north american investor site visit - home – …/media/files/e/electrocomponents/... · north...

TRANSCRIPT

NORTH AMERICAN INVESTOR SITE VISIT

3 DECEMBER 2012

FORT WORTH, TEXAS

Agenda

Group Overview Ian Mason

Allied Overview Lee Davidson & Team

Q&A All

Lunch All

Allied Operations & Site Tour Kenneth Bradley

Q&A All

33

800K Catalogues 54% eCommerce

44,000 Parcels Daily

> 1m Customers

Strong Brands

2,500 Major Suppliers > 550,000 Products

17 Distribution Centres 90+% of World GDP

Electrocomponents: who we are

The World’s distributor of choice

3

44

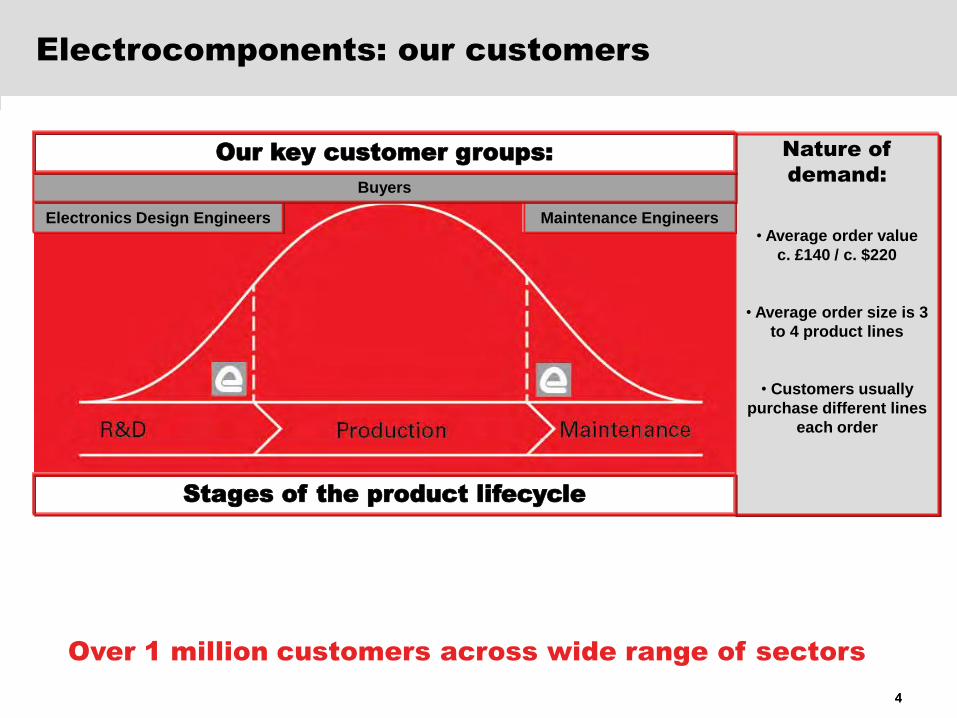

Electrocomponents: our customers

Over 1 million customers across wide range of sectors

Nature of

demand:

• Average order value

c. £140 / c. $220

• Average order size is 3

to 4 product lines

• Customers usually

purchase different lines

each order

Stages of the product lifecycle

Electronics Design Engineers Maintenance Engineers

Buyers

Our key customer groups:

4

% of Contribution Number of

H1 FY13 Group as % of Market distribution

revenue revenue position centres

Continental Europe 33% 19% No. 1 6

North America 22% 14% No. 3 1

Asia Pacific 14% 6% No. 1 8

International 69% 14% No. 1 15

UK 31% 28% No. 1 2

Group 100% 19% No. 1 17

5

Electrocomponents: where we operate

A well-invested global footprint,

opportunity to drive higher International returns

5

A

B

C

D

E

F

Structural growth opportunity – theory

Growing market share

Highly fragmented markets (ca. 85%)

Market share gains by 5 main players

We are the leading global distributor

Increasing competitive advantages

Growing markets

c.£30bn/c.$45bn available market

Electronics 2 x GDP

Maintenance GDP

Emerging markets

Growing share of growing markets

NOW (1)

FUTURE (1)

(1): Illustrative market shares 66

77

International growth driven by share gains and

underlying market growth

Structural growth through the cycle – in practice

International Sales CAGR Development, FY03 - FY12

0.9%

3.4%

3.8%4.7%

8.0%

0%

2%

4%

6%

8%

Nominal GDP grow th (1) Electronics (2) Market Grow th Share Gains Sales CAGR

CA

GR

, F

Y0

3 -

FY

12

(1) Nominal GDP grow th w eighted to Electros geographic split

(2) Weighted for exposure to faster Electronics grow th

7

Our competitive advantages vs. smaller players

Structural trends favour larger, global competitors

8

Service

accuracy

Product range

& availability

Partnerships

with leading

global

suppliers

Offer

Multi-channel

approach

Global

customer

reach

Sales & marketing

eCommerce

capabilities

8

99

Group strategy

• Focus on core strengths

• Global approach, delivered locally

• International growth

• Electronics and Maintenance

• eCommerce

• Operating leverage

• UK profitability

“The world’s distributor of choice”

Vision

Strategy

Priorities

Accelerating implementation

9

IT FINANCE HR

SALESOFFER MARKETING

STRATEGY

1010

New global organisation structure in place

Significant change to how we run the business

Strong forces driving globalisation

Reorganised whole of business in 6 months

From country-based to function-based

Faster implementation of strategy and

increased efficiency

Global Operating Model

1111

Single, global product offer

Improving the profitability of our offer

Integration of electronics, maintenance

and supply chain

Industry-leading product range and

service available globally

Dynamic pricing to transform value for

money perception

Drive higher return on stock

Five product categories

Famous

for

Known

for

Also

sell

Electronics (semiconductors,

passives &

electromechanical)

Automation & Control

Test & Measurement

Support

Electrical

Electronics(semiconductors, passives & electromechanical)

Automation & Control

1212

Sales: focused on growing target customers

Human touch to develop existing customers

Focused, local sales approach

Develop and grow existing customers

Deliver the best customer experience

Share best practice, improve efficiency

Targeting 4 contact groups

Electronic Design

EngineersMachine &

Panel Builders

Maintenance

Engineers

Buyers

Test & Measurement

Electrical

Electronics(semiconductors, passives & electromechanical)

Automation & Control

13

New global marketing approach

Single global function, balanced lifecycle approach

eCommerce “machine”

Human Touch

Cu

sto

mer sp

en

d / p

ote

ntia

l

Awareness

Brand awareness

Nursery

First 4 months

Development

Beyond 4 months

Acquisition

First purchase

• Contacts know who

we are

• Build the brand

• Acquire contacts in

both new and existing

customers

• Drive average

purchases higher

• Spot the winners’ and

nurture them

• Drive breadth of

purchase and average

order f requency

Single global effort across contact lifecycle

14

Highly attractive financial characteristics

A result of our business model and market position

EPS Growth

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

FY08 FY09 FY10 FY11 FY12

pen

ce

7% CAGR through the global

economic recession

Strong cash conversion

0%

20%

40%

60%

80%

100%

120%

140%

FY08 FY09 FY10 FY11 FY12

Co

nvers

ion

of

net

pro

fit

to f

ree c

ash

flo

w

5-yr average

101%

Strong balance sheet

0.0

0.5

1.0

1.5

2.0

FY08 FY09 FY10 FY11 FY12

Net

deb

t to

EB

ITD

A (

x)

5-yr average 1.3x

High return on capital employed

0%

10%

20%

30%

FY08 FY09 FY10 FY11 FY12

RO

CE

5-yr avge 21.6%

14

Proforma return on sales range of 8% - 12%

* Based on historical performance adjusted for FY12 International:UK sales mix

Strong margins delivered through the cycle

Proforma Group Return on Sales (%) *

10.0% 10.1%10.2% 10.2%

11.4%11.1%

10.2%

7.8%

9.5%

7.9%

9.0%

0%

2%

4%

6%

8%

10%

12%

FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12

Re

turn

on

Sa

les

%

1515

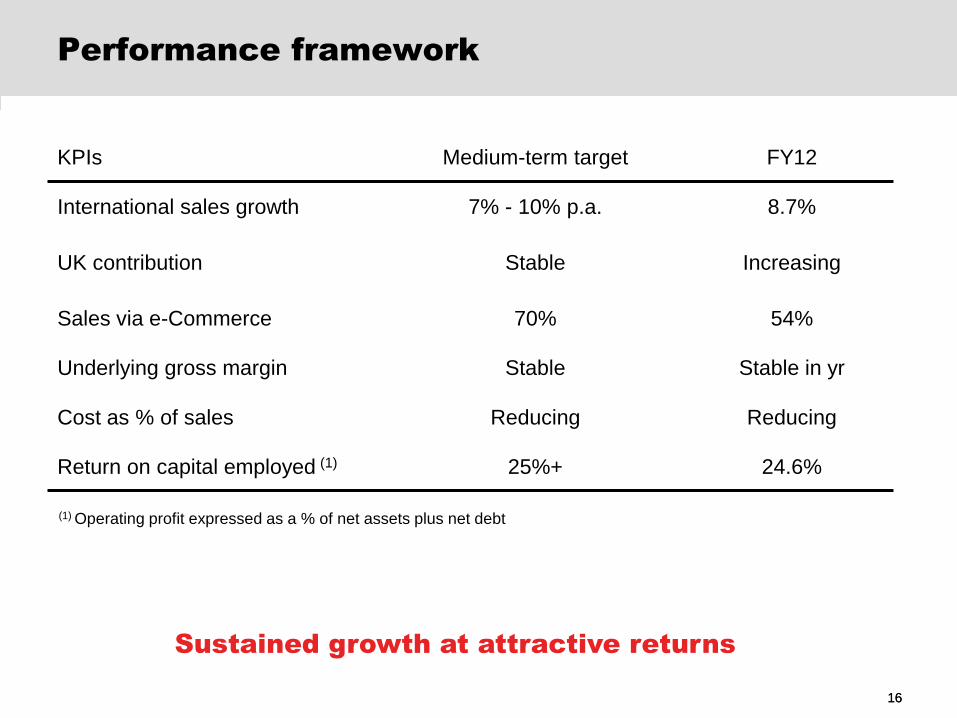

Performance framework

KPIs Medium-term target FY12

International sales growth 7% - 10% p.a. 8.7%

UK contribution Stable Increasing

Sales via e-Commerce 70% 54%

Underlying gross margin Stable Stable in yr

Cost as % of sales Reducing Reducing

Return on capital employed (1) 25%+ 24.6%

(1) Operating profit expressed as a % of net assets plus net debt

Sustained growth at attractive returns

1616

17

Recent trading: key themes

Short-term and long-term performance improvement

Difficult market conditions during H1 FY13, particularly in electronics

Significant impact on H1 FY13 financial performance

Decisive actions taken and expect stronger H2 FY13

New organisation structure to accelerate strategy and drive efficiencies

Structural growth opportunity from advantages over smaller competitors

Recent sales growth performance

October Group sales trends consistent with H1

FY12 Q1 Q2 H1 October

Continental Europe 1% (1)% 0% 1%

North America (4)% (6)% (5)% (6)%

Asia Pacific (3)% 3% 0% (1)%

International (2)% (2)% (2)% (2)%

UK 5% 5% 5% 3%

Group 0% 0% 0% 0%

Underlying sales growth (1)

(1) Adjusted for currency and trading days18

Sales per day

Q2 Group sales 17% above 2008 levels(1)

ƒ

£’000 sales per trading day (constant currency)

£’000 sales per trading day (constant currency)

£’000 sales per trading day (constant currency)

(1) Constant currency

3,000

3,500

4,000

4,500

5,000

5,500

500

700

900

1,100

1,300

1,500

1,700

1,500

2,000

2,500

3,000

3,500

4,000

Group sales per day

UK sales per day

International sales per day

19

2020

Summary

We are a strong and well-invested global business

Through the last 5 years we have taken market share from smaller competitors and

demonstrated that the structural growth opportunity exists

Our global scale and reach, broad product range, high customer service level and

eCommerce capabilities are key differentiators

We have a clear and consistent strategy and are now evolving to a global operating

model to increase pace and effectiveness of strategy implementation

The business has highly attractive financial characteristics

Targeting International sales growth of 7% - 10% pa

Leveraging competitive advantages to gain market share

20

Agenda

Group Overview Ian Mason

Allied Overview Lee Davidson & Team

Q&A All

Lunch All

Allied Operations & Site Tour Kenneth Bradley

Q&A All

Allied: proud of our heritage

Founded in 1928 as Allied Radio

Began as the radio parts distribution arm of

Columbia Radio Corporation

Acquired by Electrocomponents in 1999

A long legacy of excellent customer service

22

Allied sales history

23

A strong track record of sales growth

0

50

100

150

200

250

300

350

400

450

500

FY95 FY96 FY97 FY98 FY99 FY00 FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12

Sale

s $

m

Sales CAGR since FY95 = 9%

Last 10 years sales CAGR = 11%

Sales facts:

6,000+ inbound calls per day

4,500+ orders shipped per day

9,000+ lines billed/shipped per day

$375-$400 average order size

200k+ annual catalogue production

33%+ eCommerce share

Product facts:

300+ suppliers

Over 115k SKU’s in inventory

Allied key facts

Employee facts:

c.800 employees

400 sales

200+ front office

180 warehouse

Delivering a broad product range and service excellence

24

Systems investment:

– 2012: SAP ERP infrastructure c.$20m

– New sales tool to allow sales to work more effectively

– Infrastructure to support back-office processes efficiently

– Improved data analytics to support eCommerce growth

Warehouse investment:

– 2007: New warehouse c.$40m

– Capacity to expand

Inventory investment:

-- Doubled inventory levels to over $95m in last 7 years, tripled since 2002

People investment:

– Employee base of 800, strong culture to support growth

– Increase in employee numbers of 300 over last 10 years

Allied: a strong platform for growth

A well-invested business

25

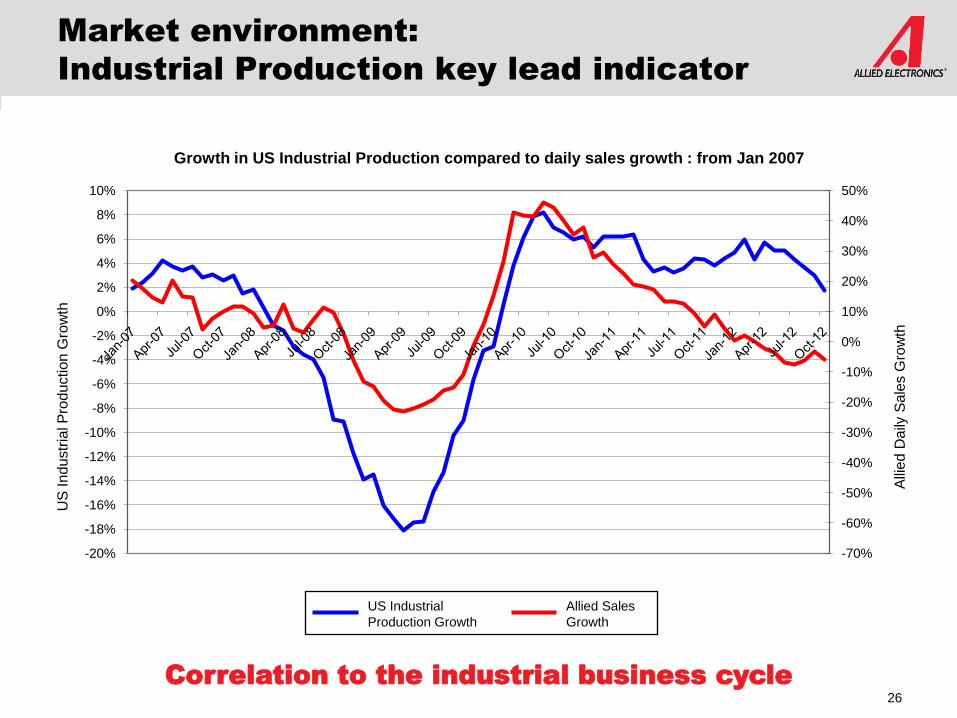

Market environment:

Industrial Production key lead indicator

Correlation to the industrial business cycle

26

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

-20%

-18%

-16%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Growth in US Industrial Production compared to daily sales growth : from Jan 2007

US Industrial

Production Growth

Allied Sales

Growth

US

In

du

str

ial P

rodu

ction

Gro

wth

Alli

ed D

aily

Sa

les G

row

th

Allied sales and operating margin performance

Increased scale leading to higher operating margins

27

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

100

200

300

400

FY08 FY09 FY10 FY11 FY12

Sales and Return on Sales %

Sales

ROS %

Allied return on capital and cash conversion

Attractive financial characteristics

28

0%

10%

20%

30%

40%

FY08 FY09 FY10 FY11 FY12

Retu

rn o

n c

ap

ital

em

plo

yed

Return on Capital

Average30%

0%

50%

100%

150%

200%

250%

FY08 FY09 FY10 FY11 FY12

Co

nvers

ion

of

net

pro

fits

to

fre

e c

ash

fl

ow

Cash Conversion Ratio

Average 110%

53 sales offices across North America

Sales: Allied’s local presence

300 Inside Sales Reps

50+ Outside Sales Reps

40+ National Sales Center Reps & sales support staff

7 Regional Directors

5 National Account Managers

Recognising the value of local sales offices

29

Machine and Panel Builders

Design, development & production support at

small/medium-sized OEMs/CMs

Board level & control cabinet applications

Emergency/shortage support

Maintenance Engineers

Routine supply room support

Scheduled maintenance

Support emergency/unplanned needs

Industrial-focus, multiple end-markets

Electronic Design Engineers

Government driven/supported

True R&D/High-tech

Universities

Allied customer segments

All key customer segments served

30

Customer split by contact type

Maintenance Engineers

Machine and Panel

Builders

Buyers

Electronics Design

Engineers

Allied product mix by technology

Focused on electronics & automation and control

31

Automation & Control

Interconnect

Power

Electromechanical

Wire & Cable

Passive/Active/ Opto

Test & Measurement

Other

Supplier and portfolio management

Supplier Relationship

Strategic Planning

Portfolio

Evaluation

Market

Positioning

Execution & Feedback

32

Win-win supplier relationships a key competitive advantage

• Top 20 Suppliers drive 43% of sales

• Strategic and Tactical suppliers combine to account for 66% of sales

Supplier focus drives growth

Prioritised approach to managing suppliers

33

Print marketing

Reaching over 20 million customers per year

34

Online marketing

Over 70 million customer touch points per year

35

Internal marketing

A closed loop marketing communication strategy 36

Search traffic

Referral traffic

Direct traffic

Campaigns

Website traffic drivers

Extensive SEM presence

Search a key driver of website traffic

37

Engaging email program

Targeted and relevant email campaigns

38

Conclusion

Business has a good financial characteristics

– Strong cash flow and returns

– Ability to leverage cost base to deliver return to bottom line

– Solid financial investment base to support growth

Focused business with strong local sales presence within a clear global strategy

Win-win partnerships with key suppliers

Market fundamentals supporting a multi-channel marketing approach

Well-invested business, confidence in the future

Committed to delivering a great experience

39

Agenda

Group Overview Ian Mason

Allied Overview Lee Davidson & Team

Q&A All

Lunch All

Allied Operations & Site Tour Kenneth Bradley

Q&A All

Agenda

Group Overview Ian Mason

Allied Overview Lee Davidson & Team

Q&A All

Lunch All

Allied Operations & Site Tour Kenneth Bradley

Q&A All

Agenda

Group Overview Ian Mason

Allied Overview Lee Davidson & Team

Q&A All

Lunch All

Allied Operations & Site Tour Kenneth Bradley

Q&A All

Warehouse operations: our facility

Distribution center opened in Sept 2007

290k square foot warehouse

180 employees

115k unique stocked materials

Capacity utilization

– Forward pick face 63%

– High bay 75%

– Pallet 88%

Work environment

– Quiet environment

– Solar tube lighting

– Climate controlled

– Best in class Health & Safety record

43

A modern facility to support future growth

Warehouse operations: technical solutions

Warehouse management system

Warehouse conveyor system

– RF technology

– Paperless picking

Conveyor

– PLC

– OSR

Inbound receiving

44

Recent investment in systems to drive efficiency

Order processing

– 4,500+ Daily orders

– 9,000+ Daily order lines

– 90% Domestic / 10% Export

99.9% Orders Inducted Shipped the

Same Day

94.0% Stocked Product Linefill

Hours of Operation:

– Monday to Friday

– 4am to 10.30pm

Warehouse operations: service delivery

45

Delivering reliable and accurate service

Warehouse operations: facility layout

46

Agenda

Group Overview Ian Mason

Allied Overview Lee Davidson & Team

Q&A All

Lunch All

Allied Operations & Site Tour Kenneth Bradley

Q&A All

Allied Electronics

Committed to Delivering a Great

Customer Experience

Appendix

Allied Executive Team

Lee DavidsonPresident

(10 years)

Mark SimonVP Sales

(8 years)

Scott McLendonVP Marketing & Product Mgt

(6 years)

Dennis CashVP HR/Admin

(9 years)

Ken KempkerChief Financial Officer

(4 years)

Andy JacksonVP CIO

(2 years)

Kenneth BradleyVP Supply Chain

(9 years)

49

eCommerce grown rapidly since FY09

eCommerce will become the channel of choice

eCommerce strategy began 2008

Rapid growth 2008 – 2011

Temporary decline in 2012

50

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

FY07 FY08 FY09 FY10 FY11 H1 FY12 FY12

eCommerce as a % of Sales