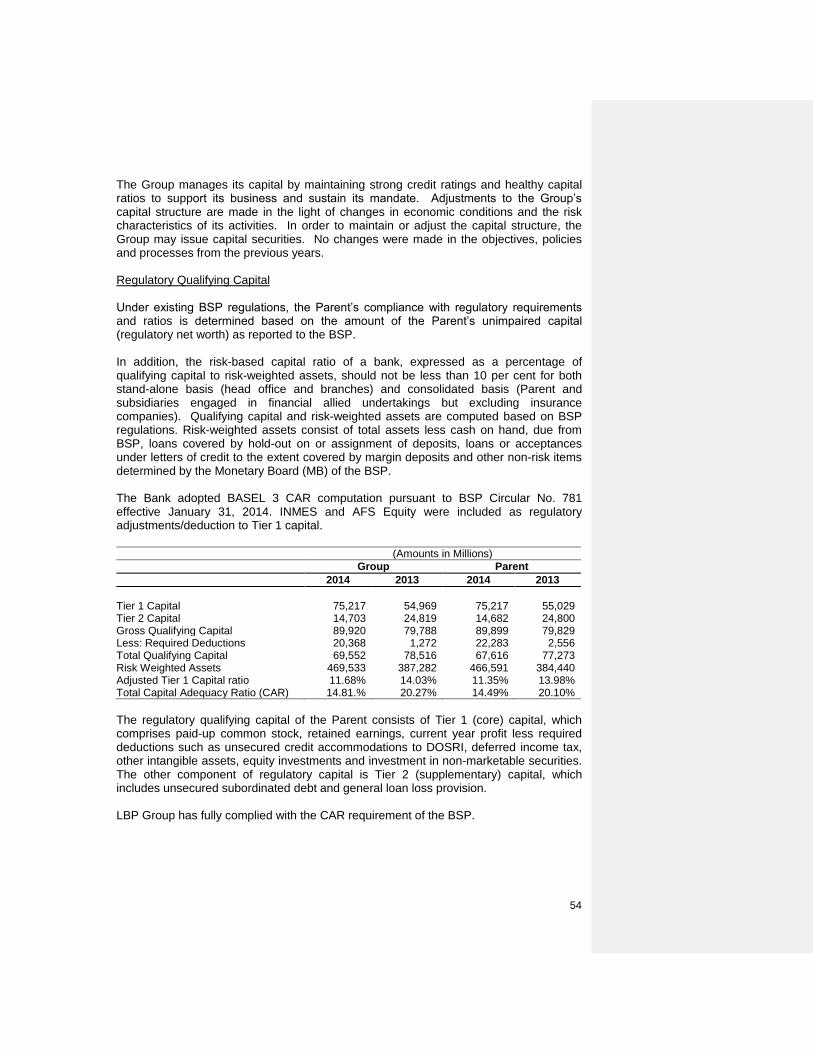

notes to financial statements - land bank of the · notes to financial statements (amounts in...

TRANSCRIPT

10

LAND BANK OF THE PHILIPPINES NOTES TO FINANCIAL STATEMENTS

(Amounts in thousands, except as indicated)

1. Corporate Information

The Land Bank of the Philippines (Parent) is a financial institution wholly-owned by the National Government. The Parent was established in 1963 as the financial intermediary of the Land Reform Program of the government. Later, it became the first universal bank by charter with expanded commercial banking powers to sustain its social mission of spurring countryside development. The Parent is a depository bank of the government and its various instrumentalities. The Parent services the requirements of the national government, local government units and government-owned and controlled corporations. As of December 31, 2014, 69 percent of the deposit portfolio came from the government while the rest came from private depositors. The Parent and its subsidiaries (Group) are engaged in the business of banking, financing, leasing, real estate, insurance brokering and other related services to personal, commercial, corporate and institutional clients. The Group‟s products and services include deposit-taking, lending and related services, treasury and capital market operations, trade services, payments and cash management, and trust services. The Parent‟s principal office of business is located at the LandBank Plaza, 1598 M.H. Del Pilar corner Dr. J. Quintos Streets, Malate, Manila. The accompanying comparative financial statements of the Parent were authorized for issue by the Parent‟s Board of Directors on February 23, 2015 while those of the subsidiaries were approved for issue by their respective Board of Directors on various dates. 2. Summary of Significant Accounting Policies

2.1 Basis of Financial Statements Preparation The accompanying financial statements have been prepared on a historical cost basis except for financial assets and financial liabilities at fair value through profit or loss (FVPL), available-for- sale (AFS) investments, and derivative financial instruments that have been measured at fair value. The financial statements of the Parent include the accounts maintained in the Regular Banking Unit (RBU) and Foreign Currency Deposit Unit (FCDU). The financial statements individually prepared for these units are combined after eliminating inter-unit accounts. The functional currency of RBU and FCDU is Philippine Peso and United States Dollar (USD), respectively. For financial reporting purposes, FCDU accounts and foreign

11

currency-denominated accounts in the RBU are translated in Philippine Peso based on the Philippine Dealing System (PDS) closing rate prevailing at end of the year. The consolidated financial statements are presented in Philippine peso, and all values are rounded to the nearest thousand pesos (P000) except when otherwise indicated. 2.2 Statement of Compliance The consolidated financial statements of the Group and of the Parent have been prepared in compliance with the Philippine Financial Reporting Standards (PFRS). 2.3 Basis of Consolidation The consolidated financial statements include the financial statements of the Parent and the following wholly-owned subsidiaries:

Name

Country of Incorporation

Principal Activity

Functional Currency

LBP Leasing Corporation Philippines Leasing Philippine peso LBP Insurance Brokerage Inc. Philippines Insurance brokerage Philippine peso LBP Resources and Development Corporation

Philippines

Real estate

Philippine peso

Masaganang Sakahan, Inc. Philippines Trading Philippine peso LBP Financial Services-Italy Italy Financial services Euro

The consolidated financial statements were prepared using consistent accounting policies for like transactions and other events in similar circumstances. All significant inter-company balances and transactions have been eliminated in consolidation. Significant Accounting Policies

Foreign currency translation Transactions and balances The books of accounts of the RBU are maintained in Philippine Peso, while those of the FCDU are maintained in USD. For financial reporting purposes, the foreign currency-denominated monetary assets and liabilities in the RBU are translated in Philippine Peso based on the Philippine Dealing System (PDS) closing rate prevailing at the statement of financial position date. Foreign exchange differences arising from revaluation and translation of foreign-currency denominated assets and liabilities are credited to or charged against operations in the year in which the rates change. Non-monetary items that are measured in terms of historical cost in a foreign currency are translated using the exchange rates as at the dates of the initial transactions. Non-monetary items measured at fair value in a foreign currency are translated using the exchange rates at the date when the fair value was determined.

12

Fair Value Measurement

The methods and assumptions used by the Group in estimating the fair value of the financial instruments include the following: Cash and cash equivalents and short-term investments – Carrying amounts approximate fair values due to the relatively short-term maturity of these instruments. Debt securities – Fair values are generally based upon quoted market prices. If the market prices are not readily available, fair values are estimated using either values obtained from counterparties or independent parties offering pricing services, values based on adjusted quoted market prices of comparable investments or values computed using the discounted cash flow methodology. Equity securities - Fair values are based on quoted prices published in markets. Loans and receivables – Fair values of loans are estimated using the discounted cash flow methodology using the Parent‟s current incremental lending rates for similar types of loans. Mortgage loans – Fair values of loans on real estate are estimated using the discounted cash flow methodology using the Parent‟s current incremental lending rates for similar types of loans. Short-term investments – Carrying amounts approximate fair values. Others – Quoted market prices are not readily available for these assets. They are not reported at fair value and are not significant in relation to the Group‟s total portfolio of securities. Obligations to repurchase securities are recorded at cost which approximates fair value. Liabilities – Fair values are estimated using the discounted cash flow methodology using the Parent‟s current incremental borrowing rates for similar borrowings with maturities consistent with those remaining for the liability being valued. Except for the long-term fixed rates liabilities and floating rate liabilities with repricing periods beyond three months, the carrying values approximate fair values due to the relatively short term maturities of the liabilities or frequency of the repricing. Financial Instruments Date of recognition

Purchases or sales of financial assets that require delivery of assets within the time frame established by regulation or convention in the marketplace are recognized on the settlement date - the date that an asset is delivered to or by the Group. Securities transactions are also recognized on settlement date basis. Deposits, amounts due to banks and customers and loans are recognized when cash is received by the Group or advanced to the borrowers.

13

Initial recognition of financial instruments

All financial instruments, including trading and investment securities and loans and receivables, are initially measured at fair value. Except for financial assets and financial liabilities valued at FVPL, the initial measurement of financial instruments includes transaction costs. The Group classifies its financial assets in the following categories: financial assets at FVPL, HTM investments, AFS investments, and loans and receivables while financial liabilities are classified as financial liabilities at FVPL and financial liabilities carried at amortized cost. The classification depends on the purpose for which the investments were acquired and whether they are quoted in an active market. Management determines the classification of its investments at initial recognition and, where allowed and appropriate, re-evaluates such designation at every reporting date. Reclassification of financial assets A financial asset is reclassified out of the FVPL category when the following conditions are met:

the financial asset is no longer held for the purpose of selling or repurchasing it in the near term; and

there is a rare circumstance. A financial asset that is reclassified out of the FVPL category is reclassified at its fair value on the date of reclassification. Any gain or loss already recognized in the consolidated statement of comprehensive income is not reversed. The fair value of the financial asset on the date of reclassification becomes its new cost or amortized cost, as applicable. Determination of fair value The fair value for financial instruments traded in active markets at the statement of financial position date is based on their quoted market price or dealer price quotations (bid price for long positions and ask price for short positions), without any deduction for transaction costs. When current bid and asking prices are not available, the price of the most recent transaction is used since it provides evidence of the current fair value as long as there has not been a significant change in economic circumstances since the time of the transaction. For all other financial instruments not listed in an active market, the fair value is determined by using appropriate valuation techniques. Valuation techniques include net present value techniques, comparison to similar instruments for which market observable prices exist, options pricing models, and other relevant valuation models. ‘Day 1’ difference

Where the transaction price in a non-active market is different from the fair value from other observable current market transactions for the same instrument or based on a valuation technique whose variables include only data from observable market, the Group recognizes the difference between the transaction price and fair value (a „Day 1‟

14

difference) in the statement of comprehensive income. In cases where the transaction price used is made of data which is not observable, the difference between the transaction price and model value is only recognized in the statement of comprehensive income when the inputs become observable or when the instrument is derecognized. For each transaction, the Group determines the appropriate method of recognizing the „Day 1‟ difference amount. (a) Financial assets designated at fair value through profit or loss (FVPL) FVPL consists of securities held for trading and financial assets that are voluntarily designated as FVPL on trade date. The FVPL category includes government debt securities purchased and held principally with the intention of selling them in the near term. These securities are carried at fair market value, based primarily on quoted market prices, or if quoted market prices are not available, discounted cash flows using market rates that are commensurate with the credit quality and maturity of the investments. Realized and unrealized gains and losses on these instruments are recognized under the trading and foreign exchange profits accounts in the statement of comprehensive income. (b) Loans and receivables, amounts due from BSP and other banks, interbank loans receivable and securities purchased under resale agreements These are financial assets with fixed or determinable payments and fixed maturities that are not quoted in an active market. They are not entered into with the intention of immediate or short-term resale and are not classified as other financial assets held for trading, designated as AFS investments or financial assets designated at FVPL. (c) Held-to-Maturity (HTM) investments HTM investments are quoted non-derivative financial assets with fixed or determinable payments and fixed maturities for which the Group‟s management has the positive intention and ability to hold to maturity. Where the Group sells other than an insignificant amount of HTM investments or those close to maturity, the entire category would be tainted and reclassified as AFS investments. These investments are carried at amortized cost using the effective interest rate method, reduced by any impairment in value. Gains and losses are recognized in statement of comprehensive income when the HTM investments are derecognized or impaired, as well as through the amortization process. (d) Available-for-sale (AFS) investments AFS investments are those which do not qualify to be classified as designated as FVPL, HTM or loans and receivables. They are purchased and held indefinitely, but which the Group anticipates to sell in response to liquidity requirements or changes in market conditions. AFS investments are carried at fair market value. The effective yield component (including premium, discounts and directly attributable transaction costs) and foreign exchange restatement results of available-for-sale debt securities are reported in earnings. Dividends on AFS equity instruments are recognized in the statement of

15

comprehensive income when the entity‟s right to receive payment is established. The unrealized gains and losses arising from the recognition of fair value changes on AFS assets are reported as a separate component of capital funds in the statement of financial position. Impairment of Financial Assets The Group determines at each reporting date whether there is objective evidence that a financial asset may be impaired. Financial assets carried at amortized cost A financial asset or a group of financial assets is impaired and impairment losses are incurred if, and only if, there is objective evidence of impairment as a result of one or more events that occurred after the initial recognition of the asset (a „loss event‟) and that loss event has an impact on the estimated future cash flows of the financial asset or group of financial assets that can be reliably estimated. The Group first assesses whether objective evidence of impairment exists individually for financial assets that are individually significant, and individually or collectively for assets that are not individually significant. If it is determined that no objective evidence of impairment exists for individually assessed financial asset, whether significant or not, the asset is included in a group of financial assets with similar credit risk characteristics (i.e., on the basis of the Group‟s scoring process that considers asset term, industry and collateral) and that group of assets is collectively assessed for impairment. Those characteristics are relevant to the estimation of future cash flows for group of such assets by being indicative of the debtors‟ ability to pay all amounts due according to the contractual terms of the assets being evaluated. Assets that are individually assessed for impairment and for which an impairment loss is or continues to be recognized are not included in a collective assessment for impairment. If there is objective evidence that an impairment loss on loans and receivables carried at amortized cost has been incurred, the amount of the loss is measured as the difference between the asset‟s carrying amount and the present value of the estimated future cash flows (excluding future credit losses that have not been incurred) discounted at the financial asset‟s original effective interest rate. The carrying amount of the asset is reduced through use of an allowance account. The amount of loss is charged to current operations. If a loan or HTM investment has a variable interest rate, the discount rate for measuring any impairment loss is the current effective interest rate determined under the contract. If, in a subsequent year, the amount of the estimated impairment loss decreases because of an event occurring after the impairment was recognized, any amounts formerly charged are credited to „Provision for credit and impairment losses‟ in the statement of comprehensive income and the allowance account, reduced. The HTM investments, together with the associated allowance accounts, are written off when there is no realistic prospect of future recovery and all collateral has been realized.

16

The calculation of the present value of the estimated future cash flows of a collateralized financial asset reflects the cash flows that may result from foreclosure less costs for obtaining and selling the collateral, whether or not foreclosure is probable. Future cash flows in a group of financial assets that are collectively evaluated for impairment are estimated on the basis of the contractual cash flows of the assets and historical loss experience for assets with similar credit risk characteristics. Historical loss experience is adjusted on the basis of current observable data to reflect the effects of current conditions that did not affect the period on which the historical loss experience is based and to remove the effects of conditions in the historical period that do not exist currently. Estimates of changes in future cash flows for groups of assets are made to reflect and be directionally consistent with changes in related observable data from period to period (such as changes in unemployment rates, property prices, payment status, or other factors indicative of changes in the probability of losses in the group and their magnitude). The methodology and assumptions used for estimating future cash flows are reviewed regularly by the Group to reduce any differences between loss estimates and actual loss experience. When a loan is uncollectible, it is written off against the related allowance for loan impairment. Such loans are written off after all the necessary procedures have been completed and the amount of the loss has been determined. Subsequent recoveries of amounts previously written off are charged to income. Restructured loans Where possible, the Group seeks to restructure loans rather than to take possession of collateral. This may involve extending the payment arrangements and the agreement of new loan conditions. Once the terms have been renegotiated, the loan is no longer considered past due. Management continuously reviews restructured loans to ensure that all criteria are met and that future payments are likely to occur. The loans continue to be subject to an individual or collective impairment assessment, calculated using the loan‟s original effective interest rate. The difference between the recorded value of the original loan and the present value of the restructured cash flows, discounted at the original effective interest rate, is recognized in „Provision for credit losses‟ in the statement of comprehensive income. Assets Carried at Cost If there is objective evidence that an impairment loss on an unquoted equity instruments that are not carried at fair value because its fair value cannot be reliably measured, or on a derivative asset that is linked to and must be settled by delivery of such unquoted equity instrument has been incurred, the amount of the loss is measured as the difference between the asset‟s carrying amount and the present value of estimated future cash flows discounted at the current market rate of return for a similar financial asset.

17

AFS Investments

If an AFS investment is impaired, an amount comprising the difference between its cost (net of any principal payment and amortization) and its current fair value, less any impairment loss on that security previously recognized in profit or loss – is removed from equity and recognized in the statement of comprehensive income. Impairment losses on equity instruments recognized in the statement of comprehensive income are not reversed through the statement of comprehensive income. If, in a subsequent period, the fair value of a debt instrument classified as AFS investment increases and the increase can be objectively related to an event occurring after the impairment loss was recognized in profit or loss, the impairment loss is reversed through the statement of comprehensive income. Derecognition of Financial Assets and Liabilities Financial Assets. A financial asset (or, where applicable, a part of a financial asset or part of a group of similar financial assets) is derecognized when: the rights to receive cash flows from the asset have expired; the Group retains the right to receive cash flows from the asset, but has assumed an obligation to pay them in full without material delay to a third party under a „pass-through‟ arrangement; or the Group has transferred its rights to receive cash flows from the asset and either (a) has transferred substantially all the risks and rewards of the asset, or (b) has neither transferred nor retained substantially all the risks and rewards of the asset, but has transferred control of the asset.

Where the Group has transferred its rights to receive cash flows from an asset and has neither transferred nor retained substantially all the risks and rewards of the asset nor transferred control of the asset, the asset is recognized to the extent of the Group‟s continuing involvement in the asset. Continuing involvement that takes the form of a guarantee over the transferred asset is measured at the lower of the original carrying amount of the asset and the maximum amount of consideration that the Group could be required to repay. Where continuing involvement takes the form of a written and/or purchase option (including a cash-settled option or similar provision) on the transferred asset, the extent of the Group‟s continuing involvement is the amount of the transferred asset that the Group may repurchase, except that in the case of a written put option (including a cash-settled option or similar provision) on an asset measured at fair value, the extent of the Group‟s continuing involvement is limited to the lower of the fair value of the transferred asset and the option exercise price. Financial Liabilities. A financial liability is derecognized when the obligation under the liability is discharged or cancelled or expired. When an existing financial liability is replaced by another from the same lender on substantially different terms, or the terms of an existing liability are substantially modified, such an exchange or modification is treated as a derecognition of the original liability and the recognition of a new liability, and the difference in the respective carrying amounts is recognized in profit or loss.

18

Derivative Instruments

The Group enters into derivative contracts such as currency forwards and currency swaps to manage its foreign exchange exposure. These derivative financial instruments are initially recorded at fair value on the date at which the derivative contract is entered into and are subsequently remeasured at fair value. Any gains or losses arising from changes in fair values of derivatives (except those accounted for as accounting hedges) are taken directly to the statement of comprehensive income. Derivatives are carried as assets when the fair value is positive and as liabilities when the fair value is negative. Derivative instruments are booked at its notional amount under contingent account on trade date and subsequently measured using the mark to forward methods. Any gains/(losses) arising from the market valuation are booked under asset account “Derivatives with positive fair value“ if the market valuation is positive and under the liability account “Derivatives with negative fair value” if the market valuation is negative contra foreign exchange gain/(loss) account. For the purpose of hedge accounting, hedges are classified primarily as either: a) a hedge of the fair value of an asset, liability or a firm commitment (fair value hedge); or b) a hedge of the exposure to variability in cash flows attributable to an asset or liability or a forecasted transaction (cash flow hedge). The Group did not apply hedge accounting treatment for its derivative transactions. The Group has certain derivatives that are embedded in host financial contracts (such as structured notes, debt investments, and loan receivables) and non-financial contracts (such as purchase orders, lease contracts and service agreements). These embedded derivatives include credit default swaps (which are linked to a reference bond), and calls and puts in debt and equity securities; conversion options in loans receivable; and foreign-currency derivatives in debt instruments, lease contracts, purchase orders and service agreements. Embedded derivatives are separated from their host contracts and carried at fair value with fair value changes being reported through profit or loss, when the entire hybrid contracts (composed of both the host contract and the embedded derivative) are not accounted for as financial instruments at FVPL and when their economic risks and characteristics are not closely related to those of their respective host contracts. Offsetting financial instruments Offsetting of financial assets and financial liabilities are only made and the net amount are reported in the statement of financial position when there is a legally enforceable right to offset the recognized amounts and the Group intends to either settle on a net basis, or to realize the asset and the liability simultaneously. Fiduciary Activities Assets and income arising from fiduciary activities together with related undertakings to return such assets to customers are excluded from the financial statements where the Group acts in a fiduciary capacity such as nominee, trustee or agent.

19

Subsequent Events Any post-year-end event that provides additional information about the Group‟s position at the statement of financial position date (adjusting event) is reflected in the financial statements. Post-year-end events that are non adjusting events, if any, are disclosed in the Notes to the financial statements, when material. Impairment of Property and Equipment, Investment Property and Other Resources At each reporting date, the Group assesses whether there is any indication that the property and equipment and investment properties may be impaired. Where an indicator of impairment exists, the Group makes a formal estimate of recoverable amount. Where the carrying amount of an asset exceeds its recoverable amount, the asset is considered impaired and is written down to its recoverable amount. Recoverable amount is the higher of an asset‟s or cash-generating unit‟s fair value less costs to sell and its value in use and is determined for an individual asset, unless the asset does not generate cash inflows that are largely independent of those from other assets or group of assets. Investments in Subsidiaries The Group‟s investments in subsidiaries and entities in which the Group has control are accounted for under the cost method of accounting in the separate financial statements. These are carried in the statement of financial position at cost less any impairment in value.

Property and Equipment Property and equipment are carried at cost less accumulated depreciation and amortization and any impairment in value. When the assets are sold or retired, their cost and accumulated depreciation and amortization are eliminated from the accounts and any gain or loss resulting from their disposal is included in the statement of comprehensive income.

The initial cost of property and equipment comprises its purchase price and any directly attributable cost of bringing the asset to its working condition and location for its intended use. Expenditures incurred after the fixed assets have been put into operation, such as repairs and maintenance costs, are normally charged to profit and loss in the period in which the costs are incurred.

Depreciation and amortization is calculated on a straight-line basis over the estimated useful life (EUL) of the property and equipment as follows:

Number of Years

Buildings 10 - 30 Furniture, fixtures and equipment 5 - 10 Leasehold rights 10 - 30* Transportation equipment 7 - 10

20

*EUL shall depend on the length of the lease. It shall be the period of the lease or the EUL of the assets, as given, whichever is shorter.

The useful life and depreciation and amortization methods are reviewed periodically to ensure that the period and method of depreciation and amortization are consistent with the expected pattern of economic benefits from items of property and equipment. Investment properties Property acquired by the Group in settlement of loans through foreclosure or dation in payment, and that is not significantly occupied by the Group, is classified as investment property. Investment property comprises land and building. Investment properties are measured at their fair value as the deemed cost as allowed under PFRS 1 and PAS 40. Subsequent to initial recognition, investment properties are stated at cost less accumulated depreciation and impairment loss. Investment properties are derecognized when they have either been disposed of or when the investment property is permanently withdrawn from use and no future benefit is expected from its disposal. Any gains or losses on derecognition of an investment property are recognized in the profit and loss in the year of derecognition. Expenditures incurred after the fixed investment properties have been put into operation, such as repairs and maintenance costs, are normally charged to income in the period in which the costs are incurred. Depreciation is calculated on a straight-line basis over 10 to 30 years, which is the estimated useful life of the investment properties. Intangible Assets Computer software Acquired computer software licenses are capitalized on the basis of the costs incurred to acquire and bring to use the specific software. These costs are amortized on the basis of the expected useful lives (three to five years). Costs associated with developing or maintaining computer software programs are recognized as an expense as incurred. Income Taxes Income tax on the profit for the year comprises current tax only. Income tax is recognized in the statement of comprehensive income except to the extent that it relates to items recognized directly in equity. Current income tax is the expected tax payable on the taxable income for the year using tax rates enacted or substantially enacted as of the reporting date, and any adjustment to tax payable in respect to previous years. Deferred tax assets are recognized for the future tax consequences attributable to temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amount used for taxation purposes and the carry forward benefits of the net operating loss carryover (NOLCO) and the minimum corporate

21

income tax (MCIT) over the regular corporate income tax. The amount of deferred tax provided is based on the expected manner of realization or settlement of the carrying amounts of assets and liabilities, using tax rates that have been enacted or substantially enacted as of the reporting date. A deferred tax asset is recognized only to the extent that it is probable that future taxable profits will be available against which the asset can be utilized. Deferred tax assets are reduced to the extent that it is no longer probable that the related tax benefit will be realized. The carrying amount of the deferred tax asset is reviewed at each reporting date and reduced, if appropriate. Employee Benefits The Group maintains a defined contribution plan which provides for estimated pension benefits on its contributory retirement plan covering all regular employees. Leases (a) LBP Group is the lessee

(i) Operating lease - leases in which substantially all risks and rewards of ownership are retained by another party, the lessor, are classified as operating leases. Payments, including prepayments, made under operating leases (net of any incentives received from the lessor) are charged to the statement of comprehensive income on a straight-line basis over the period of the lease. (ii) Financial lease - leases of assets where the LBP Group has substantially all the risks and rewards of ownership are classified as finance leases. Finance leases are capitalized at the lease‟s commencement at the lower of the fair value of the leased property and the present value of the minimum lease payments. Each lease payment is allocated between the liability and the finance charges so as to achieve a constant rate on the finance balance outstanding. The corresponding rental obligations, net of finance charges, are included in deferred credits and other liabilities. The interest element of the finance cost is charged to the statement of comprehensive income over the lease period so as to produce a constant periodic rate of interest on the remaining balance of the liability for each period.

(b) LBP Group is the lessor

(i) Operating lease - properties leased out under operating leases are included in investment property in the statement of financial position. Rental income under operating leases is recognized in the statement of comprehensive income on a straight-line basis over the period of lease. (ii) Finance lease - when assets are leased out under a finance lease, the present value of the lease payments is recognized as a receivable. The difference between the gross receivable and the present value of the receivable is recognized as unearned income.

Lease income under finance lease is recognized over the term of the lease using the net investment method before tax, which reflects a constant periodic rate of return.

22

Revenue Recognition Interest income and fees which are considered an integral part of the effective yield of a financial asset are recognized using the effective interest method, unless collectibility is in doubt. Interest is recognized on impaired loans and other financial assets based on the rate used to discount future cash flows to their net present value. Dividend income is recognized when the right to receive payment is established. Gains or losses arising from the trading of securities and foreign currency are reported in the statement of comprehensive income. Generally, commissions, service charges and fees are recognized only upon collection or accrued where there is reasonable degree of certainty as to its collectibility. Commitment fees received to originate a loan when the loan commitment is outside the scope of PAS 39 are deferred and recognized as an adjustment to the effective interest rate. If the loan commitment expires, the fee is recognized as revenue on expiry. Borrowing Costs Borrowing costs are expensed when incurred. Changes in Accounting Policies and Disclosures New and amended Standards and Interpretations

The Group applied the following applicable new and revised accounting standards. Unless otherwise indicated, these new and revised accounting standards have no impact to the Group. Except for these standards and amended PFRS which were adopted as of January 1, 2014, the accounting policies adopted are consistent with those of the previous financial year. PAS 32, Financial Instruments: Presentation – Offsetting Financial Assets and Financial Liabilities (Amendments) The amendments clarify the meaning of “currently has a legally enforceable right to set-off” and also clarify the application of the PAS 32 offsetting criteria to settlement systems (such as central clearing house systems) which apply gross settlement mechanisms that are not simultaneous. The amendments have no impact on the Group‟s financial position or performance. PAS 36, Impairment of Assets – Recoverable Amount Disclosures for Non-Financial Assets (Amendments)

These amendments remove the unintended consequences of PFRS 13 on the disclosures required under PAS 36. In addition, these amendments require disclosure of the recoverable amounts for the assets or cash-generating units (CGUs) for which impairment loss has been recognized or reversed during the period. These amendments

23

are effective retrospectively for annual periods beginning on or after January 1, 2014 with earlier application permitted, provided PFRS 13 is also applied. The amendments have no impact on the Group‟s financial position or performance. Investment Entities (Amendments to PFRS 10, PFRS 12 and PAS 27)

These amendments provide an exception to the consolidation requirement for entities that meet the definition of an investment entity under PFRS 10. The exception to consolidation requires investment entities to account for subsidiaries at fair value through profit or loss. This amendment is not relevant to the Group since none of the entities in the Group qualifies as an investment entity under PFRS 10.

Annual Improvements to PFRS/PAS (2010-2012 cycle)

In the 2010-2012 annual improvement cycle, seven amendments to six standards were issued, which included an amendment to PFRS 13, Fair Value Measurement. The amendment to PFRS 13 is effective immediately and it clarifies that short-term receivables and payables with no stated interest rates can be measured at invoice amounts when the effect of discounting is immaterial. This amendment has no impact on the Group‟s financial position or performance. New Standards, Amendments and Interpretations not yet adopted

The Group intends to adopt the following standards when they become effective. Except as otherwise indicated, the Group does not expect the adoption of these new and amended standards to have significant impact on its financial statements. New Standards

PFRS 9, Financial Instruments – Classification and Measurement (2010 version) –

PFRS 9 (2010 version) reflects the first phase on the replacement of PAS 39 and applies to the classification and measurement of financial assets and liabilities as defined in PAS 39, Financial Instruments: Recognition and Measurement. PFRS 9 requires all financial assets to be measured at fair value at initial recognition. A debt financial asset may, if the fair value option (FVO) is not invoked, be subsequently measured at amortized cost if it is held within a business model that has the objective to hold the assets to collect the contractual cash flows and its contractual terms give rise, on specified dates, to cash flows that are solely payments of principal and interest on the principal outstanding. All other debt instruments are subsequently measured at fair value through profit or loss. All equity financial assets are measured at fair value either through other comprehensive income (OCI) or profit or loss. Equity financial assets held for trading must be measured at fair value through profit or loss. For FVO liabilities, the amount of change in the fair value of a liability that is attributable to changes in credit risk must be presented in OCI. The remainder of the change in fair value is presented in profit or loss, unless presentation of the fair value change in respect of the liability‟s credit risk in OCI would create or enlarge an accounting mismatch in profit or loss. All other PAS 39 classification and measurement requirements for financial liabilities have been carried forward into PFRS 9, including the embedded derivative separation rules and the criteria for using FVO. The adoption of the first phase of PFRS 9 will have an effect on the classification

24

and measurement of the Group‟s financial assets, but will potentially have no impact on the classification and measurement of financial liabilities.

PFRS 9 (2010 version) is effective for annual period beginning on or after January 1, 2015. This mandatory adoption date was moved to January 1, 2018 when the final version of PFRS 9 was adopted by the Philippine Financial Reporting Standards Council (FRSC). Such adoption, however, is still for approval by the Board of Accountancy (BOA). Philippine Interpretation IFRIC 15, Agreements for the Construction of Real Estate

This Interpretation covers accounting for revenue and associated expenses by entities that undertake the construction of real estate directly or through subcontractors. The Securities and Exchange Commission (SEC) and the FRSC have deferred the effectivity of this interpretation until the final Revenue standard is issued by the International Accounting Standards Board (IASB) and an evaluation of the requirements of the final Revenue standard against the practices of the Philippine real estate industry is completed. Adoption of the interpretation when it becomes effective will not have any impact on the financial statements of the Group. The following new standards and amendments issued by the IASB were already adopted by the FRSC but are still for approval by BOA. Amendments

PAS 16, Property, Plant and Equipment and PAS 38, Intangible Assets – Clarification of Acceptable Methods of Depreciation and Amortization

The revised PAS 16 and PAS 38 both establish the principle for the basis of depreciation and amortization as being the expected pattern of consumption of the future economic benefits of an asset. The amendments to PAS 16 explicitly prohibits revenue-based depreciation of property, plant and equipment while the amendments to PAS 38 introduce a rebuttable presumption that a revenue-based amortization method for intangible assets is inappropriate for the same reason that there are multiple factors that influence revenue and that not all these factors are related to the way the asset is used or consumed. The revised standards are effective for periods beginning January 1, 2016, with earlier application permitted. PAS 16, Property, Plant and Equipment and PAS 41, Agriculture – Change in Financial Reporting for Bearer Plants The amendments require entities to account for bearer plants in the same way as property, plant and equipment in PAS 16, Property, Plant and Equipment, because their operation is similar to that of manufacturing, bringing them within the scope of PAS 16, instead of PAS 41. The produce growing on bearer plants will remain within the scope of PAS 41. The amended standards are effective for annual periods beginning on or after January 1, 2016, with earlier application permitted. The amendments are not applicable to the Group.

25

PAS 27, Separate Financial Statements – Equity Method in Separate Financial Statements The amendments will allow entities to use the equity method to account for investments in subsidiaries, joint ventures and associates in their separate financial statements. Entities already applying PFRS and electing to change to the equity method in its separate financial statements will have to apply that change retrospectively. For first-time adopters of PFRS electing to use the equity method in its separate financial statements, they will be required to apply this method from the date of transition to PFRS. The amendments are effective for annual periods beginning on or after January 1, 2016, with early adoption permitted. These amendments will not have any impact on the Group‟s consolidated financial statements. PFRS 10, Consolidated Financial Statements and PAS 28, Investments in Associates and Joint Ventures – Sale or Contribution of Assets between an Investor and its Associate or Joint Venture These amendments address an acknowledged inconsistency between the requirements in PFRS 10 and those in PAS 28 (2011) in dealing with the sale or contribution of assets between an investor and its associate or joint venture. The amendments require that a full gain or loss is recognized when a transaction involves a business (whether it is housed in a subsidiary or not). A partial gain or loss is recognized when a transaction involves assets that do not constitute a business, even if these assets are housed in a subsidiary. These amendments are effective from annual periods beginning on or after January 1, 2016. Annual Improvements to PFRSs (2010 - 2012 cycle)

The Annual Improvements to PFRSs (2010 - 2012 cycle) which will take effect for annual periods beginning on or after January 1, 2015, contain non-urgent but necessary amendments to the following standards: PFRS 2, Share-based Payment – Definition of Vesting Condition The amendment revised the definitions of vesting condition and market condition and added the definitions of performance condition and service condition to clarify various issues. This amendment shall be prospectively applied to share-based payment transactions for which the grant date is on or after January 1, 2015. This amendment does not apply to the Group as it has no share-based payments. PFRS 3, Business Combinations – Accounting for Contingent Consideration in a Business Combination The amendment clarifies that a contingent consideration that meets the definition of a financial instrument should be classified as a financial liability or as equity in accordance with PAS 32. Contingent consideration that is not classified as equity is subsequently measured at fair value through profit or loss whether or not it falls within the scope of PFRS 9 (or PAS 39, if PFRS 9 is not yet adopted). The amendment shall be prospectively applied to

26

business combinations for which the acquisition date is on or after January 1, 2015. The Group shall consider this amendment for future business combinations. Revaluation Method (Amendments to PAS 16 and PAS 38 – Proportionate Restatement of Accumulated Depreciation and Amortization) The amendment clarifies that, upon revaluation of an item of property, plant and equipment, and intangible assets, the carrying amount of the asset shall be adjusted to the revalued amount, and the asset shall be treated in one of the following ways: a. The gross carrying amount is adjusted in a manner that is consistent with the

revaluation of the carrying amount of the asset. The accumulated depreciation or amortization at the date of revaluation is adjusted to equal the difference between the gross carrying amount and the carrying amount of the asset after taking into account any accumulated impairment losses.

b. The accumulated depreciation or amortization is eliminated against the gross

carrying amount of the asset. The amendments also clarify that the amount of the adjustment of the accumulated amortization should form part of the increase or decrease in the carrying amount accounted for in accordance with the standard. The amendment shall apply to all revaluations recognized in annual periods beginning on or after the date of initial application of this amendment and in the immediately preceding annual period. PAS 24, Related Party Disclosures – Key Management Personnel The amendments clarify that an entity is a related party of the reporting entity if the said entity, or any member of a group for which it is a part of, provides key management personnel services to the reporting entity or to the parent company of the reporting entity. The amendments also clarify that a reporting entity that obtains management personnel services from another entity (also referred to as management entity) is not required to disclose the compensation paid or payable by the management entity to its employees or directors. The reporting entity is required to disclose the amounts incurred for the key management personnel services provided by a separate management entity. The amendments are applied retrospectively and affect disclosures only. Annual Improvement to PFRSs (2011-2013 cycle)

The Annual Improvements to PFRSs (2011 - 2013 cycle) contain non-urgent but necessary amendments to the following standards: PFRS 1, First-time Adoption of Philippine Financial Reporting Standards – Meaning of ‘Effective PFRSs’ The amendment clarifies that an entity may choose to apply either a current standard or a new standard that is not yet mandatory, but that permits early application, provided either standard is applied consistently throughout the periods presented in the entity‟s

27

first PFRS financial statements. This amendment is not applicable to the Group as it is not a first-time adopter of PFRS. PFRS 13, Fair Value Measurement – Portfolio Exception The amendment clarifies that the portfolio exception in PFRS 13 can be applied to financial assets, financial liabilities and other contracts. The amendment is effective for annual periods beginning on or after July 1, 2014 and is applied prospectively. PAS 40, Investment Property The amendment clarifies the interrelationship between PFRS 3 and PAS 40 when classifying property as investment property or owner-occupied property. The amendment stated that judgment is needed when determining whether the acquisition of investment property is the acquisition of an asset or a group of assets or a business combination within the scope of PFRS 3. This judgment is based on the guidance of PFRS 3. This amendment is effective for annual periods beginning on or after July 1, 2014 and is applied prospectively. The amendment has no significant impact on the Group‟s financial position or performance. Annual Improvements to PFRSs (2012 - 2014 cycle)

The Annual Improvements to PFRSs (2012 - 2014 cycle) are effective for annual periods beginning on or after January 1, 2016 and are not expected to have a material impact on the Group. They include: PFRS 5, Non-current Assets Held for Sale and Discontinued Operations – Changes in Methods of Disposal The amendment is applied prospectively and clarifies that changing from a disposal through sale to a disposal through distribution to owners and vice-versa should not be considered to be a new plan of disposal, rather it is a continuation of the original plan. There is, therefore, no interruption of the application of the requirements in PFRS 5. The amendment also clarifies that changing the disposal method does not change the date of classification. PFRS 7, Financial Instruments: Disclosures – Servicing Contracts PFRS 7 requires an entity to provide disclosures for any continuing involvement in a transferred asset that is derecognized in its entirety. The amendment clarifies that a servicing contract that includes a fee can constitute continuing involvement in a financial asset. An entity must assess the nature of the fee and arrangement against the guidance in PFRS 7 in order to assess whether the disclosures are required. The amendment is to be applied such that the assessment of which servicing contracts constitute continuing involvement will need to be done retrospectively. However, comparative disclosures are not required to be provided for any period beginning before the annual period in which the entity first applies the amendments.

28

PFRS 7 – Applicability of the Amendments to PFRS 7 to Condensed Interim Financial Statements

This amendment is applied retrospectively and clarifies that the disclosures on offsetting of financial assets and financial liabilities are not required in the condensed interim financial report unless they provide a significant update to the information reported in the most recent annual report. PAS 19, Employee Benefits – Regional Market Issue regarding Discount Rate

This amendment is applied prospectively and clarifies that market depth of high quality corporate bonds is assessed based on the currency in which the obligation is denominated, rather than the country where the obligation is located. When there is no deep market for high quality corporate bonds in that currency, government bond rates must be used. PAS 34, Interim Financial Reporting – Disclosures of Information ‘Elsewhere in the Interim Financial Report’ This amendment is applied retrospectively and clarifies that the required interim disclosures must either be in the interim financial statements or incorporated by cross-reference between the interim financial statements and wherever they are included within the greater interim financial report (e.g., in the management commentary or risk report). Effective January 1, 2018

PFRS 9, Financial Instruments – Hedge Accounting and Amendments to PFRS 9, PFRS 7 and PAS 39 (2013 version)

PFRS 9 (2013 version) already includes the third phase of the project to replace PAS 39 which pertains to hedge accounting. This version of PFRS 9 replaces the rules-based hedge accounting model of PAS 39 with a more principles-based approach. Changes include replacing the rules based hedge effectiveness test with an objectives-based test that focuses on the economic relationship between the hedged item and the hedging instrument, and the effect of credit risk on that economic relationship; allowing risk components to be designated as the hedged item, not only for financial items but also for non-financial items, provided that the risk component is separately identifiable and reliably measurable; and allowing the time value of an option, the forward element of a forward contract and any foreign currency basis spread to be excluded from the designation of a derivative instrument as the hedging instrument and accounted for as costs of hedging. PFRS 9 also requires more extensive disclosures for hedge accounting. PFRS 9 (2013 version) has no mandatory effective date. The mandatory effective date of January 1, 2018 was eventually set when the final version of PFRS 9 was adopted by the FRSC. The adoption of the final version of PFRS 9, however, is still for approval by BOA. The adoption of PFRS 9 will have an effect on the classification and measurement of the Group‟s financial assets but will have no impact on the classification and measurement

29

of the Group‟s financial liabilities. The adoption will also have an effect on the Group‟s application of hedge accounting. PFRS 9, Financial Instruments (2014 or final version)

In July 2014, the final version of PFRS 9, Financial Instruments, was issued. PFRS 9 reflects all phases of the financial instruments project and replaces PAS 39, Financial Instruments: Recognition and Measurement, and all previous versions of PFRS 9. The standard introduces new requirements for classification and measurement, impairment, and hedge accounting. PFRS 9 is effective for annual periods beginning on or after January 1, 2018, with early application permitted. Retrospective application is required, but comparative information is not compulsory. Early application of previous versions of PFRS 9 is permitted if the date of initial application is before February 1, 2015. The adoption of PFRS 9 will have an effect on the classification and measurement of the Group‟s financial assets and impairment methodology for financial assets, but will have no impact on the classification and measurement of the Group‟s financial liabilities. The adoption will also have an effect on the Group‟s application of hedge accounting. The Group is currently assessing the impact of adopting this standard. The Group conducted an evaluation of the financial impact of the adoption of PFRS 9 based on the audited financial statements as of December 31, 2013 and decided not to early adopt PFRS 9 in its 2014 financial reporting. 3. Significant Accounting Judgments and Estimates

The preparation of the financial statements in compliance with PFRS requires the Group to make estimates and assumptions that affect the reported amounts of resources, liabilities, income and expenses and disclosure of contingent resources and contingent liabilities. Future events may occur which will cause the assumptions used in arriving at the estimates to change. The effects of any change in estimates are reflected in the financial statements as they become reasonably determinable. Estimates and judgments are continually evaluated and are based on historical experience and other factors, including expectations of future events that are believed to be reasonable under the circumstances. Judgments

In the process of applying the Group‟s accounting policies, Management has made the following judgments, apart from those involving estimations, which have the most significant effect on the amounts recognized in the financial statements: a. Operating lease commitments The entity has entered into commercial property leases on its investment property portfolio. The entity has determined that it retains all the significant risks and rewards of ownership of these properties which are leased out on operating leases.

30

b. Impairment losses on loans and receivables and HTM investments

The Group reviews its loans and receivables and HTM investments to assess impairment at least on an annual basis or earlier when an indicator of impairment exists. In determining whether an impairment loss should be recorded in the statement of comprehensive income, the Group makes judgments as to whether there is any observable data indicating that there is a measurable decrease in the estimated future cash flows from a portfolio of financial asset before the decrease can be identified with an individual asset in that portfolio. This evidence may include observable data indicating that there has been an adverse change in the payment status of borrowers in a group, or national or local economic conditions that correlate with defaults on assets in the group. Management uses estimates based on historical loss experience for assets with credit risk characteristics and objective evidence of impairment similar to those in the portfolio when scheduling its future cash flows. The methodology and assumptions used for estimating both the amount and timing of future cash flows are reviewed regularly to reduce any differences between loss estimates and actual loss experience. The carrying values of receivables from customers and HTM investments of the Group and the Parent are P498,001,532 and P496,290,816 as of December 31, 2014 and P363,315,524 and P361,103,483 as of December 31, 2013, respectively. c. Impairment of AFS investments

The Group determines that available-for-sale investments are impaired when there has been a significant or prolonged decline in the fair value below its cost. This determination of what is significant or prolonged requires judgment. In making this judgment, the Group evaluates among other factors, the normal volatility in price. In addition, impairment may be appropriate when there is evidence of deterioration in the financial health of the investee, industry and sector performance, changes in technology, and operational and financing cash flows. The carrying values of AFS investments of the Group and the Parent are P191,341,109 and P191,341,109 as of December 31, 2014 and P179,836,155 and P179,836,155 as of December 31, 2013, respectively. d. Classification under HTM investments The classification of non-derivative financial assets with fixed or determinable payments and fixed maturity as held-to-maturity requires significant judgment. In making this judgment, the Group evaluates its intention and ability to hold such investments to maturity. Further, the Group determines whether the investments are quoted or not; unquoted debt investments are classified under Loans and receivables. If the Group fails to keep these investments to maturity other than for specific circumstances – for example, selling an insignificant amount or close to maturity – it will be required to reclassify the entire held-to-maturity portfolio as available-for-sale. The investments would therefore be measured at fair value instead of amortized cost. The carrying values of held-to-maturity investments of the Group and the Parent are P95,814,860 and P95,025,587 as of December 31, 2014 and P40,904,585 and P40,101,183 as of December 31, 2013, respectively. e. Recognition of deferred tax asset

The Group cannot yet establish when it will realize its deductible temporary differences and carry forward benefits of NOLCO and MCIT. When the Group is already in a

31

positive tax position, the Management will review the level of deferred tax assets that it will recognize in the books. Estimation uncertainty

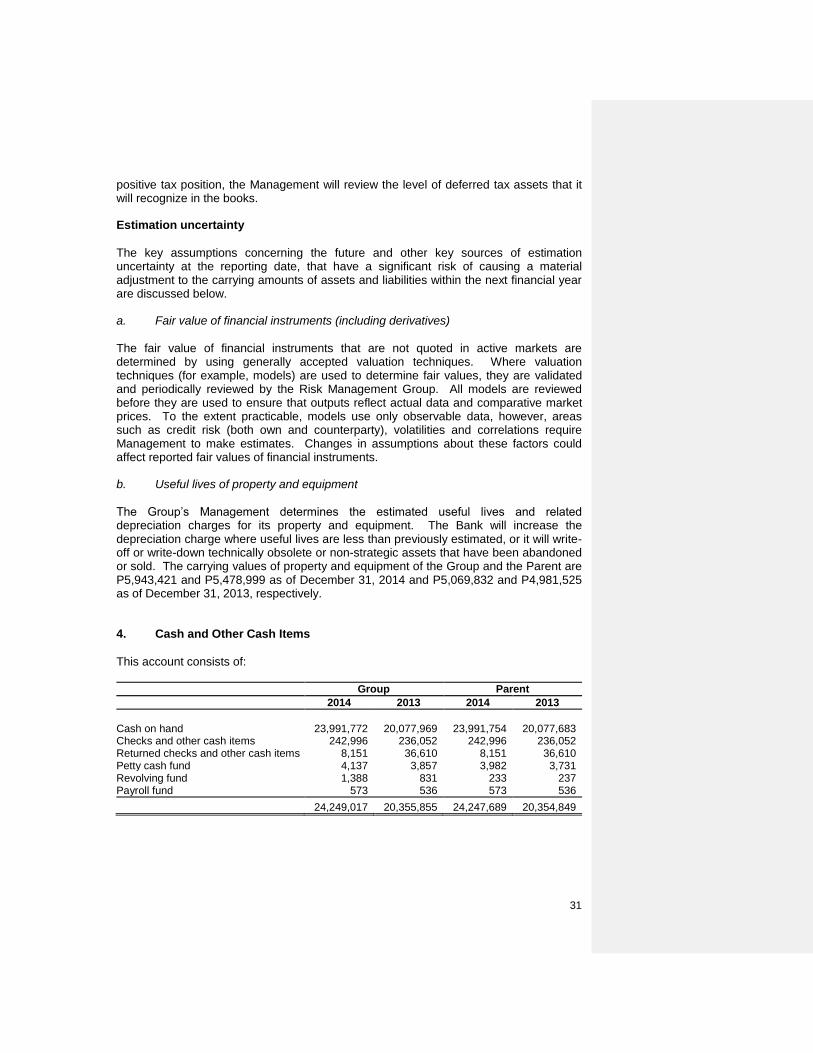

The key assumptions concerning the future and other key sources of estimation uncertainty at the reporting date, that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year are discussed below. a. Fair value of financial instruments (including derivatives) The fair value of financial instruments that are not quoted in active markets are determined by using generally accepted valuation techniques. Where valuation techniques (for example, models) are used to determine fair values, they are validated and periodically reviewed by the Risk Management Group. All models are reviewed before they are used to ensure that outputs reflect actual data and comparative market prices. To the extent practicable, models use only observable data, however, areas such as credit risk (both own and counterparty), volatilities and correlations require Management to make estimates. Changes in assumptions about these factors could affect reported fair values of financial instruments. b. Useful lives of property and equipment The Group‟s Management determines the estimated useful lives and related depreciation charges for its property and equipment. The Bank will increase the depreciation charge where useful lives are less than previously estimated, or it will write-off or write-down technically obsolete or non-strategic assets that have been abandoned or sold. The carrying values of property and equipment of the Group and the Parent are P5,943,421 and P5,478,999 as of December 31, 2014 and P5,069,832 and P4,981,525 as of December 31, 2013, respectively. 4. Cash and Other Cash Items

This account consists of: Group Parent

2014 2013 2014 2013

Cash on hand 23,991,772 20,077,969 23,991,754 20,077,683 Checks and other cash items 242,996 236,052 242,996 236,052 Returned checks and other cash items 8,151 36,610 8,151 36,610 Petty cash fund 4,137 3,857 3,982 3,731 Revolving fund 1,388 831 233 237 Payroll fund 573 536 573 536

24,249,017 20,355,855 24,247,689 20,354,849

32

5. Due from Bangko Sentral ng Pilipinas

This account represents the Parent‟s demand and special deposits in local currency maintained with BSP to meet reserve requirements and to serve as clearing account for interbank claims consistent with BSP guidelines. 6. Due from Other Banks

This account consists of:

Group Parent

2014 2013 2014 2013

Deposit with local banks 216,299 119,205 122,502 69,267 Deposit with foreign banks 6,168,740 3,077,076 6,162,883 3,071,220

6,385,039 3,196,281 6,285,385 3,140,487

The Group maintains nostro accounts on global basis with 22 foreign depository banks totaling 28 and 30 bank accounts in 2014 and 2013, respectively, the most significant of which are as follows:

2014 2013

1. Wells Fargo Bank, N.A. 2. Standard Chartered Bank, N.Y.

1. Wells Fargo Bank, N.A. 2. Standard Chartered Bank, N.Y.

3. The Bank of New York 3. Standard Chartered Bank, Tokyo 4. Standard Chartered Bank, Frankfurt 4. Mizuho Corporate Bank

5. Mizuho Corporate Bank 5. The Bank of New York

Deposits with foreign banks as of December 31, 2014 include special deposit account with Standard Chartered Bank - Tokyo and Bank of Tokyo-Mitsubishi, UFJ amounting to JPY393.22 million and JPY0.13 million, respectively, which are restricted for disbursements on special lending projects. 7. Interbank Loans Receivables

This account consists of the Parent‟s loans receivable from domestic and foreign banks amounting to P17,243,602 and P7,036,608 as of December 31, 2014 and 2013, respectively. Interbank loans receivable carry interest rates at December 31, as follows:

2014 2013

Domestic 2.31% to 3.22% 2.00% to 2.75% Foreign 0.05% to 0.18% 0.05% to 0.35%

33

8. Securities Purchased under Agreements to Resell

This account consists of:

Group Parent

2014 2013 2014 2013

Government Securities Purchased under

Reverse Repurchase Agreement 56,390,000 6,122,000 56,390,000 6,122,000

56,390,000 6,122,000 56,390,000 6,122,000

Securities Purchased under Agreements to Resell of the Group carry interest rate at 4.00 per cent and 3.50 per cent as of December 31, 2014 and 2013, respectively. 9. Financial Assets at Fair Value Through Profit or Loss

This consists of:

Group Parent

2014 2013 2014 2013

Government Securities – Domestic 13,059,318 6,215 13,059,318 6,215 Government Securities – Foreign 399,972 260,099 399,972 260,099 Private Securities – Domestic 46,634 92,116 46,634 92,116 Derivative with positive fair value 1,306,916 1,988,647 1,306,916 1,988,647

14,812,840 2,347,077 14,812,840 2,347,077

Financial Assets at Fair Value Through Profit or Loss (FVPL) of the Group carry interest rates at December 31 as follows: 2014 2013

Domestic 1.62% to 4.17% 4.80% to 10.50% Foreign 7.25% to 7.39% 1.62% to 8.00%

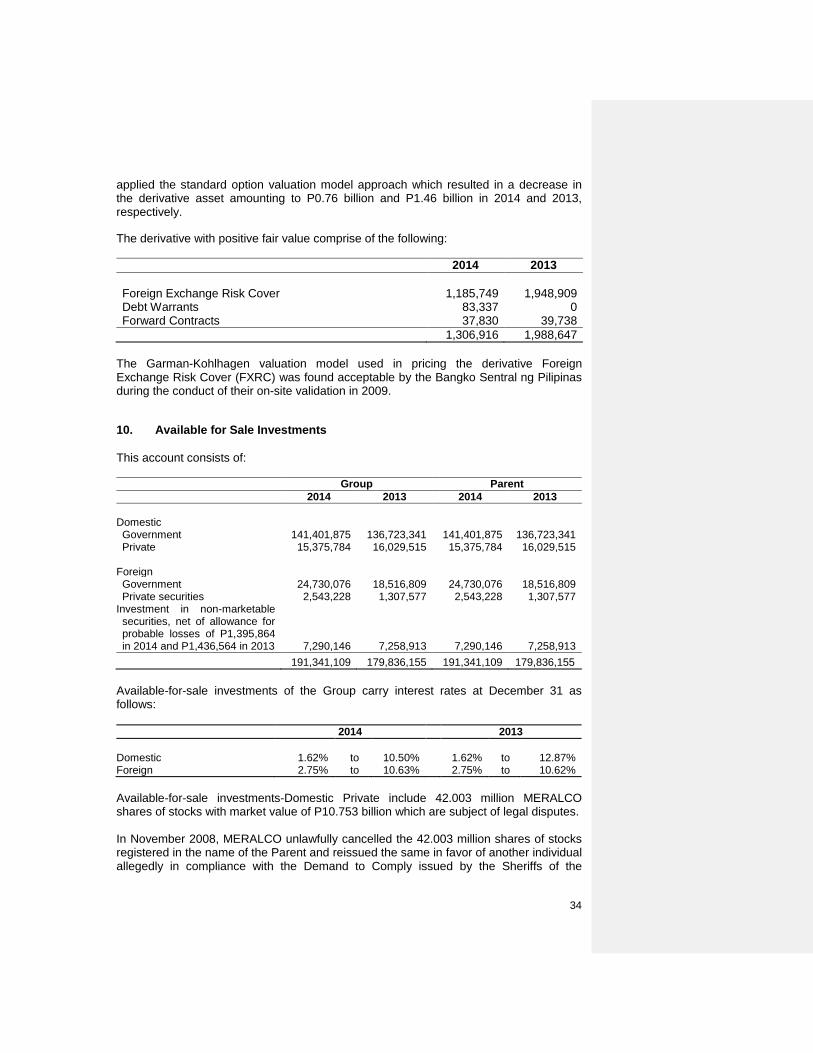

Financial Assets at FVPL includes the foreign exchange (FX) risk cover of the Parent's borrowings from multilateral agencies amounting to P1.19 billion in 2014 and P1.95 billion in 2013 which is treated as a derivative financial instrument per BSP Monetary Board Resolution No. 1063 dated August 14, 2008. Under a Memorandum of Agreement between the National Government (thru the Department of Finance) and the Parent, the former shall guarantee and assume the FX risk relating to foreign currency denominated borrowings from multilateral agencies (i.e. World Bank, Asian Development Bank, JICA, etc.) which are relent in local currencies. The fair value changes on the FX risk cover are reported immediately in the statement of comprehensive income. As of December 31, 2014, the outstanding notional amount of the FX risk cover amounted to US$7.77 million and JPY8,392.67 million. Prior to 2007, the value of the FX risk cover as an option derivative varies on the movement of the foreign exchange rates of the Bills Payable. Beginning 2007, in accordance with Monetary Board Resolution No. 1063 dated August 14, 2008, the Bank

34

applied the standard option valuation model approach which resulted in a decrease in the derivative asset amounting to P0.76 billion and P1.46 billion in 2014 and 2013, respectively.

The derivative with positive fair value comprise of the following:

2014 2013

Foreign Exchange Risk Cover 1,185,749 1,948,909 Debt Warrants 83,337 0 Forward Contracts 37,830 39,738

1,306,916 1,988,647

The Garman-Kohlhagen valuation model used in pricing the derivative Foreign Exchange Risk Cover (FXRC) was found acceptable by the Bangko Sentral ng Pilipinas during the conduct of their on-site validation in 2009.

10. Available for Sale Investments

This account consists of:

Group Parent

2014 2013 2014 2013

Domestic Government 141,401,875 136,723,341 141,401,875 136,723,341 Private 15,375,784 16,029,515 15,375,784 16,029,515

Foreign Government 24,730,076 18,516,809 24,730,076 18,516,809 Private securities 2,543,228 1,307,577 2,543,228 1,307,577

Investment in non-marketable securities, net of allowance for probable losses of P1,395,864 in 2014 and P1,436,564 in 2013 7,290,146 7,258,913 7,290,146 7,258,913

191,341,109 179,836,155 191,341,109 179,836,155

Available-for-sale investments of the Group carry interest rates at December 31 as follows: 2014 2013

Domestic 1.62% to 10.50% 1.62% to 12.87% Foreign 2.75% to 10.63% 2.75% to 10.62%

Available-for-sale investments-Domestic Private include 42.003 million MERALCO shares of stocks with market value of P10.753 billion which are subject of legal disputes. In November 2008, MERALCO unlawfully cancelled the 42.003 million shares of stocks registered in the name of the Parent and reissued the same in favor of another individual allegedly in compliance with the Demand to Comply issued by the Sheriffs of the

35

Department of Agrarian Reform (DAR) Regional Adjudicator. Of these 42.003 million shares, 3.37 million shares had been negotiated by another party; 37.23 million shares remained quarantined at the Philippine Depository and Trust Corporation (PDTC); and another 1.4 million shares has not yet been lodged with PDTC. However, the execution sale which was the basis for the issuance of the Demand to Comply was null and void from the beginning because of the Supreme Court‟s Temporary Restraining Order (TRO) enjoining the sale and the Resolution quashing all acts done pursuant to the Adjudicator‟s Writ. On December 17, 2008, the DAR Adjudication Board so ordered and required: 1) For MERALCO to cancel the Stock Certificates issued in favor of another party; 2) To restore the ownership of the subject MERALCO shares of stock to the Land

Bank of the Philippines and to record the same in the Stock and Transfer Book of MERALCO; and

3) For the Philippine Stock Exchange, Inc. (PSE), the Philippine Depository and Trust Corporation (PDTC), the Securities Transfer Services, Inc. (STS), the Philippine Dealing System Holdings, Corp. and Subsidiaries (PDS Group) and any stockholder, dealer or agent of subject MERALCO shares to forthwith STOP: trading or dealing those shares and/or affecting settlement thereof, inter alia, so as to undo the foregoing contravening acts.

The Parent‟s shares of stock in MERALCO are not part of the Agrarian Reform Fund (ARF), a fund which is solely answerable to the obligation of the National Government pursuant to its Agrarian Reform Program. In accordance with Section 63 of Republic Act 6657 (Comprehensive Agrarian Reform Law), assets of the bank cannot be used to pay for land acquisition as this shall only be sourced from the ARF. In its December 14, 2011 Decision in G.R. No. 188376, the Supreme Court directed MERALCO to return to the Land Bank of the Philippines (LBP) 42,002,750 MERALCO shares of stock. The Supreme Court further declared that the MERALCO shares of stocks are corporates assets of LBP illegally taken to satisfy the payment of just compensation that should have been appropriated only from the ARF. This ruling has become final and executory on September 11, 2012 (Entry of Judgment). LBP immediately filed a motion before the Regional Agrarian Reform Adjudicator (RARAD) for the issuance of a writ of execution to implement the Supreme Court decision. This was, however, vigorously opposed by the other party. On April 1, 2013, the RARAD finally issued the Writ of Execution. As partial compliance, MERALCO delivered to LBP 38,635,950 shares including cash dividends in the total amount of P1,206,955,617.77; and property dividends consisting of 108,884,212 shares of stock in Rockwell Land Corporation.

Still undelivered are 3,366,800 shares, plus accrued cash dividends thereon, amounting to P161,303,398.00 as of September 30, 2014, plus 9,488,394 shares of stock in Rockwell Land Corporation as property dividends, and the unpaid dividends due from the 1,402,750 MERALCO shares amounting to P8,145,009.73. These 1.4 million shares are part of the 38.63 million shares restored to LBP, but certificated in the name of the other party before the Supreme Court decision was partially implemented.

36

To recover fully the MERALCO shares and dividends, LBP sent its June 18, 2014 Letter to the Office of the Regional Adjudicator Region IV – B (MIMAROPA) requesting the office to direct the Sheriff to perform all necessary acts for the full implementation of the April 1, 2013 Writ of Execution such as, but not limited to, the issuance of another Demand to Comply to be served upon MERALCO. LBP again sent the August 15, 2014 Letter to RARAD reiterating its request to expedite the full implementation of the Supreme Court‟s ruling in G.R. No. 188376 and to prevent further damage to LBP. On February 6, 2015, LBP received the January 24, 2014 Sheriff’s Report from the Sheriff of the Regional Adjudicator Region IV-B (MIMAROPA) regarding MERALCO‟s partial compliance of the December 14, 2011 Supreme Court Decision in G.R. No. 188376. LBP‟s June 18, 2014 Letter and August 15, 2014 Letter were not acted upon by the RARAD, and no further writ of execution or demand to comply were issued. Since RARAD no longer issued a writ of execution or demand to comply, LBP sent the February 11, 2015 Letter addressed to MERALCO to demand the delivery of the remaining 3,366,800 shares of stocks plus unpaid dividends. MERALCO failed to respond to LBP‟s demand. On account of the January 24, 2014 Sheriff’s Report and MERALCO‟s failure to respond to LBP‟s February 11, 2015 Letter, LBP prepared a petition for contempt against MERALCO and its representatives for failing to deliver the remaining 3,366,800 shares of stocks plus accrued dividends and the unpaid dividends due from the 1,402,750 MERALCO shares delivered to LBP, and to compel full compliance with the December 14, 2011 Supreme Court Decision.

On March 10, 2015, the petition was sent to the Office of the Government Corporate Counsel (OGCC) for review and signature. OGCC approved the filing of the petition before the Supreme Court. On April 14, 2015, the Petition to Cite Respondents in Indirect Contempt was filed before the Supreme Court. Parent‟s Accumulated market gains/losses on AFS government and private issues as of December 31, 2014 amounted to P15,856.43 million. Parent‟s Net unrealized gains/losses on AFS was P13,505.33 million. The difference in the amount outstanding of the local currency accumulated market gains/losses and net unrealized gains/losses on AFS as of December 31, 2014 in the amount of P2,351.10 million, represents the remaining unamortized portion of the net unrealized gain or loss, that has been recognized directly in equity when the Available-for-sale securities has been reclassified to Held to maturity securities on various dates. The said amount shall be continuously amortized to profit or loss over the remaining life of the Held-to-maturity securities. Total Investment in Non-Marketable Equity Securities (INMES) account of the Parent includes investment of US$143.15 million (P6,781.38 million) in Metro Rail Transit Corporation‟s (MRTC) preference shares and Unsecuritized Equity Rental Payments. In 2008, the National Government, as confirmed through Executive Order No. 855 dated January 18, 2010, instructed LBP and the Development Bank of the Philippines (DBP) to acquire majority interest in MRTC as a result of the recommendation made by the inter-agency Committee tasked to review the MRT III project. In the same year, the LBP

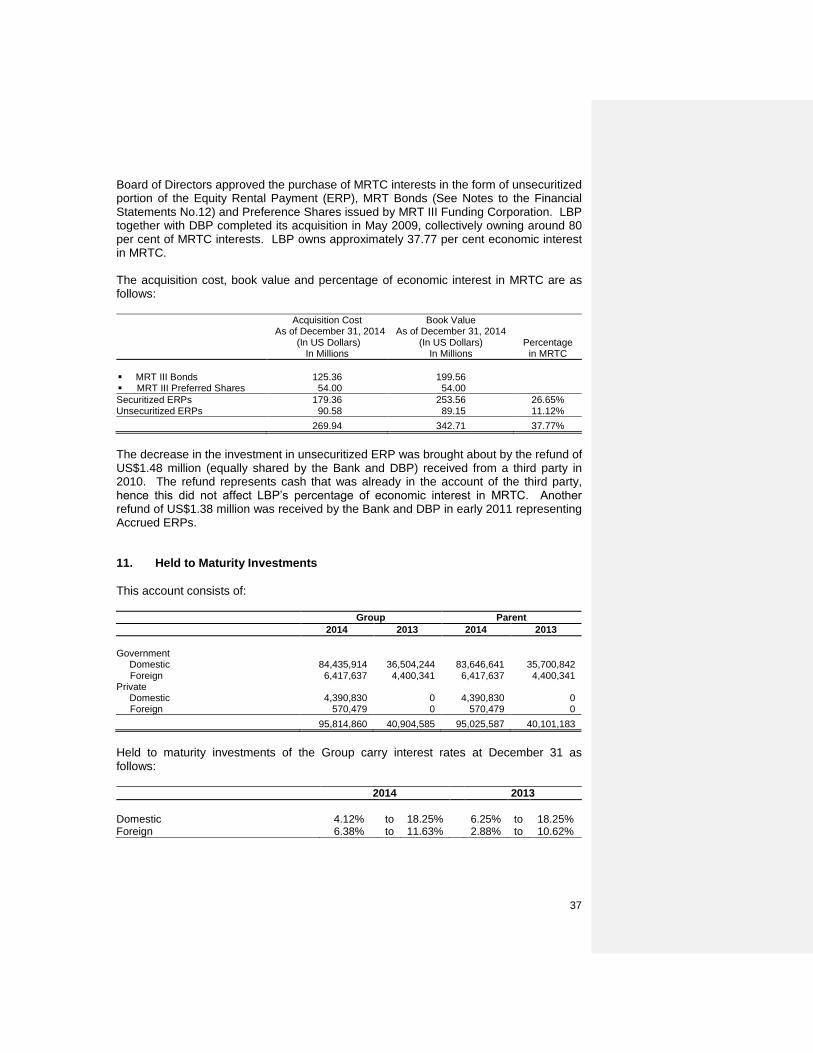

37

Board of Directors approved the purchase of MRTC interests in the form of unsecuritized portion of the Equity Rental Payment (ERP), MRT Bonds (See Notes to the Financial Statements No.12) and Preference Shares issued by MRT III Funding Corporation. LBP together with DBP completed its acquisition in May 2009, collectively owning around 80 per cent of MRTC interests. LBP owns approximately 37.77 per cent economic interest in MRTC. The acquisition cost, book value and percentage of economic interest in MRTC are as follows:

Acquisition Cost As of December 31, 2014

(In US Dollars) In Millions

Book Value As of December 31, 2014

(In US Dollars) In Millions

Percentage in MRTC

MRT III Bonds 125.36 199.56 MRT III Preferred Shares 54.00 54.00

Securitized ERPs 179.36 253.56 26.65% Unsecuritized ERPs 90.58 89.15 11.12%

269.94 342.71 37.77%

The decrease in the investment in unsecuritized ERP was brought about by the refund of US$1.48 million (equally shared by the Bank and DBP) received from a third party in 2010. The refund represents cash that was already in the account of the third party, hence this did not affect LBP‟s percentage of economic interest in MRTC. Another refund of US$1.38 million was received by the Bank and DBP in early 2011 representing Accrued ERPs. 11. Held to Maturity Investments

This account consists of:

Group Parent

2014 2013 2014 2013

Government

Domestic 84,435,914 36,504,244 83,646,641 35,700,842 Foreign 6,417,637 4,400,341 6,417,637 4,400,341

Private Domestic 4,390,830 0 4,390,830 0 Foreign 570,479 0 570,479 0

95,814,860 40,904,585 95,025,587 40,101,183

Held to maturity investments of the Group carry interest rates at December 31 as follows: 2014 2013

Domestic 4.12% to 18.25% 6.25% to 18.25% Foreign 6.38% to 11.63% 2.88% to 10.62%

38

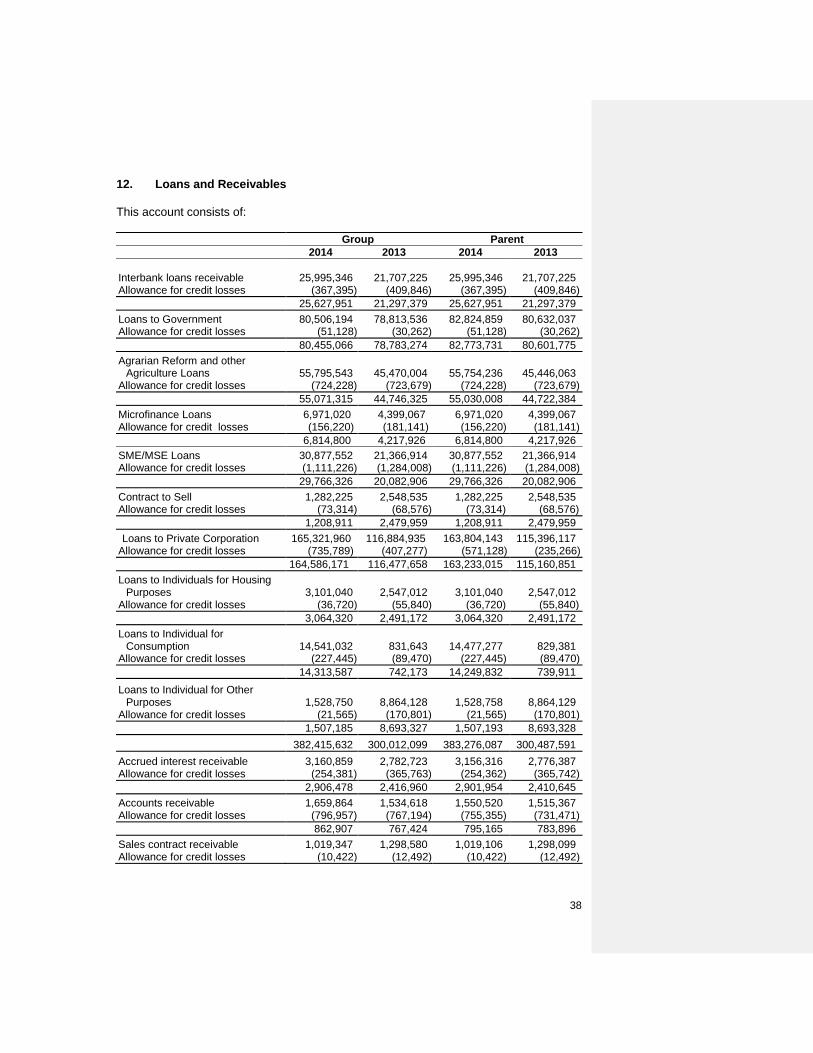

12. Loans and Receivables

This account consists of: Group Parent

2014 2013 2014 2013

Interbank loans receivable 25,995,346 21,707,225 25,995,346 21,707,225 Allowance for credit losses (367,395) (409,846) (367,395) (409,846)

25,627,951 21,297,379 25,627,951 21,297,379

Loans to Government 80,506,194 78,813,536 82,824,859 80,632,037 Allowance for credit losses (51,128) (30,262) (51,128) (30,262)

80,455,066 78,783,274 82,773,731 80,601,775

Agrarian Reform and other Agriculture Loans 55,795,543 45,470,004 55,754,236 45,446,063

Allowance for credit losses (724,228) (723,679) (724,228) (723,679)

55,071,315 44,746,325 55,030,008 44,722,384

Microfinance Loans 6,971,020 4,399,067 6,971,020 4,399,067 Allowance for credit losses (156,220) (181,141) (156,220) (181,141)

6,814,800 4,217,926 6,814,800 4,217,926

SME/MSE Loans 30,877,552 21,366,914 30,877,552 21,366,914 Allowance for credit losses (1,111,226) (1,284,008) (1,111,226) (1,284,008)

29,766,326 20,082,906 29,766,326 20,082,906

Contract to Sell 1,282,225 2,548,535 1,282,225 2,548,535 Allowance for credit losses (73,314) (68,576) (73,314) (68,576)

1,208,911 2,479,959 1,208,911 2,479,959

Loans to Private Corporation 165,321,960 116,884,935 163,804,143 115,396,117 Allowance for credit losses (735,789) (407,277) (571,128) (235,266)

164,586,171 116,477,658 163,233,015 115,160,851

Loans to Individuals for Housing Purposes 3,101,040 2,547,012 3,101,040 2,547,012

Allowance for credit losses (36,720) (55,840) (36,720) (55,840)

3,064,320 2,491,172 3,064,320 2,491,172

Loans to Individual for Consumption 14,541,032 831,643 14,477,277 829,381

Allowance for credit losses (227,445) (89,470) (227,445) (89,470)

14,313,587 742,173 14,249,832 739,911

Loans to Individual for Other Purposes 1,528,750

8,864,128 1,528,758

8,864,129 Allowance for credit losses (21,565) (170,801) (21,565) (170,801)

1,507,185 8,693,327 1,507,193 8,693,328

382,415,632 300,012,099 383,276,087 300,487,591

Accrued interest receivable 3,160,859 2,782,723 3,156,316 2,776,387 Allowance for credit losses (254,381) (365,763) (254,362) (365,742)

2,906,478 2,416,960 2,901,954 2,410,645

Accounts receivable 1,659,864 1,534,618 1,550,520 1,515,367 Allowance for credit losses (796,957) (767,194) (755,355) (731,471)

862,907 767,424 795,165 783,896

Sales contract receivable 1,019,347 1,298,580 1,019,106 1,298,099 Allowance for credit losses (10,422) (12,492) (10,422) (12,492)

39

Group Parent

2014 2013 2014 2013

1,008,925 1,286,088 1,008,684 1,285,607

Due from ARF 316,154 21,045 316,154 21,045