network technology engineering and planning...

TRANSCRIPT

Insights and strategies from three different operational perspectives: q Network Technology

q Engineering and Planning

q Strategic Planning

Build-Out Strategies Going Forward

Brian Wagner VP of Sales Engineering/Carrier Relations

Mammoth Networks

Build-Out Strategies Going Forward

q Introduction - Brian Wagner, Mammoth Networks

q Network Technology – Kevin Arthur, CentraCom

q Engineering & Planning – Ron Ellis, NexTech

q Strategic Planning – Greg Lowe, Syringa Networks

q Wrap-Up Summary Q &A – Brian Wagner, Mammoth Networks

Panel Participants and Outline

Buildout Strategies Moving Forward Network Technologies

Kevin Arthur – VP Network Operations

CentraCom Background ✦ CentraCom began in 1903 as a rural telephone company in Fairview, UT due

to Mountain Bell deciding not to provide service to Fairview.

✦ CentraCom expanded through acquisition of Bell and other telephone exchanges with the last landline network expansion in 2001.

✦ With the pending decline of the landline CentraCom began to look at CATV networks to not only fend off competition in it’s ILEC areas but also expand the company’s network into new areas.

✦ Fiber based rural CLEC began in 2006 to serve major commercial customers in Nevada that could not get advanced services from ILEC in the territory.

CentraCom Background ✦ In 2008 fiber was built into Salt Lake City connecting our network both rural

and metro to the communications hub for the state.

✦ Metro area CLEC started in 2009 partnering with state agencies, school districs, and health care companies.

✦ The metro CLEC quickly began to grow with customers from all sizes of enterprise, wireless carriers, state and local government offering them a pure IP network and full services and support on top.

✦ In 2013 CentraCom began to move into NNI relationships with other carriers exchanging traffic on each others networks to serve more customers than ever possible using our own network.

Traditional Strategies – ILEC telco ✦ In 2001 we had 2 Nortel DMS-10s, 7 Alcatel OC3 nodes, 12 AFC

shelves fed by copper spans, a few flavors of DSL, and dialup services.

✦ Grow the ILEC by upgrading switching and transmission to give new features and higher DSL speeds.

✦ Build fiber to metro area hubs as well as the outer reaches of our network to reduce maintenance and expand offering to those customers.

Traditional Strategies – CATV network ✦ In 2003 our first CATV network was limited to video only to add to

CentraComs offered services. Soon after cable modem was deployed using DOCSIS 1.0. Packetcable voice service added soon after.

✦ Expand CATV network through acquisition to enhance offering to telco customers as well as limit threatening competition.

✦ Grow network with tech. Deployed DOCSIS 3 in 2010. 50Mbps offered. 100Mbps tested and ready to offer once demand is seen.

Traditional Strategies - CLEC ✦ Our CLEC began in 2006 in West Wendover, NV. Now we have CLEC

customers including schools, hospitals, wireless carriers, and enterprise all over Utah.

✦ Personal service. Get to know your business customers well and be ready to support their IT services as well as carrier services. “What do you need? We can do it!”.

✦ Build for less. We have done our construction with an in house crew.

✦ Organization. From sales, to construction, to network turn up, to billing there are many opportunities for the customer experience to degrade.

Traditional Strategies In General ✦ Keep network strategies separate. We have 3 distinct networks and

3 distinct strategies in building those networks.

✦ Remain flexible. Avoid dedicating yourself to one technology or vendor. Stay on top of new technologies while using all you can out of the old.

✦ Keep staff training up to date both in house and vendor provided.

Traditional Strategies In General ✦ Keep good relationships with peer companies.

✦ Greater pool of experience.

✦ Save time and money when looking at new tech.

✦ Bring work in house.

✦ In house construction and engineering has always been a great advantage over competition for us.

Strategies Moving Forward Technology selection

✦ Simple, usually not multi service platform. Less points of complete services failure, and cross conversion allows more reliability.

✦ Equipment readily available on the used market.

Strategies Moving Forward Keeping a balanced approach on where to put time/money

✦ Grow next gen networks while maintaining legacy networks.

Become more tech savvy

✦ Rely less on vendor support, stock spares, keep techs trained.

✦ Offer expertise to business customers who don’t want to hire an IT staff.

✦ Continually find the best gear for ourselves and our customers.

Strategies Moving Forward Embracing our competition as opportunity

✦ Wireless carriers through backhaul.

✦ Wireline carriers through NNI.

Communication and organization

✦ Seamless transition from sales to billing.

Thank you

Ron Ellis Director of Opera2ons

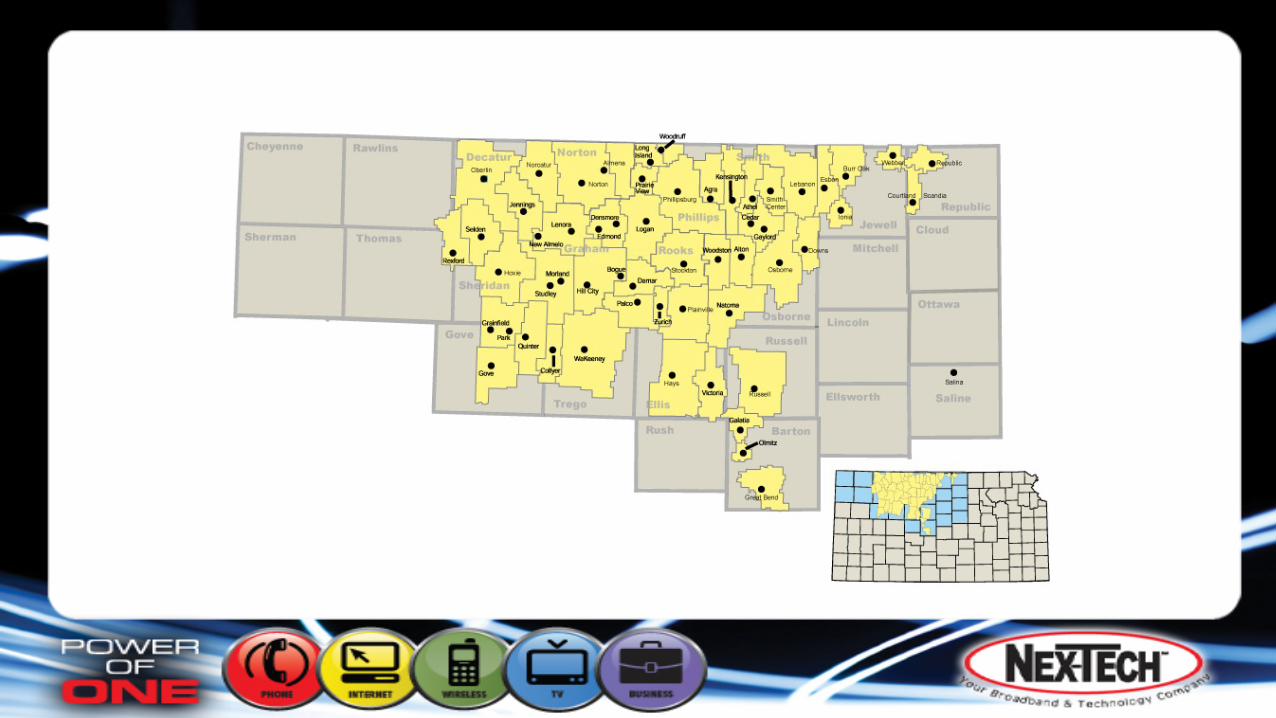

Our Company At A Glance • Nex-‐Tech has been in the communica2ons industry since

1951. We provide communica2ons services to over 9,300 square miles in northwest and central Kansas. These communica2on services include:

• We currently provide these services to over 22,000

residen2al customers, over 4,600 business customers, and employ about 337 full and part-‐2me employees.

• Local Phone & Long Distance • High-‐Speed Internet • Advanced TV Services • Business & Technology Solu2ons • Home Security

Buildout Strategies • We believe in FTTP • It helps future proof your access side • We use ac2ve • Our Network today is a mix of Layer 2 and 3

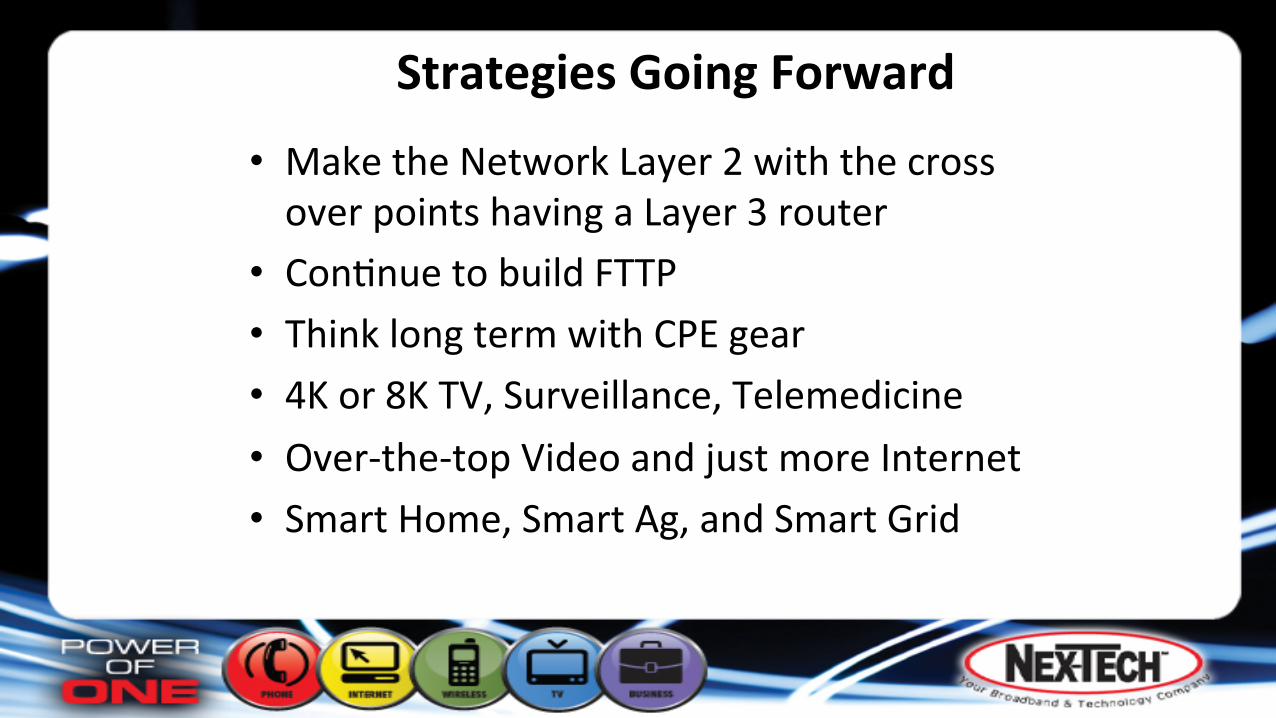

Strategies Going Forward

• Make the Network Layer 2 with the cross over points having a Layer 3 router

• Con2nue to build FTTP • Think long term with CPE gear • 4K or 8K TV, Surveillance, Telemedicine • Over-‐the-‐top Video and just more Internet • Smart Home, Smart Ag, and Smart Grid

Summary

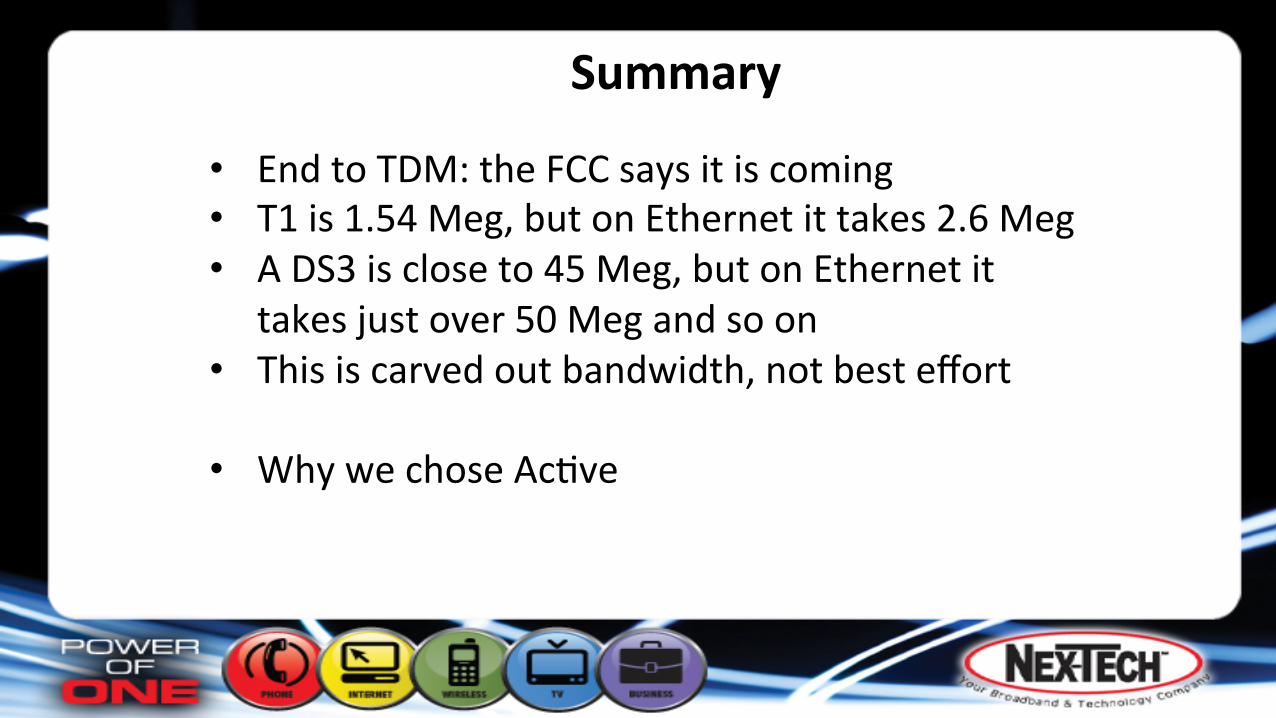

• End to TDM: the FCC says it is coming • T1 is 1.54 Meg, but on Ethernet it takes 2.6 Meg • A DS3 is close to 45 Meg, but on Ethernet it

takes just over 50 Meg and so on • This is carved out bandwidth, not best effort

• Why we chose Ac2ve

Ron Ellis Director of Opera2ons

Strategic Planning

Build Out Strategies Going Forward

4/14/14 Confidential

Company Background

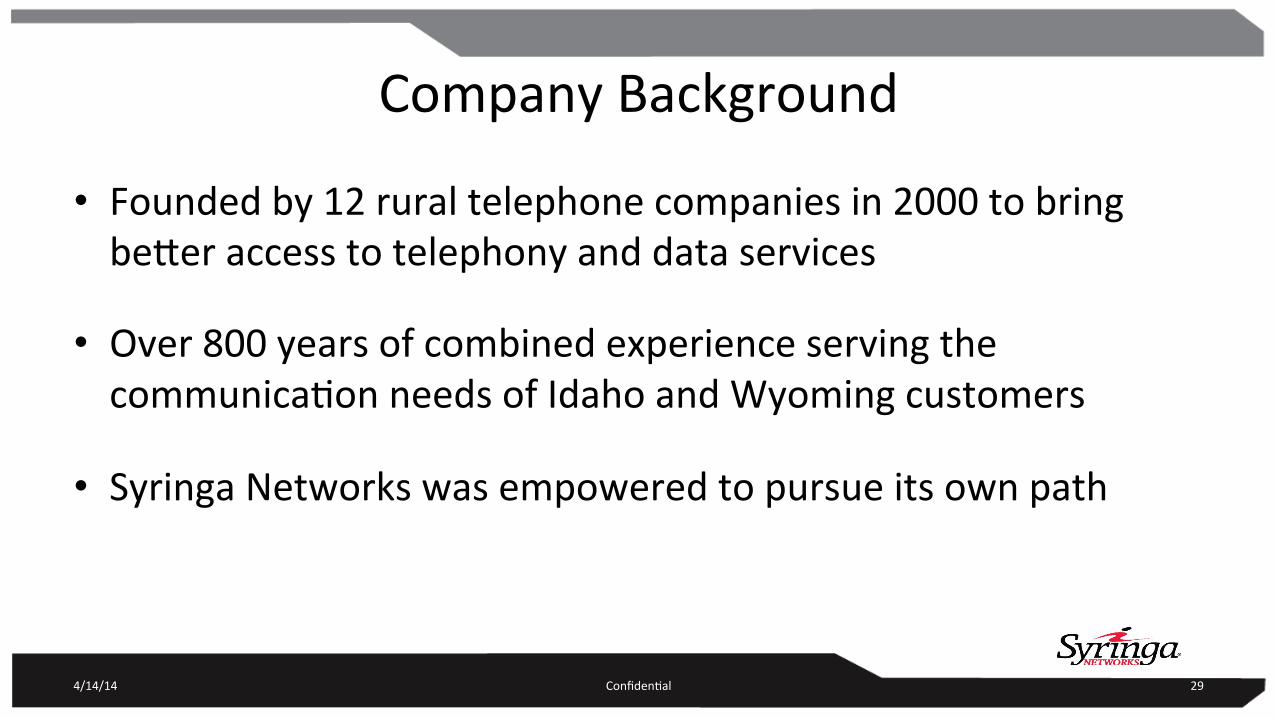

• Founded by 12 rural telephone companies in 2000 to bring be_er access to telephony and data services

• Over 800 years of combined experience serving the communica2on needs of Idaho and Wyoming customers

• Syringa Networks was empowered to pursue its own path

4/14/14 Confiden2al 29

Company Background

4/14/14 Confiden2al 30

• Central Offices in Idaho and Utah

• 140 employees

• 3000 miles of fiber

• We offer 4G LTE to Dark Fiber

• Co-located in key carrier hotels across the US

• One of Idaho’s top 75 privately held companies

2002# 2003# 2004# 2005# 2006# 2007# 2008# 2009# 2010# 2011# 2012# 2013#

Revenue&

Revenue#

TRADITIONAL BUILD OUT STRATEGIES Ninety Nine Percent Of The Time

4/14/14 Confiden2al 31

Step 1: Marke2ng And Sales

• We have a highly compensated marke2ng and sales team – Constantly evalua2ng opportuni2es in and out of market – Knowledge housed in a Customer Resource Management (CRM) database – We know our compe22on and we work with the customer to get a solu2on that exceeds their goals

• Fiber build out plans are directly spun from customer acquisi2on or pursuit thereof

4/14/14 Confiden2al 32

99% Of The Builds Are Contract Based

• Can be a lit service or a dark fiber IRU • We map poten2al builds into Google Earth as part of our staking and route selec2on

• We collect all costs associated with a poten2al build – CAPEX -‐ Outside Plant costs, CPE switches, Etc. – OpEx – Permits, Type II circuit MRC, Agent Fees, Port fees, Building Entrance, Equipment annual maintenance, Etc.

– Core Charge – A forward looking $/Mb charge placed on the circuit to set aside margin for future builds and equipment

4/14/14 Confiden2al 33

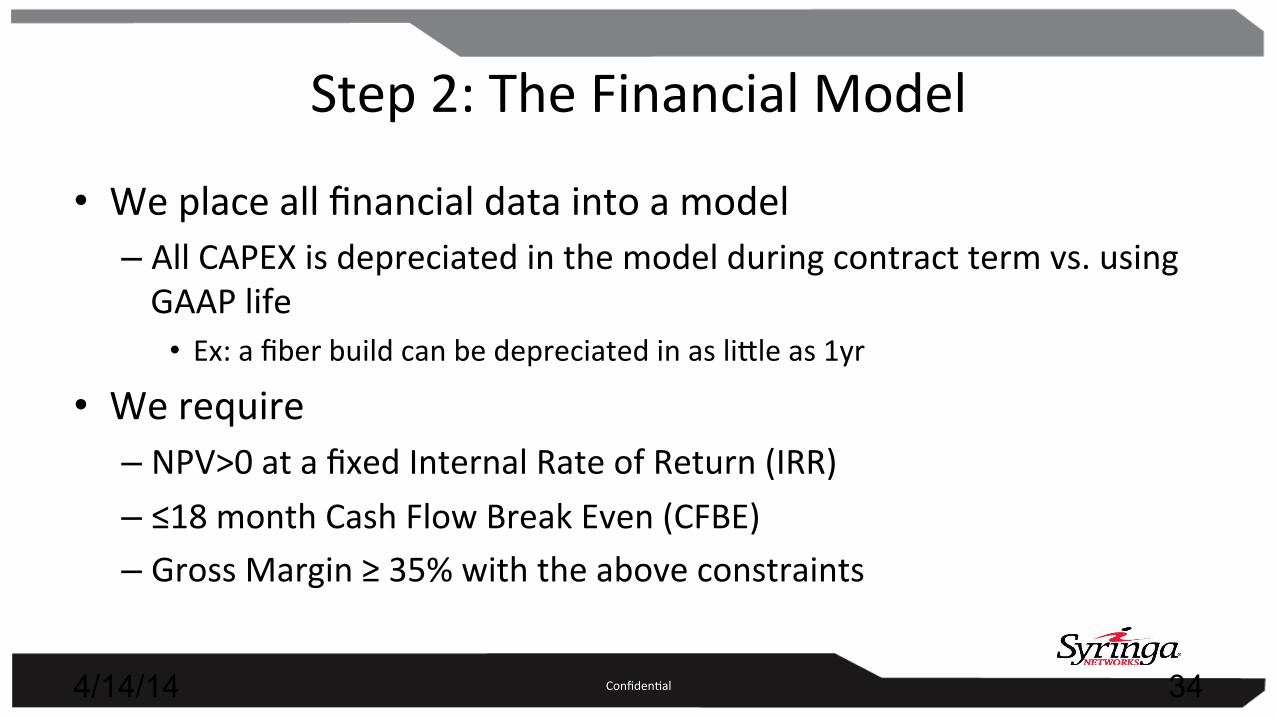

Step 2: The Financial Model

• We place all financial data into a model – All CAPEX is depreciated in the model during contract term vs. using GAAP life

• Ex: a fiber build can be depreciated in as li_le as 1yr

• We require – NPV>0 at a fixed Internal Rate of Return (IRR) – ≤18 month Cash Flow Break Even (CFBE) – Gross Margin ≥ 35% with the above constraints

4/14/14 Confiden2al 34

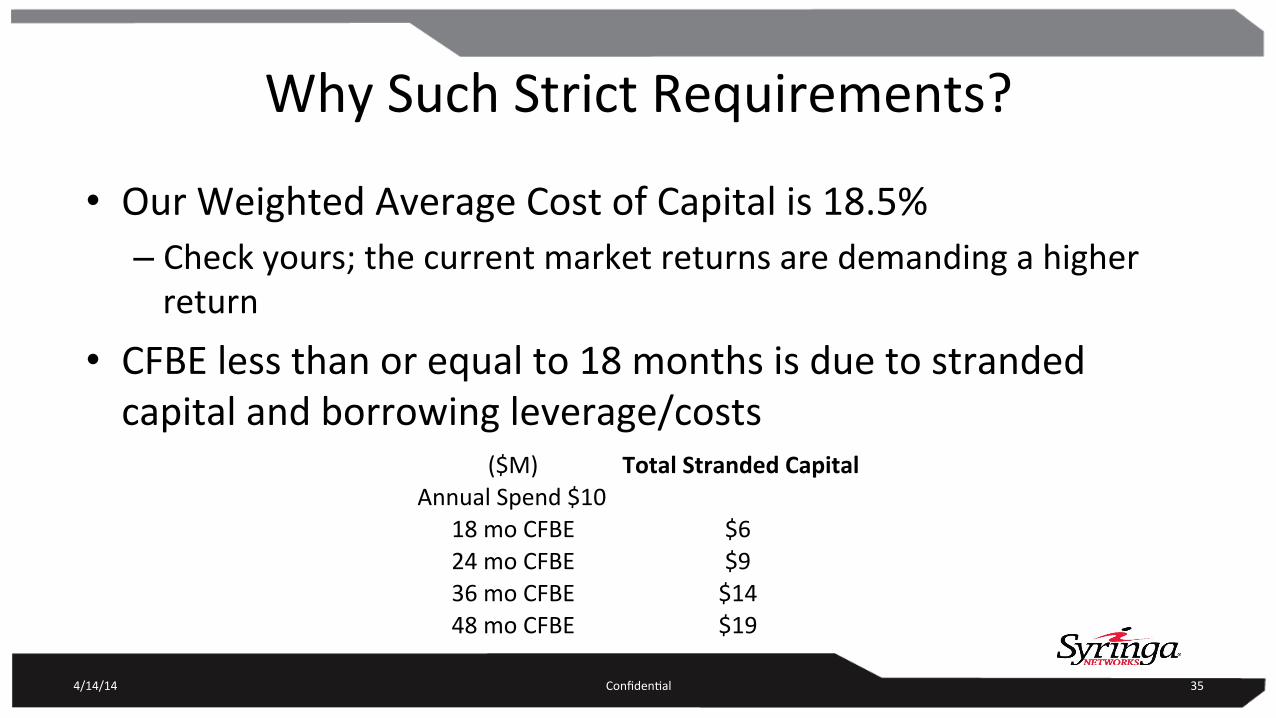

Why Such Strict Requirements?

• Our Weighted Average Cost of Capital is 18.5% – Check yours; the current market returns are demanding a higher return

• CFBE less than or equal to 18 months is due to stranded capital and borrowing leverage/costs

4/14/14 Confiden2al 35

($M) Total&Stranded&CapitalAnnual*Spend*$10

18*mo*CFBE $624*mo*CFBE $936*mo*CFBE $1448*mo*CFBE $19

And If It Doesn’t Conform?

• We increase the MRC, NRC, and/or contract term length un2l it conforms

• We may no longer be compe22ve – If not, we take a pass on the opportunity and save our cash – Being afraid to say “no” leads to bad build outs

• Strategic planning isn’t fiber; it’s sales genera2on and cash management

4/14/14 Confiden2al 36

THE NO CONTRACT BUILD OUT The One-‐Percenter

4/14/14 Confiden2al 37

The Analysis

• Using databases and Google Earth, we create a KMZ showing: – All business with >$5M in sales and more than 5 employees that are located within 1000’ of the proposed route

– We remove all chain stores from the map (Home Depot, McDonalds, etc.)

– We establish a fixed OSP lateral cost for 1000’ of fiber in the market

4/14/14 Confiden2al 38

The Analysis (Cont.)

• We es2mate an addressable market for the remaining business based upon IT spend

• We examine all compe22on and price points for the routes • We make an assump2on for market penetra2on and market maturity

• We place the assump2on in our financial model, look at the damage, and decide

4/14/14 Confiden2al 39

SUMMARY

4/14/14 Confiden2al 40

Summary • The strategy of viewing marke2ng and sales as the engine that drives the rest of your company will lead to a larger fiber footprint

• Managing your cash flows around build outs yields stronger opera2ng results

• Minimizing stranded capital allows a war chest for the 1% case that needs to be pursued

• Saying “no” may be the most profitable thing you can do on any given deal

4/14/14 Confiden2al 41

4/14/14 Confiden2al 42

Thank You

Ø Customer-driven approach

Ø Change

Ø Flexibility

Different organizations but many commonalities

Questions?

» Moderator: Brian Wagner, VP of Sales Engineering/Carrier Relations – Mammoth Networks

» Panelist 1: Kevin Arthur, VP of Operations - CentraCom

» Panelist 2: Ron Ellis, Director of Operations - NexTech

» Panelist 3: Greg Lowe, CEO – Syringa Networks

Build-Out Strategies Moving Forward