new pff master presentation final 2.ppt - read-only ... · brand reputation brand is the unique...

TRANSCRIPT

2

John D’AgostinoManaging Director, DMS Governance

3

Good Morning

What We Will Talk About

4

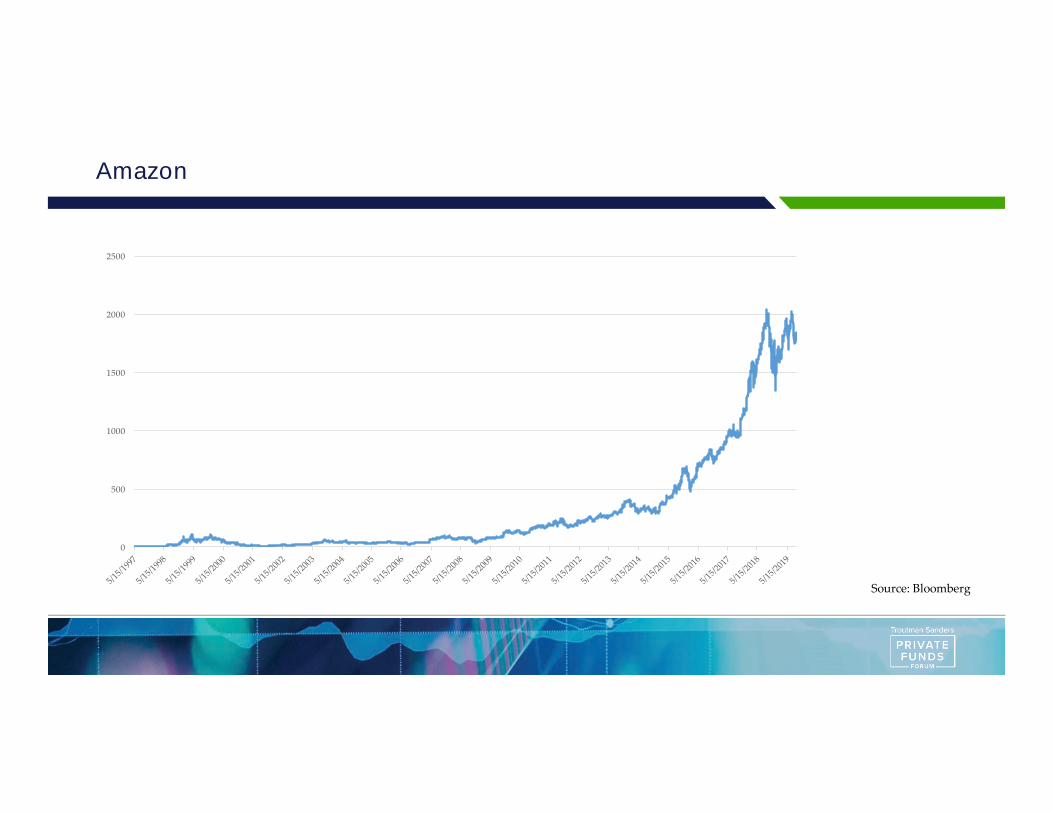

Bubbles

Digital Assets, BlockChain and AI

Trends

Keys To Success

5

1. Credentialize

2. Say Something Benignly Provocative

3. Make audience gasp/smile

4. Walk back #2

5. Bask In Glory

Bubbles are Good

6

Stanford’s Peter Koudijs says a bubble is:

“where investors buy an asset not for its

fundamental value, but because they plan to

resell, at a higher price, to the next investor.”

Primary Rules of Asset Bubbles

7

Perspective determines characterization.

• “Bubble” vs volatile asset

Impact determines response.

• Productive vs inert

• Who is harmed?

Bubble?

8

1000

1200

1400

1600

1800

2000

2200

Source: Bloomberg

Amazon

9

0

500

1000

1500

2000

2500

Source: Bloomberg

Bubbles Produce Fat Tails

10

Source for Failure Rate: Investment cycles and startup innovation. Ramana Nandan; Matthew Rhodes-Kropf, Harvard Business School, Harvard University, United States

-236%

21% 20%

-250%

-200%

-150%

-100%

-50%

0%

50%

Failure Patents Revenue

11

Practical FintechA cynically enthusiastic approach

Who You Should Listen To:

12

Hype Cycle

13

Self Fulfilling

14

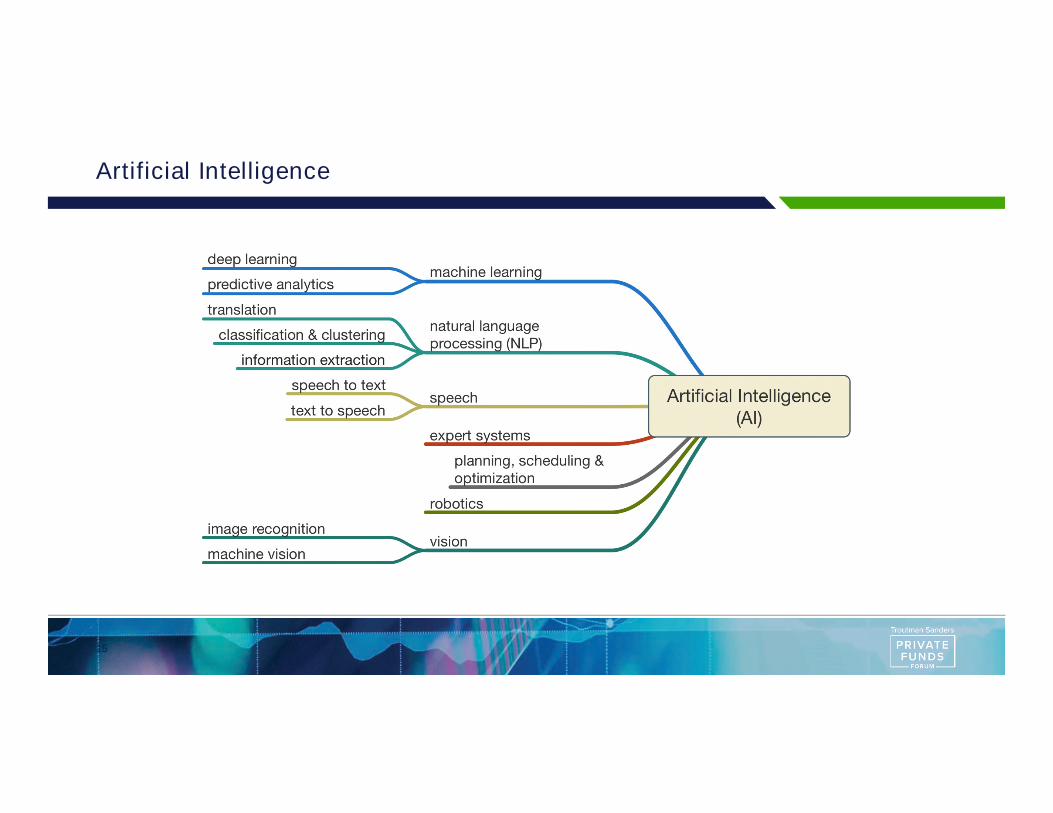

Artificial Intelligence

15

AI Tells

16

Long term prediction

Small Data

No manual intervention

Blockchain

17

Blockchain Tells

18

Public v Private

“The Blockchain” vs “A” Blockchain

Scalability vs Security

51% is “no big deal”

19

Trends

Banking Problem

20

Personal Savings Rate

Banking Solution

21

Random Guess Academic Affiliation Social Media Our Method (SocPhys)

215+% better at behavior prediction than social media driven models

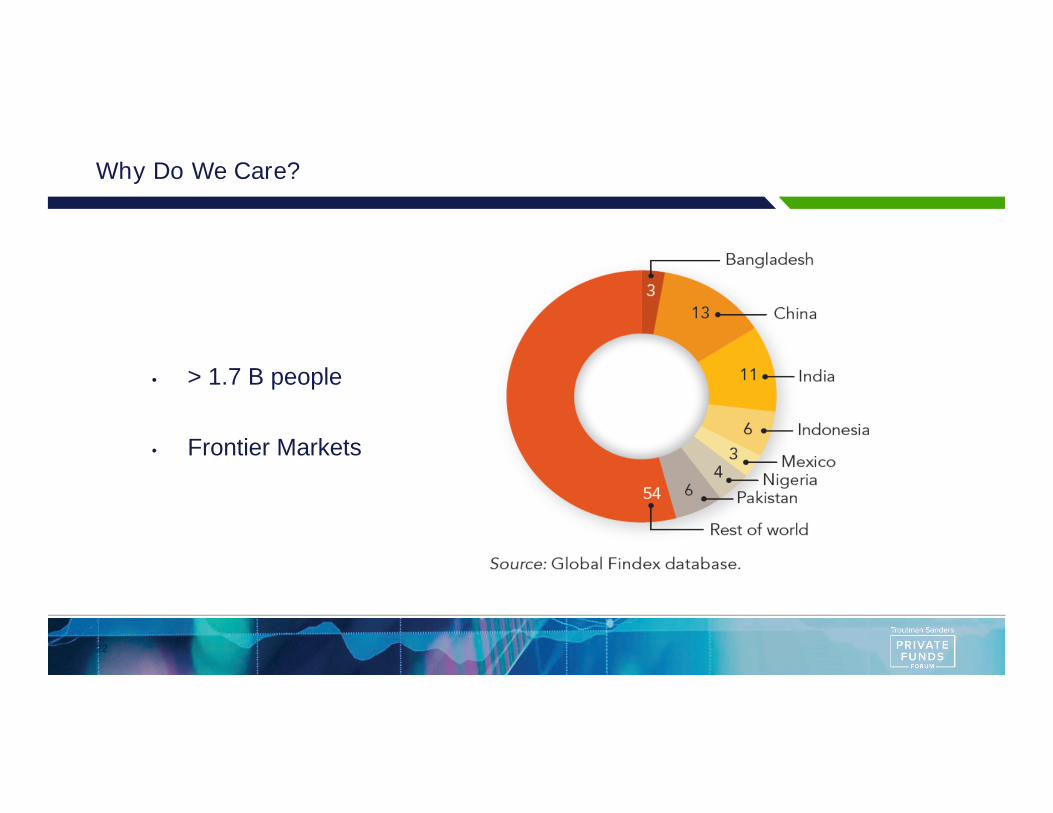

Why Do We Care?

22

• > 1.7 B people

• Frontier Markets

Cost To Acquire

23

Libra

24

Facebook, the popular American social media platform, unveils its ambitious plans to launch Libra, a digital cryptocurrency, which will allow its billions of users to indulge in financial transactions across the globe.

• Blockchain: Libra

• Wallet: Calibra

• Programming language: Move

Why Is This So Important?

25

Asset Management: Fractionalization of Traditional Assets

26

Asset Management: Fractionalization of New Assets

27

Skins

28

Trends in Investor Due Diligence –Allocators and the Dawn of OCIOs8:45 a.m. – 9:45 a.m.

Amanda Tepper, Founder and CEOChestnut Advisory

Moderator

Panelists

Marcia NelsonManaging DirectorAlberleen Family Office Solutions

Alena KarrConsultant, Formerly, Head of Operational Due Diligence Northern Trust Asset Management

Maura HarrisDirector of Due DiligenceBostwick Capital

Moderator

Panelists

Privacy and Information Security10:00 a.m. – 11:00 a.m.

Wynter Deagle, PartnerTroutman Sanders

Charles Daly. ESQ, PartnerConstellation Advisers

Monique S. Botkin, Associate General CounselInvestment Adviser Association

Chris Haley, Legal Technology DirectorTroutman Sanders eMerge

John Araneo, General Counsel & Managing DirectorAlign Cybersecurity

John O’Neill, Director and Senior Counsel AMG

CLE Credit Provided

Moderator

Panelists

Emerging Managers and Capital Raising11:15 a.m. – 12:15 p.m.

Paul Steffens, PartnerTroutman Sanders

Chrystalle H. Anstett, Co-Head of Private CreditEaton Partners

Hayden Isbister, Managing Partner & Head of Corporate PracticeCayman Islands Office, Mourant

Kathy Kohler, Senior PartnerLumentus

Spring Hollis, Founding MemberStar Strong Capital

Jilbert El-Zmetr, Head of MPS Operations, Director of Business DevelopmentSiepe

Troutman Sanders Private Funds Forum

State of the Fundraising MarketSeptember 26, 2019

COMPETITION IS UP

EATON PARTNERS 36

RECORD NUMBER OF FUNDS IN MARKET – 5,514 TARGETING $1.5 TRILLION

PRIVATE CAPITAL FUNDS IN MARKET: 2010-2019 YTD

Source: Preqin Pro

COMMITMENTS ARE DOWN

EATON PARTNERS 37

PRIVATE CAPITAL FUNDRAISING PEAKED IN 2017 AND IS NOW DECLINING

PRIVATE CAPITAL HISTORICAL FUNDRAISING, 2004-2019 YTD

Source: Preqin Pro

CAPITAL CONSOLIDATION IS UP

EATON PARTNERS 38

COMMITMENTS CONTINUE TO GO INTO THE HANDS OF FEWER MANAGERS:

Number of Funds Closed Since 2015 :

2015: 2817

2016: 2944

2017: 2816

2018: 2263

2019 YTD : 822

Source: Preqin Pro

WHAT’S HOT?

EATON PARTNERS 39

Cell Towers

Aircraft Leasing

Sustainable Agriculture

Shipping

Cyber Security

Litigation Finance

Lower Middle Market Buyout

Sector-focused Credit

Social Impact (ESG)Healthcare

Distressed Trigger Funds

Digital Infrastructure

Asset-based Lending

Cannabis

Opportunity Zones

Life Settlements

Uncorrelated / Niche

OPEN-ENDED SALES CYCLE

EATON PARTNERS 40

WHAT DOES IT TAKE TO RAISE $1 BILLION?

2,058 (Total)/801 (Qualified)

7,481

439

1

Investors Contacted

Calls Made

Capital Raised ($,BN)

Meetings Held

Source: Eaton Partners.

OPEN-ENDED SALES CYCLE

Time to Commitment

(Months)Emails Phone Calls Meetings

Average 14 76 23 5

Shortest Time to Ticket 7 36 6 2

Longest Time to Ticket 33 85 51 3

TOTAL TOUCH POINTS FROM INITIAL CONTACT TO ALLOCATION

EATON PARTNERS 41

Source: Eaton Partners.

OPEN-ENDED SALES CYCLE

EATON PARTNERS 42

FULLY ONE-THIRD OF COMMITTED INVESTORS INITIALLY DECLINE

Source: Eaton Partners.

33%

8% 25%Initially Said

NoTook a first

meeting, then said No

21 Months 16 Months

CLOSED-END SALES CYCLE: FUND I

EATON PARTNERS 43

WHAT DOES IT TAKE TO HIT THE TARGET?

1,650 (Total) /1,066 (Qualified)

2,567

274

$600m

Source: Eaton Partners.

Investors Contacted

Calls Made

Capital Raised ($)

Meetings Held

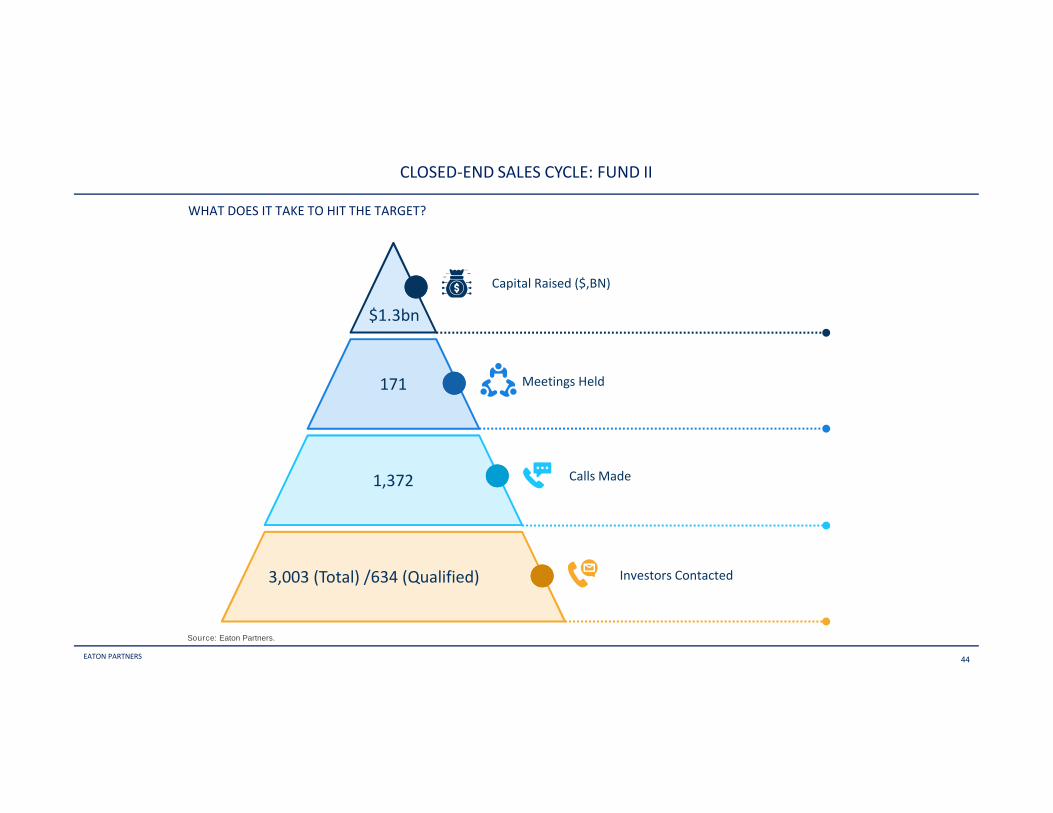

CLOSED-END SALES CYCLE: FUND II

EATON PARTNERS 44

WHAT DOES IT TAKE TO HIT THE TARGET?

3,003 (Total) /634 (Qualified)

1,372

171

$1.3bn

Source: Eaton Partners.

Investors Contacted

Calls Made

Capital Raised ($,BN)

Meetings Held

Moderator

Panelists

Emerging Managers and Capital Raising11:15 a.m. – 12:15 p.m.

Paul Steffens, PartnerTroutman Sanders

Chrystalle H. Anstett, Co-Head of Private CreditEaton Partners

Hayden Isbister, Managing Partner & Head of Corporate PracticeCayman Islands Office, Mourant

Kathy Kohler, Senior PartnerLumentus

Spring Hollis, Founding MemberStar Strong Capital

Jilbert El-Zmetr, Head of MPS Operations, Director of Business DevelopmentSiepe

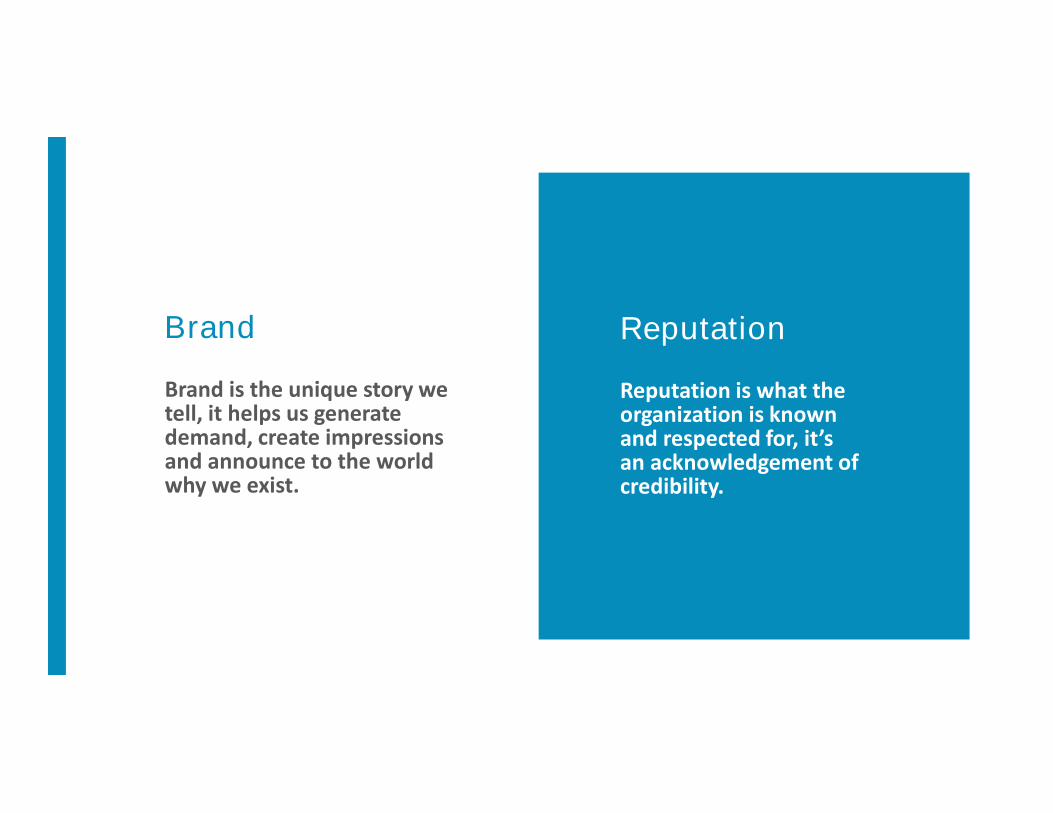

Brand Reputation

Brand is the unique story we tell, it helps us generate demand, create impressions and announce to the world why we exist.

Reputation is what the organization is known and respected for, it’s an acknowledgement of credibility.

Reputation &

Brand

Performance Quality Content

Key drivers of asset growth

Referrals, word of mouth, those that know you

Google builds reputations

Building reputations

Google by the numbers

5.6 billionsearches per day worldwide

92%

34% of users don’t click any links in results

of users click only on the first page

55% of users only click on the top-three links

90%

4% Of users click on ads

Googlemarketshareworldwide

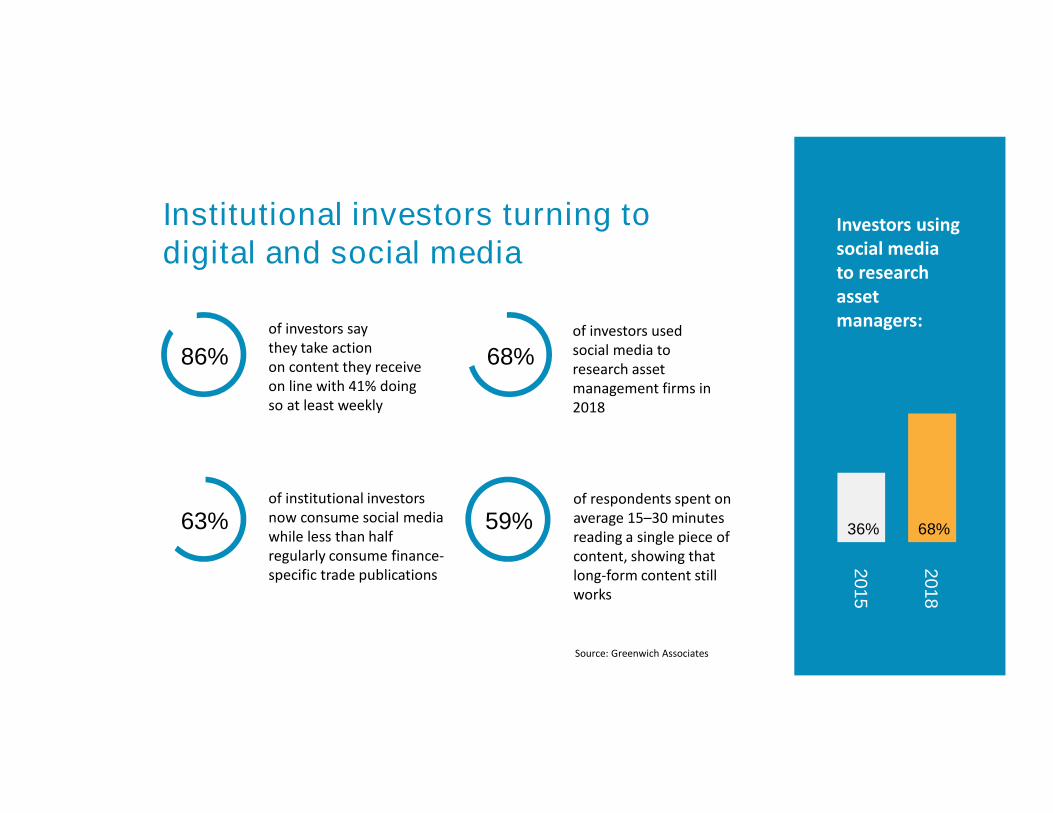

Institutional investors turning to digital and social media

86%

63%

of investors used social media to research asset management firms in 2018

59%of respondents spent on average 15–30 minutes reading a single piece of content, showing that long-form content still works

of institutional investors now consume social media while less than half regularly consume finance-specific trade publications

68%

Investors using social media to research asset managers:of investors say

they take action on content they receive on line with 41% doing so at least weekly

36% 68%

20

15

20

18

Source: Greenwich Associates

Where are they going?

Source: Greenwich Associates

CNBC

New York Times

Business Insider

Google Finance

Bloomberg

Forbes

Fortune

Financial Times

Wall Street Journal

21%

18%

17%

16%

13%

12%

11%

9%

7%

7%

22%

OW

NE

D

3rd Party Advocated

Cause

Corporate / Brand

PA

ID

EARNED

Digital Reputation Ecosystem

1. Focus on organic search

2. Define SEO strategy

3. Control the narrative

4. Optimize owned assets

5. Engage in social media

Developing a digital reputation – Top 5

Moderator

Panelists

The Intersection of ESG and Infrastructure / Energy1:15 p.m. – 2:15 p.m.

Hayden Baker, PartnerTroutman Sanders

Delilah Rothenberg, Managing DirectorDevelopment Capital Strategies

Scott Jacobs, CEOGenerate Capital

Maria Mähl, PartnerArabesque Asset Management

Justin DeAngelis, PartnerDenham Capital

Moderator

Panelists

Offshore Funds Update2:30 p.m. – 3:30 p.m.

Mase Kazemi, Head of Fund AccountingCentaur USA

Catherine Houts, DirectorTax KPMG in the Cayman Islands

Catherine Pham, PartnerMourant

Ivana Faltysova, Executive DirectorCayman Office, DMS Governance

Mitzie Pierre, Chief Compliance OfficerUS and Canada, IFM Investors

Robert Friedman, PartnerTroutman Sanders

59

Resource Guide: Private Fund Adviser Regulation & Enforcement

Troutman Sanders Private Funds ForumSeptember 26, 2019

Prepared by Kurt Wolfe

Moderator

Panelists

Private Fund Adviser Regulation and Enforcement3:45 p.m. – 4:45 p.m. **This event is closed to the media

Ghillaine Reid, PartnerTroutman Sanders

L. Allison Charley, Senior Principal ConsultantACA Compliance Group

Nancy Lynch, Senior CounselAmericas, Legal & Compliance Division, Man Group

Mark Mandel, PartnerTroutman Sanders

Joel Mack, Supervisory Special AgentFederal Bureau of Investigation

CLE Credit Provided

This Resource Guide offers a primer on key themes and topics in the private fund adviser

regulatory and enforcement space. It also provides references and links to helpful materials, for

further reading. In particular, this Resource Guide covers the following:

• The Investment Adviser Standard of Conduct

• Expenses and Expense Allocation

• Conflicts of Interest

• Advertising

• Cybersecurity

Resource Guide: Private Fund Adviser Regulation and Enforcement

61

62

The Investment Adviser Standard of Conduct

“[A]n investment adviser must, at all

times, serve the best interest of its client

and not subordinate its client’s interest

to its own.” – SEC Chair Jay Clayton1

In June 2019, in connection with the adoption of Regulation Best Interest, the SEC issued an

Interpretive Release to affirm and clarify the Commission’s views of the fiduciary duty that

investment advisers owe to their clients under the Advisers Act.2

• The Interpretive Release provides textual support for principles that have long informed the SEC’s

examination and enforcement efforts,3 including:

– The Duty of Care. An adviser must serve the best interest of its client, based on the client’s objectives. The

Interpretive Release notes that the duty of care extends to i) providing advice that is in the client’s best interest, ii)

seeking best execution, and iii) monitoring the relationship and client objectives on an ongoing basis.

– The Duty of Loyalty. An adviser must not subordinate its clients’ interests to its own; conflicts of interest and all

material facts relating to the advisory relationship must be fully and fairly disclosed.

The Commission also adopted a rule that will require investment advisers to provide retail

investors with Form CRS / Form ADV Part 3, which includes a relationship summary that contains

information about the firm’s services, fees and costs, conflicts of interest, the legal standard of

conduct, and whether or not the firm and its financial professionals have disciplinary history.4

Investment Adviser Standard of Conduct

63

1. SEC Chairman Jay Clayton, Regulation Best Interest and the Investment Adviser Fiduciary Duty: Two Strong Standards that Protect

and Provide Choice for Main Street Investors (July 8, 2019), available at https://www.sec.gov/news/speech/clayton-regulation-best-

interest-investment-adviser-fiduciary-duty; see also Chairman Jay Clayton, Statement at the Open Meeting on Commission Actions to

Enhance and Clarify the Obligations Financial Professionals Owe to our Main Street Investors (June 5, 2019), available at

https://www.sec.gov/news/public-statement/statement-clayton-060519-iabd.

2. See SEC Adopts Rules and Interpretations to Enhance Protections and Preserve Choice for Retail Investors in Their Relationships

With Financial Professionals, SEC Press Release No. 2019-89 (June 5, 2019), available at https://www.sec.gov/news/press-

release/2019-89; Final Rule - Form CRS Relationship Summary and Form ADV Amendments, Release No. IA-5247, available at

https://www.sec.gov/rules/final/2019/34-86032.pdf; Commission Interpretation - Standard of Conduct for Investment Advisers, Release

No. IA-5248, available at https://www.sec.gov/rules/interp/2019/ia-5248.pdf.

3. See ACA Compliance Group, Investment Adviser Standard of Conduct and Form CRS - What You Need to Know (Part 1 of 2) (July 11,

2019), available at https://www.acacompliancegroup.com/blog/investment-adviser-standard-conduct-and-form-crs-what-you-need-

know-part-1-2.

4. See ACA Compliance Group, Investment Adviser Standard of Conduct and Form CRS – What You Need Know (Part 2 of 2) (July 25,

2019), available at https://www.acacompliancegroup.com/blog/investment-adviser-standard-conduct-and-form-crs-%E2%80%93-what-

you-need-know-part-2-2.

Resources

64

65

Expenses and Expense Allocation

“By far the most common

deficiencies noted by our

examiners in private equity

relate to expenses and expense

allocation.” –Marc Wyatt, Former

Director of OCIE5

The allocation of fees and expenses—and related disclosures—are of paramount importance for

OCIE and the SEC Enforcement Staff.

• For example, examiners have noted instances of advisers improperly shifting expenses away from the

adviser and to the funds or portfolio companies (e.g., by hiring the adviser’s employees as

“consultants” paid by the funds).6

• Examiners also pay particular attention to the (disproportionate) alloction of fees or expenses across

multiple funds, the fund manager, and portfolio companies.

• Indeed, egregious examples of improper expense allocation may involve shifting expenses away from

proprietary funds, or funds created for preferred investors, to flagship co-mingled funds.

• Examiners have also repeatedly noted issues around undisclosed accelerated monitoring fees.

OCIE now consistently counts “disclosure of the costs of investing” among its annual

examination priorities, with a particular focus on whether expenses are calculated and charged in

accordance with disclosures.7

Fees and Expenses: Risks and Regulatory Focus

66

There have been several noteworthy enforcement actions in this area, including:

• The Commission settled charges against a private fund adviser and its principal for using funds to pay for the adviser’s

operating expenses in a manner not clearly authorized under the funds’ governing documents or accurately reflected in

the funds’ financial statements.8

• The Commission has settled charges against private equity fund advisers for misallocating so-called “broken deal”

expenses.9

• The Commission settled charges against numerous advisers for inadequate disclosures related to the acceleration of

certain monitoring fees paid by the funds’ portfolio companies.10

• The Commission settled charges against an adviser for the “horizontal” misallocation of expenses between two

portfolio companies with different investors. The adviser caused one portfolio company to pay a disproportionate share

of the companies’ joint expenses, to the detriment of that fund’s investors.11

• The Commission settled charges against an adviser for the “vertical” misallocation of expenses between the adviser

and the funds it managed. The adviser improperly allocated its own consulting, legal and compliance-related expenses

to funds in violation of the funds’ organizational documents.12

Fees and Expenses: Enforcement Actions

67

5. Former OCIE Director Marc Wyatt, Private Equity: A Look Back and a Glimpse Forward (May 13, 2015), available at

https://www.sec.gov/news/speech/private-equity-look-back-and-glimpse-ahead.html (hereinafter “Wyatt Speech”).

6. See, e.g., Mary Jo White, Keynote Address at the Managed Fund Association: “Five Years On: Regulation of Private Fund Advisers After Dodd-Frank” (Oct.

16, 2015), available at https://www.sec.gov/news/speech/white-regulation-of-private-fund-advisers-after-dodd-frank.html (hereinafter “White Speech”).

7. See OCIE, 2018 National Exam Program Examination Priorities, available at https://www.sec.gov/about/offices/ocie/national-examination-program-priorities-

2018.pdf (hereinafter “2018 Exam Priorities”); OCIE, 2019 Examination Priorities, available at https://www.sec.gov/files/OCIE%202019%20Priorities.pdf;

OCIE, Overview of the Most Frequent Advisory Fee and Expense Compliance Issues Identified in Examinations of Investment Advisers (April 12, 2018),

available at https://www.sec.gov/files/ocie-risk-alert-advisory-fee-expense-compliance.pdf (hereinafter “2019 Exam Priorities”).

8. In the Matter of Alpha Titans, LLC, et al., Release No. IA-4073 (Apr. 29, 2015), available at https://www.sec.gov/litigation/admin/2015/34-74828.pdf.

9. See In the Matter of Kohlberg Kravis Roberts & Co. L.P., Release No. IA-4131 (Jun. 29, 2015), available at https://www.sec.gov/litigation/admin/2015/ia-

4131.pdf; SEC Charges Investment Adviser for Allocating All Broken Deal Expenses to Private Equity Fund Without Disclosure (Sept. 21, 2017), available at

https://www.sec.gov/litigation/admin/2017/ia-4772-s.pdf.

10. See In the Matter of Blackstone Management Partners L.L.C., et al., Release No. IA-4219 (Oct. 7, 2015), available at

https://www.sec.gov/litigation/admin/2015/ia-4219.pdf; In the Matter of TPG Capital Advisors, LLC, Release No. IA-4830 (Dec. 21, 2017), available at

https://www.sec.gov/litigation/admin/2017/ia-4830.pdf.

11. In the Matter of Lincolnshire Management, Inc., Advisers Act Release No. 3927 (Sept. 22, 2014), available at http://www.sec.gov/litigation/admin/2014/ia-

3927.pdf.

12. In the Matter of Cherokee Investment Partners, LLC and Cherokee Advisers, LLC, Advisers Act Release No. 4258 (Nov. 5, 2015), available at

https://www.sec.gov/litigation/admin/2015/ia-4258.pdf.

Resources

68

69

Conflicts of Interest

“It is thus critically important that

advisers disclose all material

information, including conflicts of

interest, to investors at the time

their capital is committed.” –

Andrew Ceresney, Former SEC

Director of Enforcement13

Investment advisers are expected to disclose any conflicts of interest that might provide

incentives to recommend certain products or allocate trades/opportunities to certain funds. Fund

advisers must also disclose conflicts of interest relating to payments to affiliated persons or

entities.

Disclosure of conflicts is a perennial focus area for OCIE and the SEC Enforcement Staff.14

• For example, the SEC has noted that fund advisers may not be adequately disclosing conflicts related

to the allocation of trades and investment opportunities (e.g., among the advisers’ proprietary funds

and the personal accounts of their portfolio managers).

• Examiners have also noted instances of funds failing adequately to disclose other investors’ priority

co-investment rights.

• Examiners also focus on the disclosure of conflicts relating to compensation paid to the firm’s

individual partners, advisors and affiliates.

Conflicts of Interest: Risks and Regulatory Focus

70

There have been several noteworthy enforcement actions in this area, including:

• The Commission settled charges with a New York-based private equity firm and four executives for

failing to disclose conflicts of interest to a fund client and investors when fund and portfolio company

assets were used for payments to former firm employees and an affiliated entity.15

• The Commission settled charges with an adviser for failing to disclose and obtain fund advisory board

consent for a series of transactions, including: (a) a series of loans to the funds’ portfolio companies,

resulting in the adviser obtaining interests in portfolio companies that were senior to the interests held

by the funds; (b) causing more than one of its funds to invest in the same portfolio company at

differing priority levels, potentially favoring one fund client over another; and (c) causing certain of the

funds’ investments to exceed concentration limits set forth in the funds’ governing documents.16

• The Commission settled charges with an adviser for failing to disclose to its private equity clients

conflicts of interest surrounding its receipt of compensation from a company that provided services to

fund portfolio companies.17

Conflicts of Interest: Enforcement Actions

71

13. Andrew Ceresney, Securities Enforcement Forum West 2016 Keynote Address: Private Equity Enforcement (May 12,

2016), available at https://www.sec.gov/news/speech/private-equity-enforcement.html. (Enforcement action summaries

in this section derive from this Ceresney speech.)

14. See, e.g., 2018 Exam Priorities (emphasizing that it is “important for financial professionals to inform investors of any

conflicts of interest that might provide incentives for the financial professionals to recommend certain types of products

or services to investors”); see also 2019 Exam Priorities.

15. SEC Charges Private Equity Firm and Four Executives With Failing to Disclose Conflicts of Interest, SEC Press

Release No. 2015-250 (Nov. 3, 2015), available at https://www.sec.gov/news/pressrelease/2015-250.html.

16. In the Matter of JH Partners, LLC, Advisers Act Release No. 4276 (Nov. 23, 2015), available at

https://www.sec.gov/litigation/admin/2015/ia-4276.pdf.

17. SEC Charges a New York-Based Investment Adviser for Breach of Fiduciary Duty, Admin Proc. File No. 3-18449 (April

24, 2018), available at https://www.sec.gov/enforce/ia-4896-s.

Resources

72

73

Advertising

It is unlawful for advisers to have advertising that is false or misleading or that contains any untrue statements of material fact.

The Advertising Rule prohibits an adviser, directly or indirectly, from publishing, circulating, or distributing any advertisement that contains any untrue

statement of material fact, or that is otherwise false or misleading. Advertising Rule compliance is a recurring focus of the OCIE examination staff.18

OCIE has issued a Risk Alert detailing common exam deficiencies relating to the advertising,19 which include:

• Misleading Performance Results. The staff noted advertisements that improperly compared results to a benchmark but did not include disclosures about the

limitations inherent in such comparisons; advertisements that contained hypothetical or back-tested performance results; and advertisements that presented

performance results without deducting advisory fees.

• Misleading One-on-One Presentations. The staff noted examples of advisers touting performance results in certain one-on-one presentations, but not in

relevant disclosures.

• Cherry-Picked Profitable Stock Selections. The staff warned advisers not to include only profitable stock selections or recommendations in presentations,

client newsletters, or on their websites, without meeting the pre-conditions in the Advertising Rule.

• Misleading Use of Third Party Rankings or Awards. The staff noted examples of advertisements containing the potentially misleading references to awards or

rankings conferred by third parties that failed to disclose facts, which staff believes were material under the circumstances, about such awards or rankings.

• Testimonials. The staff warned against published client testimonials that attest to the adviser’s services or otherwise endorse the adviser that may be

prohibited testimonials (e.g., client endorsements published in firm websites, social media pages, reprints of third party articles, or pitch books).

• Compliance Policies and Procedures. The staff highlighted examples of advisers failing to adopt compliance policies and procedures reasonably designed to

prevent deficient advertising practices. Of note, the staff identified lax policies and procedures pertaining to the process for reviewing and approving

advertising materials prior to their publication or dissemination; and confirming the accuracy of performance results in compliance with the Advertising Rule.

The SEC is expected to release amendments to the Advertising Rule in 2019.

Advertising: Risks and Regulatory Focus

74

OCIE and the Enforcement Division are increasingly interested in firms’ advertisements in social

media.

• Last summer, the Commision settled enforcement actions with two SEC-registered investment

advisers, three investment adviser representatives, and a marketing consultant who committed and/or

caused violations of the Testimonial Rule under the Advisers Act through their use of social media and

the internet, including testimonial advertisements on various public social media websites and videos

containing client testimonials on YouTube. The enforcement actions resulted from examination

referrals.20

• Also last year, the Commission settled an enforcement action with an investment adviser that touted

hypothetical returns from its blended stock research ratings without disclosing that some of their

superior performance came from back-testing models.21

Advertising: Enforcement Actions

75

18.See OCIE Risk Alert, Observations from Examinations of Investment Advisers: Compliance,

Supervision, and Disclosure of Conflicts of Interest (July 23, 2019), available at

https://www.sec.gov/files/OCIE%20Risk%20Alert%20-%20Supervision%20Initiative.pdf (noting

deficiencies in supervisory procedures relating to the Advertising Rule).

19.See OCIE Risk Alert, The Most Frequent Advertising Rule Compliance Issues Identified in OCIE

Examinations of Investment Advisers (Sept. 14, 2017), available at

https://www.sec.gov/ocie/Article/risk-alert-advertising.pdf (including links to several enforcement

actions and no-action letters).

20.SEC Charges Investment Advisers and Representatives for Violating the Testimonial Rule Using

Social Media and the Internet (July 10, 2018), available at https://www.sec.gov/enforce/3-18586-90-s.

21.In the Matter of Massachusetts Financial Services Company (August 31, 2018), available at

https://www.sec.gov/litigation/admin/2018/ia-4999.pdf.

Resources

76

77

Cybersecurity

83% of registered investment

advisers identify cybersecurity as the

“hottest” compliance topic and 70%

have increased compliance testing in

this area. – ACA Compliance Group

2019 Investment Management

Compliance Survey

According to the Investment Adviser Association and ACA Compliance Group, 83% of registered investment

advisers identify cybersecurity as the “hottest” compliance topic and 70% have increased compliance testing in

this area.22

In 2017, OCIE issued a Risk Alert detailing observations from examinations conducted pursuant to the

Cybersecurity Examination Initiative, which included obvservations on advisers’ cybersecurity preparedness in

the following areas: (1) governance and risk assessment; (2) access rights and control; (3) data loss prevention;

(4) vendor management; (5) training; and (6) incident response.23

Since at least 2015, OCIE has identified cybersecurity as an examination priority. In 2018, for example, OCIE

explained the exam staff “will continue to prioritize cybersecurity in each of our examination programs,”

focusing on the elements outlined in the 2015 cybersecurity Risk Alert.24

• Indeed, in recent months, the SEC commenced a series of targeted cybersecurity examinations of registered

invesgments advisers.25

The SEC is also increasingly focused on data protection and data privacy issues affecting investment advisers.26

Cybersecurity

78

22. 2019 Investment Management Compliance Testing Survey Results (July 15, 2019), available at

https://www.acacompliancegroup.com/blog/2019-investment-management-compliance-testing-survey-results.

23. OCIE Risk Alert, Observations from Cybersecurity Examinations (Aug. 7, 2017), available at

https://www.sec.gov/files/observations-from-cybersecurity-examinations.pdf.

24. See OCIE 2018 Exam Priorities; see also OCIE 2019 Exam Priorities.

25. See ACA Compliance Group, Regulatory Cyber Alert: SEC Conducting Cyber Compliance Examination Sweep of

Registered Investment Advisers (RIAs) (May 22, 2019), available at

https://www.acacompliancegroup.com/blog/regulatory-cyber-alert-sec-conducting-cyber-compliance-examination-

sweep-registered-investment.

26. See ACA Compliance Group, SEC Warns of Data Privacy Compliance Issues (April 17, 2019), available at

https://www.acacompliancegroup.com/blog/sec-warns-data-privacy-compliance-issues; see also ACA Compliance

Group, Regulatory Cyber Alert: SEC’s OCIE Issues Risk Alert on Data Storage Security (May 28, 2019), available at

https://www.acacompliancegroup.com/blog/regulatory-cyber-alert-sec%E2%80%99s-ocie-issues-risk-alert-data-

storage-security.

Resources

79

80

Other Noteworthy Enforcement Cases

The SEC brought a number of noteworthy enforcement actions involving private fund advisers and private funds in 2018-2019.

• The Commission found that a fund administrator failed to heed red flags and correct faulty accounting by two

private funds to which it provided accounting and fund administration services. The SEC alleged that the administrator

missed or ignored clear indications of fraud while contracted to keep records and prepare financial statements and

investor account statements for funds managed. In the Matter of Apex Fund Services (US), Inc., Release Nos. IA-4428,

IA-4429 (June 16, 2016), available at https://www.sec.gov/news/pressrelease/2016-120.html.

• The Commission settled charges with thirteen private fund advisers for repeated failures to file annual reports on

Form PF. See SEC Charges 13 Private Fund Advisers for Repeated Filing Failures, SEC Press Release No. 2018-100

(June 1, 2018), available at https://www.sec.gov/news/press-release/2018-100.

• The Commission found that an adviser to several private funds failed adequately to implement a compliance

program, which led to a failure to disclose to all investors all (informal) options to redeem investment funds. This

failure resulted in materially different redemption amounts for two investors. The compliance failures also resulted in

violations relating to mandatory annual audits, Form ADV disclosures, and registration documents. In the Matter of Aria

Partners GP, LLC, Release No. IA-4991 (Aug. 22, 2018), available at https://www.sec.gov/litigation/admin/2018/ia-

4991.pdf.

Other Noteworthy Enforcement Cases

81

• The Commission settled charges against an adviser and three of its affiliates for using faulty investment models and misleading

retail investors. The SEC alleged that the adviser claimed that investment decisions would be based on quantitative models, but the

models, which were developed solely by an inexperienced, junior AUIM analyst, contained numerous errors, and did not work as

promised. When the errors were discovered, the adviser stopped using the models without telling investors or disclosing the errors. See

Transamerica Entities to Pay $97 Million to Investors Relating to Errors in Quantitative Investment Models, SEC Press Release No.

2018-167 (Aug. 27, 2018), available at https://www.sec.gov/news/press-release/2018-167.

• The Commission settled charges with a private fund adviser for failure to disclose material information related to an increase in

the valuation of one of its funds to the funds’ limited partners. In the Matter of VSS Fund Management LLC and Jeffrey T. Stevenson,

Release No. IA-5001 (Sept. 7, 2018), available at https://www.sec.gov/litigation/admin/2018/ia-5001.pdf.

• The Commission revoked the registration of an investment adviser and barred its principal from the securities industry for

stealing money from a private fund the adviser managed. The principal allegedly concealed the theft of more than $3 million by

sending fraudulent account statements and tax documents and falsely reporting to the SEC that the fund had been audited and its AUM

verified. See Investment Adviser Charged With Stealing Millions From Private Fund, SEC Press Release No. 2019-45 (March 28,

2019), available at https://www.sec.gov/news/press-release/2019-45.

• The Commission settled charges against a private fund adviser and its principal for making misleading statements to investors

regarding due diligence on an investment and for failing to disclose a conflict of interest that arose when the funds invested alongside

the principal. In the Matter of Charter Capital Management, LLC, and Steven Morris Bruce, Release No. IA-5226 (April 23, 2019),

available at https://www.sec.gov/litigation/admin/2019/ia-5226.pdf.

Other Noteworthy Enforcement Cases

82

• The Commission settled charges against a private fund advisors, its CEO, and its CFO for misusing assets in a

private equity fund it advised by (i) failing to apply an offset due to the fund, (ii) improperly using fund assets to funds

the advisory business, and (iii) causing the fund to overpay operational expenses. (The Wall Street Journal called this

“the latest example of the [SEC] closely monitoring the way private-equity firms handle fund expenses.”) In the Matter of

Corinthian Capital Group, LLC, Peter B. Van Raalte, and David G. Tahan, Release No. IA-5229 (May 6, 2019), available

at https://www.sec.gov/litigation/admin/2019/ia-5229.pdf.

• The Commission settled charges against a private fund manager in the mortgage-backed securities space for

compliance deficiencies that contributed to the firm’s failure to ensure that certain securities in its flagship fund were

valued properly. See Hedge Fund Adviser to Pay $5 Million for Compliance Failures Related to Valuation of Fund

Assets, SEC Press Release No. 2019-86 (June 4, 2019), available at https://www.sec.gov/news/press-release/2019-86.

• The Commission settled charges against a portfolio manager and trader for manipulating the value of a private

fund’s investments, which artificially inflated the fund’s reported returns and caused the fund to pay too much in fees.

See SEC Charges Portfolio Manager with Mispricing Fund Investments, SEC Press Release No. 2019-135 (July 18,

2019), available at https://www.sec.gov/news/press-release/2019-135.

Other Noteworthy Enforcement Cases

83

Moderator

Speaker

Afternoon Keynote / Fireside Chat5:00 p.m. – 6:00 p.m. **This event is closed to the media

Genna GarverPartner, Troutman Sanders

Brad Katsuyama, Co-founder and CEOIEX Group