1spidi2.iimb.ernet.in/~networth/ccs/2005/561 ccs... · web viewa bridge is, in essence, short term...

TRANSCRIPT

CCS Report

CCS ReportPresented to

Professor Ravi Anshuman & PGP Office Indian Institute of Management, Bangalore

OnAugust 29, 2006

TowardsPartial Fulfillment of the Requirement for the

Post Graduate Programme

Submitted by

Vengat Krishnaraj V ( 0511127)Soudabi N (0511190)

Contents

Need for the study

1. Overview of venture capitala. Historyb. Definition

2. Snap shop of the global VC industry in 2006a. The US venture capital industryb. The European VC industryc. The Israeli VC industryd. The Chinese VC industry

3. An academic look and literature survey of the Venture capital cyclea. Deal sourcingb. Due-diligencec. Valuationd. Deal structuringe. Post financing engagementf. Exit

4. The Indian VC industrya. Overview

i. Historyii. Size, activity, investments,

iii. trendsiv. sources of fundsv. active players

vi. Peculiarities of the Indian industry5. Case studies

a. Suzlon energyb. ICICI Ventures and Dr Reddys – innovative deal structuring c. Yes Bankd. Bharti Televenturese. Patni Computersf. Biocong. India Bullsh. NDTV

Need for the study

Emerging markets are the 1st and 2nd most attractive FDI destinations for investors

globally. India has moved up the pecking order and has joined China to attain

unprecedented levels of investor confidence as can be seen from the shift over the last

three years in the AT Kearney FDI confidence survey1.

Rank 2005 2004 20031 China China China2 India United States United States3 United States India Mexico4 United Kingdom United Kingdom Poland5 Poland Germany Germany 6 Russia France India7 Brazil Australia United Kingdom8 Australia Hongkong Russia9 Germany Italy Brazil

10 Hong kong Japan Spain

While China has held the top spot since 2002, India’s entry into the top three is a recent

phenomenon. What is more interesting to note also is the fact that India and China

together hold the top spots in almost all major industries and sectors.

The report also concludes that India appears to be at the cusp of an FDI take off and

expects the long term attractiveness of India to increase in the coming years.

Private Equity and Venture Capital inflows, although they are counted as FII inflow into

the country, in terms of dynamics and purpose are in a sense more akin to FDI inflow in

the country as these inflows are more long term in nature and are primarily for the

purpose of long term investment in Indian enterprises.

Hence we believe that overseas VC and PE investment in India is set to take off into a

higher level with significant inflows and investments in the coming years. In this context

1

? AT Kearney FDI Confidence Survey 2005

it would be an useful exercise to gain a greater understanding of the dynamics and

intricacies of this industry and appreciate its importance to one of the world’s leading

emerging economies – India.

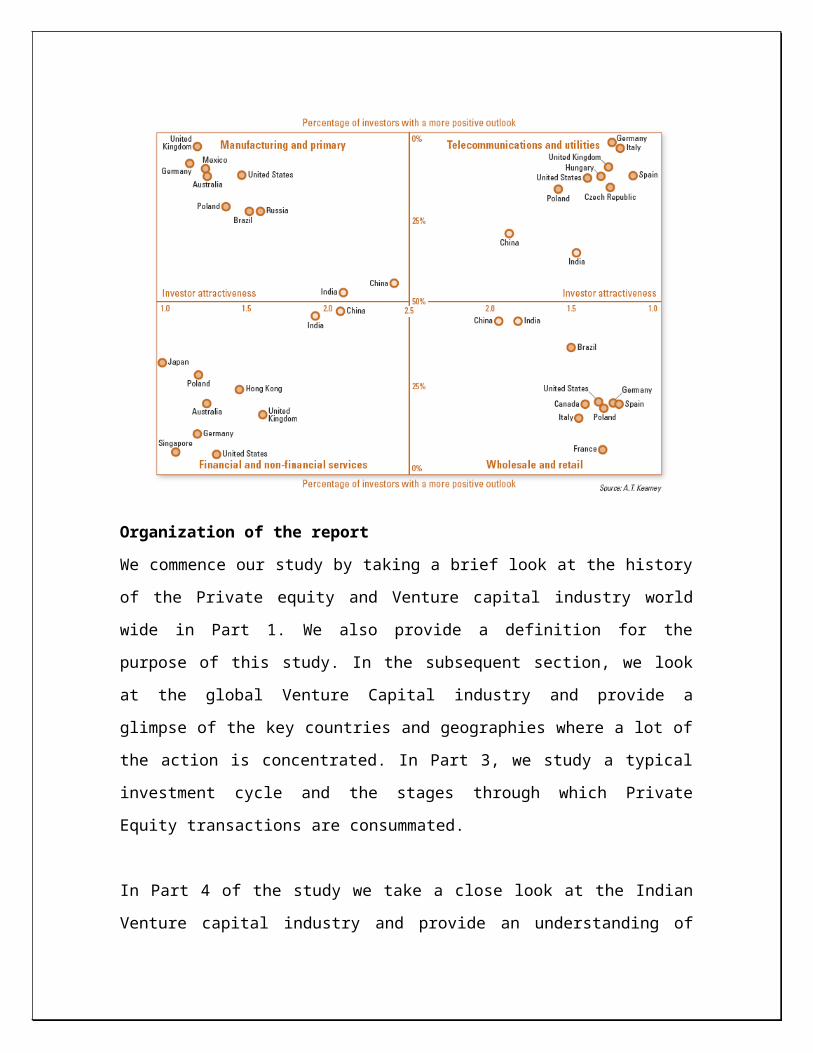

Organization of the report

We commence our study by taking a brief look at the history of the Private equity and

Venture capital industry world wide in Part 1. We also provide a definition for the

purpose of this study. In the subsequent section, we look at the global Venture Capital

industry and provide a glimpse of the key countries and geographies where a lot of the

action is concentrated. In Part 3, we study a typical investment cycle and the stages

through which Private Equity transactions are consummated.

In Part 4 of the study we take a close look at the Indian Venture capital industry and

provide an understanding of the direction and growth in investments in the last few years.

In the final section we take a closer look at a select few transactions in the Indian context

and relate them to the theoretical background of Part 3.

PART 1

History of Venture Capital and Private Equity

The concept of risk financing is as old as Columbus’ journey to America. Mark Anson2

notes that the investment decision of Queen Isabella who sold her jewelry to finance

Columbus’s fleet of ships in return for what ever spoils he could find in the New World

is probably one of history’s most profitable venture capital investments3. This in short

summarizes the private equity industry – a large risk of failure coupled with the potential

for outstanding gains.

Although the term "Venture capital" was first used as a term in a public forum by Jean

Witter in his presidential address to the 1939 Investment Bankers Association of America

convention, 4the usage of the word in its current context took shape in the post – World

War II years.

The first modern venture capital firm was American Research and Development, formed

in 1846 with the mandate to invest in growth industries – aerospace, broadcasting and

pharma.

In the mid-1950s, the U.S. federal government with the objective of speeding up the

development of advanced technologies facilitated the setting up of Small Business

Investment Companies (SBIC). Soon commercial banks were allowed to form SBICs and

within four years, nearly 600 SBICs were in operation5. SBICs have provided capital to

several of the industrial giants and household names of today including Apple, Fedex and

Intel.

The first venture capital limited partnership was formed in 1958 by Draper, Gaither and

Anderson. The next significant thrust to the venture capital industry came with the 2 “Hand book of Alternate Assets”, Mark J.P Anson3 “Towards a Global Venture Capital model”, William Megginson, University of Oklahoma, Dec 20014 Note on Venture Capital, Martin Kenney5 www.indiainfoline.com/bisc/veca/ch04.html

change in the “prudent person” standard in the pension und industry in the 1970s.

Essentially the net effect was that pension funds were allowed to invest in venture capital

investments and this opened the floodgates of capital inflow into this industry.

Definition of Venture Capital 2,3

The OECD (1996) defines venture capital “as capital provided by firms who invest

alongside management in young companies that are not quoted on the stock market. The

objective is high return from the investment. Value is created by the young company in

partnership with the venture capitalist’s money and professional expertise”. More strict

definitions of venture capital exclude buyouts, mezzanine, and other financial

transactions. Venture capitalists invest in equity in the form of common stock, or

preferred stock, convertible debentures, or other financial instruments convertible into

common stock when the small company is sold either through a merger or a public equity

offering. At this liquidity event venture capitalists realize their profits in the form of

capital gains.

Problems and confusion emerge when the terms “venture capital” and “private equity”

are being used. In the USA “venture capital” refers to early stage investment, in Europe it

also includes later stage investment. For the purpose of our analysis in this study,

although we use the terms almost interchangeably, we refer to late stage

investments, buyouts and growth investment as private equity and refer to early

stage investment as venture capital.

Role of VCs

Venture capitalists are often active investors, monitoring the progress of firms, sitting on

boards of directors, and meting out financing based on the attainment of milestones.

Unlike banks which restrict their activities to monitoring the financial health of firms that

they lend to, venture capitalists monitor strategy and investment decisions as well as take

an active role in advising the firm. Venture capitalists often intervene in the company’s

operations when necessary. In addition, venture capitalists provide entrepreneurs with

access to consultants, investment bankers, and lawyers6

There are four basic categories of institutional venture capital funds, as described in Pratt

(1997).

I. Small Business Investment Companies (SBICs): federally chartered corporations

established as a result of the Small Business Administration Act of 1958. SBICs

have invested over $14 billion in approximately 80,000 small firms. Historically,

these venture capitalists have relied on their unique ability to borrow money from

the U.S. Treasury at very attractive rates and hence were the only types of venture

capitalist that preferred to structure their investments as debt rather than equity.

II. Subsidiaries of financial institutions, particularly commercial banks. These are

generally set up with the belief that portfolio companies will ultimately become

profitable customers of the corporate parent.

III. Corporate venture capital funds are subsidiaries or stand-alone firms established by

non-financial corporations. These are generally established by industrial firms eager

to gain access to emerging technologies by making earlystage investments in high-

tech firms.

IV. Finally, venture capital limited partnerships are funds established by professional

venture capital firms, which act as the general partners organizing, investing,

managing, and ultimately liquidating the capital raised from the limited partners.

While most venture capital limited partnerships have a single-industry focus, the

firms themselves are not associated with any single corporation or group.

6‘ What drives Venture Capital Fundraising?’, Paul Gompers and Josh Lerner

Part 2

Snap shop of the global VC industry today

The 2005 Ernst & Young annual Venture Capital Insight Report identified US, Europe

and Israel as the mature hotbeds of venture capital investing and concluded that the

interesting emerging market of India and China would drive venture capital fund raising

in future.

Venture capital and private equity investments world wide reached a level of US $ 31.3

billion in 2005. The United States, Canada, Europe and Israel represented about 93% of

the capital invested while India and China represent the rest.7

U. S Venture Capital Industry

State of the industry

A total of 108 funds closed in the U.S. in 2005, raising $22.16 billion, 19% more than

was raised in 2004 and in fact the highest amount raised since 2001. Although

fundraising is still much smaller than it was in 2000, when $83.18 billion was raised in a

single year, it has rebounded over the last 5 years from the low point of $ 9.44 billion in

2003.8 Almost 8% of the funds closed during 2005 were $ 500 to $1 billion which

indicate the increasing preference for large sized funds.

Stage of investments

Investment activity by round class in 2005 showed the varying focus of investors. While

later-stage deals represented the majority of deal flow, or 37% of all venture capital deals

over the course of the year, the interest in early-stage deals ran a close second,

representing 35% of the year’s financing rounds, up from 34% in 2004. Second-round

financings which made up only 20% of deals in 2005.7 Global venture Capital Insights Report 2006, Ernst & Young8 Global venture Capital Insights Report 2006, Ernst & Young

Size of funds

Almost 8% of the funds closed during 2005 were $500-$999 million in size. Investors are

reportedly raising large funds because of the increasing globalization of the technology

market and the need to provide entrepreneurial companies with larger rounds of financing

so they can compete and create a presence internationally

.

Increased Investor Segmentation according to Industries

The investment preference of VC and PE investors in the United States is predominantly

concentrated in Information Technology and products & services followed by health care

sector with investments in biopharmaceuticals and medical devices.

European Venture Capital Industry

The European venture capital environment in 2005 showed the great contrasts in this

market. On the one hand, European liquidity activity for venture backed companies

rebounded significantly, particularly for initial public offerings (this was in part due to

the availability of exchanges such as AIM which allow small investors a viable listing

option). In addition, venture capital fundraising in Europe reached its highest level in

three years. But on the other hand, venture capital deal flow took a steep decline and the

capital invested shrank considerably.

In 2005, seed- and first-round deals accounted for just 31% of all deals in Europe, down

from 33% in 2004. In addition, the percentage of overall investment in early-stage rounds

was just 22% in 2005, down from 28% in the preceding year. In contrast, later-stage

deals represented 40% of all financing rounds in 2005, up significantly from the 33% in

2004.

The ability of venture-capital supported companies in Europe to achieve IPO exits in

larger numbers was clearly related to the new availability of exchanges such as AIM,

which provides a marketplace for relatively young entrepreneurial companies.

Chinese Venture Capital Industry9

The venture capital industry in China is heating up even though it’s a relatively recent

phenomenon. It has been emerging from decades of government-led technology policy. It

is promoted by government not as a means to private gain but as a critical mechanism of

linking S&T capabilities and outputs for economic and social development. The

institutionalization of China’s VC system is as a result of preceding and on-going

changes in China’s national innovation system and business system during the transition

era.

By late 1970s some of the problem of centrally planned system came into effect.

Inefficiencies and lower effectiveness of a centrally planned economy and R&D system

in China attract special attention during this period. Later the government changed the

system to focus more on

- Policy of decentralization

- Provide legitimacy to VC as well as private entrepreneurship

- Create institutional environment conducive to investment in new ventures

Local Governments are to have much more direct role in development of new ventures

and supporting infrastructure, including in basic activities of the VC system.

There is more uncertainty and higher risk in China, while with great opportunities Some

of the risks are higher information asymmetry, potentially higher moral hazard of

entrepreneur, shortage of experienced entrepreneurs and investors, lack of experience of

managing growing enterprise, quickly changing environment, technology application,

market, deregulation, broad infrastructure, legal framework, the lack of liquid financial

markets, et al.

In China, in 2005, there was a decline in investment activities due to the enforcement of

regulatory initiative that had halted the establishment of the offshore corporate structures

allowing foreign venture capitalists to exit a Chinese company through an IPO on a

9 China's Venture Capital System and Investment Decision-making, Dr. Wei Zhang

foreign exchange. In a development applauded by Chinese Venture Capital Association

and legal observers, China’s State Administration of Foreign Exchange recently issued a

new initiative, that laid out the process for establishing offshore structures, restoring the

exit path for foreign investors. As a result the Chinese venture-capital investment is

expected to rebound. Some of the major challenges in Chinese market include 6

Lack of NASDAQ-like exchange to provide exits for high growth venture capital

companies

Weak intellectual property regulation and protection, making it difficult to

capitalize the innovation.

Lack of a comprehensive venture capital law in terms of structures and taxations

Shortage of management talent

Underdeveloped system for technology transfer

Large degree of freedom exercised by the central government in the venture eco

system.

Lack of stability in regulations

Part 3

Venture Capital Cycle

Section summary: This section presents an academic review and literature survey of the

entire Venture capital cycle and the various considerations in each stage including

Deal sourcing

Due-diligence

Valuation

Deal structuring

Post financing engagement

Exit

Deal sourcing10

In generating a deal flow, the venture capital investor creates a pipeline of ‘deals’ or

investment opportunities that he would consider for investing in.

This is achieved primarily through plugging into an appropriate network such as the

network of venture capital funds/investors. It is also common for venture capitals to

develop working relationships with R&D institutions, academia, etc, which could

potentially lead to business opportunities.

Some of the potential sources of deals are

Referrals: Friends, business or personal acquaintances, or people with whom an

investor has co-invested in the past are good sources for new deals.

Angel organizations: There are many angel organizations that bring start-ups and

seed capital together.

10 Website : http://www.indiainfoline.com/bisc/veca/ch13.htmlWebsite :: http://www.venturechoice.com/vc_blog/

Technology centers: Universities or technology transfer institutes are seeding

grounds for early stage companies.

Entrepreneur clubs and events: Events and organizations that attract entrepreneurs

are a forum to source deals.

Broker dealers: These are individuals or firms retained by startup companies to

raise money. Broker dealers bring deals to VCs or angel investors, and in return,

they are compensated based on the amount of money raised for the company.

Investment bankers: Investment bankers are interested in establishing

relationships with promising startups, which will give them an edge over other

investment banks when the startup becomes large enough to go public, or to make

acquisitions, or to be acquired.

Service providers: A small group of professionals such as accountants, and

lawyers have broad exposure to early stage companies due to the nature of their

business. This is especially true in a country like India where auditors also double

as investment advisors in promoter driven companies.

Due Diligence11:

Due diligence can be broken down to include an initial screening of the deal and a

detailed evaluation in determining the suitability of a deal before moving to the next

stage in which the valuation and deal structure is conducted. This note will outline the

general practices involved in screening due diligence and business due diligence.

Screening Due Diligence. The intent of screening due diligence is to quickly flag the

deals that either do not fit with the investment criteria of the firm or the criteria that are

deemed necessary for success. Venture firms are often inundated with investment

opportunities. The approach to screening is to determine what is critical to its each fund

and what types of deals will fit. Fit is often characterized by the stage of the business, 11 “Note on Due Diligence in Venture capital”, Tuck School of Business, Dartmouth. Center for Private Equity and Entrepreneurship

geographic region, size of the deal, and industry sector. In screening for a high quality

deal there are a few additional areas of focus. Therefore most firms screen based on

investment fit and investment potential.

Investment Fit

– Determines if the investment proposal is consistent with the investment

philosophy of the firm - Venture capitalists may be generalist or specialist

depending on their investment strategy. As a generalist, a firm may invest in

various industry sectors, or various geographic locations, or various stages of a

company’s life. As a specialist, a firm may invest in one or two industry sectors,

or may seek to invest in only a localized geographic area. Another criterion is the

stage of the business lifecycle.

Investment potential

– Once the investment proposal is deemed to “fit” with the philosophy of the firm, a

screening is conducted to test the viability of the deal. Although screening is

unique to a particular firm’s needs, there are some common threads that a firm

evaluates.

– These include

o Management

o Market

o Product/ service

o Business model

o Origin of the deal

Valuation

Valuation in Private Equity12

Valuation in Private Equity settings which involves dealing with companies in various

stages of their life cycle and difficult to predict cash flows is often a subjective process.

Some of the common methods used are

Comparables method

NPV method

Adjusted price value method

Venture capital method and

Options valuation method

Comparables method: Often used to obtain a quick ballpark valuation

First firms that display similar ‘value characteristics’ are selected. These characteristics

include risk, growth rate, capital structure, and the size and timing of cash flows . Often,

these value characteristics are driven by other underlying attributes of the company

which can be incorporated in a multiple. This valuation method is most useful when all

the chosen comparable firms are publicly traded and their capital structure, revenue,

profit margins, net profit figures are known. Common measures used are:

P-E Ratio

Price to sales ratio

Market-to-book ratio(shareholder’s equity)

Market Value to EBITDA ratio

Some of the disadvantages of this method are

The need to make adjustments (smudge factors) to account for the illiquidity of a

private firm when using publicly traded comparables.

The difficulty of obtaining appropriate comparable companies

12 This note draws upon the work of Josh Lerner in “A Note on Valuation in Private Equity settings”, published in the Venture Capital and Private Equity Case book. And a note on How to value startups and emerging companies ? by Amit Bapat (http://cpd.ogi.edu/MST/capstone/StartUpValuation.pdf)

NPV Method

This method used the present value of cash flows discounted at the appropriate cost of

capital. The disadvantages associated with this method are that

WACC assumes a constant capital structure and a constant effective tax rate

neither of which may hold true in the case of venture backed companies with

multiple rounds of financing and probable Net operating losses in early years.

The valuation is also very sensitive to discount rate and terminal value

assumptions

Adjusted present value method is a variation of the NPV method.

When a firm’s capital structure is changing or it has net operating losses (NOL) that can

be used to offset taxable income, APV method is used. If a firm has NOLs then its

effective tax rate changes over time, as NOLs are carried forward for tax purposes and

netted against taxable income. APV accounts for the effect of the firm’s changing tax

status by valuing NOLs separately.

Thus under APV method,

First cash flows are valued ignoring the capital structure.

The discount rate used is different than in NPV method as it is assumed that the

company is financed totally by equity. This implies that the discount rate should

be calculated using unlevered beta.

The tax benefits associated with the capital structure are then estimated. The net

present value of the tax savings from tax-deductible interest payments is

quantified.

The interest payments will change over time as debt levels change. By convention

the discount rate for this calculation is pre-tax rate of return on debt which will be

lower than cost of equity.

Finally NOLs available to the company are quantified. The discount rate used to

value NOLs is often pre-tax rate on debt. If it is almost certain that NOLs will

result in tax benefits risk free rate can also be used as the discount rate.

Shortcomings of this method are similar to the NPV method. However the problems

related to WACC are eliminated.

Venture capital method

This method is the most commonly applied method in the private equity industry

especially when dealing with early stage companies. Most private equity investments are

characterized by negative cash flows and earnings in the early stages and highly

uncertain but potentially substantial future rewards. The VC method accounts for this

profile by valuing a company using a multiple, at a time in the future when it is projected

to have achieved positive cash flows and earnings. This terminal value is then discounted

back to the present value at a typically very high discount rate 40% to 75% depending on

the target IRR of the Private Equity firm to arrive at the equity stake demanded by the

investor.

Although this method is commonly used, it suffers from the excessive reliance on the PE

approach to calculating the exit valuation of the company.

Options valuation method

This is a relatively new method and is not yet extensively used even in developed

markets such as the US.

The underlying rationale for this method is as follows:

DCF methods like NPV and APV can be deficient in situations where a manager or

investor has flexibility in terms of changing rate of production, defer deployment or

abandon a project. These changes affect the value of the firm which can not be measured

accurately using discounted cash flow methods. Private equity-backed companies are

often characterized by multiple rounds of funding. Venture capitalists use this multi-stage

approach to motivate the entrepreneur to perform better and limit their exposure to a

particular company.

In this method firms are analyzed like a financial option. There are five variable

commonly used in a financial option:

X = exercise price

S = stock price

T = time to expiration

σ = standard deviation of returns on the stock

r = time value of money

In the firm option, they are interpreted as:

X = Present value of expenditures required to undertake a project

S = Present value of the expected cash flows generated by the project

T = The length of time that the investment decision can be deferred

σ = riskiness of the underlying assets

r = risk free rate of return

Once these variables are know the value of the option can be calculated using Black-

Scholes computer model.

Non Financial considerations

Along with the above valuation methods that mainly rely on financial data, investors also

consider several non financial considerations while valuing a company:

Quality of management team

Current state of technology

Current state of companies in similar market

Current market conditions

Size of the market and company’s potential to acquire market share

Track record of entrepreneur; repeat entrepreneurs get better valuation

Distribution of bargaining power between VC and entrepreneur

Cost of capital and required rates of return

When using P/E or similar benchmarks for valuation of venture capital investments the

fudge factor to accommodate liquidity discount is as much as 30% of overall valuation.13

Investor return expectations:

As a rough guideline for expected investor returns14,

Seed or startup investment 60% or more per annum

Early stage investments 50% or more per annum

Development capital investment 35-40% per annum

MBO/MBI Over 30% per annum

Other literature on the expectations of investors also paints a similar picture:

Bygrave and Timmons15 (1992), note, that independent private venture capital firms

expected a minimum annualized rate of return on individual investments that ranged from

75% for seed-stage financing to about 35% per year for bridge financing.

Rich and Gumpert16 (1991) state, that companies with fully developed products and

proven management teams should yield between 35% and 40% on their investment,

while those with incomplete products and management teams are expected to bring in

13 The Venture Capital Handbook, William Bygrave, Micheal Hay and Jos B Peeters14 Note on Deal structuring and pricing, The Venture Capital Handbook, William Bygrave, Micheal Hay and Jos B Peeters15 “Cost of capital for Venture Capitalists and Under diversified investors”, Frank Kerkins, Janet Kiholm Smith and Richard Smith, 200216 “Cost of capital for Venture Capitalists and Under diversified investors”, Frank Kerkins, Janet Kiholm Smith and Richard Smith, 2002

60% annual compounded returns. In these statements, the cited percentages properly are

interpreted as targets for analysis of a success scenario, and not as statistical expectations.

Deal Structuring

Typical deal structuring in the US17

The terms and structure of an offer to invest in a company is usually charted out in a term

sheet. There are brief preliminary, non binding documents designed to facilitate and

provide a framework for negotiations between investors and entrepreneurs. A term sheet

generally focuses on a given enterprise’s valuation and the conditions under which

investors agree to provide financing. The term sheet eventually forms the basis of several

formal agreements including the “Stock Purchase Agreement,” which is a legal document

that details who is buying what from whom, at what price, and when.

Typically, term sheets also contain additional control provisions, to mitigate various risks

that the investor perceives in an investment. The nature of securities used in these

investments also provides insights into the various risks perceived and the mitigating

mechanisms used

Commonly used securities in structuring VC deals:

Different investments have varying risk/reward characteristics which call for different

types of securities to accommodate investors goals.

The most common types used in venture capital transactions are described below.

Common stock is a type of security representing ownership rights in a company, usually

entitles the owner to one vote per share as well as any future dividend payments. Usually,

company founders, management and employees own common stock while investors own

17 “Note on Private Equity Deal Structures” Tuck school of Business, Dartmouth

preferred stock. Claims of secured and unsecured creditors, bondholders and preferred

stockholders take precedence over those of the common stockholders.

Convertible preferred stock provides its owner with the right to convert to common

shares of stock. Usually, preferred stock has certain rights that common stock does not

have, such as a specified dividend that normally accrues and senior priority in receiving

proceeds from a sale or liquidation of the company. Therefore, it provides downside

protection due to its negotiated rights and allows investors to profit from share

appreciation through conversion.

The face value of preferred stock is generally equal to the amount that the VC invested.

For valuation purposes, convertible stock is usually regarded as a common stock

equivalent. Typically, convertible preferred stock automatically converts to common

stock if the company makes an initial public offering (IPO). When an investment banking

underwriter is preparing a company to go public, it is critical that all preferred investors

agree to convert so the underwriter can show public investors that the company has a

clean balance sheet. Convertible preferred is the most common tool for private equity

funds to invest in companies.

Participating preferred stock is a unit of ownership that is essentially composed of two

elements -- preferred stock and common stock.

The preferred stock element entitles an owner to receive a predetermined sum of

cash (usually the original investment plus any accrued dividends) if the company

is sold or liquidated.

The common stock element represents additional continued ownership in the

company (i.e. a share in any remaining proceeds available to the common

shareholder class).

Like convertible preferred stock, participating preferred stock usually converts to

common stock (without triggering the participating feature) if the company makes an

initial public offering (IPO). Participation can be pari passu or based on seniority of

rounds.

Multiple Liquidation Preference is a provision that gives preferred stock holders of a

specific round of financing the right to receive a multiple (2x, 3x, or even 6x) of their

original investment if the company is sold or liquidated. A multiple liquidation

preference still allows the investor to convert to common stock if the company does well,

and it provides a higher return (assuming the selling price is sufficient to cover the

multiple) if an IPO is unlikely.

Redeemable preferred stock can be redeemed for face value at the choice of the

investor. Sometimes called straight preferred, it cannot be converted into common stock.

Usually, the terms of the issue specify when the stock must be redeemed, such as after an

IPO or a specific time period. Redeemable preferred gives the investor an exit vehicle

should an IPO or sale of the company not materialize.

Convertible debt is a loan vehicle that allows the lender to exchange the debt for

common shares in a company at a preset conversion ratio.

Mezzanine debt is a layer of financing that often has lower priority than senior debt but

usually has a higher interest rate and often includes warrants.

Senior debt is a loan that enjoys higher priority than other loans or equity stock in case

of a liquidation of the asset or company.

Subordinated debt is a loan that has a lower priority than a senior loan in case of a

liquidation of the asset or company.

Warrants are derivative securities that give the holder the right to purchase shares in a

company at a pre-determined price. Typically, warrants are issued concurrently with

preferred stock or bonds in order to increase the appeal of the stock or bonds to potential

investors. They may also be used to compensate early investors for increased risk.

Options are rights to purchase or sell shares of stock at a specific price within a specific

period of time. Stock purchase options are commonly used as long-term incentive

compensation for employees and management.

Anti-Dilution - Dilution occurs when an investor’s proportionate ownership is reduced

by the issue of new shares. Investors are primarily concerned with “down rounds,” or

financing rounds that value the company’s stock at a lower price per share than previous

rounds. Down rounds may occur due to a number of factors like economic conditions or

company performance. Since investors cannot determine with certainty whether a

company will undergo a down round, they negotiate certain rights, or anti-dilution

provisions referred to as “ratchets,” that may protect their investment.

The two most common mechanisms are full ratchets and weighted average ratchets.

Full Ratchets protect investors against future down rounds. A full ratchet

provision states that if a company issues stock to a lower price per share than

existing preferred stock, then the conversion price of the existing preferred stock

is adjusted (or “ratcheted”) downward to the new, lower price. This has the effect

of protecting the ratchet holder’s investment by automatically increasing his

number of shares at the expense of stockholders who do not enjoy full ratchet

protection.

Weighted average provisions are generally viewed as being less harsh than full

ratchets. In general, the weighted average method adjusts the investor’s

conversion price downward based on the number of shares in the new (dilutive)

issue. If relatively few new shares are issued, then the conversion price will not

drop too much and common stockholders will not be crammed down as severely

as with a full ratchet. If there are many new shares and the new issue is highly

dilutive to earlier investors, however, then the conversion price will drop more

o The weighted average protection may be broad-based, taking into

account all shares outstanding before the new dilutive issue

o Narrow based, which takes into account only preferred stock or omit

options outstanding.

Pay-to-play (aka Play or Pay) Provisions are usually used with price-based anti-

dilution measures, these provisions require an investor to participate (proportionally to

their ownership share) in down rounds in order to receive the benefits of their anti-

dilution provision. Failure to participate results in forced conversion from preferred to

common or loss or the anti-dilution protection. This encourages VCs to support

struggling portfolio companies through multiple rounds and increases the companies’

chances of survival.

Other Issues In addition to the key financial provisions described above, term sheets

usually include a number of other important items related to control, and a mix of

financial and non-financial terms is common. Many of the provisions described in this

paper, both financial and non-financial, tend to be used more often during difficult

economic times. It should be noted that overly burdensome, shortsighted terms may

misalign interests and invite the competition to provide a better deal. Some non-financial

terms are discussed below:

Voting Rights. Term sheets often address issues of control in order to allow investors in

a company to add value and also to exercise control if things go wrong. While investors

may not want majority board control if things are going well, they may negotiate

provisions that give them control if certain events occur.

Board Representation. Venture capitalists may negotiate control of part of the Board of

Directors, generally to influence decision-making and to protect their investments rather

than to run the company. Often, classes of stockholders are allowed to elect a percentage

of the board members separately. If venture capitalists invest as a syndicate and board

representation is not possible for all of the participating firms, then board observer

rights are an option. These rights allow investors to monitor their portfolio companies

and to influence decisions by being present at board meetings, but they are not allowed to

vote.

Covenants. Most preferred stock issues and debt issues have associated covenants, or

things that the portfolio company promises to do (positive covenants), and not to do

(negative covenants). They are negotiated on a case-by-case basis and often depend on

other aspects of the deal. Failure to comply with covenants can have serious

consequences to the company such as automatic default and payments due.

Vesting. This provision states that a manager or entrepreneur earns ownership of

common stock or options only after a predetermined period of time or after the company

achieves certain milestones. The most important effect of vesting is that it motivates

employees to stay with the company and may prevent them from leaving prematurely to

pursue other opportunities.

Bridge Loans. Bridge financing can be used to prepare a company for sale or as a pre-

round financing. A bridge is, in essence, short term financing designed to be either repaid

or converted into ownership securities.

In the sale case, a bridge is useful when a company needs a relatively small

amount of capital to achieve its final targets and achieve maximum value in the

eyes of potential buyers.

A bridge is also useful to pump cash into a company quickly while investors are

found to complete a formal round of financing. Bridge investors often insist on

warrants or equity kickers to compensate them for the higher risk of lending

money to high growth ventures.

If the “bridge” becomes a “pier,” that is, no additional sources of funding step up to the

challenge, then the bridge lenders have senior rights to any equity holders for the

remaining assets of the company.

Phased financing. A venture capital firm may agree to phased financing, or incremental

financing in tranches. In this case, the entrepreneur and his or her team must reach certain

milestones in order for the venture capitalist to agree to invest more capital in the startup.

This has the additional benefit of allowing the startup and the venture firms to trumpet

the larger commitment amount, generating positive PR, while limiting the actual cash

disbursements until the startup has proven itself.

Results of some theoretical studies made:18

Unlike in the United States, where the use of convertible preferred securities is

ubiquitous in private equity, substantially different securities are employed in

developing nations. More than one-half of the transactions employ common

stock, and a subset of transactions employ instruments that are essentially debt.

Private equity investor rights that are standard in the United States, such as anti-

dilution provisions, are encountered far less frequently.

In nations where the rule of law is less established, private equity groups are less

likely to employ preferred securities. They are likely, however, to have a majority

of the firm’s equity and to make the size of their equity stakes contingent on the

performance of the company.

Exits19

Exiting an investment is a key consideration that drives the structuring, valuation, post

financing role and even the prefinancing due-diligence of the investor.

There are 4 primary exit options for venture capital and private equity investments

1. IPOs or through sale in the secondary market(in the case of PIPEs)

2. Trade sale

3. Sale of the financial interest of the investor by the promoters of the company18 “PE in the Developing world: Determinants of Transaction Structures”, Josh Lerner and Antoinette Schoar19 This note draws upon, among other references, the teaching notes and class lectures of Prof. Sabarinathan of the Indian Institute of Management Bangalore.

4. Buy back of the investor’s financial through the company’s cashflows

A brief discussion on each of the methods follow

1. IPO – this is often the most preferred mode of exit by the PE/VC investors as it

usually leads to the realization of the highest returns. Typically the most

successful investments of a private equity fund reach the IPO stage. Apart from

capital appreciation, some of the other payoffs for investors is the visibility that it

creates for the VC fund. Given the levels of visibility and performance

demonstrated by IPO, it becomes easier for an investor to raise subsequent funds

and generate reputation capital based on the number of investments taken public.

Infact private equity investors have often been accused to dragging their investee

companies too soon into an IPO primarily for the purpose of creating a public

demonstration of success – a phenomenon that has been termed as

grandstanding20.

The IPO route of exit however is fraught with many difficulties and

imponderables. One important consideration is the dynamics of the market for

primary listings. Investors in the capital markets are receptive to certain industries

at certain times and luke warm to the same industries at other times. These

“windows of opportunity” are difficult to predict and time appropriately.

Further there is also the question of preparing the company to go public. A public

company under the scrutiny of the market is subject to several disclosure norms

that have direct and indirect costs on the management including the need to put in

place the necessary internal organization structure that is needed to generate

periodic filings and other indirect costs such as managerial distraction. Further the

pressure to deliver quarter on quarter earnings can force companies to focus on

20 “Grandstanding in the Venture Capital Industry” Journal of Financial Economics, 43 (September 1996) pages 133-156. Josh Lerner

short term profit maximizing behavior. It is estimated that the process of

“preparing the company” for the IPO may be as long as a year.

2. The Trade Sale

The trade sale is one of the most common exit route for investors especially in

economies where the absence of a mature capital market for small company IPOs

preclude the IPO mode of exit. Often trade sale is also a viable opportunity for

companies that have not performed as great as expected and hence serves as a

residual alternative for companies that have not made the grade for an IPO.

Further, the investors are not subject to any risk of share price decline post as IPO

exit if the trade sale route is adopted. On the negative side, the returns that are

generated in a trade sale are usually deemed lesser that that derived in an IPO.

The reason is that valuations may be more stringent in a trade sale.

Trade sales have emerged as a frequent exit route as several large business look to

grow inorganically in order to cope with rapid changes in technology, business

development cycles, and innovative new product development. Further several

startups in developed nations are built around the strategy of “built to sell” i.e.

they identify gaps in the product technology gaps of existing offerings and build

products around such gaps with the intention of achieving a sell off to large

incumbent companies at attractive valuations.

Part 4

The Indian VC and Private Equity Industry

History21

The first formal venture capital organizations in India began in the public sector.

First Phase (pre 1995)

Indian policy toward venture capital has to be seen in the larger picture of the

government’s interest in encouraging economic growth. In 1988, the Indian government

issued its first guidelines to legalize venture capital operations and were aimed at

allowing state-controlled banks to establish venture capital subsidiaries.

In November 1988, the Indian government announced an institutional structure for

venture capital (Ministry of Finance 1988). The World Bank had earlier observed that the

focus on lending rather than equity investment had led to institutional finance that had

become “increasingly inadequate for small and new Indian companies focusing on

growth” (World Bank 1989: 6).

The most important feature of the 1988 rules was that venture capital funds received the

benefit of a relatively low capital gains tax rate. They were also allowed to exit at prices

not subject to the control of the Controller of Capital Issues (which otherwise did not

permit exit at a premium over par). The funds’ promoters could be banks, large financial

institutions, or private investors. The funds were restricted to investing in small amounts

per firm (less than 100 million rupees); the recipient firms had to be involved in

technology that was “new, relatively untried, very closely held or being taken from pilot

to commercial stage, or which incorporated some significant improvement over the

existing ones in India.” The government also specified that the recipient firm’s founders

should be “relatively new, professionally or technically qualified, and with inadequate

resources or backing to finance the project.”

21 This note is based on the study by the Asia Pacific Research Center, Stanford University titled “Creating an environment: Developing Venture Capital in India”, Rafiq Dossani and Martin Kenney.

There were also other guidelines including a list of approved investment areas. Two

government-sponsored development banks, ICICI and IDBI, were required to

clear every application to a venture capital firm. Also, the Controller of Capital Issues

had to approve every line of business the VC firm wished to invest.

Four state-owned financial institutions established venture capital subsidiaries under

these restrictive guidelines and received a total of $45 million from the World Bank.

funds, two of which were established by state-level financial institutions (Andhra

Pradesh and Gujarat), one by Canara Bank and one by ICICI. The venture capital funds

were expected to be investing principally in equity or quasi-equity.

The venture capitalists agreed with the World Bank that they would operate under the

following operating guidelines:

(a) the primary target groups for investment would be private industrial firms in

sectors where India had a comparative advantage, and protected industries would

be avoided;

(b) the quality and experience of the management was key, along with the prospects

of the product;

(c) the portfolio return should be targeted to be at least a 20 percent annual return;

(d) no single firm should receive more than 10 percent of the funds, and the venture

capitalist would not own more than 49 percent of its voting stock.

ICICI had begun a small investing division at its Mumbai headquarters in 1985 focused

upon unlisted, early stage companies.

Nadkarni and ICICI Chairman Vaghul implemented a novel instrument for India, termed

the “conditional loan.” It carried no interest but entitled the lender to receive a royalty on

sales (ICICI charged between 2 percent and 10 percent as a royalty). They would

typically invest 3 million rupees in a firm, of which one-third was used to buy equity at

par for about 20–40 percent of the firm, while the rest was invested as a conditional loan,

which “was repayable in the form of a royalty (on sales) after the venture generated

sales.” There was no interest on the loan. However, the problem with this scheme is that

the loan did not provide capital gains.

In its first year, the division invested in seven such deals, of which three were in software

services, one in effluent engineering, and one in food products (a bubble gum

manufacturer). Being a novel institution in the Indian context, as Nadkarni (2000) noted,

“There was no obvious demand for this kind of funding and a lot of work went into

creating such deals...” . The company targeted deals that would earn 2–3 percent above

ICICI’s lending rate. “ … looking back, there was no sectoral focus so it is remarkable

that we invested so much in Information Technologies.” Infosys, then a fledgling startup

was rejected by ICICI, because the project was deemed too risky.

In 1988, the first organization to actually identify itself as a venture capital operation,

Technology Development & Information Company of India Ltd. (TDICI), was

established in Bangalore as a subsidiary of ICICI.

The ICICI division was merged into TDICI as an equal joint venture between ICICI and

the state-run mutual fund UTI. The major reason for creating the JV with UTI was to use

the tax pass-through, an advantage that was not available to any corporate firm at that

time other than UTI (which had received this advantage through a special act of

parliament).

Hence, the investment manager for the new funds was TDICI and the funds were

registered as UTI’s Venture Capital Unit Schemes (VECAUS). Vecaus I, established in

1988, had a paid-in capital of 300 million rupees. Founded in 1991, Vecaus II had a paid-

in capital of 1 billion rupees.

TDICI opened operations in Bangalore. Interest in technology had increased due to the

success of multinationals such as Texas Instruments and Hewlett Packard that were

operating in Bangalore. Bangalore was chosen because of the presence of Indian software

firms such as Wipro, PSI Data, and Infosys apart from the decision by the Indian

government to establish it as the national center for high technology. The research

activities of state-owned firms such as Indian Telephone Industries, Hindustan

Aeronautics Limited, the Indian Space Research Organization (ISRO), and the Defense

Research Development Organization, along with the Indian Institute of Science were

centralized there.

Vecaus I invested in several successful information technology firms in Bangalore

including Wipro for developing a “rugged zed” computer for army use. There were

several successes, including several firms which went public, such as VXL, Mastek

Software Systems, Microland, and Sun Pharmaceuticals. The fund had an inflation-

adjusted internal rate of return of 28 percent.

TDICI was the most successful of the early government-related venture capital

operations. Moreover, TDICI personnel played an important role in the formalization of

the Indian venture capital industry. Kiran Nadkarni established the Indian Venture

Capital Association, and was the Indian partner for the first U.S. firm, Draper

International to begin operations in India. In addition to Nadkarni, TDICI personnel also

left to join other firms. Vijay Angadi joined ICF Ventures. Also, a number of TDICI

alumni became managers in Indian technology firms. So, the legacy of TDICI includes

not only evidence that venture capital could be successful in India, despite all of the

constraints, but also a cadre of experienced personnel that would move into the private

sector.

Gujarat Venture Finance Limited (GVFL) began operations with a 240 million rupee

fund. GVFL was established with a handicap – It was meant to invest in the state of

Gujarat. However, though its returns were not high, it was sufficiently successful so that

in 1995, it was able to raise 600 million rupees for a second fund. In 1997 it raised

a third fund to target the information technology sector. It is estimated that GVFL made

annualized returns of the order of 15%. – a relatively weak performance.

The other two venture funds also had marginal returns. The AP Industrial Development

Corporation (APDIC) was mandated to invest in its state. Though located in a strong

high-technology region (Hyderabad), APDIC suffering from the difficulties of state-

operated funds and had a relatively low return. The final venture fund, the only bank-

operated venture capital fund, CanBank Venture Capital Fund also performed poorly.

This first stage of the venture capital industry in India was plagued by inexperienced

investment professionals, mandates to invest in certain states and sectors, and general

regulatory problems. The firms’ overall performance was poor, and only TDICI could be

considered a success. And yet, from this disappointing first stage, there came a

realization that there actually were viable investment opportunities in India.

The second stage(1995-1999)

The success of Indian entrepreneurs in Silicon Valley became far more visible in the

1990s. This attracted attention and encouraged the notion in the United States that India

might have more possible entrepreneurs. The figure on total capital under management in

India increased after 1995.The greatest source of this increase was the entrance of foreign

institutional investors including investment arms of foreign banks, but particularly

important were venture capital funds raised abroad.

NRIs were important investors in these funds coupled with the comparative decrease in

the role of the multilateral development agencies and the Indian government’s financial

institutions. The overseas private sector investors became a dominant force in the Indian

venture capital industry.

Various stages of development of risk capital in India22

22“Accessing Risk Capital in India”, Rafiq Dossani and Asawari Desai

Phase 1 Phase 2 Phase 3 Phase 4Pre 1995 1995-1997 1998-2001 2002-2005

Total Funds( $ mn) 30 125 2847 5239Number of funds(estimated) 8 20 50 75

Stages & Sectors Diversified Diversified Early stage & Growth, Telecom & IT

Growth/ Maturity, Diversified

Primary sources of funds World Bank, Government Government Overseas Institutional Overseas Institutional

Total number of transactions 30 65 548 446Average investment($ mn) 1.00 1.92 5.20 11.75

VC and PE in India - Today

The importance of India as an investment opportunity in the VC and PE industry has

been growing tremendously over the last few years. A host of factors are responsible for

this including availability of restructuring opportunities at attractive valuations, newly

deregulated industries at attractive valuations, rich talent pool, a reasonably robust legal

framework and most importantly a liquid capital market

PE investment in India

20 80 150

500

1,200

1,800

1,500

774

1,7502,000

-

500

1,000

1,500

2,000

2,500

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

USD

mn

Chart1. PE Investment in India - History23

After a down turn in 2002 and 2003 following the dot-com bust, the investment is on a

rebound once again. When VC and PE investments are taken as a total, investment in

23 Business Today, August 2005

India in 2005 was USD 2.6 billion, a 36% growth over the USD 1.9 billion invested in

200424. In 2006, given the fact that over USD 2,5 billion has already been invested in the

first 4 months, total VC and PE investment is expected to be of the order of USD 6

billion according to various market sources25.

Several VC including Draper Fisher Jurvetson, Matrix, Nexus, Helion Ventures and

Inventus have raised India specific funds for early stage VC investing in the last one year.

In the PE space too investors such as Temasek, Actis, Warburg Pincus and Chrys Capital

have earmarked significant amounts from their Global/ Asia funds for India specific

investments or have raised funds purely for the purpose of investing into India.

Though foreign investors play an important role in Indian private equity market, they

behave differently when in Indian market.26 A US investor may specialize in a particular

stage, say growth or expansion capital investments or buyouts. Further, it may also

specialize out in a particular sector, say, manufacturing. But in India, for example

Warburg and CVC have invested in a wide variety of sectors in different types of deals.

These investors have been following the classical model of specializing in the developed

market. PE firms need to be opportunistic and flexible to achieve good returns in India.

Some of the major players who invests in private equity in India are27

Fund Of Funds - These are funds that invest in funds. For example, Adams Street is an

investor in ChrysCapital.

The Buyout Funds – This is relatively new in India. Texas Pacific Group, Carlyle, and

Blackstone are primarily buyout funds that invest large amounts in entire businesses.

Mid-market Private Equity Funds - This is the most popular variety in India because

most of the private equity demand comes from mid-sized companies that are expanding.

24 Venture Intelligence Report. 25 The European Venture Capital Journal, May 30, 2006 – “Indian Buyouts”; “The India opportunity”, Business World, 14 Aug 200626 BW private equity survey 200627 Business Today, August 2006

Late-stage Private Equity Fund - Warburg, Temasek, General Atlantic Partners,

Newbridge, Carlyle, 3i and Apax are some of the funds that fall in this category. The

target companies are relatively large-cap stocks.

Real Estate Funds, Hybrid Hedge Funds and Venture Capital Funds

Private Equity fund universe:

As on 2006 there are an estimated 62 private equity players in India28.With several

foreign investment funds including Carlyle, Texas Pacific Group and the Blackstone

Group entering India in the last few years, the market is flush with funds.

S. No Type DescriptionAvg Deal

Size Examples of funds in India

1 Fund of funds Funds that invest in other funds > 100 mn Evolvence India Fund

2 Buyout fundsFunds that invest in entire businesses to gain operational control, add value and sell at a premium

~ 100 mn NewBridge, Carlyle, Apax & Blackstone, ICICI Venture

3 Late Stage PE funds Funds that target late stage/ large cap stocks 30 - 100 mn Warburg, Temasak, GAP, 3i

4 Mid market PE funds

Funds that invest in listed/unlisted mid sized companies 10- 30 mn CVC, Chrys capital, Actis, Baring, GW Capital,

Kotak, ILFS, IDC

5 VC Funds Funds that invest in Early stage, seed stage ventures 5-15 mn West Bridge(Sequioa), ICICI Ventures,

Jumpstartup, UTI VF, Intel Capital

6 Real Estate Funds Invest in Real Estate projects IREO, OZ Capital, Trikona, Ascendas India Property Fund

7 Hybrid Hedge Funds

Opportunistic investment across board from private equity to corporate bonds Oaktree, New Vernon, Pequot Capital

Table: VC Fund Universe in India29

28 “Conducting Successful transactions in India” Ernst & Young29 “Conducting Successful transactions in India”, Ernst & Young

Private Equity Investment by Industry

Industry USD mn % USD mn %IT & ITES 976 59% 412 19%Manufacturing 149 9% 371 22%Healthcare and lifesciences 98 6% 269 16%Textiles 15 1% 147 9%BFSI 54 3% 306 19%Media 61 4% 102 6%Engineering and Construction 188 11% 92 6%Others 112 7% 485 29%TOTAL 1,653 100% 2,184 100%Source: Venture Intelligence Roundup

2004 2005

Venture Capital Investment by Industry

Industry USD mn % USD mn %IT & ITES 206 69% 261 56%Retail 16 5% 23 5%Healthcare and lifesciences 16 5% 82 18%BFSI 16 5% 22 5%Media - 0% 52 11%Others 43 14% 27 6%TOTAL 297 100% 467 100%Source: Venture Intelligence Roundup

2004 2005

Early stage vs. late stage

Private Equity Investment by Stage

Stage USD mn % USD mn %Early Stage 55 3% 79 4%Early stage - cros border 48 3% 71 3%Growth stage 192 12% 332 15%Late stage 298 18% 632 29%PIPE 547 33% 763 35%Buyout 514 31% 306 14%TOTAL 1,654 100% 2,183 100%Source: Venture Intelligence Roundup

2004 2005

Venture Capital Investment by Stage

Industry USD mn % USD mn %Early India 55 19% 79 0.16 Early Indo - US 48 16% 71 0.15 Growth 192 65% 332 0.69 TOTAL 295 100% 482 1.00 Source: Venture Intelligence Roundup

2004 2005

As figures show, the market in India is mainly focused on post-venture private equity

deals. This is a feature of emerging markets. The table given below substantiates this

point. Most of the private equity funds investing in India are foreign funds and the early

stage comprises of the highest risk- highest return investments. Most foreign PE funds

feel that they are already taking on a higher level of risk as they are investing in an

emerging market. Therefore they prefer to back established companies with strong

financials, market presence and solid management that are perceived to be lower risk

than start-ups whose business model is untested.

% of total risk capital invested in seed and early-stage firms

China

India Israel UK US

12.5 6 32 39 29 Sources: China: Zero2ipo-CVCAnnual Report 2005

Seed and Early Stage Investment – Selected Countries, 2004

The other reasons favoring late stage investments to early stage are the following:30

30 Utz C, 2005, Early Stage Enterprises, Position Paper, Australian Venture Capital Association

Transaction costs – the costs to an investor of appraising the risks and returns from an investment tend to be fixed and high relative to the size of the investment.

Transaction size – venture capital investors typically require a minimum transaction size, which is often higher than the average early stage company’s requirement..

High risk - higher for early stage (and particularly pre-revenue) companies – because the management team or company’s product and market may be unproven.

Lack of exit options – there is no secondary market for trading in smaller firms’ shares.

Due to the current post 'tech-wreck' environment, many venture capitalists have retreated from early stage investments in favor of later stage investments and turnaround opportunities.

Other trends

The telecommunications and education infrastructure are advanced relative to India’s

stage of development. Relative to most other countries, skills are not in short supply.

Other positive features that make India an attractive investment destination include:

Human capital: sufficient rising number of graduates in various fields

Success of the software and services industry, leading to the creation of a cadre of

engineers and other domain experts with marketing and product development

skills

A cadre of returnees from western countries with advanced technical and business

development skills

Opportunities in newly competitive exporters, e.g., textiles, the auto components

industry and healthcare.

The growth of domestic markets in fast-growing sectors such as

telecommunications, finance and retail.

Presence of risk capital providers in centers outside the main commercial center,

Mumbai, and, in consequence, closer to the locations of small and medium

enterprises

Expanding pool of multinational firms operating in the country which provide

access to the latest technologies in a range of sectors and create future

entrepreneurs.

Exit

According to Nainesh Jaisingh, head, India Pvt Equity, Standard Chartered Bank, “Exits

in India were predominantly happening through the capital markets. This was largely

because the capital markets are well developed in India as compared to some other

countries. Of late, however, we are seeing exits through buyouts and sale to strategic

investors.”31 The current private equity market boom is driven mainly due to the high rate

of return that the firms get at exit which in turn is a function of the state of the capital

markets. It could also be imputed that that private equity firms bring in new ideas,

professionalism and global expertise into the board room.

Among different types of exits the strategic buyer (as against a financial buyer) brings in

a lot of managerial inputs which helps in the company to achieve the targeted growth

besides offering a higher value in the market. In the case of buyouts, the premium paid

for acquiring the controlling stake is much higher than the market price. PE to PE sales is

another way of exit. In such a case where a private equity firms who wants to invest in a

growth stage buys the company from another PE firm who has already invested in the

early stage of financing. In such a case the valuation will be for future earnings and will

be higher than the traditional valuation.

As is the case globally, the most preferred route of exit in India is the IPO. A lot of

promoters especially of new age enterprises do not have a controlling stake in their

companies as they are forced to dilute their stake to raise start-up/growth capital. In such

31 Profit through exits, Business India, Aug 2006

cases, exit by private equity firms through IPOs allows the dispersion of ownership and

gives them a controlling edge despite not having the majority stake.

Some concerns

One concern is that of asset price inflation32. There is a good probability that a PE

firm pays more when most funds are looking at the same asset, especially in a bull

market. In such case the prices might not be in line with the valuation figures.

Another concern expressed in the business circle is that of the situation when

India loses its fancy or other markets with lower valuations catches the attention

of foreign PE firms. There is a need for more homegrown PE firms to come up to

balance the growth of foreign funds in India

Currently, PE investment is mostly in the form of equity. Private funds offering

mezzanine equity, senior debts and hybrid instruments have not thrived in India.

Pension funds and institutions need to participate more in PE funds.

A comparison of the Indian VC industry and the Chinese Industry

0

500

1000

1500

2000

2500

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

US

D m

n

India China

Private Equity Investment, China vs. India33

32 Business India, February 200633 TSJ Media Reports, Zero2Ipo-CVCA Annual Report 2005

While in terms of total volume of investment, China still lags behind India, China leads

in early stage financing. Further, the decline in investments in China in 2005 is due to a

regulatory initiative by China’s State Administration of Foreign Exchange (SAFE),

(Circulars 11 and 29) that banned offshore corporate structures allowing foreign-venture

capitalists to exit through an IPO on a foreign exchange. However, SAFE recently issued

new regulations (Circular 75) that laid out a new process for establishing offshore

structures, restoring the exit path.

Which country is more attractive for the following attributes?34

Given the likely hood that India would compete with China for overall portfolio

allocation of global investors, a comparison of the investment attractiveness of India vs.

China could throw insights into the nature of fund flow.

34 A.T. Kearney FDI Confidence Index 2004

0 20 40 60 80 100 120

Highly Educated workforce

Management Talent

Rule of Law

Transparency

Cultural barriers

Regulatory Environment

Availablity of M&A targets

Customer Sophistication

Competitor presence

Tax Regime

Political/ social stability

Quallity of life

Economic reform

Financial/ economic stability

Infrastructure

Production/ labour reforms

Government incentives

Access to export markets

Market growth potential

Market size

China India

As per the AT Kearney Confidence survey India scores favorably in the educated work

force and management talent while the lack of a sufficient local market is deemed as a

disadvantage while competing for foreign funds

Case studies

In this section we provide case studies of select private equity transactions:

1. Yes Bank

2. Suzlon energy

3. Dr. Reddys Labs

4. Patni Computers

5. Bharti

6. Biocon

7. India Bulls

8. NDTV

Suzlon energy

PE Investors: ChrysCapital, Citicorp

Instruments used: Redeemable convertible preference shares

In October 2005, the company was listed in the Indian stock markets. The closing price

on the IPO date was Rs 693. The cashflow and IRR to the investors is calculated below:

Amount DateTime

elapsed(years) IRRChryscapitalInitial investment (500,000,080) 9-Apr-04Partial Exit - GSIC 2,461,313,200 11-Jul-05 1.25Partial Exit - TRP 1,593,750,000 8-Sep-05 1.42Listing(proxy exit) 5,199,315,660 19-Oct-05 1.53 679%CitiCorpInitial investment (499,999,920) 10-Aug-04Listing(proxy exit) 14,288,662,080 19-Oct-05 1.19 1566%

Terms of the Investment,

The Preference Shares held by the Private Equity Investors are required to be

compulsorily redeemed if the Company undertakes an initial public offer before

December 31, 2005

o The redemption will be made out of the proceeds of the initial public

offer.

The Private Equity Investors have the option to convert the Preference Shares

after December 31, 2005 on the occurrence of the following events:

o Non-completion of an initial public offer;

o A change in control of the Company through a sale of Equity Shares of

the Company or otherwise;

o A sale of 51% or more of the assets of the Company;

o the assignment of any intellectual property owned or used by the

Company which is essential for the continued operation of the business of

the Company

o Default under the Shareholders Agreement (non-occurrence of IPO by

July 1, 2008).

Under the terms of the Shareholder Agreements,

The Board of the Company shall have a maximum of 12 Directors of which,

o One director each shall be a nominee of the Private Equity Investors.

Decisions on certain fundamental matters shall not be taken and/or implemented

without the written consent of the Private Equity Investors

Decisions of fundamental matters shall not be taken or implemented without the

affirmative vote of the Private Equity Investors

o These matters relate to mergers or winding up of the Company,

o the divestment or sale of assets of the Company in excess of Rs. 250

million,

o disposal of intellectual property developed by the Company,

o acquisitions, investments in subsidiaries and securities,

o capital expenditure in excess of Rs. 100 billion,

o indebtedness in excess of 10% above the amounts stated in the annual

budgets of the Company,

o increase in the issued share capital of the Company,

o buyback of shares,

o declaration of dividend in excess of Rs. 330 million or 30% of the net

profits after tax of the Company,

o giving or renewing guarantees in respect of subsidiaries and affiliates,

transactions with affiliates,

o amendments to the articles and memorandum of association and

commencement of a new line of business.

These rights fall away on the Private Equity Investors shareholding falling below

5% or if preference shares held by the investors are redeemed whichever is later.

After the completion of the Issue, upon the redemption of the preference shares

these rights shall not be available to ChrysCapital. Citicorp would continue to

exercise these rights under the above agreement.

Private Equity Investors are prohibited from transferring the Equity Shares held

by them

At any time prior to an initial public offer, if any of the parties desire to transfer a

portion of the Equity Shares held by them to any third party, they shall first offer

the same to the other parties to the Shareholder Agreements.

Further in the event that an initial public offer has not been undertaken by the

Company and the promoters propose to transfer the Equity Shares held by them

the Private Equity Investors shall have tag-along rights, exercisable at their sole

discretion to ensure that all the Shares held by the Private Equity Investors shall

be sold if the Equity Shares proposed to be transferred represent more than 25.1%

of the Shares of the Company and if such percentage is less than 25.1%, the

Private Equity Investors shall have the right to require a pro-rata transfer of the

Equity Shares held by them.

In the event that the Company seeks to create, issue or allot Equity Shares except

in the course of making an IPO, the Private Equity Investors shall have a right to

subscribe for a portion of such proposed issue of Equity Shares to ensure that the

shareholding of the Private Equity Investors remain same after such issue.

In the event the Company proposes to create, issue or allot Shares at a price lower

than the price at which the shares were subscribed to by the Private Equity

Investors, it shall offer to issue such Shares to the Private Equity Investors.

It is also proposed in the Shareholder Agreements, that the Company, undertake

an initial public offer prior to December 31, 2006

Under the terms of the Shareholder Agreements, non-occurrence of an initial

public offering or an offer for sale prior to July 1, 2008 constitutes an event of

default upon which, the Private Equity Investors may require the Company

o (i) to redeem the Preference Shares with the accrued dividends;

o (ii) to convert the Preference Shares and require the Company to follow a

high dividend policy of paying 50% of the profit after tax as dividend or

o (iii) to convert the Preference Shares and, sell their shareholding and

assign their rights under this Agreement.

ICICI Venture’s investment in DRL35

A "Private Investment for Royalties from a Public Enterprise's Future Revenues" deal36.

Dr Reddy’s Laboratories in 2005:

Hyderabad based, publicly listed pharmaceuticals firm Dr Reddy's Laboratories(DRL) a

leading Indian pharmaceutical company, has faced rough weather since mid-2004. Some

of its molecules haven't been doing as well as expected in the U.S. market, and the Indian

pharmaceutical market has been sluggish owing to the introduction of VAT(Value Added