north american light vehicle production - autosteel/media/files/autosteel/great designs in...

TRANSCRIPT

North American Light Vehicle Production: A Decade of Change Within a Globally

Integrated Industry

Michael Robinet

Managing Director, IHS Automotive

Advisory Services Practice

May 14, 2014

© 2014 IHS

NA Production Update

1) Inserted Into a Global Framework

2) Changing With The Times

3) Summary

2

IHS Corporate Overview

3

• In business since 1959, we are a leading global source of information and expert

analysis in pivotal areas shaping today’s global business landscape

• Data and expertise from industry-specialized professionals enables innovative and

successful decision making

• Helping governments, multi-national organizations , regional companies and

technical professionals in more than 180 countries

• Approx. 8,000+ IHS colleagues in 140 offices located in 31 countries speaking 42

languages

• IHS customers include 80% of the Global Fortune 500, and nearly 70% of the US

Fortune 1,000

• IHS is a publically traded company on the NYSE under the “IHS” symbol

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

World USA Japan EuroZone

Brazil Russia India China

2013 2014 2015 Avg 2016-2021

An

nu

al R

ea

l G

DP

Gro

wth

in

%

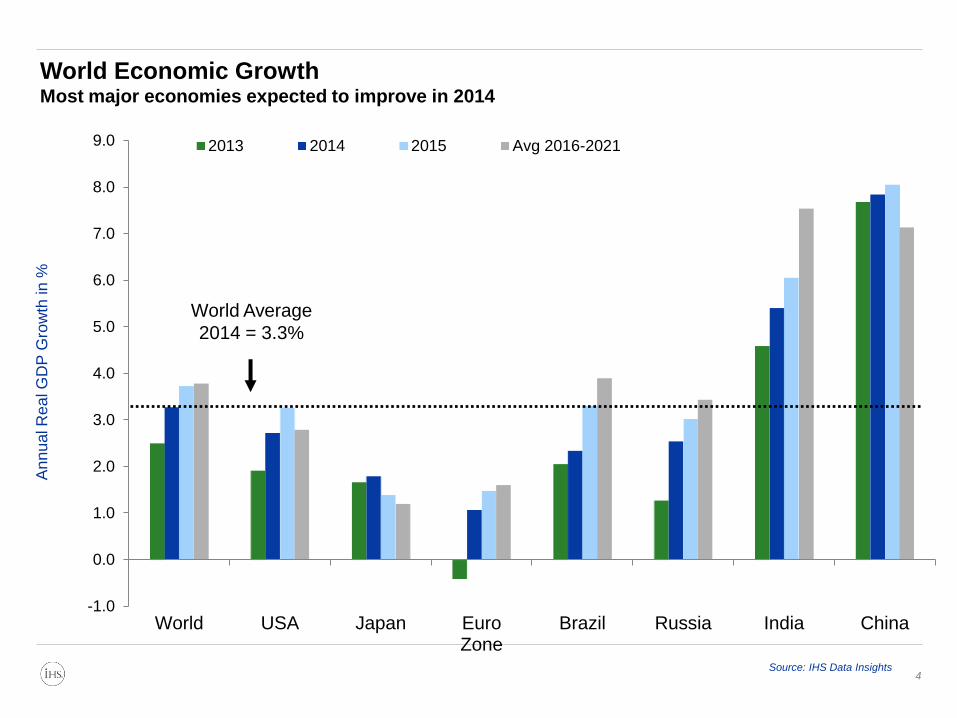

Source: IHS Data Insights

World Average

2014 = 3.3%

World Economic Growth Most major economies expected to improve in 2014

4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

1998 2000 2002 2004 2006 2008 2010 2012 2014 20160.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Canadian dollar Euro

Japanese yen Chinese renminbi

(Canadian dollars per US dollar, quarterly averages) (Euro per US dollar, quarterly averages)

(Yen per US dollar, quarterly averages)

4

5

6

7

8

9

1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

(Yuan per US dollar, quarterly averages)

Exchange rates per US dollar

5

60

80

100

120

140

1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

© 2014 IHS

IHS AUTOMOTIVE driven by POLK

© 2014 IHS 7

IHS AUTOMOTIVE driven by POLK

Global Production

(45%=C/E EU)

(65%=Mexico)

106

1.5

7.6

6.7

2.5 0.5 2.2

85

40

50

60

70

80

90

100

201

3 A B C D E

FF

202

1

Glo

ba

l LV

Pro

du

cti

on

(m

il)

7%

36%

32%

12%

10%

A

B

C

D

E

FF

106

2.5 2.4

1.2 1.0 1.0 0.9 0.9 0.7 0.6 0.6 9.0

85

40

50

60

70

80

90

100

201

3

Oth

er

202

1

Glo

bal LV

Pro

du

cti

on

(m

il)

Global Production Outlook

2013 – 2021: Market Growth

IHS AUTOMOTIVE driven by POLK

Variance By Global Segment Top 10 - Variance By OEM

© 2014 IHS 8

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2010 2012 2014 2016 2018 2020

Weig

hte

d C

ad

en

ce (

Years

) Program Cadence

20%

40%

60%

80%

2000 2010 2020

Mu

lti R

egio

n S

har

e

Multi-Region Platforms

101

85

134

117 130

136

107 112

151

125

0

20

40

60

80

100

120

140

160

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Lau

nch

Ev

en

t C

ou

nt

Global Launch Events

0 100,000 200,000 300,000 400,000 500,000

2010

2015

2020

Average Platform Volume (Over 50K/Year)

Faster, Greater Scale & Integrated Industry Pace and Risk Rises …

Global Segment Shifts Growing Smaller & Converging ….

A-Segment

B-Segment

C-Segment

D-Segment

Full-Size

Full-Frame

E-Segment

Mini/Compact

Full-Frame

6% 17%

25% 18%

10%

14%

10%

8%

22%

27%

17%

6%

12%

8%

6%

25%

30%

16%

6%

10%

7%

Global Production by Segment

1% 19%

22%

17%

17%

24%

2%

22%

33%

16%

6%

21%

6%

26%

35%

13%

4%

16%

NAFTA Production by Segment

2000 2010

2020

2000

2010

2020

• NAFTA begins to converge with global trends in the mid-segments (B, C & D)

• Greater than 60% of global volume is C-segment or smaller by 2020

• In NAFTA, more than 75% of volume is D-segment and smaller by 2020

10

© 2014 IHS 13

15

.8

15

.3

15

.1 12

.6

8.6

11

.9

13.1

15

.4

16

.2

16

.8

17

.3

17

.7

17

.8

18

.0

18.2

18

.2

0%

20%

40%

60%

80%

100%

0

4

8

12

16

20

2005 2010 2015 2020

Millio

ns

NA Production Underutilized Capacity % Utilization

IHS AUTOMOTIVE driven by POLK

16 vehicles

NA Light Vehicle Production

14

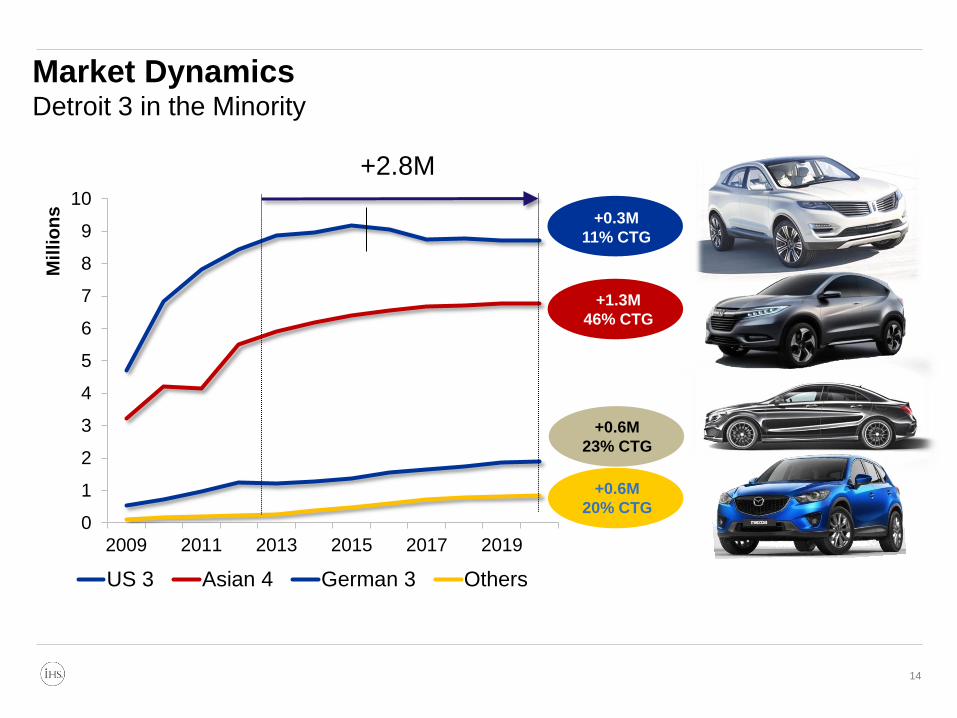

Market Dynamics Detroit 3 in the Minority

0

1

2

3

4

5

6

7

8

9

10

2009 2011 2013 2015 2017 2019

Mil

lio

ns

US 3 Asian 4 German 3 Others

+0.3M

11% CTG

+1.3M

46% CTG

+0.6M

23% CTG

+0.6M

20% CTG

+2.8M

30

43

24 23

20 19 19

25

17

43

33

37

35

39 37

32

0

10

20

30

40

50

2005 2007 2009 2011 2013 2015 2017 2019

North American Program Launches

15 Source: IHS Automotive Light Vehicle Production Forecast

Market Dynamics Launch Activity Surges, Investment & Competition Too

NAFTA Output By Region Shifting Towards the US South & Mexico

19

2.3

1.9

1.3

1.3

0.9

0.6

0.7

0.7

0.9

0.9

0

1

2

3

4

2000 2005 2010 2015 2020

Mill

ion

s Canada 2.9

2.6

1.9 2.2

1.8

6.5

5.7

3.3

5.2

5.1

1.3

1.2

1.2

1.5

1.6

0

1

2

3

4

5

6

7

8

9

2000 2005 2010 2015 2020

Mill

ion

s Mid West 7.8 6.9

4.5

6.8 6.7

1.9

1.7

0.4

0.8

0.9

1.0

2.0

1.9

3.5

3.6

0

1

2

3

4

5

2000 2005 2010 2015 2020

Mill

ion

s South East

2.9

3.7

2.3

4.4 4.6

1.0

1.5

2.8

2.7

2.3

3.4

4.2

2.4

2.7

3.8

0

2

4

6

8

10

2000 2005 2010 2015 2020

x 1

00

00

0 South West & CA

440K

570K 520K 550K

610K

1.1

0.9

1.2

1.6

1.8

0.8

0.7

1.1

1.8

2.6

0

1

2

3

4

5

2000 2005 2010 2015 2020

Mill

ion

s Mexico

18%

38% 20%

5%

19%

13%

39% 25%

3%

20%

10%

37%

25%

4%

24%

Share by Region

2020

2015

2010

US Midwest

US Southeast

US SW

& CA

Detroit 3

Non-Domestic

4.0

0

1

2

3

4

5

2000 2005 2010 2015 2020

x 1

00

00

0 North East

40K

400K

Over 50% of NA output will be

south of Ohio by 2014

1.9 1.6

2.3

3.3

4.4

Mexican production growth is one of the

fastest through the balance of the decade –

rivaling Brazil, Russia and India

© 2014 IHS 20

IHS AUTOMOTIVE driven by POLK

LV Production Locational Analysis 2013-16 Change

20

+750-1,000

+500-750

+250-500

+100-250

-100-100

-100-250

-250-500

-500-750

-750-1000

(Thousands)

Cambridge

Detroit

Columbus

Georgetown Kansas

City

Greenville Chattanooga

Montgomery Canton Arlington

Hermosillo

Monterrey

Queretaro

Puebla

1, 2 & 4 hour

logistics circles

© 2014 IHS 21

IHS AUTOMOTIVE driven by POLK

LV Production Locational Analysis 2016-20 Change

21

Cambridge

Detroit

Columbus

Georgetown Kansas

City

Greenville Chattanooga

Montgomery Canton Arlington

Hermosillo

Monterrey

Queretaro

Puebla

+750-1,000

+500-750

+250-500

+100-250

-100-100

-100-250

-250-500

-500-750

-750-1000

(Thousands)

1, 2 & 4 hour

logistics circles

NA Production Update

1) Inserted Into a Global Framework

2) Changing With The Times

3) Summary

22

We Too Can Change ..

© 2014 IHS 23

IHS AUTOMOTIVE driven by POLK

Efficiency Tradeoffs Shift Over Time

• Efficiency gains emanate from several sources with a cost:

• Lightweighting costs $80-180 per 1% FE increase

• Diesel technology costs $130 per 1% FE increase

• Hybrid powertrains cost $110-220 per 1% FE improvement

• Fuel economy regulations stiffen by 5% per year after 2015MY

• Each cycle will need to reach gains of 20-25% by the end of the cycle

• Every OEM has mass reduction goals averaging 3-5% per year

depending upon CAFE credits, current vehicle mass, supplier affiliations

and capital infrastructure

© 2014 IHS 24

Propulsion

• Hybrids, Electrics

• Boosting & Valve Technology

• Transmission & Driveline

Weight

• BIW & Closures

• Build Process

• Joining and corrosion

• Safety & Tradeoffs

Parasitics

• Aerodynamics

• Rolling Resistance

• Energy/Thermal Management

Powertrain Technology Trends

25

• VVT almost standard on any new engine; many migrating to advanced designs

• GDI and gas boosting both ramp up quickly. The initial rollout is being led by American and

German manufacturers, although the others aren’t far behind

• Stop/Start technology growing, helped by CAFE off-cycle credits

• Diesel and Hybrid/EV still relatively low-volume players in North American market, though

Hybrids gain traction late in the decade

0

2

3

5

6

8

10

11

13

14

16

18

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Un

its (

Mill

ion

s)

Variable Valve Timing

Gas Direct Injection

E85

Gas Boosted

Cylinder Deactivation

Diesel

Hybrid/EV

Stop/Start

AdvancedTransmissions*

North American Installations

* 6+ Speed/CVT/DCT/EV

Source: IHS Automotive Powertrain and Component Forecasts

Massive Structural Change Through 2025

Development Production Aftermarket

26

Development Production Aftermarket

2014 2017 2022 2027

Technologies required to meet

FE gains due for the 2025 period

are required to be tested, cost

proven and design integrated by

the 2017-19 timeframe.

Vehicle Cycle 1

Vehicle Cycle 2

Vehicle design cycles

starting in 2013 have

less than 2 cycles to

comply with the 2025

NHTSA standards – an

increase of over 45%

from 2016 levels.

US Fuel Economy/Emission Standards 2025

FE standards stiffen by 45% from 2016 to 2025

Mid-Cycle Review is gearing to be a

substantial battle with OEMs and

suppliers on both sides

New Platform Concepts

27

Vehicle Height

Vehicle Ride

Height

EMP2

“Advanced modularity allows for

new combinations: Four different

track widths; Five wheelbases;

Two cockpit and cowl solutions;

Two rear suspension

architectures”

•2020 scale: 1.7 million units

•2020 program count: 50+

MQB A/B

“One of the prominent

characteristics of the Modular

Transverse Matrix is the uniform

mounting position of ALL engines.

Assembly kit allows for synergies

between all vehicle classes”

•2020 scale: 5.6 million units

•2020 program count: 130+

CMF1

“Common Module Family is based

on the assembly of compatible

Big Modules: engine bay, cockpit,

front underbody, rear underbody

and electrical/electronic

architecture”

•2020 scale: 1.7 million units

•2020 program count: 50+

Mass Distribution and System Pressures

40

24

16

15

5

Body

Chassis

Powertrain

Interior

Electrical65 9

7

8

1 10

Conventional Steel

High/Medium Strength Steel

Polymer/Composite

Aluminum

Magnesium

Other

Vehicle Composition by Material

Source = Oak Ridge National Library Source = Oak Ridge National Library

Vehicle System Weight Distribution

•Pressure for weight reduction is slated to focus on body and structure first as aluminum,

advanced high strength steels and lighter forgings begin to penetrate the body and structure

•Second focal point will be chassis/suspension with a material shift towards New steel

forming processes, aluminum and new drive designs.

A Decade of Structural Change Emerges

Regulations

Safety

Consumers

Product Design

Manufacturing

© 2014 IHS 29

• A & B segment • Steel

Intensive

• C & D & FF

segment • Steel and

Aluminum

• D, E segment • Aluminum

intensive

• Forming

• Recycling

• Joining

• Durability

• Multi-material

construction

What Impacts Material

Substitution?

• OEM capital & supplier

infrastructure

• Efficiency of other FE

measures

• Competition & CAFE credits

• Cost and engineering

capability

• Vehicle vocation/durability

• Cadence & tooling

• Platform cycle position

• Global production and supply

• Safety compliance

NA Production Update

1) Inserted Into a Global Framework

2) Changing With The Times

3) Summary

30

© 2014 IHS 31

Vehicle Efficiency

Relative Costs/ Risk Mitigation

Global Integration

Logistics Pressures

Skills & Supplier

Capability/ Capacity

Currency Stability

• Material shifts have long-

term impacts: build

process, durability, safety,

internal skills,

infrastructure, warranty

and speed to market

• Each OEM has an

implementation path

dependent on platform

cadence, credits, supplier

capability and capital

• Supply base requires a

healthy regional industry –

think clusters

• Not business as usual …

IHS AUTOMOTIVE driven by POLK

The Decade of Challenges ….

© 2014 IHS

Thank You

Michael Robinet

Managing Director, IHS Automotive

Advisory Services

w w w . a u t o s t e e l . o r g

North American

Light Vehicle Metallic Material Trends

Great Designs in Steel is Sponsored by:

Use your web-enabled device to download the presentations from today’s event

PRESENTATIONS WILL BE AVAILABLE MAY 16