new ice contracts still sitting on runway · pdf fileproud partner of the saskatchewan...

TRANSCRIPT

Publications Mail Agreement Number 40069240

ALSO IN THIS ISSUEONLY YOU CAN PREVENT RESIDUE ISSUES

CONTROL TRAFFIC FARMING MAY FIT PRAIRIES

MARKETS: LIVESTOCK PAIN AN EARLY WARNING FOR GRAIN

P L A N N I N G T H E N E X T C R O P — A N D B E Y O N D

www.agcanada.com $4.25 N O V E M B E R 2 0 12 E D I T I O N

NEW ICE CONTRACTS STILL SITTING ON RUNWAY PG.10

PRIVATES PASS ON CWB CANOLA DELIVERIES PG.12

Proud partner of theSaskatchewan Roughriders

Bigger yields, better profi ts, serious bragging rights.

Nodulator® XL inoculant drives your pea and lentil yields straight into the big leagues – for a championship Return on Investment.

When you inoculate with Nodulator® XL, it unleashes a unique, more active

strain of rhizobium for enhanced nitrogen-fi xing within nodules and

more vigorous plant growth. That means higher yields and a

Return on Investment that crushes the competition.

Nodulator® XL is registered for both peas and lentils, with your choice of

formulations: liquid, self-adhering peat or solid core granule. Want to go big?

Grab the Nodulator® XL Q-Pak – a convenient 364 kg (800 lb.)

soft-sided tote that’s perfect for larger operations.

Nodulator® and XLerated Performance. Accelerated Yield.™ are trademarks or registered trademarks

used under license by Becker Underwood Canada Ltd. The Becker Underwood logo is a trademark

of Becker Underwood, Inc. and is licensed to Becker Underwood Canada Ltd.

www.nodulatorxl.com

BU27096NodX_CrG_AE.indd 1 9/6/12 9:38 AM

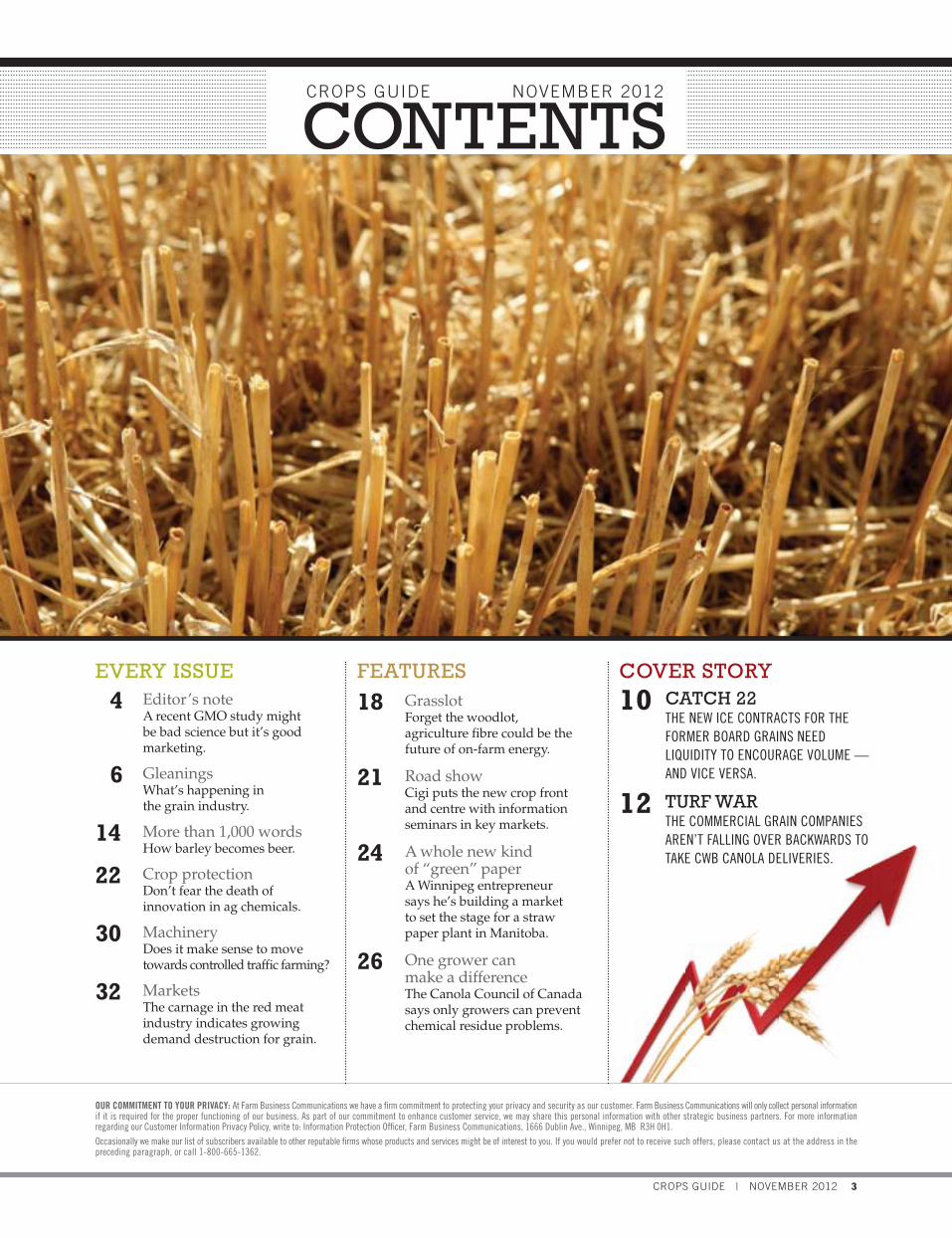

CROPS GUIDE | NOVEMBER 2012 3

CONTENTS

FEATURES

18 GrasslotForget the woodlot, agriculture fi bre could be the future of on-farm energy.

21 Road showCigi puts the new crop front and centre with information seminars in key markets.

24 A whole new kind of “green” paperA Winnipeg entrepreneur says he’s building a market to set the stage for a straw paper plant in Manitoba.

26 One grower can make a differenceThe Canola Council of Canada says only growers can prevent chemical residue problems.

OUR COMMITMENT TO YOUR PRIVACY: At Farm Business Communications we have a fi rm commitment to protecting your privacy and security as our customer. Farm Business Communications will only collect personal information if it is required for the proper functioning of our business. As part of our commitment to enhance customer service, we may share this personal information with other strategic business partners. For more information regarding our Customer Information Privacy Policy, write to: Information Protection Offi cer, Farm Business Communications, 1666 Dublin Ave., Winnipeg, MB R3H 0H1.

Occasionally we make our list of subscribers available to other reputable fi rms whose products and services might be of interest to you. If you would prefer not to receive such offers, please contact us at the address in the preceding paragraph, or call 1-800-665-1362.

EVERY ISSUE

4 Editor’s noteA recent GMO study might be bad science but it’s good marketing.

6 GleaningsWhat’s happening in the grain industry.

14 More than 1,000 wordsHow barley becomes beer.

22 Crop protectionDon’t fear the death of innovation in ag chemicals.

30 MachineryDoes it make sense to move towards controlled traffi c farming?

32 MarketsThe carnage in the red meat industry indicates growing demand destruction for grain.

CROPS GUIDE NOVEMBER 2012

COVER STORY

10 CATCH 22THE NEW ICE CONTRACTS FOR THE FORMER BOARD GRAINS NEED LIQUIDITY TO ENCOURAGE VOLUME — AND VICE VERSA.

12 TURF WARTHE COMMERCIAL GRAIN COMPANIES AREN’T FALLING OVER BACKWARDS TO TAKE CWB CANOLA DELIVERIES.

EDITORIAL STAFF

Editor: Gord Gilmour (204) 294-9195 Fax (204) 942-8463Email: [email protected]

REGULAR CONTRIBUTORS

Brad Brinkworth David Drozd Ron Friesen Richard Kamchen Gord Leathers Warren Libby Jay Whetter Rebeca Kuropatwa

ADVERTISING SALES

Cory Bourdeaud’hui(204) 954-1414 Cell (204) 227-5274Email: [email protected]

Lillie Ann Morris(905) 838-2826 Email: [email protected]

Head office: 1666 Dublin Ave., Winnipeg, MB R3H 0H1

Advertising Services Co-ordinator:Sharon Komoski(204) 944-5758 Fax (204) 944-5562Email: [email protected]

Publisher: Bob Willcox Email: [email protected]

Associate Publisher/Editorial Director: John Morriss Email: [email protected]

Production Director: Shawna GibsonEmail: [email protected]

Director of Sales and Circulation: Lynda TitykEmail: [email protected]

Circulation Manager: Heather AndersonEmail: [email protected]

Art Director: Jenelle Jensen

Contributing Photographer: Ryan Fennessy

Contents of this publication are copyrighted and may be reproduced only with the permission of the editor. CROPS GUIDE is published by Farm Business Communications, 1666 Dublin Ave.,

Winnipeg, MB R3H 0H1. Head office: Winnipeg, Manitoba

Printed by Transcontinental LGM-Coronet.

CROPS GUIDE is published 7 times a year.

Publications Mail Agreement Number 40069240.

Canadian Postmaster: Return undeliverable Canadian addresses (covers only) to: Circulation Dept, 1666 Ave.,

Winnipeg, MB R3H 0H1.U.S. Postmaster: Send address changes and undeliverable addresses (covers only) to: Circulation Dept., 1666 Dublin

Ave., Winnipeg, MB R3H 0H1.

ISSN 1927-5382 (Print)ISSN 1927-5390 (Online)

Subscription inquiries:Call toll-free 1-800-665-1362 or email: [email protected]

U.S. subscribers call 1-204-944-5766

CROPS GUIDE is printed with linseed oil-based inks.PRINTED IN CANADA

Vol. 01 No. 06website: www.agcanada.com

The editors and journalists who write, contribute and provide opinions to CROPS GUIDE and Farm Business Communications attempt to provide accurate and useful opinions, information and analysis. However, the editors, journalists, CROPS GUIDE and Farm Business Communications, cannot and do not guarantee the accuracy of the information contained in this publication and the editors as well as CROPS GUIDE and Farm Business Communications assume no responsibility for any actions or decisions taken by any reader for this publication based on any and all information provided.

EDITOR’S NOTEPL ANNING THE NE X T CROP— AND BEYOND

www.agcanada.com

G O R D G I L M O U R go rd .g i lmour@fbcpub l i sh ing .com

By now you’ve no doubt heard that GMO crops are giving us all tumours.

Or at least that’s the media and activist interpretation of a recently

released and very controversial study that showed elevated levels of tumours in lab rats.

Predictably the organic industry is making hay with the news, claiming this proves that there are many unanswered questions about GMO crops.

I’m going to ignore the science for the pur-poses of this column, and will simply note it’s a single, unreplicated study.

Instead, I’m going to spend a bit of time encouraging you to put your emotions away and take a long, hard look at what’s now being done with this information — and what that might tell you about the future.

First and foremost, you are going to have to accept that every time something like this comes up, one of your competitors is going to try to take advantage of it. It might be infuri-ating to, but if you didn’t see it coming, you need to go try and buy a truck or car.

I did recently, and it was an interesting experience. If I believed any of the salespeople I spoke to, I was lucky to have come to see them, because other than their fine automo-biles, there wasn’t anything out there except a lot of unsafe junk.

That is, in fact, pretty much the entire essence of marketing; convincing potential cus-tomers that your products are better and safer than the competition.

The eternal conundrum of Prairie grain growers is that most are commodity growers. While there are certainly compelling argu-ments about why the industry has developed that way — distance to market, for example — I do think the whole industry needs to take a long, hard look at this mindset and admit it is in many ways an Achilles heel.

It’s a model that essentially accepts right from the start that you will be receiving low-est-commmon-denominator pricing for your products. Call it the grain farming equivalent of minimum wage. It also accepts that your products will be generic and interchangeable with those coming from competitors.

I’m not for a second suggesting that Prai-rie grain growers should look at this and as a group switch over to organic production. But

I am saying that you should look at what the organic growers are doing and recognize that effort could be reproduced again and again.

I can even think of one obvious niche that’s ripe for exploitation without even breaking a sweat — and the food industry is even setting the table for it to happen. It’s the fundamental disconnection between consumer perceptions of farms and the reality out in the field.

For most urbanites the concept of “farm” conjures up an image of something like the small mixed farm my maternal grandparents were running back in the 1970s when I was a little kid.

It was picturesque, welcoming and an anachronism even then. A better picture of what the new farm model looked like was down the road a few miles at my paternal grandparents’ place, where my father had returned from the agriculture college at the University of Saskatch-ewan. Things were proceeding at a much more scientific pace, with a move to a grain-only operation, larger equipment and a bigger land base — typical evolution in other words.

So can someone explain to me why when I go to the store I’m bombarded with images more appropriate to the distant past of red barns and the like? And why the largest agribusinesses out there are anxious to wrap themselves up in the flag and call themselves such-and-such farm?

The answer, of course, is that it sells and these sophisticated companies know it. My question to you though, is whether it’s a gigan-tic leap to imagine a future where smaller farmers — what we would consider lifestyle operators — begin marketing under a banner claiming they were “traditional family farms?”

Unless commodity growers can get their heads around this challenge they’re going to face the death of a thousand cuts, as their mar-ket becomes more segmented and specialized.

I don’t want to suggest this is inevitable, but rather to encourage growers — and their associations — to consider the implications of this trend. They need to do a better job of understanding what consumers want, com-municating what they’re doing and — per-haps most importantly — do a much better job of actually listening to consumers rather than “educating” them, which is really a code word for bringing them into line.

If you’re not willing to take up this chal-lenge, I suspect you won’t like the results. �

Pay attention

4 CROPS GUIDE | NOVEMBER 2012

www.dseriescanola.ca

D315

3

D315

4S

NEW

D315

2

Roundup Ready® is a registered trademark used under license from Monsanto Company.The DuPont Oval logo, DuPont and FarmCare® are registered trademarks or trademarks of E. I. du Pont de Nemours and Company or its affi liates. E. I. du Pont Canada Company is a licensee. Pioneer®, the Trapezoid symbol, and Pioneer Protector are registered trademarks of Pioneer Hi-Bred International, Inc.© Copyright 2012 DuPont Canada. All rights reserved.

ReDefi ning Canola PerformancePioneer® brand D-Series canola hybrids are bred to deliver outstanding performance. D3153 delivers high yield with exceptional standability and harvestability. D3152 adds the Pioneer Protector® Clubroot trait for protection from this devastating disease. And new D3154S has the Pioneer Protector® Sclerotinia trait for built-in protection.

D-Series canola hybrids are available exclusively from select independent and Co-op retailers and are backed with service from DuPont Canada.

Purchases of D-Series canola hybrids will qualify you for the 2013 DuPont™ FarmCare® Connect Grower Program. Terms and Conditions apply.

DP86 D-Series Canola_CGW_AE.indd 1 12-08-29 11:28 AM

RichaRdson to boost West coast poRt gRain stoRage

Grain handler Richardson International has applied for per-mits to boost its Port Metro Vancouver terminal’s grain storage space by about two-thirds.

The Winnipeg company, currently Canada’s second-biggest grain handler, plans to build an 80,000-tonne capacity concrete grain storage annex at its Vancouver port site.

After it takes down its current steel storage bins at the site, Richardson said this $120-million expansion project would net about 70,000 tonnes of new storage, bringing the terminal’s total storage capacity to 178,000 tonnes.

“Increasing storage capacity at our Vancouver terminal is critical to our business,” Darwin Sobkow, Richardson’s vice-president for agribusiness operations, said in a release.

Richardson’s Vancouver terminal is now running at “maxi-mum capacity,” the company said, handling about three million tonnes of grains and oilseeds per year.

The company’s grain handle is also expected to rise in coming months through its planned acquisition of 19 Prairie elevators now owned by Viterra, Canada’s No. 1 handler.

Pending approval from federal antitrust watchdogs, that sale — part of a $900-million deal with Viterra’s proposed new owner, Glencore International — would put Richardson near the No. 1 spot among Canadian handlers.

Given “growing global demand,” Richardson said, it expects to be able to handle over five million tonnes per year with this additional storage capacity in hand.

The company recently spent $20 million to improve rail receiving capacity and increase “operating efficiencies” at the Vancouver terminal, reconfiguring its rail yard and adding a sec-ond rail unload pit and rail car indexer.

With those upgrades complete, Richardson said, it can double the number of rail cars it unloads at the terminal to 300 cars a day on a double track, up from 150 on a single track.

The proposed storage expansion project will also include new distribution equipment and an upgraded dust filtration system, the company said.

6 CROPS GUIDE | NOVEMBER 2012

GleaninGs G R a I N I N D U S t R y N E w S

industry notes

A major buying group for crop inputs has set up a new partnership aiming to bring in Canadian farmers as the owners of a new nitrogen fertilizer manufacturing plant.

Saskatoon-based Farmers of North America (FNA) recently launched FNA Fertilizer Limited Partnership (FNA FLP) to run what it calls “ProjectN,” which will now seek seed capital to build and operate such a plant.

FNA itself would not be the owner of such a plant, but instead is “organizing and providing the catalyst to see a fertilizer plant built,” spokesman Bob Friesen said in a release. “Participation in fertilizer manufacturing will allow farmers to capture more of the value chain.”

FNA, which began importing offshore nitrogen for its members in 2001, said Wednesday that its ProjectN working group has already run a review of the nitrogen fertilizer sector, considering natural gas pricing, plant scale, market demand, competitive supply and “other indicators framing the business case for a new development.”

FNA ran its initial engineering feasibility study for such a plant in 2010, and found in a separate 2011 survey that fertilizer is an “invest-ment priority” for 74 per cent of FNA members.

“The business case is compelling,” said Friesen, a former president of the Canadian Federation of Agriculture and CEO of FNA’s Strategic Agriculture Institute (FNA-STAG). “The real question is if and to what extent farmers want to gain a return on investment to offset the high cost of fertilizer rather than merely paying for it.”

Whether farmers take part in ProjectN or not, they’ll be the ones who indirectly pay for any new fertilizer plants in the future, as part of the base cost of their fertilizer, he said.

Since North America now imports almost seven million tonnes of fertilizer per year, FNA said, farmers are obviously “paying for all the plants that now exist and the profits they make.”

FNA FLP’s goal, FNA said, will be to bring farmers in as equity owners of a new N plant through committed purchase contracts for the plant’s products.

The new company’s business plan “provides a unique form of sta-bility and risk mitigation to underpin the success of the project, while providing farmers a certainty of supply of a key farm input.”

If ProjectN gets a strong response to its seed capital raise, “concrete announcements” on the plant’s scale and exact site would follow in a “relatively short time frame,” Friesen said.

Once the engineering work is completed, land secured and regula-tory approvals obtained, FNA FLP would move to raise equity for the plant, seek out operating partners and arrange financing for the build.

Fna seeks FaRmeR investment FoR n FeRtilizeR plant

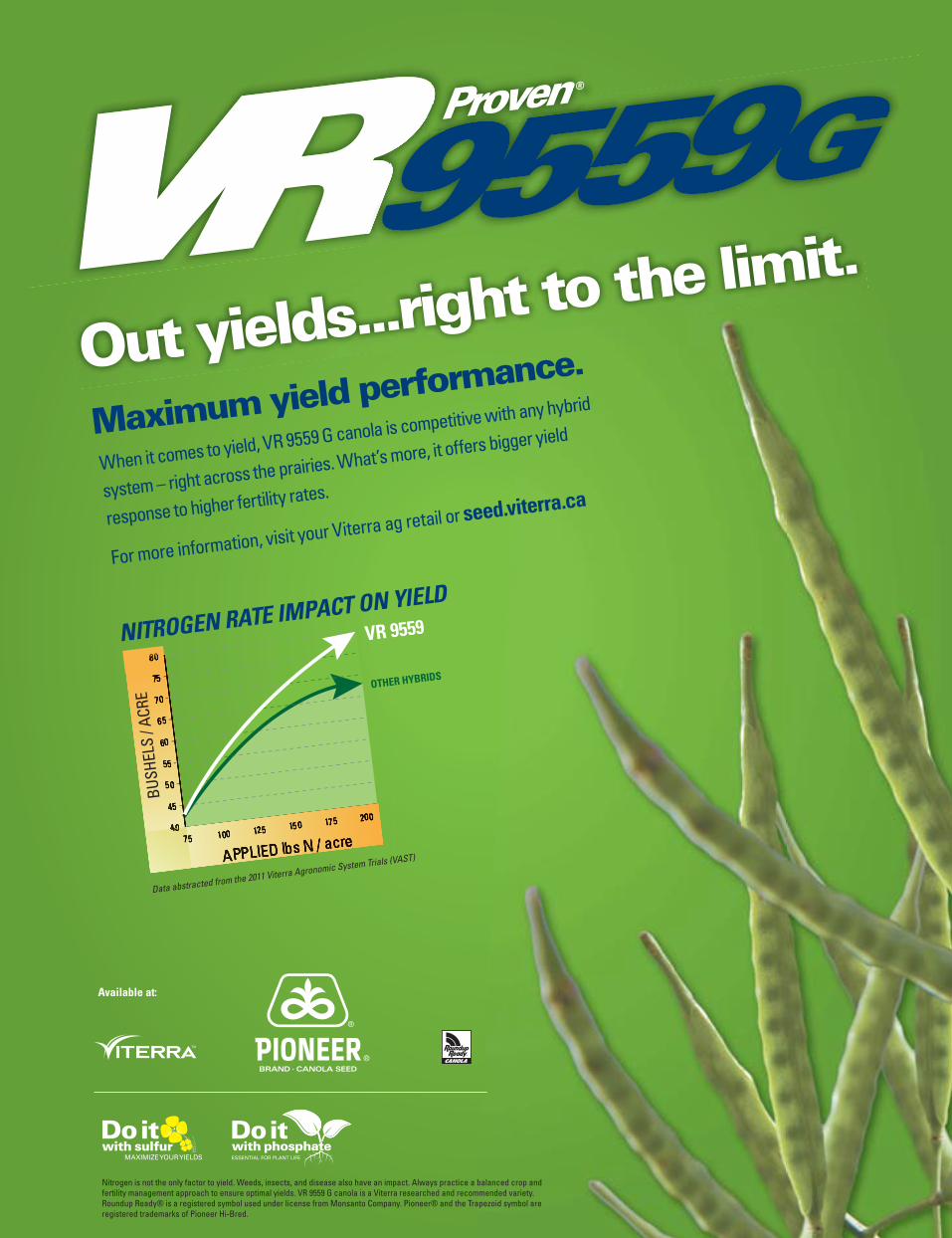

Out yields...right to the limit.

When it comes to yield, VR 9559 G canola is competitive with any hybrid

system – right across the prairies. What’s more, it offers bigger yield

response to higher fertility rates.

For more information, visit your Viterra ag retail or seed.viterra.ca

Maximum yield performance.

Available at:

Nitrogen is not the only factor to yield. Weeds, insects, and disease also have an impact. Always practice a balanced crop and fertility management approach to ensure optimal yields. VR 9559 G canola is a Viterra researched and recommended variety. Roundup Ready® is a registered symbol used under license from Monsanto Company. Pioneer® and the Trapezoid symbol are registered trademarks of Pioneer Hi-Bred.

NITROGEN RATE IMPACT ON YIELD

Data abstracted from the 2011 Viterra Agronomic System Trials (VAST)

Appointments

Burrows named Cigi direCtor, Client relations and CommuniCations

The former director of branding for the

Canadian Wheat Board is the new director of

client relations and communications for Cigi, the

former Canadian International Grains Institute.

Dave Burrows joined Cigi September 24,

the organization said in a recent media release.

Burrows brings over 30 years of market-

ing, client relations, branding and strategic

planning experience to his new role. At the

CWB he developed branding campaigns

domestically and in international markets to

promote Canadian wheat during his eight

years there.

Prior to his experience with the CWB,

Burrows held senior positions in strategic

planning, client services, branding and market-

ing for McKim Communications, Palmer Jarvis

DDB, the Winnipeg Free press and Hershey

Canada Inc.

As director, client relations and commu-

nications, Burrow’s responsibilities include

developing strategic business, marketing,

branding and communications plans that will

support industry and farmers in the promo-

tion of Canada’s field crops as well as manag-

ing Cigi’s growing list of commercial business

relationships and partnerships.

Give us your inputIf you have a milestone you feel should be noted in our regular Gleanings column,

please send the information, along with an electronic photo of any individual noted in the item,

to Crops guide editor Gord Gilmour at: [email protected].

8 CROPS GUIDE | NOVEMBER 2012

U.S. agri-food giant Cargill plans to build a second Canadian canola-crushing and processing plant in central Alberta in time for the 2014 harvest.

Cargill brass were at Camrose, Alta. recently to launch work on an 850,000-tonne-per-year crush plant just south of the com-munity, about 80 km southeast of Edmonton.

“The facility will have the capacity to process both conventional and specialty canola seed, which will enable us to significantly increase our contracting programs in the area,” Ken Stone, Cargill’s commercial manager for Canadian canola processing, said in a release.

A spokesperson for Cargill, which already runs the largest canola-crushing plant in Canada at Clavet, Sask., said the company expects to source canola within a 300-km radius of the new facility.

Cargill’s fellow processing giants Bunge and ADM operate crush plants respectively at Fort Saskatchewan, Alta., about 100 km north, and at Lloydminster, Alta., about 225 km east.

“Canola continues to be a very competitive crop for the Canadian grower and Camrose is an excellent location for value-added canola processing,” Mark Stonacek, president of Cargill’s North American grain and oilseed business, said in the company’s release.

In 2012-13, he said, canola acres in Canada were over 21 million, indicating the canola indus-try “will continue to grow, driven by competitive access to a large North American livestock industry for canola protein meal and continued strong demand for canola oil.”

Cargill’s other facilities at Camrose include the animal nutrition plant it built there in 1982, a Cargill AgHorizons grain elevator on the north side of town and an office for the company’s spe-cialty canola program.

Cargill plans major Canola Crusher in Central alta.

Still waiting on one last regulatory approval, Canada’s biggest grain handler and its proposed buyer now expect to seal their deal by mid-November at the latest.

Regina-based Viterra and its suitor, Swiss commodity giant Glencore International, said Wednesday that they have now extended the “outside date for completion of the acquisi-tion” to Nov. 15.

Apart from the usual closing conditions, the companies are waiting on just one last regulatory approval, from China’s Ministry of Commerce (MOFCOM), as per that coun-try’s Anti-Monopoly Law.

Viterra’s assets in China include a joint-venture investment of up to US$25 million in a canola-crushing facility in Fangchenggang, commissioned last year. Viterra also runs a trading office in Shanghai and a representa-tive’s office in Beijing.

Once MOFCOM’s approval has been received, Viterra and Glencore said, the two

companies will announce a specific closing date on which the formal acquisition will take place.

The two companies, which announced plans for Glencore’s friendly $6.1-billion take-over bid in March this year, said they “con-tinue to engage with MOFCOM to ensure approval as soon as possible.”

Canadian agribusinesses Agrium and Rich-ardson International are still set to buy a num-ber of Viterra’s ag retail, grain-handling and processing assets from Glencore, in deals worth $1.8 billion and $800 million respectively.

Those deals also require approvals, not yet granted, from Canadian authorities. Cal-gary-based Agrium, for one, recently said it expects to complete its deal for the bulk of Viterra’s Canadian and Australian farm sup-ply stores by the end of 2012 or in early 2013.

Successful conclusions to those sales aren’t required for Glencore’s takeover of Viterra.

Viterra – glenCore deal Close to Closure

Share your story, hear others and

learn more at AgricultureMoreThanEver.ca

POWERED BY FArM CrEdiT CAnAdA

“I’m really excited about what the future is in agriculture as a whole.I think more than ever it’s got to be run with a business plan and a sharp pencil.”

– Doug Seland, Alberta

it’s time to tell the real storyCanadian agriculture is a modern, vibrant and diverse industry, filled with forward-thinking

people who love what they do. But for our industry to reach its full potential this has to be

better understood by the general public and, most importantly, by our industry itself.

The story of Canadian agriculture is one of success, promise, challenge and determination.

And the greatest storytellers are the 2.2 million Canadians who live it every day.

Be proud. Champion our industry.

09/12-18723-2E M

18723_2E_M Gloves 10x13.indd 1 10/1/12 10:33 AM

W innipeg’s Inter-continentalEx-change (ICE) launched mill-i n g w h e a t ,

durum and barley futures last Janu-ary in anticipation of an open, freely traded wheat and barley market in Western Canada but, since that time, industry high hopes for success have been diminished.

“I’d be happier if there were higher volumes, there’s no question about that,” says ICE president and chief operating officer Brad Vannan.

ICE launched its new markets last winter to demonstrate the ability and support to provide open-market pric-ing, with the full understanding that initially, achieving a truly indepen-dently priced physical market while the Canadian Wheat Board still had a monopoly would be extremely dif-ficult, Vannan says. The task would be just that much more challenging given wheat isn’t forward priced like canola as quality can vary so much more at harvest time.

But Vannan adds any disappoint-ment he’s had has been curbed by the beginnings of growth and activity in the milling wheat contract, which is quoted actively and whose prices are accurate to the marketplace.

Vannan insists there remains con-siderable interest in ICE’s wheat mar-

ket, but would-be users are keeping their distance, at least for now.

“It’s unusable,” says commodity broker and trader Ken Ball of Union Securities. “It would be perilous for me to take my customers into a mar-ket like that, because with the low volumes and open interest, we could get trapped for weeks and weeks possibly and never be able to get out of that position if we needed to.”

Before even considering entering an order in milling wheat, Ball says he’d need to see the market consis-tently trade 500 to 1,000 contracts daily, with an open interest of at least several thousand contracts.

Although many traders would willingly participate, they’re first waiting to see significant volumes before taking the plunge.

“If there’s no liquidity, people don’t trade it. But if people don’t trade it, there’s no liquidity,” says Jonathon Driedger, senior analyst with FarmLink Marketing Solutions.

Certainly not helping matters is the fact domestic grain companies are perfectly content using U.S. mar-kets, which have the liquidity neces-sary to easily get in and out of posi-tions, notes analyst Errol Anderson of ProMarket Communications.

“They’re dealing with U.S. buyers now; they’re used to dealing with their U.S. contracts,” says Anderson.

“I hate to say it, but there just isn’t a whole heck of a lot of need — when you’re talking to an American buyer, he won’t think in Winnipeg wheat. He’ll be thinking Minneapolis or Kansas City or Chicago.”

Everyone in the know points out the difficulty of creating successful new markets, explaining even huge exchanges have tried and failed on that score numerous times.

Exchanges like London and the CME have attempted to launch futures contracts of commodities that are much larger than even our wheat market — which has the added burden of com-peting contracts in the U.S. — and have failed miserably, despite multiple resources and commercials at all stages of the supply chain, Driedger says.

“Many, many more new contracts fail than succeed. You kind of have the deck stacked against you from the start regardless,” says Driedger. “I’m sure some of the commercials here would rather see a contract traded domestically that they can deliver against and there’s less basis volatility. But at the end of the day, unless a lot of them are actively trading it and you’ve got activity on both the buy and sell side of the market, it’s going to have a tough time getting its legs underneath it.”

And the days of getting com-mitments from grain companies to

COVER STORY open market

10 CROPS GUIDE | NOVEMBER 2012

ICe searches for volumes; awaiting evolved cash market

B y R i c h a R d K a m c h e n

CaTCh 22

trade a new contract, as happened when canola was first introduced, are long gone.

At that time in the early 1960s, the scores of grain companies in existence agreed they’d all trade a certain number of canola con-tracts every day, and every night have x-amount of open positions on the books. After a couple months, liquidity developed, speculators were drawn in, and the canola mar-ket became functional.

Fast forward to today, where most of those grain companies no longer exist, and futures activity has gone from face-to-face transactions on a trading floor to the anonymity of computer screens.

“It was easier then, to get every-body to participate: they’re right there in the pit together,” says Ball. “But now, it’s all invisible, and it’s going to be harder to put pressure on people to get involved if they’re not right there.”

Many U.S. exchanges offer incen-tives to local traders to participate and thereby bolster volumes, and ICE is doing likewise.

“We provide a separate fee cate-gory for what we call liquidity provid-ers, so those traders pay much lower fees — in fact, right now, for the new products, it’s free,” says Vannan.

That alone, however, won’t be enough to get the new markets going. “It can help facilitate, but it’s more like the grease in the wheel rather than the wheel itself,” says Driedger.

HORSE BEFORE THE CARTVannan agrees, explaining that

liquidity providers need someone to trade against for the contract to be

relevant to them. He points out the physical — or cash — market, which remains in its infancy, will need to mature first before futures have a chance of taking off.

“You have to understand we didn’t have an open cash market until August 1,” says Vannan. “We haven’t had a freely traded wheat market in 70 years, and so it’s going to take a little bit of time for that marketplace to develop.”

The Prairie wheat and barley cash market has undergone a massive upheaval, something the industry is still working through. The CWB is still involved by offering pooling and flat pricing, but various grain compa-nies are also competing for farmers’ grain. And adding another dimen-sion to the changed playing field is Glencore’s acquisition of Viterra.

Moreover, with the U.S. drought causing grain prices to soar, farm-ers have delayed selling their crops. A number of farmers forward priced a significant portion of their canola — evidenced by record open inter-est in ICE’s canola contract in August — meaning those farmers have good cash flow and can afford to be patient and study their options. On top of that, they’ve been busy harvesting and determining the quality of their crop.

“The cash market’s still evolving and the futures market is derived from the cash market. So you need to be able to allow that cash market to evolve a little bit before there’s a clear understanding of what the dis-tinction within the Canadian market is,” Vannan says.

But getting the cash market to that level of development could easily take

two crop years, Vannan says the big grain traders have told him. And that’s why ICE is willing to be patient and not throw in the towel prematurely.

“If you see that there is growth and that the contract is moving for-ward, there’s something to be said for being patient. If we didn’t see that contract was making any progress at all, we might take a different view of it going forward,” Vannan says.

His confidence in milling wheat in particular becoming an active and suc-cessful market in Winnipeg reflects his belief in how much more relevant it is

“ I’d be happier if there were higher volumes, there’s no question about that.”

— Brad Vannan,COO, ICE

CROPS GUIDE | NOVEMBER 2012 11

PHOT

O CR

EDIT:

VIC

TORI

A AN

NE P

HOTO

GRAP

HY

SUPERIOR WEED CONTROLGet the advantage of superior annual and perennial weed control from Genuity® Roundup Ready® systems and capture the full yield potential of today’s elite canola genetics. www.genuitycanola.ca

Always follow grain marketing and all other stewardship practices and pesticide label directions. Details of these requirements can be found in the Trait Stewardship Responsibilities Notice to Farmers printed in this publication. © 2012 Monsanto Canada, Inc.

Continued on page 12

to domestic players versus competing U.S. markets. Whereas most U.S. mar-kets were created over a century ago around the principle of pulling grain into the centre of the continent to the Mississippi River, the Canadian system is the opposite, where grain is moved to the outside, either to the St. Law-rence Seaway or the West Coast.

“That creates a different pricing mechanism,” Vannan says, adding that growing conditions and harvest timing in Prairie spring wheat-grow-ing areas also differ from those in the U.S. As corn and soybeans move into traditional U.S. spring wheat acres, Canada becomes an even more important world supplier of spring wheat, he adds.

“We’ve got a contract that’s specifically designed for the Cana-dian marketplace, and we’ve got the Canadian marketplace becom-ing a more important source of sup-ply for hard red spring wheat out of North America. So we’re better posi-tioned going forward because we’ve designed a contract that’s really a 21st century contract, and one that was meant to integrate into the grain-handling system that we have today, not one that we had a century ago.”

DIVERGENCESignificant divergence between

the western Canadian cash situation and U.S. futures could also play a major role in attracting more busi-ness to the Winnipeg futures.

“There’d be some trade starting to develop, absolutely,” says Ander-son. “And there’d probably be some potential spread trading between our market and the U.S. A situation like that could possibly give our market a kick-start, which we badly need. If we can just get it, then suddenly everybody will start promoting it to their people and we have a market.”

Vannan notes the French futures exchange Matif ’s wheat market experienced just such a divergence years ago, which resulted in a mori-bund European contract gaining popularity very quickly.

“When you saw there was a fun-damental difference in how the Euro-pean wheat was moving from the way North American wheat was moving, that’s when the trading community saw a lot more value in having a dis-tinct futures market,” Vannan says.

But while Driedger admits such divergence could spur some activity, he doesn’t believe it would provide any guarantees of success.

“If there’s markets out of line, a lot of that work can be done through cash spreads rather than necessarily having a whole lot of futures transacted. A lot of that can just be done by commercials arbitraging cash markets if spreads get out of line,” Driedger says. n

T he former Canadian Wheat Board is plunging into canola marketing this crop year, but its efforts may be stymied by resis-tance from elevator companies.

While CWB reached handling agreements with all western Canadian grain companies for farmers’ deliveries of wheat, durum and barley contracted with the CWB, the same is not true for canola. Viterra, Richardson Inter-national, Cargill, Louis Dreyfus and Paterson Grain are not on board to accept farmers’ deliveries of canola on behalf of the CWB, leaving only 42 Prairie delivery points and one in B.C. available.

Brian Gwyer, CWB director of oilseed and pulse trading and sales, didn’t want to put a target on CWB canola sales this year, but conceded it would be better if the CWB had more elevator coverage.

The potential extra expense and time on the road to reach elevators that will accept canola contracted with the CWB may dis-suade farmers from pooling their canola, says Keystone Agricultural Producers presi-dent Doug Chorney.

“That really cuts their market share to just the areas around those delivery points,” agrees University of Saskatchewan agricul-tural economist Murray Fulton.

Western Canadian Wheat Growers Asso-ciation president Kevin Bender expects the CWB’s canola program will be small, espe-cially if there are handlers that aren’t going to participate.

“I suppose there are still the smaller com-panies and the inland terminals,” adds a market analyst who wished to remain anon-ymous. “However, I still wonder how many of those will want to give up bin space for CWB canola. Hard to say.”

But Derek Brewin of the University of Manitoba’s agribusiness and agricultural economics department, points out it took the CWB some time to negotiate its elevator agreements on wheat and barley. He also notes that canola is a very different market than wheat, with less quality variation and a huge domestic crush demand that doesn’t exist for wheat.

“Viterra, Richardson, Cargill, and Louis Dreyfus are involved in domestic process-ing and probably don’t value the CWB’s co-ordination or any foreign customer base in the canola market,” says Brewin. “They probably do value these things in wheat — we’ll see if that can be an advantage for farmers in the long run. The CWB seems to be managing wheat quality values better than the trade so far this year.”

And while 42 delivery points isn’t a lot, it still represents about 20 per cent of the total number of elevators, which may still be enough to cover a significant number of farmers.

“So the CWB might have some negotiat-ing power for rail service and export cus-tomers,” Brewin says.

Longer term, the elevators’ reluctance to deal with the CWB on canola may be a fore-shadowing of things to come. The CWB has five years to transition into a new entity, be it corporate or farmer owned, but either way, the existing grain companies would still have an added competitor to face, meaning it’s not in their interests for the CWB to be reasonably strong, says Fulton.

“They wouldn’t be able to bid on it because of competition issues, so that really means (it’s) the likes of Bunge that could come in and purchase it, which would be good for the industry as a whole, but wouldn’t be good for those that are in the business right now,” says Fulton.

The latter would also be true if the CWB became a farmer-run operation. “I wouldn’t think that would be particularly attractive to the existing firms… There has been a sense among some people, in the short run, there’s no advantage to the existing firms handling grain for the wheat board. The long-term profit incentive doesn’t look much better.”

“It’s one of those things where it’s a pain-ful death and it’s going to take an extra year or two. I don’t think they’ll be in it (market-ing in general) for very long,” adds Errol Anderson of ProMarket Communications.

POOLING ADVANTAGESLike with wheat, the theoretical advan-

tage the canola pool offers farmers is in helping them manage their risk, while also allowing them to spend more time on their crops as opposed to chasing commodity futures, according to CWB president and CEO Ian White.

“A big advantage to contracting with CWB is that farmers can sign first and choose their grain handler later. That means they can shop their grain around to get the best possible deal on handling and elevation fees.”

A segment of farmers has demonstrated an interest in the CWB pooling canola, going back to 2006 and the Manitoba Canola Grow-ers Association’s annual meeting, when a resolution was passed on alternative ways of marketing canola in order to shake up low prices and slow export sales.

Rick White, general manager of the Canadian Canola Growers Association lauds multiple selling options for farmers.

Turf WarMajor handlers reluctant to sign on for CWB canola collection

B y R i c h a R d K a m c h e n

COVEr STOrY open Market

12 CROPS GUIDE | NOVEMBER 2012

Continued from page 11

For some farmers, pooling may be an attractive option if they don’t have the time to market all of their grain themselves and are receptive to passing off some of that work.

But White, who has a 3,000-acre grains and oilseeds farm in southeast Saskatchewan with his wife, notes that while canola can take time to market, farmers have demonstrated the skills to do it. He adds farmers don’t need to rely on the CWB to attain an aver-age price either.

“For other farmers, they can dollar-cost average their sales across the year without the CWB if they wanted to.”

Pooling may attract farmers during times when prices are down but the grower believes they will climb higher, says Western Cana-dian Wheat Growers Association president Kevin Bender. But with prices as strong as they’ve been, farmers have been trying to lock them in, especially those who believe values will fall. Also limiting interest in the canola pool is the fact many farmers would have sold canola prior to the CWB’s announcement, Bender says

“The majority of farmers are more likely to take the cash price spot market or basis contract approach to pooling their risk,” says Chorney. “But good for (CWB) for trying it out. Even if we don’t participate in the pooling program, having the wheat board

out there setting prices makes the line companies more account-able, and any time you get more competition for our grain to be bought, it’s a good thing for farmers.”

The anonymous market analyst hadn’t heard of much farmer interest in the canola pool, but believes there will always be some who’ll find the averaging approach a pool provides appealing.

“As such, I can’t see why some growers won’t put a portion of their production into the pool; if for no other reason, to see how it goes and to see how the results compared to their own market-ing,” the market analyst says. “Of course, in this debate there are always growers who will use the CWB, and those who won’t touch a board contract if it was written on a gold slab. That issue will impact how much of the market the CWB finally attracts.”

CWB’s pooling option offers value for both customers and farmers, says Gwyer.

“We have customers who are canola customers as well as wheat customers that have long-term relationships with us. Essentially, customers want to deal with somebody they have experience with, so there’s a large number of our customers who’ve always wanted to buy canola from us.”

For farmers, pooling becomes a much more attractive option during periods of particularly volatile markets, he says.

“We’ve had a summer and fall where prices went mainly up, but I think farmers are already seeing that prices can move quite a lot on canola… In a volatile market with a lot of uncertainty, it’s a hedge for people to use,” Gwyer says, but adds he wouldn’t ever recommend anybody put 100 per cent of their grain into a pool.

The CWB’s Harvest Pool sign-up deadline is October 31. The marketing period runs from harvest to June 30, 2013. Initial pay-ments for canola equal approximately 75 per cent of anticipated final Harvest Pool returns. �

In this debate there are always growers who will use the CWB, and those who won’t touch a board contract if it was written on a gold slab.

www.roundup.ca www.genuitycanola.ca

Fall checklist BookGenuity RoundupReadycanola

BookRoundup WeatherMAXherbicide

Bookwintervacation

checklist

Always follow grain marketing and all other stewardship practices and pesticide label directions. Details of these requirements can be found in the Trait Stewardship Responsibilities Notice to Farmers printed in this publication. Roundup WeatherMAX® is a registered trademark of Monsanto Technology LLC, Monsanto Canada Inc. licensee. © 2012 Monsanto Canada, Inc.

engineered to work together.Book Roundup WeatherMAX® herbicide with your Genuity® Roundup Ready® canola this fall.

CROPS GUIDE | NOVEMBER 2012 13

MORE THAN 1,000 WORDS

The good folks at the Canadian Malt

Barley Technical Centre (CMBTC) pilot

brewery in Winnipeg were extremely

helpful and guided him through the

intricate world of brewing and malting.

For those who aren’t familiar with this

operation it’s a unique asset for the

Canadian malt barley industry.

Their claim to fame is their ability

to take your malt barley and from it

produce any beer in the world to the

spec of the brewing company. They’re

an essential technical resource to prove

to customers that your products will

work in their recipes.

Malting: The starting point is fresh malt (1)

which is steeped in warm water for a

day or two to bring it to the required

moisture level (2). It’s then transferred

to the sprouting vessel (3) where cool,

moist air is blown through to encourage

sprouting (4). The final malting stage is

kiln drying with hot air which produces

a finished malt (5) in this case a

standard malt for a pale lager.

Brewing:Taking it to the next step, the malt

barley may, depending on the recipe,

be mixed with other grains like ground

wheat (6), corn (7) or rice (8).

A cereal cooker (9) is then

used to cook a mash.

14 CROPS GUIDE | nOvEMEBER 2012

Barley It’s said that a picture is worth 1,000 words and as part of our ongoing effort to present Crops Guide readers with a clearer view of activities in the agriculture world, we sent photographer Charles Lumsden on a freelancer’s dream assignment — a brewery tour.

1

3

2

6

4

5

7 8 9

CROPS GUIDE | NOVEMEBER 2012 15

The next stop is the mash tun (10)

where water is added and the

mixture is heated. This stage is where

enzymes in the malt break down

the starch into fermentable sugars,

typically maltose, forming the liquid

basis for beer, known as a wort.

From there it’s on to the lauter

tun (11) where the liquid is

separated from the spent grain.

In the kettle (12) hops are

added (13) and the wort is

sterilized by raising its temperature

to stop the enzymatic action.

A whirlpool tank (14) is then

used to separate the remaining

vegetative matter from the wort

which is then cooled (15).

The wort is then placed in the

fermenter (16), where yeast is added.

It consumes the sugar in the wort

over the course of the next seven to

14 days, and produces ethanol as a

byproduct of that process.

Bottled beer (17) is then pasteurized

(18), while draft beer (19) is not.

10 11 12 13

14 15

16

17

18 19

to beer

WESTRIGHT ACROSS THEHIGH PERFORMANCE

CEREALS

Part of your well-balanced farm business.

CDC Stanley and CDC Abound were bred at the Crop Development Centre, University of Saskatchewan.

High yield potential and reliable disease packages make Viterra’s High Performance Cereals the trusted choice for western Canadian growers. With popular varieties such as Xena, AC Navigator, and 5700PR, growers continue to have a trusted source for proven success in the field. Contact your local Viterra Ag retail or visit seed.viterra.ca to learn more about our complete High Performance Cereals line-up. Book your 2013 cereals today.

GROWING REGIONS

WESTRIGHT ACROSS THEHIGH PERFORMANCE

CEREALS

Part of your well-balanced farm business.

CDC Stanley and CDC Abound were bred at the Crop Development Centre, University of Saskatchewan.

High yield potential and reliable disease packages make Viterra’s High Performance Cereals the trusted choice for western Canadian growers. With popular varieties such as Xena, AC Navigator, and 5700PR, growers continue to have a trusted source for proven success in the field. Contact your local Viterra Ag retail or visit seed.viterra.ca to learn more about our complete High Performance Cereals line-up. Book your 2013 cereals today.

GROWING REGIONS

18 CROPS GUIDE | NOVEMBER 2012

O ilmen say energy comes out of the ground and New Energy Farm’s Dean Tiessen of Leamington, Ont. concurs — but with a crucial difference.

A greenhouse vegetable grower, Tiessen heats his buildings by burning the woody stalks of Miscanthus giganteus, a perennial grass that he grows on some of his marginal land.

It’s early days yet, but more and more observers think purpose-grown energy crops may be the future of farm-ing energy, rather than simply repurposing food crops.

“It’s truly an amazing crop,” Tiessen said. “About 40 per cent of our operating cost is energy because of where we’re located. We take this wonderful energy grass, use it as fuel and turn it into tomatoes for both domestic and export consumption.”

Energy is a tricky issue. We’re completely sur-rounded by it but it’s difficult to secure a ready source of usable, storable and transportable energy. For the last 100 years we’ve been using fossil fuels, the diesel that feeds the tractor, the natural gas that heats the build-ings, runs the boilers and fuels the crop dryers and the gasoline that powers the small trucks or quads.

Natural gas and petroleum are a stored chemi-

cal form of solar energy captured by green plants in another age of the planet, pressed and processed for bil-lions of years. It’s stored geologically until we extract it, refine it and sell it. Fossil fuels have served us well but they also present us with two tightly related problems.

The first is the cost. Basic economics states that the price will always trend upward as the demand outstrips the supply. It’s a finite resource so the more we use, the less we have — and we use an awful lot. The second problem goes to the very heart of how we power our society, because fossil fuels are a dense pack-age of energy that are easily contained, relatively safe and very portable. They’re very good at what they do and we’ve developed effective technology that uses them very well.

Over the next century, as the supply drops, it will be both economically beneficial, as well as socially and environmentally responsible, to find workable alterna-tives. It’s doubtful that we’ll find a straight replacement so we’ll depend on a combination of different methods and this will still include petroleum. For Tiessen’s farm, energy grass is a good fit.

grasslotOne Ontario vegetable grower is using marginal land to grow energy grass — call it a new take on the old woodlot practice. It’s part of a growing interest in energy-only crops

B y G o r d L e a t h e r s

Bioenergy

Continued on page 20

Prod

uced

by:

SeC

an

Prod

uct/

Cam

paig

n N

ame:

SeC

an V

espe

rD

ate

Prod

uced

: Oct

ober

201

2

Ad N

umbe

r: SE

C-VE

SP-1

2CG

Publ

icat

ion:

Cro

ps G

uide

Trim

- 10

” x

13”

Ble

ed -

10.5

” x

13.5

”

Genes that fit your farm.®

800-665-7333www.secan.com

Genes that fit your farm.®

800-665-7333www.secan.comDeveloped by Agriculture & Agri-Food Canada, Winnipeg.

‘AC’ is an official mark used under license from Agriculture & Agri-Food Canada. Genes that fit your farm® is a registered trademark of SeCan.

SEC-VESP-12CG

NEW

AC® Vesper VBMIDGE TOLERANT WHEAT

We’re #1!

NEW

AC® Vesper VBMIDGE TOLERANT WHEAT

We’re #1!

✔ #1 for yield in SaskSeed ✔ #1 for yield in Seed Manitoba✔ Best FHB rating in a

midge tolerant wheat

✔ #1 for yield in SaskSeed ✔ #1 for yield in Seed Manitoba✔ Best FHB rating in a

midge tolerant wheat

SEC-VESP-12T_CG.qxd 10/5/12 1:43 PM Page 1

20 CROPS GUIDE | NOVEMBER 2012

“It’s a carbon-neutral opportunity but the main thing is it’s economical,” he said. “A lot of our focus has been on economics but there’s also significant reduction in environ-mental impact and we need economical solu-tions that will reduce environmental impact without inhibiting economic growth.”

Tiessen is essentially employing a plant to capture solar energy through photosyn-thesis and store it as a carbohydrate. When he burns the grass the energy is released as heat and used to keep the greenhouse at the perfect temperature for growing those tomatoes.

It’s a variation on an older idea when farmers relied on the woodlot, a small patch of forest within the family holdings, to provide some timber as well as firewood. Energy grass is simply a wood substitute. The Europeans started using M giganteus as a fuel source in the 1980s and they’ve found it can grow up to 10 feet tall in one season with a yield of 10 tons per acre with rela-tively little input.

“This is a small boiler system in Germany that is creating heat to dry paint as an indus-trial process as well as to heat a day-care centre and six homes,” Tiessen said. “And there’s a small farmer in the area who’s growing the grass. He operates this boiler and he’s created a nice little local utility.”

Burning the grass is a handy way to use locally grown energy. But, if you want to bat in the bigger leagues and market the product on a larger scale, you have to be able to convert a lignin/cellulose stalk to something more storable and more trans-portable. There are two ways you can do that, according to Tom Voigt, a turf grass specialist with the extension department at the University of Illinois.

“You want to densify the material so that you can get as many BTUs per truckload as you can move,” he says. “It has to be chopped up. In some places people make pellets or briquettes and these are a couple of different ways to handle it.”

Transporting unprocessed stalks means a lot of the package is made up of air. We’re not interested in filling up a lot of premium transport space with air. A forage chop-per will take that out and make the fuel denser and this may be suitable for short-haul transport.

The future of biomass energy is deeper and more complex than that. A really good, and much more versatile fuel would be suit-able for applications beyond boilers. We need to get it into gas tanks. We have to find an energy-efficient way to break those long chain polymers like lignin, a major compo-nent of wood, and cellulose, the principal component of plant cell walls. In an ideal world we’ll break the long chain molecules into short chain carbohydrates and these can be fermented into an alcohol.

“British Petroleum who is funding a big renewable energy project at the University

of Illinois and the University of California Berkeley,” Voigt says. “They’re looking at liq-uid transportation fuels and, as part of this project, we’ve developed one of our biggest experiments, a 320-acre energy farm.”

The farm is an initiative of the Energy Biosciences Institute, the formal partner-ship between the University of Illinois, UC Berkeley and British Petroleum (BP). The idea is to find what plants will provide the highest yields of energy stock with the low-est inputs, what rotations of different crops will work most economically and different methods of processing biomass into usable energy. There’s also tremendous potential to take land that’s not suitable for food crops and put it to work.

“The United States has pulled upwards of 800 million acres out of agriculture and put them into protected lands or what they would call CRP lands and CRP lands are usually paid by the government for some-

one to keep it out of agriculture,” Tiessen says. Those lands were set aside because they weren’t agriculturally productive.”

These lands can be productive with the right kind of crops and the long-term, peren-nial energy crops may be the way to do that without compromising food production. There are scientists looking at species such as switch grass or recreating a native prairie system, a stable, low-maintenance polycul-ture. Voigt says there’s a long way to go but it’s a step in the right direction.

“I think from an energy security point of view, being able to produce an energy crop means that we’re not as dependent on countries that don’t necessarily like us and that’s a positive No. 1. No. 2, we’re looking at a method of rejuvenating or upgrading the rural economy and that’s certainly a posi-tive. We see this as maybe a way to provide good opportunities in rural areas for college-educated agriculture kids.” �

Get the N that delivers all seasoN loNG.

ESN® SMART NITROGEN® is the best choice for your farm because timely nitrogen feeding enhances yield and crop

quality. With a single application, ESN nourishes crops throughout the growing season, so you get everything you

can out of your nitrogen investment. Get the facts from your retailer, or visit SmartNitrogen.com/cg.

Agrium Advanced Technologies (AAT) is a strategic business unit of Agrium Inc. AAT produces and markets controlled-release nutrients, micronutrients and plant protection products for sale to the agricultural, professional turf and ornamental markets primarily in North America.

©2012 Agrium Advanced Technologies. ESN; ESN SMART NITROGEN; SMARTER WAYS TO GROW A SMARTER SOURCE OF NITROGEN. A SMARTER WAY TO GROW and AGRIUM ADVANCED TECHNOLOGIES and Designs are all trademarks owned by Agrium Inc.

08/12-17798-07

BIOENERGY

Continued from page 18 It’s a carbon-neutral opportunity, but the main thing is it’s economical. A lot of our focus has been on the economics.

— Dean Tiessen, New Leaf Energy Farm

Starting in November Cigi will deliver a series of new crop infor-mation seminars to customers of Canadian wheat. With partici-pation from the Canadian Grain

Commission and Canadian grain exporters invited to join the missions, Cigi technical staff will meet with customers in Southeast Asia, Europe, Latin America, and North Africa.

“This year will be very different from the past when we travelled with the Canadian Wheat Board to deliver crop and processing information to their customers,” says Earl Geddes, Cigi executive director. “This time we’ve invited a number of Canadian grain exporters and their customers to the seminars.

“The industry has made it clear they want to be involved in the process so their partici-pation this year is important so they can pro-vide input in the future,” he says. “We are covering a lot of area and this is the first time Cigi is initiating these seminars on our own.”

Geddes stresses that the seminars are cus-

tomer focused, targeting buyers of Cana-dian wheat who are willing to pay the most for quality, and that other competitors such as the U.S. are undertaking similar efforts. “This is about Canada putting its best foot forward and making sure the information customers receive is what they need to make constructive decisions about buying western Canadian grain. We have a significant range of participants expected at these meetings, usually industry players at the senior level, the most important buyers. ”

He says farmers may be interested to know that Canadian grain companies buying their wheat for export are active in this type of wheat promotion, aside from conducting any of their own direct-marketing activity.

“What’s also different this year is rather than doing company-specific new crop seminars, Cigi will be holding regional seminars inviting all customers from the same area,” Geddes says. “This effort is more about wheat promotion, market development and customer care.”

Ashok Sarker, head of Cigi Milling Tech-nology, who has participated in new crop missions since they started in the mid-1990s, says the seminar information is crucial to buyers and millers as their customers expect the same flour quality from year to year.

“It’s the obligation of millers to fulfil their customers’ requirements and grain buyers from milling companies to make sure that millers are happy with the purchases,” he says. “This is a very involved and com-plicated process because there are a lot of unknowns during new crop. Customers want information on the quality of Canadian grain as soon as possible so they can put the pieces together to get the best deal. They want to know about the (flour) processing qualities — not just about protein, grade, and class — and wherever possible to find out about how to optimize the processing of wheat from a given crop year so they get the most out of it.”

The new crop assessment done by Cigi’s technical staff provides customers with an early look at quality information in advance of the annual CGC harvest assessment. Four major grain companies are submitting grain samples to Cigi, covering five regions in Western Can-ada, from which the composite samples will be created. Portions of the original samples will be analyzed at Cigi for the companies and the rest will be used for the new crop composite sam-ples to determine wheat quality characteristics by class, grade and region.

“Dealing directly with the grain compa-nies instead of receiving the samples just from the CWB as was done in the past is the only change with this testing,” says Sarker. “We will analyze and evaluate the composites for end-use quality as we have done before. This way we can continue to provide the custom-ers of Canadian grain with the same level of information, with the same speed, detail and regional breakdown, and give them a good overview of the quality of the new crop.”

He adds that the first-hand information is also valuable for Cigi to access throughout the year for technical programs and cus-tomer assistance.

“What we’re doing is very important for customers as they won’t miss one step in this whole process,“ says Sarker. “They saw us at the last new crop seminars with the CWB and are seeing us again which gives them confidence the system is working well and is going full steam ahead as it always has. We’re maintaining that continuity with cus-tomers which is important for them.” �

Get the N that delivers all seasoN loNG.

ESN® SMART NITROGEN® is the best choice for your farm because timely nitrogen feeding enhances yield and crop

quality. With a single application, ESN nourishes crops throughout the growing season, so you get everything you

can out of your nitrogen investment. Get the facts from your retailer, or visit SmartNitrogen.com/cg.

Agrium Advanced Technologies (AAT) is a strategic business unit of Agrium Inc. AAT produces and markets controlled-release nutrients, micronutrients and plant protection products for sale to the agricultural, professional turf and ornamental markets primarily in North America.

©2012 Agrium Advanced Technologies. ESN; ESN SMART NITROGEN; SMARTER WAYS TO GROW A SMARTER SOURCE OF NITROGEN. A SMARTER WAY TO GROW and AGRIUM ADVANCED TECHNOLOGIES and Designs are all trademarks owned by Agrium Inc.

08/12-17798-07

PRODUCT PROMOTION

CROPS GUIDE | NOVEMBER 2012 21

Road showCigi new crop seminars promote Canadian wheat to customers

B Y E L L E N G O O D M A N , C I G I

Warren libbyPresident of

Savvy Farmer

22 CROPS GUIDE | NOVEMBER 2012

C a n a d a h a s a n extremely demand-ing regulatory sys-tem for crop protec-tion products, which

is a good thing in terms of produc-ing safe and effective products with minimal environmental impacts.

Where it can be a bit more bur-densome however, is when this high bar limits the number of tools you find in your chemical toolbox when it’s time to hit the field and grapple with the production chal-lenge of the day.

This rigorous registration system works against broad labels that cover a wide variety of crops, as each crop fre-quently requires its own separate data and research, under local conditions. This tends to encourage companies to take a strategic approach, and apply for a shallow label to get their prod-ucts onto market more quickly, and only then work towards adding more crops and pests to the label after their product is out and generating revenue.

From a producer perspective this can make for real frustrations. For example soybean growers in the Red River Valley of Manitoba might look just a few miles to the south and see producers spraying a product they’re only legally allowed to use on canola or edible beans.

For these reasons the next time you run into your local BASF represen-tative, it might not be a bad idea to give them a little pat on the back. The company not only registered its new fungicidal active ingredient fluxapy-roxad here in Canada, it also went the extra mile to create and register several end-use brands that targeted multiple crops right from day one.

BASF has registered six products containing fluxapyroxad, and by my count, these products can be used on over 150 different crops to control a wide spectrum of diseases. Chances

are very good that there will be a fluxapyroxad product for a crop you will be growing in 2013.

Our understanding is that BASF has chosen the brand name XEMIUM for these new prod-ucts, which have both preven-tative and curative activity. As a result Xemium can control diseases through several stages of the fungal life cycle including spore germina-tion, germ tube growth, aspersoria formation and mycelia growth.

Xemium is labelled to control a

broad range of diseases belonging to the following major classes: Asco-mycetes, Basidiomycetes, Deutero-mycetes, and Zygomycetes. These groups include blights, moulds, rusts, leaf spots, mildew, and even seedling diseases, covering several of the key disease groups affecting many crops.

One of the key claims of Xemium is that it exhibits outstanding mobil-ity in both the plant and its roots. It enters the “plumbing system” of the plant, providing plant-wide distri-bution. This feature should provide some forgiveness for less-than-per-fect application techniques. Perhaps even more interesting is the claim that rainfall can somehow revive Xemium to give continuous protection during prolonged disease periods. If true, this feature in itself should be worthy of giving Xemium a try next season.

In recent years there has been a lot of talk that the invasion of so many generic brands will mean that the big discovery companies will no longer be interested in registering

innovative products here in Canada. I think that BASF’s introduction of Xemium proves that theory wrong, since this one is definitely innova-tive and looks like a real winner.

Another factor that’s beginning to dissipate is the “Roundup effect,” as its been dubbed, which refers to the efficacy and affordability of glypho-sate products. Because they, in tan-dem with herbicide-tolerant crops, were so cheap and effective many say they discouraged companies from making new investments in herbi-

cide products, and some companies even halted for a time their discovery programs aimed at identifying new chemical compounds that could form the basis for the next generation of active ingredients.

Today, however, glyphosate-tolerant weeds are a real threat to this product’s long-term efficacy. The appearance of glyphosate-resis-tant kochia in Alberta and giant ragweed in Ontario underlines the importance of new research, and crop protection companies have begun to respond with a greater focus on new products.

It may take a few years, but I fully expect that this work will result in another flush of innovative weed-control products arriving on the Canadian market. n

Warren Libby is president of Savvy Farmer, a web-based service for farmers and crop protection dealers. He previ-ously held leadership positions in several crop protection companies and is the for-mer chairman of CropLife Canada.

Innovation… alive and strongRecent developments in the crop protection industry should help alleviate concerns that innovation in the sector is on the wane

CROP PROTECTION

Do you have a crop protection issue you’d like Warren to write about? Send any suggestions to [email protected].

The next time you run into your local baSF representative, it might not be a bad idea to give them a little pat on the back.

F100-25374-1-Authority_Charge-Crops_GuideColor: 4/colorSize: T - 8”x11.5 B - NO BLEED Crops GuideSIZE A

Now Registered in Flax, Field Peas, Chickpeas and Sunfl owers

Always read and follow label directions. FMC and Authority are registered trademarks and Investing in farming’s future is a service mark of FMC Corporation. ©2012 FMC Corporation. All rights reserved. F100-25608 10/12

• New mode of action (Group 14) –weed resistance management

To learn more about Authority® Charge talk with your retailer today!

Excellent solution for Kochia and other tough weeds

• Early weed removal benefits of pre-emergent–controls flushing weeds, higher yields due to less competition with the crop

F100-025608-1-Authority_Charge- Crops_Guide.indd 1 10/12/12 10:06 AM

Agri fibre

24 CROPS GUIDE | NOVEMBER 2012

E xcess cereal straw has been a problem in southern Manitoba for as long as they’ve been growing wheat, oats

and barley in the region.That’s hardly surprising because

the Red River Valley was a tall grass prairie zone, where outsized bio-mass was fostered by higher annual rainfall than the rest of the Prairies.

For growers that’s meant a serious management challenge year after year as they’ve struggled to incorporate the residue or resorted to burning.

It’s a situation that’s caused more than one entrepreneur to look at the waste fibre and see an opportunity. Notably a now-defunct strawboard plant at Elie, Man. attempted to con-vert straw to building materials.

The key problem there was a

typical cart-and-horse conundrum familiar to any entrepreneur — how to build a market for an untried product. One Winnipeg-based entre-preneur thinks he’s found the key to this challenge in a cereal-straw based paper that’s currently being manufactured in India.

Jeff Golfman, co-founder and president of Prairie Pulp and Paper, is bringing “Step Forward” paper to mar-ket across Canada throughout Canada to prove there’s a market, a crucial hurdle to clear the way to building a production facility in Manitoba.

“To build a straw-based, tree-free paper mill in Manitoba, we need to have sales numbers of Step Forward paper reflecting a public demand for it in Canada,” said Golfman. He anticipates achieving that demand within a couple of years.

Prairie Pulp and Paper is a research, development, sales, and marketing company led by Golf-man, former Manitoba finance min-ister Clayton Manness (chairman),

Canada’s #1 source for pest control information

• Find the ideal treatments for any crop situation • Identify over 1,000 weeds, insects & diseases • Find any Label or MSDS sheets in one spot • Keep pest control records with a click of the mouse • Information is updated weekly

Let Savvy Farmer simplify pest control on your farm

In 2012 Savvy Farmer will bring users even more valuable information. To learn more, please visit

www.savvyfarmer.com

Phot

o cr

edit:

ww

w.Pr

airi

e-Pa

Per.

com

SteP forward PaPer iS now available in StaPleS outletS acroSS canada and a u.S. launch iS Planned. backerS Say thiS indian-made Product will helP develoP a market for the new Product which may reSult in a manitoba PaPer Plant in the future.

A whole new kind of “green” pAperB y r e B e c A K u r o p A t w A

a U.S.-based venture capital group and a consortium of public sector, R&D scientists, engineers, as well as marketing, sales, and agricultural experts.

A key investor and champion of Step For-ward paper is actor Woody Harrelson, who has been a friend and business partner of Golfman’s for 14 years.

“Woody has been an environmentalist and activist for many years,” said Golfman. “What is particularly important to him is saving trees from being cut down.”

Golfman says the project is a win-win for everyone — from farmers reaping extra income, to spared trees, low-carbon footprint, and Canadians enjoying affordable, quality paper, something he insists is going to be important well into the future, regardless how communications technology evolves.

Although today’s world is a digital one, society continues to go through hard copy paper as much as ever.

“The paperless office is a myth,” said Golfman. “People still like reading books in traditional paper format. Finding an alter-native paper source makes so much sense. We’re saving trees from being cut down by using wheat straw instead of forest fibre.”

Golfman (44), who was born in Vancou-ver and raised in Winnipeg, has been on the forefront of working to make the world a bit greener with past projects like founding Winnipeg’s Blue Box curbside recycling pro-gram, youth environmental education, and organizing environmentally themed events.

Golfman said he became interested in paper from agricultural fibre because it seemed like an obvious alternative to har-vesting trees: “Making paper from renew-able agricultural fibre simply makes sense.”

The current formulation of the paper is 80 per cent wheat straw and 20 per cent Forest Stewardship Council-certified wood fibre. Golfman says it’s aimed at home and office use as well as the commercial printing market. With worldwide patents pending on its process, Golfman sees the potential to establish Canada as an international leader in agricultural fibre paper production.

“The straw we buy from farmers is what is left over after food has been harvested — it’s agricultural waste turned into something very useful,” he said.

The straw fibre paper was launched nationally in Canada in August through 335 Staples business supply stores and a U.S. rollout is currently in the planning stages. �

CROPS GUIDE | NOVEMBER 2012 25

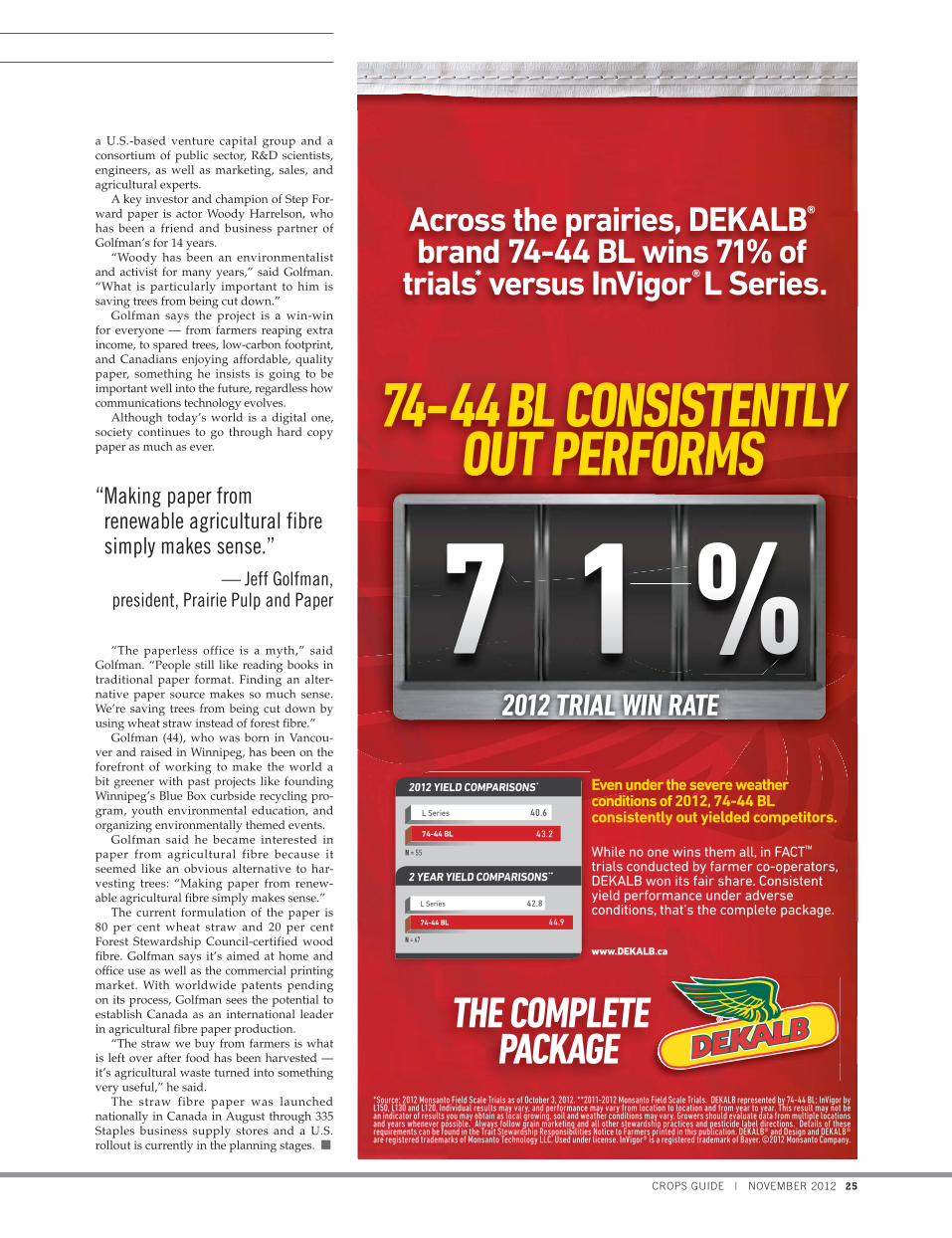

74- 44 BL CONSISTENTLY OUT PERFORMS

Across the prairies, DEKALB® brand 74-44 BL wins 71% of

trials* versus InVigor® L Series.

Even under the severe weather conditions of 2012, 74-44 BL consistently out yielded competitors. While no one wins them all, in FACT™ trials conducted by farmer co-operators, DEKALB won its fair share. Consistent yield performance under adverse conditions, that’s the complete package.

*Source: 2012 Monsanto Field Scale Trials as of October 3, 2012. **2011-2012 Monsanto Field Scale Trials. DEKALB represented by 74-44 BL; InVigor by L150, L130 and L120. Individual results may vary, and performance may vary from location to location and from year to year. This result may not be an indicator of results you may obtain as local growing, soil and weather conditions may vary. Growers should evaluate data from multiple locations and years whenever possible. Always follow grain marketing and all other stewardship practices and pesticide label directions. Details of these requirements can be found in the Trait Stewardship Responsibilities Notice to Farmers printed in this publication. DEKALB® and Design and DEKALB® are registered trademarks of Monsanto Technology LLC. Used under license. InVigor® is a registered trademark of Bayer. ©2012 Monsanto Company.

www.DEKALB.ca

OUT PERFORMSOUT PERFORMS

%2012 TRIAL WIN RATE

7 1N = 55

2012 YIELD COMPARISONS*

2 YEAR YIELD COMPARISONS**

N = 67

44.974-44 BL

40.6L Series

74-44 BL 43.2

42.8L Series

“ Making paper from renewable agricultural fibre simply makes sense.”

— Jeff Golfman,president, Prairie Pulp and Paper

canola

26 CROPS GUIDE | NOVEMBER 2012

T hink countries turn a blind eye to trace amounts of unapproved products or pesticide residues? Think again.

Ever since European test labs discovered an unapproved geneti-cally modified trait in a Canadian flax sample in 2009, the Canadian flax industry hasn’t been the same. Flax sales to Europe before the dis-covery of Triffid in shipments were 400,000 tonnes per year, and now they’re 30,000 tonnes, reports the Flax Council of Canada. A good por-tion of that drop is because of Triffid.

Herbicide-tolerant flax variety Triffid was developed in Saskatoon but never commercially produced.

It was deregistered because cus-tomers didn’t want it. Yet, almost a decade after the breeding program shut down, trace amounts of seed with Triffid genes were found in Canadian flax delivered to Europe. The European Union closed its doors to Canadian flax, and then implemented testing of all ship-ments before sales could resume. Testing continues to this day.

This is not a food safety issue, but it’s still a very costly trade disruption, the Flax Council of Canada reports.

Pesticide residue on seed can also lead to trade disruptions. Just ask edible bean growers. In the mid-2000s, a delivery of pinto beans from Alberta to the U.S. was detected

with 0.021 parts per million (ppm) of vinclozolin — the active ingredi-ent in Ronilan. This was well within the Canadian maximum residue limit (MRL) of one ppm, but Ronilan was not licensed in the U.S. for use on pinto beans. In that case, the approved MRL for vinclozolin on pinto beans in the U.S. was zero.

“The case helped propel the har-monized approach that U.S. and Cana-dian regulators take in setting MRLs on a continental basis, but at the time it caused a disruption in trade as buyers and sellers on both sides of the bor-der stepped back to determine what the impacts were on them,” says Mark Goodwin, pest management co-ordina-tor for Pulse Canada.

For the canola industry, given its size and value to Canadian farm-ers, any market disruption could be very costly, says Curtis Rempel, vice-president of crop production for the Canola Council of Canada.

“We want to be proactive when it comes to providing safe food and meeting key markets’ food safety rules,” Rempel says. “Everyone, including every individual canola grower, has a responsibility to pro-tect our markets. This is the motiva-tion behind the Canola Council’s Export Ready program. We want to prevent trade interruptions.”

Get to know each product’s PHIAn important restriction for each

pesticide is its pre-harvest inter-val (PHI), which is the minimum days between pesticide spraying and when the crop is swathed or straight combined.

“The name pre-harvest interval

is confusing because growers often think of ‘harvest’ as combining,” says Rempel, “but the PMRA defi-nition of harvest is the removal of a crop from its base — the cutting.”