio Project was prepared by, or under the supervision of, J. G. Moore, whilst the updates of Mineral Resources for the Macraes Project and Reefton Project were updated by S. Doyle. S. Doyle, K. Madambi, and J. G. Moore are Members and Chartered professionals with the Australasian Institute of Mining and Metallurgy and each is a “qualified person” for the purposes of NI 43-101. S. Doyle is also a member of the Australian Institute of Geoscientists. R, Corbett is a Registered Professional Engineer (Ontario) and is a “qualified person” for the purposes of NI 43-101. All such persons are “qualified persons” for the purposes of NI 43-101 and have sufficient experience relevant to the style of mineralisation and type of deposit under consideration and to the activity which they are undertaking to qualify as a Competent Person as defined in the JORC Code. Messrs Corbett, Doyle, Madambi, Moore and Ristorcelli consent to inclusion in this Fact Book of the matters based on their information in the form and context in which it appears.

OceanaGold has adopted United States dollars (USD) as its presentation currency. The financial information is presented in USD and all numbers in this document are expressed in USD unless otherwise stated.

Cover image: Macraes Goldfield, New Zealand

3Section title

Contents

5 The Business at a Glance 6 Map of Operations and Assets 7 OceanaGold at a Glance 8 Chairman Letter 9 CEO Letter10 Vision and Values11 Investment Highlights & Strategy12 Operating Summary13 Company History

15 Operations16 Didipio Mine, Philippines20 Macraes Goldfield, New Zealand: Macraes Open Pit22 Macraes Goldfield, New Zealand: Frasers Underground23 Reefton Goldfield, New Zealand:

Reefton Open Pit24 Processing, New Zealand25 El Dorado Project: El Salvador26 Resource Development27 Reserves & Resources28 Sustainability

31 Financials and Investor Information

32 Five Year Financial Summary33 Operating Costs34 Capital Expenditure & Liquidity 35 Share Information36 Our Team 38 Glossary39 Key Investor Dates

and Corporate Directory

4 OceanaGold Corporation Fact Book 2014

Macraes Open Pit and entrance to Frasers Underground mine, New Zealand

5Section title

Multinational gold producer and developer

5

The Business at a Glance

6 OceanaGold Corporation Fact Book 2014

Wellington

Auckland

Macraes Open PitFrasers Underground

Reefton Open Pit

Christchurch

Dunedin

Map of Operations and Assets

San Salvador

New Zealand

El SalvadorPhilippines

Mineral Reserves Gold (Moz) Copper (’000t)

3.14 210

Proven 1.38 90

Probable 1.76 120

Mineral Resources Gold (Moz) Copper (’000t) Silver (Moz)

Resources1 12.04 290 11.38

Measured & Indicated 8.34 260 9.48

Inferred 3.70 30 1.90

Didipio MineEl Dorado Project2

Luzon

Mindanao

Manila

1. Resources are inclusive of reserves and reserves are in situ ounces. Please refer to page 27 for Reserves/Resource statement.2. Please refer to page 25 for for further information on the status of permit applications at El Dorado.

The Business at a Glance 7

OceanaGold at a Glance

OceanaGold TodayOceanaGold is a significant multinational gold producer listed on the Toronto, Australian and New Zealand stock exchanges. The Company has a portfolio of operating, development and exploration assets located in the northern Philippines, South Island of New Zealand and El Salvador. There were 1,376 full time employees at the end of 2013.

The Didipio Mine in the Philippines commenced commercial production on April 1, 2013 and is forecast to produce on average 100,000 ounces of gold and 14,000 tonnes of copper over its 15 year mine life. The Company is forecast to produce approximately 200,000 ounces of gold per annum from its New Zealand operations.

Financial Snapshot

Year ended 31 December 2013 2012 2011 2010 2009

Revenue US$m 553.6 385.4 395.6 305.6 237.1

EBITDA1 US$m 262.4 144.6 163.9 139.5 106.2

Operating profit US$m 135.2 53.1 78.5 71.8 40.4

Earnings before income tax1 US$m 106.1 31.7 65.2 55.4 25.6

Net earnings before impairment US$m 91.3 20.7 44.2 44.4 54.5

Net earnings/(loss) US$m (47.9) 20.7 44.2 44.4 54.5

Diluted earnings/(loss) per share US$ (0.16) 0.08 0.17 0.20 0.29

Cash and cash equivalents US$m 24.8 96.5 170.0 181.3 42.4

Gold produced oz 325,732 232,909 252,499 268,602 300,391

Gold sold2 oz 308,081 230,119 249,261 268,087 300,044

Average gold price received US$ / oz 1,382 1,675 1,587 1,140 790

Copper produced tonnes 23,059 - - - -

Copper sold2 tonnes 21,290 - - - -

Average copper price received US$/tonne 7,127 - - - -

Cash operating cost3 US$ / oz 426 940 875 570 411

Cash operating margin US$ / oz 956 735 712 570 379

1. Excluding gain / (loss) on undesignated hedges and non cash impairment charge 2. Includes Didipio Q1 2013 pre commerical production of 2,791 ounces of gold and 1,549 tonnes of copper sold 3. Net of by-product credits based on ounces of gold sold and includes the Didipio nine month period of commerical production in 2013

GO

LD ‘0

00 O

UN

CE

S

CO

PP

ER

’000

TO

NN

ES

2007

2008

2009

2010

2011

2012

2013

2014

E

2014

E

2013

50

0

150

250

350

0

5

10

15

20

25

GO

LD ‘0

00 O

UN

CE

S

CO

PP

ER

’000

TO

NN

ES

2007

2008

2009

2010

2011

2012

2013

2014

E

2014

E

2013

50

0

150

250

350

0

5

10

15

20

25

Production Profile

8 OceanaGold Corporation Fact Book 2014

Chairman Letter

Your Board has overseen an eventful 2013 which has positioned OceanaGold as a robust, profitable gold and copper producer with multiple mines and a growing international reputation as a well- managed, transparent and aspirational player in the Pacific basin.

The smooth commissioning of Didipio into commercial production by April and the stellar production since then was most timely, as our New Zealand (NZ) operations came under extreme margin pressure due to the combined impacts of softness in the gold price and escalating currency strength of the New Zealand Dollar. Early response to the NZ issues resulted in these operations being rescheduled, judicious and modest gold hedging denominated in NZ dollars being implemented and certainty around protecting modest margins and mine life achieved. I must stress that this was only possible due to the excellent productivity and workplace relations embodied in the NZ workforce and community. With these attributes amply demonstrated, we can now aggressively look at other production alternatives for these operations. While it would appear they may not always continue to deliver the current scale, they could well extend the profitable life, particularly at Macraes, for at least a decade.

On May 15, 2013, the Board had the great pleasure to attend a low key opening ceremony for the Didipio Mine in the North East highlands of Luzon. As I commented at the time to the attendees, largely comprising our workforce, surrounding communities and Philippine dignitaries, it was the crowning achievement of some 25 years of effort since discovery. And while the current reserve life is some 15 years, there is the regional mineralisation endowment to materially extend this life. One highlight of this commissioning period and subsequent production has been the exceptional safety record being created and Michael Holmes, our Chief Operating Officer, and his operating team are to be credited with an extraordinary performance.

Crossing the Rubicon into being a Philippine producer, with the structure of the first mine to operate under a FTAA (Financial or Technical Assistance Agreement) meant that both we and the Philippine government agencies involved were in somewhat unchartered waters. On your behalf, I must single out Joey Leviste (Chairman of OceanaGold Philippines Inc.), Chito Gozar (Senior Vice President Communications & External Affairs) and Brennan Lang (General Manager, Didipio) for their achievement in enabling Didipio to be constructed on schedule and bedding down the multitude of issues which were encountered and resolved in the first year of production.

The strategic vision of your Company is to take the results achieved in 2013 in production, commercial success, community relations, safety and environment as a springboard to adding growth via solid asset additions. A small step in this was the merger of Pacific Rim Corp. into OceanaGold, delivering ownership of a mature, high grade gold deposit in El Salvador. We would hope that further progress in this strategy will deliver accretive assets in the coming year.

The Company fully realises that the progress achieved in 2013 is a critical milestone in its evolution. However, it cannot rest on these achievements, but turn them to account in pursuit of improved operating efficiencies, safety and community relations. This provides the balance sheet and basis for aggressively seeking further corporate opportunities which complement our skill sets and result in increased shareholder security and investment return.

Sincerely,

Jim Askew, Chairman of the Board March 2014

“One highlight of (the Didipio) commissioning period and subsequent production has been the exceptional safety record being created…” Jim Askew

9The Business at a Glance

CEO Letter

To all of our shareholders, employees, Government agencies, suppliers and all our other stakeholders, welcome to the 2014 OceanaGold Fact Book.

Last year was both a tough year and a very successful one. Tough because we saw a dramatic drop in the gold price which wiped around 20% from our revenue line and required a fast response from our New Zealand operations. To the very great credit of all of our staff in New Zealand, the mobilisation to develop and execute new business plans there was virtually automatic, highlighting the great quality of our people and the culture existing within the Company. We were also successful because against this tough gold price environment, we successfully brought on line the highly competitive Didipio Mine which has essentially transformed OceanaGold into a low cost gold producer.

The achievements at Didipio over the past three years cannot be overstated. From the community relations teams on the ground at Didipio, to the construction teams who delivered the project on time and close to budget, to the operations teams that have commissioned and ramped up the mine to full production with excellent results. Many of the qualities demonstrated by the people that have worked on Didipio have emanated from within the existing company in New Zealand and therefore everyone in the company should be very proud of this achievement. An achievement which many people in the mining industry, both technical and financiers, thought could not be done. We have proven them all wrong.

Despite the lower gold price environment that has led to the tough decisions to cut back on production in New Zealand, the future for our Company now looks brighter than ever. We continue to drive for efficiency, and look to unlock the organic value from our existing operations, such as unlocking the tungsten value at Macraes and optimising the design and timing for the underground development at Didipio. These studies are a key focus for the Company in 2014 that will drive up shareholder value.

Most pleasingly our safety performance continues to improve as we pursue our goal of being injury free at all of our workplaces. We made good progress on this journey last year where we were lost time injury free at Didipio, an outstanding achievement for any new mining operation. We will never rest in our efforts to improve safety performance until we can ensure that no one will be injured when on the job at one of our workplaces.

The success of Didipio and the efficiency gains in New Zealand resulted in record production and record EBITDA for the year. This allowed us to repay some US$64 million of net borrowings putting us well on the way to deleveraging the business in line with our peer group of gold companies. Our finance team also successfully completed the payment of the last of the convertible notes financed in part by cash, and in doing so, commenced a new era of simpler financing structures and a cleaner balance sheet. This is an area that we have strategically strived to reach as it delivers a strong and robust company going forward that will be attractive to long term investors.

Looking back more generally at what we have achieved at OceanaGold over the past three years, I am personally very proud of everyone involved. The strength of management who have embraced our values to operate in all areas has underpinned a very strong mining company and look forward with great confidence to its ongoing success. I would like to take this opportunity to thank all of our stakeholders for supporting our Company and assisting us to get to this important stage in the transformation of OceanaGold.

Mick Wilkes, Managing Director and CEO March 2014

“ We successfully brought on line the…Didipio Mine which has…transformed OceanaGold into a low cost gold producer.” Mick Wilkes

10 OceanaGold Corporation Fact Book 2014

OceanaGold VisionWe will be a mid-tier, multinational gold producer

delivering superior shareholder returns in a safe and sustainable manner by developing and operating

high quality assets. We will be the partner, employer and mining company of choice.

Operations Development Growth

Efficient mines underpinned by judicious investment

Didipio operating to its full potential

Substantial low cost reserves

World Class Skills

Operational efficiency Mine design optimisation Converting opportunity

Strong Balance Sheet

Low debt Strategic capital allocation Strong investor base

Partner and Employer of Choice

Safety Environment Employees Community Government

Our ValuesThe ‘right way’ to do things at OceanaGold is through

demonstrating the following values:Respect > Integrity > Teamwork > Innovation > Action > Accountability

Our MottoInnovation > Performance > Growth

Vision and Values

11The Business at a Glance

Multinational Gold ProducerOrganic Growth StrategyFocused on Profitability> Solid production growth with reducing cash cost profile> Proven & probable reserves of 3.14 million ounces of gold

and 210,000 tonnes of copper> Total Resources of 12.0 million ounces of gold, 290,000

tonnes of copper and 11.4 million ounces of silver> The Didipio Mine in Luzon, Philippines commenced commercial

production in April 2013 and is expected to be one of the lower cost gold producers (net of by-product credits) and has transformed OceanaGold into a low cost producer

> Strong management team with significant experience and proven track record in acquiring, developing and operating gold mines internationally

> Solid reputation for operational excellence in environmentally sensitive areas

> Extensive history of successful commitment to sustainability

Investment Highlights Strategy

The Company’s business strategy: > Maximising profitability through efficient operations and

judicious investment;> Successfully ramping up the Didipio Mine to its full potential;> Developing new reserves and resources at its existing mines

from in-pit and near mine exploration or from satellite projects located within the current tenements;

> Implementing performance excellence programs that drive efficiency and increase profit margins from our existing operations; and

> Pursuing selective accretive acquisition and resource development opportunities that are complementary and add low cost gold reserves to the business.

Didipio Mine Philippines, commenced commercial production, April 2013

12 OceanaGold Corporation Fact Book 2014

Operating Summary

OceanaGold’s producing assets are Macraes (Open Pit and Frasers Underground) and the Reefton Open Pit mine, located in the South Island of New Zealand. Commercial production of the Didipio Mine commenced April 1, 2013.

Financial Statistics1 2013 2012 2011 2010 2009

Gold Sales (ounces) 308,081 230,119 249,261 268,087 300,044

Copper Sales (tonnes) 21,290 - - - -

Average Gold Price Received (US$ per ounce) 1,382 1,675 1,587 1,140 790

Average Copper Price Received (US$ per tonne) 7,127 - - - -

Cash Operating Cost1,2 (US$ per ounce) 426 940 875 570 411

Cash Operating Margin (US$ per ounce) 956 735 712 570 379

New Zealand Operating Statistics 2013 2012 2011 2010 2009

Gold Produced (ounces) 259,455 232,909 252,499 268,602 300,391

Total Ore Mined (tonnes) 8,650,072 6,872,686 8,103,693 7,905,464 6,258,806

Ore Mined Grade Gold (grams/tonne) 1.31 1.34 1.21 1.43 1.85

Total Waste Mined incl. pre-strip (tonnes) 56,544,293 54,580,473 59,176,017 57,643,657 61,087,834

Mill Feed (dry milled tonnes) 7,290,217 7,462,375 7,588,354 7,081,488 6,913,713

Mill Feed Grade Gold (grams/tonne) 1.35 1.20 1.25 1.45 1.68

Recovery Gold (%) 81.3 81.0 82.9 81.6 80.0

Didipio Operating Statistics 2013 2012 2011 2010 2009

Gold Produced (ounces) 66,277 - - - -

Copper Produced (tonnes) 23,059 - - - -

Total Ore Mined (tonnes) 8,787,878 - - - -

Ore Mined Grade Gold (grams/tonne) 0.58 - - - -

Ore Mined Grade Copper (%) 0.58 - - - -

Total Waste Mined incl. pre-strip (tonnes) 14,398,928 - - - -

Mill Feed (dry milled tonnes) 2,578,295 - - - -

Mill Feed Grade Gold (grams/tonne) 0.94 - - - -

Mill Feed Grade Copper (%) 0.98 - - - -

Recovery Gold (%) 83.0 - - - -

Recovery Copper (%) 91.5 - - - -

1. Didipio Mine commenced commercial production on April 1, 2013. In the first quarter of 2013, prior to commercial production, 2,791 ounces of gold and 1,549 tonnes of copper were sold from the Didpio Mine which is included in the gold and copper sold statistics. For cash cost calculation purposes, the revenue received for this period was netted off against capitalised development costs and therefore excluded from the cash cost calculation. 2. Net of by-product credits.

Full details can be found in the quarterly Management Discussion and Analysis (“MD&A”) documents available on the Company’s website.

13The Business at a Glance

Macraes Mining Company Limited commenced gold production at Macraes.

Pressure oxidation and autoclave facility commissioned at Macraes, only one of three in the southern hemisphere.

Two millionth ounce of gold poured from Macraes Open Pit Mine.

Frasers Underground Mine commissioned.Didipio placed under care & maintenance following Global Financial Crisis.

Oceana Gold Ltd incorporated.

Merger with Climax Mining bringing the Didipio Gold-Copper Project into the Company.

Record gold production for New Zealand operations (300,000 oz).

Didipio Mine construction recommenced in June.

Didipio Mine commenced commercial production in April.El Dorado Project1 in El Salvador acquired.Record gold production from New Zealand and Philippines operations.

Reefton Goldfield acquired from CRA Limited.

Oceana Gold Ltd listed on ASX and NZX.

OceanaGold Corporation listed on TSX.Reefton Open Pit Mine commissioned.Flotation cells commissioned at Macraes, the largest of this type operating in the world.

Three millionth ounce of gold poured from the Macraes process plant.

Didipio Mine construction completed and first concentrate produced in December.

Company History

1999

1999

1990

2005

2006

2003

2004

2011

2010

2012

2013

El Dorado HistoryModern mining and milling at the El Dorado Mine commenced in 1948. Over 270,000 tonnes of ore and approximately 72,500 ounces of gold were extracted until the mine closed in 1953, mainly due to low gold prices. Exploration was conducted from 1975 to 1976 and further deposits and prospects were identified between 1993 and 1995. Dayton Mining Corporation acquired the El Dorado Project in 2000 and amalgamated with Pacific Rim Mining Corp in 2002 through a reverse take-over.

Reefton Mining HistoryThe Reefton goldfield is historically one of New Zealand’s most prolific gold mining areas, having produced over two million ounces of gold from underground mining from when gold was first discovered in the Reefton area in about 1870 until the last large underground mine closed in 1951.

Macraes Mining HistoryThe Macraes area is a mature exploration province with the earliest alluvial mining occurring in 1862. In 1989, the original Macraes tenements were sold by Golden Point Mining and BHP Gold Mines (New Zealand) to the Macraes Mining Company.

Didipio Mining HistoryThe Didipio area was first recognised as a gold province in the 1970s, when indigenous miners from Ifugao Province discovered alluvial gold deposits in the region. Gold was mined either by the excavation of tunnels following high-grade quartz-sulphide veins or by hydraulicing in softer, clay-altered zones. Gold was also recovered by panning and sluicing gravel deposits in nearby rivers, and small-scale alluvial mining still takes place. No indications of the amount of gold recovered have been recorded.

2007

2008

2009

1. Please refer to page 25 for further information on the status of permit applications at El Dorado.

14 OceanaGold Corporation Fact Book 2014

Didipio process plant, Philippines, Ball mill and SAG mill (left), flotation circuit (foreground) and cyclone tower (top)

15Section title

We develop and operate quality assets in a safe and sustainable manner

Operations

15

16 OceanaGold Corporation Fact Book 2014

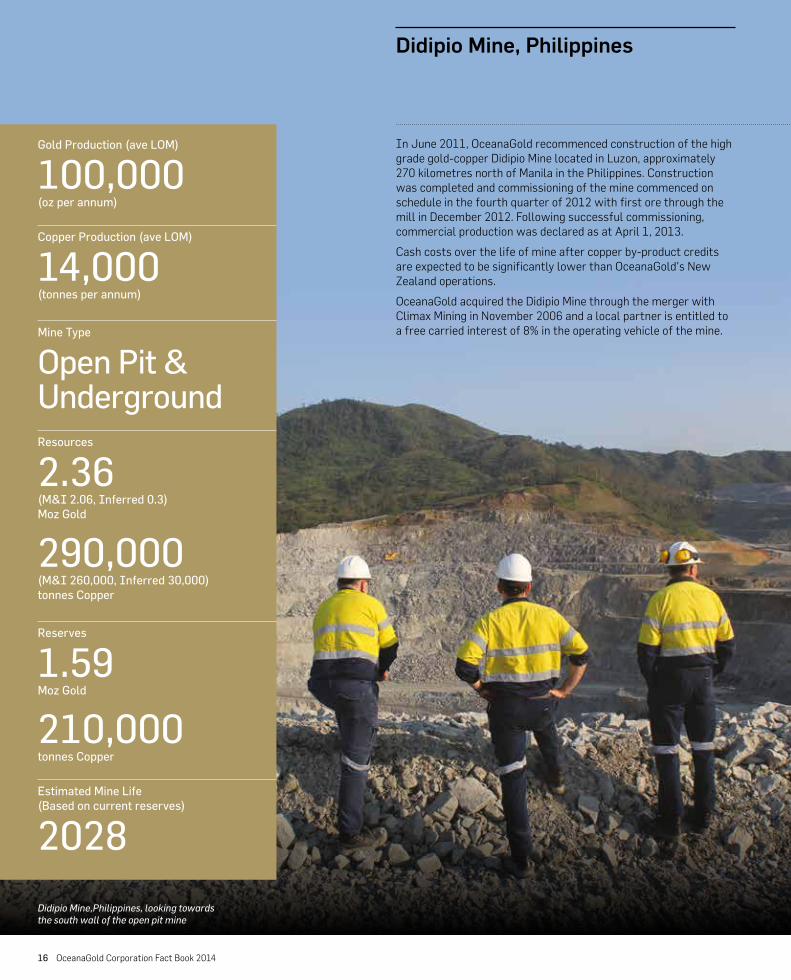

Didipio Mine, Philippines

In June 2011, OceanaGold recommenced construction of the high grade gold-copper Didipio Mine located in Luzon, approximately 270 kilometres north of Manila in the Philippines. Construction was completed and commissioning of the mine commenced on schedule in the fourth quarter of 2012 with first ore through the mill in December 2012. Following successful commissioning, commercial production was declared as at April 1, 2013.

Cash costs over the life of mine after copper by-product credits are expected to be significantly lower than OceanaGold’s New Zealand operations.

OceanaGold acquired the Didipio Mine through the merger with Climax Mining in November 2006 and a local partner is entitled to a free carried interest of 8% in the operating vehicle of the mine.

Gold Production (ave LOM)

100,000(oz per annum)

Copper Production (ave LOM)

14,000(tonnes per annum)

Mine Type

Open Pit & UndergroundResources

2.36(M&I 2.06, Inferred 0.3) Moz Gold

290,000 (M&I 260,000, Inferred 30,000) tonnes Copper

Reserves

1.59Moz Gold

210,000tonnes Copper

Estimated Mine Life (Based on current reserves)

2028

Didipio Mine,Philippines, looking towards the south wall of the open pit mine

17Operations

Open pit pre-strip mining commenced in January 2012. Current mining operations are focused on delivering ore from stages 2 and 3 of the open pit. Stage 4 stripping commenced in 2013. Mining is contracted out to a Filipino mining contractor with certain contractual obligations to ensure targets for Filipino training and employment are met. Mining operations continue to provide competent waste rock to build out the tailings storage facility (TSF) lifts. The Company expects to continue building the TSF lifts over the next four years to reach the ultimate life of mine capacity.

Open pit mining (based on current mine plan)> Strip ratio 3.45:1> Five pit stages > 300m deep open cut down to an elevation of 2,380mRL> Conventional drill and blast> Loading of haul trucks by hydraulic excavators> Open pit mining costs including pre-stripping are forecast

at US$2.70 per tonne mined (average next five years)

Underground mining (based on current mine plan)> Sub-level open stoping with cemented paste backfill> Mines in parallel with the open pit> Decline commences in 2016 from side of open pit> Production to commence in 2019> Near full production 2021, due to bottom up sequence> Base level 2,180mRL> Maximum mining rate 1.2Mtpa> Six year production life after development > Underground mining costs are forecast at US$34 per tonne

of ore mined

Ore BodyChalcopyrite (sulphide mineral of copper and iron) and gold are the main economic minerals in the deposit. Chalcopyrite occurs as fine-grained disseminations, aggregates, fracture fillings and stock work veins, particularly within the vein zone of alteration. Some bornite (also a sulphide mineral of copper and iron) is also present.

The ore body contains a higher concentration of copper near surface and hence copper production in the early years is expected to be higher than the average life of mine production and lower in the later years.

A model of the ore body is available on the following website link: www.oceanagold.com/our-business/philippines/didipio-mine/

MiningThe Didipio gold-copper deposit will be mined by both open pit and underground methods. Open pit mining is expected to operate on its own for the first 4 years with the underground development currently planned to commence with minimal ore in years 5 to 7. Open pit and underground activities will run concurrently until the pit is completed in year 12 with final low grade ore stock piles from open pit mining to be milled at the end of both open pit and underground operations.

Operational Statistics

Didipio Mine

Q4 Dec 31 2013

Q3 Sep 30 2013

Q2 Jun 30 2013

Q1 Mar 31 2013*

Year 2013*

Gold Produced (ounces) 27,713 18,011 13,676 6,877 66,277

Copper Produced (tonnes) 7,536 6,150 5,710 3,663 23,059

Total Ore Mined (tonnes) 2,618,832 2,602,651 1,729,314 1,837,081 8,787,878

Ore Mined Grade Gold (grams/tonne) 0.69 0.58 0.55 0.49 0.58

Ore Mined Grade Copper (%) 0.53 0.55 0.64 0.65 0.58

Total Waste Mined including pre-strip (tonnes) 3,473,327 3,832,560 4,342,999 2,750,042 14,398,928

Mill Feed (dry milled tonnes) 729,121 672,921 727,550 448,703 2,578,295

Mill Feed Grade Gold (grams/tonne) 1.33 0.97 0.75 0.59 0.94

Mill Feed Grade Copper (%) 1.09 0.97 0.91 0.92 0.98

Recovery Gold (%) 88.7 86.2 77.5 79.8 83.0

Recovery Copper (%) 95.0 94.2 87.3 88.6 91.5

*Note: The Didipio Mine commenced commercial production on April 1, 2013 therefore Q1 2013 operational statistics are pre-commercial production

18 OceanaGold Corporation Fact Book 2014

Trafigura is a leading international commodity trader that specialises in the supply and transport of concentrates, and owns and operates concentrate storage facilities in China and worldwide that support the company’s trading activity.

Copper concentrate is transported by truck from the Didipio Mine site to the port of San Fernando, a distance of around 350 kilometres by road. OceanaGold manages the copper concentrate land transportation and during 2013 purchased its own trucks and employed Filipino drivers. Generally there are 20 trucks on the road running daily and the average truck capacity is 20 tonnes. Given the long distance and passing through various communities en route, the Company is providing additional driver training and adding cameras and systems to reduce risks of road incidents.

The combined concentrate haulage and handling cost at the port, including warehousing and loading is forecast at around US$60 per wet metric tonne. In 2013 a total of 75,000 dry metric tonnes of Didipio copper concentrate was shipped from port to Asian smelters, primarily to Japan and Korea, with cargo varying from 5,000 to 10,000 dry metric tonnes at estimated freight costs of US$30 per wet metric tonnes. The estimated average moisture content is 10%.

ProcessingConstruction of a mineral processing facility to the north of the open pit mine was completed on schedule in the fourth quarter of 2012. Ore is processed with a conventional SAG/Ball mill grinding circuit followed by froth flotation for recovery of copper-gold concentrate. A gravity circuit is incorporated within the grinding circuit to produce gold bullion on site. Concentrate is transported by road to existing port facilities for export.

Initial nameplate capacity throughput rate of 2.5Mtpa was achieved in 2013, with 2014 throughput planned at 3Mtpa building up to the final expanded capacity of 3.5Mtpa by the end of 2014.

The Ball Mill Work Index is 14.6 kilowatt hours per tonne.

Approximately 50% of the average life of mine processing costs represents diesel power for the generators. During 2013 OceanaGold completed a feasibility study on connectivity to grid power which has the potential for annual operating cost savings. Regardless, self generation is deemed necessary to ensure the reliability of power supply.

Processing costs are estimated to average US$10 to US$11 per tonne milled (assuming no grid power connectivity as mentioned above). Overhead and site costs include administrative cost associated with maintaining the site at Didipio, meals, accommodation, transport and community relations and are forecast at US$10 to US$11 per tonne milled (average over the next five years).

In 2012, the Company announced the signing of an Offtake Agreement with Trafigura in relation to the sale and purchase of copper concentrate from the Didipio Mine with a minimum period of five years from the start of production. OceanaGold sells 100% of the Didipio copper-gold concentrate production to Trafigura at competitive terms and conditions, including treatment and refining charges. Trafigura takes delivery of copper-gold concentrate at the port and manages sea transportation from port to port.

Didipio Mine, Philippines

Didipio Mine Philippines, first gold poured May 2013

19Operations

Financial or Technical Assistance Agreement (“FTAA”)The Didipio Mine is held under the FTAA between OceanaGold and the Philippines Government which allows for 100% foreign ownership of the mining operations contractor. The FTAA covers an area of approximately 129 square kilometres in the provinces of Nueva Vizcaya and Quirino. There are currently six signed FTAAs and OceanaGold is the first company to operate under such a contract.

In accordance with OceanaGold’s FTAA agreement, the Company has a period of up to five years from the start of commercial production to recover its pre-operating expenses, property expenses and taxes paid during the recovery period. Following the earlier of five years or full recovery of pre-operating expenses and other recoverable items, the Government is entitled to 60% of “Net Revenue” and 40% will be that of OceanaGold.

Pre-operating expenses includes development and construction costs of the mine, payments to claim owners and landowners, exploration programs, maintenance of exploration tenement, feasibility studies, administration of offices, financing costs and the net commissioning cost up to commercial production. It also includes payments made by predecessor companies. Should OceanaGold not fully recover its pre-operating expenses in the five year period, the Company is entitled to a depreciation allowance for the outstanding balance for the following three years.

“Net Revenue” is calculated on gross revenue less operating costs and other allowable deductions. The Government’s Share includes all taxes paid such as corporate and excise tax, royalties, free carried interest paid and as such OceanaGold will be required to pay the difference between the 60% Net Revenue amount less all Government Share items paid during the period.

The Company has been granted a six year corporate tax holiday with a potential extension for a further two years.

FTAA Net Revenue

Net Revenue Calculation

Revenue

Less Operating costs

Less Depreciation of post development capital expenditure (excluding Underground development)

Less Underground mine development

= Net Revenue (Up to 5 years to recover the pre-operating expenses and other allowable items from Net Revenue)

Government Share ( = 60% Net Revenue post recovery)

The following items shall be included in the Government Share:

2% Net Smelter Royalty paid

2% Excise Duty paid (2% gross sales for gold, 2% copper concentrate)

Corporate Tax (current tax rate 30%)

Other taxes (e.g. Withholding tax)

8% Free Carried paid (entitles the holder to 8% of equity in the operating vehicle and dividends to be paid after recovery or pre-operating expenses)

Further details can be found in the NI 43-101 “Technical Report for the Didipio Project” dated July 29 2011, available on the Company’s website.

20 OceanaGold Corporation Fact Book 2014

Macraes Goldfield, New Zealand: Macraes Open Pit

The Macraes Goldfield is New Zealand’s largest gold producing operation and consists of the Macraes Open Pit and Frasers Underground mine with an adjacent process plant inclusive of an autoclave for pressure oxidation of the ore. OceanaGold’s mining and exploration permits at Macraes cover a contiguous area of 26,480 hectares. The Macraes mine is located 90 kilometres north of Dunedin in the Otago region of New Zealand’s South Island. It has been in operation since 1990 and the Macraes process plant has produced approximately 4.0 million ounces of gold (as at the end of March 2014).

Ore BodyThe Macraes ore body is located within a shallow dipping shear zone which dips 15 to 20 degrees to the Northeast and has a known strike extent in excess of 30 kilometres. Gold is mostly associated with sulphides, and occurs principally as microblebs within pyrite and arsenopyrite grains. This gold is refractory and is not readily recoverable by standard cyanidation methods. Frasers Stage 5, Frasers West and Frasers-Innes Mills are the only open pit stages currently being mined. As a result of the prolonged and sustained drop in the gold price, the Macraes mine plan was re-optimised in early 2014 and based on this plan, the Frasers 6 open pit cutback has been redesigned and a smaller cutback at Frasers 6 and Frasers-Innes Mills is planned to commence in the first half of 2014.

Mine Type

Open PitGold Resources (Moz)

4.65(M&I 3.15, Inferred 1.5)

Gold Reserves (Moz)

1.23Estimated Mine Life (Based on current life of mine plan)

2017Gold Production

90,000– 100,000(oz per annum)

Macraes prcoess plant, New Zealand, 6Mtpa mill primary grinding circuit

21Operations

New Zealand Mining Fleet

Macraes Quantity Gross Weight (tonnes)

Payload

Excavators 4 180-350 21-39 tonnes

Dump Trucks 10-18 250-318 147-191 tonnes

Water Trucks 2 59,000-130,000 L

Drills 4

Tracked Dozers 3

CAT Graders 2

Wheeled Dozers 1 69

Loaders 4 18-55 7-20 tonnes

Reefton Quantity Gross Weight (tonnes)

Payload

Excavators 3 170-180 21 tonnes

Dump Trucks 14 150-250 100-150 tonnes

Water Trucks 2 23-30 16-30 kL

Drills 2 22

Tracked Dozers 3 50-70

CAT Graders 2 30

Wheeled Dozers 1 47

Loaders 3 18-25 5-10 tonnes

The open pit mine will supply approximately 4.8 million tonnes of ore per annum to the process plant, while the Frasers Underground mine supplies a further 0.9 million tonnes of ore per annum. Stockpiles of ore provide supplementary feed when required and the Company plans to increase the processing of stockpiles from 2014 onwards. The current combined open pit, stockpile and underground reserves of 1.35 million ounces of gold support a mine life at Macraes of approximately eight years. Based on the current life of mine plan, the mine life is to the end of 2017.

Benches of 7.5 metres are drilled and are mined in three 2.5 metre flitches. Mine Technicians collect samples from the drill rig at 2.5 metre vertical intervals which are dispatched to an on-site laboratory for gold analysis. The Mine Geologists use the assay data, in conjunction with geological mapping, to create a 3D model of the grade distribution for each flitch. These models are used to delineate areas of ore and waste.

Explosives are used to loosen the rock prior to excavation by hydraulic diggers. In areas containing gold, Ore Spotters are employed to supervise the extraction of the ore. Dump trucks haul the ore to the Run of Mine (ROM) pad for processing to begin, whilst waste rock (rock that doesn’t contain gold) is hauled to “rock stacks”, designed to blend in with the surrounding landscape. The average Life of Mine strip ratio is approximately 10-12:1 however may fluctuate year on year depending on the mine plan and amount of pre-strip activity.

At Macraes, average mining cost including pre-strip, for the open pit is approximately US$1.60 – US$1.80 per tonne mined.

Operational Statistics (Macraes Goldfield operation statistics include Macraes Open Pit and Frasers Underground mines)

Macraes Goldfield 2013 2012 2011 2010 2009

Gold Produced (ounces) 198,820 169,609 174,851 182,759 213,049

Total Ore Mined (tonnes) 6,962,730 5,558,056 6,589,904 6,365,855 4,833,671

– Macraes Open Pit 6,081,774 4,830,969 5,742,884 5,446,063 3,927,997

– Frasers Underground 880,956 727,087 847,020 919,792 905,674

Ore Mined Grade (grams/tonne) 1.27 1.29 1.07 1.26 1.67

– Macraes Open Pit 1.18 1.14 0.90 1.02 1.40

– Frasers Underground 1.88 2.24 2.20 2.66 2.83

Total Waste Mined incl. pre-strip (tonnes) 38,725,444 36,363,043 44,407,352 43,944,947 48,578,180

Mill Feed (dry milled tonnes) 5,811,868 5,789,255 5,817,001 5,458,607 5,635,537

Mill Feed Grade (grams/tonne) 1.30 1.12 1.12 1.28 1.47

Recovery (%) 81.4 81.1 83.3 81.3 79.6

22 OceanaGold Corporation Fact Book 2014

Macraes Goldfield, New Zealand: Frasers Underground

Frasers Underground mine was developed to target down-dip extensions of the Hanging Wall shear mineralisation currently being mined in the Macraes Open Pit. The underground mine, which was commissioned in January 2008, is currently 625 metres below surface and 110 metres below sea level, with over 41 kilometres of developed tunnel drives.

Mining is focused on the higher grade, upper section of the Hanging Wall shear. Resource development drilling from jump up rises and stockpiles is ongoing and continues to extend mine life.

Ore BodyThe ore body is the down dip extension to Macraes, open at depth and sits on the Hanging Wall shear as well as along structurally lower, sub-parallel shears. Within Panel 2 of the Frasers Underground mine, the Hanging Wall shear mineralisation is typically between 5 and 10 metres thick.

MiningMining is performed using retreat long hole open stoping. Narrow pillars are left between the stope voids which are 15 metres wide and up to 200 metres long.

Production stoping occurs in the Hanging Wall shear and a second thinner mineralised shear, 10 to 20 metres beneath and sub-parallel to the Hanging Wall Shear.

The mine produces about 900,000 tonnes of ore per year using a highly mechanised mining fleet of electric/hydraulic powered drill rigs, large 50 tonne dump trucks and remote controlled loaders that enter the mining stopes that are too dangerous for personnel. In late 2012 the development of a fibre optic cable linked to the lower levels of the Frasers Underground allowed for remote bogging from a surface (above ground) facility.

The main entrance to the mine is a 5.0 metre wide by 6.0 metre high decline that spirals down beside the ore at a gradient of 1.0 vertical metre per 7.0 horizontal metres and access to the mining areas is by smaller 4.5 metre by 4.5 metre headings.

Fresh air, at a rate of 210 cubic metres per second is brought into the mine via the decline and a 350 metre long vertical shaft. A nearby escapeway shaft has a ladderway that provides an additional entry/exit point to the mine. A dewatering station pumps out water up to 17 litres per second. Other infrastructure underground include a refuelling station, emergency refuges, explosives magazine, pumping stations, electrical transformers, a lunch room and small workshops.

Mining costs at the underground mine are approximately US$45 per tonne of ore mined.

Mine Type

UndergroundGold Resources (Moz)

1.46(M&I 0.86, Inferred 0.6)

Gold Reserves (Moz)

0.12Estimated Mine Life (Based on current life of mine plan)

mid 2015Gold Production

40,000– 55,000(oz per annum)

Frasers Underground Mine, New Zealand

23Operations

Reefton Goldfield, New Zealand: Reefton Open Pit

Mine Type

Open PitGold Resources (Moz)

1.64(M&I 0.74, Inferred 0.9)

Gold Reserves (Moz)

0.19Estimated Mine Life (Based on current life of mine plan)

mid 2015Gold Production

50,000– 70,000(oz per annum)

Operational Statistics

Reefton Goldfield 2013 2012 2011 2010 2009

Gold Produced (ounces) 60,635 63,300 77,648 85,843 87,342

Total Ore Mined (tonnes) 1,687,342 1,314,630 1,513,789 1,539,609 1,425,135

Ore Mined Grade (grams/tonne) 1.47 1.56 1.80 2.11 2.46

Total Waste Mined incl. pre-strip (tonnes) 17,818,849 18,217,430 14,768,665 13,698,710 12,509,654

Mill Feed (dry milled tonnes) 1,478,349 1,643,120 1,771,353 1,622,881 1,278,176

Mill Feed Grade (grams/tonne) 1.57 1.48 1.67 2.01 2.60

Recovery (%) 81.1 80.6 81.4 82.5 81.5

The Reefton mine was commissioned in 2007 and comprised of a series of open pits developed along a major regional shear structure and its offshoots of which OceanaGold has 53,930 hectares under permit. It is located seven kilometres southeast of the township of Reefton a historic mining district in the West Coast region of New Zealand’s South Island.

Ore BodyMineralisation is hosted within a complex network of shears that typically dip at 60 degrees near-surface and shallow to 40 degrees at depth. Underground miners historically worked high grade quartz shoots, hosted within these shears. Proportions of these shoots remain as high grade pillars and are recovered via open pit mining at Globe. The main focus of the Globe Open Pit however is the enveloping network of shearing which hosts refractory gold within sulphides.

The ore zone varies in thickness between 2 metres and 30 metres and exhibits extensive lateral and vertical continuity.

MiningThe ore is supplied from one open pit which sits along the mineralised shear zone. The mining operation consists of the Globe Progress Open Pit which includes the General Gordon ore body. The pit is mined in various stages. The haul roads are designed at a 1:9 gradient to reduce the mining footprint. The topsoil is removed from disturbed areas and stored for use during the rehabilitation of the mine.

The ore is drilled for grade control & blast holes on a 5 metre by 5 metre pattern using RC drilling techniques. Additional blast holes are drilled separately. The ore is then blasted to a depth of 7.5 metres and mined selectively in 2.5 metre flitches to reduce ore loss and dilution.

The average Life of Mine strip ratio is approximately 8-10:1 however may fluctuate year on year depending on the mine plan and amount of pre-strip activity.

Reefton mining costs, including pre-strip are approximately US$2.60 to US$3.00 per tonne mined.

24 OceanaGold Corporation Fact Book 2014

Processing, New Zealand

OceanaGold currently operates two processing plants in New Zealand. At Macraes, the processing plant is situated within short distance of the open pit and includes a pressure oxidation plant for the processing of sulphide ore.

The Macraes process plant is capable of treating approximately 6 million tonnes of ore per annum which is put through crushing, grinding, flotation, fine grinding, pressure oxidation, carbon in leach (CIL), elution, electro winning and smelting. Refractory ore requires multistage processing to increase recoveries. Since 2007, flotation concentrate from the Reefton mine has been transported by rail and road to Macraes to utilise surplus autoclave capacity.

At the second processing plant in Reefton, the ore is put through crushing, grinding, flotation and concentrate dewatering. The processing plant is operating well above its name plate capacity of 1 million tonnes per annum with average throughput over the last three years of approximately 1.6 million tonnes per annum.

At Macraes, the Ball Mill Work Index is 12.5 kilowatt hours per tonne (kWh/t). At Reefton, the Crushing Work Index averages 11.6 kWh/t and the Ball Mill Work Index is 17.0 kWh/t.

Refractory gold concentrate produced from the Reefton processing plant is transported 600 kilometres by road, rail, and then road again to Macraes for treatment through the autoclave pressure oxidation and carbon in cyanide leaching to release the gold. Without this technology it would be hard to realise the value as direct leaching of refractory concentrate to obtain gold results in very poor recoveries.

The autoclave operates at pressure of 3,140 kilopascals and an average temperature of 225 degrees Celsius. Grind size is important to the oxidation kinetics and feed is finely ground with approximately 90% of the feed at 20 microns. The autoclave is designed for 50 minutes residence time targeting 98% oxidation however these targets vary with feed from Macraes and Reefton to optimise CIL recoveries.

Flotation recovery is approximately 88%, CIL recovery is around 93-95% with an overall recovery greater than 81% achieved over the last four years. Overall recovery improvement has been achieved through optimising autoclave oxidation rates and the passivation of preg-robbing species in the concentrate to produce better CIL recoveries.

The end product is a bar of doré bullion which is approximately 90% pure weighing 18-20 kilograms and containing around 600 gold ounces. The doré bars are sold and transported to the Perth (Australia) Mint for further refinement.

Routine maintenance is carried out at the process plants to ensure optimal throughput and efficiency. Sections of the plant are shutdown at different frequencies and duration to allow maintenance to be conducted. As a result, plant utilisation is approximately 95% of the year.

Processing costs for Macraes Open Pit and Frasers Underground are approximately US$9.00 to US$10.00 per tonne of ore milled. Reefton processing costs are approximately US$13.00 to US$14.00 per tonne ore milled and include transportation costs of approximately US$13.00 per ounce and Macraes processing charges. Macraes processes on average 50,000 tonnes of Reefton concentrate annually.

Run-of-MineOre

Run-of-MineOre

ROMBin

ROMBin

Ball Mills

EmergencyFeed

Grizzly

Unit Cells andCleaners

Cyclones

FloatTails

Mixed TailsDam

ElutionColumn

RegenKiln

BarrenCarbon

CIL 1CIL 2 CIL 3

CIL 4CIL 5

Tk-09

Gold Bullion

15m ConWashThickener

Loaded Carbon

Scats

Vent Scrubber

Autoclave

Autoclave Discharge Wash Thickeners

Flash Vessel

FloatTailCIL

Tail

Discharge Wash Solution

Macraes Con Storage

Inco Cyanide Kill Unit

RegrindMill

Limestone

Wash Water

Jaw

Mill 500

Mill 02

Mill 350

Rougher/scavengers3 X 300 m3 and 2 X 150 m3

³

Recleaners 6x16 m3

³

Cleaner-Scavengers5x38 m3

³

CIL 6

Reefton Con Storage

Storage Bin

Repulp

From Reefton

Isamill

CampaignTreatment

JawCrusher

SAGMill 01

Cleaners4x38 m3

ElectrowinningCells

BarringFurnace

Eluate

Flow diagram for Macraes processing plant

25Operations

El Dorado Project: El Salvador

El Dorado Project, El SalvadorOceanaGold acquired 100% of the advanced stage El Dorado Project in November 2013 through the acquisition of Pacific Rim Mining Corp. The project is located approximately 74 kilometres north east of the capital San Salvador (accessed by paved road) and 10 kilometres southwest of the town of Sensuntepeque. The El Dorado Project area covers 14,407 hectares of exploration licences and 1,275 hectares under an exploitation licence application and contains several prospects and deposits. The acquisition of the El Dorado Project aligns well with OceanaGold’s strategy to invest in high quality, low cost opportunities and utilise its proven mine developing capabilities and experience to advance the El Dorado Project. Permit applications for the El Dorado Project are currently outstanding.2

Ore BodyThe El Dorado licence area contains a number of mineralised quartz-carbonate vein systems that were formed as a result of near-surface hydrothermal activity. They are found in three districts, north, central and south, that are distinguished from each other by the dominant vein orientations and the level of the hydrothermal system that is exposed on the present-day surface. The gold and silver-rich veins, which typically contain less than 2% sulphides, have complex, multistage histories of formation.

The dimensions of mineralised veins are as varied as their exploration status, ranging from those known only in single outcrops to those that have been traced on the surface over lengths of between one and two kilometres. Systems of related veins are up to three kilometres long. In those veins that have been mined or extensively drilled, mineralisation has developed with vertical extents of approximately 500 metres. While broadly extensive and continuous, the veins can be geometrically complex at the mining scale. Geological detailed mapping has been completed over the entire project.

Mining in El Salvador The current Mining Law was enacted in 1996 and last amended in 2001. The Government owns all mineral rights and mining laws do not discriminate between nationals and foreigners. The Environmental Impact Study permit is issued by the Ministry of Natural Resources and Environment, and is a prerequisite for the Exploitation Concession permit which is issued by the Ministry of Economy. The Exploitation Concession permit holder must commence development activities within 12 months of the permit grant.

Community ProgramsThe Company conducts various programs for the local communities in El Salvador. The current programs include English and computer classes for children and adults and vocational skills training. A reforestation campaign involves field workers collecting local seeds for the nursery with over 3,500 trees planted each year. Over 70,000 trees have been planted in the last 20 years. The Company will continue these programs in 2014 and enhance its engagement with the local community.

Resources

1.60(M&I 1.30, Inferred 0.3) Moz Gold

11.38(M&I 9.48, Inferred 1.9) Moz Silver

1. Source: The World Factbook, CIA 2. In 2009, Pacific Rim filed an arbitration claim with the International Centre for the Settlement of Investment Disputes, seeking monetary compensation under the Investment Law of El Salvador. This followed the passive refusal of the Government of El Salvador to issue a decision on Pacific Rim’s application for environmental and mining permits for the El Dorado Project. As a result of the on-going arbitration action, the Company has not had the ability to confirm or renew any Salvadoran exploration licences. Please refer to “Other Projects”, “Risk Factors” and “Legal Proceedings” sections of the Company’s Annual Information Form dated March 31, 2014 for further information. The Company will continue to provide material updates on its website.

Language: Spanish

GDP: US$47 billion

Currency: US dollars

Population: 6.1 million

Capital: San Salvador

Republic of El Salvador1

Unemployment rate: 6.9%

El Dorado Project, El Salvador, community tree planting program

26 OceanaGold Corporation Fact Book 2014

Resource Development

OceanaGold’s resource development strategy is focused on discovery that has potential to extend the mine life at its operations.

In 2013, the Company invested US$6.7 million (2012 US$14.9 million) with the majority incurred in New Zealand. OceanaGold plans to invest a total of US$5 - US$10 million on resource development activities in 2014 in the Philippines and maintenance of the El Salvador exploration assets.

PhilippinesExploration in the Philippines focused on delineating potential copper and gold drill targets within the Financial or Technical Assistance Agreement (FTAA) area and adjacent OceanaGold controlled explorations permits.

The exploration activities are focused on identifying drilling targets within the broader FTAA area and on drilling near mine. The Company also conducted additional drilling of the Didipio ore body to better define the high grade zones.

In 2014, the Company plans to drill the near mine prospect of San Pedro and the broader FTAA area should the renewal of the FTAA exploration permits be granted.

Drilling at San Pedro prospect, 1.4 kilometres northwest of Didipio, will test for a porphyry copper-gold target beneath areas of extensive alluvial mine workings. Other areas of interest that can be tested by drilling when the FTAA exploration permit is granted include Mogambos, Papaya, and D’Fox prospects.

New Zealand

Macraes The Macraes mineral permits cover 35 kilometres of strike length of the gold mineralised Hyde-Macraes Shear Zone (HMSZ). During 2013 a successful application was made to NZPAM1 to extend the Mining Permit 41-064 over the Coronation deposit to enable mining in 2016. A geological review was also undertaken of prospective areas adjacent to OceanaGold’s current permit holding. This resulted in a prospecting permit application over the historic Lots Wife workings, located nine kilometres to the south east of the plant, which has the potential to host shallow open pitiable resources.

In 2013 the resource development drilling program consisted of 109 holes comprising 6,678 metres of reverse circulation drilling and 3,472 metres of diamond drilling spread across four prospects (Coronation, Deepdell, Frasers Open Pit and Frasers Underground). Following completion of the drilling, the resource estimates for the respective prospects were updated and resulted in modest resource increases for Coronation, Deepdell and Frasers Underground.

In 2014 surface exploration will focus on reviewing current resource estimates in conjunction with optimisation studies to determine the most effective places to drill in order to continue the process of converting resources to reserves. Resource development drilling in the Frasers Underground will continue on an intermittent basis as and when drilling platforms become available.

Historically at Macraes the Round Hill and Golden Point prospects were mined on an intermittent basis until 1953 for gold and tungsten. In the early 1980s these areas were initially being explored by Homestake and BP Minerals (NZ) Ltd for the tungsten potential. The change to gold exploration was triggered by the rapid rise of the gold price in the mid 1980s. In recent years the price of tungsten has increased significantly and as a result OceanaGold, in 2013 commenced a program of re-assaying assay pulps derived from the 25 years of drilling at Macraes. This work will continue in 2014 leading to an updated gold and tungsten resource estimate for Round Hill, a pre-feasibility study on the commercial production of a tungsten concentrate and an initial assessment of other prospects tungsten potential in the HMSZ.

ReeftonIn 2013, resource development at Reefton focused on greenfields and brownfields drilling with programs near the historic Blackwater Mine and the Globe Progress Mine. A total of 18 diamond drill holes for 3,701 metres were completed.

The deep-drilling program at Blackwater to test the continuity of mineralisation below the historic workings and to delineate an inferred resource of approximately 500,000 ounces, was completed in January 2013. The deep-drilling program and subsequent historical data reviews resulted in an increase in the Blackwater Inferred resource by 0.25 Moz to 0.9Mt @ 23 g/t Au for 0.7 Moz of gold. The Blackwater technical study investigating re-opening the mine is near completion with a decision expected in the first half of 2014.

In 2014, resource development activities at Reefton will focus on consolidating the understanding of the Reefton Goldfield though analysis of recently collected data and historical information. Additionally, various mapping and sampling programs will be undertaken with an objective of identifying new targets for follow-up.

1. NZPAM = New Zealand Petroleum and Minerals (the government organisation charged with managing the New Zealand mineral permits regime)

27Operations

Reserves & Resources

As OceanaGold’s main listing is on the Toronto Stock Exchange, the Company adopts the Canadian Institute of Mining NI 43-101 listing requirement of publishing its resource inventory.

As at 31 December 2013, OceanaGold had a total Measured and Indicated Mineral Resources of 8.34 million ounces of gold, 9.48 million ounces of silver and 260,000 tonnes of copper. This includes Mineral Reserves of 3.14 million ounces of gold and 210,000 tonnes of copper. The tables below summarise the Company’s Mineral Resource and Mineral Reserve inventories as at December 31, 2013. The Mineral Resources stated include the Mineral Reserves. Please refer to www.oceanagold.com for full Reserves and Resource statement.

Resource Statement as at December 31, 2013

Resource Measured Indicated Note: all resources are inclusive of reserves.

1. OceanaGold retains a 40% interest in the Sams Creek project in the South Island of New Zealand. The project contains a total of 10.1 Mt @ 1.77 g/t Au for 575 koz Indicated resource, as well as 10 Mt @ 1.3 g/t Au for 440 koz of Inferred resource. 40% of the total Sams Creek inventory has been included in OceanaGold’s resource table. The project is not considered material to OceanaGold at this time.

2. 0.47 g/t EqAu cut-off above the 2,390mRL and 1.5 g/t cut-off below the 2,390mRL. No resource reported below 2,180mRL. EqAu cut-off is gold equivalent based on US$1,450/oz gold and US$3.0/lb copper.

3. The El Dorado Project is not considered material at this time. Please refer to www.oceanagold.com for the press release dated October 8, 2013 for more details on the status of the permit applications and arbitration for the El Dorado Project as at the end of 2013. El Dorado resource cut-offs are based on 2008 assumptions of US$980/oz gold and US$20/oz silver.

For Macraes and Reefton (which have shorter projected mine lives than Didipio) resource cut-offs are based on US$1,250/oz gold.

Area Mt Au g/t Au Moz

Ag g/t Ag Moz

Cu % Cu Mt Mt Au g/t Au Moz

Ag g/t Ag Moz

Cu % Cu Mt

Macraes Total 31.7 1.24 1.26 85.6 1.00 2.75

Reefton Total 2.0 1.70 0.11 13.5 1.46 0.63

Sams Creek1 4.0 1.77 0.23

Didipio Total2 18.0 1.26 0.73 0.51 0.09 43.0 0.96 1.33 0.39 0.17

El Dorado Total3 0.8 11.30 0.28 75.7 1.90 3.5 9.00 1.01 67.5 7.58

Total Resource 52.4 1.41 2.38 1.90 0.09 149.7 1.24 5.96 7.58 0.17

Resource Measured & Indicated Inferred Resource

Area Mt Au g/t Au Moz

Ag g/t Ag Moz

Cu % Cu Mt Mt Au g/t Au Moz

Ag g/t Ag Moz

Cu % Cu Mt

Macraes Total 117.3 1.06 4.01 65.0 1.0 2.1

Reefton Total 15.5 1.50 0.74 7.8 3.7 0.9

Sams Creek1 4.0 1.77 0.23 4.2 1.3 0.2

Didipio Total2 61.0 1.05 2.06 0.42 0.26 14.7 0.6 0.3 0.2 0.03

El Dorado Total3 4.3 9.42 1.30 69.0 9.48 0.8 9.4 0.3 71 1.9

Total Resource 202.1 1.28 8.34 9.48 0.26 92.4 1.3 3.7 1.9 0.03

Reserve Statement as at December 31, 2013

Reserve Proven Probable Total ReserveFigures are in-situ delivered to ROM. Macraes and Reefton cut-offs are based on US$1,250/oz gold (0.4 g/t Au for Macraes Open Pit, 0.5 g/t Au for Reefton and 2.1 g/t Au cut-off for Frasers Underground). Didipio cut-offs are Net Metal Value based, using US$1,250/oz gold and US$3.25/lb copper (0.55 g/t AuEq for open pit and 1.9 g/t AuEq for underground).

Area Mt Au g/t Au Moz

Cu % Cu Mt Mt Au g/t Au Moz

Cu % Cu Mt Mt Au g/t Au Moz

Cu % Cu Mt

Macraes 21.2 1.00 0.68 20.8 1.01 0.68 42.0 1.00 1.35

Reefton 0.9 1.53 0.04 3.3 1.40 0.15 4.2 1.43 0.19

Didipio 16.7 1.23 0.66 0.52 0.09 29.0 1.00 0.93 0.42 0.12 45.6 1.09 1.59 0.46 0.21

Total 38.8 1.11 1.38 0.09 53.2 1.03 1.76 0.12 91.9 1.06 3.14 0.21

Mineral Reserves

GO

LD A

ND

GO

LD E

QU

IVA

LEN

T M

oz

0

1

2

3

4

5

6

DEC

201

3

DEC

201

2

DEC

201

1

DEC

201

0

DEC

200

9

DEC

200

8

28 OceanaGold Corporation Fact Book 2014

Sustainability

As the Company’s transformation into a mid-tier, multinational gold producer continued in 2013, we worked hard to deliver positive results across our business and looked for opportunities to further improve upon our social licence to operate.

Our sustainability programs are designed to meet the growing needs of our valued stakeholders. Their involvement in our activities and satisfaction with what we do is the cornerstone of our success and development. We have a staunch commitment to making sure our operations enrich, empower and improve the lives of our stakeholders, by creating a positive, long-lasting legacy that respects human rights and delivers enduring benefits and opportunities beyond the life cycle of our operations.

With over 23 plus years of operating sustainably in New Zealand and more recently in the Philippines, the Company expanded its footprint into the Americas in El Salvador. As we continue to grow, our ability to advance sustainability programs and deliver economic benefit grows too. Didipio has demonstrated this, where the direct and indirect benefits it contributes to the Philippine economy has made it a significant economic driver in the region.

Our vision underpins our projects and programs, ensuring we never take for granted the importance of our social licence or lose sight of the fact that sustainable development is an ongoing journey requiring continued review and improvement and close collaboration with our stakeholders.

As a growing, multinational company that is seeking to be the partner, employer and gold company of choice, we have a responsibility to set the bar high, to lead by example and pursue best practice sustainable development across our business where possible. The key to our vision is our core corporate values of respect, integrity, teamwork, innovation, action and accountability and is executed by our strong, diverse workforce.

Macraes Goldfield, New Zealand, water quality sampling at Lone Pine water storage dam

29

2013 Sustainability Highlights

> Developed a new set of corporate sustainability performance targets

> Established a Sustainability Steering Committee to drive sustainable development programs including full adoption of the Equator Principles by the end of 2014

> Awarded ‘Most Environment Compliant’ industry by Philippines Department of Environment and Natural Resources

> Increased water recycled across all operations> Reduced waste to landfill across all operations> Over 98% Filipino workforce at the Didipio operations,

including over 50% from the local communities> Used 100% Philippines and 80% New Zealand based

contractors> Worked 8.8 million man hours at Didipio with no

Lost Time Injury> Reduced total company LTIFR (Lost Time Injury

Frequency Rate) to 1.0 from 1.76 in previous year> Increased the female proportion of the total workforce

to 18% from 13% in 2013

Operations

Didipio Mine, Philippines, water quality monitoring upstream of Didipio

30 OceanaGold Corporation Fact Book 2014

Reefton process plant, New Zealand; feed hopper and conveyor, primary crusher, conveyor through to grinding mill, flash flotation circuit (foreground) and final ore concentrate storage hopper (middle background)

31Section title

Focused on profitability

Financials and Investor Information

31

32 OceanaGold Corporation Fact Book 2014

Five Year Financial Summary

Statement of Operations US$Year Ended 31 December

2013$’000

2012$’000

2011$’000

2010$’000

2009$’000

Gold sales 553,612 385,448 395,609 305,638 237,057

Cost of sales, excluding depreciation and amortisation (260,651) (226,039) (216,789) (150,697) (121,310)

General & administration (28,423) (14,911) (14,537) (13,805) (9,179)

Foreign currency exchange gain/(loss) 1,267 (961) 320 (961) (24)

Other income/(expense) (3,445) 1,095 (680) (660) (366)

EBITDA1 262,360 144,632 163,923 139,515 106,178

Depreciation and amortisation (129,315) (91,376) (85,822) (69,337) (66,181)

Net interest expense and finance costs (26,978) (21,510) (12,909) (14,780) (14,389)

Earnings/(loss) before income tax1 106,067 31,746 65,192 55,398 25,608

Tax (expense) on earnings/loss (13,290) (11,426) (21,025) (22,638) (11,865)

Earnings/(loss) after income tax1 92,777 20,320 44,167 32,760 13,743

Impairment charge (193,300) - - - -

Gain/(loss) on fair value of undesignated hedges (2,083) 503 - 16,215 58,241

Tax (expense) / benefit on gain/loss on undesignated hedges and impairment charge

54,749 (151) - (4,540) (17,472)

Net profit/(loss) (47,857) 20,672 44,167 44,435 54,512

Net Earnings per Share US$

Basic earnings/(loss) per share $(0.16) $0.08 $0.17 $0.20 $0.32

Diluted earnings/(loss) per share $(0.16) $0.08 $0.17 $0.20 $0.29

Weighted average no. of shares for diluted EPS (‘000) 298,908 296,250 307,023 270,999 214,192

Cash Flows

Cash flows from Operating Activities 159,429 115,253 154,555 52,260 94,183

Cash flows from Investing Activities (158,812) (294,548) (146,595) (107,809) (71,013)

Cash flows from Financing Activities (83,190) 108,919 (16,110) 186,798 2,933

Balance Sheet as at 31 December 2013 2012 2011 2010 2009

Cash and Cash Equivalents 24,788 96,502 169,989 181,328 42,423

Other Current Assets 126,400 89,276 56,491 47,320 30,032

Non Current Assets 745,368 845,878 591,155 477,568 433,541

Total Assets 896,826 1,031,656 817,635 706,216 505,996

Current Liabilities 129,478 199,413 123,623 63,091 185,061

Non Current Liabilities 175,618 222,383 215,772 209,984 138,656

Total Liabilities 305,096 421,796 339,395 273,075 323,717

Total Shareholders’ Equity 591,730 609,860 478,240 433,141 182,279

OceanaGold’s financial year end is 31 December and the Company’s financial information is presented in United States dollars (“US$”), unless otherwise stated. 1. Excluding gain / (loss) on undesignated hedges and impairment charge

33Financial and Investor Information

Operating Costs

OceanaGold’s operating cash cost per ounce of gold sold decreased significantly from US$940 in 2012 to US$426 per ounce net of by-product credits in 2013 reflecting the commencement of commercial production of the Didipio Mine on April 1, 2013. All-In Sustaining Costs (“AISC”) (per the World Gold Council methodology) for 2013 were US$868 per ounce of gold sold.

Didipio cash costs over the life of mine after copper by-product credits are expected to be significantly lower than OceanaGold’s New Zealand operations. Prior to commercial production, operating costs net of any revenue received at the Didipio Mine were capitalised to the balance sheet and will be amortised against future production which will be reflected in the income statement.

At Didipio, electricity is currently being sourced from diesel powered generators and represents a high proportion of operating costs at approximately US$0.28 per kilowatt hour. OceanaGold is currently reviewing possible connectivity to the power grid which is expected to reduce power (diesel) costs. In New Zealand, electricity is sourced from the electricity transmission network grid of which approximately 75% is derived from renewable (mainly hydro, also geothermal and wind) sources. Power prices excluding line and network charges average approximately NZD2-15c per kilowatt hour.

As OceanaGold reports its financial results in United States Dollars (“USD”), the foreign exchange rate used for translation may have a material impact on the reported costs. Cash spent on pre-stripping is capitalised in the balance sheet and amortised against future production in the profit and loss statement.

RoyaltiesIn New Zealand (for Macraes and Reefton), royalties to a maximum of 1% ad valorem or 5% of accounting profits, whichever is greater, are payable to the Crown annually. At Macraes, OceanaGold pays a 5% gross smelter royalty to O.W. Hopgood for gold production from a former permit area held by O.W. Hopgood over Round Hill. Most of the Reefton Project permits are also subject to a royalty agreement with Royalco Resources Limited (“Royalco”).

For the Reefton mine, a royalty based on the NZD gold price applied until the mine produced 400,000 ounces, a milestone the Company achieved in third quarter 2012. Production from other resources in the Reefton Project attracts an annual royalty of between 1% and 3% of gold produced according to the gold price at the time the royalty is due. The royalty reverts to 1.5% of annual gold production from all of the Reefton Project permits once an aggregate of 1,000,000 ounces of gold is produced. Based on the current forecast mining schedule, this royalty will not be applicable.

In 2013, royalties represented less than 1% of New Zealand gold sales. Going forward royalties for the New Zealand operations are expected to be lower.

In the Philippines the local claim owner syndicate is entitled to a 2% net smelter return (NSR) royalty on production. An additional royalty of 0.6% of 92% NSR (capped at a total of A$13.5 million) is payable to a third party.

Royalties are included in the reported cash cost amounts.