nlb montenegrobanka ad, podgorica consolidated …

TRANSCRIPT

NLB MONTENEGROBANKA AD, PODGORICA Consolidated financial statements for the year ended 31 December 2012 prepared in accordance with International Financial Reporting Standards

CONTENTS Page

Independent Auditor’s report

Consolidated Statement of comprehensive income 3

Consolidated Statement of financial position 4

Consolidated Statement of changes in equity 5

Consolidated Statement of Cash Flows 7

Notes to financial statements 8-75

NLB MONTENEGROBANKA A.D. PODGORICA Consolidated financial statements for the year ended 31 December 2012

(All amounts in thousand EUR unless otherwise stated)

3

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

FOR THE YEAR ENDED 31 DECEMBER 2012

Note 2012 2011

Interest income 7 34,924 41,068

Interest expenses 7 (16,099) (18,019)

Net interest income 18,825 23,049

Dividend income - 5

Fee and commission income 8 8,660 8,700

Fee and commission expense 8 (4,166) (3,913)

Net fee and commission income 4,494 4,787

Gains less losses from financial instruments held for trading 9 1,125 901 Foreign exchange translation gains less losses 10 (446) (12) Other operating income 11 322 500

Personnel expenses 12 (7,983) (7,636)

Operating lease expenses (1,460) (1,511)

Depreciation and amortisation 13 (1,455) (1,584)

Other operating expenses 14 (3,639) (3,707)

Provision for other liabilities and charges 15 (162) 1,115

Impairment charge 16 (27,833) (14,606)

(Loss)/Profit before income tax (18,212) 1,301

Income tax expenses 17 (2,835) (133)

(Loss)/Profit for the year (21,047) 1,168

Other comprehensive income, net of income tax

Fair value reserve (available-for-sale investments)

Net change in fair value 20, 33 79 (40) Other comprehensive income for the period, net of income tax 79 (40)

Total comprehensive (loss)/income for the period (20,968) 1,128

(Loss)/Profit attributable to:

Owners of the parent (21,053) 1,161 Non-controlling interest 6 7

Loss for the period (21,047) 1,168

Total comprehensive (loss)/income attributable to:

Owners of the parent (20,975) 1,121

Non-controlling interest 6 7

Total comprehensive (loss)/income for the period (20,968) 1,128

Basic and diluted earnings per share (in EUR) 18 (6.558) 0,500

Notes on pages 8 to 75 are an integral part of these consolidated financial statements.

NLB MONTENEGROBANKA A.D. PODGORICA Consolidated financial statements for the year ended 31 December 2012

(All amounts in thousand EUR unless otherwise stated)

4

CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 31 DECEMBER 2012

Note 2012 2011

Assets

Cash and balances with Central bank 19 51,741 54,497

Financial assets available for sale 20 36,235 18,880

Loans and advances to banks 21 50,660 32,485

Loans and advances to customers 22 364,598 415,072

Property and equipment 23 4,358 5,269

Intangible assets 24 1,007 1,093

Other assets 25 2,065 1,288

Total assets 510,664 528,584

Liabilities

Derivatives – hedge accounting 26 200 441

Deposits from banks 27 1,226 753

Due to customers 27 356,528 378,085

Borrowings from banks 27 48,628 61,406

Borrowings from other customers 27 14,399 22,185

Debt securities issued 28 4,025 4,021

Subordinated liabilities 29 14,199 9,938

Provisions 30 2,103 1,934

Deferred tax liabilities 31 3,478 634

Current tax liability - 76

Other liabilities 32 14,970 3,451

Total liabilities 459,756 482,924

Capital and reserves attributable to owners of parent

Share capital 33 39,425 12,925

Share premium 33 7,146 7,146

(Accummulated) retained earnings 33 (1,269) 19,784

Reserves 33 5,582 5,664

50,884 45,519

Non-controlling interest 33 24 141

Total equity 50,908 45,660

Total equity and liabilities 510,664 528,584

Podgorica 05 August, 2013 On behalf of the Bank: Svetlana Ivanović Robert Kleindienst Anton Ribnikar Director of Finance and Accounting Executive Director Chief Executive Officer

Notes on pages 8 to 75 are an integral part of these consolidated financial statements.

NLB MONTENEGROBANKA A.D. PODGORICA Consolidated financial statements for the year ended 31 December 2012

(All amounts in thousand EUR unless otherwise stated)

5

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

Share

capital Share

premium Revaluation

reserves Profit

reserves Retained earnings Total

Non-controlling

interest Total

equity

Balance as at 1 January 2012 12,925 7,146 5 5,659 19,784 45,519 141 45,660

Total comprehensive income of the period

Loss for the period - - - - (21,053) (21,053) 6 (21,047)

Other comprehensive income, net of income tax Net change in fair value of available-for-sale investments - - 79 - - 79 - 79

Total comprehensive income for the period - - 79 - (21,053) (20,974) 6 (20,968)

Transactions with owners, recorded directly in equity Contributions by and contributions to owners

Increase of share capital 26,500 - - (161) 26,339 - 26,339 Total contributions by and distributions to owners 26,500 - - (161) - 26,339 - 26,339 Disposal of non-controlling interest in subsidiary - - - - - - (123) (123)

Balance as at 31 December 2012 39,425 7,146 84 5,498 (1,269) 50,884 24 50,908

Notes on pages 8 to 75 are an integral part of these consolidated financial statements.

NLB MONTENEGROBANKA A.D. PODGORICA Consolidated financial statements for the year ended 31 December 2012

(All amounts in thousand EUR unless otherwise stated)

6

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY (continued)

Share

capital Share

premium Revaluation

reserves Profit

reserves Retained earnings Total

Non-controlling

interest Total

equity

Balance as at 1 January 2011 12,925 7,146 45 5,659 18,623 44,398 134 44,532

Total comprehensive income of the period

Profit - - - - 1,161 1,161 7 1,168

Other comprehensive income, net of income tax Net change in fair value of available-for-sale investments - - (40) - - (40) (40)

Total other comprehensive income - - (40) - - (40) - (40)

Total comprehensive income for the period - - (40) - 1,161 1,121 7 1,128

Transactions with owners, recorded directly in equity Contributions by and contributions to owners - - - - - - - - Total contributions by and distributions to owners - - - - - - - -

Balance as at 31 December 2011 12,925 7,146 5 5,659 19,784 45,519 141 45,660

Notes on pages 8 to 75 are an integral part of these consolidated financial statements.

NLB MONTENEGROBANKA A.D. PODGORICA Consolidated financial statements for the year ended 31 December 2012

(All amounts in thousand EUR unless otherwise stated)

7

CONSOLIDATED STATEMENT OF CASH FLOWS FOR THE YEAR ENDED 31 DECEMBER 2012

Notes on pages 8 to 75 are an integral part of these consolidated financial statements.

2012 2011

CASH FLOWS FROM OPERATING ACTIVITIES

Interest received 34,286 41,301

Interest paid (15,877) (17,166)

Commission received 8,684 8,868

Commission paid (1,194) (3,882)

Net trading income 1,086 930

Payments to employees and suppliers (12,828) (12,569)

Other income 309 269

Other expenses (174) (154)

Dividends received - 5 Cash flows from operating activities before changes in operating assets and liabilities 11,292 17,602

Decrease/(increase) in operating assets 8,589 (5,237)

Net decrease/(increase) of obligatory reserve 3,767 (667)

Net increase in financial assets available for sale (16,316) (1,443)

Net decrease/(increase) in loans and advances 21,591 (3,329)

Net decrease/(increase) in other assets (453) 202

Increase in operating liabilities (30,273) 821

Net increase in deposits and borrowings at amortized cost (41,712) 1,772

Net increase/(decrease) in other liabilities 11,439 (951)

Cash flow from operating activities (10,392) 13,186

Income tax paid (76) (27)

Net cash flow from operating activities (10,466) 13,159

CASH FLOWS FROM INVESTING ACTIVITIES

Receipts from investing activities 202 74

Proceeds from sale of property and equipment 74 74

Proceeds from equity investments 128 -

Payments from investing activities (466) (1,083)

Purchase of property and equipment (298) (581)

Purchase of intangible asset (168) (502)

Net cash flow from investing activities (264) (1,009)

CASH FLOW FROM FINANCING ACTIVITIES

Proceeds from financing activities 30,500 -

Proceeds from subordinated liabilities 4,000 -

Proceeds from share issue 26,500 -

Net cash flow from financing activities 30,500 -

Effects of exchange rate changes on cash and cash equivalents (584) 834

Net (decrease) /increase of cash and cash equivalents 19,770 12,150

Cash and cash equivalents at beginning of year 78,270 65,286

Cash and Cash equivalents at end of year (Note 19) 97,456 78,270

NLB MONTENEGROBANKA A.D. PODGORICA Notes to the consolidated financial statements for the year ended 31 December 2012

(All amounts in thousand EUR unless otherwise stated)

8

1. General information NLB Montenegrobanka AD, Podgorica (hereinafter: the Bank) and its subsidiary (together “the Group”) is providing universal banking services. NLB Montenegrobanka AD, Podgorica was founded in 1990 as a joint stock company. In 1995 the Bank was registered with the Commercial Court in Podgorica as a joint stock company. In 2002, following the harmonization process with the Company Law, the Bank was registered with the Central Registry of the Commercial Court in Podgorica — Registry number 4- 0006161/001. The Bank was registered with the Security Issuers Register of the Securities Commission under No. 275 (Decision No. 02/3-282/2-02). The Bank has its primary listing on the Montenegro stock exchange. The Bank is controlled by Nova Ljubljanska banka d.d. Ljubljana incorporated in Slovenia (Parent), which owns 96.70% of the ordinary shares as at 31 December 2012 (31 December 2011: 89.95% ordinary shares). The largest shareholders of Nova Ljubljanska banka d.d. Ljubljana are the Republic of Slovenia, owning 40.21 % of shares, and KBC Bank N.V. Brussels (hereinafter: KBC), owning 22.04 %. The Bank’s gyro account number with the Central Bank of Montenegro is 907-53001-03 — Payment operations. Pursuant to the Banking Law, Memorandum of Association, Articles of Association and Decision of the Central Bank of Montenegro, the Bank’s operations are permitted to include the following: • Accepting deposits and other funds from citizens and legal entities and granting loans and other placements from funds received wholly or partially on its own behalf; • Issuing guarantees and taking over other responsibilities; • Buying and collecting receivables; • Issuing, processing and recording payment instruments (including credit cards, traveller’s and banker’s checks); • Payment transfers with foreign banks: • Financial lease; • Trading in foreign currency on its own or Client’s behalf and account through currency and interest instruments, including foreign currency transactions; • Collecting data, performing analyses and providing information and advice on creditworthiness of legal entities and entrepreneurs, as well as other business issues; • Depot operations; • Safe custody • Securities’ transaction in accordance with the Law, with the Central Bank’s preapproval. The Bank operates through its Head Office in Podgorica and a network of branches (19) and cash desks (3) in the towns of: Podgorica, Ulcinj, Bar, Budva, Cetinje, Bijelo Polje, Rožaje, Mojkovac, Herceg Novi, Kotor, Nikšić, Tivat, Pijevlja, Berane and Tuzi. As of 31 December 2012 the Bank had 330 employees (2011: 338 employees). According to the Law and Articles of Association the Bank is managed by shareholders, depending on the amount of their equity. The managing bodies of the Bank are: Shareholders’ Assembly, which consists of all shareholders of the Bank and the Board of Directors, whose members are appointed by the Shareholders’ Assembly. The Board of Directors has five members, the majority of which are not employed with the Bank. The General Manager is the member of Board of Directors and the chief executive of the Bank. Management of the Bank consists of Chief executive (CEO) and executive directors (members of management). The Bank is represented by Chief executive who coordinates the work of executives and monitors the execution of activities within the Bank on daily basis. Permanent body of the Board of Directors is Audit committee. The Management of the Bank has administrative bodies: -Assets and Liabilities Committee (ALCO) -Credit Committees -Other Committees established by management for specific issues. These consolidated financial statements have been approved for issue by the Management Board on 05 August 2013.

NLB MONTENEGROBANKA A.D. PODGORICA Notes to the consolidated financial statements for the year ended 31 December 2012

(All amounts in thousand EUR unless otherwise stated)

9

2. Summary of significant accounting policies The principal accounting policies applied in the preparation of these consolidated financial statements are set out below. These policies have been consistently applied to all the years presented, unless otherwise stated. 2.1. Statement of compliance These consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) adopted by the International Accounting Standards Board (IASB). The Bank prepares consolidated financial statements which include the Bank and its subsidiary. The subsidiary, over which the Bank has the power to govern the financial and operating policies generally accompanying a shareholding of more than one half of the voting rights, is fully consolidated. 2.2. Basis of preparation The consolidated financial statements have been prepared under the historical cost convention as modified by the valuation of available-for-sale financial assets, except for those with no reliable measurement of fair value, financial assets and financial liabilities designated at fair value through profit and loss including derivative financial instruments. The preparation of financial statements in conformity with IFRS requires the use of certain critical accounting estimates and assumptions that affect the amounts of assets and liabilities presented, disclosure of contingent assets and liabilities at balance sheet date and the reported amounts of income and expenses incurred in the accounting period. Estimates and related assumptions are based on historical experience and the information available at the date of preparation of financial statements, which constitutes the basis for estimation of fair value of assets and liabilities which cannot be designated using other sources. The actual results may differ from these estimates. Critical accounting estimates, including the factors considered by management in making their judgement that the Bank is a going concern, are disclosed in note 4. Estimates and assumptions are subject to regular review. Modifications of accounting estimates are recognized as incurred if related exclusively to that particular period, i.e. in periods in which they incurred and future periods, if related to current and future period. 2.2.1 Implementation of new and revised International Financial Reporting Standards

During the current year, the NLB Group adopted all new and revised standards and interpretations issued by the International Accounting Standards Board (hereinafter: the IASB) and the International Financial Reporting Interpretations Committee (hereinafter: the IFRIC) and endorsed by the EU that are effective for accounting periods beginning on January 1, 2012.

a) Accounting standards and amendments to existing standards effective for annual periods beginning on January 1, 2012 that were endorsed by EU and adopted by us

- IFRS 7 (amendment) - Disclosures, Transfers of Financial Assets (effective for annual periods beginning on or after July 1, 2011). The amendment requires additional disclosures in respect of risk exposures arising from transferred financial assets. The amendment includes a requirement to disclose by class of asset the nature, carrying amount and a description of the risks and rewards of financial assets that have been transferred to another party yet remain on the entity's statement of financial position. Disclosures are also required to enable a user to understand the amount of any associated liabilities, and the relationship between the financial assets and associated liabilities. Where financial assets have been derecognized but the entity is still exposed to certain risks and rewards associated with the transferred asset, additional disclosure is required to enable the effects of those risks to be understood. The amendment impacts presentation aspects.

- Other revised standards and interpretations: amendments to IFRS 1 - Fist time Adoption of IFRS, relating to severe hyperinflation and removal of fixed dates for first-time adopters and amendment to IAS 12 - Income Taxes, relating to the recovery of underlying assets – investment property measured at fair value. The amendments do not have an impact on financial statements on the NLB Group.

NLB MONTENEGROBANKA A.D. PODGORICA Notes to the consolidated financial statements for the year ended 31 December 2012

(All amounts in thousand EUR unless otherwise stated)

10

2. Summary of significant accounting policies (continued)

b) Accounting standards and amendments to existing standards issued that were endorsed by EU but not early adopted by the NLB Group:

- IAS 19 (amendment) - Employee Benefits (effective for annual periods beginning on or after January 1, 2013, with earlier application permitted). Amendment to standard relates to the recognition and measurement of defined benefit obligations and to the disclosure to all employee benefits. The amendment will not have an impact on financial statements on the NLB Group.

- IAS 1 (amendment) - Presentation of Financial Statements (effective for annual periods beginning on or after July 1, 2012, with earlier application permitted). The amendments retain the option to present profit or loss and other comprehensive income in either a single statement or in two separate but consecutive statements. However, the amendments require additional disclosures to be made in the other comprehensive income section, such that items of other comprehensive income are grouped into two categories: items that will not be reclassified subsequently to profit or loss; and items that will be reclassified subsequently to profit or loss when specific conditions are met. Income tax on items of other comprehensive income must be allocated on the same basis. The amendment impacts presentation aspects.

- IFRS 7 (amendments) - Offsetting Financial Assets and Financial Liabilities (effective for annual periods beginning on or after January 1, 2013). The amendment requires disclosures that will enable users of an entity’s financial statements to evaluate the effect or potential effect of netting arrangements, including rights of set-off. The amendment will have an impact on disclosures of financial instruments on the NLB Group.

- IAS 32 (amendments) - Offsetting Financial Assets and Financial Liabilities (effective for annual periods beginning on or after January 1, 2014). The amendment added application guidance to IAS 32 to address inconsistencies identified in applying some of the offsetting criteria. This includes clarifying the meaning of ‘currently has a legally enforceable right of set-off’ and that some gross settlement systems may be considered equivalent to net settlement.

- IFRS 10 - Consolidated Financial Statements, IFRS 11 - Joint Arrangements, IFRS 12 - Disclosures of Interests in Other Entities, a revised version of IAS 27 - Separate Financial Statements, which has been amended for the issuance of IFRS 10 but retains the current guidance for separate financial statements, and a revised version of IAS 28 - Investments in Associates and Joint Ventures, which has been amended for conforming changes based on the issuance of IFRS 10 and IFRS 11. Standards are effective for annual periods beginning on or after January 1, 2014, with earlier application permitted as long as each of the other standards is also applied early. However, entities are permitted to include any of the disclosure requirements in IFRS 12 into their consolidated financial statements without the early adoption of IFRS 12. The NLB Group is currently evaluating the potential impact that the adoption of the standards will have on its consolidated financial statements.

- IFRS 10 (new standard). The new standard replaces the parts of IAS 27 - Consolidated and Separate Financial Statements that deal with consolidated financial statements. SIC 12 Consolidation - Special Purpose Entities has been withdrawn upon the issuance of IFRS 10. Under IFRS 10, there is only one basis for consolidation, that being control. In addition, IFRS 10 includes a new definition of control that contains three elements: control over an investee, exposure, or rights to variable returns from its involvement with the investee, and the ability to use its control over the investee to affect the amount of the investor's returns. Extensive guidance has been added in IFRS 10 to deal with complex scenarios.

- IFRS 11 (new standard). The new standard replaces IAS 31 - Interests in Joint Ventures. IFRS 11 deals with how a joint arrangement, over which two or more parties have joint control, should be classified. SIC 13 Jointly Controlled Entities - Non-monetary Contributions by Venturers has been withdrawn upon the issuance of IFRS 11. Under IFRS 11, joint arrangements are classified as joint operations or joint ventures, depending on the rights and obligations of the parties to the arrangements. In contrast, under IAS 31, there are three types of joint arrangements: jointly controlled entities, jointly controlled assets and jointly controlled operations. In addition, joint ventures under IFRS 11 must be accounted for using the equity method of accounting, whereas jointly controlled entities under IAS 31 may be accounted for using the equity method of accounting or proportionate accounting.

NLB MONTENEGROBANKA A.D. PODGORICA Notes to the consolidated financial statements for the year ended 31 December 2012

(All amounts in thousand EUR unless otherwise stated)

11

2. Summary of significant accounting policies (continued)

- IFRS 12 (new standard). The new standard is a disclosure standard and is applicable to entities that have interests in subsidiaries, joint arrangements, associates and/or unconsolidated structured entities. In general, the disclosure requirements in IFRS 12 are more extensive than those in the current standards.

- IFRS 13 (new standard) - Fair Value Measurement (effective for annual periods beginning on or after January 1, 2013, with earlier application permitted). The standard establishes a single source of guidance for fair value measurements and disclosures about fair value measurements. The standard defines fair value, establishes a framework for measuring fair value, and requires disclosures about fair value measurements. The scope of the standard is broad; it applies to both financial instruments and non-financial instruments for which other standards require or permit fair value measurements and disclosures about fair value measurements, except in specified circumstances. In general, the disclosure requirements in IFRS 13 are more extensive than those required in the current standards. For example, quantitative and qualitative disclosures based on the three-level fair value hierarchy, currently required for financial instruments only under IFRS 7 Financial Instruments: Disclosures, will be extended by IFRS 13 to cover all assets and liabilities within its scope. The NLB Group is currently evaluating the potential impact that the adoption of the standard will have on its consolidated financial statements.

- Other revised standards and interpretations: amendment to IFRIC 20 - Stripping Costs in the Production Phase of a Surface Mine. The amendment will not have an impact on financial instruments on the NLB Group.

c) Accounting standards and amendments to existing standards issued but not endorsed by EU:

- IFRS 9 - Financial Instruments IFRS 9 issued in November 2009 replaces those parts of IAS 39 relating to the classification and measurement of financial assets. IFRS 9 was further amended in October 2010 to address the classification and measurement of financial liabilities. Key features of the standard are as follows:

- Financial assets are required to be classified into two measurement categories: those to be measured

subsequently at fair value, and those to be measured subsequently at amortized cost. The decision is to be made at initial recognition. The classification depends on the entity’s business model for managing its financial instruments and the contractual cash flow characteristics of the instrument.

- An instrument is subsequently measured at amortized cost only if it is a debt instrument and both (i) the objective of the entity’s business model is to hold the asset to collect the contractual cash flows, and (ii) the asset’s contractual cash flows represent only payments of principal and interest (i.e. it bears only “basic loan features”). All other debt instruments are to be measured at fair value through profit or loss.

- All equity instruments are to be measured subsequently at fair value. Equity instruments that are held for trading will be measured at fair value through profit or loss. For all other equity investments, an irrevocable election can be made at initial recognition, to recognize unrealized and realized fair value gains and losses through other comprehensive income rather than profit or loss. There is to be no recycling of fair value gains and losses to profit or loss. This election may be made on an instrument-by-instrument basis. Dividends are to be presented in profit or loss, as long as they represent a return on investment.

- Most of the requirements in IAS 39 for classification and measurement of financial liabilities were carried forward unchanged to IFRS 9. The key change is that an entity will be required to present the effects of changes in own credit risk of financial liabilities designated as at fair value through profit or loss in other comprehensive income.

- Adoption of IFRS 9 is mandatory from January 1, 2015, while earlier adoption is permitted, but the EU has not yet endorsed it. The NLB Group is considering the implications of the standard, the impact on the NLB Group and the timing of its adoption.

NLB MONTENEGROBANKA A.D. PODGORICA Notes to the consolidated financial statements for the year ended 31 December 2012

(All amounts in thousand EUR unless otherwise stated)

12

2. Summary of significant accounting policies (continued)

- Amendments to IFRS 10 - Consolidated Financial Statements, IFRS 11 Joint Arrangements, IFRS 12 Disclosures of Interests in Other Entities - Transition Guidance (effective for annual periods beginning on or after January 1, 2014, with earlier application permitted). Amendments were issued to ease transition to new standards by restrictions of requirements regarding assurance of adjusted comparable data for comparable period.

- Amendments to IFRS 10 Consolidated Financial Statements, IFRS 11 Joint Arrangements, IFRS 12 Disclosures of Interests in Other Entities – Investment Entities (effective for annual periods beginning on or after January 1, 2014, with earlier application permitted). Amendments include the creation of a definition of an investment entity, the requirement that such entities measure investment in subsidiaries at fair value through profit and loss instead of consolidating them, new disclosure requirements for investment entities and requirement for an investment entity’s separate financial statements.

- Annual improvements to IFRS 2009-2011 cycle. The improvements consist of a mixture of substantive changes and clarifications and are effective for annual periods beginning on or after January 1, 2013. Amendments to IFRS 1 Fist time Adoption of IFRS include explanations of additional comparative information disclosures. If additional comparative information is provided, the information should include disclosure of comparative information for any additional statements included beyond the minimum comparative financial statement requirements. Presenting additional comparative information voluntarily would not trigger a requirement to provide a complete set of financial statements. Amendments to IAS 16 Property, plant and equipment classifies spare parts, stand-by equipment and servicing equipment as property, plant and equipment when they meet the definition of property, plant and equipment in IAS 16 and as inventory otherwise. Amendments to IAS 32 Financial instruments: Presentation require that income tax relating to distributions to holders of an equity instrument and to transaction costs of an equity transaction should be accounted for in accordance with IAS 12 Income Taxes. Amendments to IAS 34 Interim Financial Reporting require separate disclosure of total assets and total liabilities for a particular reportable segment in interim financial reporting only when the amounts are regularly provided to the chief operating decision maker and there has been a material change from the amounts disclosed in the last annual financial statements for that reportable segment. Amendments to IFRS 1 First-time Adoption of International Financial Reporting Standards require that borrowing costs incurred on or after the date of transition to IFRSs that relate to qualifying assets under construction at the date of transition should be accounted for in accordance with IAS 23 Borrowing Costs.

- Other revised standards and interpretations: IFRS 1 - Fist time Adoption of IFRS, relating to prospective application related to government loans are not expected to affect the NLB Group’s financial statements.

2.3. Consolidation

The subsidiary, over which the Bank has the power to govern the financial and operating policies generally accompanying a shareholding of more than one half of the voting rights, is fully consolidated. The subsidiary is consolidated from the date on which control is transferred to the Bank, and is de-consolidated from the date on which control ceases. Where necessary, the accounting policies of the subsidiary have been amended to ensure consistency with the policies adopted by the Bank. The financial statements of consolidated subsidiaries were prepared as of the parent entity’s reporting date. Non-controlling interests are disclosed in the consolidated statement of changes in equity. Non-controlling interest is that part of the net results and of the equity of a subsidiary attributable to interests which are not owned, directly or indirectly, by the Bank. The Bank measures non-controlling interest on a transaction on a transaction basis, either at fair value, or the non-controlling interest's proportionate share of net assets of the acquired. Non controlling interest is included in balance sheet. Inter-company transactions, balances and unrealized gains on transactions between the Bank and its subsidiary are eliminated. Unrealized losses are also eliminated unless the transaction provides evidence of impairment of the asset transferred. The Bank applies a policy of treating transactions with non-controlling interests as transactions with equity owners of the Bank.

NLB MONTENEGROBANKA A.D. PODGORICA Notes to the consolidated financial statements for the year ended 31 December 2012

(All amounts in thousand EUR unless otherwise stated)

13

2. Summary of significant accounting policies (continued)

2.4. Segment reporting Operating segments are reported in a manner consistent with internal reporting to the executive body, i.e. ALCO committee, which makes decisions regarding the allocation of resources and assesses the performance of a specific segment. All transactions between operating segments are conducted on an arm’s length basis. Income and expenses directly associated with each segment are included in determining each segment’s performance. In accordance with IFRS 8, the Bank has the following reportable segments: Retail banking, Corporate banking and Financial markets. 2.5. Foreign currency translation

a) Functional and presentation currency

Items included in the financial statements are measured by using the currency of the primary economic environment in which the Bank operates (functional currency). The consolidated financial statements are presented in EUR, which is the Bank’s functional and presentation currency.

b) Transactions and balances

Foreign currency transactions are translated into EUR using the exchange rate prevailing at the dates of the transactions. Monetary assets and liabilities denominated in foreign currency at balance sheet date are translated into EUR using the year-end exchange rates. Non-monetary items measured at historical cost in foreign currency are translated into EUR using the exchange rate prevailing at the date of the transaction. Foreign exchange gains and losses resulting from the settlement of such transactions and from the translation of monetary assets and liabilities denominated in foreign currencies are recognized in the profit and loss. Translation differences resulting from changes in the amortized cost of monetary items denominated in foreign currency and classified as available-for-sale financial assets are recognized in the profit and loss. Translation differences on non-monetary items, such as equities classified as available-for-sale, are included together with valuation reserves in the valuation (losses)/gains taken to other comprehensive income and accumulated in revaluation reserve in equity. Gains and losses resulting from foreign currencies purchases and sale for trading purposes are included in the profit and loss as gains less losses from financial instruments held for trading. Official exchange rates for major currencies used in the translation of the consolidated statement of financial position items denominated in foreign currencies were as follows: In EUR 2012 2011 USD 0.7586 0.7729 CHF 0.8278 0.8226

NLB MONTENEGROBANKA A.D. PODGORICA Notes to the consolidated financial statements for the year ended 31 December 2012

(All amounts in thousand EUR unless otherwise stated)

14

2. Summary of significant accounting policies (continued) 2.6 Financial assets

2.6.1. Classification The Bank classifies its financial assets in the following categories: financial assets at fair value through profit or loss; loans and receivables and available-for-sale financial assets. Management determines the classification of its investments at initial recognition. (a) Financial assets at fair value through profit or loss

This category has two sub-categories: financial assets held for trading, and those designated at fair value through profit or loss at inception. A financial asset is classified as held for trading if it is acquired or incurred principally for the purpose of selling in the near term or if there is evidence of an actual pattern of short-term profit-taking or if it is decided by the Management. Derivatives are always categorized as held for trading unless they are designated as hedging instruments. (b) Loans and receivables Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market, other than: (a) those that the Bank intends to sell immediately or in the short term, which are classified as held for trading, and those that the entity upon initial recognition designates as at fair value through profit or loss; (b) those that the Bank upon initial recognition designates as available for sale; or (c) those for which the Bank may not recover substantially all of its initial investment, other than because of credit deterioration. (c) Available-for-sale financial assets

Financial instruments are classified as available-for-sale financial assets if they cannot be classified as one of the remaining three categories of financial assets – held to maturity financial assets, financial assets at fair value through profit and loss or loans. Available-for-sale investments are those intended to be held for an indefinite period of time, which may be sold in response to needs for liquidity or changes in interest rates, exchange rates or equity prices. These financial instruments include investments in equity and debt securities. 2.6.2. Measurement and Recognition

Financial assets are initially recognized at fair value plus transaction costs for all financial assets not carried at fair value through profit or loss. Financial assets carried at fair value through profit and loss are initially recognized at fair value, and transaction costs are recorded in profit and loss. Financial assets at fair value through profit or loss and available-for-sale financial assets are subsequently measured at fair value. Gains and losses arising from changes in the fair value of the financial assets at fair value through profit or loss are included in the profit and loss in the period in which they arise. Gains/losses arising from changes in the fair value of available-for-sale financial assets are recognized in other comprehensive income, until the financial asset is derecognized or impaired, when the cumulative gain or loss previously recognized in other comprehensive income is recognized in the profit and loss. The fair values of quoted investments in active markets are based on current bid prices. If there is no active market for a financial asset, the Bank establishes fair value using valuation techniques. These include the use of recent arm’s length transactions, discounted cash flow analysis, option pricing models and other valuation techniques commonly used by market participants.

NLB MONTENEGROBANKA A.D. PODGORICA Notes to the consolidated financial statements for the year ended 31 December 2012

(All amounts in thousand EUR unless otherwise stated)

15

2. Summary of significant accounting policies (continued) Interest calculated using effective interest rate method and translation differences on monetary securities classified as available for sale are directly recognized in profit or loss, while translation differences on non-monetary securities available for sale are recognized in other comprehensive income, along with the change in its fair value.

Dividends on available-for-sale equity instruments are recognized in the profit and loss when the Bank’s right to receive payment is established.

Loans and advances are initially recognised at fair value plus transaction costs. Subsequently, they are carried at amortised cost, using effective interest method. 2.6.3. De-recognition

Financial assets are derecognised when the contractual rights to the cash flows from the financial assets has expired or where the Bank has transferred substantially all risks and rewards of ownership. Financial liabilities are derecognised when they are extinguished − that is, when the obligation is discharged, cancelled or expires. Carrying value of financial liabilities derecognized based on debt to equity swap, is extinguished with equivalent value of share capital issued based on market value per share recorded in the Montenegrin stock exchange for the Bank. 2.6.4. Fair value of financial instruments The fair values of quoted investments in active markets are based on their market price at balance sheet date, i.e. current bid prices. If there is no active market for a financial asset, the Bank establishes fair value using valuation techniques. These include the use of recent arm’s length transactions, discounted cash flow techniques or pricing models. If discounted cash flow techniques are used, estimated future cash flows are based on Management’s best estimates, and the discount rate is a market based rate at the reporting date for an instrument with similar terms and conditions. If pricing models are used, inputs are based on market based measurements at the reporting date. 2.7 Offsetting financial instruments Financial assets and liabilities are offset and the net amount reported in the balance sheet when there is a legally enforceable right to offset the recognised amounts and there is an intention to settle on a net basis, or realize the asset and settle the liability simultaneously. 2.8 Derivative financial instruments and hedge accounting Derivative financial instruments are initially recognised at fair value. At the balance sheet date derivatives are re-measured at fair value within assets when favorable to the Bank and within liabilities when unfavorable to the Bank.

The method of recognising the resulting fair value gain or loss depends on whether the derivative is designated as a hedging instrument, and if so, the nature of the item being hedged. Changes in the fair value of derivative instruments not qualified for hedge accounting are recognized immediately in the profit and loss in Gains less losses from financial instruments held for trading. Derivative financial instruments are classified as financial instruments held for trading, unless designated as hedge accounting instruments, when specific rules used in hedge accounting are applied for their recognition. Changes in the fair value of derivatives that are designated and qualify as fair value hedges are recognized in the profit and loss, together with any changes in the fair value of the hedged items attributable to the hedged risks. Effective changes in fair value of hedging instruments and related hedged items are reflected in ‘fair value adjustments in hedge accounting’.

NLB MONTENEGROBANKA A.D. PODGORICA Notes to the consolidated financial statements for the year ended 31 December 2012

(All amounts in thousand EUR unless otherwise stated)

16

2. Summary of significant accounting policies (continued) 2.9. Interest income and expenses

Interest income and expenses for all interest-bearing financial instruments are recognised in the profit and loss on an accruals basis using the effective interest rate method. The effective interest method is a method of calculating the amortised cost of a financial asset or a financial liability and of allocating the interest income or interest expense over the relevant period. The effective interest rate is the rate that exactly discounts estimated future cash payments or receipts through the expected life of the financial instrument or, when appropriate, a shorter period to the net carrying amount of the financial asset or financial liability. The calculation includes all fees and points paid or received between parties to the contract that are an integral part of the effective interest rate, transaction costs and all other premiums or discounts. Interest income includes interest from investments with fixed return and securities designated at fair value through profit and loss, as well as accrued discounts and premiums on securities. Once a financial asset or a group of similar financial assets has been written down as a result of an impairment loss, interest income is recognised using the rate of interest used to discount the future cash flows for the purpose of measuring the impairment loss. 2.10. Fee and commission The fee and commission income and expenses arisen from providing, i.e. using of banking services are recorded in the profit and loss as incurred, i.e. at the moment the services are provided, i.e. used. Loan commitment fees for loans that are likely to be drawn down are deferred (together with related direct costs) and recognised as an adjustment to the effective interest rate on the loan. Fee and commission income and expenses also include fees from letters of guarantees and letters of credit issued by the Bank in favour of the clients, fees arising from domestic and international bank charges, agent services and other services provided by the Bank. 2.11. Impairment of financial assets a) Financial assets carried at amortised cost

The Bank assesses at each balance sheet date whether there is objective evidence that a financial asset or group of financial assets is impaired. A financial asset or a group of financial assets is impaired only if there is objective evidence of impairment as a result of one or more loss events that occurred after the initial recognition of the asset and if those events have a reliable impact on the estimated future cash flows. The criteria that the Bank uses to determine that there is objective evidence of an impairment loss include:

significant financial difficulties experienced by the borrower,

breach of contracts/loan covenants or conditions, default or delinquency in contractual payments of principal or interest,

Initiation of bankruptcy proceedings,

deterioration in the fair value of collateral,

Deterioration of the borrower’s competitive position. The process of impairment testing is as follows: - significant loans and advances are individually reviewed, - other loans and advances are assessed collectively, - individually reviewed loans and advances showing no evidence of impairment are included in the group of loans and

advances with similar credit risk characteristics and collectively assessed for impairment,

- loans and advances that are individually assessed for impairment and for which an impairment loss is or continues to

be recognized are not included in a collective assessment of impairment,

NLB MONTENEGROBANKA A.D. PODGORICA Notes to the consolidated financial statements for the year ended 31 December 2012

(All amounts in thousand EUR unless otherwise stated)

17

2. Summary of significant accounting policies (continued)

For the purpose of collective assessment of impairment the following is considered:

- future cash flows for the group of loans and advances are assessed with regard to historical loss statistics for assets with similar credit risk characteristics,

- the discount factor used for discounting cash flows represents the specific average effective interest rate of the group of loans and advances,

- the appropriateness of methodology and assumptions used with determining future cash flows are subject to regular review.

For the purposes of a collective evaluation of impairment, the Bank uses migration matrices, which show expected migration of customers between internal rating classes. The probability of migration is assessed on the basis of past years’ experience, that is annual migration matrices for different types of customers. Exposures to individuals are additionally analyzed with regard to type of products. Based on the migration matrices and assessment of average repayment rate for D and E rated customers, the Bank recognizes impairment losses also for clients that currently show no signs of impairment, but on the basis of past experience the Bank justifiably estimates that some losses have already been incurred. If it is determined that, with regard to loans and advances and formed groups, objective evidence of impairment loss exists, the amount of the loss is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows discounted at the financial asset’s original effective interest rate. The carrying amount of the asset is reduced through the use of an allowance account and the amount of the loss is recognised in the profit and loss. If financial assets have a variable interest rate, the discount rate for measuring any impairment loss is the current effective interest rate determined under the contract. Loans and receivables are eventually written off when all possibilities for their collection are exhausted, in accordance with internal Bank regulations, against the related allowance account for impairment. Subsequent recoveries of previously written off loans are recognised as decrease of loss from impairment of assets in the profit and loss. b) Financial assets classified as available for sale The Bank assesses at each balance sheet date whether there is objective evidence that financial assets available for sale are impaired. In case of equity investments classified as available for sale, significant or prolonged decline in the fair value of the security below its cost is considered an objective evidence of impairment. If any such evidence exists, the cumulative loss is removed from other comprehensive income and recognised in the profit and loss. Impairment losses recognised in the profit and loss on equity instruments are not reversed through the profit and loss; subsequent increases in fair value after impairment are recognized in other comprehensive income. If, in a subsequent period, the fair value of a debt instrument classified as available for sale increases and the increase can be objectively related to an event occurring after the impairment loss was recognised in the profit and loss, the impairment loss is reversed through the profit and loss. The following factors are considered in determining impairment losses on debt instruments:

- Default or delinquency in interest or principal payments; - Liquidity difficulties of the issuer; - Breach of contract covenants or conditions; - Bankruptcy of the issuer; - Deterioration of economic and market conditions and - Deterioration in the credit rating of the issuer below the acceptable level.

Impairment losses recognized in the profit and loss are measured as the difference between the carrying amount of the financial asset and its current fair value. The current fair value of the instrument is its market price or discounted future cash flows, when the market price is not obtainable.

NLB MONTENEGROBANKA A.D. PODGORICA Notes to the consolidated financial statements for the year ended 31 December 2012

(All amounts in thousand EUR unless otherwise stated)

18

2. Summary of significant accounting policies (continued) c) Renegotiated loan Loans for which, due to deterioration of the debtor’s credit rating, new payment terms have been renegotiated, are no longer considered to be past due, but are treated as new loans. d) Repossessed assets In certain circumstances, assets are repossessed following the foreclosure on loans that are in default. These assets are except where otherwise stated, included in “Other Assets”. Repossessed Assets are held temporarily for disposal and are valued at the lower of cost and net realisable value. Any gains or losses on disposal are included in “Other operating income”. 2.12 Intangible assets Licenses

Separately acquired licenses are shown at historical cost. Licenses have a finite useful life and are carried at cost less accumulated amortization. Amortization is calculated using the straight-line method to allocate the cost of licenses over their estimated useful life of five years. Computer software Computer software costs are capitalized in the amount of costs incurred to bring software to use. These costs are amortized over their estimated useful lives of ten years. The depreciation period for intangible assets begins when they become available for use. 2.13 Property, plant and equipment Property, plant and equipment are stated at cost less accumulated depreciation and any impairment loss. Cost includes expenditure that is directly attributable to the acquisition of the fixed asset. The assets’ residual values and useful lives are reviewed and adjusted if appropriate at each balance sheet date. The Bank assesses whether there is objective evidence that assets may be impaired. If any such evidence exists, the recoverable amount is estimated. The recoverable amount is the higher of fair value less costs to sell and value in use. If value in use is higher than carrying value, the asset should not be subject to impairment.

Subsequent costs are included in the asset’s purchase cost or are recognised as a separate asset, only when it is probable that future economic benefits associated with the item will flow to the Bank and the cost of the item can be measured reliably. All other repairs and maintenance are charged to other operating expenses during the financial period in which they are incurred. Depreciation of assets is calculated using the straight-line method to allocate their cost to their residual values over their estimated useful lives. The following are approximations of the annual rates used:

%

Buildings 3

Computers and computer equipment 20

Furniture and equipment 10

Vehicles 20

Leasehold improvements 20

The depreciation period for fixed assets begins when they become available for use. Gains and losses on disposals are determined by comparing proceeds with carrying amount. These are included in other operating income/expenses in the profit and loss.

NLB MONTENEGROBANKA A.D. PODGORICA Notes to the consolidated financial statements for the year ended 31 December 2012

(All amounts in thousand EUR unless otherwise stated)

19

2. Summary of significant accounting policies (continued) 2.14 Non-current assets held for sale Non-current assets are classified as held for sale if their carrying amount will be recovered through a sale transaction rather than through continuing use. The condition is met only when the sale is highly probable and the asset is available for immediate sale in its present condition. The sale should be finished within one year from the date of classification, or in an extensive period if the sale process had already begun. Non-current assets held for sale are measured at the lower of the assets’ previous carrying amount and fair value less cost of sale. 2.15 Leases Leases in which a significant portion of the risks and rewards of ownership are retained by the lessor are classified as operating leases. Payments made under operating leases are charged to the profit and loss on a straight-line basis over the period of the lease. When an operating lease is terminated before the lease period has expired, any payments required to be made to the lessor by way of penalty are recognized as expenses in the period in which termination takes place. 2.16 Cash and balances with Central bank Cash and cash equivalents comprise balances with less than 90 days maturity from the date of acquisition, including cash and non-restricted balances with the Central bank of Montenegro (except for 50 % of obligatory reserves), and amounts held with domestic and foreign banks. Obligatory reserves Decision on Obligatory Reserves of Banks with the Central Bank of Montenegro stipulates the calculation, setting aside and usage of obligatory reserve funds with the Central Bank of Montenegro. The new Decision of the Central Bank of Montenegro on Obligatory Reserves of Banks with the Central Bank of Montenegro has been enacted in 2011, (“Official gazette of Montenegro”, no. 35/11) and it prescribes that obligatory reserve is to be calculated at the rate of 9.5% on the part of the base consisting of call and termed deposit contracted with maturity up to one year, i.e. 365 days; at the rate of 8.5% on the part of the base consisting of termed deposits with contractual maturity over one year, i.e. over 365 days. On the termed deposits with maturity over one year, i.e. over 365 days, with the clause concerning possibility of re-depositing within the period less than one year, i.e. less than 365 days, obligatory reserves are made by applying a rate of 9.5 %.

According to the Decision Amending Decision on Obligatory Reserves of Banks with the Central Bank of Montenegro (“Official gazette of Montenegro”, no. 35/11, 22/12) the banks have been given the possibility to keep up to 35% of obligatory reserves in the form of Treasury bills issued by Montenegro, as well as the possibility to use up to 50% of obligatory reserve funds when necessary for maintenance of daily liquidity. The Bank used the possibility to invest 35% of obligatory reserves into Treasury bills of Montenegro, whereas it did not use the obligatory reserve funds for maintenance of daily liquidity.

The Central Bank pays monthly interest to the Bank, which is calculated at the rate of 1% per annum on 25%, of the obligatory reserve set aside, i.e. on 15% according to the amended Decision on Obligatory Reserves f Banks with Central Bank of Montenegro. A bank that miscalculates the obligatory reserves or fails to set aside obligatory reserves within defined time period, is obliged to pay monthly interest on the determined amount of the lower obligatory reserves at the rate of 12% per annum.

NLB MONTENEGROBANKA A.D. PODGORICA Notes to the consolidated financial statements for the year ended 31 December 2012

(All amounts in thousand EUR unless otherwise stated)

20

2. Summary of significant accounting policies (continued) 2.17. Provisions Provisions are recognised when: - the Bank has a present legal or constructive obligation as a result of past events; - it is more likely than not that an outflow of resources will be required to settle the obligation and - The amount can be reliably estimated. Provisions are measured at the present value of the expenditures expected to be required to settle the obligation. Provisions are reviewed at each balance sheet date and adjusted so as to reflect the best current estimate. If it is no longer likely that an outflow of funds which generates economic benefits will be required for settlement of the liability, the provision is derecognised through the profit and loss. 2.18. Financial guarantee contracts Financial guarantee contracts are contracts that require the issuer to make specified payments to reimburse the holder for a loss it incurs because a specified debtor fails to make payments when due, in accordance with the terms of a debt instrument. Such financial guarantees are given to banks, financial institutions and other bodies on behalf of customers to secure loans, overdrafts and other banking facilities. Financial guarantees at the date of issue are recognised at fair value which is equal to the amount of the fee received. The fee is amortized to the profit and loss during the contract period using the straight-line method. The Bank’s liabilities under guarantees are subsequently measured at the greater of:

the initial measurement, less amortization calculated to recognize fee income over the period of guarantee; or

the best estimate of the expenditure required to settle the obligation. 2.19. Borrowings Borrowings are recognised initially at fair value net of transaction costs incurred. Borrowings are subsequently stated at amortised cost; any difference between proceeds net of transaction costs and the redemption value is recognised in the profit and loss over the period of the borrowings using the effective interest method. 2.20. Debt securities in issue Issued debt securities are recognized at their fair value plus transaction costs that are directly attributable to the issue of the debt securities. Issued debt securities are subsequently measured at amortised cost. Interests, discounts and premiums are recognized in the profit and loss as interest expenses deferred over their maturity period. 2.21. Employee benefits a) Pension obligations Short-term employee benefits include salaries and all contributions. Short-term employee benefits are recognized as expenses in the period in which they were incurred. The Bank and its employees are obliged to make payments to the pension fund of the Republic of Montenegro in accordance with the defined contribution plan. The Bank has no legal or constructive obligation to pay further contributions that are the obligation of the Fund. Taxes and contributions relating to contribution plans are recognized as expenses in period to which they relate to.

NLB MONTENEGROBANKA A.D. PODGORICA Notes to the consolidated financial statements for the year ended 31 December 2012

(All amounts in thousand EUR unless otherwise stated)

21

2. Summary of significant accounting policies (continued) 2.21. Employee benefits (continued) b) Retirement indemnity bonuses Total expenses for long term provisions related to the future outflows regarding retirement of employees are assessed based on actuarial calculations. For the purposes of the assessment, the Bank engages a certified actuary who performs the calculation of the present value of future liabilities by using the applicable discount rate. These obligations are measured at the present value of future cash outflows considering future salary increases and then apportioned to past and future employee service based on benefit plan terms and conditions. All gains and losses arising from changes in assumptions and experience adjustments are recognized immediately in the profit and loss. c) Termination benefits and jubilee awards Termination benefits are payable when employment is terminated, before the regular retirement date, or whenever an employee accepts voluntary redundancy in exchange for these benefits. The Bank pays jubilee awards in periods of 10, 20 and 30 years. The most important assumptions used in the actuarial calculation are: adequate discounting factor, number of employees that have right for retirement benefits, increase in salaries in accordance with inflation, promotions and salaries increase in accordance with past service. 2.22. Taxation Current income tax Income tax is calculated in accordance with the Law on Income Tax by applying the prescribed rate on the taxable income as disclosed in the Tax return. The taxable income is determined by reconciling the income disclosed in the profit and loss for certain incomes and expenses, in a manner defined by the tax regulations. The income tax expense is calculated by applying a rate of 9% on taxable income (2011: 9%). Deferred income tax Deferred income taxes are provided on temporary differences between the tax base of assets and liabilities and their carrying amounts in the financial statements of the Bank. Deferred income tax is calculated, using the balance sheet liability method, for all temporary differences arising between the tax bases of assets and liabilities and their carrying amounts for financial reporting purposes. Deferred tax assets are recognized if it is probable that future taxable profit will be available against which the temporary differences can be utilized.

Deferred tax related to fair value re-measurement of available-for-sale investments is charged or credited directly to other comprehensive income, and simultaneously recognised in the profit and loss together with the deferred gain or loss. Deferred taxes are calculated based on the 9% rate. 2.23. Share Capital Paid in share capital of the Bank is the monetary amount paid by the shareholders. The share capital of the Bank comprises ordinary shares and is recorded as a separate position within the balance sheet.

Dividends on shares are recognised in equity in the period in which their payment was approved. 2.24. Fiduciary activities The Bank manages a significant amount of assets on behalf of legal entities and individuals and charges fees for such services. These assets are not shown in the Bank’s balance sheet but details on fiduciary activities are given in note 35.

NLB MONTENEGROBANKA A.D. PODGORICA Notes to the consolidated financial statements for the year ended 31 December 2012

(All amounts in thousand EUR unless otherwise stated)

22

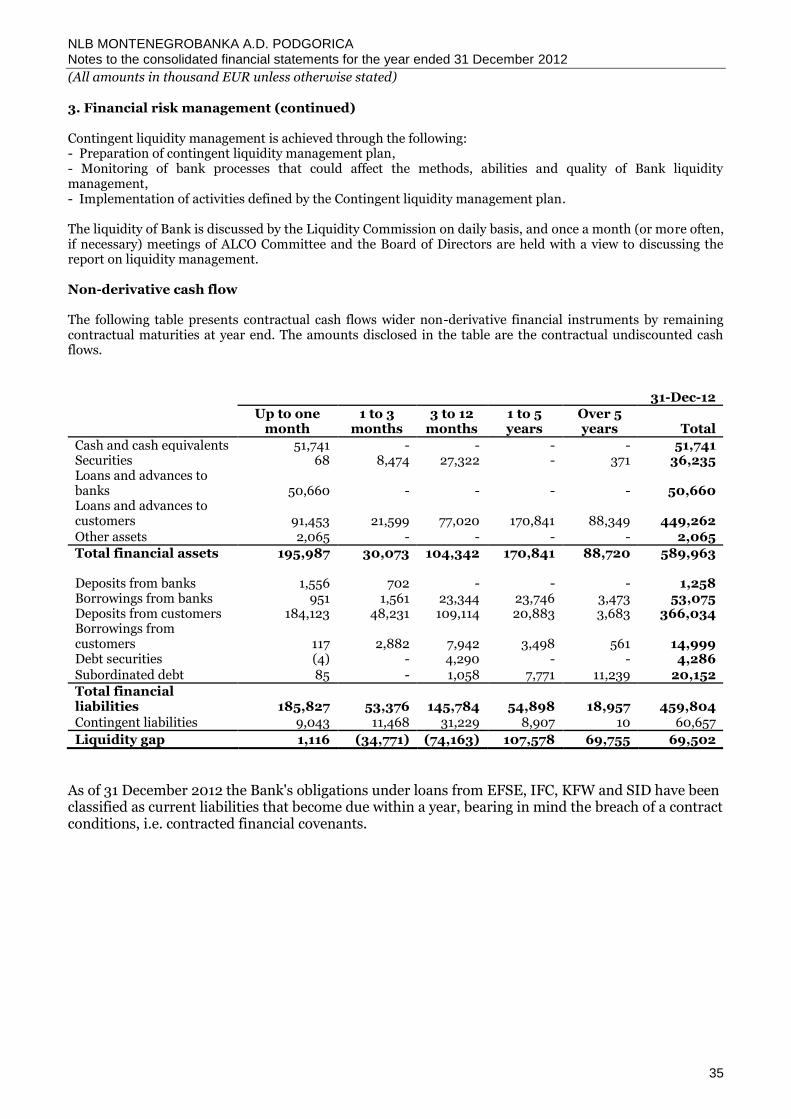

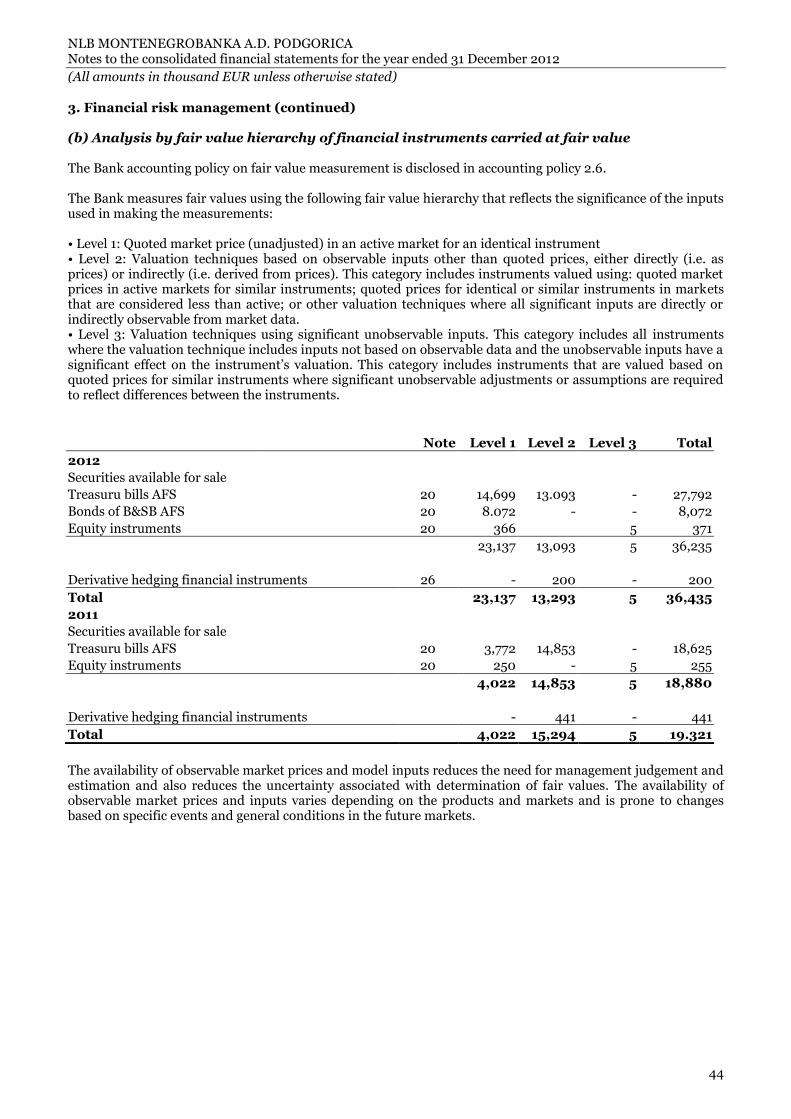

3. Financial risk management

The Bank has exposure to the following risks: • Credit risk, • liquidity risk, • market risks, • operational risks and • country risk. This note presents information about the Bank’s exposure to each of the above risks, the Bank’s objectives, policies and processes for measuring and managing risk, and the Bank’s management of capital. Risk management framework The Board of Directors has overall responsibility for the establishment and oversight of the Bank’s risk management framework. The Board has established the Asset and Liability Committee (ALCO), Credit Committees and Audit Committee. The Bank’s risk management policies are established to identify and analyze the risk faced by the Bank, to set appropriate risk limits and controls, and to monitor risks and adherence to limits. Risk management policies and systems are reviewed regularly to reflect changes in market conditions, products and services offered. The Bank’s Audit Committee is responsible for monitoring compliance with the Bank’s risk management policies and procedures, and for reviewing the adequacy of the risk management framework in relation to the risk faced by the Bank. The Bank’s Audit Committee is assisted in by Internal Audit. Internal Audit undertakes both regular and ad-hoc reviews of risk management controls and procedures, the results of which are reported to the Audit Committee. Financial risk management is based on organisational independence, high quality procedures, an appropriate system of internal controls, and is aimed at minimising risks in terms of achieving projected business and financial performance and the optimal use of capital. Risk management process in the Bank is mainly regulated by the Law on banks and other regulations of the Central bank of Montenegro. In addition, the risk management process is regulated by the internal regulations defining the aim of management, methodology and monitoring specific types of risk. Those internal regulations are adopted by the Board of Directors. Year 2012 is characterized by the extended effects of the global financial crisis. This is especially shown in the increase of insolvency, and, consequently, growth of overdue loans and non-quality assets in banks. Under these conditions the Bank continued to prepare more frequent credit analyses of materially significant clients and various types of stress scenarios. As for market risk management, the Bank had low risk exposure. In the structural liquidity segment, in accordance with the strategy of investing in debt securities, the Bank commences generating secondary liquidity reserves through investment in state bonds of the countries with the highest rating and in domestic treasury bills.

NLB MONTENEGROBANKA A.D. PODGORICA Notes to the consolidated financial statements for the year ended 31 December 2012

(All amounts in thousand EUR unless otherwise stated)

23

3. Financial risk management (continued) 3.1 Credit risk Credit risk is the risk of financial loss to the Bank if a customer or counterparty to a financial instrument fails to meet its contractual obligations, and arises principally from the Bank’s loans and advances to customers and other banks and investment debt securities. For risk management reporting purposes, the Bank considers and consolidates all elements of credit risk exposure (such as individual obligor default risk, country and sector risk). The credit portfolio of the Bank comprises the loans, securities, interest, fees, deposits and advances as well as guarantees, letters of credit, commitments and contingencies and derivatives towards corporate entities, banks, state, private entrepreneurs, individuals and other customers. Prior to granting, each placement is classified and its top limit is determined. In classification, the Bank uses internal methodology which implies a debtor’s ability to make regular payments to the Bank and other creditors. It is necessary to account for both managerial and financial abilities of debtors, quality as well as quantity information. In addition, the classification takes into consideration the previous client relationship with the Bank, the ability to provide cash flows to meet future obligations, and other relevant factors such as information on the general economic cycle, condition and prospects of the industry and debtor’s position within the industry, and the reconciliation of the purpose of the loan to a debtor’s industry. In addition to monitoring individual placements, credit risk is monitored at the level of the entire portfolio. Thus, the structure and movement of portfolio is monitored in terms of structure by types of credit, credit rating groups, by types of products, industries, and amounts of placements. Special attention is paid to transfer matrices, monitoring of overdue payments, low quality assets and monitoring of major debtors, i.e. all clients and group of associated clients with a total exposure above 10% of risk capital. The Bank calculates impairment provisions in accordance with the International Financial Reporting Standards. The provisions are calculated with regard to the risk of individual placement and existence of objective evidence of impairment, taking into consideration quality, value, and market quality of collaterals. Impairment provisions are created on a group and individual basis. Individually significant placements are assessed for impairment on an individual basis, while the remainder of the credit portfolio is assessed collectively. Individually significant placements are placements with: • Banks • All placements in A, B and C category whose exposure is over EUR 200,000 • All placements in D and E category whose exposure is over EUR 10,000 • Retail clients with exposure exceeding EUR 500,000 a) Derivatives The Bank maintains strict control limits on net open derivative positions, i.e. the difference between purchase and sale contracts, both by amount and term. The Bank mainly concludes currency and interest rate derivative contracts for the purposes of hedging the positions within the Bank’s book. The amount subject to credit risk is limited to the recoverable credit value of instruments, defined by the statute. This credit risk exposure is monitored and managed as part of the overall lending limits with customers, together with potential exposures from market movements. b) Credit-related commitments Credit-related commitments are instruments which ensure that funds are available to a customer as required. Guarantees and commercial letters of credit – which are written undertakings by the Bank on behalf of a customer authorising a third party to draw drafts on the Bank up to a stipulated amount in case of default of the Client - carry the same credit risk as loans. With respect to credit risk on commitments to extend credit, the Bank is potentially exposed to loss in an amount equal to the unused commitments. However, the likely amount of loss is less than the total unused commitments, as most commitments to extend credit are contingent upon customers maintaining specific credit standards. The Bank monitors the term to maturity of credit commitments because a longer term period generally implies a greater degree of credit risk.

NLB MONTENEGROBANKA A.D. PODGORICA Notes to the consolidated financial statements for the year ended 31 December 2012

(All amounts in thousand EUR unless otherwise stated)

24

3. Financial risk management (continued) 3.1 Credit risk (continued) c) Internal rating system

31 December 2012 31 December 2011

Loans and advances %

Impairment provisions%

Loans and advances %

Impairment provisions%

A 38.72% 0.97% 40.96% 2.62% B 18.26% 2.49% 27.63% 7.52% C 13.28% 11.37% 16.36% 31.39% D+E 29.74% 85.17% 15.05% 58.48% Total 100.00% 100.00% 100.00% 100.00%

A credit rating reflects the credit quality of a customer, whose exposure derives from a financial instrument. An “A” credit rating is given to first-class customers, who are not expected to encounter difficulties in repaying their obligations. A credit rating of “B” indicates customers with a slightly worse financial position, which is temporary in nature and does not indicate difficulties in repaying obligations. A credit rating of “C” indicates customers who are undercapitalized and highly indebted, or those customers that generally do not generate sufficient cash flows to repay their obligations, and so thus may pay their obligations in arrears. Credit ratings of “D” and “E” indicate customers with evident financial difficulties, or those who are in the process of compulsory settlement or bankruptcy. It is expected that these clients will not be able to repay most or even any of their obligations from their operating cash-flow. Customers with a “C” credit rating or worse must provide additional collateral to cover their exposure in the amount of credit replacement value. Maximum credit risk exposure

31. December 2012

Gross maximum

exposure Impairment

provision

Net maximum

exposure Loans and advances to banks 50,660 - 50,660

Loans and advances to clients

Loans to government 7,903 (343) 7,560

Loans to financial organisations 1,667 (16) 1,651 Loans to individuals 175,961 (18,656) 157,305 Credit line 1,098 (426) 672 Credit cards 8,781 (1,668) 7,113 Housing loans 114,971 (10,845) 104,126 Consumer loans 50,534 (5,624) 44,910 Other loans to individuals 577 (93) 484 Loans to legal entities 251,100 (53,018) 198,082 Loans to small and medium entities 243,317 (51,499) 191,818 Loans to large entities 7,783 (1,519) 6,264

Total loans and advances to clients 436,631 (72,033) 364,598

Government securities 35,864 - 35,864 Other assets 1,801 (959) 842 Contingent liabilities 60,657 (1,311) 59,346 Letters of credit 5,531 - 5,531 Short-term guarantees 41,904 (1,311) Long-term guarantees 6,552 47,145 Other commitments and contingencies 6,670 - 6,670 TOTAL 585,613 (74,303) 511,310

NLB MONTENEGROBANKA A.D. PODGORICA Notes to the consolidated financial statements for the year ended 31 December 2012

(All amounts in thousand EUR unless otherwise stated)

25

3. Financial risk management (continued) 3.1 Credit risk (continued)

31. December 2011

Gross maximum

exposure Impairment

provision

Net maximum

exposure Loans and advances to banks 32,485 - 32,485

Loans and advances to clients

Loans to government 8,116 (224) 7,892 Loans to individuals 182,528 (15,547) 166,981 Credit line 1,242 (338) 904 Credit cards 9,141 (1,181) 7,960 Housing loans 119,450 (8,866) 110,584 Consumer loans 51,983 (5,066) 46,917 Other loans to individuals 712 (96) 616 Loans to legal entities 269,022 (28,823) 240,199 Loans to small and medium entities 260,868 (28,769) 232,099 Loans to large entities 237 (1) 236 Loans to financial organisations 7,917 (53) 7,864 Total loans and advances to clients 459,666 (44,594) 415,072

Government securities 18,625 - 18,625 Other assets 1,496 (896) 600 Contingent liabilities 85,756 (1,149) 84,607 Letters of credit 4,400 (6) 4,394 Short-term guarantees 33,708 (494) 33,214 Long-term guarantees 30,797 (641) 30,156 Other commitments and contingencies 16,851 (8) 16,843 TOTAL 598,028 (46,639) 551,389

The maximum exposure represents a worst case scenario of credit risk exposure, which is the maximum possible loss without taking account of any collateral held. For on-balance-sheet assets, the exposures set out above are based on net carrying amounts as reported in the balance sheet and on nominal amounts of receivables for off-balance sheet items.

NLB MONTENEGROBANKA A.D. PODGORICA Notes to the consolidated financial statements for the year ended 31 December 2012

(All amounts in thousand EUR unless otherwise stated)

26

3. Financial risk management (continued) 3.1 Credit risk (continued) Loans and other financial assets that are neither past due nor impaired and group net impaired loans and other financial assets for A and B clients who are not past due

2012

A B C D + E Total

Loans to banks 50,629 31

50,660

Loans to clients

Loans to financial organisations 856 74

930

Loans to government

2,332

2,332

Loans to individuals 107,518 6,269

2 113,789

Credit line 559 11

570

Credit cards 6,281 175

6,456

Housing loans 69,450 4,713

74,163

Consumer loans 30,926 1,371

2 32,298

Other loans to individuals 302

302

Loans to legal entities 10,550 45,360 527 29 56,466

Loans to small and medium entities 10,550 45,358 527 29 56,464

Loans to large entities

2

2

Total loans and advances to clients 118,924 54,035 527 31 173,517

Other assets 655 39

704

Total 170,208 54,105 527 31 224,881

2011

A B C D + E Total

Loans to banks 32,212 273

32,485

Loans to clients

Loans to government 0 1,768 13 0 1,781

Loans to individuals 115,614 6,976 21 53 122,664

Credit line 742 25 3 49 819

Credit cards 6,802 250 17 4 7,073

Housing loans 74,477 4,010 -

-

78,487

Consumer loans 33,209 2,691 1

35,901

Other loans to individuals 384

384

Loans to legal entities 27,732 56,660 1,182 142 85,716

Loans to small and medium entities 20,732 55,756 1,182 142 77,812

Loans to large entities

2

2

Loans to financial organisations 7,000 902

-

- 7,902

Total loans and advances to clients 143,346 65,404 1,216 195 210,161

Financial instruments available for sale 18,625

18,625

Other assets 545 18 2 8 573

Total 194,728 65,695 1,218 203 261,844

NLB MONTENEGROBANKA A.D. PODGORICA Notes to the consolidated financial statements for the year ended 31 December 2012

(All amounts in thousand EUR unless otherwise stated)

27

3. Financial risk management (continued) 3.1 Credit risk (continued) Loans and other financial assets that are past due and not impaired and group net impaired loans and other financial assets for A and B clients who are past due

31. December 2012 Up to 30 days Up to 90 days Over 90 days Total

Loans to banks - - - -

Loans to government 3 - - 3

Loans to financial organisations -

692 -

692

Loans to individuals 20,517 10,675 173 31,365

Credit line 33 13 47 93

Credit cards - 343 101 444

Housing loans 15,070 8,362 - 23,432

Consumer loans 5,414 1,957 25 7,396

Other loans to individuals - - - -

Loans to legal entities 12,739 7,249 - 19,988

Loans to small and medium entities 11,620 6,389 - 18,009

Loans to large entities 1,119 860 - 1,979

Total loans and advances to clients 33,259 18,616 173 52,048

Other assets 10 1 43 54

Total 33,269 18,617 216 52,102

31. December 2011 Up to 30 days

Up to 90 days

Over 90 days Total

Loans to banks 0 0 0 0

Loans to government 3,234 462 0 3,696