nhs - payment by results · nhs payment by results ... four pronged approach to reform. this...

TRANSCRIPT

NHS Payment by results Topic Gateway Series

NHS payment by results Topic Gateway Series No. 41

1

Prepared by Liz Murby and Technical Information Service November 2007

NHS Payment by results Topic Gateway Series

About Topic Gateways

Topic Gateways are intended as a refresher or introduction to topics of interest

to CIMA members. They include a basic definition, a brief overview and a fuller

explanation of practical application. Finally they signpost some further resources

for detailed understanding and research.

Topic Gateways are available electronically to CIMA members only in the CPD

Centre on the CIMA website, along with a number of electronic resources.

About the Technical Information Service

CIMA supports its members and students with its Technical Information Service

(TIS) for their work and CPD needs.

Our information and accounting specialists work closely together to identify or

create authoritative resources to help members resolve their work related

information needs. Additionally, our accounting specialists can help CIMA

members and students with the interpretation of guidance on financial reporting,

financial management and performance management, as defined in the CIMA

Official Terminology 2005 edition.

CIMA members and students should sign into My CIMA to access these services

and resources.

The Chartered Institute of Management Accountants 26 Chapter Street

London SW1P 4NP

United Kingdom

2

T. +44 (0)20 7663 5441 F. +44 (0)20 7663 5442 E. [email protected] www.cimaglobal.com

NHS Payment by results Topic Gateway Series

3

Definition

‘Payment by results’ (PbR) is the name of the current funding flows mechanism

employed in the UK NHS. It is defined by the Department of Health in the

following statement of intent:

‘The aim of payment by results is to provide a transparent, rules based system for

paying trusts. It will reward efficiency, support patient choice and diversity, and

encourage activity for sustainable waiting time reductions.

Payment will be linked to activity and adjusted for case mix. Importantly, this

system will ensure a fair and consistent basis for hospital funding rather than

being reliant, principally, on historic budgets and the negotiating skills of

individual managers.’

Context PbR is a sector specific funding flows mechanism, although similar systems exist

in some other developed health economies. For this reason students are unlikely

to study this specific topic.

However, the topic has associations with the current CIMA syllabus. CIMA

students will learn and may be examined on this topic in paper P1, Management

Accounting Performance Evaluation, chapter 8, Developments in Management

Accounting and paper P2, Management Accounting Decision Management,

Chapter 10, Activity-based approaches.

Overview

PbR is part of the NHS reforms initiated by the NHS Plan (2000) which set out a

four pronged approach to reform. This approach has been described as a 'supply

side' and a 'demand side' reform programme.

A 2003 consultation (Payment by results: preparing for 2005) on the technical

aspects of payment by results, identified four principle policy directions that PbR

was intended to underpin.

Devolution: the belief that important decisions should be taken as close to the

patient as possible, within a national framework of standards and accountability.

Choice: the belief that patients should be able to take key decisions about the

care they receive from the NHS.

NHS Payment by results Topic Gateway Series

4

Plurality: the belief in a 'mixed' economy of public and private sector healthcare

provision. Over the last several years there has been a growth in independent

sector hospital provision in England. PbR makes the price of each procedure

transparent to all.

Investment: NHS investment is made on the basis that the NHS must spend the

money wisely and efficiently. The national tariff is the 'new' basis of NHS funding

and provides a series of benchmarks against which relative costs can be

measured.

Background and history Information setting out the recent history behind the development of the PbR

framework is found on the Department of Health website. www.dh.gov.uk

[Accessed 12 March 2008]

The NHS plan, together with Delivering the NHS plan, sets out a major

programme of NHS investment, expansion and reform over a ten year period.

Consequently, the PbR initiative is being implemented incrementally, in terms of

both scope and financial impact.

In terms of scope, PbR began in a small way in 2003-04 and was extended in

2004-05. For the majority of NHS Trusts, PbR included only elective care in

2005-06. The following year, PbR was extended to include non-elective, accident

and emergency, outpatient and emergency admissions for all Trusts.

2007-08 marked a year of consolidation with no significant changes to the tariff.

The financial impact of PbR was also introduced gradually with a four year

transition path, which comes to a close in 2008-09.

The relevant consultation processes governing these changes are outlined below.

Consultations and policy developments post 2000 In July 2000, the NHS plan introduced the government’s intention to link the

allocation of hospital funds to the activity undertaken by hospitals.

www.dh.gov.uk

[Accessed 12 March 2008]

In order to optimise extra resources, the government proposed major changes to

the way money flows around the NHS. The plan also included differentiation

between incentives for routine surgery and those for emergency admissions.

Hospitals would be paid for the elective activity they undertake, a system of

payment by results.

NHS Payment by results Topic Gateway Series

5

In November 2002, the government issued a response to the consultation paper,

'Reforming financial flows: payment by results', on plans for the introduction of

PbR. http://digbig.com/4wxqx

[Accessed 19 May 2008]

In August 2003, the government issued the consultation paper Payment by

results: preparing for 2005. This identified the key decisions needed for

implementing the next stage of PbR. It outlined how PbR will apply to NHS

foundation trusts from April 2004 and to all NHS trusts from April 2005.

Feedback was sought on the proposed approaches. http://digbig.com/4wxqy

[Accessed 19 May 2008]

Key elements of payment by results 1. The national tariff

The national tariff is the inflation adjusted national average cost of procedure.

It comprises three components:

• a definition (the healthcare resource group or HRG, backed up by detailed

clinical definition)

• a currency (the time spent in hospital, from admission to discharge)

• a financial sum (based on the NHS defined 'average' cost).

2. Healthcare resource groups (HRGs)

HRGs are a standard method of analysing clinical procedures and hospital

activity, based upon diagnosis and any interventions.

http://digbig.com/4wxra

[Accessed 19 May 2008]

3. The market forces factor (MFF)

The MFF is an adjustment to the tariff that reflects the different costs of

healthcare provision in different parts of the country.

It was developed to adjust the unavoidable variations in input costs, for

example, staff costs, regional weighting, land, buildings and equipment in

health care delivery.

NHS Payment by results Topic Gateway Series

6

4. NHS reference costs

NHS reference costs are an analysis of each HRG's spending at the end of the

financial year. They are a standardised presentation of the costs of NHS

services, prepared and published annually. http://digbig.com/4wxrb

[Accessed 19 May 2008]

The underlying intention of reference costs publication is to allow cost

comparisons between services through the use of a consistent approach to

costing.

Differences between reference costs and the tariff arise from:

• the effects of time related inflation, data collection and other adjustments

• a variation in the scope of each.

Application

How payment by results works 1. Tariff for hospital in-patient procedure

For each HRG, the Department of Health publishes tariffs (prices) for urgent

and non-urgent ‘spells’ (a ‘spell’ refers to time spent in hospital from

admission to discharge).

The tariff is based upon the inflation-adjusted national average NHS cost of

the procedure in question.

The prices are derived from Department of Health ‘reference costs’, which use

the cost information provided by all NHS providers as part of their annual

reference costs submission. They reflect the actual (rather than budgeted) cost

of procedures, and should ensure full recovery of all relevant support

functions and overhead costs.

2. Regional adjustment

This is an adjustment to the price, to reflect the fact that the cost of running a

hospital varies from one part of the country to another. This is known as the

MFF.

3. Income calculation

The price multiplied by the MFF represents the amount of income an NHS

Trust can expect to receive for each procedure it undertakes.

NHS Payment by results Topic Gateway Series

7

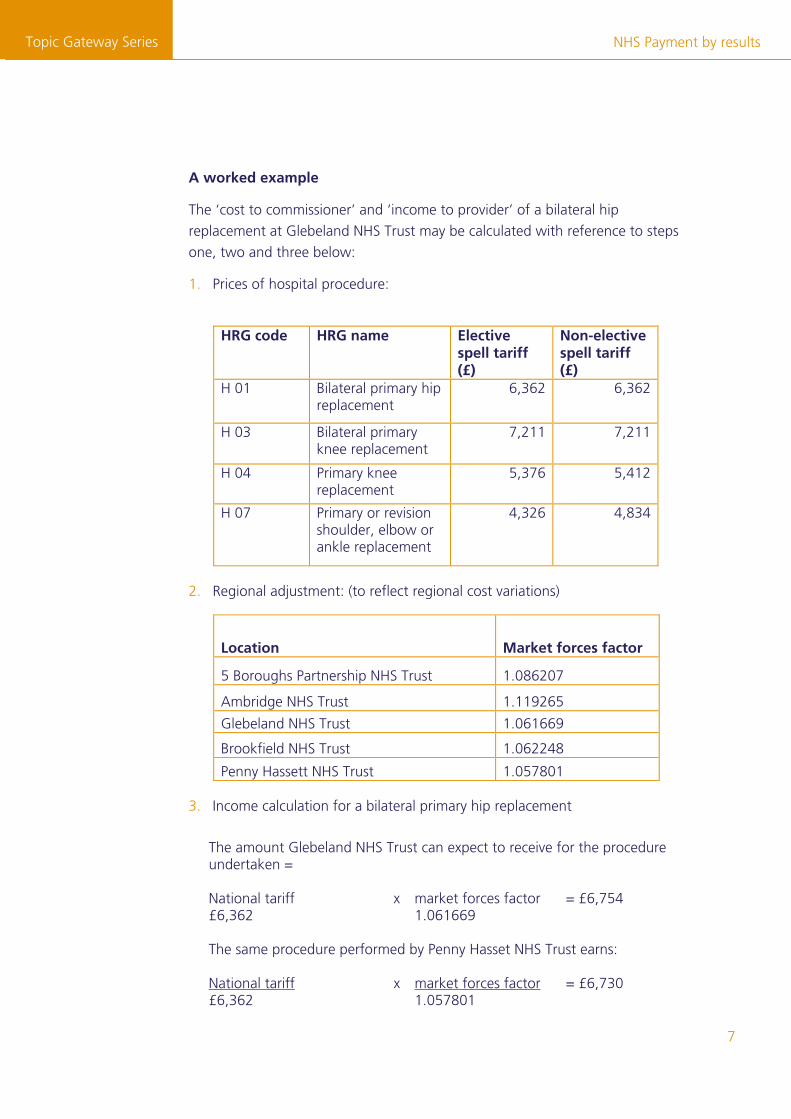

A worked example

The ‘cost to commissioner’ and ‘income to provider’ of a bilateral hip

replacement at Glebeland NHS Trust may be calculated with reference to steps

one, two and three below:

1. Prices of hospital procedure:

HRG code HRG name Elective

spell tariff (£)

Non-elective spell tariff (£)

H 01 Bilateral primary hip replacement

6,362 6,362

H 03 Bilateral primary knee replacement

7,211 7,211

H 04 Primary knee replacement

5,376 5,412

H 07 Primary or revision shoulder, elbow or ankle replacement

4,326 4,834

2. Regional adjustment: (to reflect regional cost variations)

Location Market forces factor

5 Boroughs Partnership NHS Trust 1.086207

Ambridge NHS Trust 1.119265

Glebeland NHS Trust 1.061669

Brookfield NHS Trust 1.062248

Penny Hassett NHS Trust 1.057801

3. Income calculation for a bilateral primary hip replacement

The amount Glebeland NHS Trust can expect to receive for the procedure undertaken = National tariff x market forces factor = £6,754 £6,362 1.061669 The same procedure performed by Penny Hasset NHS Trust earns: National tariff x market forces factor = £6,730 £6,362 1.057801

NHS Payment by results Topic Gateway Series

8

Under PbR, a basic premise is the application of the national tariff and therefore

the ‘cost to commissioner’ is the same regardless of the provider used. The actual

income received by the provider may be different due to the top-up provided in

the form of the MFF, which is paid to providers by the Department of Health.

Related tools and techniques The primary objective of PbR is the delivery of optimal efficiency in health service

provision by NHS organisations.

A range of topic gateways providing guidance and information relevant to

management accounting is available to CIMA members. Those topic gateways,

which may be of particular interest and value for those operating under a PbR

regime, include:

• activity based costing and management (ABC/ABM)

• planning and forecasting.

Other helpful tools and approaches include:

• target costing

• value analysis

• value engineering

• just-in-time (JIT)

• total quality management (TQM)

• materials requirements planning (MRP)

• kaizen

• lean manufacturing

• cause-effect analysis (‘fishbone’ diagrams).

The topic gateways are available from www.cimaglobal.com/mycima [Accessed 12 March 2008]

NHS Payment by results Topic Gateway Series

9

Further information

Articles

Banham, R. Off target? CFO Magazine, May 2000, Volume 16, Issue 6,

pp 127-130

Bayou, M. and Reinstein, A. Three routes for target costing. Managerial Finance,

1998, Volume 24, Number 1, pp 28-45

Chen, R.C. and Chung, C.H. Cause-effect analysis for target costing. Accounting

Quarterly, Winter 2002, Volume 3, Issue 2, pp 1-9

Cooper, R. and Chew, W. B. Control tomorrow’s costs through today’s designs. Harvard Business Review, January-February 1996, Volume 74, Issue 1, pp 88-97

Davila, A. and Wouters, M. Designing cost-competitive technology products

through cost management. Accounting Horizons, 2004, Volume 18, Issue 1, pp

13-26

Ellwood, S. The NHS financial manager in 2010. Public Money and Management,

January-March 2000, Volume 20, Issue 1, pp 23-30

Ellwood, S. Full-cost pricing rules within the National Health Service internal

market: accounting choices and the achievement of productive efficiency.

Management Accounting Research, 1996, Volume 7, pp 25-51

Gagne, M. L. and Discenza, R. Target costing. Journal of Business and Industrial

Marketing, 1995, Volume 10, Issue 1, pp 16-22

Jackson, A. and Lapsley, I. The diffusion of accounting practices in the new

‘managerial’ public sector. International Journal of Public Sector Management,

2003, Volume 16, Number 5, pp 359-372

Lockamy, A. and Smith, W. Target costing for supply chain management: criteria

and selection. Industrial Management and Data Systems, 2000, Volume 100,

Numbers 5-6, pp 210-218

Sakurai, M. Target costing and how to use it. Journal of Cost Management for

the Manufacturing Industry, Summer 1989, Volume 3, Number 2, pp 39-50

Spear, S. Fixing healthcare from the inside, today. Harvard Business Review,

September 2005, Volume 83, Issue 11, p. 162

NHS Payment by results Topic Gateway Series

10

Swenson, D. et al. Best practices in target costing. Management Accounting

Quarterly, Winter 2003, Volume 4, Issue 2, pp 12-17

Tinkler, M. and Dubé, D. Strength in numbers. CMA Management, September

2002, Volume 76, Issue 6, pp 14-17

Books (2005). CIMA Official Terminology. Oxford: CIMA Publishing

CIMA research Bourn and Sutcliffe. (eds). (1996). Management accounting in healthcare. London: CIMA

Ellwood, S. (1996). Cost-based pricing in the NHS internal market. CIMA

Research Studies. London: CIMA

Northcott, D. and Llewellyn, S. (2004). Decision making in health care: exploring

cost variability. CIMA Research Executive Summary. Available from:

www.cimaglobal.com/researchexecsummaries [Accessed 12 March 2008]

Other research (2005). NHS Costing Manual. Department of Health http://digbig.com/4wxrc

[Accessed 19 May 2008]

(2005). Financial management in the NHS: NHS (England) summarised accounts

2003-04. National Audit Office and Audit Commission

(2004). Achieving first-class financial management in the NHS: a sound basis for

better healthcare. Audit Commission. www.audit-commission.gov.uk

[Accessed 12 March 2008]

(1999). Target costing for effective cost management: product cost planning at

Toyota Australia. IFAC Financial and Management Accounting Committee

Websites The Audit Commission www.audit-commission.gov.uk

[Accessed 12 March 2008]

Specific pages of interest include Payment by Results.

NHS Payment by results Topic Gateway Series

11

Chartered Institute of Management Accountants (CIMA)

www.cimaglobal.com [Accessed 12 March 2008]

Connecting for Health Supports the NHS to deliver better, safer care to patients, via new computer

systems and services, that link GPs and community services to hospitals.

http://digbig.com/4wxrd

[Accessed 19 May 2008]

UK Department of Health www.dh.gov.uk/en/index.htm [Accessed 12 March 2008]

Specific pages of interest are:

Payment by Results http://digbig.com/4wxre [Accessed 19 May 2008]

BMA - Caring for the NHS http://digbig.com/4wxrf [Accessed 19 May 2008]

Health Matters Health Matters is an independent non-profit UK magazine covering the NHS,

public health and health politics. www.healthmatters.org.uk

[Accessed 12 March 2008]

Healthcare Resource Groups: Casemix

The Casemix Service develops clinical grouping methodologies and software

products that enable the NHS to record clinical activity.

http://digbig.com/4wxrh

[Accessed 19 May 2008]

Healthcareworkforce.nhs.uk

Provides one stop access to NHS healthcare workforce planning information,

knowledge, intelligence and practical tools.

www.healthcareworkforce.nhs.uk

[Accessed 12 March 2008]

The King’s Fund

The King's Fund is an independent charitable foundation working for better

health, especially in London. www.kingsfund.org.uk/index.html [Accessed 12 March 2008]

NHS Payment by results Topic Gateway Series

[Accessed 12 March 2008]

NHS Costing Manual

Sets out the principles and practice of costing to be applied in the NHS.

http://digbig.com/4wxrj [Accessed 19 May 2008]

NHS Networks

Promotes and connects the many networks which exist throughout the

NHS, and encourages the formation of new ones.

www.networks.nhs.uk/1.php

[Accessed 12 March 2008]

Office of Health Economics

Provides independent research, advisory and consultancy services on

policy implications and economic issues within the pharmaceutical,

health care and biotechnology sectors.

www.ohe.org/page/index.cfm

[Accessed 12 March 2008]

12

No responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this publication can be accepted by the authors or the publishers.

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means method or device, electronic (whether now or hereafter known or developed), mechanical, photocopying, recorded or otherwise, without the prior permission of the publishers.

Permission requests should be submitted to CIMA at [email protected]

Copyright ©CIMA 2006

First published in 2006 by:

The Chartered Institute of Management Accountants 26 Chapter Street London SW1P 4NP United Kingdom

Printed in Great Britain