november 2016 cav: the road ahead - clorosurclorosur.org/seminar2016/presentation/17/01-ihs.pdf ·...

TRANSCRIPT

CAV: THE ROAD AHEAD

NOVEMBER 2016

Hazel Kreuz, Global Director, Chlor-Alkali/Vinyls

+1 832 619 8592

© 2016 IHS. ALL RIGHTS RESERVED.

Prepared for Clorosur 2016 Buenos Aires, Argentina

© 2016 IHS. ALL RIGHTS RESERVED.

About IHS Markit IHS Markit thinks about the world in a unique way.

We call this The New Intelligence.

IHS Markit’s singular ability to look across complex industries, financial markets, and

government actions that drive the global economy and provide our customers with insights,

perspective and solutions for what really matters.

Energy Chemical Automotive Financial Markets

Product Design Technology, Media &

Telecom

Maritime & Trade Aerospace,

Defense & Security

2

© 2016 IHS. ALL RIGHTS RESERVED.

Discussion

Agenda

1. Economic outlook

2. Directions for Chlor-alkali

3. The PVC road ahead

4. Key take-aways

LG Chem / November 2016

© 2016 IHS. ALL RIGHTS RESERVED.

LG Chem / November 2016

Economic Outlook: What train are we on?

© 2016 IHS. ALL RIGHTS RESERVED.

Global economic growth remains subdued

• Global growth will stay below 3% in 2017 as slowdowns in Europe and

China offset accelerations in the United States and emerging markets.

• US economic growth will pick up from 1.4% in 2016 to 2.2% in 2017,

led by growth in consumer spending and business fixed investment.

• Economic and political uncertainty will hurt UK investment, consumer

spending, and capital inflows in the year ahead.

• Eurozone growth is projected to slow from 1.6% in 2016 to 1.3% in

2017, reflecting increased political instability and banking problems.

• China’s economic growth will slow further because of

imbalances in credit, housing, and industrial markets.

• Deep recessions in Brazil and Russia are ending.

LG Chem / November 2016

© 2016 IHS. ALL RIGHTS RESERVED.

-2

0

2

4

6

NAFTA OtherAmericas

WesternEurope

EmergingEurope

Mideast-N. Africa

Sub-Saharan

Africa

Japan OtherAsia-

Pacific

An

nu

al

perc

en

t ch

an

ge

2015 2016 2017 2018 2019–23

Asia-Pacific (excluding Japan) will achieve the fastest

growth in real GDP

LG Chem / November 2016

Real GDP

Source: IHS © 2016 IHS

© 2016 IHS. ALL RIGHTS RESERVED.

Latin America – 3 Regions on 2 Continents With

Significant Potential

South

America

North

America

-12.0

-9.0

-6.0

-3.0

0.0

3.0

6.0

9.0

12.0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Latin America

World

Brazil

Mexico

Argentina

Venezuela

Colombia

% GDP Growth

• Large market with 640 Million of

finished goods consumers

• Mid America: MEX, VEN, COL

• East of Andes: BRA, ARG

• West of Andes: CHL, PER

LAPPC / November 2016

7

© 2016 IHS. ALL RIGHTS RESERVED.

Real GDP Growth in South America

8

LAPPC / November 2016

-12

-9

-6

-3

0

3

6

Brazil Argentina Venezuela Colombia Chile Peru

2015 2016 2017 2018 2019–23

© 2016 IHS

An

nu

al

Pe

rce

nt

Ch

an

ge

Source: IHS

© 2016 IHS. ALL RIGHTS RESERVED.

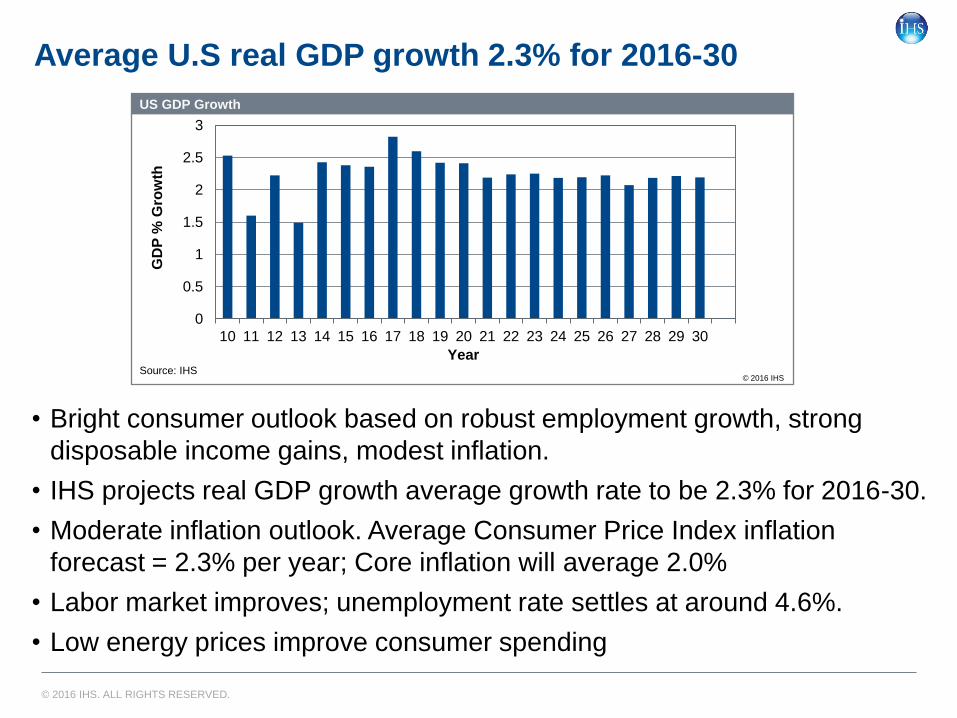

Average U.S real GDP growth 2.3% for 2016-30

• Bright consumer outlook based on robust employment growth, strong

disposable income gains, modest inflation.

• IHS projects real GDP growth average growth rate to be 2.3% for 2016-30.

• Moderate inflation outlook. Average Consumer Price Index inflation

forecast = 2.3% per year; Core inflation will average 2.0%

• Labor market improves; unemployment rate settles at around 4.6%.

• Low energy prices improve consumer spending

0

0.5

1

1.5

2

2.5

3

10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30

US GDP Growth

Source: IHS

GD

P %

Gro

wth

Year

© 2016 IHS

© 2016 IHS. ALL RIGHTS RESERVED.

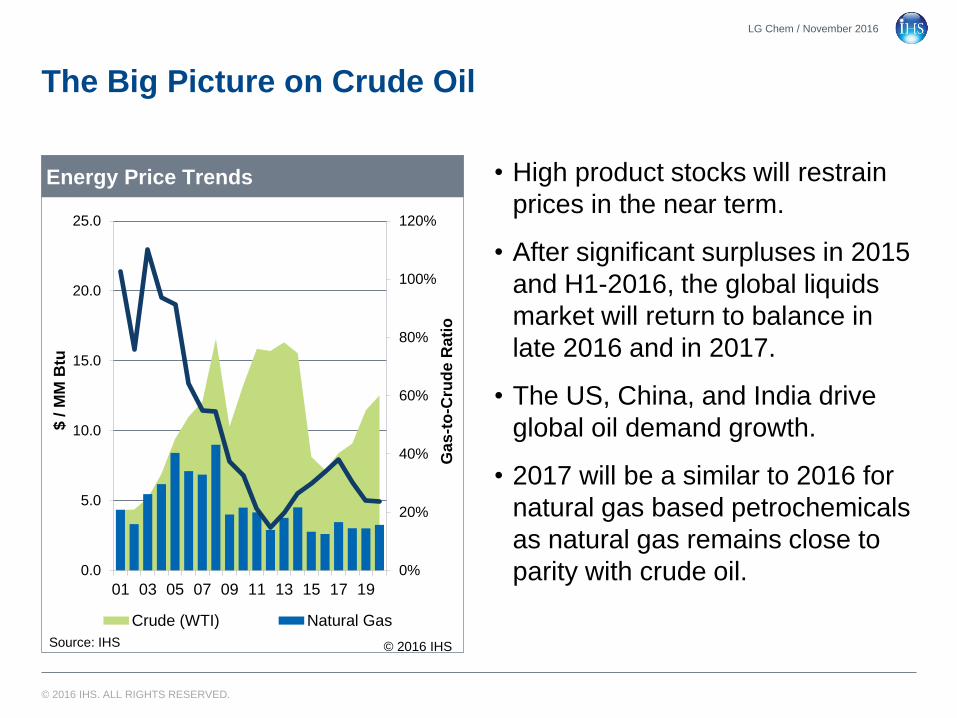

The Big Picture on Crude Oil

0%

20%

40%

60%

80%

100%

120%

0.0

5.0

10.0

15.0

20.0

25.0

01 03 05 07 09 11 13 15 17 19

Crude (WTI) Natural Gas

Energy Price Trends

Source: IHS

$ / M

M B

tu

Ga

s-t

o-C

rud

e R

ati

o

© 2016 IHS

• High product stocks will restrain

prices in the near term.

• After significant surpluses in 2015

and H1-2016, the global liquids

market will return to balance in

late 2016 and in 2017.

• The US, China, and India drive

global oil demand growth.

• 2017 will be a similar to 2016 for

natural gas based petrochemicals

as natural gas remains close to

parity with crude oil.

LG Chem / November 2016

© 2016 IHS. ALL RIGHTS RESERVED.

LG Chem / November 2016

The Chlor-Alkali Market: Picking up the pace

© 2016 IHS. ALL RIGHTS RESERVED.

North America Caustic Supply Consolidation

14,500

15,000

15,500

16,000

16,500

0

20

40

60

80

100

2010 2015 2016 Pre A/WMerge

2016 Post A/WMerge

Axiall Dow Dow/Mitsui FPC Georgia Gulf

Olin OxyChem PPG Shintech Sunbelt

Westlake Others Total Capacity

North America Caustic Capacity

Source: IHS © 2016 IHS

Pe

rce

nta

ge

Th

ou

sa

nd

Me

tric

To

ns

© 2016 IHS. ALL RIGHTS RESERVED.

Higher Asset Utilization In Chlor-Alkali Will Drive

Improved Profitability By 2020

13

50%

60%

70%

80%

90%

100%

0.0

20.0

40.0

60.0

80.0

100.0

10 11 12 13 14 15 16 17 18 19 20 21

Demand Total Capacity Operating Rate

World: Caustic Soda Supply & Demand

Source: IHS © 2016 IHS

Op

era

tin

g R

ate

Millio

n D

ry M

etr

ic T

on

s

• Global operating rates currently

below 80%; China operating

rates below 70%

• No significant capacity increases

on the horizon beyond 2017

• EU mandate to close or convert

mercury cell plants reduce

capacity

• Steady demand growth over the

forecast period raises operating

rates to upper 80’s% in forecast

period; some regional operating

rates will be > 90%

© 2016 IHS. ALL RIGHTS RESERVED.

Global Surplus Caustic Capacity To Decline Due

To Limited Capacity Growth

14

0%

5%

10%

15%

20%

25%

30%

35%

0

5

10

15

20

25

30

35

90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20 22

Excess Capacity Over Demand Excess as % of Demand

Average Excess as % of Demand, 90-07' Average Excess as % of Demand, 08-22'

Global Caustic Soda Excess Capacity

© 2016 IHS

Ex

ce

ss

Ca

pa

cit

y, M

illio

n M

etr

ic T

on

s

Source: IHS

Ex

ce

ss

as

a %

of

De

ma

nd

© 2016 IHS. ALL RIGHTS RESERVED.

USGC ECU Economics Improve with Higher Asset

Utilization

Caustic Prices Provide Majority of Earnings Contribution

-200

0

200

400

600

-220

0

220

440

660

09 10 11 12 13 14 15 16 17 18 19 20 21

Do

lla

rs P

er

Sh

ort

To

n

Do

lla

rs P

er

Me

tric

To

n

ECU Value from Chlorine (Asset-sharing) ECU Value from Caustic

ECU Value ECU Cash Margin

US Gulf Coast Chlor-Alkali Annual ECU Economics

Source: IHS © 2016 IHS

15

© 2016 IHS. ALL RIGHTS RESERVED.

Global Crude Prices Recover as Oil Supply/Demand

Balances Tighten

0

30

60

90

120

0

5

10

15

20

10 11 12 13 14 15 16 17 18 19 20 21

Crude Oil vs. Natural Gas

Natural Gas WTI Brent

Global Crude Oil vs. USGC Natural Gas

Source: IHS © 2016 IHS

$/B

arre

l, Cru

de

$/ M

MB

tu,

Natu

ral G

as

• Demand growth of 1.1-1.5 MMb/d from

2016-20 underpins oil market outlook.

• Oil prices remain low enough to force US

crude production lower.

• OPEC production remains high and surplus

capacity available from OPEC falls to

extremely low levels.

• Driven by power and LNG exports, North

American gas demand reaches 105 Bcf/d

by 2020, but….

• N. American gas supply is plentiful and low

cost. Rapid demand growth leads to higher

natural gas prices, but remain under $4 per

MMBtu

16

© 2016 IHS. ALL RIGHTS RESERVED.

US Gulf Coast & China ECU Advantage Driven By Low

Cost Energy

0

100

200

300

400

500

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

USGC Diap NEA Memb WEP Memb/Merc ChinaNotes: * NEA Excludes China

Global ECU Cash Cost

Source: IHS © 2016 IHS

U.S

. D

oll

ars

Pe

r M

etr

ic T

on

17

© 2016 IHS. ALL RIGHTS RESERVED.

ECU Cash Cost Curve

North America has a sustainable advantage under current energy scenario

Brent

Crude

USGC

Natural Gas

($/Bbl) ($/MM Btu)

43 2.39

MDE Avg

NAM Avg NEA Avg WEP Avg

0

200

400

600

800

1000

0.0 20.0 40.0 60.0 80.0

World Cost Curve: ECU World Cost Curve: ECU

Cumulative Production - MMT

World Cost Curve: ECU World Cost Curve: ECU World Cost Curve: ECU World Cost Curve: ECU World Cost Curve: ECU World Cost Curve: ECU World Cost Curve: ECU World Cost Curve: ECU World Cost Curve: ECU World Cost Curve: ECU World Cost Curve: ECU World Cost Curve: ECU World Cost Curve: ECU 2016 World Cost Curve: ECU

Do

lla

rs P

er

Me

tric

To

n

Source: IHS © 2016 IHS

MDE Avg

NAM Avg

NEA Avg

WEP Avg

0

200

400

600

800

1000

0.0 20.0 40.0 60.0 80.0 100.0

2019 World Cost Curve: ECU

Do

lla

rs P

er

Me

tric

To

n

Source: IHS © 2016 IHS

Cumulative Production - MMT

Brent

Crude

USGC

Natural Gas

($/Bbl) ($/MM Btu)

71 2.95

18

© 2016 IHS. ALL RIGHTS RESERVED.

-1

0

1

2

3

4

5

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0

NEA xChina WEP NAM

Indexed CAV ROI trend with time (NAM 2000 as 1)

Source: IHS © 2016 IHS

Shale Gas Driving ROI Advantage

19

ERCO Port Edwards Day / September 2016

© 2016 IHS. ALL RIGHTS RESERVED.

Mercury Phase-out Impact on European Capacity

Will Help Improve Industry Asset Utilization

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

2010 2012 2014 2016 2018 2020

Diaphragm cell Diaphragm Abestos cell

Membrane cell Mercury cell

Others

European Chlorine Capacity

© 2016 IHS

MM

T

Source: IHS

• Net Capacity loss ≈ 1 dmt

• Capacity loss limited by several

membrane plants expansion:

• Akzo (Frankfurt)

• BASF (Ludwigshafen)

• Rokita (Brzeg Dolny)

• Spolchemie, CABB, ICL

• Some conversion delays expected

• Asbestos extension and

conversion

20

© 2016 IHS. ALL RIGHTS RESERVED.

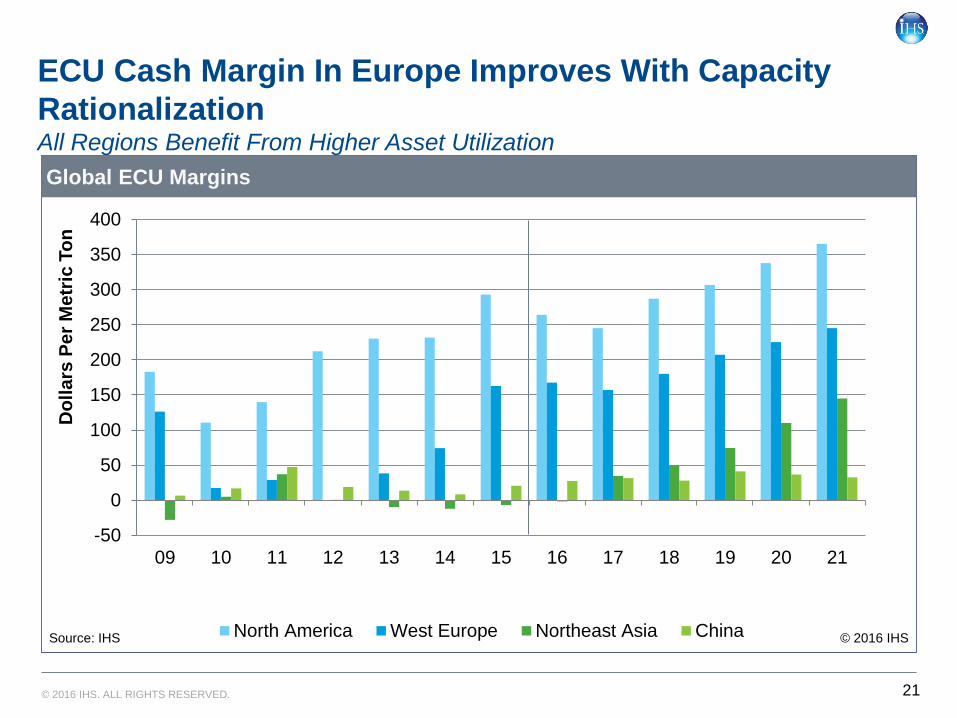

ECU Cash Margin In Europe Improves With Capacity

Rationalization All Regions Benefit From Higher Asset Utilization

-50

0

50

100

150

200

250

300

350

400

09 10 11 12 13 14 15 16 17 18 19 20 21

Do

lla

rs P

er

Me

tric

To

n

North America West Europe Northeast Asia China

Global ECU Margins

Source: IHS © 2016 IHS

21

© 2016 IHS. ALL RIGHTS RESERVED.

US Caustic Trade Reflects Global Cost Advantage

• 2Q 2016: Record USGC

exports

• Net exports must increase to

handle the additional caustic

generated by chlorine chain

exports

• Imports on North America’s

East coast will decline

• Growing exports become a

more significant percentage

of output

22

ERCO Port Edwards Day / September 2016

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

10 15 20

Imports Exports Net Trade

United States: Caustic Soda Trade

Source: IHS © 2015 IHS

Forecast

Millio

n M

etr

ic T

on

s

Exports

Imports

© 2016 IHS. ALL RIGHTS RESERVED.

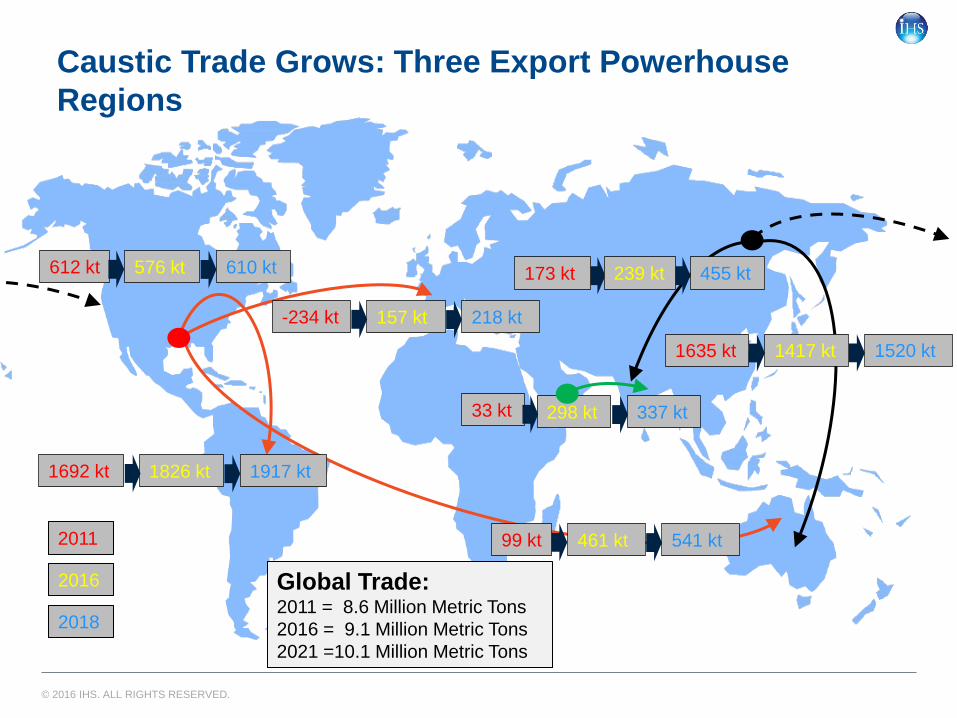

Caustic Trade Grows: Three Export Powerhouse

Regions

Global Trade: 2011 = 8.6 Million Metric Tons

2016 = 9.1 Million Metric Tons

2021 =10.1 Million Metric Tons

2016

2018

2011 461 kt 541 kt 99 kt

157 kt 218 kt -234 kt

1826 kt 1692 kt 1917 kt

298 kt 337 kt 33 kt

576 kt 612 kt 610 kt

1520 kt 1635 kt 1417 kt

455 kt 239 kt 173 kt

© 2016 IHS. ALL RIGHTS RESERVED.

Near-to-Medium Term Chlor-Alkali Take-Aways

• US cost advantage (energy and ethylene) declined near term with lower oil; expected to

recover with rising oil and steady gas prices, and higher utilization.

• Trade flow shifts Europe becomes net importer; US poised to increase caustic and vinyls

exports; South America imports increase from the US

• Merger & acquisition activity continues as the global market consolidates(Olin/Dow,

INOVYN/VYNOVA, Westlake/Axiall, Solvay/Unipar Carbochloro)

24

• New US capacity requires higher vinyls and caustic

exports

• Availability of ethylene becoming a potential limiting

factor for merchant US buyers. Ethylene integration in

the US remains key question.

• Europe is high cost but with modern C-A industry

and higher utilization and margins post 2017; note risk

of currency movement on export strategy.

• Asia has high cash cost and excess capacity.

China is self-sufficient in PVC production – crude to

coal ratio will play a role in domestic asset utilization

© 2016 IHS. ALL RIGHTS RESERVED.

PVC: The Road Ahead

LG Chem / November 2016

© 2016 IHS. ALL RIGHTS RESERVED.

Global Ethylene Prices US moves up: higher cash cost on ethane feed and spot price increases

LG Chem / November 2016

400

600

800

1,000

1,200

1,400

1,600

1,800

14 M M J S N 15 M M J S N 16 M M J S N 17 M M J S N 18 M M J S N

US Average Acquisition Price WEP Contract Price SEA CFR Spot Price

Global Monthly Ethylene Prices

Source: IHS © 2016 IHS

Do

lla

rs P

er

Me

tric

To

n

© 2016 IHS. ALL RIGHTS RESERVED.

Timely Start-up of Ethylene Crackers is Critical

LG Chem / November 2016

----

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2016 2017 2018 2019 2020

Mexico US

New Ethylene Capacity in NAM

Source: IHS © 2016 IHS

Th

ou

sa

nd

Me

tric

To

ns

* Capacity is prorated depending on startup date.

© 2016 IHS. ALL RIGHTS RESERVED.

Higher PVC Operating Rates as Capacity Stabilizes

LG Chem / November 2016

50%

60%

70%

80%

90%

100%

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

11 12 13 14 15 16 17 18 19 20 21 26

Demand (2.6/3.0) Total Capacity (2.1/1.3) Operating Rate

World: PVC Supply & Demand

Source: IHS © 2016 IHS

(% AAGR = 11-16/16-26)

Millio

n M

etr

ic T

on

s

Op

era

tin

g R

ate

© 2016 IHS. ALL RIGHTS RESERVED.

PVC Trade Grows, More Intra-Region Flow

1,164 kt

612 kt

511 kt

292 kt 515 kt 180 kt

465 kt

950 kt

535 kt

260 kt 570 kt 300 kt

1,450 kt

500 kt

2015

2018 Trade: 2015 = 8.6 Million Metric Tons

2018 = 8.9 Million Metric Tons

© 2016 IHS. ALL RIGHTS RESERVED.

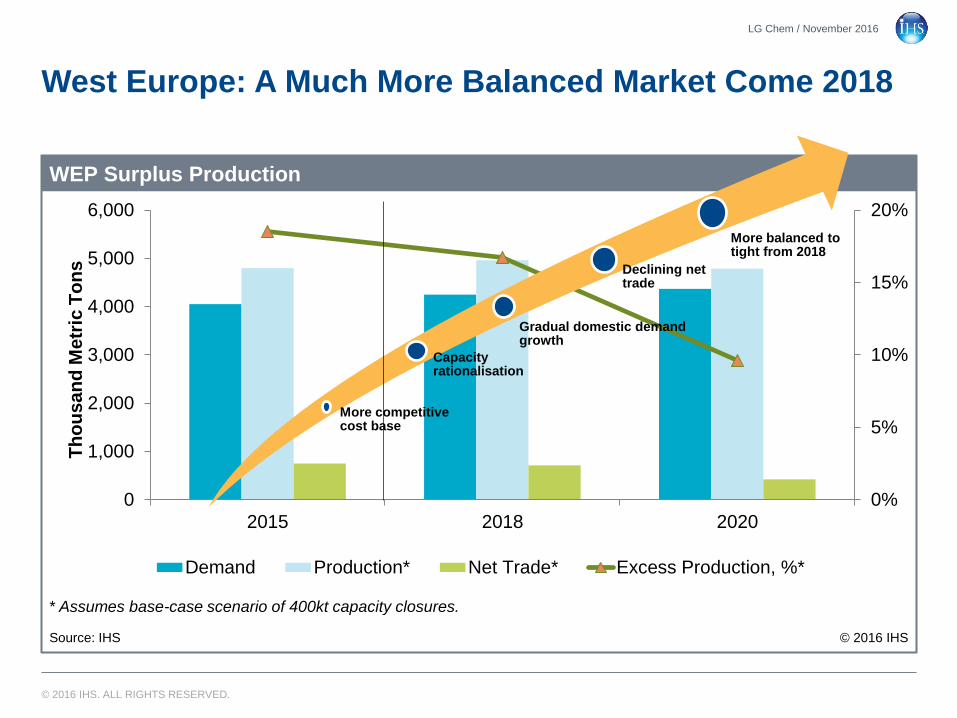

West Europe: A Much More Balanced Market Come 2018

0%

5%

10%

15%

20%

0

1,000

2,000

3,000

4,000

5,000

6,000

2015 2018 2020

Demand Production* Net Trade* Excess Production, %*

WEP Surplus Production

Source: IHS

* Assumes base-case scenario of 400kt capacity closures.

© 2016 IHS

Th

ou

sa

nd

Me

tric

To

ns

More competitive cost base

Capacity rationalisation

Gradual domestic demand growth

Declining net trade

More balanced to tight from 2018

LG Chem / November 2016

© 2016 IHS. ALL RIGHTS RESERVED.

PVC Global Prices: From Downhill To Uphill

LG Chem / November 2016

600

800

1,000

1,200

10

11

12

13

14

15

16

17

18

19

20

US

Do

lla

rs P

er

Me

tric

To

n

U.S. Netback West Europe Netback Asia Spot

Regional PVC Netback Comparison

Source: IHS © 2016 IHS

Note: Contracts After Discount and Freight

© 2016 IHS. ALL RIGHTS RESERVED.

PVC Market in the Balance

LG Chem / November 2016

Strong Market

Factors PVC

North America

Weak Market

Factors

New PVC capacity

Relative low ECU & PVC costs

Crude oil

rebounding

Volatile

ethylene prices in US

Snug ethylene supply in

spring due to turnarounds

High growth in multifamily

and single family

residential construction

© 2016 IHS. ALL RIGHTS RESERVED.

PVC Margins: Recovery On The Horizon

-80

0

80

160

240

320

400

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

NAM WEP NEA

Regional PVC Margins

Source: IHS © 2016 IHS

Do

lla

rs p

er

Me

tric

To

n

LG Chem / November 2016

© 2016 IHS. ALL RIGHTS RESERVED.

PVC Key Take-Aways

• Ethylene trend is a key driver for PVC

prices.

• The cost advantage for PVC producers

in North America has narrowed, but

rising oil price will increase advantage.

• US housing starts are still increasing.

• Excess PVC capacity curtailments in

China.

• No more new PVC capacity announced,

hence operating rates are expected to

increase in the next few years.

• Growth demand in Asia is key for the

global market.

LG Chem / November 2016

© 2016 IHS. ALL RIGHTS RESERVED.

The Big Picture: Road map take-aways for the

CAV Future

• Caustic soda, PVC and ethylene

prices trend up through the forecast

period

• Until operating rates reach a level

sufficient to sustain reinvestment

grade returns, there will be no

significant new capacity

• Location of new investment will be

defined by relative energy costs

• South American growth will be fueled

by caustic soda and vinyls imports

through the forecast period

LG Chem / November 2016

CAV

© 2016 IHS. ALL RIGHTS RESERVED.. No portion of this report may be reproduced, reused, or otherwise distributed in any form without prior written consent,

with the exception of any internal client distribution as may be permitted in the license agreement between client and IHS. Content reproduced or redistributed

with IHS permission must display IHS legal notices and attributions of authorship. The information contained herein is from sources considered reliable but its

accuracy and completeness are not warranted, nor are the opinions and analyses which are based upon it, and to the extent permitted by law, IHS shall not be

liable for any errors or omissions or any loss, damage or expense incurred by reliance on information or any statement contained herein. For more information,

please contact IHS at [email protected], +1 800 IHS CARE (from North American locations), or +44 (0) 1344 328 300 (from outside North America). All

products, company names or other marks appearing in this publication are the trademarks and property of IHS or their respective owners. V2.0-29.04.14

Americas:

+1.800.IHS.CARE (+1.800.447.2273);

Europe, Middle East, and Africa:

+44.(0).1344.328.300;

Asia and the Pacific Rim:

+604.291.3600;

Contact us