notes from the ambassador bank vault april 11, 2017 flying ... · business activity to retain and...

TRANSCRIPT

1 | P a g e

Notes from the Ambassador Bank Vault April 11, 2017

Flying Under The Radar: Small and Micro-Cap Banks in Central Pennsylvania

“You don’t come to Central Pennsylvania on a low-carb diet, that’s for sure,” – anonymous Visitors Bureau representative. Central Pennsylvania is a fragmented banking market – there are many smaller community banks, but only a few with assets greater than $2 billion. We define Central Pennsylvania as the area ranging from Maryland on the south to New York State on the north; and stretching through the prime farmlands of Lancaster County to the western border of Centre County. Please see the map on Page 7.

This report highlights the publicly-traded banks in Central Pennsylvania with total assets between $700 million and $5.0 billion. As shown below, there are 11 institutions headquartered in this region that fit this criterion. We opine that the community banks within this range are large enough to operate fairly efficiently and are small enough to deliver personalized services. These bank stocks typically trade under the radar screen – they are not widely followed by brokerage firms or institutional investors for several reasons, which include small market capitalizations and low trading volumes. Community banks in Central Pennsylvania have generally performed well since the Great Recession as most management teams have proven resourceful with regard to operating in a slower growth economy. Credit quality has been good, lower-cost deposit bases have remained intact, and capital has not been a serious issue. However, revenue generation – particularly loan growth – remains spotty although there are pockets with superior growth prospects. The longer-term challenge for much of Central Pennsylvania is to create sufficient business activity to retain and attract Millennials, who are just starting to assert their economic power.

Figure 1

Institution HQ Ticker Stock Price

($)

Mkt Cap

($mm)

Total Assets

($000s)

Tang Eq/ Assets

(%)

Div Yld (%)

LTM P/E (x)

Price/ TBV (%)

Insider Owner

(%)

Inst. Owner

(%)

ACNB Corporation Gettysburg ACNB 29.75 180 1,206,320 9.4 2.7 16.5 160 3 18 Citizens & Northern Corp. Wellsboro CZNC 22.70 276 1,242,292 14.1 4.6 17.5 158 3 29 Citizens Financial Services Mansfield CZFS 52.76 175 1,223,018 8.4 3.2 14.0 174 12 8 Codorus Valley Bancorp, Inc. York CVLY 26.18 221 1,611,587 9.5 2.1 16.9 145 4 53 ENB Financial Corp Ephrata ENBP 35.15 100 984,253 9.6 3.2 13.3 106 2 31 First Keystone Corporation Berwick FKYS 25.55 145 984,283 9.4 4.2 15.2 160 12 2 Franklin Financial Services Chambersburg FRAF 30.35 131 1,127,443 9.6 2.8 16.1 122 4 1 Kish Bancorp, Inc. Belleville KISB 54.00 67 725,071 7.2 3.4 14.5 129 16 1 Mid Penn Bancorp, Inc. Millersburg MPB 27.20 115 1,032,599 6.4 1.9 14.7 174 12 5 Orrstown Financial Services Shippensburg ORRF 20.05 167 1,414,504 9.5 2.0 24.8 124 12 42 Penns Woods Bancorp, Inc. Williamsport PWOD 42.99 204 1,348,590 9.0 4.4 16.3 171 4 28 Median 167 1,206,320 9.4 3.2 16.1 158 4 18

Source: S&P Global Market Intelligence. Pricing data as of April 7, 2017. Financial data as of or for the 12 months ending Dec. 31, 2016. Rick Weiss Matt Resch Rob Pachence Dave Danielson 610.724.7133 610.351.1633 610.351.1633 240.242.4083 [email protected] [email protected] [email protected] [email protected]

2 | P a g e

Table of Contents Highlights ..................................................................................................................................................... 3

Market Area ................................................................................................................................................. 7

Company Descriptions ................................................................................................................................. 8

Company Ratios ......................................................................................................................................... 19

Mergers and Acquisitions .......................................................................................................................... 22

Appendix A: Deposit Market Share by Selected County ............................................................................ 25

Random (But Not Alternative) Central Pennsylvania Facts

• The Shawnee and Delaware Indians were State College’s earliest inhabitants. The valley and Mount Nittany are named for the mythical princess Nita-Nee, a Lenni-Lenape of the Delaware Tribe.

• The State College Area High School was the first U.S. school to teach drivers education in 1958.

• In 1728, Chester County residents complained that “thieves, vagabonds, and ill people” had infested the westernmost areas of the county, which led to the creation of Lancaster County in 1730.

• Despite its origins as a county founded by “deplorables”, Lancaster County formed the Union Fire Company in 1742, based on an idea by Benjamin Franklin. It was the first in the nation.

• The nation’s first major nuclear power plant accident was at Three Mile Island (Dauphin County) in 1979.

• The streetlights in Hershey are shaped like the famous HERSHEY®’S KISSES.

• Adams County is on the Mason-Dixon Line, which divided the North and South during the Civil War.

• Central Pennsylvania is more conservative; and clearly divided politically from southeastern Pennsylvania and the greater Pittsburgh metroplitan area.

• In 1906, President Theodore Roosevelt described the Harrisburg Capitol as “the handsomest building that I ever saw.”

3 | P a g e

Highlights

• This Industry Report highlights key performance ratios and valuation metrics of 11 Central Pennsylvania community banks using December 2016 quarter data.

• There are 166 depository institutions, including 89 which are publicly-traded, in Pennsylvania. The top five banks have a combined deposit market share of approximately 51%. PNC Financial Services (NYSE: PNC) is the market leader with a 24% deposit share. Of the top ten Pennsylvania banks in terms of market share, only PNC and F.N.B. Corporation (NYSE: FNB) are headquartered in-state.

• The median return on assets (ROA) and return on average tangible common equity (ROATCE) of the 11 Central Pennsylvania community banks highlighted herein were 0.85% and 9.7%, respectively, compared with 0.84% and 8.9% for all Pennsylvania community banks of similar asset size. The same ratios were 0.81% and 8.6% for the same-sized banks in the mid-Atlantic region. (These ratios use the most recent trailing 12-months financial data.)

• The 11 highlighted banks generally have solid balance sheets that reflect strong asset quality, solid funding sources, and acceptable tangible capital ratios. Revenue generation, however, is likely to remain a challenge particularly if the yield curve should flatten or significant loan growth fails to materialize. Spread income, as is the case with community banks in general, represents the overwhelming majority of revenue.

• The weighted average yields on loans and investment securities vary considerably among the highlighted institutions. Prolonged historically low interest rates have dialed up the pressure on asset/liability officers to maximize profitability without sacrificing risk management standards.

• Based on anecdotal evidence, loan demand has slowed in the first quarter of 2017, reflecting uncertainty among small business owners. Community banks are generally exposed to commercial real estate, middle market commercial lending, and residential mortgage lending. The loan composition for each of the highlighted banks is shown in the Company Descriptions section of this report.

• For community banks in general, increased commercial real estate (“CRE”) loan concentration has attracted more regulatory scrutiny. Bank regulators, including The Office of the Comptroller of the Currency (“OCC”), the Board of Governors of the Federal Reserve System (“Fed”), and the Federal Deposit Insurance Corporation (“FDIC”) have greater concerns regarding low capitalization rates and fast-appreciating property values.

• Institutions with outsized CRE loan portfolios should expect regulators to require more detailed plans to identify, measure, and monitor CRE concentrations; raise underwriting standards; slow growth; and/or to raise capital.

• Central Pennsylvania is home to 4.4 million people, or about half of Pennsylvania’s population. Culturally and demographically, the Central Pennsylvania population is best characterized by what it is not – similar to Philadelphia or Pittsburgh markets!

• According to the U.S. Bureau of Labor Statistics, the Harrisburg-Carlisle market and Pennsylvania state unemployment rates were 4.4% and 5.0%, respectively, in February 2017. The rate was 4.7% for the nation in April 2017.

• Fairly recent acquisitions of a few larger Central Pennsylvania banks created opportunities for locally-based

institutions. These deals include BB&T Corporation’s (NYSE: BBT) acquisitions of Susquehanna Bancshares and National Penn Bancshares; F.N.B. Corporation’s purchase of Metro Bancorp, Inc. and the S&T Bancorp (NASDAQ: STBA) acquisition of Integrity Bancshares, Inc.

• Smaller institutions often combine to achieve economies of scale, including the ability to raise loans-to-one

borrower limits. Depending upon the deal price, acquiring core deposits may be preferable vs. organic growth. This becomes even more vital in a rising interest rate environment as core deposits become more valued.

4 | P a g e

• Several smaller Pennsylvania banks have expanded into faster-growing market areas. For example,

Citizens Financial Services, Inc. (OTC Pink: CZFS) based in northcentral Pennsylvania, acquired First National Bank of Fredericksburg in Lebanon County. Other banks that have recently expanded their presence in Lancaster County include Centric Financial Corp (OTC Pink: CFCX), Mid-Penn Bancorp, Inc. (NASDAQ: MPB), Orrstown Financial Services (NASDAQ: ORRF), and Univest Corporation of Pennsylvania (NASDAQ: UVSP). Univest, which entered Lancaster County in 2016, recently opened its fourth retail office in that county.

• Effective cyber-security remains a huge concern for banks of all sizes and involves much more than a one-

time technology upgrade.

• To date, most of the banking industry’s investment in technology has been defensive in order to meet regulatory concerns. At some point, however, banks will have to adapt to the Millennial Generation’s preference to conduct business transactions online.

5 | P a g e

Valuation Summary Figure 2

Valuation metrics generally appear rich due to the bank stock rally following Donald Trump’s election. Investor optimism is attributable to widespread beliefs (without much supporting data) that his Administration’s pro-business/growth policies such as less regulations and taxes, will lead to higher interest rates and steeper yield curve; and in turn, significantly lift bank earnings. This may or may not bring more bank mergers – potential buyers have stronger currencies, but banks are sold and not bought; and potential sellers may prefer independence if the operating environment improves.

Source: S&P Global Market Intelligence. Pricing data as of April 7, 2017. Financial data as of or for the period ending Dec. 31, 2016. Investors expect a certain level of return to compensate them for their investment. Because the stock price theoretically should reflect expectations regarding the level of future dividends, earnings and earnings growth ultimately determine the valuation. In theory, if a company fails to generate a required level of return, shareholders will sell shares until the price equals the cost of capital. On the other hand, higher returns should drive the share price higher. An added degree of caution is required when analyzing returns on equity (ROE) for banks due to legislative/regulatory demands for capital. Financial institutions must exceed (or at least match) regulatory requirements and publish the ratios in public financial reports. Capital levels, therefore, are often higher than needed strictly to maximize economic profit.

Some of the companies with particularly high ROEs may also be those with the lower equity ratios, which inflates the ROE relative to peers with strong equity ratios. A few companies with particularly high ROE ratios may not be able to sustain them if regulators or investors demand more equity capital. Companies with very high equity ratios, on the other hand, have relatively understated ROEs. The following figures, therefore, are best viewed along with other financial data to assess the overall profitability and risk of the bank in question.

Median LTM

P/E (x)

Median Price/

TBV (%)

Central PA banks in this Industry Report 16.1 158 All Pennsylvania banks and thrifts 15.6 130 All U.S. banks and thrifts 17.4 135

6 | P a g e

Figure 3: Before and after the U.S. Presidential Election

Source: S&P Global Market Intelligence. Pricing data as of April 7, 2017. Financial data as of or for the 12 months ending Dec. 31, 2016.

Source: S&P Global Market Intelligence. Pricing data as of June 10, 2016. Financial data as of or for the 12 months ending Mar. 31, 2016.

7 | P a g e

Market Area

Home to approximately 4.4 million people, the Central Pennsylvania market area is primarily rural with pockets of smaller metropolitan areas. The region features prime farmland, national forests, and major rivers. We believe that many natural barriers, such as mountains, forests, and rivers have separated communities and tend to limit widespread merger and acquisition activity across the state. Central Pennsylvania encompasses many counties which are more countryside and slower-growing compared with other parts of the state. Several banks’ core markets, however, include much of the Marcellus Shale gas fields and would likely see significantly increased economic activity if and when energy commodity prices rebound. The Marcellus Shale gas fields stretch 600 miles along the Appalachian Mountains from New York State to West Virginia. According to the Pennsylvania Department of Labor and Industry, about 90,000 direct and indirect jobs have been created – about 1.5% of total employment in a state with 5.7 million jobs. Although drilling and the attributes of Marcellus Shale are hotly debated across the state (and political lines), it appears evident that the economic benefits are primarily realized in areas where drilling occurs, rather than throughout the entire state. The following map highlights the Central Pennsylvania region as defined in this report. Figure 4

Central Pennsylvania Region

8 | P a g e

Company Descriptions

ACNB Corporation (NASDAQ: ACNB). Headquartered in Gettysburg, ACNB’s principal market area is Adams County, located in southcentral Pennsylvania. Adams County depends on agriculture, industry, and tourism to provide employment for its residents. The company also operates in the rural areas of the Harrisburg-Carlisle MSA and York-Hanover MSA and parts of Franklin County and serves its marketplace through 22 branches. ACNB provides full-service commercial banking and operates under a charter from the Pennsylvania Department of Banking and Securities. On November 22, 2016, ACNB agreed to acquire Maryland-based, New Windsor Bancorp, which had total assets of approximately $311 million. As of December 31, 2016, ACNB had total assets of $1.2 billion, total deposits of $967.6 million, and total stockholders’ equity of $120.1 million.

Source: S&P Global Market Intelligence

9 | P a g e

Citizens & Northern Corporation (NASDAQ: CZNC). The company is headquartered in Wellsboro, which is the county seat of Tioga County and home of Pennsylvania’s Grand Canyon. Virtually all of the company’s offices are located in the “Marcellus Shale,” an area extending across portions of New York State, Pennsylvania, Ohio, Maryland, West Virginia and Virginia. In recent years, most of the Pennsylvania counties in which the company operates were significantly affected by an upsurge in natural gas exploration, as technological developments made exploration of the Marcellus Shale commercially feasible. After a surge of activity in 2009 through most of 2011, the market price of natural gas declined, causing Marcellus Shale natural gas exploration activity to slow, though some activity has continued to occur. Through December 31, 2016, Citizens & Northern has not experienced significant credit issues as a result of the expansion and subsequent reduction in Marcellus Shale-related activity. Approximately 70-75% of the company’s revenue is derived from spread income. As of December 31, 2016, total assets, deposits, and shareholders’ equity were $1.2 billion, $983.8 million, and $186.0 million, respectively.

Source: S&P Global Market Intelligence

10 | P a g e

Citizens Financial Services, Inc. (OTC Pink: CZFS). Headquartered in Mansfield, Tioga County, Citizens Financial is a commercial bank engaged in a broad range of banking activities and services for individual, business, governmental and institutional customers. The company’s primary market area consists of Bradford, Clinton, Potter and Tioga counties in north central Pennsylvania and Allegany, Steuben, Chemung and Tioga counties in southern New York State. With the completion of the First National Bank of Fredericksburg acquisition on June 30, 2015, the company added seven additional banking offices in south central Pennsylvania; four offices in Lebanon Country, two offices in Schuylkill County, and one office in Berks County. During 2016, the bank opened a full service branch in Lancaster and Union counties, Pennsylvania. Approximately 80-85% of the company’s revenue is derived from spread income. For each of the past five years, the company’s return on average assets (ROA) and return on average equity has exceeded 1.0% and 10.0%, respectively. As of December 31, 2016, total assets, deposits, and shareholders’ equity were $1.2 billion, $1.0 billion, and $123.3 million, respectively.

Source: S&P Global Market Intelligence

11 | P a g e

Codorus Valley Bancorp, Inc. (NASDAQ: CVLY). Based in York County, Codorus Valley Bancorp is a Pennsylvania business corporation whose primary business consists of managing PeoplesBank, which was organized in 1864. PeoplesBank, which is a Pennsylvania-chartered bank, offers a full range of business and consumer banking services. Codorus Valley operates 26 financial centers located in York and Cumberland counties, Pennsylvania, and in Baltimore, Harford and Carroll counties, and Baltimore City, Maryland. Most of the company’s business is with customers in York County, Pennsylvania and northern Maryland. The company had the second largest share of deposits in York County with deposits totaling 14.1 percent of the market as of June 30, 2016, the latest available measurement date. Approximately 80-85% of the company’s revenue is derived from spread income. As of December 31, 2016, Codorus Valley had total consolidated assets of $1.6 billion, total deposits of $1.3 billion, and total shareholders’ equity of $155.0 million.

Source: S&P Global Market Intelligence

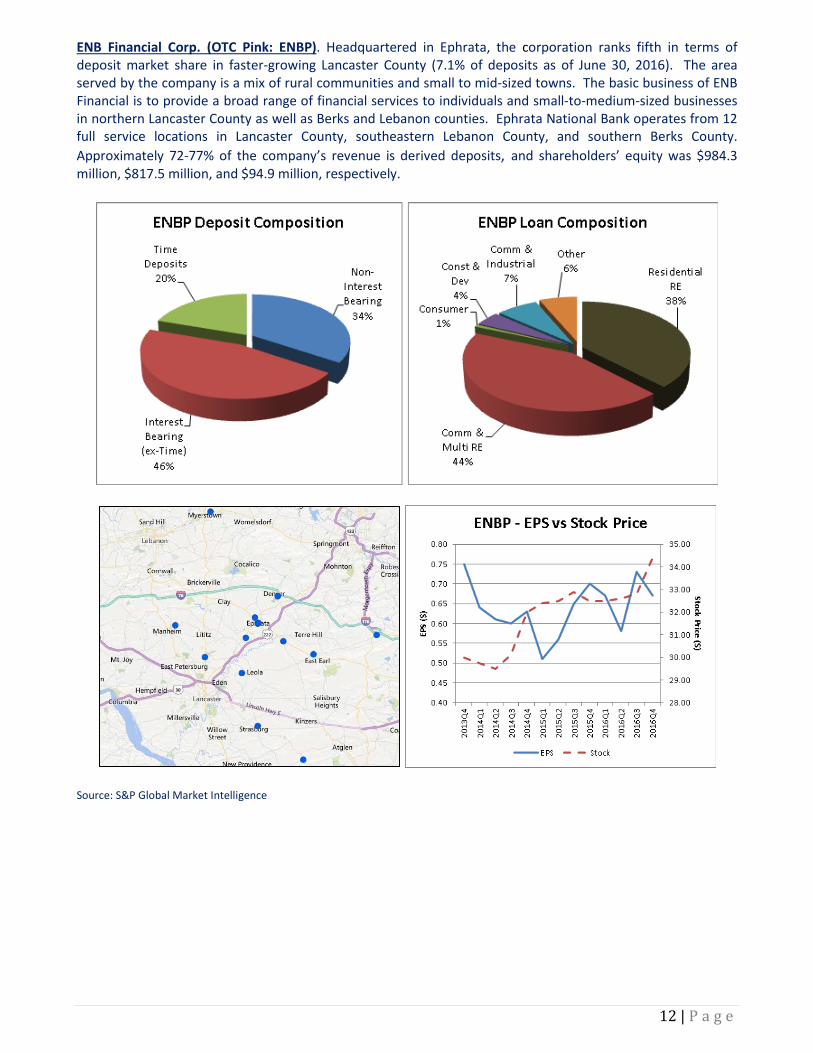

12 | P a g e

ENB Financial Corp. (OTC Pink: ENBP). Headquartered in Ephrata, the corporation ranks fifth in terms of deposit market share in faster-growing Lancaster County (7.1% of deposits as of June 30, 2016). The area served by the company is a mix of rural communities and small to mid-sized towns. The basic business of ENB Financial is to provide a broad range of financial services to individuals and small-to-medium-sized businesses in northern Lancaster County as well as Berks and Lebanon counties. Ephrata National Bank operates from 12 full service locations in Lancaster County, southeastern Lebanon County, and southern Berks County. Approximately 72-77% of the company’s revenue is derived deposits, and shareholders’ equity was $984.3 million, $817.5 million, and $94.9 million, respectively.

Source: S&P Global Market Intelligence

13 | P a g e

First Keystone Corporation (OTC Pink: FKYS). First Keystone is a Pennsylvania business corporation and bank holding company of First Keystone Community Bank. Originally formed in 1864, First Keystone Community Bank is a Pennsylvania-chartered institution and has a commercial banking operation and trust department as its major lines of business. The primary market area reaches from Monroe and Montour counties along the Interstate 80 corridor through parts of Columbia and Luzerne counties as well as other adjoining counties. The company’s eastern market area is centered in Stroudsburg, Pennsylvania and serves all of Monroe County, as well as adjoining counties of Pike and Northampton. The market is a mix of rural communities and small to mid-sized towns. Approximately 75-80% of the company’s revenue is derived from spread income. At December 31, 2016, First Keystone had total consolidated assets, deposits, and stockholders’ equity of approximately $984.2 million, $726.0 million, and $109.7 million, respectively.

Source: S&P Global Market Intelligence

14 | P a g e

Franklin Financial Services Corporation (OTCQX: FRAF). Headquartered in Chambersburg, in south central Pennsylvania, Franklin conducts substantially all of its business through its wholly-owned banking subsidiary, F&M Trust. Established in 1906, F&M Trust is a full-service, Pennsylvania-chartered commercial bank and trust company. The company offers a wide variety of banking services to businesses, individuals, and governmental entities and operates 22 community banking offices. There are six commercial bank competitors in Franklin County and the company has approximately 31% of the Franklin County deposit market share. Franklin’s approximate deposit market share in other counties is: Fulton (33%), Cumberland (3%) and Huntingdon (3%). Approximately 75% of the company’s revenue is derived from spread income. As of December 31, 2016, total assets, deposits, and stockholders’ equity were $1.1 billion, $982.1 million, and $116.5 million, respectively. Trust assets under management were $622.6 million.

Source: S&P Global Market Intelligence

15 | P a g e

Kish Bancorp (OTC PInk: KISB). Headquartered in Belleville (near State College), Kish operates 14 banking offices and financial centers in Centre, Huntingdon, and Mifflin counties. Kish was organized in 1935, through a merger of Farmers National Bank of Belleville and The Belleville National Bank, both of which can be traced to the early 20th century. The core of Kish’s business is focused on its local communities and serving the needs of its individuals, families, and businesses in its market area. As of December 31, 2016, total assets, deposits, and shareholders’ common equity were $725.1 million, $561.9 million, and $53.6 million, respectively.

Source: S&P Global Market Intelligence

16 | P a g e

Mid-Penn Bancorp (NASDAQ: MPB). Headquartered in Millersburg (near Harrisburg), Mid-Penn Bank operates 21 branches in six Central Pennsylvania counties. Millersburg Bank, the predecessor to Mid-Penn, was organized shortly after the Civil War in 1868 and obtained trust powers in 1935. The company is supervised by the Pennsylvania Department of Banking and Securities and the FDIC. Mid-Penn is a commercially-oriented bank, which caters to small and mid-sized businesses and retail customers. The company also provides a full range of trust and retail investment services. The company acquired Phoenix Bancorp on March 1, 2015, which increased total assets by approximately $140 million and expanded the company’s presence in Schuylkill County and established a presence in Luzerne County. Approximately 85-90% of the company’s revenue is derived from spread income. On March 30, 2017, the company agreed to acquire Scottdale Bank & Trust Co., (OTC Pink: SDLJ) which is based in western Pennsylvania and had total assets of $263 million. Ambassador Financial Group, Inc. served as financial advisor to Scottdale. As of December 31, 2016, total assets, deposits, and shareholders’ common equity were $1.0 billion, $935.4 million, and $70.5 million, respectively.

Source: S&P Global Market Intelligence

17 | P a g e

Orrstown Financial Services, Inc (NASDAQ: ORRF). Headquartered in Shippensburg, Orrstown Financial was organized in 1987, and is the holding company for Orrstown Bank. The bank was originally organized in 1919 as a state-chartered bank. Orrstown provides banking and bank-related services through 24 offices, located in South Central Pennsylvania, principally in Cumberland, Franklin, Lancaster, Dauphin, and Perry counties and in Washington County, Maryland. The bank grants commercial, residential, consumer and agribusiness loans in its market areas. A majority of the company’s loan assets are loans for business purposes. Approximately 62% of the loan portfolio is comprised of commercial loans and 65-70% of the company’s revenue is derived from spread income. As of December 31, 2016, total assets, deposits, and shareholders’ common equity were $1.4 billion, $1.0 billion, and $133.1 million, respectively. Trust assets under management were $1.1 billion.

Source: S&P Global Market Intelligence

18 | P a g e

Penns Woods Bancorp (NASDAQ: PWOD). Headquartered in Williamsport, Penns Woods Bancorp conducts business across six central Pennsylvania counties through 24 branches. The holding company’s two banking subsidiaries, Jersey Shore State Bank (“JSSB”) and Luzerne Bank, operate as fairly distinct entities. Luzerne, formerly Luzerne National Bank Corporation, was acquired in June 2013. The acquisition increased the company’s total assets by $307 million and expanded its presence in contiguous Luzerne and Lackawanna counties. Penns Woods’s market area includes regions that should benefit over the long term from the Marcellus Shale gas fields, but the decline in energy prices slowed economic vitality in those markets. Approximately 80% of the company’s revenue is derived from spread income. As of December 31, 2016, total assets, deposits, and shareholders’ common equity were $1.3 billion, $1.0 billion, and $136.3 million, respectively.

Source: S&P Global Market Intelligence

19 | P a g e

Company Ratios

Profitability Our sense is that the central Pennsylvania economies remain healthy, but the relatively large number of banks competing for market share in an overall slower-growth region has traditionally resulted in loan pricing pressure. Based on anecdotal evidence, asset quality remains good, but we wonder if current loan pricing reflects an adequate risk premium should the economy sour or interest rates rise significantly more than what is generally expected. As is the case with community banks in general, Central Pennsylvania’s banks are challenged to better develop customer relationships, achieve a higher earnings growth rate, and gain market share. If the yield curve flattens following the Fed’s policy to raise interest rates, banks will be hurt as the majority of revenue depends upon spread income. As is the case with all banks across the nation, the highlighted institutions should benefit from less costly regulation and lower taxes, should President Trump’s goals come to fruition. Total loans as a percentage of total assets (68%) and the loan-to-deposit ratio (87%) tend to be below industry norms primarily due to the challenge of growing quality loans in slower-growth markets. The medians for the same ratios regarding peer institutions in the mid-Atlantic region were 74% and 93%, respectively. Please see Figures 6 and 7 for a break-out of the individual banks’ loan composition. As of December 31, 2016, the median investment securities-to-total asset ratio was 24% for the highlighted banks compared with a median ratio of 17% for peer banks in the mid-Atlantic region as of the same date. As a general rule in the prolonged low interest rate environment (with the stronger prospect of rising rates, banks must pay greater attention to their profitability potential while attending to interest rate risk and liquidity demands. Figure 5

Institution Ticker

ROAA (%)

ROAE

(%)

ROATCE

(%)

NIM

(%)

Non-Int Inc/Rev

(%)

Eff. Ratio

(%)

Inv Sec / Assets

(%)

Avg Inv Sec Yld

(%)

Loans / Assets

(%)

Loans / Dep.

(%)

Loan Yld (%)

ACNB Corporation ACNB 0.85 8.5 9.3 3.42 26 67 17 NA 75 94 NA Citizens & Northern CZNC 1.37 9.0 9.6 3.75 29 58 32 2.67 60 76 4.87 Citizens Financial Services CZFS 1.05 10.2 12.7 4.01 17 56 26 NA 65 80 5.04 Codorus Valley Bancorp, Inc. CVLY 1.01 9.9 10.0 3.93 16 62 13 2.39 78 101 4.93 ENB Financial Corp ENBP 0.79 7.9 7.9 3.61 26 73 32 NA 58 70 4.10 First Keystone Corporation FKYS 1.09 9.4 11.3 3.39 26 60 39 NA 53 72 NA Franklin Financial Services FRAF 0.62 5.9 6.4 3.66 15 68 13 NA 79 91 4.14 Kish Bancorp, Inc. KISB 0.70 9.4 9.7 3.11 24 80 24 NA 68 88 4.48 Mid Penn Bancorp, Inc. MPB 0.80 11.4 12.2 3.96 16 70 13 NA 78 87 4.82 Orrstown Financial Services ORRF 0.56 5.6 5.7 3.22 34 83 29 2.46 62 77 4.18 Penns Woods Bancorp, Inc. PWOD 0.87 8.4 9.9 3.40 22 65 10 3.40 80 100 3.98 Median 0.85 9.0 9.7 3.61 24 67 24 2.57 68 87 4.48

Financial data as of or for the three months ending December 31, 2016 Source: S&P Global Market Intelligence

20 | P a g e

Lending Activities As is the case with most community banks and thrifts, Central Pennsylvania banks are dependent upon interest income from loans for revenue growth. Net interest income represents 75-80% of total revenue for the highlighted banks in this report. These community banks have generally benefited from a local presence and industry consolidation. Figure 6

Institution Ticker

Residential Real Estate

($000s)

Commercial & Multifamily

Real Estate ($000s)

Consumer($000s)

Const. &

Dev. ($000s)

Comm. & Industrial

($000s)

Other ($000s)

Total

Loans ($000s)

ACNB Corporation ACNB 414,820 318,980 14,704 20,833 52,944 87,399 909,680 Citizens & Northern Corporation CZNC 396,007 165,658 13,722 39,195 83,854 53,541 751,977 Citizens Financial Services, Inc. CZFS 279,719 308,224 11,393 25,441 63,466 113,195 801,438 Codorus Valley Bancorp, Inc. CVLY 300,901 602,885 9,339 151,857 168,223 39,114 1,272,319 ENB Financial Corp ENBP 216,873 250,513 4,550 24,880 40,603 36,700 574,119 First Keystone Corporation FKYS 200,221 207,294 6,590 10,595 54,861 42,821 522,382 Franklin Financial Services FRAF 219,323 314,987 4,705 84,572 108,797 162,029 894,413 Kish Bancorp, Inc. KISB 185,503 151,974 11,715 19,600 79,508 47,327 495,627 Mid Penn Bancorp, Inc. MPB 203,432 378,815 2,131 57,677 137,001 36,826 815,882 Orrstown Financial Services, Inc. ORRF 339,754 379,670 6,993 30,748 70,071 58,923 886,159 Penns Woods Bancorp, Inc. PWOD 560,350 312,525 42,950 34,649 83,057 62,103 1,095,634 Median

279,719 312,525 9,339 30,748 79,508 53,541 815,882

Loan balances include loans held for sale. Loan balances are by collateral type, not business purpose. As of December 31, 2016 Source: S&P Global Market Intelligence, Q4 2016 Call Report

Figure 7

Institution Ticker

Residential Real Estate

(%)

Commercial & Multifamily

Real Estate (%)

Consumer(%)

Const. &

Dev. (%)

Comm. & Industrial

(%)

Other (%)

Commercial RE Loans / Total RBC

(%) ACNB Corporation ACNB 46% 35% 2% 2% 6% 10% 174% Citizens & Northern Corporation CZNC 53% 22% 2% 5% 11% 7% 87% Citizens Financial Services, Inc. CZFS 35% 38% 1% 3% 8% 14% 109% Codorus Valley Bancorp, Inc. CVLY 24% 47% 1% 12% 13% 3% 302% ENB Financial Corp ENBP 38% 44% 1% 4% 7% 6% 54% First Keystone Corporation FKYS 38% 40% 1% 2% 11% 8% 105% Franklin Financial Services FRAF 25% 35% 1% 9% 12% 18% 202% Kish Bancorp, Inc. KISB 37% 31% 2% 4% 16% 10% 137% Mid Penn Bancorp, Inc. MPB 25% 46% 0% 7% 17% 5% 328% Orrstown Financial Services, Inc. ORRF 38% 43% 1% 3% 8% 7% 227% Penns Woods Bancorp, Inc. PWOD 51% 29% 4% 3% 8% 6% 202% Median 38% 38% 1% 4% 11% 7% 174%

Loan balances include loans held for sale. Loan balances are by collateral type, not business purpose. Commercial RE Loans / Total RBC Ratio is based on bank entity data, not holding company data. As of December 31, 2016 Source: S&P Global Market Intelligence, Q4 2016 Call Report

21 | P a g e

Asset Quality Asset quality has generally remained good in recent years as Central Pennsylvania banks were largely spared from the devastating effects of the Great Recession. Figure 8

Institution Ticker

Reported NPAs

($000s)

NPAs/ Assets

(%)

NPAs/ Loans &

REO (%)

NCOs/ Avg

Loans (%)

Loan Loss Prov./

NCO (%)

Loan Loss Reserves/

Total Loans (%)

ACNB Corporation ACNB 6,103 0.51 0.67 0.13 0 1.56 Citizens & Northern Corporation CZNC 17,754 1.43 2.35 -0.03 NM 1.13 Citizens Financial Services, Inc. CZFS 12,895 1.05 1.61 0.03 NM 1.11 Codorus Valley Bancorp, Inc. CVLY 6,552 0.41 0.51 -0.05 NM 1.18 ENB Financial Corp ENBP 1,105 0.11 0.19 0.00 NM 1.32 First Keystone Corporation FKYS 4,242 0.43 0.81 0.02 NM 1.41 Franklin Financial Services FRAF 10,356 0.92 1.15 0.03 NM 1.24 Kish Bancorp, Inc. KISB NA NA NA 0.23 39 1.21 Mid Penn Bancorp, Inc. MPB 5,759 0.56 0.71 0.42 65 0.88 Orrstown Financial Services, Inc. ORRF 7,389 0.52 0.84 0.50 0 1.44 Penns Woods Bancorp, Inc. PWOD NA NA NA 0.06 217 1.18 Median 6,552 0.52 0.81 0.03 39 1.21

Financial data as of or for the three months ending December 31, 2016, or if not available as of or for the three months ending September 30, 2016 Source: S&P Global Market Intelligence

Deposits: We believe the crown jewels of a company’s franchise value rests in its core deposit base. As of December 31, 2016, the median core deposit ratio for the highlighted banks was 75%, and non-interest bearing deposits were 16% of total deposits. We define core deposits as all deposits excluding certificates of deposit. Figure 9

Institution Ticker

Non-Interest Bearing Deposits

($000s)

Interest Bearing (ex-Time) Deposits

($000s)

Time Deposits ($000s)

Total Deposits ($000s)

ACNB Corporation ACNB 180,593 19% 545,135 56% 241,893 25% 967,621 Citizens & Northern Corporation CZNC 224,175 23% 547,450 56% 212,218 22% 983,843 Citizens Financial Services, Inc. CZFS 147,425 15% 593,464 59% 264,614 26% 1,005,503 Codorus Valley Bancorp, Inc. CVLY 202,639 16% 634,853 50% 426,685 34% 1,264,177 ENB Financial Corp ENBP 280,543 34% 375,344 46% 161,604 20% 817,491 First Keystone Corporation FKYS 110,314 15% 422,347 58% 193,321 27% 725,982 Franklin Financial Services FRAF 170,345 17% 737,140 75% 74,635 8% 982,120 Kish Bancorp, Inc. KISB 73,448 13% 281,566 50% 206,914 37% 561,928 Mid Penn Bancorp, Inc. MPB 122,811 13% 629,967 67% 182,595 20% 935,373 Orrstown Financial Services, Inc. ORRF 150,747 13% 704,938 61% 296,767 26% 1,152,452 Penns Woods Bancorp, Inc. PWOD 303,277 28% 573,562 52% 218,375 20% 1,095,214 Median 170,345 16% 573,562 56% 212,218 25% 982,120 As of December 31, 2016 Source: S&P Global Market Intelligence

22 | P a g e

Mergers and Acquisitions We opine that the significant increase in bank stock prices since the election of Donald Trump and control of Congress by the Republican Party reflects investors’ anticipation for a better operating environment for financial institutions. Although no specific changes have been proposed – much less adopted – community bank earnings should improve significantly if and when regulatory burdens are eased and taxes are reduced. The wildcard - as is typically the case – is the economy, but stronger business conditions should lead to increased lending and more favorable interest rates that would positively impact bank earnings. Based on anecdotal evidence, it is unclear whether consolidation activity will accelerate if the macro environment improves significantly, even though potential buyers have stronger currencies to support higher deal prices. Banks are not bought, but are sold, and management teams may prefer independence in a more benign operating environment. Figure 10. Pennsylvania Bank Deals Since 2008

Price/ Price/ Core Deal Tangible LTM Deposit Completion Value Book Earnings Premium Buyer/Target Name Status Date*** ($MM) (%) (X) (%) Mid Penn Bancorp, Inc./ Scottdale Bank & Trust Company* Pending 3/29/17 59.1 130 NM 6.4 First Bank/ Bucks County Bank Pending 3/29/17 28.7 131 49.2 6.5 Bryn Mawr Bank Corporation/ Royal Bancshares of Pennsylvania Pending 1/31/17 127.7 224 9.8 14.4 NexTier Incorporated/ Manor Bank* Pending 12/07/16 2.3 87 NM -1.0 Standard Financial Corp./ Allegheny Valley Bancorp, Inc. Pending 08/29/16 53.4 124 15.0 3.51 Investor group/ Stonebridge Bank Pending 11/09/15 0.6 8 NM -9.7 WSFS Financial Corporation/ Penn Liberty Financial Corp. Completion 08/12/16 101.6 NA 31.8 10.6 Univest Corp. of Pennsylvania/ Fox Chase Bancorp, Inc. Completion 07/01/16 244.3 139 23.2 10.5 Beneficial Bancorp, Inc./ Conestoga Bank Completion 04/14/16 100.1 160 24.5 9.2 BB&T Corporation/ National Penn Bancshares, Inc. Completion 04/01/16 1,815.2 219 17.7 15.4 F.N.B. Corporation/ Metro Bancorp, Inc. Completion 02/13/16 473.5 178 22.7 9.4 NexTier Incorporated/ Eureka Financial Corporation Completion 01/08/16 35.3 151 21.4 13.1 Riverview Financial Corp./ Citizens National Bank of Meyersdale* Completion 12/31/15 7.8 109 68.9 1.2

Citizens Financial Services, Inc./ First Nat’l Bank of Fredericksburg Completion 12/11/15 22.9 144 NM 3.4 Juniata Valley Financial Corp./ FNBPA Bancorp, Inc.* Completion 11/30/15 13.3 129 18.2 4.2 WSFS Financial Corporation/ Alliance Bancorp, Inc. of Pennsylvania Completion 10/09/15 93.4 141 35.5 9.3 Andover Bancorp, Inc./ Community Nat’l Bank of Northwestern PA Completion 10/01/15 19.0 124 29.9 7.4 ESSA Bancorp, Inc./ Eagle National Bancorp, Inc.* Completion 07/29/15 25.3 112 NM 2.1 GNB Financial Services, Inc./ FNBM Financial Corporation* Completion 03/27/15 13.4 117 NM 3.3 S&T Bancorp, Inc./ Integrity Bancshares, Inc. Completion 03/04/15 159.4 266 16.8 15.3 Mid Penn Bancorp, Inc./ Phoenix Bancorp, Inc. Completion 03/01/15 14.5 110 26.6 1.2 Univest Corporation of Pennsylvania/ Valley Green Bank Completion 01/01/15 77.7 234 14.7 25.3 Bryn Mawr Bank Corporation/ Continental Bank Holdings, Inc. Completion 01/01/15 108.8 186 42.3 13.2

BB&T Corporation/ Susquehanna Bancshares, Inc. Completion 07/31/15 2,500.9 172 16.6 8.9 ESSA Bancorp, Inc./ Franklin Security Bancorp, Inc.* Completion 04/04/14 15.7 87 30.5 -2.9 GNB Financial Services, Inc./ Liberty Centre Bancorp, Inc. Completion 03/28/14 1.4 52 NM -6.0 Peoples Financial Services Corp./ Penseco Financial Services Corp. Completion 11/30/13 155.9 147 15.1 7.6 Riverview Financial Corporation/ Union Bancorp, Inc.* Completion 11/01/13 10.1 94 NM -0.6 Penns Woods Bancorp, Inc./ Luzerne National Bank Corporation Completion 06/01/13 46.1 165 20.3 7.5 First Priority Financial Corp./ Affinity Bancorp, Inc. Completion 02/28/13 12.7 105 NM NM S&T Bancorp, Inc./ Gateway Bank of Pennsylvania Completion 08/13/12 21.3 140 34.2 12.6 Tompkins Financial Corporation/ VIST Financial Corp. Completion 08/01/12 84.1 117 28.8 1.3

Continued on next page…

23 | P a g e

Price/ Price/ Core

Deal Tangible LTM Deposit Completion Value Book Earnings Premium Buyer/Target Name Status Date*** ($MM) (%) (X) (%) S&T Bancorp, Inc./ Mainline Bancorp, Inc. Completion 03/09/12 21.4 127 NM 2.5 Susquehanna Bancshares, Inc./ Tower Bancorp, Inc. Completion 02/17/12 342.1 149 NM 6.8 Customers Bancorp Inc/ Berkshire Bancorp, Inc. Completion 09/17/11 8.7 107 NM 0.5 GNB Financial Services, Inc./ Herndon National Bank Completion 08/06/11 8.3 101 54.2 0.3 Donegal Financial Services Corp./ Union National Financial Corp. Completion 05/06/11 25.2 94 NM -0.5 Snyder Group/ NexTier Incorporated Completion 04/19/11 NA NA NA NA Investor group/ Colonial American Bank Completion 04/15/11 NA NA NA NA F.N.B. Corporation/ Comm Bancorp, Inc. Completion 01/01/11 67.8 127 NM 3.0 Investor group/ Royal Asian Bank Completion 12/30/10 12.3 103 NM 0.7 Private Investor - James Wang/ Asian Financial Corporation Completion 12/29/10 5.1 197 NM 8.7 Tower Bancorp, Inc./ First Chester County Corporation Completion 12/10/10 64.8 91 NM -0.9 Bank of Princeton/ MoreBank Completion 09/30/10 5.5 119 NM 1.8 First Niagara Financial Group, Inc./ Harleysville National Corp. Completion 04/09/10 239.8 115 8.4 0.9 Chemung Financial Corporation/ Canton Bancorp, Inc. Completion 05/29/09 7.7 103 NM 0.5 Penseco Financial Services Corporation/ Old Forge Bank** Completion 04/01/09 58.0 173 22.3 16.2 Graystone Financial Corp./ Tower Bancorp, Inc. Completion 03/31/09 46.3 NM NM NM First Chester County Corporation/ American Home Bank, NA Completion 12/31/08 17.7 114 44.9 1.6 First Perry Bancorp, Inc./ HNB Bancorp, Inc.** Completion 12/31/08 11.3 NA NA NA NOVA Financial Holdings, Inc./ Pennsylvania Business Bank Completion 11/11/08 11.1 137 NM 3.7 F.N.B. Corporation/ Iron & Glass Bancorp, Inc. Completion 08/16/08 87.7 235 23.7 28.6

*Ambassador Deals **Deals led and completed by Ambassador team members as part of Danielson Associates ***Announcement date is listed for pending deals Source: S&P Global Market Intelligence

24 | P a g e

Figure 11. Pennsylvania Thrift Deals Since 2008

Price/ Price/ Core Deal Tangible LTM Deposit Completion Value Book Earnings Premium Buyer/Target Name Status Date*** ($MM) (%) (X) (%) Ambler Savings Bank/ Bally Savings Bank

Pending 2/17/17

NA NA NA NA Prudential Bancorp, Inc./ Polonia Bancorp, Inc. Completion 01/01/17 38.0 101 NM NA DNB Financial Corporation/ East River Bank* Completion 10/01/16 49.0 161 21.2 11.5 Emclaire Financial Corp./ United-American Savings Bank Completion 04/30/16 14.1 178 19.7 15.3 C&G Savings Bank/ Cresson Community Bank Completion 02/29/16 NA NA NA NA WSFS Financial Corp/ Alliance Bancorp of Pennsylvania Completion 10/09/15 93.4 141 35.5 9.3 WesBanco, Inc./ ESB Financial Corporation Completion 02/10/15 352.7 214 19.8 18.3 FSB Mutual Holdings, Inc./ First Federal Savings and Loan

Completion 08/01/15 NA NA NA NA

CB Financial Services, Inc./ FedFirst Financial Corporation Completion 10/31/14 55.0 109 25.2 2.4 National Penn Bancshares, Inc./ TF Financial Corporation Completion 10/24/14 141.6 154 19.0 7.7 Provident Financial Services, Inc./ Team Capital Bank Completion 05/30/14 124.4 191 19.2 9.7 WesBanco, Inc./ Fidelity Bancorp, Inc. Completion 11/30/12 72.9 171 56.4 7.1 ESSA Bancorp, Inc./ First Star Bancorp, Inc.* Completion 07/31/12 24.7 91 NM -0.9 Beneficial Mutual Bancorp, Inc. (MHC)/ SE Financial Corp. Completion 04/03/12 31.8 128 NM NA F.N.B. Corporation/ Parkvale Financial Corporation Completion 01/01/12 131.2 204 NM 5.2 Susquehanna Bancshares, Inc./ Abington Bancorp, Inc. Completion 10/01/11 273.8 129 33.4 9.1 Norwood Financial Corp./ North Penn Bancorp, Inc. Completion 05/31/11 27.4 138 20.6 6.4 Bryn Mawr Bank Corporation/ First Keystone Financial, Inc. Completion 07/01/10 32.8 100 NM NA Fidelity Savings and Loan Association of Bucks County/ Croydon

Completion 07/01/10 NA NA NA NA

Northwest Bancorp, Inc. (MHC)/ Keystone State Savings Bank Completion 10/23/09 NA NA NA NA Banco Santander, S.A./ Sovereign Bancorp, Inc. Completion 01/30/09 1,909.9 74 NM NA Harleysville National Corporation/ Willow Financial Bancorp, Inc. Completion 12/05/08 161.5 179 26.2 7.3 Sharon MHC/ Morton Savings Bank Completion 10/17/08 NA NA NA NA

*Ambassador Deals **Deals led and completed by Ambassador team members as part of Danielson Associates ***Announcement date is listed for pending deals Source: S&P Global Market Intelligence

Rick Weiss 610.724.7133 [email protected] Ryan Walker 610.851.4945 [email protected] Important Disclosure: Information contained herein is provided for informational purposes only, is not a solicitation to sell or offer to buy, and is obtained from sources believed to be reliable. We do not guarantee its accuracy or completeness. Opinions expressed reflect that of the author and are subject to change without notice. Ambassador, its officers/directors/shareholders/ employees and affiliates will not be held liable for use of this information other than for informational purposes. Ambassador, its officers/directors/shareholders/employees/affiliates and family members, may make investments in a company/security mentioned herein. Ambassador may perform/seek to perform investment banking or other services for entities mentioned herein. Prices and availability are subject to change. Additional information on securities mentioned herein is available upon request.

25 | P a g e

Appendix A: Deposit Market Share by Selected County

Adams County

Total Population: 102,750 Median HH Income: $64,028 Projected Median HH Income (5 yr CAGR): 8.29%

Deposits Market Deposits

Branch In

Market Share Per

Branch Rank Company Name Ticker Count ($MM) (%) ($MM)

1 ACNB Corporation ACNB 14 729 52.88 52 2 PNC Financial Services Group, Inc. PNC 7 441 32.00 63 3 BB&T Corporation BBT 3 144 10.44 48 4 M&T Bank Corporation MTB 2 65 4.68 32

Source: S&P Global Market Intelligence

Centre County

Total Population: 162,556 Median HH Income: $54,449 Projected Median HH Income (5 yr CAGR): 6.17%

Deposits Market Deposits

Branch In

Market Share Per

Branch Rank Company Name Ticker Count ($MM) (%) ($MM)

1 PNC Financial Services Group, Inc. PNC 6 710 22.56 118 2 F.N.B. Corporation FNB 13 553 17.58 43 3 BB&T Corporation BBT 5 419 13.33 84 4 Citizens Financial Group, Inc. CFG 4 290 9.21 72 5 M&T Bank Corporation MTB 6 246 7.83 41 6 Northwest Bancshares, Inc. NWBI 5 178 5.66 36 7 Penns Woods Bancorp, Inc. PWOD 4 151 4.81 38 8 Kish Bancorp, Inc. KISB 4 146 4.65 37 9 Fulton Financial Corporation FULT 2 109 3.47 55 10 CNB Financial Corporation CCNE 1 79 2.49 79 11 Banco Santander SAN 3 76 2.41 25 12 AmeriServ Financial, Inc. ASRV 1 64 2.03 64 13 Reliance Bancorp, MHC 1 60 1.90 60 14 Mifflinburg Bank & Trust Co. MIFF 1 30 0.95 30 15 S&T Bancorp, Inc. STBA 1 19 0.60 19 16 CBT Financial Corporation CBTC 1 16 0.52 16

Source: S&P Global Market Intelligence

26 | P a g e

Cumberland County

Total Population: 250,042 Median HH Income: $65,858 Projected Median HH Income (5 yr CAGR): 6.07%

Deposits Market Deposits

Branch In

Market Share Per

Branch Rank Company Name Ticker Count ($MM) (%) ($MM)

1 PNC Financial Services Group, Inc. PNC 11 1,572 24.08 143 2 M&T Bank Corporation MTB 16 1,477 22.64 92 3 Orrstown Financial Services, Inc. ORRF 9 645 9.88 72 4 F.N.B. Corporation FNB 7 565 8.66 81 5 S&T Bancorp, Inc. STBA 2 425 6.52 213 6 Banco Santander SAN 7 311 4.77 44 7 Citizens Financial Group, Inc. CFG 5 307 4.71 61 8 Wells Fargo & Company WFC 3 293 4.49 98 9 Franklin Financial Services Corp. FRAF 8 220 3.38 28 10 Fulton Financial Corporation FULT 4 206 3.15 51 11 BB&T Corporation BBT 5 163 2.51 33 12 Centric Financial Corporation CFCX 2 162 2.49 81 13 Mid Penn Bancorp, Inc. MPB 3 109 1.67 36 14 ACNB Corporation ACNB 1 50 0.77 50 15 Codorus Valley Bancorp, Inc. CVLY 1 16 0.25 16 16 Woodforest Financial Group, Inc. 3 3 0.05 1

Source: S&P Global Market Intelligence

27 | P a g e

Dauphin County

Total Population: 274,416 Median HH Income: $57,061 Projected Median HH Income (5 yr CAGR): 4.73%

Deposits Market Deposits

Branch In

Market Share Per

Branch Rank Company Name Ticker Count ($MM) (%) ($MM)

1 Wells Fargo & Company WFC 7 1,138 19.11 163 2 M&T Bank Corporation MTB 11 810 13.61 74 3 F.N.B. Corporation FNB 8 742 12.46 93 4 Mid Penn Bancorp, Inc. MPB 10 568 9.53 57 5 Fulton Financial Corporation FULT 8 550 9.24 69 6 PNC Financial Services Group, Inc. PNC 8 533 8.95 67 7 BB&T Corporation BBT 11 483 8.11 44 8 Citizens Financial Group, Inc. CFG 6 354 5.95 59 9 Banco Santander SAN 6 200 3.35 33 10 Centric Financial Corporation CFCX 2 178 2.99 89 11 S&T Bancorp, Inc. STBA 2 135 2.26 67 12 GNB Financial Services, Inc. GNBF 1 111 1.86 111 13 Riverview Financial Corporation RIVE 3 96 1.61 32 14 Northwest Bancshares, Inc. NWBI 1 53 0.90 53 15 Bryn Mawr Bank Corporation BMTC 1 4 0.06 4

Source: S&P Global Market Intelligence

28 | P a g e

Franklin County

Total Population: 154,711 Median HH Income: $53,431 Projected Median HH Income (5 yr CAGR): 3.94%

Deposits Market Deposits

Branch In

Market Share Per

Branch Rank Company Name Ticker Count ($MM) (%) ($MM)

1 Franklin Financial Services Corporation

FRAF 13 660 31.23 51

2 BB&T Corporation BBT 9 592 28.01 66 3 M&T Bank Corporation MTB 13 397 18.75 31 4 Orrstown Financial Services, Inc. ORRF 7 297 14.05 42 5 Mercersburg Financial Corporation MCBG 6 150 7.07 25 6 ACNB Corporation ACNB 2 17 0.82 9 7 Woodforest Financial Group, Inc. 1 1 0.07 1

Source: S&P Global Market Intelligence

29 | P a g e

Lancaster County

Total Population: 541,482 Median HH Income: $62,019 Projected Median HH Income (5 yr CAGR): 8.21%

Deposits Market Deposits

Branch In

Market Share Per

Branch Rank Company Name Ticker Count ($MM) (%) ($MM)

1 Fulton Financial Corporation FULT 28 2,914 27.61 104 2 BB&T Corporation BBT 32 2,414 22.88 75 3 PNC Financial Services Group, Inc. PNC 23 1,292 12.24 56 4 Wells Fargo & Company WFC 14 843 7.99 60 5 ENB Financial Corp ENBP 14 749 7.10 54 6 Donegal Financial Services Corp. DGICA 14 420 3.98 30 7 M&T Bank Corporation MTB 9 386 3.66 43 8 Banco Santander SAN 10 311 2.95 31 9 Citizens Financial Group, Inc. CFG 6 291 2.76 48 10 F.N.B. Corporation FNB 6 252 2.39 42 11 S&T Bancorp, Inc. STBA 3 245 2.32 82 12 Northwest Bancshares, Inc. NWBI 6 146 1.38 24 13 Bank of Bird-in-Hand 2 129 1.23 65 14 Coatesville Savings Bank 3 65 0.62 22 15 Orrstown Financial Services, Inc. ORRF 1 35 0.33 35 16 Jonestown Bank and Trust Co. JNES 1 28 0.26 28 17 Mid Penn Bancorp, Inc. MPB 2 25 0.23 12 18 Codorus Valley Bancorp, Inc. CVLY 4 6 0.05 1 19 Woodforest Financial Group, Inc. 1 1 0.01 1 20 Centric Financial Corporation CFCX 1 0 0.00 0

Source: S&P Global Market Intelligence

30 | P a g e

Lebanon County

Total Population: 138,121 Median HH Income: $58,385 Projected Median HH Income (5 yr CAGR): 4.54%

Deposits Market Deposits

Branch In

Market Share Per

Branch Rank Company Name Ticker Count ($MM) (%) ($MM)

1 Fulton Financial Corporation FULT 8 713 33.43 89 2 Jonestown Bank and Trust Co. JNES 11 396 18.57 36 3 Wells Fargo & Company WFC 5 351 16.44 70 4 Northwest Bancshares, Inc. NWBI 3 183 8.60 61 5 Citizens Financial Services, Inc. CZFS 4 137 6.43 34 6 F.N.B. Corporation FNB 3 93 4.38 31 7 BB&T Corporation BBT 2 84 3.95 42 8 M&T Bank Corporation MTB 1 80 3.74 80 9 Banco Santander SAN 2 66 3.10 33 10 ENB Financial Corp ENBP 1 19 0.90 19 11 PNC Financial Services Group, Inc. PNC 1 9 0.43 9 12 Woodforest Financial Group, Inc. 1 1 0.04 1

Source: S&P Global Market Intelligence

31 | P a g e

Lycoming County

Total Population: 115,650 Median HH Income: $48,069 Projected Median HH Income (5 yr CAGR): 7.36%

Deposits Market Deposits

Branch In

Market Share Per

Branch Rank Company Name Ticker Count ($MM) (%) ($MM)

1 Penns Woods Bancorp, Inc. PWOD 8 461 20.18 58 2 M&T Bank Corporation MTB 4 388 16.99 97 3 Muncy Bank Financial, Inc. MYBF 5 320 14.03 64 4 Woodlands Financial Services Co. WDFN 7 313 13.71 45 5 BB&T Corporation BBT 5 253 11.11 51 6 Banco Santander SAN 7 199 8.71 28 7 Citizens & Northern Corporation CZNC 6 135 5.93 23 8 F.N.B. Corporation FNB 3 112 4.91 37 9 PNC Financial Services Group, Inc. PNC 2 71 3.10 35 10 Fulton Financial Corporation FULT 1 19 0.84 19 11 Northwest Bancshares, Inc. NWBI 1 11 0.49 11

Source: S&P Global Market Intelligence

32 | P a g e

Schuylkill County

Total Population: 143,288 Median HH Income: $46,983 Projected Median HH Income (5 yr CAGR): 4.21%

Deposits Market Deposits

Branch In

Market Share Per

Branch Rank Company Name Ticker Count ($MM) (%) ($MM)

1 M&T Bank Corporation MTB 10 437 21.34 44 2 Wells Fargo & Company WFC 6 331 16.18 55 3 BB&T Corporation BBT 8 290 14.16 36 4 Banco Santander SAN 8 279 13.62 35 5 Riverview Financial Corporation RIVE 6 158 7.72 26 6 Mid Penn Bancorp, Inc. MPB 4 152 7.44 38 7 GNB Financial Services, Inc. GNBF 3 119 5.82 40 8 Fulton Financial Corporation FULT 1 93 4.52 93 9 F.N.B. Corporation FNB 3 56 2.76 19 10 Tompkins Financial Corporation TMP 1 52 2.52 52 11 Mauch Chunk Trust Financial

Corp. MCHT 2 42 2.06 21

12 Citizens Financial Services, Inc. CZFS 2 36 1.75 18 13 Woodforest Financial Group, Inc. 1 2 0.10 2

Source: S&P Global Market Intelligence

33 | P a g e

York County

Total Population: 445,335 Median HH Income: $60,870 Projected Median HH Income (5 yr CAGR): 4.54%

Deposits Market Deposits

Branch In

Market Share Per

Branch Rank Company Name Ticker Count ($MM) (%) ($MM)

1 M&T Bank Corporation MTB 26 1,753 25.30 67 2 Codorus Valley Bancorp, Inc. CVLY 21 979 14.13 47 3 Fulton Financial Corporation FULT 12 837 12.08 70 4 BB&T Corporation BBT 18 767 11.07 43 5 Banco Santander SAN 16 505 7.29 32 6 PNC Financial Services Group, Inc. PNC 8 476 6.88 60 7 Wells Fargo & Company WFC 7 476 6.88 68 8 F.N.B. Corporation FNB 5 369 5.33 74 9 York Traditions Bank YRKB 5 296 4.27 59 10 Citizens Financial Group, Inc. CFG 4 197 2.84 49 11 ACNB Corporation ACNB 5 132 1.91 26 12 Northwest Bancshares, Inc. NWBI 4 107 1.55 27 13 S&T Bancorp, Inc. STBA 1 29 0.41 29 14 Woodforest Financial Group, Inc. 3 4 0.06 1 15 Bank of New York Mellon Corp. BK 1 0 0.00 0

Source: S&P Global Market Intelligence