notification of the bank of thailand no. fpg. 3/2559 re ... · unofficial translation this...

TRANSCRIPT

Unofficial Translation This translation is for convenience of those unfamiliar with Thai language

Please refer to the Thai official version

Notification of the Bank of Thailand No. FPG. 3/2559

Re: Rules, Procedures and Conditions on Supervision of Electronic Payment Service Business

--------------------------------------------------------------------------

1. Rationale

In order that electronic payment service business is supervised for financial stability and commercial security and to promote the credibility and acceptance of electronic information system and to prevent public loss.

2. Statutory Power

By virtue of Section 4 and Section 17 of the Royal Decree Regulating on Electronic Payment Services B.E. 2551, together with Article 17 and Article 23 of the Notification of the Electronic Transactions Commission Re: Rules, Procedures and Conditions for Undertaking Electronic Payment Service Business B.E. 2559, the Bank of Thailand (BOT) hereby prescribes rules, procedures and conditions on supervision of electronic payment service business.

3. Repealed Notification

The Notification of the Bank of Thailand No. ITG. 2/2552 Re: Rules, Procedures and Conditions on Supervision of Electronic Payment Service Business, dated 30thJanuary 2009 (B.E. 2552) shall be repealed.

4. Scope of Application

This Notification shall be applied to the service providers under the Royal Decree Regulating on Electronic Payment Services B.E. 2551.

5. Content

5.1 In this Notification

“Service providers” means service providers of electronic payment services as prescribed in the Lists annexed to the Royal Decree Regulating on Electronic Payment Services B.E. 2551, consisting of the services which require to notify prior to commencement of services (List A), to request for registration prior to commencement of services (List B), and to request to obtain a license prior to the commencement of services (List C).

- 2 -

“Services which require to notify prior to the commencement of services” (List A) are namely electronic money services provided for payment of certain goods or services, as specified in advance by a single merchant, except for electronic money service limited to the purpose of facilitating customers without seeking profit from issuing cards, as prescribed by the BOT with the approval of the Electronic Transactions Commission (e-Money List A).

“Services which require to request for registration prior to commencement of services” (List B) are:

(1) credit card network service; (2) EDC network service; (3) single transaction switching system/service (Transaction Switching List B); (4) electronic money service provided for payment of certain goods or

services, as specified in advance by several merchants which operate under the same distribution channel or system (e-Money List B).

“Services which require to obtain a license prior to commencement of services” (List C) are:

(1) clearing service; (2) settlement service; (3) electronic payment service through any device or network; (4) multiple transaction switching systems/services (Transaction Switching List C); (5) bill payment service; (6) electronic money service provided for payment of certain goods or

services, as specified in advance by several merchants without restriction of location or distribution channel or system (e-Money List C).

5.2 e-Money Service

5.2.1 e-Money service providers under List A, List B and List C must maintain financial conditions and liquidity positions for continuity of services and preventing any loss to customers.

5.2.2 e-Money service providers under List C that are not the financial institutions under the Financial Institution Business Act B.E. 2551 must separate funds collected in advance from customers from their working capital funds. Those funds shall be deposited with commercial banks or specialized financial institutions under the Financial Business Act B.E. 2551, at any time, for no less than an outstanding amount of funds collected in advance. The accounts for this purpose must be separated from other accounts of service providers, must be unencumbered, and must be used only for settlement with respect to e-Money service provisions.

- 3 -

For the service providers that are the financial institutions under the Financial Institution Act B.E. 2551 shall comply with rules with respect to electronic money services issued under the Financial Institution Act B.E. 2551.

5.2.3 e-Money service providers under List C that are not the financial institutions under the Financial Institution Act B.E. 2551 must maintain a ratio of net equity to the outstanding balance of funds collected in advance to no less than 8 percent. The ratio shall be calculated at the end of the reporting quarter and submitted as a report to the BOT within 30 days from the end of the reporting quarter in accordance with regulations. Calculation methods and conditions are prescribed in the reporting forms by the BOT annexed to this Notification.

In case where such ratio is less than 8 percent, the BOT shall propose the Electronic Transactions Commission for consideration of fines and/or apply any approaches, on a case by case basis, to prevent loss to customers and the public, or in order that the service providers would improve or rectify their financial conditions to be in accordance with the regulations such as preparation of financial condition improvement plan, requiring the service provider to redeem funds collected in advance to customers, or suspension of license or revocation of license.

In addition, in order that service providers operate the business with sound financial and commercial conditions, the services are credible, and to prevent any impact on customers, the BOT shall prescribe the sequential measures when a ratio of net equity to the outstanding balance of funds collected in advance from customers has steadily declined before reaching the prescribed minimum level, as follows:

(1) When the ratio is less than 12 percent, the service provider must submit a letter of explanation for reasons and resolution to the BOT within 30 days from the last day of the quarter. In this case, the BOT may require the service provider to conduct its financial condition and performance improvement plan, and may also prescribe any other requirements;

(2) When the ratio is less than 10 percent, the BOT will require the service provider to conduct a financial condition and performance improvement plan, and submit to the BOT within the prescribed time. On this, the BOT may give any other orders or prescribe any other requirements or conditions.

5.2.4 Where the service providers under List C that are not the financial institutions under the Financial Institution Act B.E. 2551 have a ratio of net equity to the outstanding balance of funds collected in advance from customers less than the ratio as prescribed in 5.2.3 with the cause of necessity or in extraordinary circumstances, for instance, the ratio has changed as a result of a rapid increase in funds collected in

- 4 -

advance from customers while the service providers have a sound financial conditions and operating performance; the service providers may submit the BOT a request for temporary exemption from regulations together with reasons and details of necessity. The BOT may either grant or reject an exemption, or grant an exemption with conditions on a case by case basis. In this case, the BOT shall complete the consideration within 45 working days from the date receiving the request and completed documents.

5.2.5 If the service providers under List C that are not the financial institutions under the Financial Institution Act B.E. 2551 have not normally carried out their businesses for more than 1 year, the BOT shall propose the Electronic Transactions Commission for expediting the service providers to resume their operation for customer protection by implementing sequential approaches on a case by case basis, namely submission of warnings by requiring a clarification letter, requiring the conduction of financial condition improvement plan, requiring to redeem funds collected in advance to customers, or suspension of license or revocation of license.

5.2.6 In case of necessity or in extraordinary circumstances resulting in service providers under List C that are not the financial institutions under the Financial Institution Business Act B.E. 2551 fail to comply with the provisions pursuant to 5.2.3 and 5.2.5, the service providers may submit the BOT a request for exemption from regulations together with reasons, details of necessity and the expected completion date. The BOT shall accordingly submit the request to the Electronic Transactions Commission for consideration. The Electronic Transactions Commission may either grant or reject an exemption or grant an exemption with conditions on a case by case basis. In this case, the BOT and the Electronic Transactions Commission shall complete the consideration within 45 working days from the date receiving the request and completed documents.

5.3 Settlement service

The service providers must prescribe terms and conditions with respect to finality of funds transfer, which the payee can use those funds immediately, unconditionally and irrevocably. Those terms and conditions must be notified to the customers.

5.4 Electronic payment service through any device or network

5.4.1 The service providers must maintain financial conditions and liquidity positions for continuity of services and preventing any loss to customers.

5.4.2 The service providers must issue evidences of payments or any other evidence with the similar contents and submit the evidence to customers by the method as agreed upon with the customers.

- 5 -

When the service providers have issued evidences of payments or any other evidence to customers according to the provisions prescribed in the first paragraph, it is considered that the payment of customers is completed, except for cheque payment which the payment is considered final when the cheque has been completely collected.

5.5 Bill payment service

5.5.1 The service providers must maintain financial conditions and liquidity positions for continuity of services and preventing any loss to customers.

5.5.2 When the service providers receive payments, they are required to issue evidences indicating that they have received payments from customers. Such evidences may be in the form of receipt, cash receipt, deposit receipt or any other evidence with the similar content and deliver the evidences to customers by the method as agreed upon with the customers. The evidences must include at least the following details:

(1) name of service provider, name of creditor; (2) amount and details of goods or services for which the payment is

made, which may be in abbreviation or code, and reference details of customer; (3) date, month, year and time of evidence issued.

When the service providers have issued evidence of payment, it is considered that the payment of customers is completed, except for cheque payment which the payment is considered final when the cheque has been completely collected.

5.6 As deemed appropriate the BOT may require the service providers under List B and List C to conduct IT audit by external auditors according to the list prescribed by the Electronic Transactions Commission.

6. Transitional Provision

6.1 The service providers under List C that are not the financial institutions under the Financial Institution Business Act B.E. 2551 and have provided the services before the effective date of this Notification, must maintain a ratio of net equity to the outstanding balance of funds received in advance to comply with the provisions prescribed in this Notification within 180 days from the effective date of this Notification.

6.2 The service providers under List C that are not the financial institutions under the Financial Institution Business Act B.E. 2551 and have not normally carried out their businesses for more than 1 year before the effective date of this Notification, the service providers shall resume their operation within 180 days from the effective date of this Notification.

- 6 -

7. Effective Date

This Notification shall come into force as from the day following the date of its publication in the Government Gazette.

Announced on 7th April 2016 (B.E. 2559)

(Mr. Veerathai Santipraphob) Governor

Bank of Thailand

Report on ratio of net equity to the outstanding balance of funds collected in advance

Institution code …………………………….

Name of service provider …………………………….

List of services Service providers under List C that are not the financial institutions

Reporting quarter ……………………………. B.E. ………………..

Deadline for submission 30 days from the end of the quarter Unit: Million Baht

Ratio (1) Net equity

(2) Average outstanding balance of

funds collected in advance for the past 6-month period

(1)/(2) * 100 (Percent)

A ratio of net equity to outstanding balance of funds collected in advance

Month/Year (B.E.)

Requirements, calculation methods and conditions

Description

Name of report Ratio of net equity to the outstanding balance of funds collected in advance

Frequency of report submission

Quarterly

Submission date Within 30 days from the end of the quarter

Description This report is the report on ratio of net equity to the outstanding balance of funds collected in advance on a quarterly basis:

Net equity means total equity as appeared on the statement of financial condition.

Outstanding balance of funds collected in advance means the total amount of funds collected in advance from customers at the end of the reporting month.

Average outstanding balance of funds collected in advance for the past 6-month period means the monthly average of funds collected in advance from customers over the past 6 months.

Ratio of net equity to the outstanding balance of funds collected in advance means a ratio of net equity to the outstanding balance of funds collected in advance in percentage points:

In calculating the ratio, service providers shall use the data as appeared on financial statements, as follows:

1) Net equity – use a book value of equity as appeared on the statement of financial condition;

2) Outstanding balance of funds collected in advance – use a monthly average of book values of funds collected in advance over the past 6 months.

Reporting period Net equity Outstanding balance of funds collected in

advance First quarter Financial statements of

the last year October (last year) – March (current year)

Second quarter Financial statements of the last year

January – June (current year)

Third quarter Semi-Annual financial statements of the

current year

April – September (current year)

Fourth quarter Semi-Annual financial statements of the

current year

July – December (current year)

Example of calculation method

Calculation formula: Equity / Average Float 6 M (Moving Average 6 M) on a quarterly basis:

50 50 100 100 (…+…+…+100+150+200)/6 (100+150+200+250+300+350)/6

22.22%

(250+300+350+300+350+300)/6

32.43%

(300+350+300+350+400+400)/6

28.57%

50 50

100 100

100

31 March 30 June 30 September 31 December

Unofficial Translation This translation is for convenience of those unfamiliar with Thai language.

Please refer to the Thai text for the official version.

-------------------------------- Notification of the Bank of Thailand

No. FPG. 4/2559 Re: Supervisory Guidance of the Appointment of Agents

by Electronic Payment Service Providers __________________

1. Rationale

In order that the appointment of agents by electronic payment service providers is reliable and be aligned with common standards and to prevent any public loss from the services provided by the appointed agents, and to increase contact and service points, which is beneficial to customers, the public and payment systems.

2. Statuary Power

By virtue of Article 20 of the Notification of the Electronic Transactions Commission Re: Rules, Procedures and Conditions for Undertaking Electronic Payment Service Business B.E. 2559.

3. Scope of Application

This Notification shall be applied to the service providers under the Royal Decree Regulating on Electronic Payment Services B.E. 2551 that are not the financial institutions under the Financial Institution Act B.E. 2551.

On this, the service providers that are the financial institutions under the Financial Institution Act B.E. 2551 shall comply with the Notification of the Bank of Thailand Re: Rules on Appointment of Banking Agents.

4. Content

4.1 Definition

In this Notification

“Service provider” means the provider of electronic payment services as prescribed in the Lists annexed to the Royal Decree Regulating on Electronic Payment Services B.E. 2551.

- 2 -

“Agent” means a natural person or juristic person appointed by the service provider under List A, List B and List C to provide electronic payment services on behalf of the service provider to customers.

4.2 Supervision

Appointment of agents is to increase contact and service points of electronic payment service providers, therefore, the service providers and their agents must not have any arrangements considered avoiding the submission of notice, request for registration or request to obtain a license, or compliance with the Royal Decree Regulating on Electronic Payment Services B.E. 2551. On this, the service providers shall comply with the rules on appointment of agents as follows:

4.2.1 Responsibility to customers

(1) The service providers must supervise the operation of their appointed agents including natural persons or juristic persons appointed or subcontracted by the appointed agents, for all involving parties, to comply with rules as prescribed in the Royal Decree Regulating on Electronic Payment Services B.E. 2551, Notifications of the Electronic Transactions Commission and Notifications of the Bank of Thailand as well as any related laws.

(2) The service providers are wholly responsible to customers for any arrangements carried out by their appointed agents and natural persons or juristic persons appointed or subcontracted by the appointed agents, for all involving parties, as if the service providers have carried out those arrangements themselves.

4.2.2 Policy and procedures for appointment of reliable agents

The service providers must establish clear policy and procedures for appointment of agents, which must at least cover the following issues:

(1) Guidelines on the appointment of reliable agents, where the agents to be appointed may be natural persons or juristic persons, must have the qualifications and not have prohibited characteristics as follows:

(1.1) Natural person

(a) being of not less than 20 years of age;

(b) having a domicile or residence in Thailand;

(c) not having been ordered to confiscate the asset to vest on the state or not having been declared bankrupt, or had been declared

- 3 -

bankrupt but has not yet been discharged from 2 years period of bankruptcy from the bankruptcy filing date;

(d) not being an unsound-mind, incompetent or a quasi-incompetent person;

(e) not having been imprisoned by a final court judgment for offences concerning counterfeiting and alteration, theft, snatching, extortion, robbery, burglary, fraud, welshing, embezzlement, handling stolen goods, or computer-related offences under the Computer-Related Crime Act;

(f) not having been prohibited from undertaking electronic payment services within the period of five years from the date of the Notice submission;

(g) not being a director or person with managerial power of a juristic person who having been prohibited from undertaking electronic payment services or having had the license revoked within the period of five years from the date of the Notice submission, the request for registration or the request to obtain a license, as the case may be.

(1.2) Juristic person

(a) being a registered partnership, limited partnership, limited company or public limited company;

(b) directors and persons with managerial power of a juristic person must have qualifications and must not have prohibited characteristics as specified under (1.1);

(c) not having had a license suspended;

(d) not having been prohibited from undertaking electronic payment services or having had the license revoked within the period of five years from the date of the Notice submission, the request for registration or the request to obtain a license, as the case may be.

On this, the persons as specified under (1.1), (1.2) and directors or persons with managerial power of a juristic person must also have the qualifications and must not have the prohibited characteristic as follows:

(a) had not been sentenced or ordered by a court judgment to confiscate the asset to vest on the state, or not having been judged by a final court for any offences relating to anti-money laundering;

- 4 -

(b) not having been listed on the lists of designated persons or sentenced by the final court judgment for financing of terrorism under the law on combating the financing of terrorism.

If the service providers wish to appoint agents with the qualifications apart from those specified above, the service providers shall submit a request for approval to the BOT on a case by case basis. The BOT reserves rights to approve or reject the request, or approve with conditions or any other requirements as deemed appropriate. On this, the BOT shall complete the consideration within 45 working days from the date receiving the request and completed documents.

(2) Guidelines on risk management of appointment of agents of service providers, internal control system and coordination between the service providers and their appointed agents in order to prevent any risks that may arise, such as cash security, service systems security and audit on regularly basis, limit on amount holding by the agents for money transfer services, issuance of bank guarantee or placing of money as guarantee.

(3) The payment finality of transactions made by appointed agents must be under the same standards as the transactions made by the service providers.

(4) Evidence of payment transactions which appointed agents issue to customers.

(5) Essential conditions of the agreement on appointment of agents.

(6) The service providers are subject to exclude their appointed agents from operating electronic payment services as they avoid the submission of Notice, request for the registration and request to obtain a license according to the Royal Decree Regulating on Electronic Payment Services B.E. 2551.

4.2.3 Disclosure of information

(1) The service providers shall disclose the following information to customers:

(1.1) appointment of agents of service providers, such as lists and places of services of appointed agents. where the date of the latest revision to the list shall also be indicated, transactions that can be undertaken at each service place of agents, service conditions, responsibilities of service providers to customers, and consumer protection measures;

(1.2) information that may affect customers due to the appointment of agents, such as fees or service charges, any amendments to details of

- 5 -

services that may lessen customer benefits. All these information shall be disclosed to the customers in advance.

(2) The service providers shall supervise their appointed agents to disclose the following information to customers:

(2.1) transactions that can be undertaken through the agents, conditions of services, responsibilities to customers and consumer protection measures;

(2.2) information that may affect customers, such as fees or service charges, or any amendments to details of services that may lessen customer benefits. All these information shall be disclosed to customers in advance.

4.2.4 Other guidelines on customer protection

The service providers must comply with, as well as supervise their appointed agents to comply with other guidelines on customer protection, at least as follows:

(1) The payment finality of transactions

When appointed agents issue evidence of payment, or evidence of money transfer, or any other evidence with the similar contents, and submit the evidence to customers by the method as agreed upon with the customers, it is considered that the payment or money transfer transactions of the customers are completed, except for payment or money transfer transactions using cheques, where the transactions are considered completed once the cheques have been completely collected.

(2) Consumer protection including privacy of customers’ personal information:

(2.1) the service providers must require their agents to provide the services to customers only in places of business, branch offices or other distribution channels of the agents, or places of juristic persons or other parties that the agents have entered into an agreement to use those places. There must be the service days and hours specified as well as banners or logos of service providers clearly indicated at the service places. In addition, the agents may implement any other security measures at those service places or distribution channels.

(2.2) the service providers must require their agents to take responsibility for customer security and customer information privacy, unless the disclosure of this information is required by laws.

(3) Acceptance of customer complaints

- 6 -

The service providers must have in place convenient and explicit channels for accepting customer complaints. At least, there must be telephone numbers and addresses of offices or valid email addresses.

(4) Reporting of information to the Bank of Thailand

The service providers must prepare and update the list of their agents and submit it to the BOT every six months within 30 days from the end of the reporting period in accordance with procedures, conditions and reporting forms as specified in the Attachment. On this, the BOT may request for further information on a case by case basis as deemed appropriate and necessary.

4.2.5 In case of necessity or extraordinary circumstances resulting in service providers fail to comply with the regulations on qualifications of agents, guidelines on risk management from appointment of agents, disclosure of information on appointment of agents or reporting of information to the BOT; the service providers shall submit the BOT a request for exemption from regulations together with reasons, details of necessity and the expected completion date, and the BOT may either grant or reject an exemption. The BOT has power to grant the exemption for no more than 90 days, and may grant the exemption with conditions on a case by case basis.

In case where the service providers deem that they cannot comply with those provisions as prescribed in the first paragraph, the service providers shall submit the BOT a request for extension of time frame together with reasons and details of necessity. And, the BOT shall accordingly submit the request to the Electronic Transactions Commission for consideration. The Electronic Transactions Commission may approve or reject the request of extension or may approve with conditions on a case by case basis. The BOT and the Electronic Transactions Commission shall complete the consideration within 45 working days from the date receiving the request and completed documents.

5. Effective Date

This Notification shall come into force 90 days after the date of its publication in the Government Gazette.

Announced on 7th April 2016 (B.E. 2559)

(Mr. Veerathai Santipraphob) Governor

Bank of Thailand

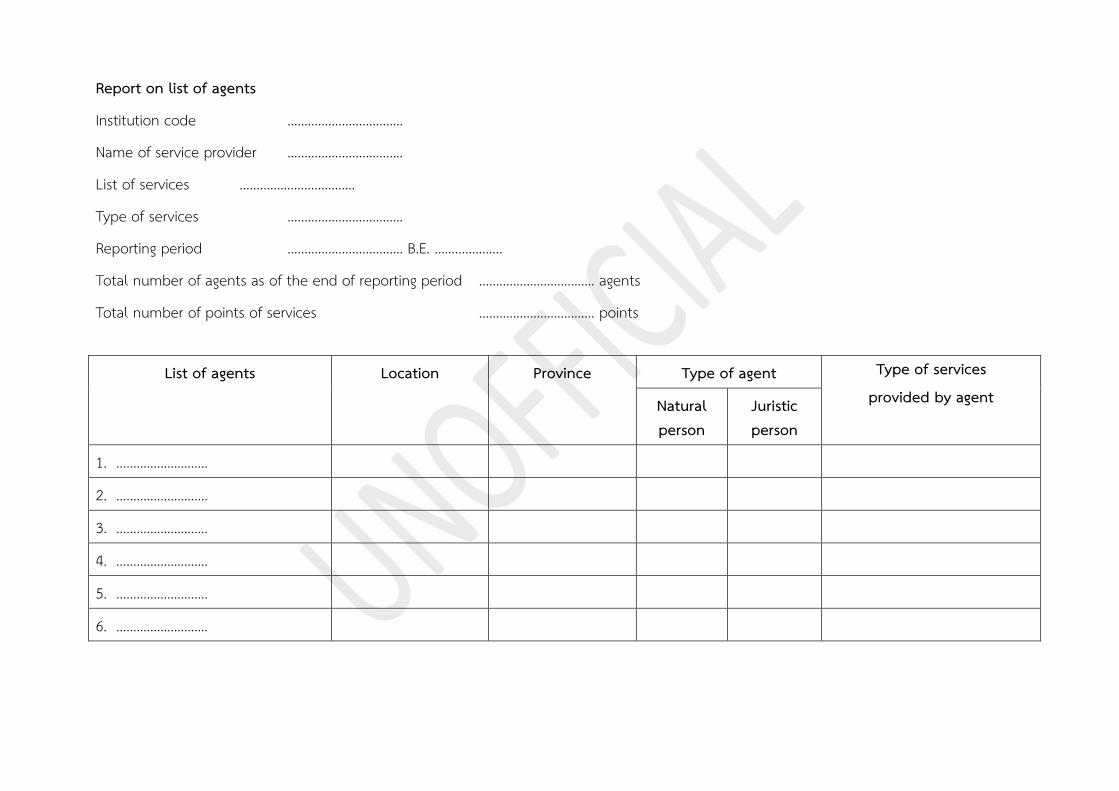

Report on list of agents

Institution code …………………………….

Name of service provider …………………………….

List of services …………………………….

Type of services …………………………….

Reporting period ……………………………. B.E. ………………..

Total number of agents as of the end of reporting period ……………………………. agents

Total number of points of services ……………………………. points

List of agents Location Province Type of agent Type of services provided by agent Natural

person Juristic person

1. ………………………

2. ………………………

3. ………………………

4. ………………………

5. ………………………

6. ………………………

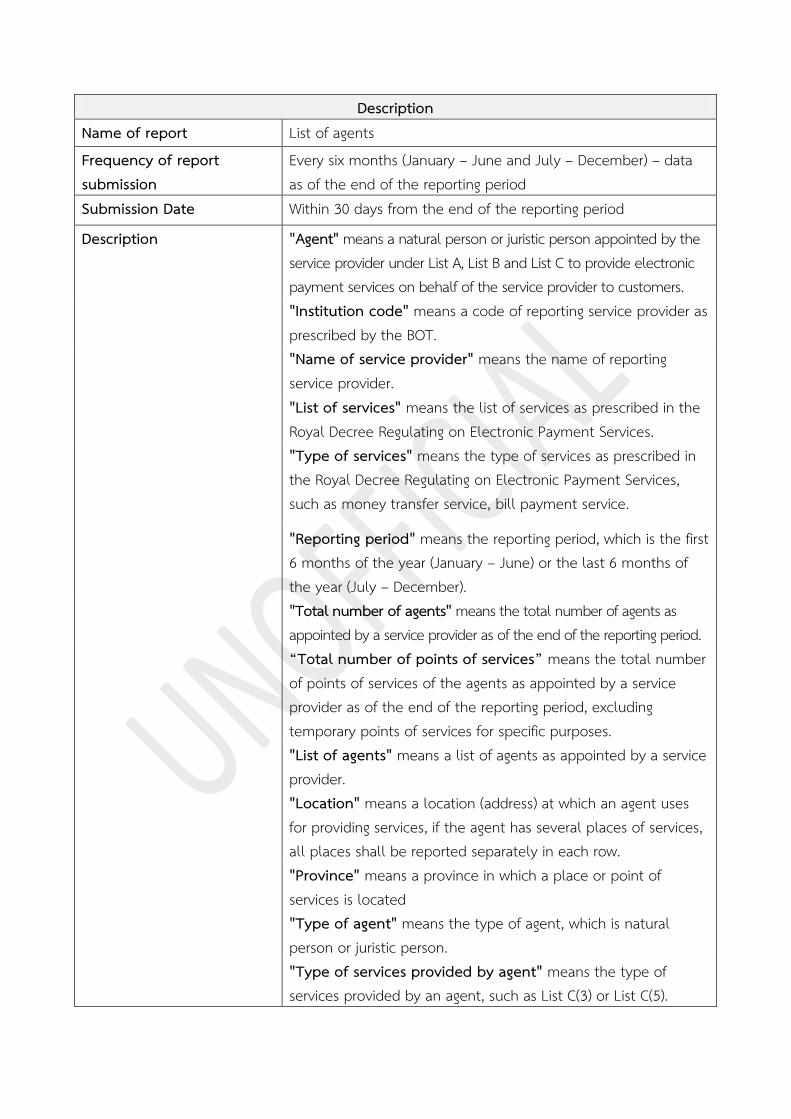

Description Name of report List of agents Frequency of report submission

Every six months (January – June and July – December) – data as of the end of the reporting period

Submission Date Within 30 days from the end of the reporting period

Description "Agent" means a natural person or juristic person appointed by the service provider under List A, List B and List C to provide electronic payment services on behalf of the service provider to customers.

"Institution code" means a code of reporting service provider as prescribed by the BOT.

"Name of service provider" means the name of reporting service provider.

"List of services" means the list of services as prescribed in the Royal Decree Regulating on Electronic Payment Services.

"Type of services" means the type of services as prescribed in the Royal Decree Regulating on Electronic Payment Services, such as money transfer service, bill payment service.

"Reporting period" means the reporting period, which is the first 6 months of the year (January – June) or the last 6 months of the year (July – December).

"Total number of agents" means the total number of agents as appointed by a service provider as of the end of the reporting period.

“Total number of points of services” means the total number of points of services of the agents as appointed by a service provider as of the end of the reporting period, excluding temporary points of services for specific purposes.

"List of agents" means a list of agents as appointed by a service provider. "Location" means a location (address) at which an agent uses for providing services, if the agent has several places of services, all places shall be reported separately in each row.

"Province" means a province in which a place or point of services is located

"Type of agent" means the type of agent, which is natural person or juristic person.

"Type of services provided by agent" means the type of services provided by an agent, such as List C(3) or List C(5).