noel atkinson, cfa · florida is a highly attractive market dueto its demographics, list of...

TRANSCRIPT

Noel Atkinson, CFA 416-343-3352 | [email protected]

Bhargav Bandala, Associate | 416-343-4203

Like a Hurricane: Liberty Plans to Take Florida by Storm June 5, 2018

We are initiating coverage of Liberty Health Sciences with a Speculative Buy rating and a 12-month price target of $2.00 per share, or 14x FY2021e (Feb) EV/Adj. EBITDA discounted one year at 15%.

• Liberty is one of the first five licensed medical marijuanacultivation and dispensary companies in Florida to openretail stores. State licensing of new producers is highlyrestricted. Florida’s medical cannabis registry could reach500,000 patients by early 2021, generating statewideindustry retail sales worth over US$1 billion annually.

• Florida medical cannabis licensees can each operate atleast 25 retail dispensaries across the state. Liberty nowhas 4 locations open and expects to increase to 12 storesby the end of CY2018 and 20 by the end of CY2019, whichshould drive significant near-term revenue growth.

• Liberty recently acquired a large, advanced greenhousefacility in Gainesville, FL, which will allow the Company toachieve 14,600 kg/year of dried flower productioncapacity by early CY2019. Vertical integration andrelatively high expected market pricing for medicalcannabis in Florida should allow Liberty to enjoy strongreturn on invested capital.

• Leading Canadian cannabis LP Aphria has licensed its IPand trademarks to Liberty and there remains a strongrelationship between the two companies. Aphria’scultivation and marketing know-how should provide acompetitive advantage to Liberty in the Florida market.

• The pending acquisition of a provisional medical cannabislicensee in Massachusetts adds cultivation and severaldispensary locations and likely expansion into the imminentadult-use (rec) market in that state.

• Our target valuation multiple reflects a heightened level ofU.S. federal political and taxation risk for participants instate-regulated cannabis programs. Positive changes in thisregard would likely result in a sizable re-rating of the stock.

Liberty Health Sciences Inc. LHS-CSE: $0.87 Rating: Speculative Buy Target: $2.00

ValuationFiscal Year (Feb) FY18e FY19e FY20e FY21eRevenue (C$MM) $0.5 $15.6 $101.0 $175.9Adj. EBITDA (C$MM) ($3.1) ($2.8) $28.7 $65.1Adj. EBITDA Margin (577%) (18%) 28% 37%Diluted EPS ($0.11) ($0.04) $0.05 $0.08Price/Sales NMF 16.9x 2.6x 1.5xEV/Adj. EBITDA NEG NEG 8.7x 3.8xP/E NEG NEG 19.2x 10.4xStock DataPrice C$0.8752-Week Range C$0.69 - C$2.88Avg Daily Vol (3-Mo) 1,805,101Shares Basic / Diluted (pro forma, MM) 302.8 / 328.1Market Cap (pro forma, C$MM) $263.5Net Cash (pro forma, C$MM) $13.3Enterprise Value (pro forma, C$MM) $250.2Mgmt & Dir. Ownership (pro forma) 27%Fiscal Year End February

Company Profile

Liberty Health Sciences is a vertically-integrated medical cannabis producer and retailer in the state of Florida. It also intends to acquire a late-stage medical cannabis license applicant in Massachusetts. Liberty has licensed Aphria Inc.'s production know-how and brand/trademarks for its operations.

Liberty Health Sciences Inc. LHS-CSE

2 of 31 June 5, 2018

Table of Contents

Investment Thesis ........................................................................................................... 3

Investment Risks .......................................................................................................... 23

Board of Directors and Key Executives ................................................................... 25

Appendix A: Financial Statements ............................................................................ 29

Liberty Health Sciences Inc. LHS-CSE

June 5, 2018 3 of 31

Investment Thesis

We expect Liberty Health Sciences to become one of the leaders in the U.S. medical cannabis sector thanks to rapidly rising acceptance of medical cannabis within Florida’s large population having an early mover advantage on leasing retail dispensary locations, and the Company’s strategic partnership with leading Canadian cannabis Licensed Producer (LP) Aphria Inc. (TSX: APH, Buy, $25.25 PT).

In June 2017 Florida enacted a broad statewide medical cannabis program and since then the state’s medical cannabis patient registry has swelled to nearly 115,000 patients. Based on data from similar medical-only states (notably Arizona and Michigan) we believe Florida’s program could reach 545,000 patients by early 2021.

Florida is a highly attractive market due to its demographics, list of qualifying conditions, limited number of medical cannabis licensees, vertical integration of production and retail, and the ability to operate medical cannabis retail stores. There are only 13 licensees approved in Florida today, and Liberty is one of just 5 licensees that have opened retail dispensaries in the state. Liberty currently operates ~10% of all dispensaries in Florida market. While there will be more licensees in the future, we anticipate Liberty and the few other early, well-funded and capable entrants will capture the best dispensary locations in larger urban areas and dominate the Florida market.

The Company has fully-funded plans to ramp production capacity from ~1,600 kg/year of dried flower currently to nearly 15,000 kg/year by early CY2019. However, only oil and other extracted products are allowed for sale in Florida and typically generate higher average prices than dried flower. Aphria’s know-how and Florida’s warm climate should allow Liberty to become one of the lowest-cost producers in the state. In FY2021 (February) we expect Liberty to have a 8% patient market share in Florida across a network of 24 dispensaries, along with wholesaling of its products to Florida licensees in non-competing locations. Moreover, we expect Liberty to be highly capital-efficient. After the recent acquisition of an advanced greenhouse facility in Gainesville, FL, we believe Liberty likely only needs to spend about C$22.5 million to retrofit the Gainesville site to reach total production capacity of ~US$230 million of annual production capacity and complete the fit-out of a 24-store retail portfolio.

Liberty is also expanding into the attractive Massachusetts market through the purchase of a provisional medical producer licensee and we expect the Company to leverage its experience in Florida to capture retail and wholesale sales in the largest adult-use/medical state market on the U.S. East Coast.

We believe Liberty represents a very appealing investment opportunity for investors that can accept an elevated level of investment risk in order to have high-quality exposure to the rapidly-expanding U.S. cannabis sector. Our target valuation reflects discounts for political risks relating to the U.S. cannabis sector and a U.S. federal income tax code that causes elevated tax rates for cannabis producers and retailers. Positive shifts on these fronts could provide substantial upside torque to our valuation.

One of First 5 Medical Cannabis Production/Retail Licensees in Florida to Launch Retail Dispensary Network

Liberty was co-founded in 2017 with initial investors including Aphria and Serruya Private Equity (which owns and operates several international retail and quick-service food chains). The Company’s mission is to leverage Aphria’s world-class cannabis cultivation, processing and patient acquisition IP in highly-populated U.S. states where state-sanctioned medical cannabis programs are in place and there are sharp restrictions on the number of producer/retailer licenses.

Liberty Health Sciences Inc. LHS-CSE

4 of 31 June 5, 2018

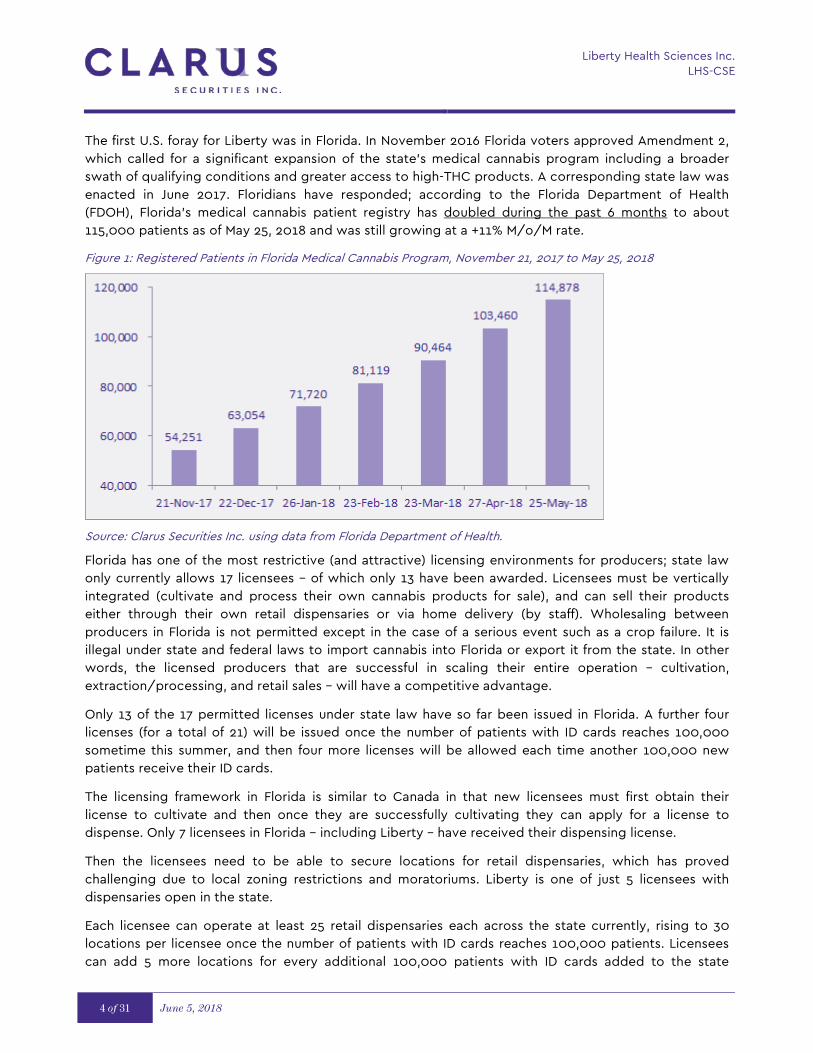

The first U.S. foray for Liberty was in Florida. In November 2016 Florida voters approved Amendment 2, which called for a significant expansion of the state’s medical cannabis program including a broader swath of qualifying conditions and greater access to high-THC products. A corresponding state law was enacted in June 2017. Floridians have responded; according to the Florida Department of Health (FDOH), Florida’s medical cannabis patient registry has doubled during the past 6 months to about 115,000 patients as of May 25, 2018 and was still growing at a +11% M/o/M rate.

Figure 1: Registered Patients in Florida Medical Cannabis Program, November 21, 2017 to May 25, 2018

Source: Clarus Securities Inc. using data from Florida Department of Health.

Florida has one of the most restrictive (and attractive) licensing environments for producers; state law only currently allows 17 licensees – of which only 13 have been awarded. Licensees must be vertically integrated (cultivate and process their own cannabis products for sale), and can sell their products either through their own retail dispensaries or via home delivery (by staff). Wholesaling between producers in Florida is not permitted except in the case of a serious event such as a crop failure. It is illegal under state and federal laws to import cannabis into Florida or export it from the state. In other words, the licensed producers that are successful in scaling their entire operation – cultivation, extraction/processing, and retail sales – will have a competitive advantage.

Only 13 of the 17 permitted licenses under state law have so far been issued in Florida. A further four licenses (for a total of 21) will be issued once the number of patients with ID cards reaches 100,000 sometime this summer, and then four more licenses will be allowed each time another 100,000 new patients receive their ID cards.

The licensing framework in Florida is similar to Canada in that new licensees must first obtain their license to cultivate and then once they are successfully cultivating they can apply for a license to dispense. Only 7 licensees in Florida – including Liberty – have received their dispensing license.

Then the licensees need to be able to secure locations for retail dispensaries, which has proved challenging due to local zoning restrictions and moratoriums. Liberty is one of just 5 licensees with dispensaries open in the state.

Each licensee can operate at least 25 retail dispensaries each across the state currently, rising to 30 locations per licensee once the number of patients with ID cards reaches 100,000 patients. Licensees can add 5 more locations for every additional 100,000 patients with ID cards added to the state

Liberty Health Sciences Inc. LHS-CSE

June 5, 2018 5 of 31

registry. However the dispensary cap sunsets in April 2020; thereafter licensees can each have unlimited numbers of dispensaries. However there will continue to be limits on the number of licensees.

Liberty has 4 stores open, which is more than 10% of the entire Florida dispensary roster. Liberty’s first dispensary opened in January 2018 in Summerfield (near Orlando and close to one of the largest retirement communities in the U.S.), followed by one in St. Petersburg in April, and two (Tampa and Port St. Lucie) in May. We understand the Tampa store is within a private hospital that sees 15,000 patients per week. We understand Liberty has signed leases for future locations in Fort Lauderdale, Miami, Jacksonville and Palm Harbor. Liberty plans to have 12 stores open by the end of CY2018 and 20 by the end of CY2019, and we project that the Florida portfolio will stabilize at 24 locations by the end of CY2020. Some of the dispensaries will also serve as distribution hubs for local home delivery.

Figure 2: Existing Liberty Retail Store Locations and Leased Sites for Future Expansion

Source: Clarus Securities Inc. using data from corporate filings.

Figure 3: Florida Medical Cannabis Program – Statewide License and Retail Store Limit Timeline

Source: Clarus Securities Inc. using data from State of Florida (Chapter 381.986, Florida Statutes) and press reports.

Liberty Health Sciences Inc. LHS-CSE

6 of 31 June 5, 2018

The ability to build a state-wide store network should allow Liberty and other early licensees to build brand awareness and capture the most attractive locations. Many cities and counties in Florida are restricting the number of dispensaries in their jurisdictions or outlawing them altogether. We expect that these local zoning restrictions will provide an effective cap on the number of dispensaries – especially in the most attractive urban markets. Later licensees will likely have a much more difficult time obtaining attractive dispensary locations and will have to come up the learning curve on cultivation and retailing while the earlier licensees pursue new innovations and product differentiations (such as Liberty’s recent licensing of topicals and edibles from companies in other states).

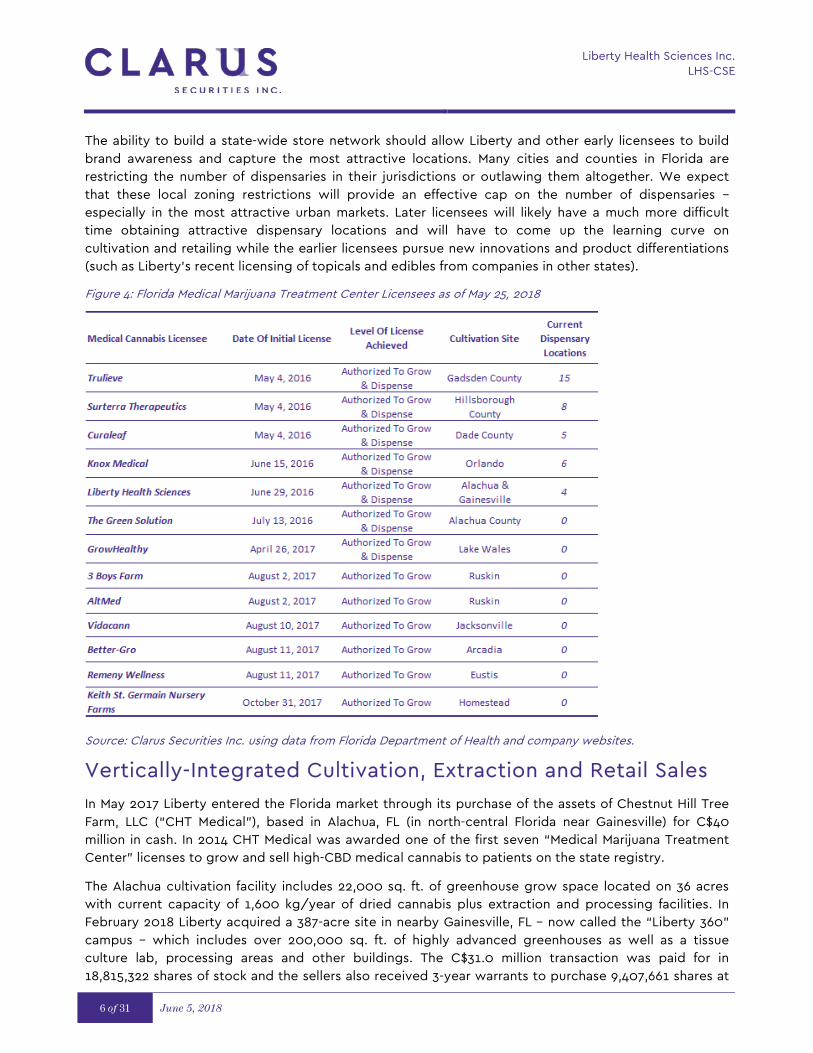

Figure 4: Florida Medical Marijuana Treatment Center Licensees as of May 25, 2018

Source: Clarus Securities Inc. using data from Florida Department of Health and company websites.

Vertically-Integrated Cultivation, Extraction and Retail Sales

In May 2017 Liberty entered the Florida market through its purchase of the assets of Chestnut Hill Tree Farm, LLC (“CHT Medical”), based in Alachua, FL (in north-central Florida near Gainesville) for C$40 million in cash. In 2014 CHT Medical was awarded one of the first seven “Medical Marijuana Treatment Center” licenses to grow and sell high-CBD medical cannabis to patients on the state registry.

The Alachua cultivation facility includes 22,000 sq. ft. of greenhouse grow space located on 36 acres with current capacity of 1,600 kg/year of dried cannabis plus extraction and processing facilities. In February 2018 Liberty acquired a 387-acre site in nearby Gainesville, FL – now called the “Liberty 360” campus – which includes over 200,000 sq. ft. of highly advanced greenhouses as well as a tissue culture lab, processing areas and other buildings. The C$31.0 million transaction was paid for in 18,815,322 shares of stock and the sellers also received 3-year warrants to purchase 9,407,661 shares at

Liberty Health Sciences Inc. LHS-CSE

June 5, 2018 7 of 31

C$2.07 per share. Liberty received the seller’s C$17.3 million of net cash on its balance sheet, which made the net purchase price C$13.7 million excluding the implied value of the warrants issued. The Company believes the acquisition will bring total capacity to 13,000 kg/year of dried flower once a fully-funded US$14 million (~C$18 million) retrofit for cannabis cultivation is completed this year.

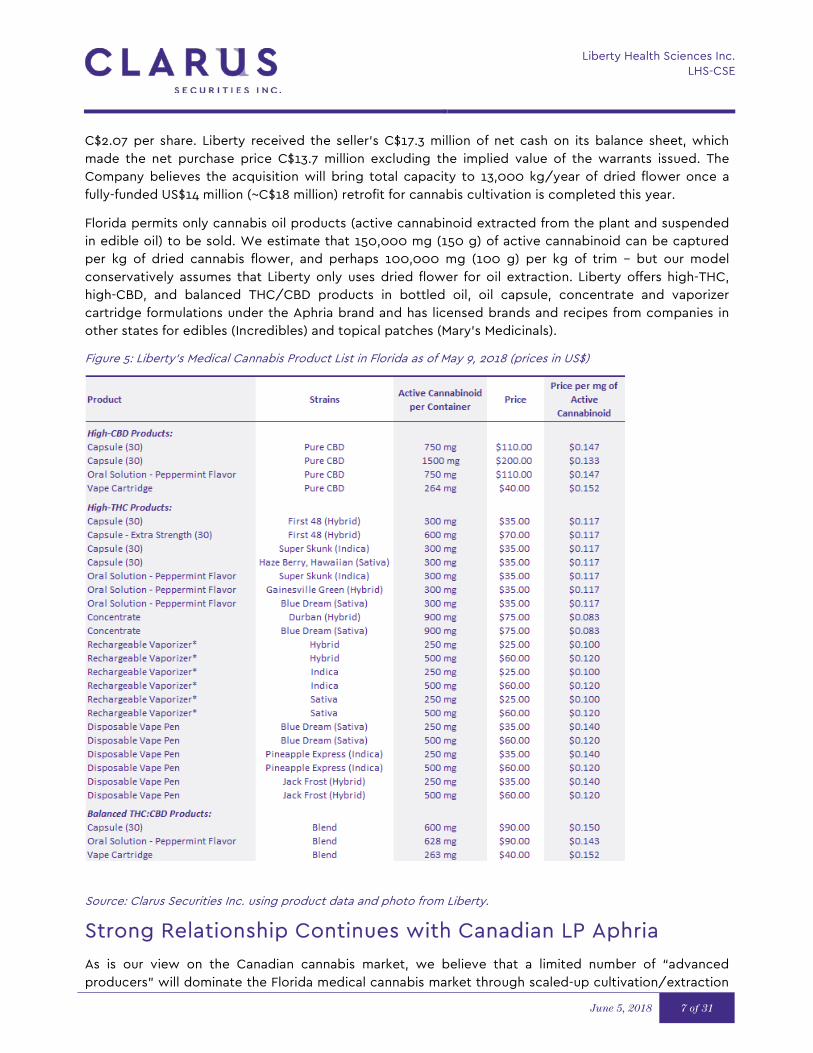

Florida permits only cannabis oil products (active cannabinoid extracted from the plant and suspended in edible oil) to be sold. We estimate that 150,000 mg (150 g) of active cannabinoid can be captured per kg of dried cannabis flower, and perhaps 100,000 mg (100 g) per kg of trim – but our model conservatively assumes that Liberty only uses dried flower for oil extraction. Liberty offers high-THC, high-CBD, and balanced THC/CBD products in bottled oil, oil capsule, concentrate and vaporizer cartridge formulations under the Aphria brand and has licensed brands and recipes from companies in other states for edibles (Incredibles) and topical patches (Mary’s Medicinals).

Figure 5: Liberty’s Medical Cannabis Product List in Florida as of May 9, 2018 (prices in US$)

Source: Clarus Securities Inc. using product data and photo from Liberty.

Strong Relationship Continues with Canadian LP Aphria

As is our view on the Canadian cannabis market, we believe that a limited number of “advanced producers” will dominate the Florida medical cannabis market through scaled-up cultivation/extraction

Liberty Health Sciences Inc. LHS-CSE

8 of 31 June 5, 2018

facilities, ability to achieve consistent harvests, developing new products, and consistently innovating to increase yield and reduce production cost. In the Florida market this also means building a portfolio of attractive retail stores in top locations. We believe many licensees in Florida will struggle to ramp production – especially as they will have to grow under food-grade conditions. This should limit new supply into the market and also keep the average cost of production relatively high. In turn, we expect limited price competition in the initial years of the program. Our price analysis of Surterra’s and Trulieve’s product lists suggests that Liberty’s pricing is highly competitive.

Leading Canadian LP Aphria formed Liberty as a vehicle to leverage its expertise in greenhouse cultivation, oil extraction and patient recruitment in the most attractive medical cannabis programs in the U.S. The companies maintain a strong relationship, with Vic Neufeld and John Cervini of Aphria on Liberty’s board and Aphria director and co-founder Cole Cacciavillani (who together with Mr. Cervini oversees Aphria’s production operations) is a strategic advisor to Liberty on cultivation operations. Aphria initially licensed its trademarks and production know-how to Liberty in return for 64.1 million Liberty shares, an annual license fee of $10,000, and a royalty of 3% of revenue of all Aphria-branded products. The royalty agreement is in place but is not being collected or accrued until the TSX permits U.S. cannabis-related revenue for TSX-listed firms.

In May 2018 Aphria furthered its relationship with Liberty by licensing its Solei brands and logo to Liberty for use in Florida and (once licensed) in Massachusetts. Solei is Aphria’s first rec-focused brand in Canada, and we understand Liberty will attempt to closely replicate the Solei products for its Florida patients. This should meaningfully boost Liberty’s product range. Aphria will in turn have a good product test bed, and we understand this is covered under Aphria’s IP royalty agreement with Liberty.

Figure 6: Aphria-Branded Medical Cannabis Products Sold by Liberty

Source: Liberty.

Between shares from a C$25 million equity investment in Liberty and the shares received under the licensing agreements, Aphria originally owned a ~38% stake in Liberty (106.9 million shares). While the TSX initially allowed Aphria to have investments in U.S. state-regulated medical cannabis companies, the TSX flip-flopped on this position in late 2017. Aphria announced in February 2018 it would divest its Liberty stake to members of the Serruya family and an affiliate of Delavaco Capital. The sale will occur in tranches through mid-2020 as the applicable Liberty shares exit mandated escrow.

Liberty Health Sciences Inc. LHS-CSE

June 5, 2018 9 of 31

While Aphria may be selling its stake in Liberty, we think the relationship remains very strong; it is telling that Aphria continues to boost its product licensing agreements with Liberty and its officers and directors continue to be part of Liberty.

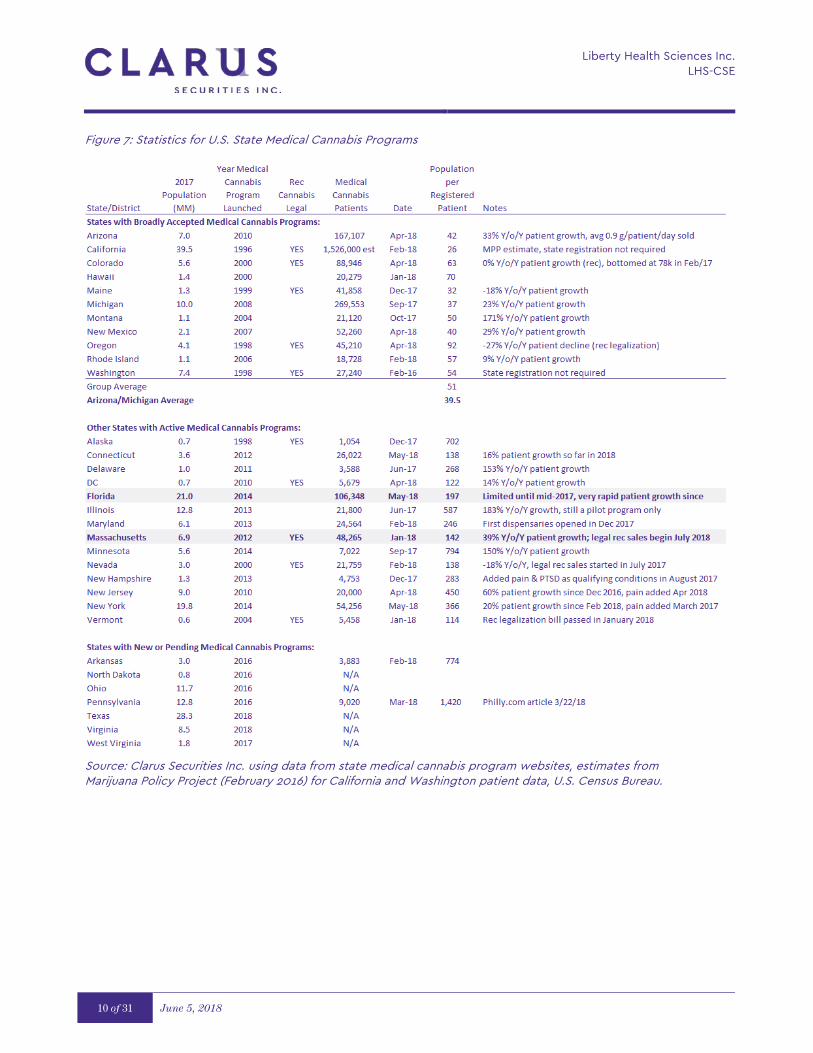

By 2021 Florida Medical Cannabis Market Could Reach 545,000 Patients with Annual Retail Sales over US$1.2 Billion

Florida is the fourth most populous U.S. state. Of its 21 million residents, over 13 million live in four large metro areas (Miami/Fort Lauderdale, Orlando, Jacksonville and Tampa/St. Petersburg). Thirteen other cities have at least 100,000 residents. Florida residents – including seasonal residents – can obtain a medical cannabis prescription if they have a qualifying condition such as cancer, epilepsy, glaucoma, HIV/AIDS, PTSD, ALS, Crohn’s, Parkinson’s, and multiple sclerosis, along with medical conditions “of the same kind or class”, any terminal condition (<1 year to live) and chronic nonmalignant pain from or originally caused by one of the qualifying conditions.

Thirty-one states and D.C. have created medical cannabis programs. We believe Arizona and Michigan are the closest comparables for what Florida’s medical cannabis program could look like in 3-5 years; they are large in area and population, are medical-only (no rec cannabis), and have broad lists of qualifying conditions. Michigan and Arizona together have an average of 1 patient per ~40 residents; applying that rate to Florida’s projected 21.5 million population in 2020 points to a market of about 545,000 patients (double the size of the entire Canadian ACMPR patient registry today).

By mid-2020 we estimate the Florida medical cannabis program to be selling an average of 60 mg/day/patient (“patient-day”) of active cannabinoid, equivalent to 0.4 grams/day of moderate-potency dried flower. This is similar to demand in the Canadian market but may prove conservative since comparable state Arizona realized average sales of 0.9 g of cannabis per patient-day in April 2018 (estimated ~135 mg/patient-day of active cannabinoid).

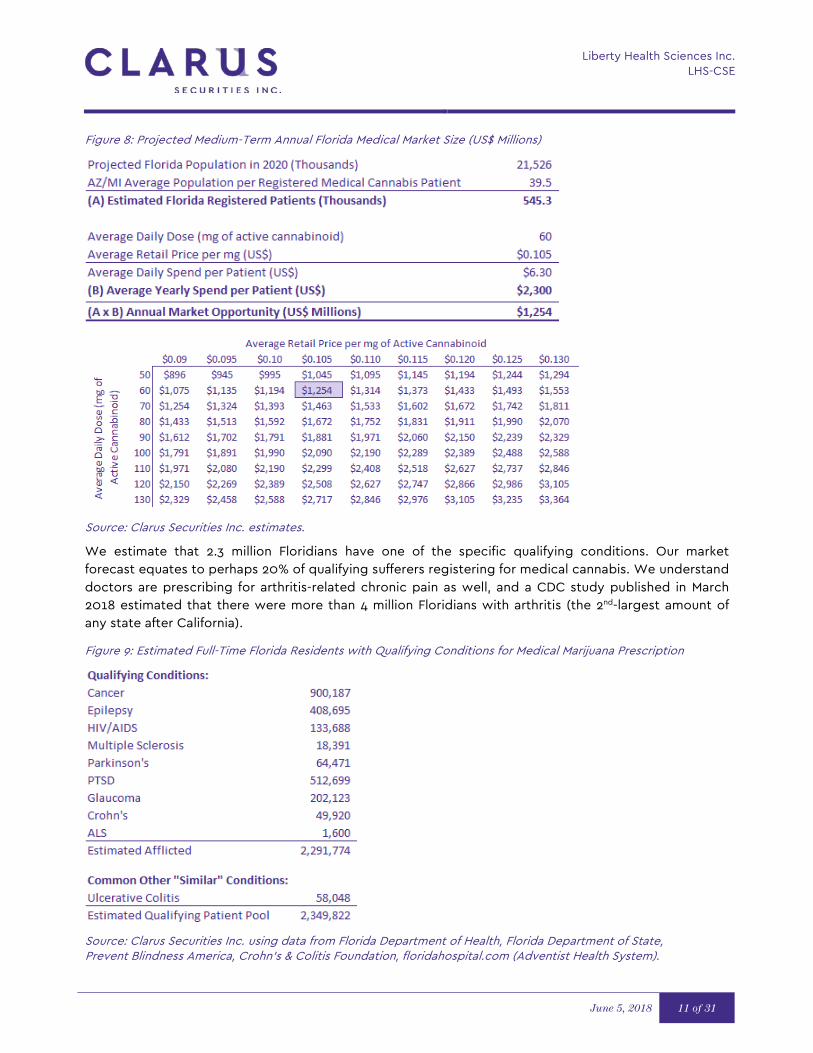

At a projected medium-term (late 2020) average retail price of US$0.105 per mg of active cannabinoid, we expect Florida’s medical cannabis program to achieve retail sales of US$2,300 per patient and statewide revenues exceeding US$1.2 billion (~C$1.6 billion) annually.

Liberty Health Sciences Inc. LHS-CSE

10 of 31 June 5, 2018

Figure 7: Statistics for U.S. State Medical Cannabis Programs

Source: Clarus Securities Inc. using data from state medical cannabis program websites, estimates from Marijuana Policy Project (February 2016) for California and Washington patient data, U.S. Census Bureau.

Liberty Health Sciences Inc. LHS-CSE

June 5, 2018 11 of 31

Figure 8: Projected Medium-Term Annual Florida Medical Market Size (US$ Millions)

Source: Clarus Securities Inc. estimates.

We estimate that 2.3 million Floridians have one of the specific qualifying conditions. Our market forecast equates to perhaps 20% of qualifying sufferers registering for medical cannabis. We understand doctors are prescribing for arthritis-related chronic pain as well, and a CDC study published in March 2018 estimated that there were more than 4 million Floridians with arthritis (the 2nd-largest amount of any state after California).

Figure 9: Estimated Full-Time Florida Residents with Qualifying Conditions for Medical Marijuana Prescription

Source: Clarus Securities Inc. using data from Florida Department of Health, Florida Department of State, Prevent Blindness America, Crohn’s & Colitis Foundation, floridahospital.com (Adventist Health System).

Liberty Health Sciences Inc. LHS-CSE

12 of 31 June 5, 2018

Florida Market Should Sustain Strong Retail Pricing Through Our Forecast Period

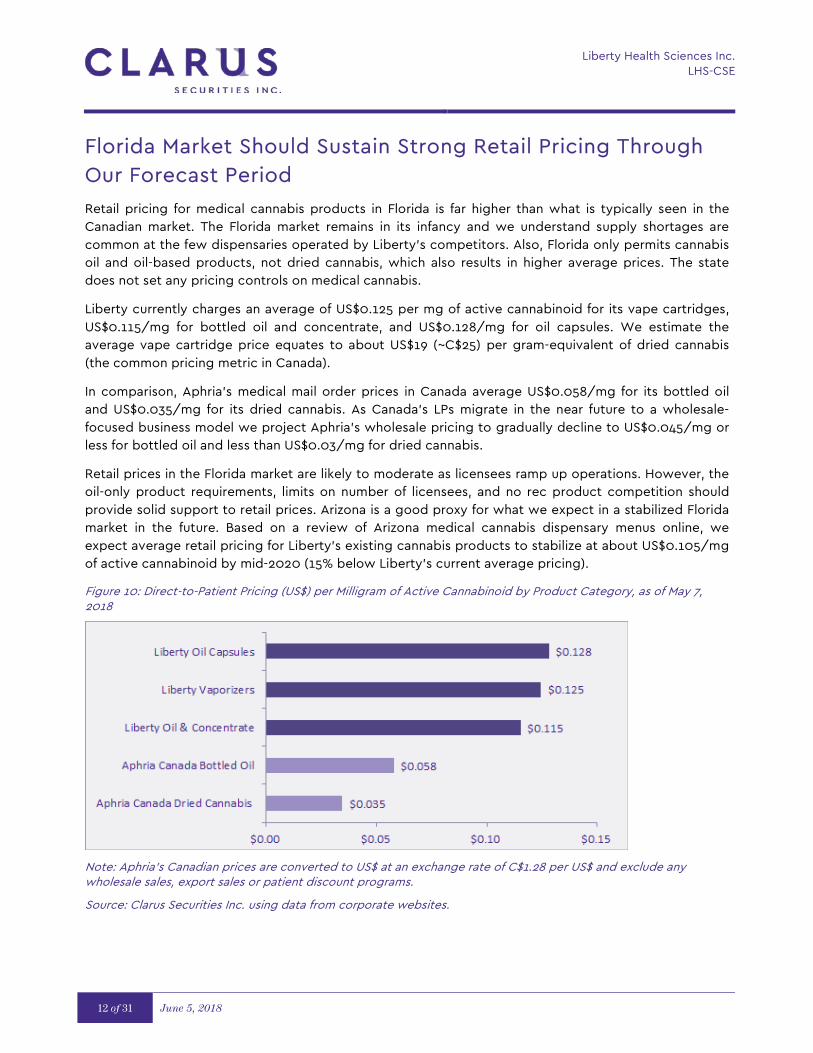

Retail pricing for medical cannabis products in Florida is far higher than what is typically seen in the Canadian market. The Florida market remains in its infancy and we understand supply shortages are common at the few dispensaries operated by Liberty’s competitors. Also, Florida only permits cannabis oil and oil-based products, not dried cannabis, which also results in higher average prices. The state does not set any pricing controls on medical cannabis.

Liberty currently charges an average of US$0.125 per mg of active cannabinoid for its vape cartridges, US$0.115/mg for bottled oil and concentrate, and US$0.128/mg for oil capsules. We estimate the average vape cartridge price equates to about US$19 (~C$25) per gram-equivalent of dried cannabis (the common pricing metric in Canada).

In comparison, Aphria’s medical mail order prices in Canada average US$0.058/mg for its bottled oil and US$0.035/mg for its dried cannabis. As Canada’s LPs migrate in the near future to a wholesale-focused business model we project Aphria’s wholesale pricing to gradually decline to US$0.045/mg or less for bottled oil and less than US$0.03/mg for dried cannabis.

Retail prices in the Florida market are likely to moderate as licensees ramp up operations. However, the oil-only product requirements, limits on number of licensees, and no rec product competition should provide solid support to retail prices. Arizona is a good proxy for what we expect in a stabilized Florida market in the future. Based on a review of Arizona medical cannabis dispensary menus online, we expect average retail pricing for Liberty’s existing cannabis products to stabilize at about US$0.105/mg of active cannabinoid by mid-2020 (15% below Liberty’s current average pricing).

Figure 10: Direct-to-Patient Pricing (US$) per Milligram of Active Cannabinoid by Product Category, as of May 7, 2018

Note: Aphria’s Canadian prices are converted to US$ at an exchange rate of C$1.28 per US$ and exclude any wholesale sales, export sales or patient discount programs.

Source: Clarus Securities Inc. using data from corporate websites.

Liberty Health Sciences Inc. LHS-CSE

June 5, 2018 13 of 31

Expecting Liberty to Capture 8% Share of Florida Market and (Eventually) Wholesale to Other Licensees

We forecast that Liberty will eventually open 24 stores across Florida and capture a 8% market share of Florida medical cannabis patients, with average purchase size of about 60 mg of cannabinoid (or about 0.4 gram-equivalent) per patient per day. We expect average sales to rise over time to US$3.9 million/store (C$5.1 million/store) by early CY2021 with about 1,700 active patients per store. The entire Florida market currently has an average of over 3,000 registered patients per store. In comparison, as of late 2016 Arizona had a similarly-sized patient registry as Florida does today with nearly three times as many medical cannabis dispensaries open (99 versus 38), and median revenue per Arizona dispensary that year was still about US$3.6 million according to Marijuana Business Daily. Florida’s licensing model could ultimately result in more dispensaries than Arizona (resulting in fewer average patients per store) but we expect well-situated stores in the larger cities (where Liberty is focusing their retail portfolio) to take up the lion’s share of the statewide sales.

Cannabis wholesaling is currently quite restricted in Florida; up to 30% of a Florida licensee’s production can be sold wholesale to another licensee but only in the event of a crop failure and requires approval from the state regulator. However, the medical cannabis producers in Florida are lobbying the state to ease those wholesaling restrictions on wholesaling between Florida producers. Consequently we assume that the wholesaling restrictions will be eased and that Liberty will begin to sell wholesale to non-competing licensees (i.e. store portfolio not geographically competing with Liberty’s) in late CY2019. Federal law prohibits sales (wholesale and retail) of cannabis across state lines.

Our forecast assumes that all retail sales are done in Liberty’s stores. However, licensees are also permitted to provide home delivery using corporate vehicles. We expect some of Liberty’s retail stores to serve as home delivery hubs for the local areas, which could meaningfully increase effective per-store revenue beyond our forecast.

Our forecast assumes wholesale shipments are 0% of total shipments in FY2019 (February), 22% in FY2020 and 43% in FY2021. We conservatively model that Liberty’s total shipment volume will average 31% of production capacity in FY2020 (February), rising to 64% in FY2021.

Liberty Health Sciences Inc. LHS-CSE

14 of 31 June 5, 2018

Figure 11: Forecast Annualized Production Capacity and Shipment Volume Run-Rate for Liberty in Florida (in kg/year of active cannabinoid)

Source: Clarus Securities Inc. estimates using data from corporate websites.

Federal Regulatory/Legislative Environment Seems to Be Rapidly Improving for State-Regulated Cannabis Programs

Cannabis and cannabis oil extracts (such as CBD) are classified by the federal U.S. Drug Enforcement Administration (DEA) as Schedule 1 drugs (as is heroin) under the U.S. Controlled Substances Act. Schedule 1 drugs are considered to have no currently accepted medical use in treatment and carry a high potential for abuse. Consequently Schedule 1 drugs are illegal to produce, distribute, dispense and possess under U.S. federal law.

Even though cannabis is federally illegal, 31 states and D.C. have implemented laws to legalize medical and/or recreational cannabis use. A non-partisan Quinnipiac University national poll released in April 2018 (n = 1,193, results +/- 3.4%) found that:

• 93% of Americans were in favor of allowing adults to legally use cannabis for medical purposes if their doctor prescribes it;

• 74% were in favor of implementing a federal bill to protect participants in state-regulated medical or recreational cannabis from federal prosecution;

• 61% said that cannabis was not a “gateway drug” that leads to abuse of hard drugs;

• 43% of respondents had used cannabis recreationally (63% of 18-34 year olds, 50% of 35-49 year olds, 46% of 50-64s, and 25% of those ages 65+); and

• A record 63% were in favor of the U.S. federally legalizing cannabis (including 41% of self-identified Republican respondents, 75% of Democrats and 67% of independents).

Florida implemented its first medical cannabis law in 2014 and expanded the program in 2017. Florida’s medical cannabis law protects program participants from prosecution under state law, but it does not protect them against federal prosecution should the federal government choose to act on federal law. While U.S. Attorney General Jeff Sessions has hardened the federal Justice Department’s (DOJ) stance on cannabis (particularly giving federal prosecutors more free reign to pursue state-program activity tied

Liberty Health Sciences Inc. LHS-CSE

June 5, 2018 15 of 31

to gangs or cross-border shipments, the legislative and regulatory environment seems to be improving rapidly for state-program participants such as Liberty.

Congress used the FY2018 federal budget to renew the one-year moratorium (through September 30, 2018) on DOJ funds from being used to prosecute medical cannabis program participants who are complying with state laws. This congressional protection of state medical cannabis programs has been renewed annually since FY2015.

Republican Senator Cory Gardner of Colorado had been blocking President Trump’s DOJ nominees since Attorney General Sessions hardened the DOJ’s stance on cannabis. In mid-April 2018, it was reported that President Trump had agreed to support a federal bill that Gardner intended to introduce that would protect state medical and recreational cannabis programs as a states-rights issue. It has been subsequently reported that Massachusetts Democratic Senator Elizabeth Warren would co-sponsor the bill with Gardner. If that bill ultimately materializes and is enacted, then the federal government would be effectively decriminalizing cannabis use so long as the participants were following state law.

Another positive for the cannabis industry is that Senate Majority Leader Mitch McConnell of Kentucky has introduced the Hemp Farming Act bill, which would re-establish hemp as an agricultural commodity and legalize the use and sale of CBD extracted from the hemp plant.

Banking and taxation have also been challenges to state-legal cannabis program participants. FinCEN – a federal banking regulator – issued a memo in January 2018 that identified increased legal risks to banks providing services to cannabis industry participants in the wake of the hardening of the DOJ stance on cannabis. However, a new federal bill called the SAFE Banking Act has been introduced in Congress with at least 15 co-sponsors and would allow U.S. banks and payment processors to freely engage with cannabis-related businesses.

The tax issue is mainly related to Section 280E of the U.S. federal tax code (“Expenditures in connection with the illegal sale of drugs”) that places an unusually heavy income tax burden on U.S. marijuana retailers. The only tax deduction that U.S. marijuana retailers can claim is for the direct purchase costs of the marijuana products sold (i.e. the costs of goods sold). The retail business unit cannot deduct rent, store labor, utilities, or other materials and supplies. Since the tax rate is applied to gross profit rather than pre-tax income, a marijuana retailer’s effective combined federal and state corporate tax rate can easily exceed 60% and smaller, less profitable retailers can even experience effective tax rates over 100% of pre-tax income.

A vertically-integrated producer/retailer such as Liberty should have a much better tax situation. The 280E tax code allows marijuana producers to deduct production and supervisory labor costs, rent, maintenance, utilities, quality control, and other production-related expenses as COGS. So long as Liberty uses GAAP accounting, it can also deduct depreciation charges, administrative labor costs related to production, and employee benefit costs. We understand that a sizable portion of a Liberty store will be considered “consultation area” (since Liberty calls them “cannabis education centers” rather than dispensaries) and the associated staff, rent and other costs for that space should not be captured under 280E tax rates.

We expect Liberty to begin paying federal income tax in FY2019, and our model anticipates the Company’s effective tax rate stabilizing at about 37% (versus 25.5% standard federal/state tax for a Florida-based business).

Liberty Health Sciences Inc. LHS-CSE

16 of 31 June 5, 2018

There is a House bill called The Small Business Tax Equity Act of 2017 that would repeal the 280E tax code for state-regulated cannabis companies and has seen intensive lobbying by the cannabis industry. There are more than 40 co-sponsors of the bill, but it has been stuck in committee since March 2017.

Efforts at the state level to expand qualifying conditions for medical cannabis programs or to introduce new medical cannabis programs have happened over the past year in several states including Florida, New York, Ohio, Pennsylvania, Texas and Virginia. California legalized adult-use recreational cannabis at the start of 2018, and Massachusetts will be doing so on July 1, 2018. New Jersey’s governor has recently voiced his support for legalizing adult-use rec cannabis in his state and it appears that Michigan voters will vote on legalization during the November elections.

Pending Massachusetts Acquisition Would Give Entry to the Largest East Coast Rec/Medical Cannabis Market

On March 27, 2018 Liberty announced the pending acquisition of a 75% stake of William Noyes Webster Foundation, Inc. (WNWF) for US$16 million (C$20.5 million) in cash. WNWF has a provisional certificate to operate as a registered medical dispensary (RMD) with a ~2,500 kg/year cultivation site in Plymouth, MA (south of Boston) and a dispensary site in Dennis, MA (on Cape Cod). Liberty anticipates that it could be in a position to request a full registered medical dispensary license for the Dennis site by the end of 2018.

In addition, WNWF is looking at additional medical dispensary sites in Dartmouth, MA (near the Rhode Island border) and Cambridge, MA (a suburb of Boston).

There are about 6.9 million people living in the state, or about 1/3 the size of Florida, and a great majority live in the eastern part of the state around Boston. Massachusetts voters approved a state medical cannabis program in 2012 but the first dispensary only opened in mid-2015. The state has limited the registry to those afflicted with a “debilitating condition that causes weakness, intractable pain, nausea, wasting, or impaired strength or ability so that one or more of a patient’s major life activities is substantially limited.” Both flower and extracted products can be sold in Massachusetts.

There were 49,524 active medical cannabis patients on the Massachusetts registry as of April 30, 2018, and the roster has been growing at about 2,000 patients per month. Sales in April totaled about 0.6 g/day for all active patients on the registry and about 1 g/day for the actual number of patients served (30,424) in April. The Massachusetts program had 26 registered dispensaries approved to sell at the end of April, along with 13 that awaited final sales approval. There were also 99 dispensaries at the provisional certificate stage, which is where WNWF’s licensure process currently stands.

Adult-use (rec) cannabis retail sales are slated to begin in Massachusetts on July 1, 2018 and will be available to people 21 or older. Entities with registered medical dispensary licenses were the first to be able to apply for recreational licenses, and so those licensees will have the first adult-use stores open. Any medical dispensary also receiving an adult-use license must set aside 35% of their product for medical patients.

Liberty Health Sciences Inc. LHS-CSE

June 5, 2018 17 of 31

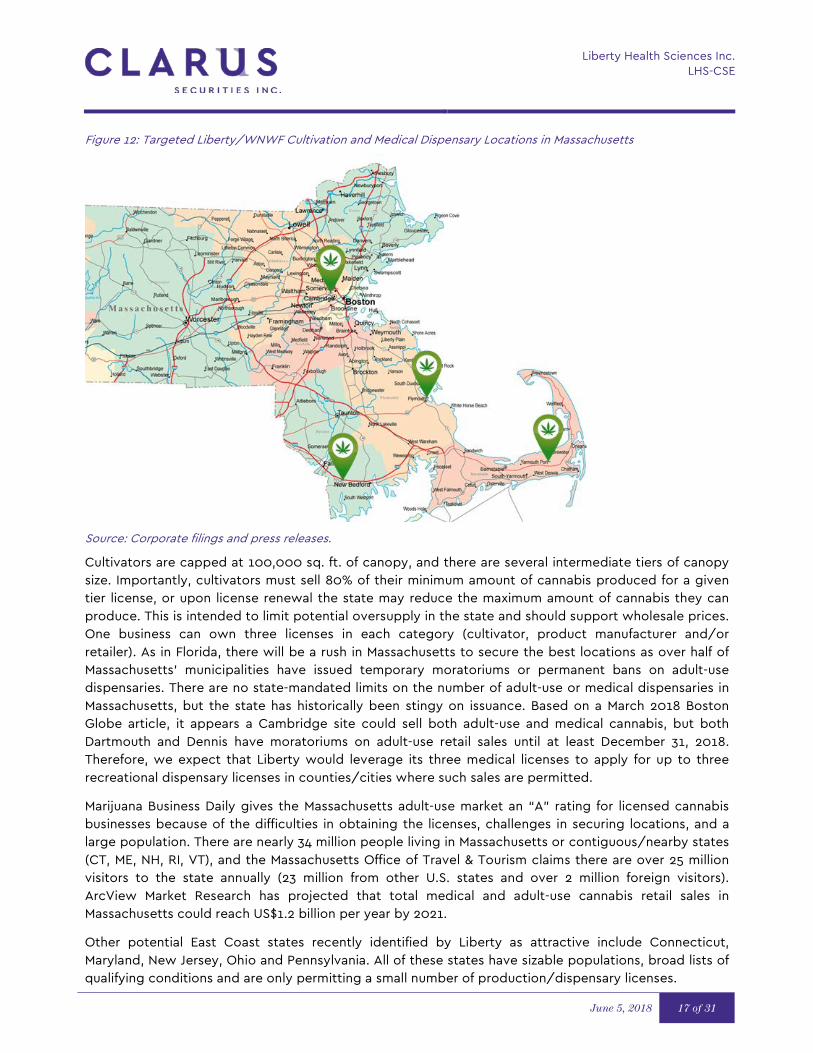

Figure 12: Targeted Liberty/WNWF Cultivation and Medical Dispensary Locations in Massachusetts

Source: Corporate filings and press releases.

Cultivators are capped at 100,000 sq. ft. of canopy, and there are several intermediate tiers of canopy size. Importantly, cultivators must sell 80% of their minimum amount of cannabis produced for a given tier license, or upon license renewal the state may reduce the maximum amount of cannabis they can produce. This is intended to limit potential oversupply in the state and should support wholesale prices. One business can own three licenses in each category (cultivator, product manufacturer and/or retailer). As in Florida, there will be a rush in Massachusetts to secure the best locations as over half of Massachusetts’ municipalities have issued temporary moratoriums or permanent bans on adult-use dispensaries. There are no state-mandated limits on the number of adult-use or medical dispensaries in Massachusetts, but the state has historically been stingy on issuance. Based on a March 2018 Boston Globe article, it appears a Cambridge site could sell both adult-use and medical cannabis, but both Dartmouth and Dennis have moratoriums on adult-use retail sales until at least December 31, 2018. Therefore, we expect that Liberty would leverage its three medical licenses to apply for up to three recreational dispensary licenses in counties/cities where such sales are permitted.

Marijuana Business Daily gives the Massachusetts adult-use market an “A” rating for licensed cannabis businesses because of the difficulties in obtaining the licenses, challenges in securing locations, and a large population. There are nearly 34 million people living in Massachusetts or contiguous/nearby states (CT, ME, NH, RI, VT), and the Massachusetts Office of Travel & Tourism claims there are over 25 million visitors to the state annually (23 million from other U.S. states and over 2 million foreign visitors). ArcView Market Research has projected that total medical and adult-use cannabis retail sales in Massachusetts could reach US$1.2 billion per year by 2021.

Other potential East Coast states recently identified by Liberty as attractive include Connecticut, Maryland, New Jersey, Ohio and Pennsylvania. All of these states have sizable populations, broad lists of qualifying conditions and are only permitting a small number of production/dispensary licenses.

Liberty Health Sciences Inc. LHS-CSE

18 of 31 June 5, 2018

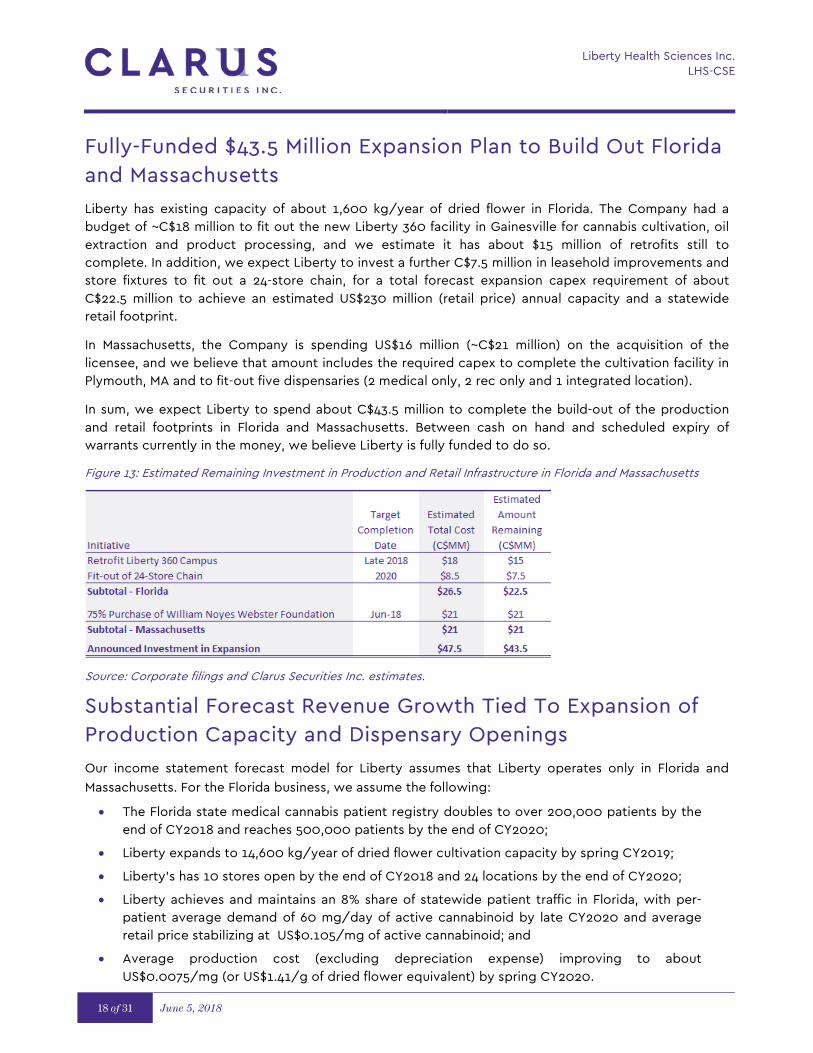

Fully-Funded $43.5 Million Expansion Plan to Build Out Florida and Massachusetts

Liberty has existing capacity of about 1,600 kg/year of dried flower in Florida. The Company had a budget of ~C$18 million to fit out the new Liberty 360 facility in Gainesville for cannabis cultivation, oil extraction and product processing, and we estimate it has about $15 million of retrofits still to complete. In addition, we expect Liberty to invest a further C$7.5 million in leasehold improvements and store fixtures to fit out a 24-store chain, for a total forecast expansion capex requirement of about C$22.5 million to achieve an estimated US$230 million (retail price) annual capacity and a statewide retail footprint.

In Massachusetts, the Company is spending US$16 million (~C$21 million) on the acquisition of the licensee, and we believe that amount includes the required capex to complete the cultivation facility in Plymouth, MA and to fit-out five dispensaries (2 medical only, 2 rec only and 1 integrated location).

In sum, we expect Liberty to spend about C$43.5 million to complete the build-out of the production and retail footprints in Florida and Massachusetts. Between cash on hand and scheduled expiry of warrants currently in the money, we believe Liberty is fully funded to do so.

Figure 13: Estimated Remaining Investment in Production and Retail Infrastructure in Florida and Massachusetts

Source: Corporate filings and Clarus Securities Inc. estimates.

Substantial Forecast Revenue Growth Tied To Expansion of Production Capacity and Dispensary Openings

Our income statement forecast model for Liberty assumes that Liberty operates only in Florida and

Massachusetts. For the Florida business, we assume the following:

• The Florida state medical cannabis patient registry doubles to over 200,000 patients by the end of CY2018 and reaches 500,000 patients by the end of CY2020;

• Liberty expands to 14,600 kg/year of dried flower cultivation capacity by spring CY2019;

• Liberty’s has 10 stores open by the end of CY2018 and 24 locations by the end of CY2020;

• Liberty achieves and maintains an 8% share of statewide patient traffic in Florida, with per-patient average demand of 60 mg/day of active cannabinoid by late CY2020 and average retail price stabilizing at US$0.105/mg of active cannabinoid; and

• Average production cost (excluding depreciation expense) improving to about US$0.0075/mg (or US$1.41/g of dried flower equivalent) by spring CY2020.

Liberty Health Sciences Inc. LHS-CSE

June 5, 2018 19 of 31

For the Massachusetts business we assume the following:

• Maximum capacity of 2,500 kg/year achieved in late CY2019;

• First dispensary opens in early CY2019, and grows to 3 medical dispensaries by summer 2019;

• One medical dispensary becomes licensed to sell adult-use cannabis, and two additional adult-use dispensaries are licensed (for a total of 5 stores in Massachusetts);

• Average retail price stabilizes at US$8.25/g by early CY2021;

• Each store averages US$3 million in annual revenue (~C$3.9 million) by early CY2021; and

• Average production cost declines to US$1.75/g (~C$2.25/g) by early CY2021.

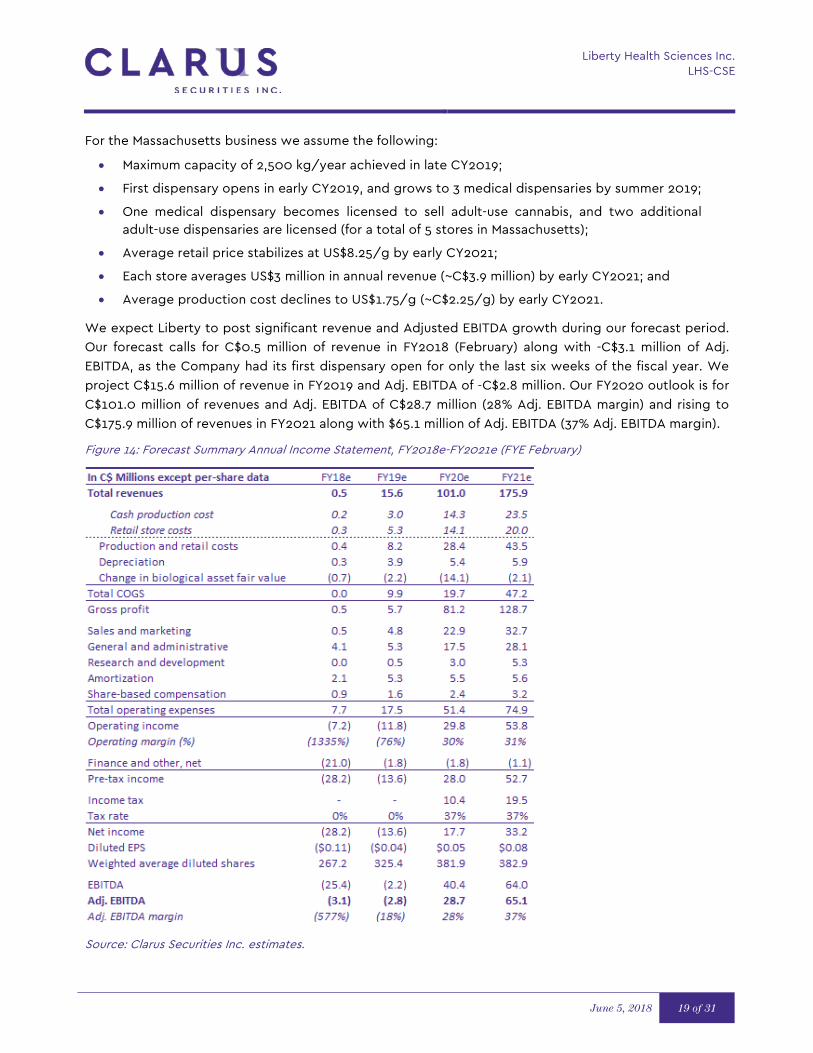

We expect Liberty to post significant revenue and Adjusted EBITDA growth during our forecast period.

Our forecast calls for C$0.5 million of revenue in FY2018 (February) along with -C$3.1 million of Adj.

EBITDA, as the Company had its first dispensary open for only the last six weeks of the fiscal year. We

project C$15.6 million of revenue in FY2019 and Adj. EBITDA of -C$2.8 million. Our FY2020 outlook is for

C$101.0 million of revenues and Adj. EBITDA of C$28.7 million (28% Adj. EBITDA margin) and rising to

C$175.9 million of revenues in FY2021 along with $65.1 million of Adj. EBITDA (37% Adj. EBITDA margin).

Figure 14: Forecast Summary Annual Income Statement, FY2018e-FY2021e (FYE February)

Source: Clarus Securities Inc. estimates.

Liberty Health Sciences Inc. LHS-CSE

20 of 31 June 5, 2018

Figure 15: Forecast Annual Revenue and Adj. EBITDA, FY2018e – FY2021e (FYE February) (in C$ Millions)

Source: Clarus Securities Inc. estimates.

Appears Fully-Funded for Florida and Massachusetts Initiatives

Liberty recently completed a unit offering for C$23 million of gross proceeds (25.56 million units at US$0.90 per unit), which included one share and 100% warrant coverage at C$1.10/share with a two-year term. We estimate the Company obtained net proceeds of about C$21.3 million from the transaction.

In November 2017 Liberty closed a US$12 million (C$15 million) secured convertible debenture offering. The debentures convert into Liberty shares at C$2.00 per share, have a 12% coupon (payable semi-annually) and mature in November 2020. The share-based purchase of the Gainesville facility also included the receipt of C$17.3 million of cash (C$3 million held back until certain performance targets met) that was on the balance sheet of the target.

We estimate Liberty has about C$43 million of cash on hand, which together with the proceeds from scheduled warrant exercises should be sufficient to fund the expansion plans in Florida and Massachusetts and fund working capital until free cash flow is achieved (which we expect in Q3/FY2020 ending November 2019).

We expect the Company to have a fully diluted equity base of about 381 million shares by the end of FY2019 (February).

The Company has no corporate debt instruments outstanding other than the convertible debentures. We do not expect Liberty to obtain a credit facility from a U.S. bank until federal banking regulations change (which may happen with the upcoming SAFE Banking Act bill).

Liberty Health Sciences Inc. LHS-CSE

June 5, 2018 21 of 31

Figure 16: Forecast Annual Cash Flow, FY2018e – FY2021e (FYE February) (in C$ Millions)

Source: Clarus Securities Inc. estimates.

Initiating Coverage with 12-Month Target Price of $2.00 per Share and Speculative Buy Rating

Our groups of comparables include Canadian medical cannabis LPs listed on the TSX or TSX Venture as well as Canadian-listed entities that invest in or operate cannabis-related businesses in the U.S. We also look at the alcohol beverage producer sector as a guideline for where valuations may go in the future as the cannabis sector matures. Estimates and valuations of the peer group constituents are adjusted for a calendar year-end where necessary. We consider calendar year estimates for Liberty to be its fiscal year ending the following February (i.e. CY2018 estimate equals our FY2019 estimate).

According to FactSet consensus estimates (with Clarus estimates used for our coverage universe), the Canadian cannabis LP group currently trades at a consensus average of 22.7x CY2019 EV/Adj. EBITDA, while the much smaller group (in size and market cap) of U.S.-focused cannabis stocks trade at 9.9x CY2019 EV/Adj. EBITDA. The current U.S.-listed peer group tends to be much earlier stage of development than Liberty or focused on highly-competitive adult-use states. We expect this segment to become more relevant if several relatively large entities complete their ongoing processes to achieve a Canadian listing. Meanwhile, the alcohol producer group trades at a consensus average of 14.6x CY2019e EV/Adj. EBITDA.

We utilize FY2021 (February) as the target year for the valuation to arrive at our 12-month target price. We believe this is the first year at which Liberty will reach meaningful capacity utilization of its production facilities in Florida and Massachusetts and have an expansive retail dispensary store network in both states.

Our 12-month target price is C$2.00 per share, or 14x FY2021 (February) EV/Adj. EBITDA discounted one year at 15%. Our target multiple reflects a substantial discount to the average current consensus CY2019e EV/Adj. EBITDA valuations of the Canadian LP sector (which we see as the closest appropriate comparable group for now). We have applied this discount due to the higher political and legal risk (at the federal level) in the U.S. for cannabis producers than for producers operating in Canada. We also note that Section 280E of the U.S. federal tax code (which directly relates to the federal classification of

Liberty Health Sciences Inc. LHS-CSE

22 of 31 June 5, 2018

marijuana as a Schedule 1 drug) imposes higher-than-normal effective tax rates on marijuana producers and retailers, which means Liberty will likely retain less of its Adjusted EBITDA as operating cash flow.

We believe positive changes to these federal tax and political issues would support a positive rerating of our target valuation. Hypothetically, applying a 20x FY2021 (Feb) EV/Adj. EBITDA valuation to Liberty shares (and removing the one-year 15% time discount we apply to our current target rating) would equate to a price of approximately C$3.00 per Liberty share.

We are initiating coverage of Liberty with a Speculative Buy rating, with us applying the Speculative moniker due to the Company’s early stage of operations, legislative/judicial uncertainty in the U.S., and our expectation that Liberty will generate negative Adjusted EBITDA on a quarterly basis for the next several quarters.

Liberty Health Sciences Inc. LHS-CSE

June 5, 2018 23 of 31

Figure 17: Table of Comparables (in C$MM except per-share data or as noted)

Note: NR = Not Rated, N/A = Not Available, NEG = Negative.

Source: FactSet; Clarus Securities Inc. estimates for Aphria Inc., Liberty Health Sciences Inc. and MedReleaf Corp.

Investment Risks

Failure to Scale Operations and Open Multiple Retail Locations. Liberty’s ability to grow, store and sell medical cannabis in Florida is dependent on its cultivation, production and sale licenses received from the Florida Department of Health. Failure to comply with the requirements of the licenses or any failure to maintain the licenses would have a material adverse impact on the business, financial condition and operating results of the Company. Additionally, multiple medical cannabis licensees in Florida received their licenses before Liberty and have already opened retail dispensaries across the state. Liberty’s success depends on the pace at which they build inventory, grow the supply chain and open retail stores.

There is no guarantee that Florida Department of Health will provide any license amendments or if Liberty can open retail stores in favorable jurisdictions and grow as expected.

Liberty Health Sciences Inc. LHS-CSE

24 of 31 June 5, 2018

Limited Operating History. Liberty was incorporated in March 2017 and opened its first licensed medical dispensary in Florida in January 2018. The Company is subject to many of the risks common to early-stage enterprises, including under-capitalization, cash shortages, limitations with respect to personnel, financial, and other resources and lack of revenues.

Agricultural and Weather Risks. Liberty’s business involves the growing of medical marijuana, an agricultural product. It is subject to risks inherent in the agricultural business, such as insects, plant diseases, weather disasters and similar agricultural risks. Although the Issuer expects that any such growing will be completed indoors under climate controlled conditions, there can be no assurance that natural elements will not have a material adverse effect on any such future production. In addition, there is no guarantee that Liberty can reasonably obtain insurance coverage against such events.

Competition. The Florida Department of Health can currently issue an additional 4 medical marijuana treatment center licenses by October 2017, followed by an additional four licenses once the state patient registry issues at least 100,000 patient ID cards to new registrants. An additional 4 licenses can be issued every time the state registry issues a further 100,000 patient ID cards to new registrants.

In addition, the maximum number of dispensaries per licensee (excluding purchases of other licensees’ dispensary rights) is currently set at 25 stores, which will increase as the patient registry grows. The cap on dispensaries per licensee will be removed altogether in April 2020.

Local Zoning Restrictions. While Florida state law requires that local municipalities either (a) prohibit all medical cannabis dispensaries within their jurisdiction or (b) apply the same zoning rules as pharmacies, several municipalities have unilaterally imposed zoning restrictions that do not adhere to state law. Some municipalities are considering changes to their pharmacy zoning in order to also restrict the number of medical cannabis dispensaries in their area. If Liberty is unable to obtain zoning approvals to have dispensaries in targeted cities or counties, then it will likely have a negative impact on its business and financial results.

U.S. Federal Cannabis Laws. Unlike in Canada which has federal legislation uniformly governing the cultivation, distribution, sale and possession of medical cannabis under the Access to Cannabis for Medical Purposes Regulations, investors are cautioned that in the U.S. medical cannabis programs are regulated at only the state level. At least 31 states, including Florida, have implemented medical cannabis programs in some form. Notwithstanding the permissive regulatory environment of medical cannabis at the state level, cannabis and CBD continue to be categorized as Schedule 1 (illegal) controlled substances under the U.S. federal Controlled Substances Act. The U.S. Congress has passed appropriations bills each of the last four years that have not allowed use of federal funds for prosecution of federal cannabis offenses of individuals who are in compliance with state medical cannabis laws. American courts have construed these appropriations bills to prevent the federal government from prosecuting individuals when those individuals comply with state law. However, because this conduct continues to violate federal law, American courts have observed that should Congress at any time choose to appropriate funds to fully prosecute under the CSA, any individual or business – even those that have fully complied with state law – could be prosecuted for violations of federal law. And if Congress restores funding, the federal government will have the authority to prosecute individuals for violations of the law before it lacked funding under the CSA's five-year statute of limitations. Violations of any federal laws and regulations could result in significant fines, penalties, administrative sanctions, convictions or settlements arising from civil proceedings conducted by either the federal government or private citizens, or criminal charges, including but not limited to disgorgement of profits, cessation of business activities or divestiture. This could have a material adverse effect on Liberty, including its reputation and ability to conduct business, its holding (directly or indirectly) of medical cannabis

Liberty Health Sciences Inc. LHS-CSE

June 5, 2018 25 of 31

licenses in the United States, the listing of its securities on various stock exchanges, its financial position, operating results, profitability or liquidity or the market price of its publicly traded shares.

Banking Services to U.S. Cannabis Companies. In February 2014, the DOJ’s Financial Crimes Enforcement Network provided guidance to banks seeking to open accounts for cannabis businesses in legalized state markets. Additionally, in July 2015, the US Senate Appropriations Committee voted in favor of allowing cannabis businesses to access federal banking services; accordingly, state chartered banks and credit unions are currently providing accounts to cannabis companies.

However, opening accounts and carrying out transactions through large institutional banks has been difficult for the cannabis players and this may impact the operational aspects of the business when the businesses become too big to be handled by the state chartered banks.

U.S. Federal Tax Code. Section 280E of the U.S. federal tax code denies business tax deductions and

credits to companies that traffic in controlled substances. It can result in relatively high effective tax rates for marijuana retailers and producers compared to other industries.

Product Liability. As a distributor of products designed to be ingested by humans, Liberty faces an inherent risk of exposure to product liability claims, regulatory action and litigation if its products are alleged to have caused significant loss or injury. In addition, the sale of Liberty’s products involves the risk of injury to consumers due to tampering by unauthorized third parties or product contamination. Previously unknown adverse reactions resulting from human consumption of Liberty's products alone or in combination with other medications or substances could occur. The Company may be subject to various product liability claims or regulatory actions as a result. It could also require Liberty to undertake a product recall.

Additional risks are listed in Liberty Health Sciences’ listing statement dated July 25, 2017, which is available on SEDAR.

Board of Directors and Key Executives

Vic Neufeld – Chairman. Mr. Neufeld is the current CEO of Aphria Inc. and former CEO of Jamieson Wellness (“Jamieson”) (TSX: JWEL, NR), Canada’s largest manufacturer and distributor of natural vitamins, minerals, concentrated food supplements, herbs and botanical medicines. Mr. Neufeld brings 15 years of experience as a chartered accountant and partner with Ernst & Young and 21 years as CEO of Jamieson. During his tenure with Jamieson, the company grew from $20 million in annual sales to over $250 million and expanded its distribution network to over 40 countries. During his time with Aphria, the company has developed a reputation for low-cost, high-margin greenhouse agronomy. Mr. Neufeld earned a Bachelor’s degree and an MBA from the University of Windsor and is a Chartered Accountant.

George Scorsis – CEO and Director. Mr. Scorsis has over 15 years’ experience as a leader in highly regulated industries including alcohol, energy drinks and medical cannabis. He previously served as President of Mettrum Corp., a Canadian medical cannabis LP, which was sold to Canopy Growth Corp. (TSX: WEED, NR) in January 2017 for over $350 million. Mr. Scorsis also served as President of Red Bull Canada and was instrumental in restructuring the organization from a geographical and operational perspective, and growing the business to $150 million in revenue. In that role, he also worked closely with Health Canada on guidelines regulating the energy drink category. Mr. Scorsis also served at Bacardi Canada where he was fundamental in new product developments and launches.

Liberty Health Sciences Inc. LHS-CSE

26 of 31 June 5, 2018

Aaron Serruya – Director. Mr. Serruya has over three decades of experience in the retail franchising sector and building consumer retail supply chains. He is President of International Franchise Inc., home of global brands such as Yogen Fruz, Pinkberry and Swensen’s Ice Cream with over 4,500 frozen yogurt and ice cream franchises in over 50 countries. In addition, he is a Managing Director at Serruya Private Equity and was involved, on an advisory level, with Coolbrands, Kahala Brands and Jamba Juice.

John Cervini – Director. Mr. Cervini, Co-founder and Vice-President, Infrastructure & Technology and director of Aphria Inc., is a fourth-generation greenhouse grower with hydroponic agricultural experience. Together with his father and brother, Mr. Cervini helped establish Lakeside Produce, one of North America’s leading sales and marketing companies selling fresh produce from Canada to multinational retailers throughout North America. Mr. Cervini is a leading innovator in greenhouse growing technology and has also overseen greenhouse expansion to Carpentaria, California and Guadalajara, Mexico. Mr. Cervini is also a director of Copperstate Farms Investors, LLC.

Michael Galloro – Director. Mr. Galloro gained public markets experience engaged a Vice President of Finance for a TSX Venture-listed company in the payment processing sector. He then served as a consultant, focused primarily on serving emerging private and publicly-listed companies with financings, M&A, and corporate structuring. Mr. Galloro earned his CPA and CA designations while working in the financial institutions practice for KPMG LLP and obtained his Honours Bachelor of Accounting degree from Brock University.

Rene Gulliver – Chief Financial Officer. Rene Gulliver brings in 30+ years of experience in a CFO role, across various major companies. He was most recently the Executive Officer and CFO at Dream Global REIT (TSX: DRG.UT, NR). Prior to this he held similar roles at Dream Unlimited, Cushman & Wakefield, Intercon Security and Royal Lepage Limited. Mr. Gulliver previously held roles at PricewaterhouseCoopers, specializing in international M&A and capital raises. He also has significant experience in capital markets, business development and operations.

Liberty Health Sciences Inc. LHS-CSE

June 5, 2018 27 of 31

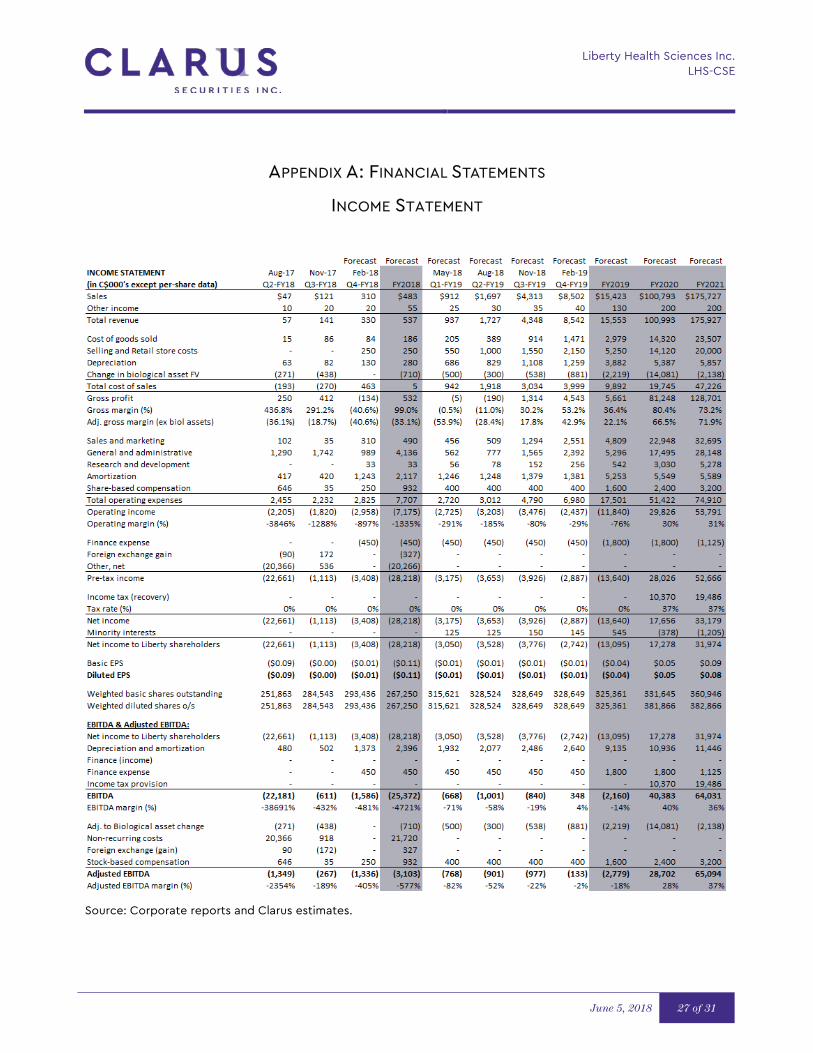

APPENDIX A: FINANCIAL STATEMENTS

INCOME STATEMENT

Source: Corporate reports and Clarus estimates.

Liberty Health Sciences Inc. LHS-CSE

28 of 31 June 5, 2018

BALANCE SHEET

Source: Corporate reports and Clarus estimates.

Liberty Health Sciences Inc. LHS-CSE

June 5, 2018 29 of 31

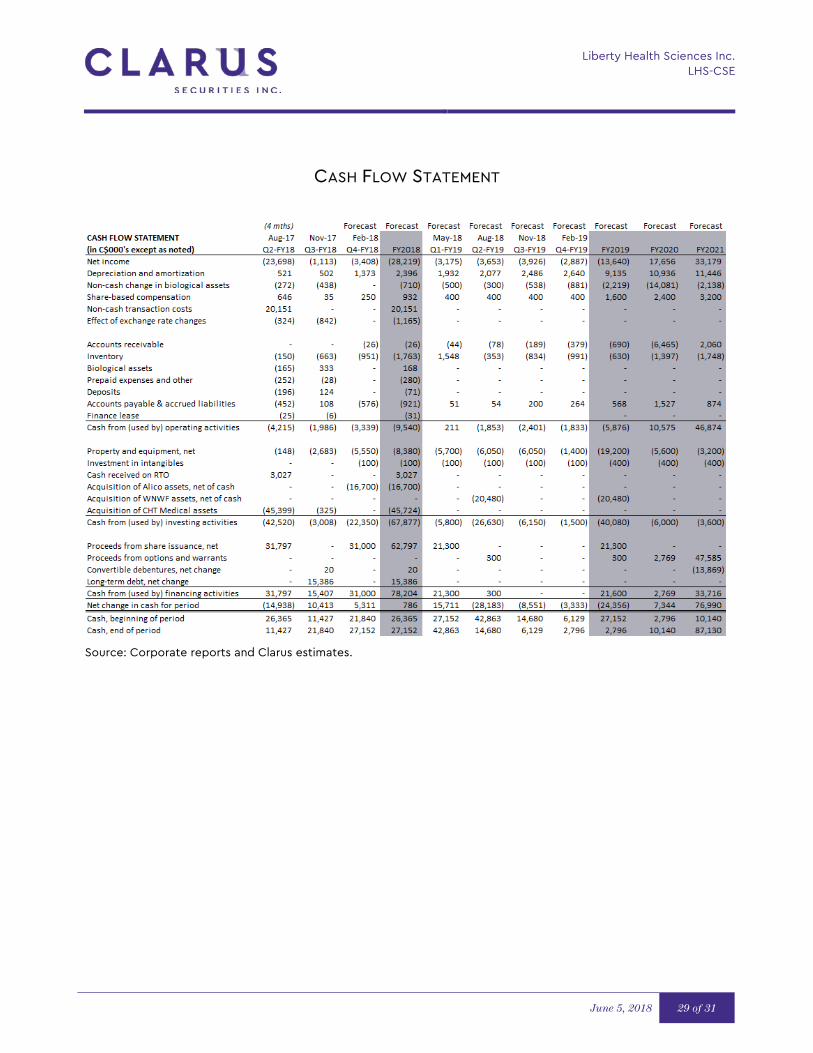

CASH FLOW STATEMENT

Source: Corporate reports and Clarus estimates.

Liberty Health Sciences Inc. LHS-CSE

30 of 31 June 5, 2018

Clarus Securities Equity Research Disclosures

Liberty Health Sciences Inc.: Within the last 24 months, Clarus Securities Inc. has managed or co-managed a public offering of securities of the Company. Within the last 24 months, Clarus Securities Inc. has received compensation for investment banking services with respect to the securities of the Company. Aphria Inc.: The analyst has visited this company’s facilities in Leamington, Ontario. No payment or reimbursement was received from the issuer for the associated travel costs. Within the last 24 months, Clarus Securities Inc. has managed or co-managed a public offering of securities of the Company. Within the last 24 months, Clarus Securities Inc. has received compensation for investment banking services with respect to the securities of the Company. MedReleaf Corp.: The analyst has visited this company’s facilities in Markham, Ontario and Bradford, Ontario. No payment or reimbursement was received from the issuer for the associated travel costs. Within the last 24 months, Clarus Securities Inc. has managed or co-managed a public offering of securities of the Company. Within the last 24 months, Clarus Securities Inc. has received compensation for investment banking services with respect to the securities of the Company. General Disclosure

The information and opinions in this report were prepared by Clarus Securities Inc. (“Clarus Securities”). Clarus Securities is a wholly-owned subsidiary of Clarus Securities Holdings Ltd. and is an affiliate of such. The reader should assume that Clarus Securities or its affiliate may have a conflict of interest and should not rely solely on this report in evaluating whether or not to buy or sell securities of issuers discussed herein.

The opinions, estimates and projections contained in this report are those of Clarus Securities as of the date of this report and are subject to change without notice. Clarus Securities endeavours to ensure that the contents have been compiled or derived from sources that we believe are reliable and contain information and opinions that are accurate and complete. However, Clarus Securities makes no representation or warranty, express or implied, in respect thereof, takes no responsibility for any errors and omissions contained herein and accepts no liability whatsoever for any loss arising from any use of, or reliance on, this report or its contents. Information may be available to Clarus Securities or its affiliate that is not reflected in this report. This report is not to be construed as an offer or solicitation to buy or sell any security. No part of this report may be reproduced or re-distributed without the written consent of Clarus Securities.

Conflicts of Interest

The research analyst and/or associates who prepared this report are compensated based upon (among other factors) the overall profitability of Clarus Securities and its affiliate, which includes the overall profitability of investment banking and related services. In the normal course of its business, Clarus Securities or its affiliate may provide financial advisory and/or investment banking services for the issuers mentioned in this report in return for remuneration and might seek to become engaged for such services from any of such issuers in this report within the next three months. Clarus Securities or its affiliate may buy from or sell to customers the securities of issuers mentioned in this report on a principal basis. Clarus Securities, its affiliate, and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities discussed herein, or in related securities or in options, futures or other derivative instruments based thereon.

Analyst’s Certification

Each Clarus Securities research analyst whose name appears on the front page of this research report hereby certifies that (i) the recommendations and opinions expressed in the research report accurately reflect the research analyst’s personal views about the Company and securities that are the subject of this report and all other companies and securities mentioned in this report that are covered by such research analyst and (ii) no part of the research analyst’s compensation was, is, or will be directly or indirectly, related to the specific recommendations or views expressed by such research analyst in this report.

Equity Research Ratings

Buy: Attractively valued and expected to appreciate significantly from the current price over the next 12-18 months. Speculative Buy: Expected to appreciate significantly from the current price over the next 12-18 months. Financial and/or operational risk is high in the analyst’s view. Accumulate: Attractively valued, but given the current market price, is expected to appreciate moderately over the next 12 -18 months. Hold: Fairly valued and expected to trade in line with the current price over the next 12-18 months. Sell: Overvalued and expected to decline from the current price over the next 12-18 months. Under review: Pending additional review and/or information. No rating presently assigned. Tender: Company subject to an acquisition bid: accept offer. A summary of our research ratings distribution can be found on our website.

Dissemination of Research

Clarus Securities’ Equity Research is available via our website and is currently distributed in electronic form to our complete distribution list at the same time. Please contact your Clarus institutional sales or trading representative or investment advisor for more information. Institutional clients may also receive our research via THOMSON and REUTERS.

Liberty Health Sciences Inc. LHS-CSE

June 5, 2018 31 of 31

For additional disclosures, please visit our website http://www.clarussecurities.com. © Clarus Securities Inc. All rights reserved. Reproduction in whole or in part without permission is prohibited.