non face-to-face transactions: risks and challenges richard parlour financial markets law...

TRANSCRIPT

Non Face-to-Face Transactions:

Risks and ChallengesRichard Parlour

Financial Markets Law International

© FMLI 2006

OARRs

• Outcome

• Agenda

• Roles

• Rules

© FMLI 2006

Outcome

• Risks of non face-to-face (NF2F) transactions

• Regulation of NF2F transactions

• Psychology of NF2F transactions

• Developing solutions for challenges of NF2F transactions

Agenda

• Key Issues• International

Experience • Role of Psychology• Developing Solutions

Roles

Richard Active participants

HANDOUT!!

Handout Survey

• Ten statements

• Select which response closest to you

• No right or wrong answers

• Be as honest as possible

• Self marking

Rules

Background for NF2F

• Desire to be Offshore Financial Centre

• Growing industrial, financial, tourism, IT sectors

• 5-6% annual growth since 1968

• >10,000 offshore entities• Banking sector

investment > $1 billion• India, South Africa• Internet banking

Local Background Risk

• Minor consumer and trans-shipment point for South Asian heroin

• Small amounts cannabis produced and consumed locally

• Low terrorism risk and experience• Significant offshore financial industry creates ML

potential • Corruption levels low (TI level 4.1)• Government committed to regulation, moderate

country risk

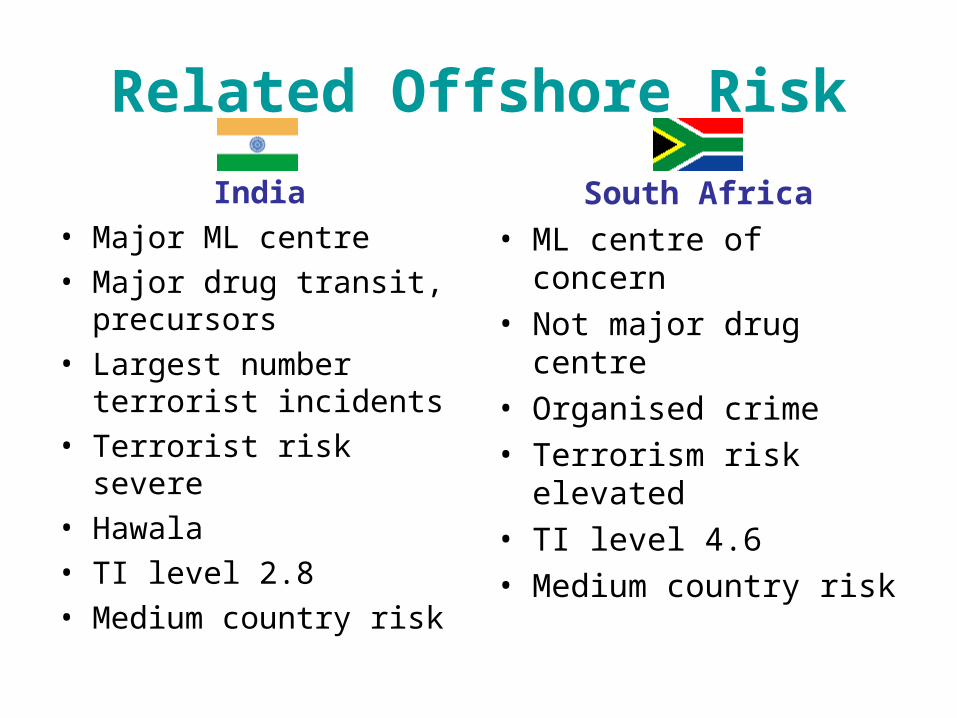

Related Offshore Risk

India• Major ML centre• Major drug transit,

precursors• Largest number terrorist

incidents• Terrorist risk severe• Hawala• TI level 2.8• Medium country risk

South Africa• ML centre of concern• Not major drug centre• Organised crime• Terrorism risk elevated• TI level 4.6• Medium country risk

Non Face-to-Face Transactions

Medium• Post• Telegraph• Telephone• Fax• Email• Internet• SMS• Instant messaging• Dealing system• Electronic banking

Risks

• “Physicalities loss”

• Privacy

• Hacking

• Cracking

• Spyware

• Data loss

• Ease of access

• Depersonalisation of contact

• Transaction speed

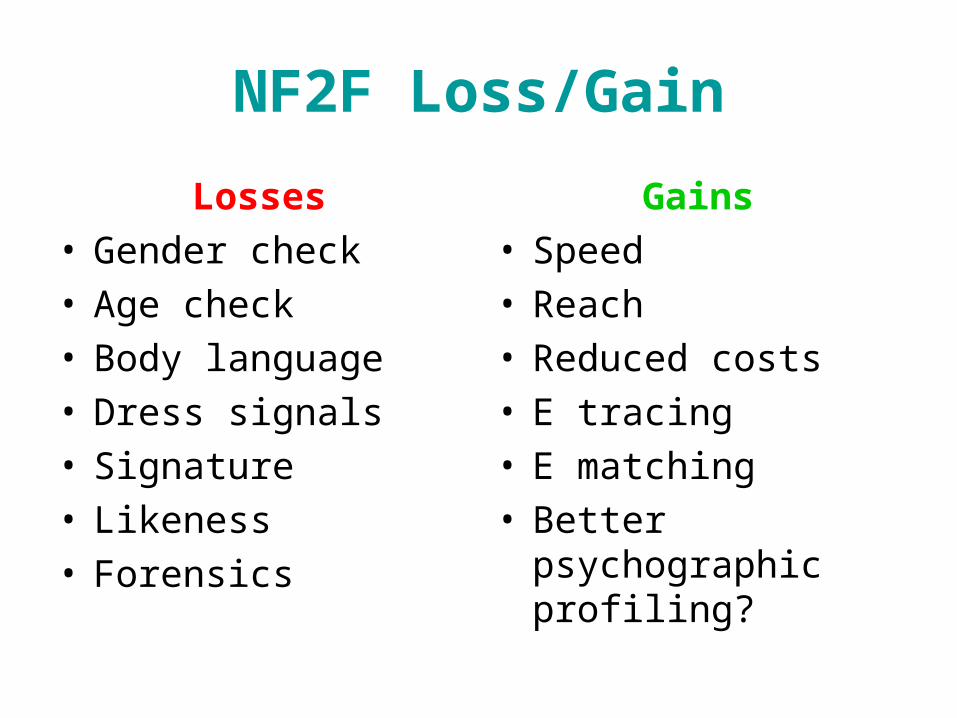

NF2F Loss/Gain

Losses• Gender check• Age check• Body language• Dress signals• Signature• Likeness• Forensics

Gains• Speed• Reach• Reduced costs• E tracing• E matching• Better psychographic

profiling?

International Experience on NF2F

• FATF recommendation 8 – policies and procedures to address any specific risks with NF2F business relationships or transactions

• BIS BCBS CDD paper 2001 2.2.6:– Apply equally effective ID procedures– Specific and adequate measures to mitigate higher

risk

• EU MLD 3 Art 13.2• Wolfsberg 1.2.5 - specifically address measures

to establish ID of NF2F customers satisfactorily

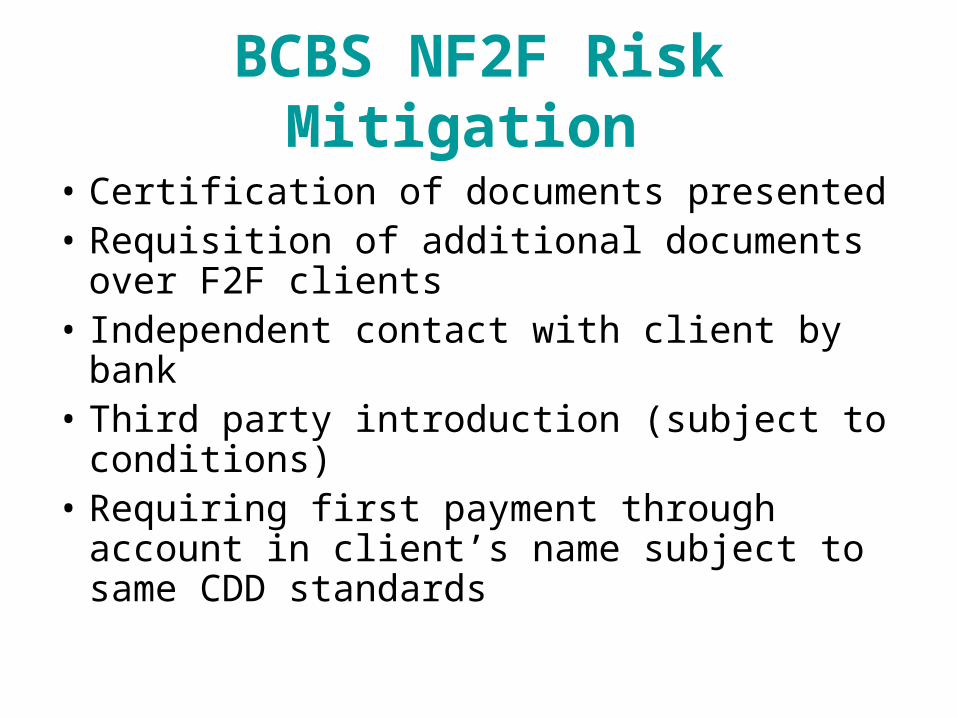

BCBS NF2F Risk Mitigation

• Certification of documents presented• Requisition of additional documents over

F2F clients• Independent contact with client by bank• Third party introduction (subject to

conditions)• Requiring first payment through account in

client’s name subject to same CDD standards

EU Third Money Laundering Directive Art 13.2

Where customer not physically present for ID, take specific and adequate measures for higher risk:

• ensuring customer ID established by additional documents, data or information;

• extra measures to verify/certify documents supplied, or confirmatory certification by MLD 3 financial institution;

• ensuring first payment through account in customer’s name with a credit institution.

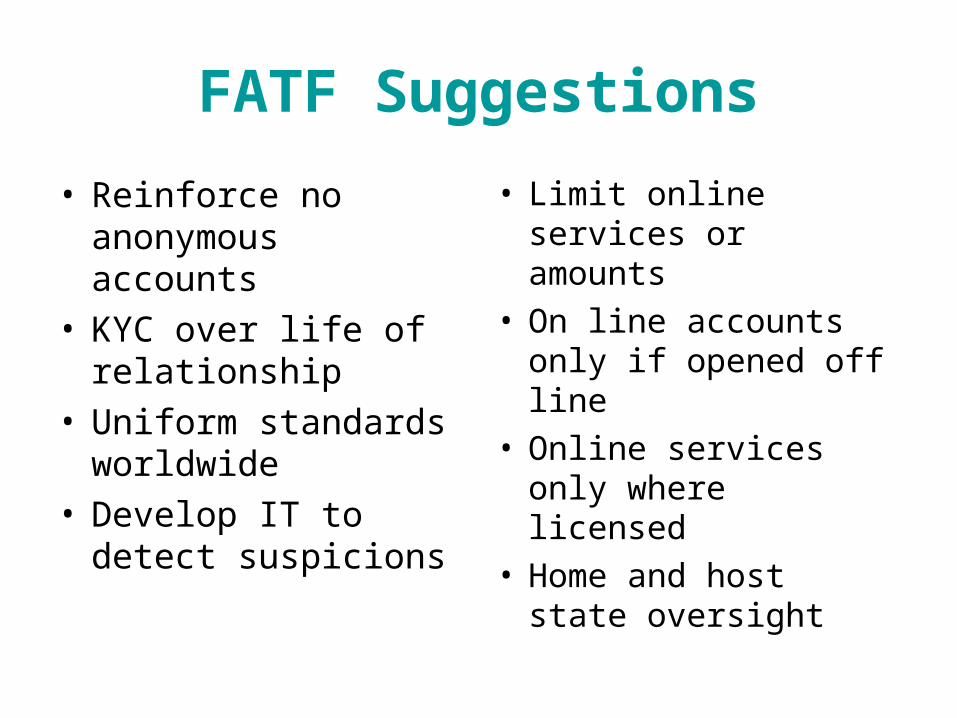

FATF Suggestions

• Reinforce no anonymous accounts

• KYC over life of relationship

• Uniform standards worldwide

• Develop IT to detect suspicions

• Limit online services or amounts

• On line accounts only if opened off line

• Online services only where licensed

• Home and host state oversight

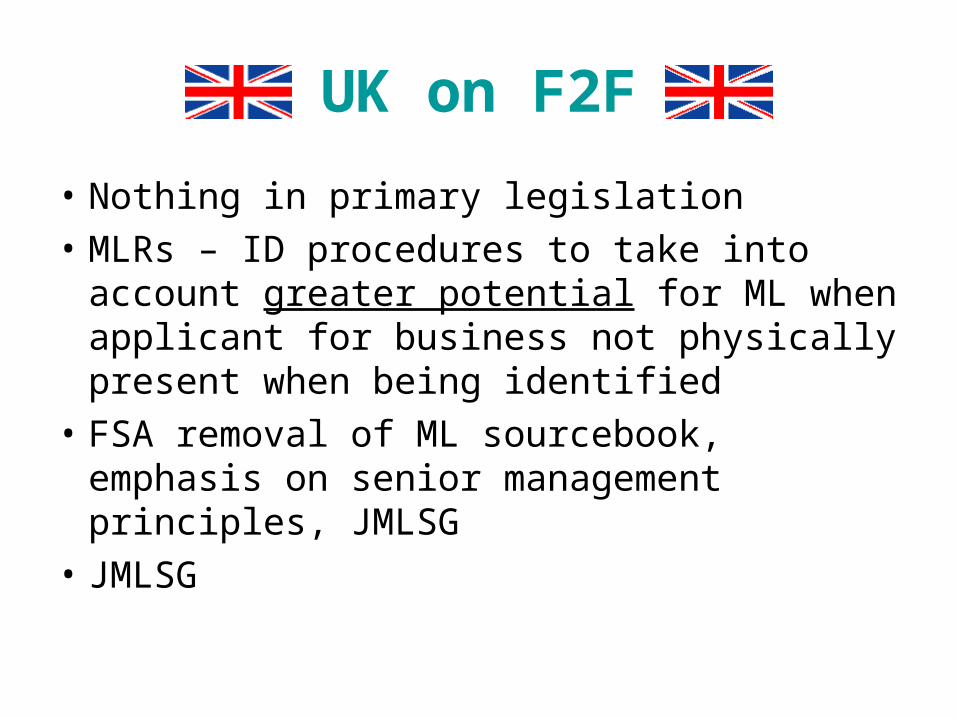

UK on F2F

• Nothing in primary legislation

• MLRs – ID procedures to take into account greater potential for ML when applicant for business not physically present when being identified

• FSA removal of ML sourcebook, emphasis on senior management principles, JMLSG

• JMLSG

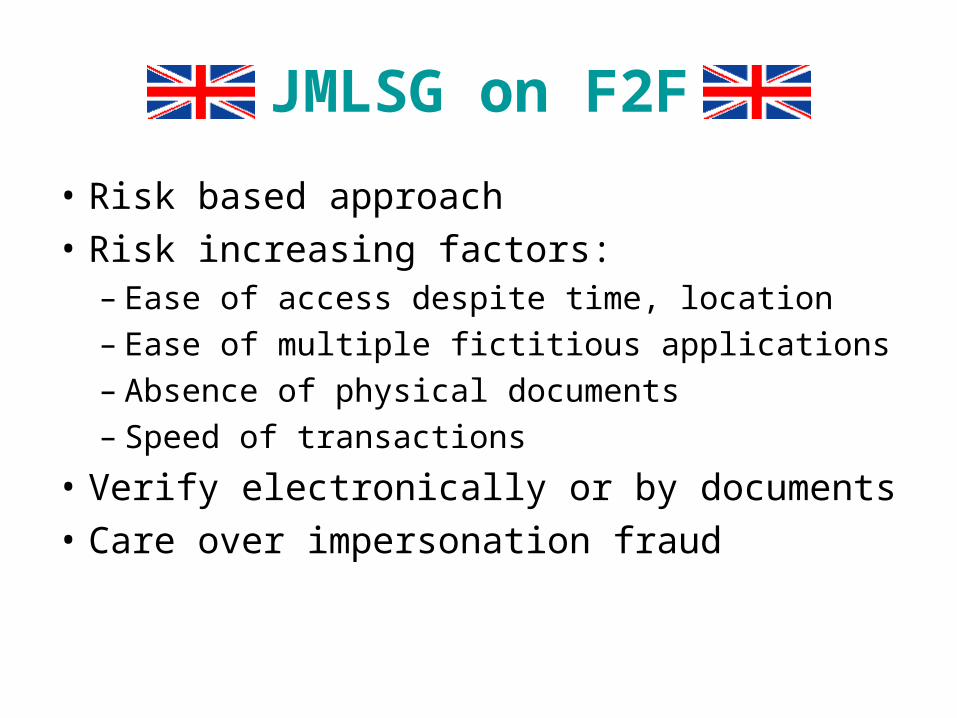

JMLSG on F2F

• Risk based approach

• Risk increasing factors:– Ease of access despite time, location– Ease of multiple fictitious applications– Absence of physical documents– Speed of transactions

• Verify electronically or by documents

• Care over impersonation fraud

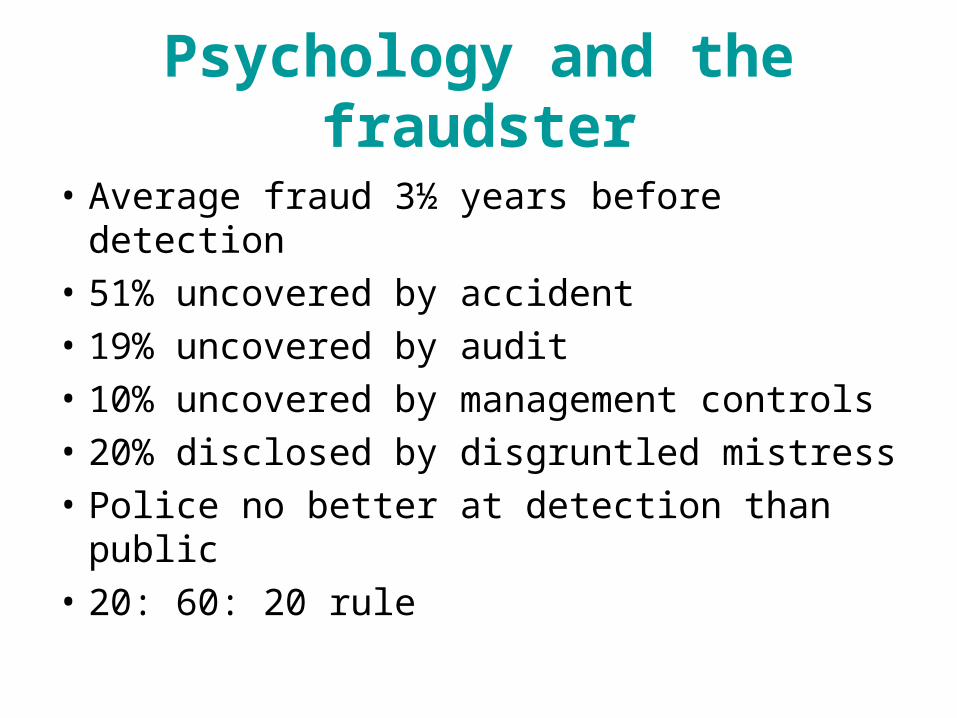

Psychology and the fraudster

• Average fraud 3½ years before detection

• 51% uncovered by accident

• 19% uncovered by audit

• 10% uncovered by management controls

• 20% disclosed by disgruntled mistress

• Police no better at detection than public

• 20: 60: 20 rule

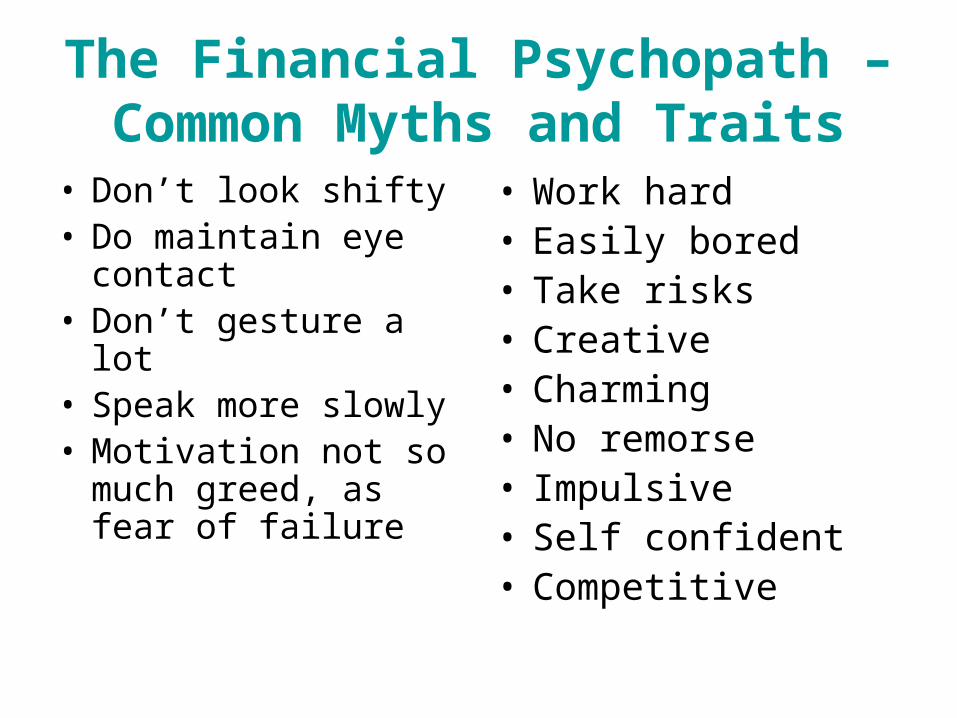

The Financial Psychopath – Common Myths and Traits

• Don’t look shifty• Do maintain eye

contact• Don’t gesture a lot• Speak more slowly• Motivation not so

much greed, as fear of failure

• Work hard • Easily bored • Take risks • Creative • Charming • No remorse • Impulsive• Self confident• Competitive

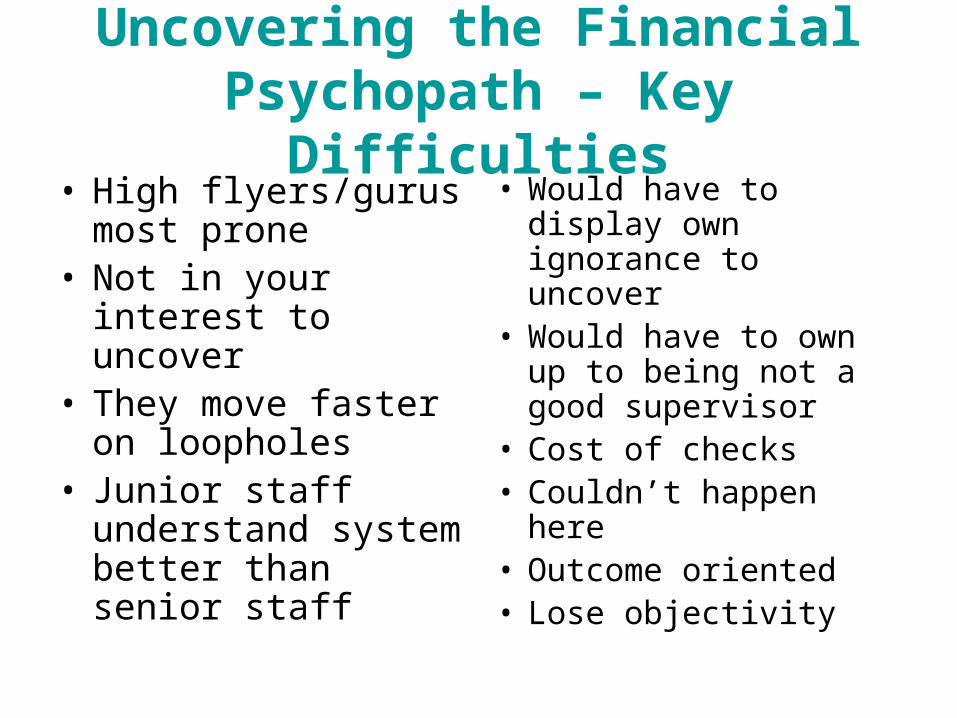

Uncovering the Financial Psychopath – Key Difficulties

• High flyers/gurus most prone

• Not in your interest to uncover

• They move faster on loopholes

• Junior staff understand system better than senior staff

• Would have to display own ignorance to uncover

• Would have to own up to being not a good supervisor

• Cost of checks• Couldn’t happen here• Outcome oriented• Lose objectivity

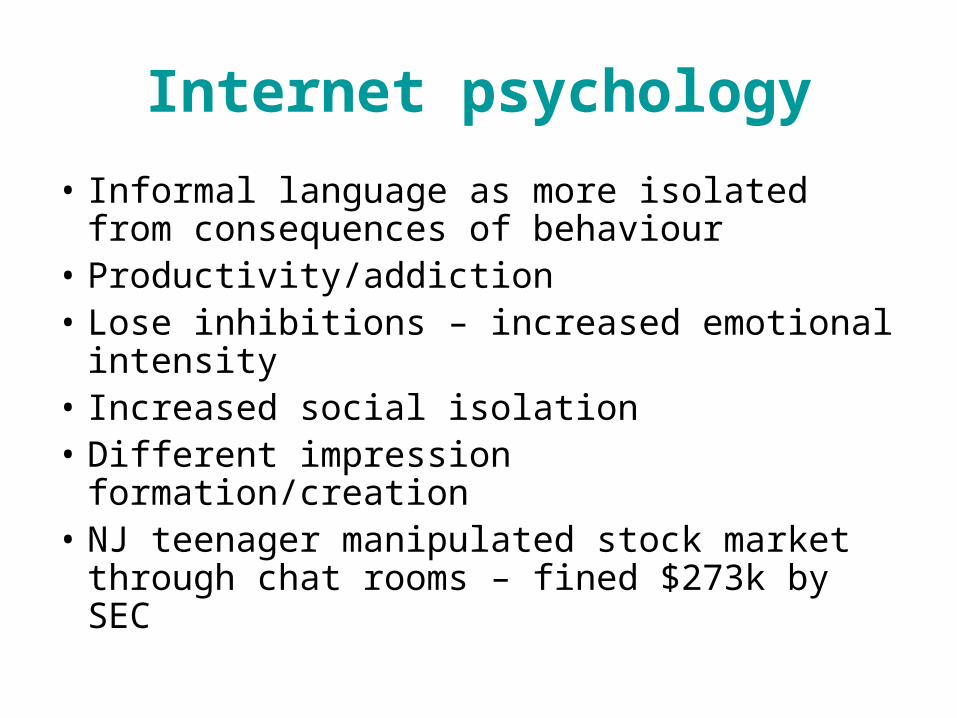

Internet psychology

• Informal language as more isolated from consequences of behaviour

• Productivity/addiction• Lose inhibitions – increased emotional

intensity• Increased social isolation• Different impression formation/creation• NJ teenager manipulated stock market

through chat rooms – fined $273k by SEC

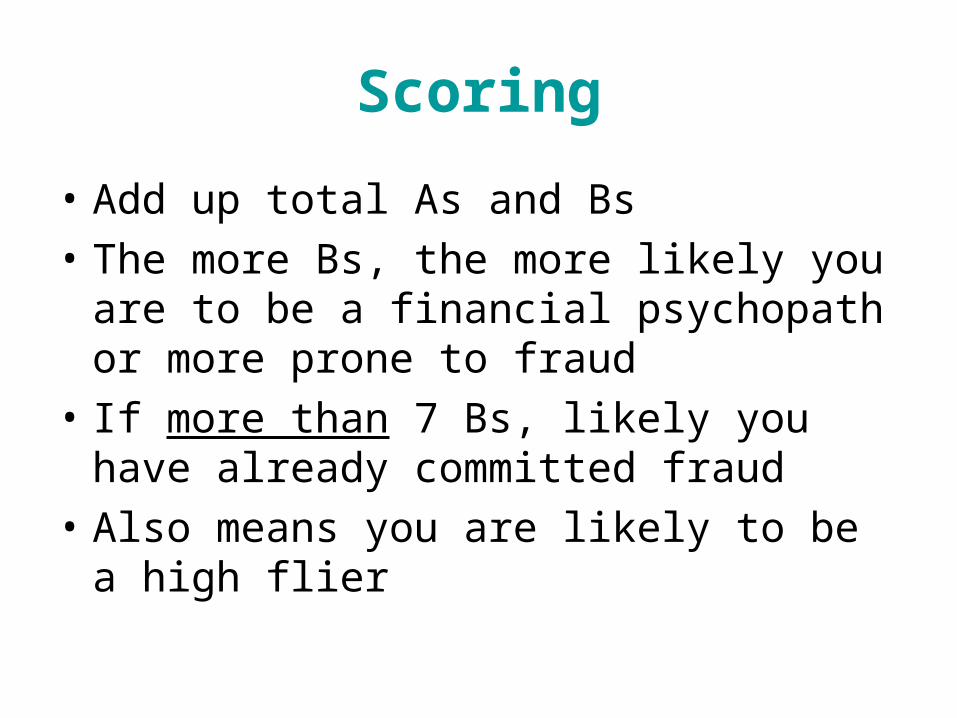

Scoring

• Add up total As and Bs

• The more Bs, the more likely you are to be a financial psychopath or more prone to fraud

• If more than 7 Bs, likely you have already committed fraud

• Also means you are likely to be a high flier

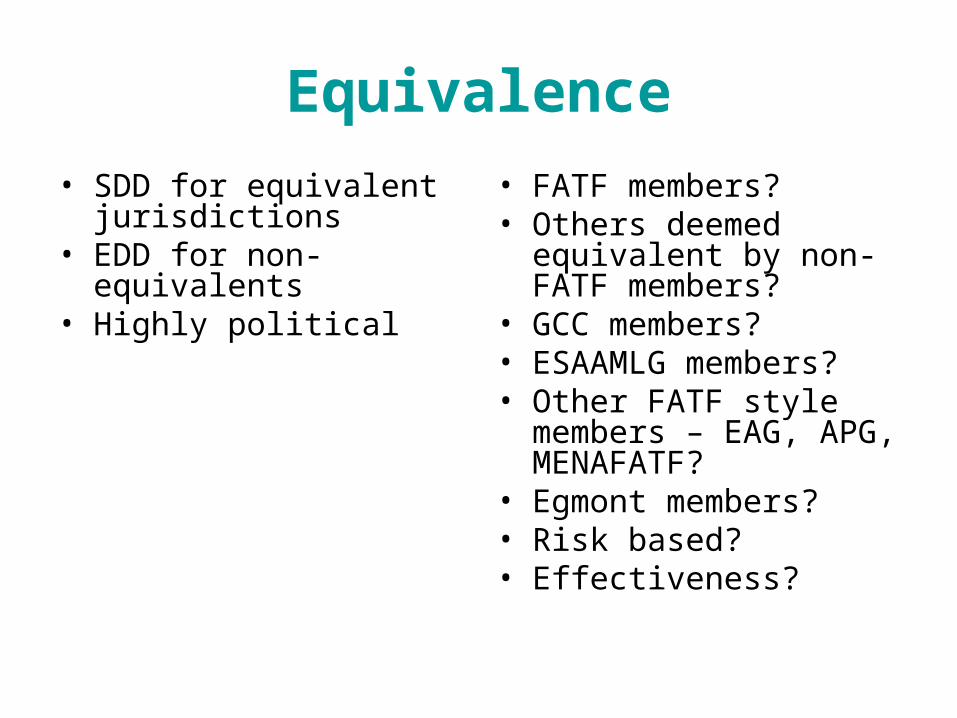

Equivalence

• SDD for equivalent jurisdictions

• EDD for non-equivalents• Highly political

• FATF members?• Others deemed

equivalent by non-FATF members?

• GCC members?• ESAAMLG members?• Other FATF style

members – EAG, APG, MENAFATF?

• Egmont members?• Risk based?• Effectiveness?

NF2F Tools

Specific• VISIT THE RISK • VTC/webcam?• EDD/lifestyle report• Limit service/level• Only if F2F a/c opening• Official documents• Information security• Encryption, comms choice, e

monitoring• Backup• Privacy policy

General• Risk assessment• Added documentation• Database/ Internet searches• Document certification• References/3rd parties• Credit checks• Sanctions checks• Regular KYC• Transaction monitoring IT• First payment through client

account at third bank• Disaster recovery plan

Conclusion

• Key Issues• International

Experience• Role of Psychology• Developing Solutions

Still Curious?

www.fmli.co.uk

Richard Parlour

Financial Markets Law International

© FMLI 2006