north america - unece

TRANSCRIPT

North America: Housing, the Economy and Timber Harvest

Silva 2015

“The Value of Forests”

Wood and wood products markets

November 3, 2015

Engelberg, Switzerland

©2015 Forest2Market®, Inc. 2

Today’s Agenda

• US housing and the forest industry

• The future for building with wood

• Canadian lumber production

• US regional production trends

• “Softwood Lumber Agreement”

• Pulp and paper outlook

• North American forest product exports

©2015 Forest2Market®, Inc. 3

©2015 Forest2Market®, Inc. 4

Principal timber regions In North America

Building with wood

©2015 Forest2Market®, Inc. 5

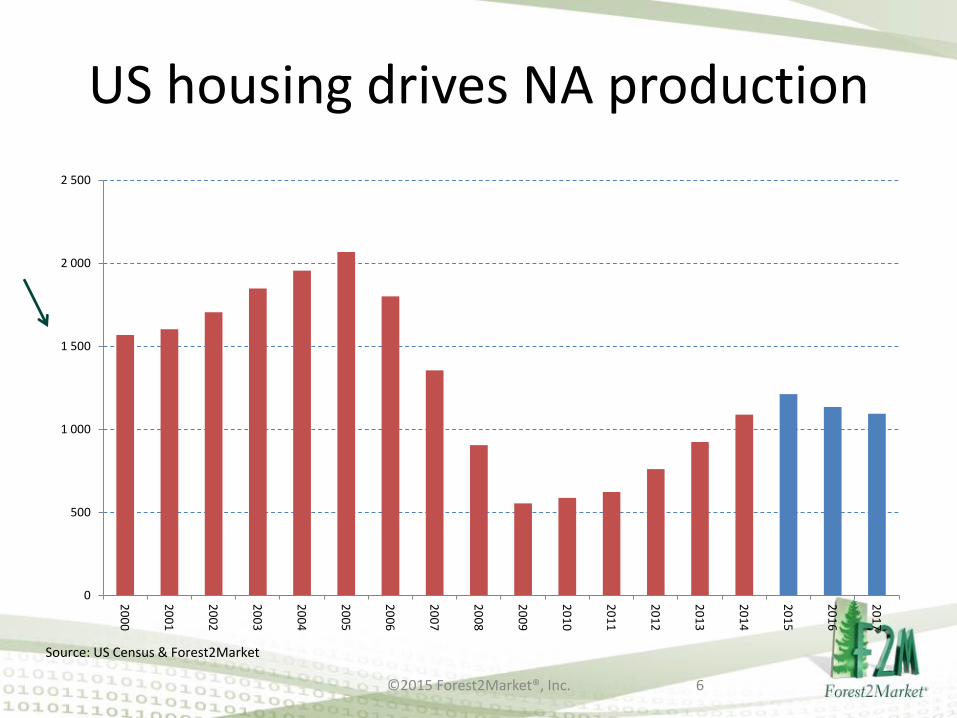

US housing drives NA production

©2015 Forest2Market®, Inc. 6

Source: US Census & Forest2Market

0

500

1 000

1 500

2 000

2 500

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

0

500

1 000

1 500

2 000

2 500

19591961196319651967196919711973197519771979198119831985198719891991199319951997199920012003200520072009201120132015

Total starts Single family Poly. (Single family)

Changing demographics of housing

©2015 Forest2Market®, Inc. 7

1993 87% single

Source: US Census

2015 61% single

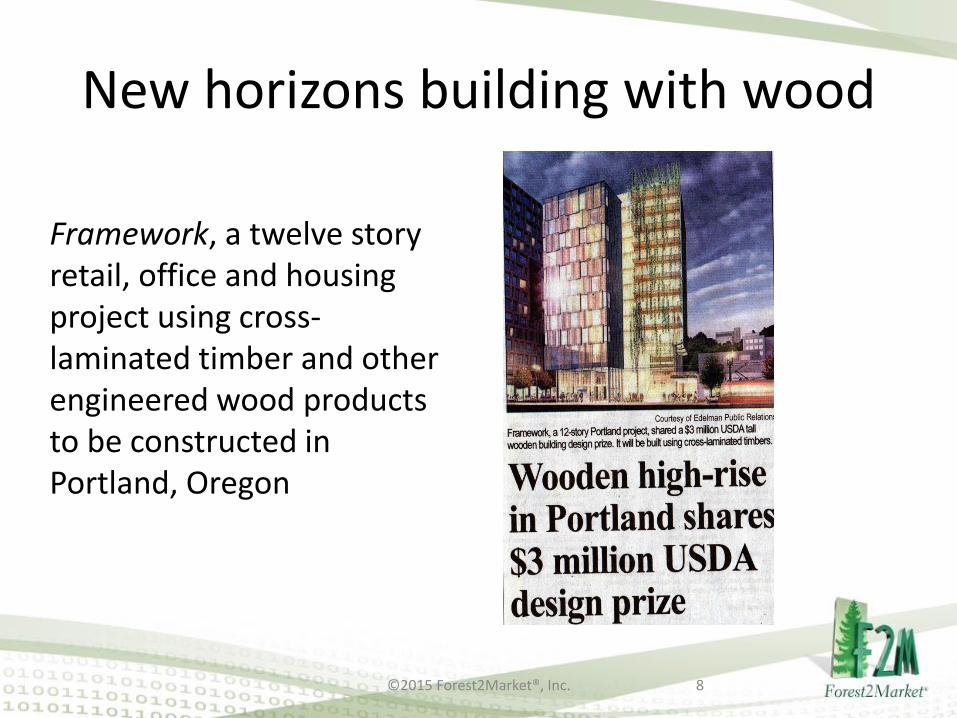

New horizons building with wood

Framework, a twelve story retail, office and housing project using cross-laminated timber and other engineered wood products to be constructed in Portland, Oregon

©2015 Forest2Market®, Inc. 8

Canadian forest industry

©2015 Forest2Market®, Inc. 9

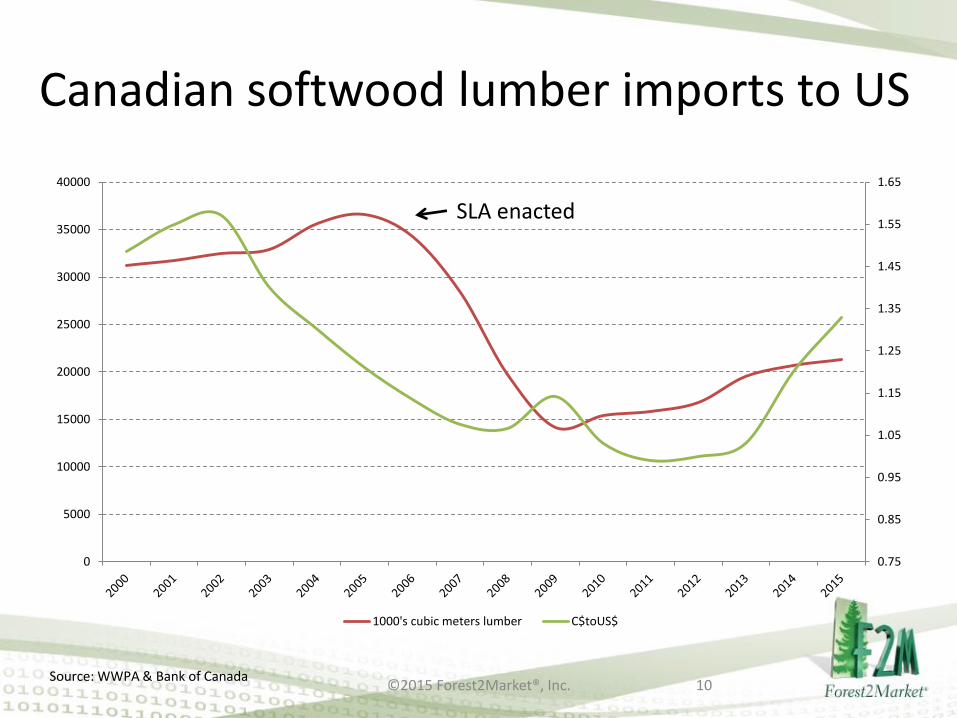

Canadian softwood lumber imports to US

©2015 Forest2Market®, Inc. 10Source: WWPA & Bank of Canada

0.75

0.85

0.95

1.05

1.15

1.25

1.35

1.45

1.55

1.65

0

5000

10000

15000

20000

25000

30000

35000

40000

1000's cubic meters lumber C$toUS$

SLA enacted

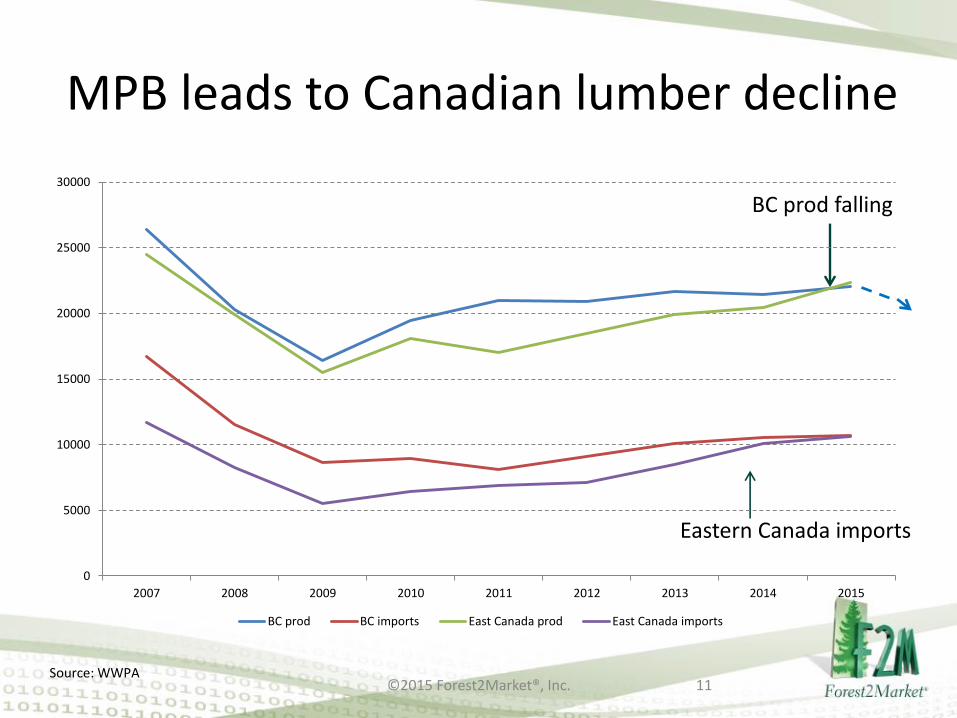

MPB leads to Canadian lumber decline

©2015 Forest2Market®, Inc. 11

BC prod falling

Eastern Canada imports

Source: WWPA

0

5000

10000

15000

20000

25000

30000

2007 2008 2009 2010 2011 2012 2013 2014 2015

BC prod BC imports East Canada prod East Canada imports

Softwood lumber agreement

• Adopted in 2006; resulting from a disagreement over whether Canadian stumpage pricing process constituted an unfair subsidy that disadvantaged the US lumber industry

• SLA expired in October 2015 • What has changed? Mountain pine beetle infestation in BC,

Canadian producers supply China’s demand for wood products, Canadian industry now owns a large stake in US lumber production

• Strong US $ makes Canadian lumber imports attractive• As demand from China falls, US producers are concerned about a

“wall of wood” from across the border• Canadian producers see new trade restrictions as an unnecessary

intrusion on free trade, an effort to prop up values of US private forests and fear further duties could be retro-active

• A “sticky wicket” as they say!

©2015 Forest2Market®, Inc. 12

US industry outlook

©2015 Forest2Market®, Inc. 13

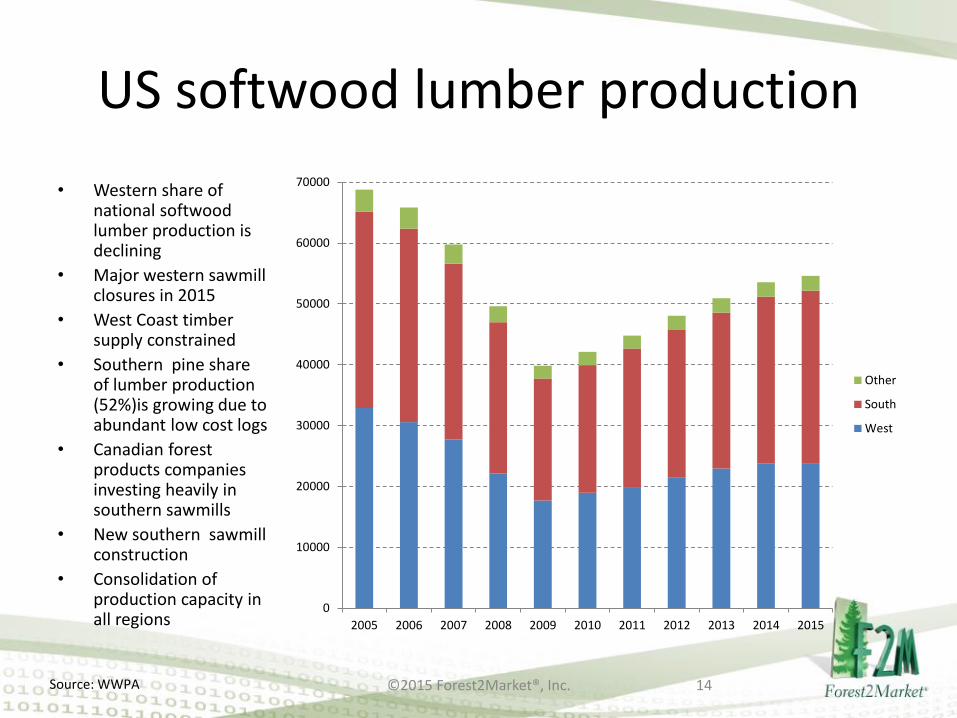

US softwood lumber production

• Western share of national softwood lumber production is declining

• Major western sawmill closures in 2015

• West Coast timber supply constrained

• Southern pine share of lumber production (52%)is growing due to abundant low cost logs

• Canadian forest products companies investing heavily in southern sawmills

• New southern sawmill construction

• Consolidation of production capacity in all regions

©2015 Forest2Market®, Inc. 14Source: WWPA

0

10000

20000

30000

40000

50000

60000

70000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Other

South

West

US Pacific Northwest

©2015 Forest2Market®, Inc. 15

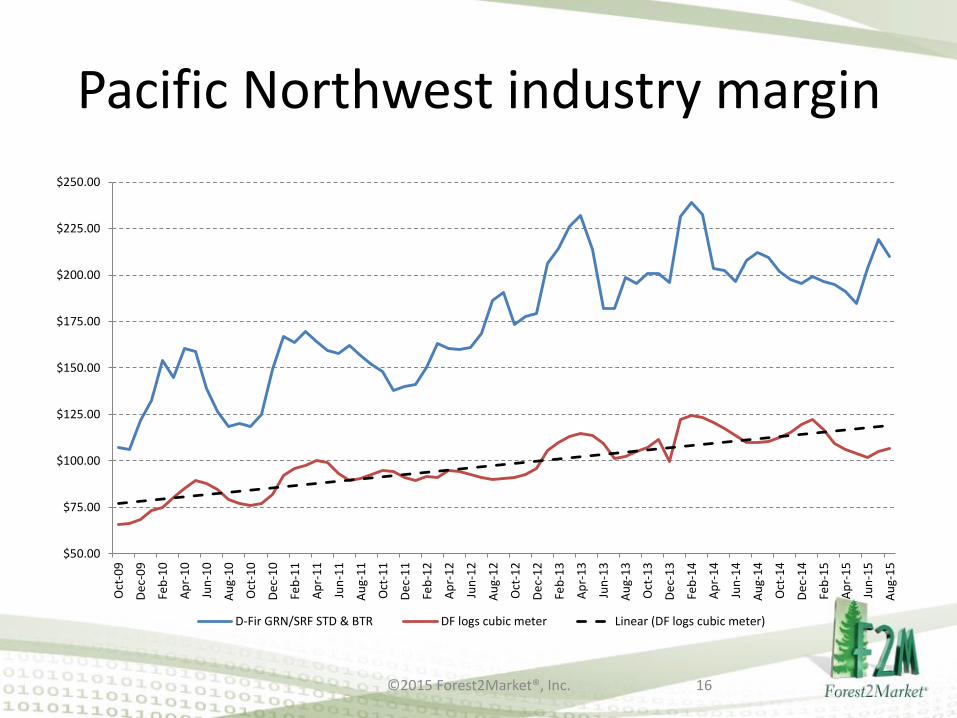

Pacific Northwest industry margin

©2015 Forest2Market®, Inc. 16

$50.00

$75.00

$100.00

$125.00

$150.00

$175.00

$200.00

$225.00

$250.00

Oct

-09

De

c-0

9

Feb

-10

Ap

r-1

0

Jun

-10

Au

g-1

0

Oct

-10

De

c-1

0

Feb

-11

Ap

r-1

1

Jun

-11

Au

g-1

1

Oct

-11

De

c-1

1

Feb

-12

Ap

r-1

2

Jun

-12

Au

g-1

2

Oct

-12

De

c-1

2

Feb

-13

Ap

r-1

3

Jun

-13

Au

g-1

3

Oct

-13

De

c-1

3

Feb

-14

Ap

r-1

4

Jun

-14

Au

g-1

4

Oct

-14

De

c-1

4

Feb

-15

Ap

r-1

5

Jun

-15

Au

g-1

5

D-Fir GRN/SRF STD & BTR DF logs cubic meter Linear (DF logs cubic meter)

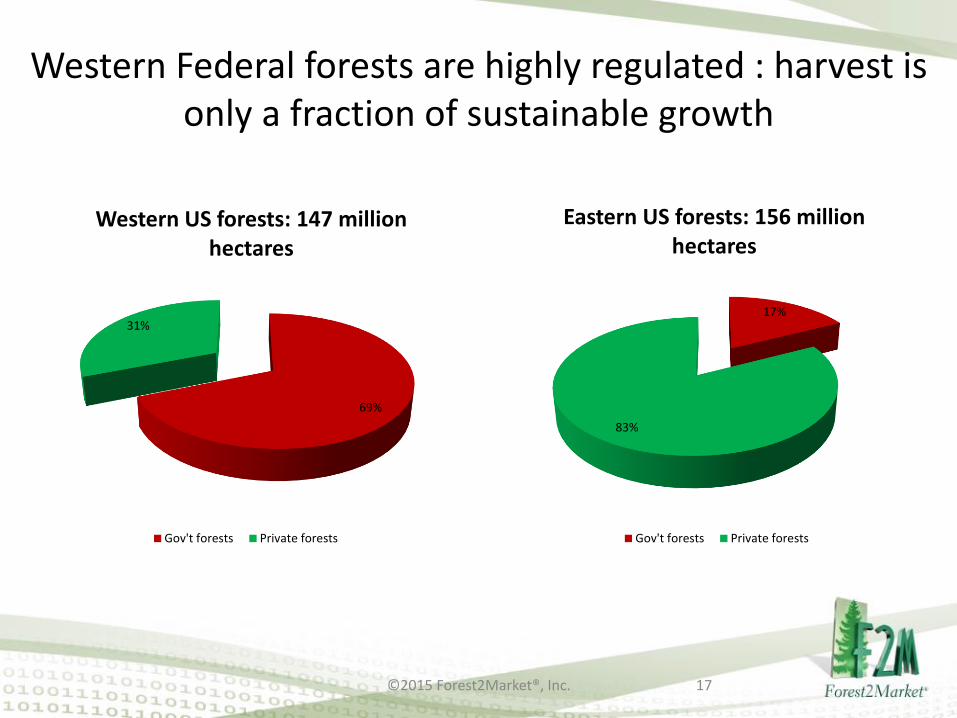

Western Federal forests are highly regulated : harvest is only a fraction of sustainable growth

©2015 Forest2Market®, Inc. 17

69%

31%

Western US forests: 147 million hectares

Gov't forests Private forests

17%

83%

Eastern US forests: 156 million hectares

Gov't forests Private forests

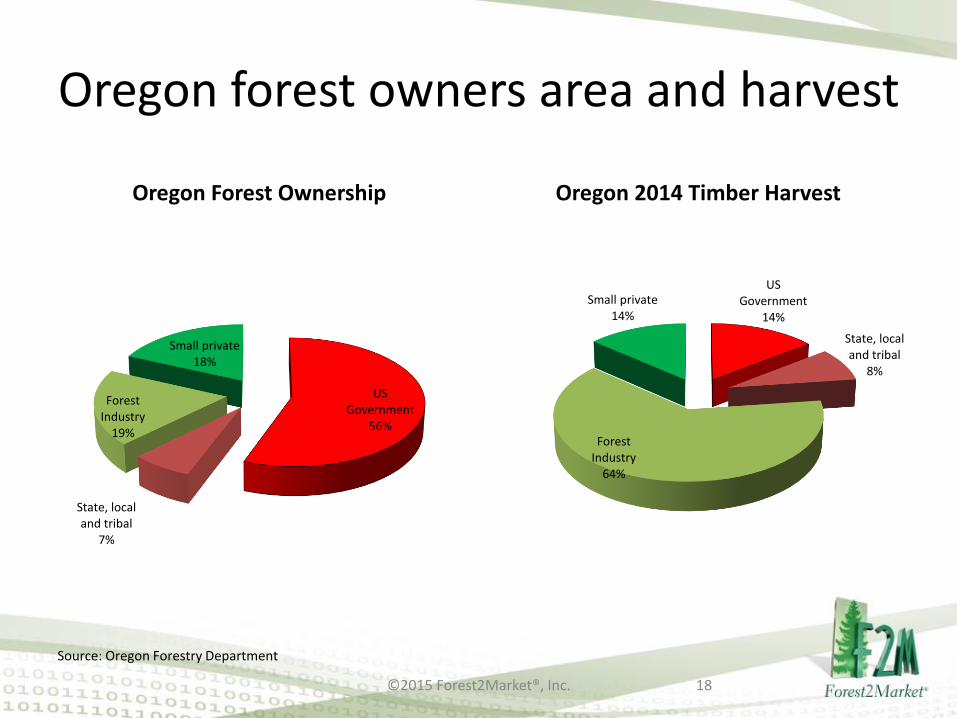

Oregon forest owners area and harvest

©2015 Forest2Market®, Inc. 18

US Government

56%

State, local and tribal

7%

Forest Industry

19%

Small private18%

Oregon Forest Ownership

US Government

14%

State, local and tribal

8%

Forest Industry

64%

Small private14%

Oregon 2014 Timber Harvest

Source: Oregon Forestry Department

US Southern pine

©2015 Forest2Market®, Inc. 19

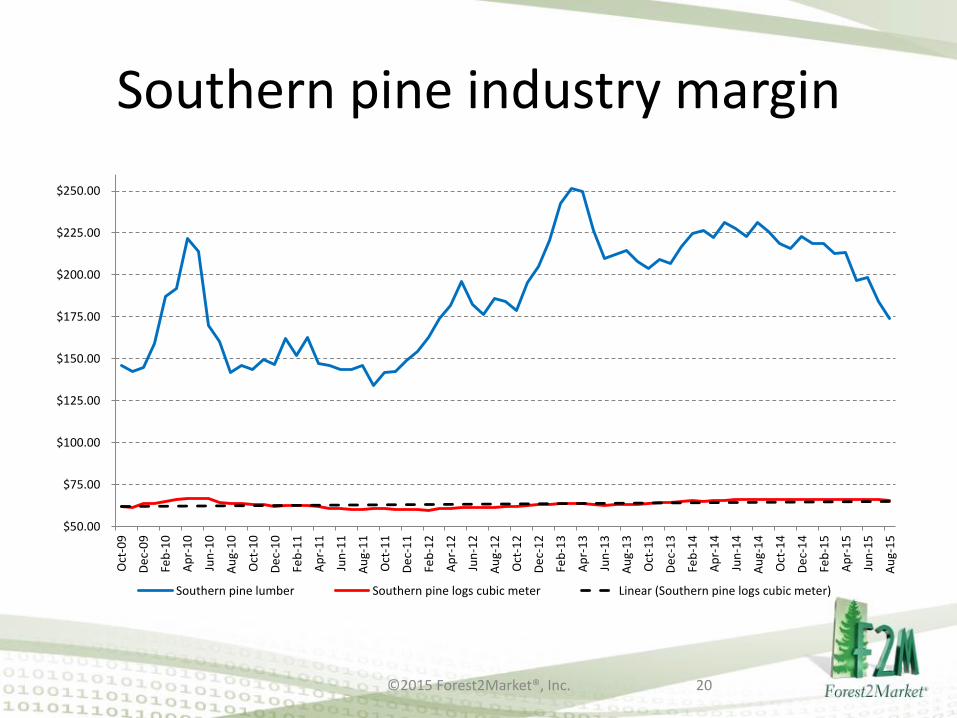

Southern pine industry margin

©2015 Forest2Market®, Inc. 20

$50.00

$75.00

$100.00

$125.00

$150.00

$175.00

$200.00

$225.00

$250.00

Oct

-09

De

c-0

9

Feb

-10

Ap

r-1

0

Jun

-10

Au

g-1

0

Oct

-10

De

c-1

0

Feb

-11

Ap

r-1

1

Jun

-11

Au

g-1

1

Oct

-11

De

c-1

1

Feb

-12

Ap

r-1

2

Jun

-12

Au

g-1

2

Oct

-12

De

c-1

2

Feb

-13

Ap

r-1

3

Jun

-13

Au

g-1

3

Oct

-13

De

c-1

3

Feb

-14

Ap

r-1

4

Jun

-14

Au

g-1

4

Oct

-14

De

c-1

4

Feb

-15

Ap

r-1

5

Jun

-15

Au

g-1

5

Southern pine lumber Southern pine logs cubic meter Linear (Southern pine logs cubic meter)

Canadian forest industry moves south

• The Southern US pine region has abundant, low cost timber from productive, well managed private forests

• Canfor, West Fraser and Interfor; leading Canadian forest products companies hedge their bets

• 35 pine sawmills in Texas, Arkansas, Louisiana, Mississippi, Alabama, Georgia, South Carolina, North Carolina and Florida are now owned by these three companies

• 11,000,000 cubic meters of production capacity• 30 % of Southern pine framing construction lumber

production

©2015 Forest2Market®, Inc. 21

US pulp and paper industry

©2015 Forest2Market®, Inc. 22

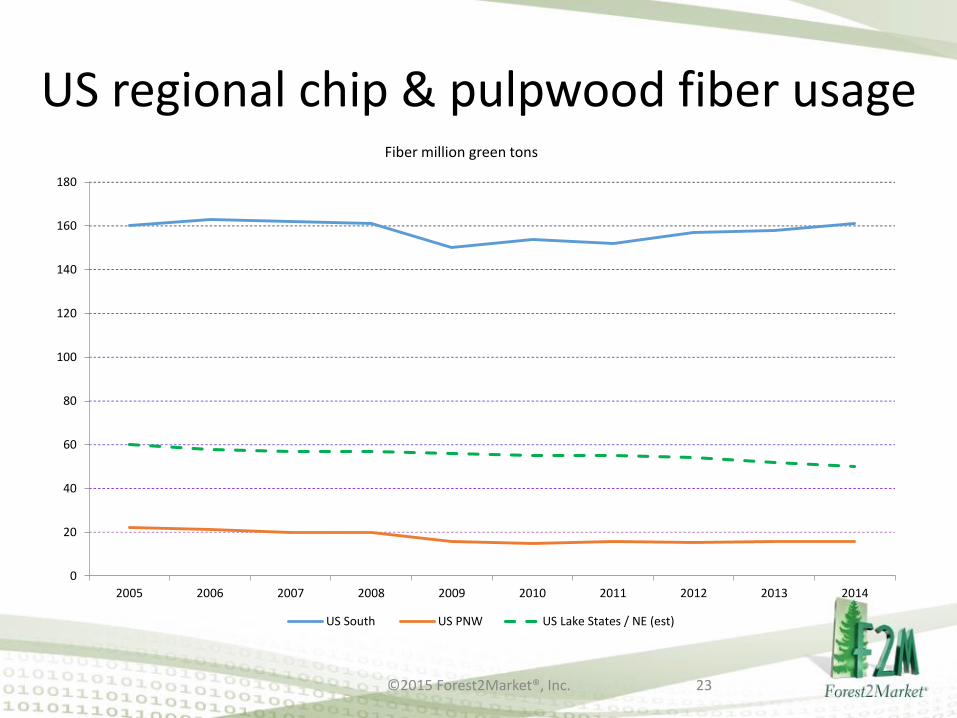

US regional chip & pulpwood fiber usage

©2015 Forest2Market®, Inc. 23

Fiber million green tons

0

20

40

60

80

100

120

140

160

180

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

US South US PNW US Lake States / NE (est)

Regional US pulpwood pricing

©2015 Forest2Market®, Inc. 24

$20.00

$25.00

$30.00

$35.00

$40.00

$45.00

$50.00

$55.00

$60.00

4Q2012 1Q2013 2Q2013 3Q2013 4Q2013 1Q2014 2Q2014 3Q2014 4Q2014 1Q2015 2Q2015 3Q2015

South PNW Lake States/Northeast

US Dollars per green ton

NA woodchip, fiber and paper outlook• Linerboard and packaging industry healthy• Newsprint, coated free sheet printing and writing paper

segment is suffering• Southern operators benefit from low cost fiber and

efficient mills• Fuel pellet producers have increased capacity and

competition for fiber in the South and Northeast• Revived interest in Northwest pulp & paper operations• Northwest faces tighter chip supply and increasing fiber

cost – less available pulpwood and residual chips• Lake States and Northeast - very expensive fiber; older,

less efficient mills with declining product line at risk • Declining harvest and lumber production due to MPB will

negatively influence British Columbia wood chip supply ©2015 Forest2Market®, Inc. 25

Forest product exports to Asia

©2015 Forest2Market®, Inc. 26

Strong $ benefits New Zealand loggers

©2015 Forest2Market®, Inc. 27

0

5000

10000

15000

20000

25000

30000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

vo

lum

e c

ub

ic m

ete

rs

China log imports by selected country

Russia New Zealand USA CanadaSource: China Customs

Asian demand for US logs slowing

©2015 Forest2Market®, Inc. 28

0

1000

2000

3000

4000

5000

6000

7000

8000

Vo

lum

e 1

000's

cu

bic

mete

r

Northwest Log Exports to Asia - Breakbulk Volume

Japan Korea ChinaSource: US Dept of CommerceSource: US Dept of Commerce

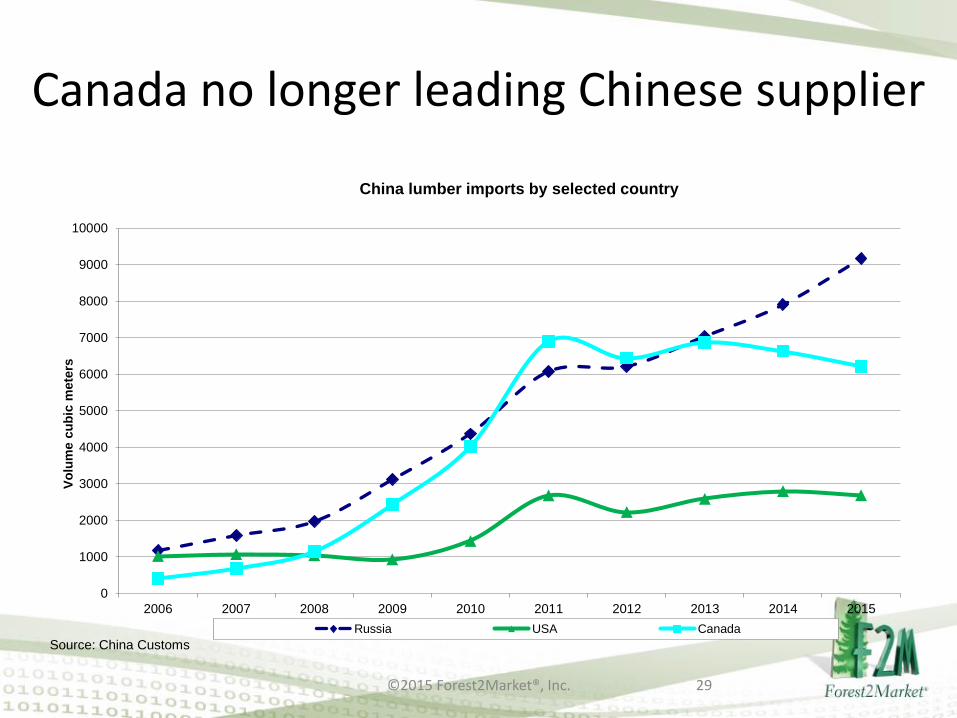

Canada no longer leading Chinese supplier

©2015 Forest2Market®, Inc. 29

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Vo

lum

e c

ub

ic m

ete

rs

China lumber imports by selected country

Russia USA Canada

Source: China Customs

Concluding thoughts

• Soft recovery for US housing market

• Multi-level building with wood

• British Columbia production declining

• Growth for Southern US pine industry

• US linerboard, packaging business is strong

• Strong US $ influence on wood imports & exports

• China’s demand for wood products is slowing

• South American imports: productive plantations, modern pulp and panel mills, Asia and US $ ?

©2015 Forest2Market®, Inc. 30

Forest2Market: The highest quality wood raw material analysis available

Gordon CulbertsonDirector-International Business Development

(541) 285 [email protected]

Forest2Market®15720 Brixham Hill Avenue, Suite 550Charlotte, NC 28277

www.forest2market.com

©2015 Forest2Market®, Inc. 31

Merci vielmal!

©2015 Forest2Market®, Inc. 32