nonprofit accounting - continuing education for tax

TRANSCRIPT

Nonprofit Accounting Steven M. Bragg

Course # 5.14.6002, Version 2003, 16 CPE Credits

Course CPE Information

i

Course CPE Information Course Expiration Date Per AICPA and NASBA Standards (S9-06), QAS Self-Study courses must include an expiration date that is no longer than one year from the date of purchase or enrollment. Field of Study Accounting. Some state boards may count credits under different categories—check with your state board for more information. Course Level Overview. Prerequisites There are no prerequisites. Advance Preparation None. Course Description This practical guide shows how to create and operate a nonprofit accounting system and produce financial statements, all while operating in accordance with nonprofit accounting standards. The course walks the accountant through basic nonprofit accounting concepts and then discusses more advanced topics, including budgeting, controls, ratio analysis, revenue recognition, joint costs, split-interest agreements, tax reporting, and mergers and acquisitions. In short, the course offers a wealth of information for understanding nonprofit transactions and financial statements. Nonprofit Accounting is designed for financial professionals to use as a reference tool for devel-oping accounting systems and researching the correct accounting to deal with various transac-tions and reports. With its complete coverage of these topics and more, it will earn a permanent place on your bookshelf. © Copyright Accounting Tools Inc. 2020 Publication/Revision Date May 2020

Instructional Design

ii

Instructional Design This Self-Study course is designed to lead you through a learning process using instructional methods that will help you achieve the stated learning objectives. You will be provided with course objectives and presented with comprehensive information and facts demonstrated in ex-hibits and/or case studies. Review questions will allow you to check your understanding of the material, and a qualified assessment will test your mastery of the course. Please familiarize yourself with the following instructional features to ensure your success in achieving the learning objectives. Course CPE Information The preceding section, “Course CPE Information,” details important information regarding CPE. If you skipped over that section, please go back and review the information now to ensure you are prepared to complete this course successfully. Table of Contents The table of contents allows you to quickly navigate to specific sections of the course. Learning Objectives and Content Learning objectives clearly define the knowledge, skills, or abilities you will gain by completing the course. Throughout the course content, you will find various instructional methods to help you achieve the learning objectives, such as examples, case studies, charts, diagrams, and expla-nations. Please pay special attention to these instructional methods, as they will help you achieve the stated learning objectives. Review Questions The review questions accompanying this course are designed to assist you in achieving the course learning objectives. The review section is not graded; do not submit it in place of your qualified assessment. While completing the review questions, it may be helpful to study any un-familiar terms in the glossary in addition to course content. After completing the review ques-tions, proceed to the review question answers and rationales. Review Question Answers and Rationales Review question answer choices are accompanied by unique, logical reasoning (rationales) as to why an answer is correct or incorrect. Evaluative feedback to incorrect responses and reinforce-ment feedback to correct responses are both provided. Glossary The glossary defines key terms. Please review the definition of any words you are not familiar with. Index The index allows you to quickly locate key terms or concepts as you progress through the in-structional material.

Instructional Design

iii

Qualified Assessment Qualified assessments measure (1) the extent to which the learning objectives have been met and (2) that you have gained the knowledge, skills, or abilities clearly defined by the learning objec-tives for each section of the course. Unless otherwise noted, you are required to earn a minimum score of 70% to pass a course. If you do not pass on your first attempt, please review the learning objectives, instructional materials, and review questions and answers before attempting to retake the qualified assessment to ensure all learning objectives have been successfully completed. Answer Sheet Feel free to fill the Answer Sheet out as you go over the course. To enter your answers online, follow these steps:

1. Go to www.westerncpe.com. 2. Log in with your username and password. 3. At the top right side of your screen, hover over “My Account” and click “My CPE.” 4. Click on the big orange button that says “View All Courses.” 5. Click on the appropriate course title. 6. Click on the blue wording that says “Qualified Assessment.” 7. Click on “Attempt assessment now.”

Evaluation Upon successful completion of your online assessment, we ask that you complete an online course evaluation. Your feedback is a vital component in our future course development.

Western CPE Self-Study 243 Pegasus Drive

Bozeman, MT 59718 Phone: (800) 822-4194

Fax: (206) 774-1285 Email: wcpe@western-

cpe.com Website: www.western-

cpe.com Notice: This publication is designed to provide accurate information in regard to the subject matter covered. It is sold with the understanding that neither the author, the publisher, nor any other individual involved in its distribution is engaged in rendering legal, accounting, or other professional advice and assumes no liability in connection with its use. Because regulations, laws, and other professional guidance are constantly changing, a professional should be con-sulted should you require legal or other expert advice. Information is current at the time of printing.

Table of Contents

4

Table of Contents

Course CPE Information .............................................................................................................................................i

Instructional Design ................................................................................................................................................... ii

Table of Contents ......................................................................................................................................................... 4

Chapter 1 – Overview of the Nonprofit Entity ........................................................................................................ 14 Learning Objectives ................................................................................................................................................. 14 Introduction ............................................................................................................................................................. 14 Definition of a Nonprofit Entity ............................................................................................................................... 14 Nonprofit Organizational Structure ......................................................................................................................... 18 Summary .................................................................................................................................................................. 19 Chapter 1 – Review Questions ................................................................................................................................. 20

Chapter 2 – Basic Nonprofit Accounting Concepts ................................................................................................ 21 Learning Objectives ................................................................................................................................................. 21 Introduction ............................................................................................................................................................. 21 Double Entry Bookkeeping ...................................................................................................................................... 21 The Journal Entry .................................................................................................................................................... 22 The Accounting Equation ........................................................................................................................................ 22 The Chart of Accounts ............................................................................................................................................. 24 The Accrual Basis of Accounting ............................................................................................................................. 27 The Cash Basis of Accounting ................................................................................................................................. 27 The Modified Cash Basis of Accounting .................................................................................................................. 28 Converting Cash Basis to the Accrual Basis ........................................................................................................... 28 Generally Accepted Accounting Principles (GAAP) ............................................................................................... 29 Net Assets ................................................................................................................................................................. 30

Net Assets without Donor Restrictions ................................................................................................................ 30 Net Assets with Donor Restrictions ..................................................................................................................... 30 Net Assets Summary ........................................................................................................................................... 30

The Release from Restriction Concept ..................................................................................................................... 31 Inter-Fund Receivables and Payables ..................................................................................................................... 32 Board-Designated Funds ......................................................................................................................................... 32 Program Identification ............................................................................................................................................ 32 The Management and Administration Classification............................................................................................... 33 The Fundraising Classification ............................................................................................................................... 33 Bookkeeping Concerns ............................................................................................................................................ 34 Case Study ............................................................................................................................................................... 35

Table of Contents

5

Summary .................................................................................................................................................................. 39 Chapter 2- Review Questions .................................................................................................................................. 40

Chapter 3 Nonprofit Financial Statements.............................................................................................................. 41 Introduction ............................................................................................................................................................. 41 The Statement of Financial Position ........................................................................................................................ 41 The Statement of Activities ....................................................................................................................................... 45 The Statement of Cash Flows .................................................................................................................................. 48

The Direct Method ............................................................................................................................................... 48 The Indirect Method ............................................................................................................................................ 50 How to Prepare the Statement of Cash Flows ..................................................................................................... 51

Reporting of Expenses by Nature and Function ...................................................................................................... 52 Financial Statement Disclosures ............................................................................................................................. 55 Summary .................................................................................................................................................................. 57 Chapter 3 - Review Questions ................................................................................................................................. 58

Chapter 4 – Revenue Accounting ............................................................................................................................. 59 Learning Objectives ................................................................................................................................................. 59 Introduction ............................................................................................................................................................. 59 Types of Revenue ..................................................................................................................................................... 59 Promises to Give ...................................................................................................................................................... 60 Pass-Through Contributions ................................................................................................................................... 62 Exchange Value ....................................................................................................................................................... 63 Transfers of Assets ................................................................................................................................................... 64 Discounts from Revenue .......................................................................................................................................... 64 Sales Taxes .............................................................................................................................................................. 64 The Allowance for Uncollectible Pledges ................................................................................................................ 64 Restricted Fund Releases ......................................................................................................................................... 65 Revenue Journal Entries .......................................................................................................................................... 65 Special Reporting Considerations ........................................................................................................................... 66 Revenue Recordkeeping ........................................................................................................................................... 67 Revenue Disclosures ................................................................................................................................................ 73 Summary .................................................................................................................................................................. 73 Chapter 4 - Review Questions ................................................................................................................................. 74

Chapter 5 – Government Grants .............................................................................................................................. 75 Introduction ............................................................................................................................................................. 75 Overview of Government Grants ............................................................................................................................. 75 Grant Accounting .................................................................................................................................................... 75 Income from Government Grants ............................................................................................................................ 77

Table of Contents

6

Credits on Expenditures .......................................................................................................................................... 77 Grant Reporting ....................................................................................................................................................... 77 Summary .................................................................................................................................................................. 78 Chapter 5 - Review Questions ................................................................................................................................. 79

Chapter 6 - Investment Accounting ......................................................................................................................... 80 Introduction ............................................................................................................................................................. 80 Contributed Investments .......................................................................................................................................... 80 Purchased Investments ............................................................................................................................................ 80 Subsequent Measurement of Investments................................................................................................................. 80 Gains and Losses on Investment .............................................................................................................................. 81 The Equity Method of Accounting ........................................................................................................................... 81 Investment Disclosures ............................................................................................................................................ 84 Summary .................................................................................................................................................................. 85 Chapter 6 - Review Questions ................................................................................................................................. 86

Chapter 7 – Inventory Accounting ........................................................................................................................... 87 Introduction ............................................................................................................................................................. 87 The Periodic Inventory System ................................................................................................................................ 87 The Perpetual Inventory System .............................................................................................................................. 88 Inventory Cost Layering Overview .......................................................................................................................... 89 The First in, First Out Method ................................................................................................................................ 90 The Last in, First Out Method ................................................................................................................................. 91 The Specific Identification Method .......................................................................................................................... 92 The Lower of Cost or Market Rule .......................................................................................................................... 93 Inventory Disclosures .............................................................................................................................................. 95 Summary .................................................................................................................................................................. 96 Chapter 7 - Review Questions ................................................................................................................................. 97

Chapter 8 – Fixed Asset Accounting ........................................................................................................................ 98 Introduction ............................................................................................................................................................. 98 Initial Recognition of Fixed Assets .......................................................................................................................... 98 The Capitalization Limit .......................................................................................................................................... 99 Restrictions on Contributed Assets ........................................................................................................................ 100 Valuation of Contributed Assets ............................................................................................................................ 100 Valuation of Contributed Services ......................................................................................................................... 101 Valuation of Art, Historical Treasures, and Similar Items .................................................................................... 101 Depreciation of Fixed Assets ................................................................................................................................. 102 Depreciation Accounting Entries........................................................................................................................... 104

Table of Contents

7

Accumulated Depreciation .................................................................................................................................... 105 Asset Impairment ................................................................................................................................................... 106 Recordation of Fixed Assets .................................................................................................................................. 106 Fixed Asset Disclosures ......................................................................................................................................... 107 Summary ................................................................................................................................................................ 108 Chapter 8 - Review Questions ............................................................................................................................... 109

Chapter 9 - Lease Accounting ................................................................................................................................ 110 Introduction ........................................................................................................................................................... 110 The Nature of a Lease ............................................................................................................................................ 110 Lease Components (Lessee) ................................................................................................................................... 111 Initial Direct Costs ................................................................................................................................................ 113 Lease Consideration .............................................................................................................................................. 113 The Lease Term ..................................................................................................................................................... 113 Initial Measurement of Lease Payments ................................................................................................................ 114 Subsequent Measurement of Lease Payments ........................................................................................................ 115 Types of Leases ...................................................................................................................................................... 115 Asset and Liability Recognition (Lessee) ............................................................................................................... 116

Initial Measurement ........................................................................................................................................... 116 Short-Term Leases ............................................................................................................................................. 116 Finance Leases ................................................................................................................................................... 116 Operating Leases ............................................................................................................................................... 118 Right-of-Use Asset Impairment ......................................................................................................................... 118 Leasehold Improvement Amortization .............................................................................................................. 119 Subleases ........................................................................................................................................................... 119 Maintenance Deposits ........................................................................................................................................ 119 Derecognition .................................................................................................................................................... 119

Elections ................................................................................................................................................................ 120 Discount Rate .................................................................................................................................................... 120 Separation of Non-Lease Components .............................................................................................................. 120

Sale and Leaseback Transactions .......................................................................................................................... 120 Lease Disclosures .................................................................................................................................................. 121

Lessee Disclosures ............................................................................................................................................. 122 Sale and Leaseback Transactions ...................................................................................................................... 123

Summary ................................................................................................................................................................ 123 Review Questions ................................................................................................................................................... 124

Chapter 10 – Pension Plan Accounting .................................................................................................................. 125 Introduction ........................................................................................................................................................... 125 Overview of Retirement Benefits............................................................................................................................ 125 Defined Benefit Plans ............................................................................................................................................ 125

Expense Attribution for Delayed Vesting .......................................................................................................... 128 Discount Rates ................................................................................................................................................... 129 Settlements and Curtailments ............................................................................................................................ 129

Table of Contents

8

Termination Benefits ......................................................................................................................................... 130 Combined Pension Plans ................................................................................................................................... 131

Defined Contribution Plans ................................................................................................................................... 131 Presentation of Retirement Benefit Information .................................................................................................... 131 Retirement Benefit Disclosures .............................................................................................................................. 131

Defined Benefit Plan Disclosures ...................................................................................................................... 131 Plan Assets ......................................................................................................................................................... 134 Defined Contribution Plan Disclosures ............................................................................................................. 134

Summary ................................................................................................................................................................ 134 Chapter 10 - Review Questions ............................................................................................................................. 135

Chapter 11 – Joint Costs and Allocations .............................................................................................................. 136 Introduction ........................................................................................................................................................... 136 Costs of Activities that Include Fundraising .......................................................................................................... 136 Allocations ............................................................................................................................................................. 140 Disclosures ............................................................................................................................................................ 143 Summary ................................................................................................................................................................ 143 Chapter 11 – Review Questions ............................................................................................................................. 144

Chapter 12 – Accounting Changes and Error Corrections .................................................................................. 145 Introduction ........................................................................................................................................................... 145 Changes in Accounting Principle .......................................................................................................................... 145 Changes in Accounting Estimate ........................................................................................................................... 146 Changes in Reporting Entity .................................................................................................................................. 146 Correction of an Error in Previously Issued Financial Statements ....................................................................... 146 Corrections Related to Prior Interim Periods ....................................................................................................... 147 Summary ................................................................................................................................................................ 147 Chapter 12 – Review Questions ............................................................................................................................. 148

Chapter 13 – Fair Value .......................................................................................................................................... 149 Introduction ........................................................................................................................................................... 149 The Fair Value Concept......................................................................................................................................... 149

Fair Value Differences from Actual Prices Paid ................................................................................................ 150 Fair Value Measurement Approaches ................................................................................................................ 150 Fair Value Option .............................................................................................................................................. 152

Summary ................................................................................................................................................................ 153 Chapter 13 – Review Questions ............................................................................................................................. 154

Chapter 14 – Other Accounting Topics ................................................................................................................. 155 Introduction ........................................................................................................................................................... 155 Petty Cash .............................................................................................................................................................. 155 Interest in a Perpetual Trust .................................................................................................................................. 157

Table of Contents

9

Receivables ............................................................................................................................................................ 157 Contingent Liabilities ............................................................................................................................................ 157 Line of Credit ......................................................................................................................................................... 158 Disclosures ............................................................................................................................................................ 159 Summary ................................................................................................................................................................ 159 Chapter 14 – Review Questions ............................................................................................................................. 159

Chapter 15 – Split-Interest Agreements ................................................................................................................ 161 Introduction ........................................................................................................................................................... 161 Split-Interest Agreements ....................................................................................................................................... 161

Types of Split-Interest Agreements ................................................................................................................... 161 Accounting for Split-Interest Agreements ......................................................................................................... 162 Initial Measurement ........................................................................................................................................... 163 Ongoing Measurement....................................................................................................................................... 164 Termination ....................................................................................................................................................... 164

Classification of Net Assets ................................................................................................................................... 164 Disclosures ............................................................................................................................................................ 165 Summary ................................................................................................................................................................ 165 Chapter 15 – Review Questions ............................................................................................................................. 166

Chapter 16 – Affiliated Organizations ................................................................................................................... 167 Introduction ........................................................................................................................................................... 167 Affiliated Organizations......................................................................................................................................... 167 Special Purpose Entities ........................................................................................................................................ 168 Noncontrolling Interests ........................................................................................................................................ 169 Related Parties ...................................................................................................................................................... 169 Disclosures ............................................................................................................................................................ 170

Revenue Sharing ................................................................................................................................................ 170 Consolidated Financial Statements .................................................................................................................... 170 Noncontrolling Interests .................................................................................................................................... 170 Related Party Transactions ................................................................................................................................ 171

Summary ................................................................................................................................................................ 172 Chapter 16 – Review Questions ............................................................................................................................. 172

Chapter 17 – Mergers and Acquisitions ................................................................................................................ 173 Introduction ........................................................................................................................................................... 173 The Nonprofit Merger ............................................................................................................................................ 173 The Nonprofit Acquisition ...................................................................................................................................... 173

Identifiable Assets and Liabilities, and Noncontrolling Interests ...................................................................... 175 Goodwill Calculation ......................................................................................................................................... 177 Contribution Received ....................................................................................................................................... 178 Presentation Issues ............................................................................................................................................. 178

Goodwill Amortization Option .............................................................................................................................. 178

Table of Contents

10

Goodwill Testing.................................................................................................................................................... 179 Disclosures ............................................................................................................................................................ 182

Merger Disclosures ............................................................................................................................................ 182 Acquisition Disclosures ..................................................................................................................................... 184

Summary ................................................................................................................................................................ 185 Chapter 17 – Review Questions ............................................................................................................................. 186

Chapter 18 – Nonprofit Tax Reporting ................................................................................................................. 187 Introduction ........................................................................................................................................................... 187 Overview of the Form 990 ..................................................................................................................................... 187 The Form 990 ........................................................................................................................................................ 190 The Form 990-EZ .................................................................................................................................................. 192 The Form 990-N .................................................................................................................................................... 195 The Form 990-T ..................................................................................................................................................... 195 The Form 1099 ...................................................................................................................................................... 196 The Form W-2 ........................................................................................................................................................ 197 Form W-3 ............................................................................................................................................................... 200 Payroll Taxes ......................................................................................................................................................... 202

Social Security Tax ............................................................................................................................................ 202 Medicare Tax ..................................................................................................................................................... 203 Types of Tax Deposit Schedules ....................................................................................................................... 203 The Form 941 .................................................................................................................................................... 206

Summary ................................................................................................................................................................ 210 Chapter 18 – Review Questions ............................................................................................................................. 211

Chapter 19 – Closing the Books.............................................................................................................................. 212 Introduction ........................................................................................................................................................... 212 Journal Entries ...................................................................................................................................................... 212

The Accruals Concept........................................................................................................................................ 212 Adjusting Entries ............................................................................................................................................... 213 Reversing Entries ............................................................................................................................................... 213 Common Adjusting Entries ............................................................................................................................... 214 Closing Entries .................................................................................................................................................. 217

Prior Closing Steps: Update Reserves ................................................................................................................... 218 Core Closing Steps: Issue Customer and Donor Invoices ..................................................................................... 219 Core Closing Steps: Reconcile the Bank Statement ............................................................................................... 219 Core Closing Steps: Calculate Depreciation ......................................................................................................... 221 Core Closing Steps: Accounts Payable ................................................................................................................. 221 Core Closing Steps: Review Journal Entries ......................................................................................................... 222 Core Closing Steps: Reconcile Accounts ............................................................................................................... 223 Core Closing Steps: Close Subsidiary Ledgers ..................................................................................................... 224 Core Closing Steps: Create Financial Statements ................................................................................................. 225

Table of Contents

11

Core Closing Steps: Review Financial Statements ................................................................................................ 225 Core Closing Steps: Accrue Tax Liabilities ........................................................................................................... 225 Core Closing Steps: Close the Month .................................................................................................................... 226 Core Closing Steps: Add Disclosures .................................................................................................................... 226 Core Steps: Issue Financial Statements ................................................................................................................. 226 Delayed Closing Steps: Issue Invoices .................................................................................................................. 226 Delayed Closing Steps: Closing Metrics ............................................................................................................... 227 Delayed Closing Steps: Document Future Closing Changes ................................................................................ 227 Delayed Closing Steps: Update Closing Procedures ............................................................................................ 228 Summary ................................................................................................................................................................ 228 Chapter 19 – Review Questions ............................................................................................................................. 229

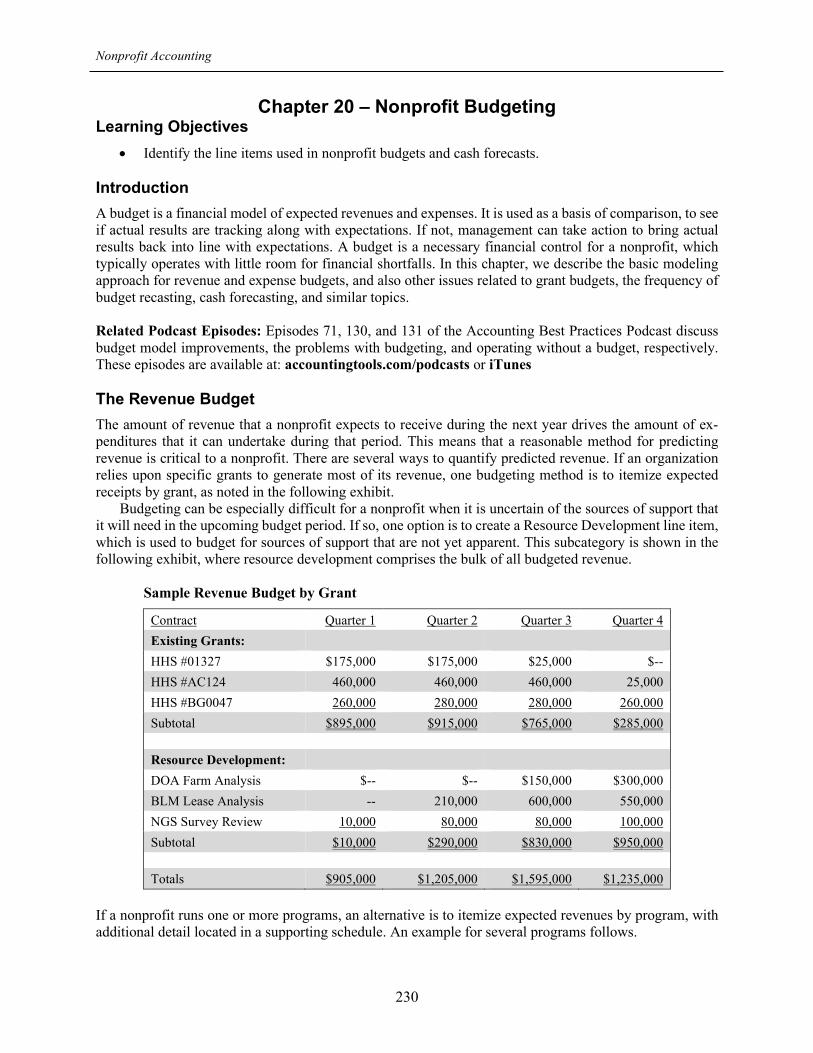

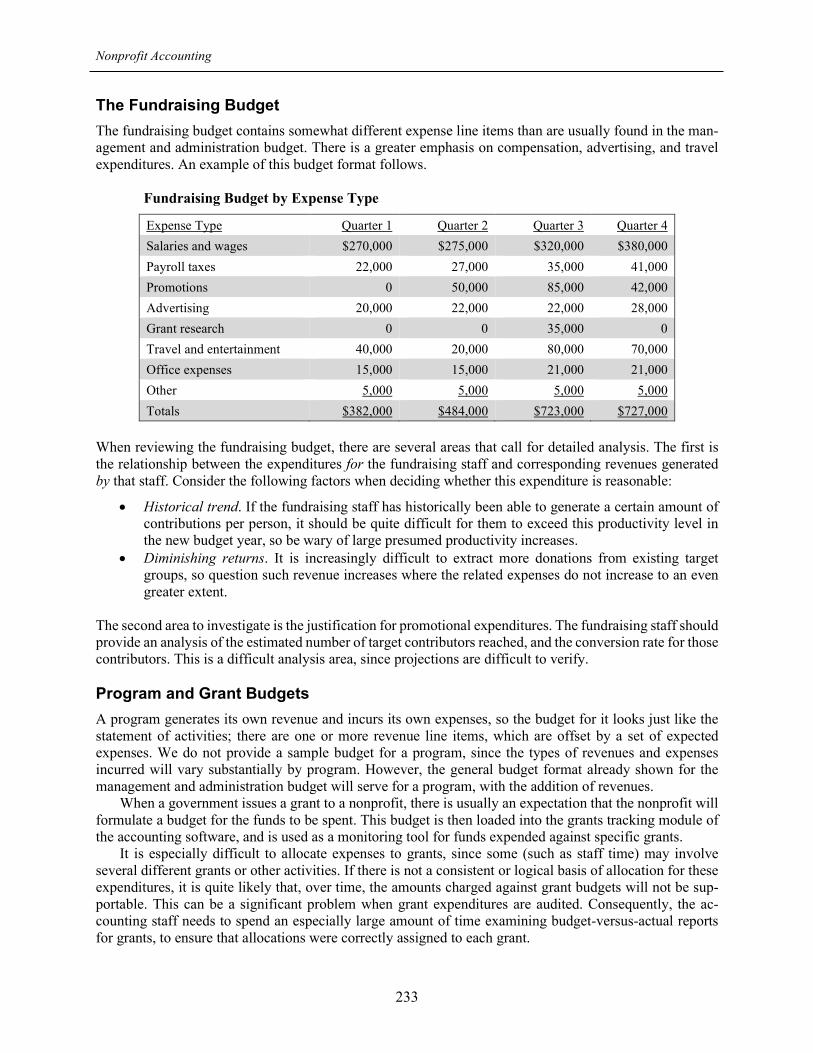

Chapter 20 – Nonprofit Budgeting ......................................................................................................................... 230 Introduction ........................................................................................................................................................... 230 The Revenue Budget .............................................................................................................................................. 230 The Management and Administration Budget ....................................................................................................... 231 The Fundraising Budget ........................................................................................................................................ 233 Program and Grant Budgets ................................................................................................................................. 233 The Compensation Budget ..................................................................................................................................... 234

The Compensation Budget ................................................................................................................................ 234 Treatment of Hourly Pay and Overtime............................................................................................................. 236 The Benefits Budget .......................................................................................................................................... 237

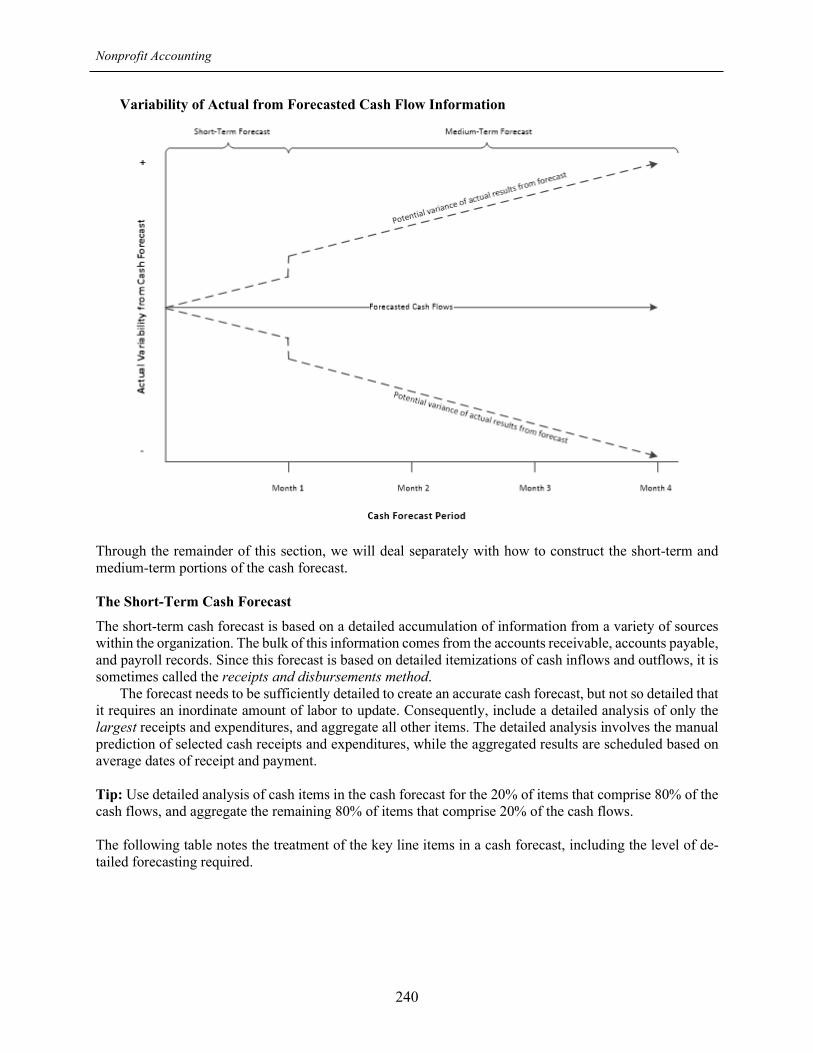

Budget Recasting ................................................................................................................................................... 239 Budget Linkages .................................................................................................................................................... 239 Cash Forecasting ................................................................................................................................................... 239

The Short-Term Cash Forecast .......................................................................................................................... 240 The Medium-Term Cash Forecast ..................................................................................................................... 243

Summary ................................................................................................................................................................ 244 Chapter 20 – Review Questions ............................................................................................................................. 245

Chapter 21 – Accounting Controls ......................................................................................................................... 246 Introduction ........................................................................................................................................................... 246 The Proper Balance of Control Systems ................................................................................................................ 246 Control Principles ................................................................................................................................................. 248 Constructing a System of Controls ........................................................................................................................ 249 Cash Controls ........................................................................................................................................................ 250 Fixed Asset Controls .............................................................................................................................................. 252 Payables Controls .................................................................................................................................................. 254 Payroll Controls .................................................................................................................................................... 258 Summary ................................................................................................................................................................ 262

Table of Contents

12

Chapter 21 – Review Questions ............................................................................................................................. 263

Chapter 22 – Nonprofit Policies ............................................................................................................................. 264 Introduction ........................................................................................................................................................... 264 General Accounting Policies ................................................................................................................................. 264

Cash ................................................................................................................................................................... 264 Fixed Assets ....................................................................................................................................................... 264 Payables ............................................................................................................................................................. 266 Payroll................................................................................................................................................................ 267

Nonprofit-Specific Policies .................................................................................................................................... 267 Donor Receipts .................................................................................................................................................. 267 Donated Assets .................................................................................................................................................. 268 Investments ........................................................................................................................................................ 268 Operations .......................................................................................................................................................... 269 Joint Ventures .................................................................................................................................................... 270 Lobbying and Political Campaigns .................................................................................................................... 271 Tax Filings ......................................................................................................................................................... 271

Summary ................................................................................................................................................................ 271 Chapter 22 – Review Questions ............................................................................................................................. 272

Chapter 23 – Analysis of a Nonprofit’s Financial Health .................................................................................... 273 Introduction ........................................................................................................................................................... 273 The Auditor’s Report ............................................................................................................................................. 273 Horizontal Analysis ............................................................................................................................................... 274 Vertical Analysis .................................................................................................................................................... 275 Expense Proportions Analysis ............................................................................................................................... 277 Fundraising Effectiveness Ratio ............................................................................................................................ 278 Revenue Concentration Analysis ........................................................................................................................... 279 Traffic Light Revenue Analysis .............................................................................................................................. 280 Traditional Ratio Analysis ..................................................................................................................................... 280

Current Ratio ..................................................................................................................................................... 280 Quick Ratio ........................................................................................................................................................ 281 Days Sales in Accounts Receivable ................................................................................................................... 282 Days Sales in Inventory ..................................................................................................................................... 283 Days Payables Outstanding ............................................................................................................................... 283

Free Cash Flow ..................................................................................................................................................... 284 The Profitability Conundrum ................................................................................................................................. 285 Summary ................................................................................................................................................................ 285 Chapter 23 – Review Questions ............................................................................................................................. 286

Review Question Answers and Rationales ............................................................................................................. 287

Glossary .................................................................................................................................................................... 298

Index ......................................................................................................................................................................... 303

Table of Contents

13

Qualified Assessment ............................................................................................................................................... 307

Answer Sheet ............................................................................................................................................................ 318

Course Evaluation ................................................................................................................................................... 344

Nonprofit Accounting

14

Chapter 1 – Overview of the Nonprofit Entity Learning Objectives After completing this section of the course, you will be able to:

• Cite why the 501(c)(3) designation is valuable and what an entity with such designation cannot engage in • Specify an activity that a 501(c)(3) entity is likely to engage in

Introduction There are more than 1.5 million nonprofit organizations in the United States, according to the National Center for Charitable Statistics. These organizations account for more than 9% of the total wages and sala-ries paid in the United States. To give the reader a better understanding of this massive part of the economy, we define in this chapter the nonprofit entity, its tax classification, filing requirements, and organizational structure. Definition of a Nonprofit Entity Many entities consider themselves to be nonprofits, and advertise themselves as such. But what is a non-profit? According to the Financial Accounting Standards Board (which issues the accounting standards that govern nonprofits), the key criteria that define a nonprofit are:

• No ownership interests • An operating purpose other than to earn a profit • It receives significant contributions from third parties that do not expect a return

Conversely, an entity that cannot be considered a nonprofit is one that is owned by investors, or which provides dividends or other economic benefits to its owners or members. Thus, credit unions and employee benefit plans are not considered nonprofit entities.

To further clarify the status of nonprofits, the types of organizations included the following table are all considered to be nonprofits.

General Types of Nonprofit Entities

Cemetery organizations Political parties Civic and community organizations Political action committees Colleges and universities Private and community foundations Cultural organizations Professional associations Elementary and secondary schools Public broadcasting stations Federated fundraising organizations Religious organizations Fraternal organizations Research and scientific organizations Health care entities Social and country clubs Labor unions Trade associations Libraries Voluntary health and welfare entities Museums Zoological and botanical societies Performing arts organizations

Many nonprofit organizations seek nonprofit status from the Internal Revenue Service (IRS), so that they can avoid paying federal income taxes, and can instead plow these funds back into their core missions. The

Nonprofit Accounting

15

IRS deals with these organizations in section 501(c) of the Internal Revenue Code. This section of the Code currently provides for 29 types of nonprofit organizations, which are as follows: Types of Nonprofit Organizations

Section of IRS Code

Organization Type

Activities Conducted

501(c)(1) Corporations organized under an Act of Con-gress

Instrumentalities of the United States

501(c)(2) Title holding corporation for exempt organi-zation

Holds title to property of an exempt organization

501(c)(3) Religious, educational, charitable, scientific, literary, testing for public safety, to foster na-tional or international sports competition, or prevention of cruelty to children or animals organizations

Activities of a nature implied by the description of the class of organization

501(c)(4) Civic leagues, social welfare organizations, and local associations of employees

Promotion of community welfare; charitable, edu-cational, or recreational

501(c)(5) Labor, agricultural, and horticultural organi-zations

Educational; the purpose being to improve condi-tions of work, and to improve efficiency

501(c)(6) Business leagues, chambers of commerce, and real estate boards

Improvement of business conditions of one or more lines of business

501(c)(7) Social and recreational clubs Pleasure, recreation, and social activities 501(c)(8) Fraternal societies and associations Lodge providing for payment of life, sickness, acci-

dent or other benefits to members 501(c)(9) Voluntary employees beneficiary associa-

tions Providing for payment of life, sickness, accident, or other benefits to members

501(c)(10) Domestic fraternal societies and associations Lodge devoting its net earnings to charitable, frater-nal, and other specified purposes

501(c)(11) Teachers’ retirement fund associations Teachers’ association for payment of retirement benefits

501(c)(12) Benevolent life insurance associations, mu-tual ditch or irrigation companies, mutual or cooperative telephone companies, etc.

Activities of a mutually beneficial nature similar to those implied by the description of the organization

501(c)(13) Cemetery companies Burials and incidental activities 501(c)(14) State-chartered credit unions, mutual reserve

funds Loans to members

501(c)(15) Mutual insurance companies or associations Providing insurance to members substantially at cost

501(c)(16) Cooperative organizations to finance crop operations

Financing crop operations in conjunction with ac-tivities of a marketing or purchasing association

501(c)(17) Supplemental unemployment benefit trusts Provides for payment of supplemental unemploy-ment compensation benefits

501(c)(18) Employee funded pension trust (created be-fore June 25, 1959)

Payment of benefits under a pension plan funded by employees

Nonprofit Accounting

16

Section of IRS Code

Organization Type

Activities Conducted

501(c)(19) Post or organization of past or present mem-bers of the armed forces

Activities implied by the nature of the organization

501(c)(20) Formerly used for group legal services plan No longer used 501(c)(21) Black lung benefit trusts Funded by coal mine operators to satisfy their lia-

bility for disability or death due to black lung dis-eases

501(c)(22) Withdrawal liability payment fund To provide funds to meet the liability of employers withdrawing from a multi-employer pension fund

501(c)(23) Veterans’ organization (created before 1880) To provide insurance and other benefits to veterans 501(c)(24) Formerly used for Section 4049 ERISA

trusts No longer used

501(c)(25) Title holding corporations or trusts with mul-tiple parent corporations

Holding title and paying over income from property to 35 or fewer parents or beneficiaries

501(c)(26) State-sponsored organization providing health coverage for high-risk individuals

Provides health care coverage to high-risk individu-als

501(c)(27) State-sponsored workers’ compensation rein-surance organization

Reimburse members for losses under workers’ compensation acts

501(c)(28) National railroad retirement investment trust Manages and invests the assets of the Railroad Re-tirement Account

501(c)(29) CO-OP health insurance issuers A qualified health insurance issuer which has re-ceived a loan or grant under the CO-OP program

(Extracted from the Organization Reference Chart in IRS Publication 557, Tax-Exempt Status for Your Organization) Most of the subsections of this code deal with very specific types of organizations, and so do not apply to most nonprofits. The area that is applicable to the largest cross-section of nonprofits is 501(c)(3), which applies to religious, educational, charitable, scientific, literary, testing for public safety, fostering of national or international sports competition, or prevention of cruelty to children or animals organizations. Most of the entities granted 501(c)(3) status have operations that are either charitable, educational, or religious in nature. This subset of entities engages in the following types of activities: Charitable

• Relief of the poor or underprivileged • Advancement of religion • Advancement of education or science • Construction or maintenance of public buildings and other works • Reduction of the burdens of government • Reduction of neighborhood tensions • Elimination of prejudice and discrimination • Defense of human and civil rights • Reduction of community deterioration and juvenile delinquency

Educational

• Schools, including primary and secondary schools, colleges, and trade schools • Public discussion forums, panels, and lectures

Nonprofit Accounting

17

• Correspondence instruction via radio or television • Museums, orchestras, planetariums, and zoos • Non-profit day-care facilities • Youth sports organizations

Religious

• Churches, including mosques, synagogues, and temples • Mission organizations • Speakers’ organizations • Nondenominational ministries and ecumenical organizations • Faith-based social agencies

The 501(c)(3) designation is especially important, because donors can make tax-deductible donations to these organizations. Both individuals and corporations are much more likely to donate to a 501(c)(3) entity for this reason. In addition, local governments may grant these organizations exemption from income, sales, or property taxes. Thus, the 501(c)(3) designation is highly prized. Conversely, other types of nonprofit organizations may not qualify for these tax-deductible donations, and so are much less likely to attract contributions from donors. For example, a social or recreational club (designated as a 501(c)(7) organiza-tion) does not pay income taxes, but donations to it are not tax-deductible.

The IRS mandates the following requirements for an entity that wishes to apply for the 501(c)(3) des-ignation:

• The entity is organized and operated exclusively for one or more exempt purposes. This means that the entity is organized as a corporation, trust, or unincorporated association. The articles of incor-poration (or equivalent) must:

o Limit the purposes of the entity to exempt activities; o Not expressly permit activities unrelated to the exempt mission of the entity; and o Permanently dedicate its assets to the designated exempt purposes.

• The entity cannot engage in the following activities:

o Participation in the political campaigns of candidates for any office o Lobbying activities, other than an insubstantial part of total activities o Have its earnings benefit an individual o Operate for the benefit of any private interests, such as the founder or the founder’s family o Operate a trade or business not related to its exempt purpose o Engage in activities that are illegal or violate public policy

If the 501(c)(3) designation is granted to a nonprofit, the entity then has the following obligations from the perspective of the IRS:

• Recordkeeping. Keep sufficiently detailed records that include sources of support, such as contri-butions, grants, and sponsorships.

• Filings. File an annual report with the IRS, which may be either the Form 990, Form 990-EZ, Form 990-N (reserved for entities with gross receipts of $50,000 or less), or Form 990-PF (which is filed by private foundations). The Form 990-T is also filed to report any gross income from an unrelated trade or business of $1,000 or more. A few entities are exempted from filing these forms. If a nonprofit does not file one of these forms for three consecutive years, it loses its tax-exempt status.

Note: Churches are exempt from filing the Form 990.

Nonprofit Accounting

18

• Public inspection. A nonprofit must make its 501(c)(3) application and annual returns available for

public inspection. • Donation documentation. The entity must provide to donors a written acknowledgement of any

donation made of $250 or more. Also, a written disclosure must be made to any donor paying the entity more than $75 that is partly a contribution, and partly for goods and services provided by the entity.

To apply for 501(c)(3) status, an entity must complete and submit to the IRS the Form 1023, Application for Recognition of Exemption under Section 501(c)(3) of the Internal Revenue Code. This form must be filed no later than the end of the 27th month after the entity was legally formed. If the status is then granted, the tax exemption is considered to be from the date of creation of the entity. If an entity instead files after the deadline, the tax exemption will take effect only as of the date of the application, though it is possible to request a retroactive exemption.

An IRS examiner will review the Form 1023 and any attached documentation, to see if the submitting entity is worthy of 501(c)(3) status. This can be a prolonged process that calls for the submission of addi-tional documentation to the IRS. If the review is favorable, the IRS will issue a determination letter that recognizes the tax-exempt status of the entity. Many larger donors will request a copy of this determination letter before they agree to issue contributions. Tip: The determination letter is an important document, and so should be stored in a nonprofit’s permanent file, where it is less likely to be mislaid or destroyed. Consider retaining copies in several locations. If lost, the letter can be replaced by the IRS with a letter confirming the tax-exempt status of the entity. When a donor makes a contribution to a nonprofit that can be classified as a charitable deduction, the donor then claims the contribution on his or her individual tax return. It is the responsibility of the donor to deter-mine the amount that can be deducted, and when to do so. The nonprofit has no liability for how a donor uses a tax deduction. Nonprofit Organizational Structure Though earning a profit is not the main intent of a nonprofit, it is critical for the organization to be properly run, to ensure that programs are properly administered, contributions are solicited in an effective manner, and expenses are closely monitored. Consequently, a nonprofit may have an organizational structure that is similar in some respects to that of a for-profit entity. There is a board of directors whose members are ultimately responsible for the strategic direction of the organization. The executive director fulfills the role of a chief executive officer, managing the enterprise on behalf of the board of directors. Below the executive director are department managers. Typical manager titles may include several program directors, a control-ler and an administration director. There is also likely to be a fundraising coordinator, who is also known as a development director. If a large number of volunteers work on behalf of the organization, there may also be a volunteer coordinator. The following organization chart shows the higher levels of a nonprofit.

Nonprofit Accounting

19

Nonprofit Organizational Structure

Board of Directors

Executive Director

Controller

Director of Administration

Development Director

Program Director

Volunteer Coordinator

Related Podcast Episode: Episode 285 of the Accounting Best Practices Podcast discusses the nonprofit CFO. The episode is available at: accountingtools.com/podcasts or iTunes Summary In this chapter, we have defined the nonprofit entity and pointed out its tax status, filing requirements, and organizational structure. In the following chapters, we turn to the accounting and tax reporting requirements of the nonprofit organization. Some of these topics are highly specific to nonprofits, such as the accounting for government grants, split-interest agreements, and contributions. Other topics, such as lease accounting, budgeting, and closing the books, can be applied to all types of organizations, but are still critical to the proper recordation, reporting, and control of accounting transactions by a nonprofit.

Nonprofit Accounting

20