network reliability assessment - koç hastanesihome.ku.edu.tr/~indr343/files/chapter 29 (markov...

TRANSCRIPT

1

INDR 343

Stochastic Models

Department of Industrial Engineering

Koç University

Chapter 29

Markov Chains

Süleyman Özekici

ENG 119, Ext: 1723

S. Özekici INDR 343 Stochastic Models 2

Course Topics

• Markov Chains (Chapter 29)

• Queueing Models (Chapter 17)

• Inventory Models (Chapter 18)

• Markov Decision Models (Chapter 19)

2

S. Özekici INDR 343 Stochastic Models 3

Markov Chains and Processes

• Stochastic processes

• Introduction to Markov chains

• Transient analysis

• Classsification of states

• Ergodic and potential analysis of MC

• Introduction to Markov processes

• Ergodic and potential analysis of MP

S. Özekici INDR 343 Stochastic Models 4

Stochastic Processes

• Many stochastic models in operations research are represented using a collection of

random variables that are indexed by time, so that

Xt = state of the system at time t

• Some examples are

– Xt = the number of shoppers who arrived at a supermarket until time t

– Xt = the amount of inventory in stock at the end of week t

– Xt = the number of patients in the emergency room of an hospital at

time t

– Xt = the price of a share of common stock that is traded at Istanbul

Stock Exchange at the close of day t

– Xt = the functional state of a workstation at time t

– Xt = the number of vehicles that arrive at the Boğaziçi bridge during day t

– Xt = the time of arrival of the tth customer to a bank during a given day

– Xt = the number of wins of a soccer team in t matches played

3

S. Özekici INDR 343 Stochastic Models 5

Stochastic Analysis

• A stochastic process X is a collection of random variables

• If T = {0, 1, 2, 3, ...}, then X is a dicrete-time process

• If T = [0, +∞), then X is a continuous-time process

• If Xt is a discrete random variable, taking values in a set like {0, 1, 2, ... },

then X is a discrete-state process

• If Xt is a continuous random variable, taking values in a set like [0, +∞), then

X is a continuous-state process

• We need to determine the probability law of X, and analyze it to detemine

P{Xt = i} (Transient analysis)

limt+∞ P{Xt = i} (Ergodic analysis)

};{ TtXX t

0

( ) (Potential analysis)t

t

t

E f X+

S. Özekici INDR 343 Stochastic Models 6

Markov Chain: Definition

• The discrete time and state stochastic process X = {Xt; t = 0, 1, 2, ...} is said to be a

Markov chain if it satisfies the following so-called Markov property

P{Xt+1 =j | X0 = k0, ..., Xt-1 = kt-1, Xt = i} = P{Xt+1 = j | Xt = i}

for i,j in {0, 1, 2, ..., M} • We will suppose in this course that these conditional probabilities do not depend on

time t, so that the transition probabilities are given by the following transition matrix

P{Xt+1 = j | Xt = i} = Pij

• In general, the n-step transition matrix is denoted by

P{Xt+n = j | Xt = i} = Pij(n)

• We know that

1

0

0

)(

)(

M

j

n

ij

n

ij

P

P

4

S. Özekici INDR 343 Stochastic Models 7

An Inventory Example

• Suppose that the weekly demand for cameras in a store D1, D2, ... are independent and identically distributed random variables that have a Poisson distribution with mean 1. This means

P{Dt = n}= e-11n/n!

• The number of cameras is observed at the close of the working day every Saturday and if there are no cameras left 3 new cameras are ordered. The order is received at the beginning of the week on Monday morning (immediate delivery). If there are 1, 2 or 3 cameras in the store, no new order is placed.

• This ordering policy is known as the (s, S) policy where s = 0 and S = 3 in this example (i.e., order up to S units whenever you have s or less units left in stock).

• If there is no stock left when a customer arrives, then the sale is lost.

• Let Xt be the number of cameras left in the store at the end of week t

S. Özekici INDR 343 Stochastic Models 8

1

1

t 1

max{3- ,0} if 0

max{ - ,0} if 1

t t

t

t t

D XX

X D X

+

+

+

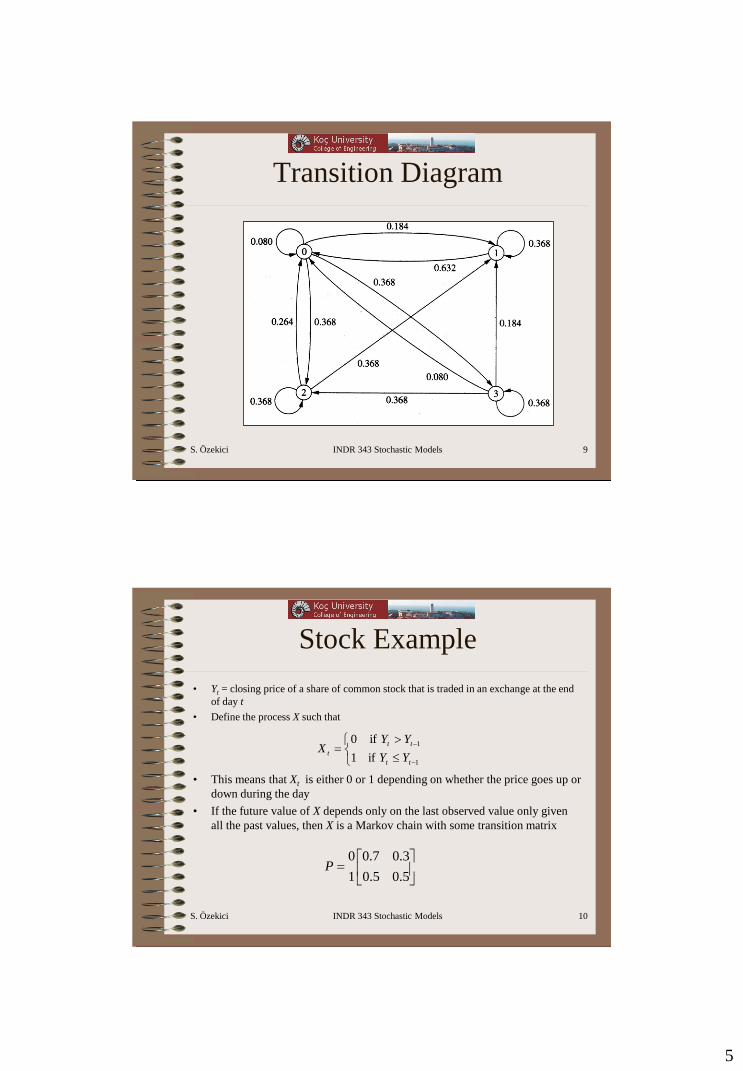

The Transition Matrix

632.0!0

)1(1}0{1}1{

184.0!2

)1(}2{

368.0368.0184.0080.0

0368.0368.0264.0

00368.0632.0

368.0368.0184.0080.0

3

2

1

0

10

1110

12

101

++

+

eDPDPP

eDPP

P

tt

t

5

S. Özekici INDR 343 Stochastic Models 9

Transition Diagram

S. Özekici INDR 343 Stochastic Models 10

Stock Example

• Yt = closing price of a share of common stock that is traded in an exchange at the end

of day t

• Define the process X such that

• This means that Xt is either 0 or 1 depending on whether the price goes up or

down during the day

• If the future value of X depends only on the last observed value only given

all the past values, then X is a Markov chain with some transition matrix

if1

if0

1

1

tt

tt

tYY

YYX

5.05.0

3.07.0

1

0P

6

S. Özekici INDR 343 Stochastic Models 11

Another Stock Example

• Suppose that the value of X depends on the previous 2 values of X only, then

Zt = (Xt, Xt-1) is a Markov chain with states

0 = (0, 0): the stock increased both today and yesterday

1 = (1, 0): the stock increased today and decreased yesterday

2 = (0, 1): the stock decreased today and increased yesterday

3 = (1, 1): the stock decreased both today and yesterday

• The transition matrix is

7.003.00

5.005.00

04.006.0

01.009.0

3

2

1

0

P

S. Özekici INDR 343 Stochastic Models 12

Gambling Example

• Suppose that a player has $1 and with each play of a game wins $1 with

probability p or loses $1 with probability (1 - p). The game ends when the

fortune of the player becomes $3 or when he goes broke.

• Let Xt be the amount of money that the player has at the end of the tth game,

then X is a Markov chain with states {0, 1, 2, 3} and transition matrix

1000

010

001

0001

3

2

1

0

pp

ppP

7

S. Özekici INDR 343 Stochastic Models 13

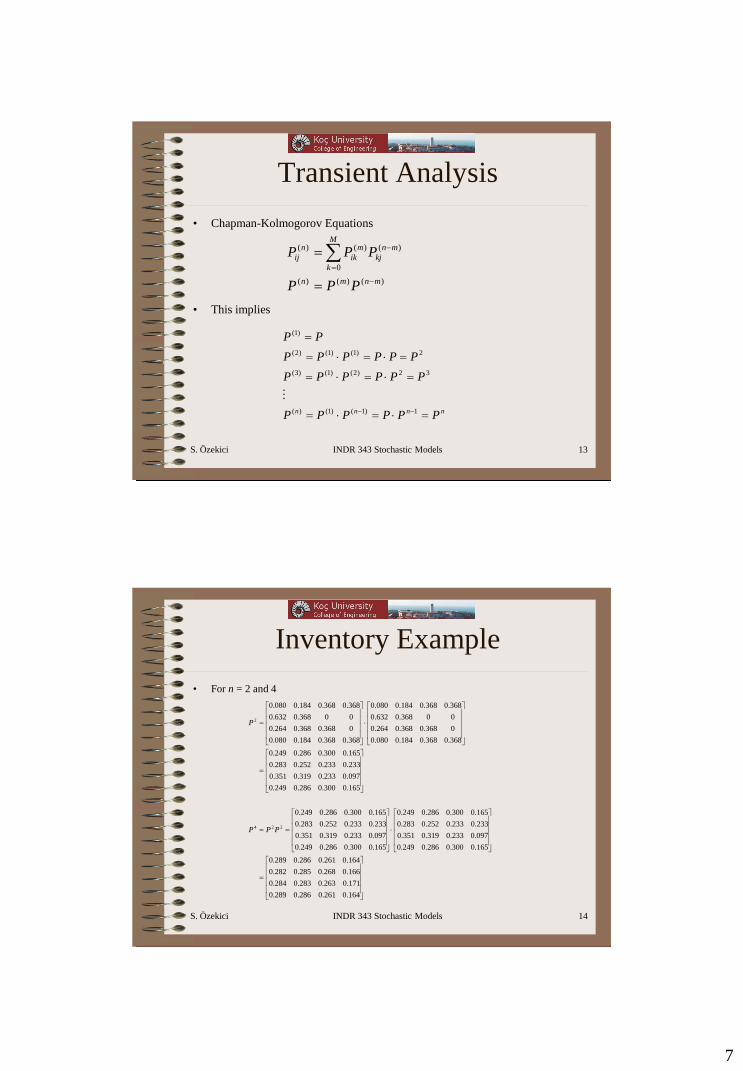

Transient Analysis

• Chapman-Kolmogorov Equations

• This implies

)()()(

0

)()()(

mnmn

M

k

mn

kj

m

ik

n

ij

PPP

PPP

nnnn PPPPPP

PPPPPP

PPPPPP

PP

1)1()1()(

32)2()1()3(

2)1()1()2(

)1(

S. Özekici INDR 343 Stochastic Models 14

Inventory Example

• For n = 2 and 4

164.0261.0286.0289.0

171.0263.0283.0284.0

166.0268.0285.0282.0

164.0261.0286.0289.0

165.0300.0286.0249.0

097.0233.0319.0351.0

233.0233.0252.0283.0

165.0300.0286.0249.0

165.0300.0286.0249.0

097.0233.0319.0351.0

233.0233.0252.0283.0

165.0300.0286.0249.0

165.0300.0286.0249.0

097.0233.0319.0351.0

233.0233.0252.0283.0

165.0300.0286.0249.0

368.0368.0184.0080.0

0368.0368.0264.0

00368.0632.0

368.0368.0184.0080.0

368.0368.0184.0080.0

0368.0368.0264.0

00368.0632.0

368.0368.0184.0080.0

224

2

PPP

P

8

S. Özekici INDR 343 Stochastic Models 15

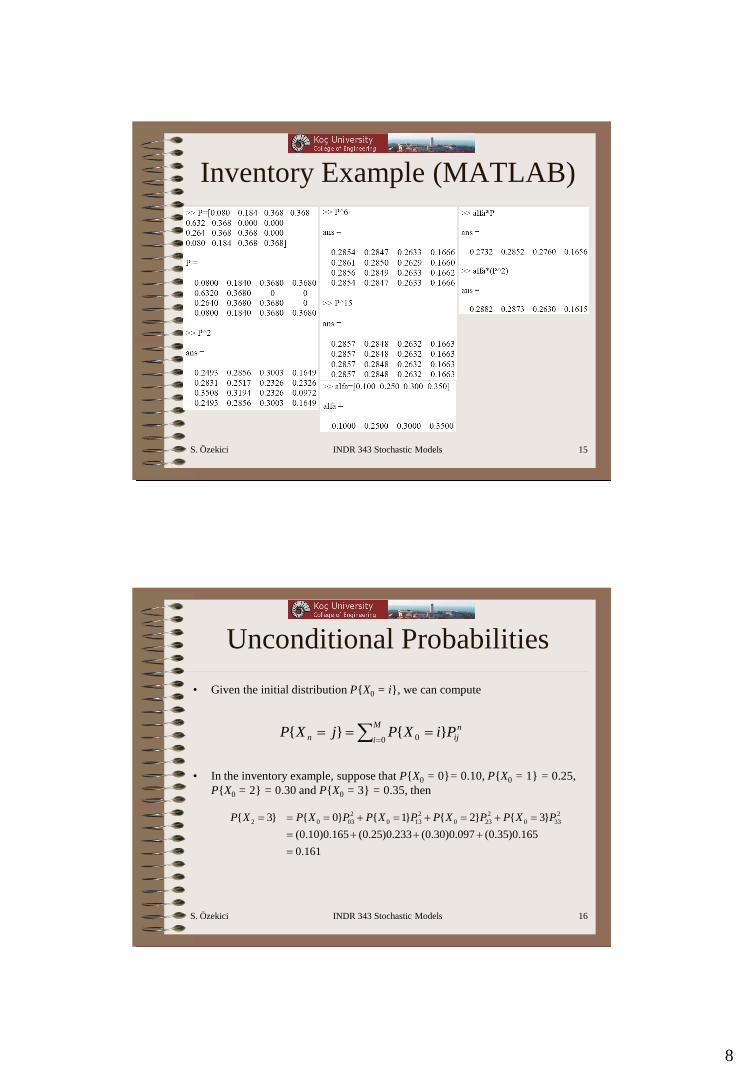

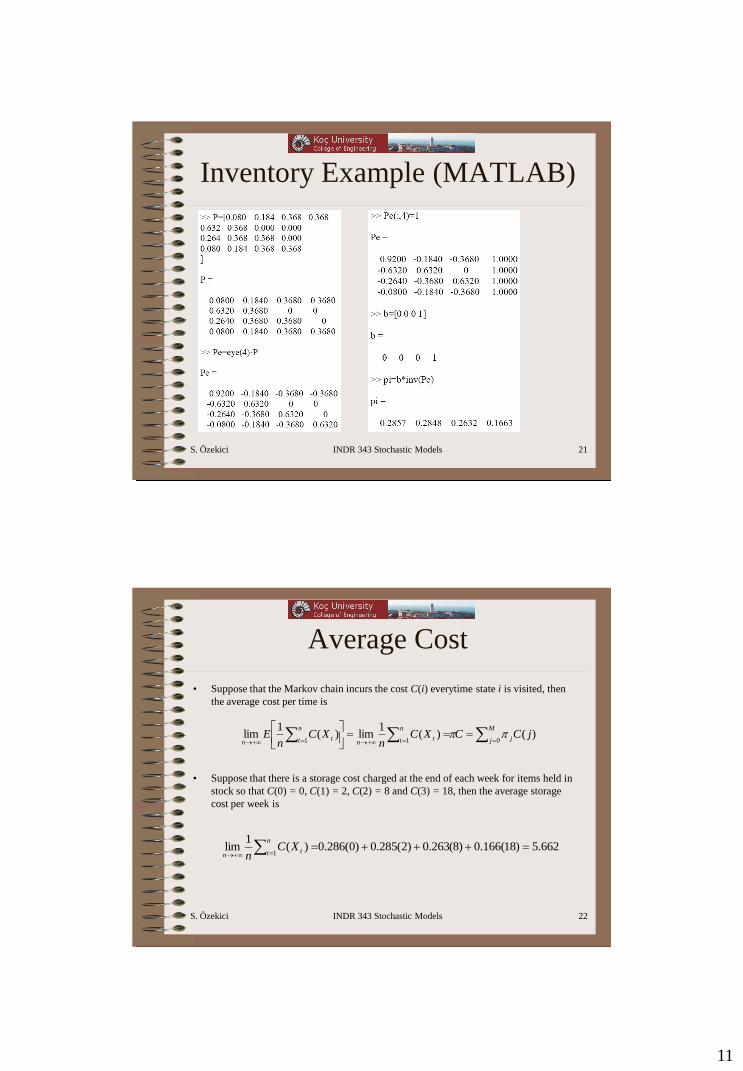

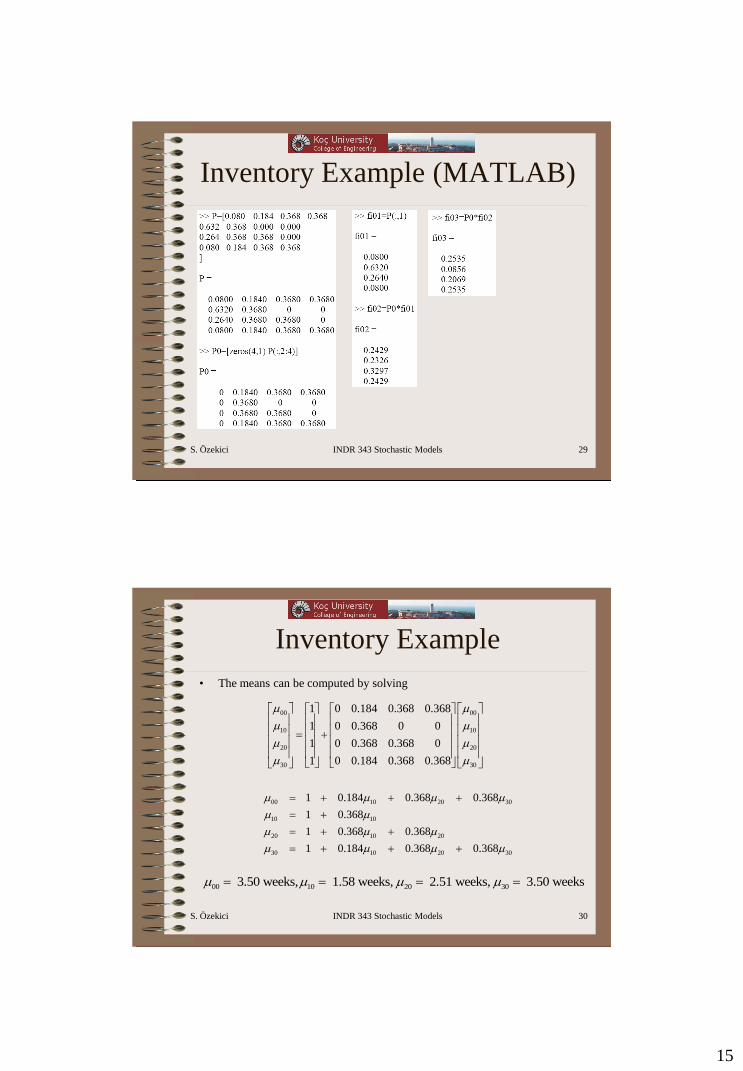

Inventory Example (MATLAB)

S. Özekici INDR 343 Stochastic Models 16

Unconditional Probabilities

• Given the initial distribution P{X0 = i}, we can compute

• In the inventory example, suppose that P{X0 = 0}= 0.10, P{X0 = 1} = 0.25,

P{X0 = 2} = 0.30 and P{X0 = 3} = 0.35, then

M

i

n

ijn PiXPjXP0 0 }{}{

2 2 2 2

2 0 03 0 13 0 23 0 33{ 3} { 0} { 1} { 2} { 3}

(0.10)0.165 (0.25)0.233 (0.30)0.097 (0.35)0.165

0.161

P X P X P P X P P X P P X P + + +

+ + +

9

S. Özekici INDR 343 Stochastic Models 17

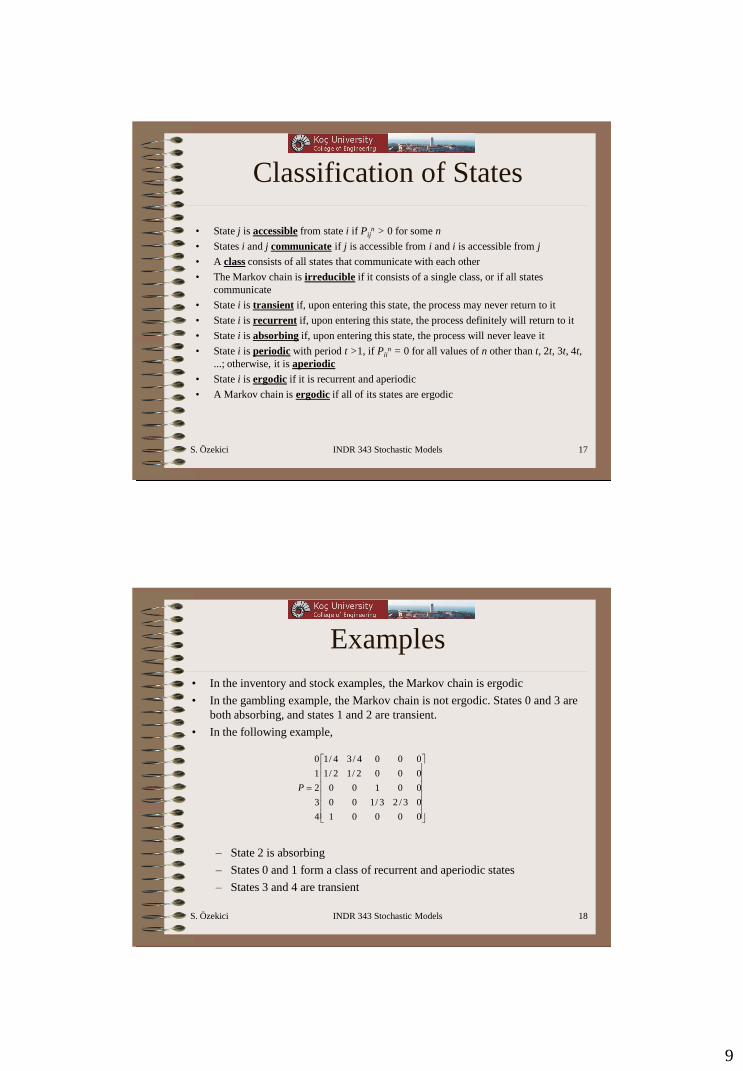

Classification of States

• State j is accessible from state i if Pijn > 0 for some n

• States i and j communicate if j is accessible from i and i is accessible from j

• A class consists of all states that communicate with each other

• The Markov chain is irreducible if it consists of a single class, or if all states

communicate

• State i is transient if, upon entering this state, the process may never return to it

• State i is recurrent if, upon entering this state, the process definitely will return to it

• State i is absorbing if, upon entering this state, the process will never leave it

• State i is periodic with period t >1, if Piin = 0 for all values of n other than t, 2t, 3t, 4t,

...; otherwise, it is aperiodic

• State i is ergodic if it is recurrent and aperiodic

• A Markov chain is ergodic if all of its states are ergodic

S. Özekici INDR 343 Stochastic Models 18

Examples

• In the inventory and stock examples, the Markov chain is ergodic

• In the gambling example, the Markov chain is not ergodic. States 0 and 3 are

both absorbing, and states 1 and 2 are transient.

• In the following example,

– State 2 is absorbing

– States 0 and 1 form a class of recurrent and aperiodic states

– States 3 and 4 are transient

00001

03/23/100

00100

0002/12/1

0004/34/1

4

3

2

1

0

P

10

S. Özekici INDR 343 Stochastic Models 19

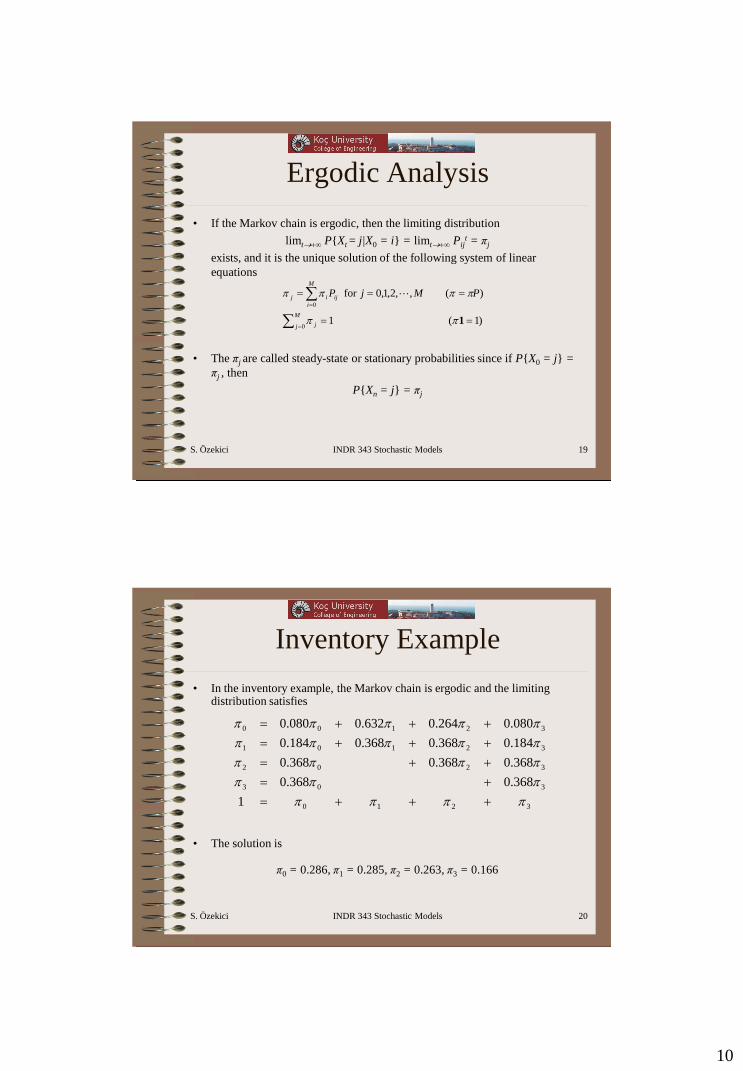

Ergodic Analysis

• If the Markov chain is ergodic, then the limiting distribution

limt+∞ P{Xt = j|X0 = i} = limt+∞ Pijt = πj

exists, and it is the unique solution of the following system of linear

equations

• The πj are called steady-state or stationary probabilities since if P{X0 = j} =

πj , then

P{Xn = j} = πj

)1( 1

)( ,,2,1,0for

0

0

1

M

j j

M

i

ijij PMjP

S. Özekici INDR 343 Stochastic Models 20

Inventory Example

• In the inventory example, the Markov chain is ergodic and the limiting distribution satisfies

• The solution is

π0 = 0.286, π1 = 0.285, π2 = 0.263, π3 = 0.166

3210

303

3202

32101

32100

1

368.0368.0

368.0368.0368.0

184.0368.0368.0184.0

080.0264.0632.0080.0

+++

+

++

+++

+++

11

S. Özekici INDR 343 Stochastic Models 21

Inventory Example (MATLAB)

S. Özekici INDR 343 Stochastic Models 22

Average Cost

• Suppose that the Markov chain incurs the cost C(i) everytime state i is visited, then

the average cost per time is

• Suppose that there is a storage cost charged at the end of each week for items held in

stock so that C(0) = 0, C(1) = 2, C(2) = 8 and C(3) = 18, then the average storage

cost per week is

++

M

j j

n

t tn

n

t tn

jCCXCn

XCn

E011

)()(1

lim)(1

lim

662.5)18(166.0)8(263.0)2(285.0)0(286.0)(1

lim1

+++ +

n

t tn

XCn

12

S. Özekici INDR 343 Stochastic Models 23

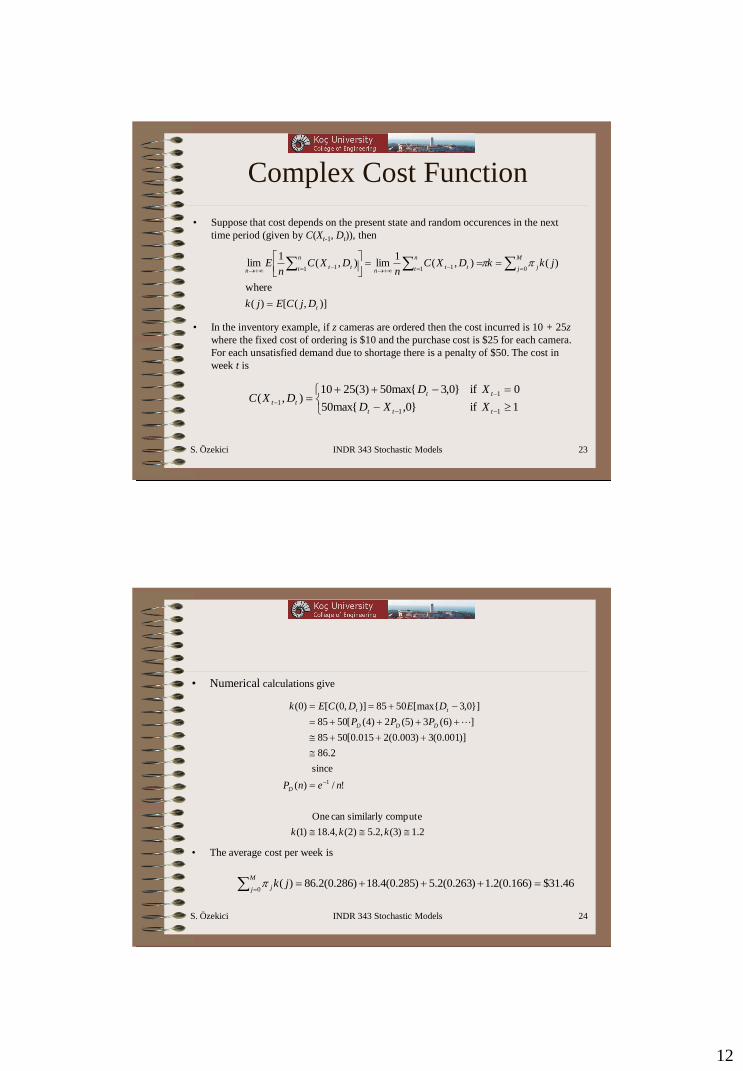

Complex Cost Function

• Suppose that cost depends on the present state and random occurences in the next

time period (given by C(Xt-1, Dt)), then

• In the inventory example, if z cameras are ordered then the cost incurred is 10 + 25z

where the fixed cost of ordering is $10 and the purchase cost is $25 for each camera.

For each unsatisfied demand due to shortage there is a penalty of $50. The cost in

week t is

)],([)(

where

)(),(1

lim),(1

lim01 11 1

t

M

j j

n

t ttn

n

t ttn

DjCEjk

jkkDXCn

DXCn

E

+ +

++

1 if}0,50max{

0 if}0,350max{25(3)10),(

11

1

1

ttt

tt

ttXXD

XDDXC

S. Özekici INDR 343 Stochastic Models 24

• Numerical calculations give

• The average cost per week is

2.1)3(,2.5)2(,4.18)1(

computesimilarly can One

!/)(

since

2.86

)]001.0(3)003.0(2015.0[5085

])6(3)5(2)4([5085

}]0,3{max[5085)],0([)0(

1

+++

++++

+

kkk

nenP

PPP

DEDCEk

D

DDD

tt

46.31$)166.0(2.1)263.0(2.5)285.0(4.18)286.0(2.86)(0

+++

M

j j jk

13

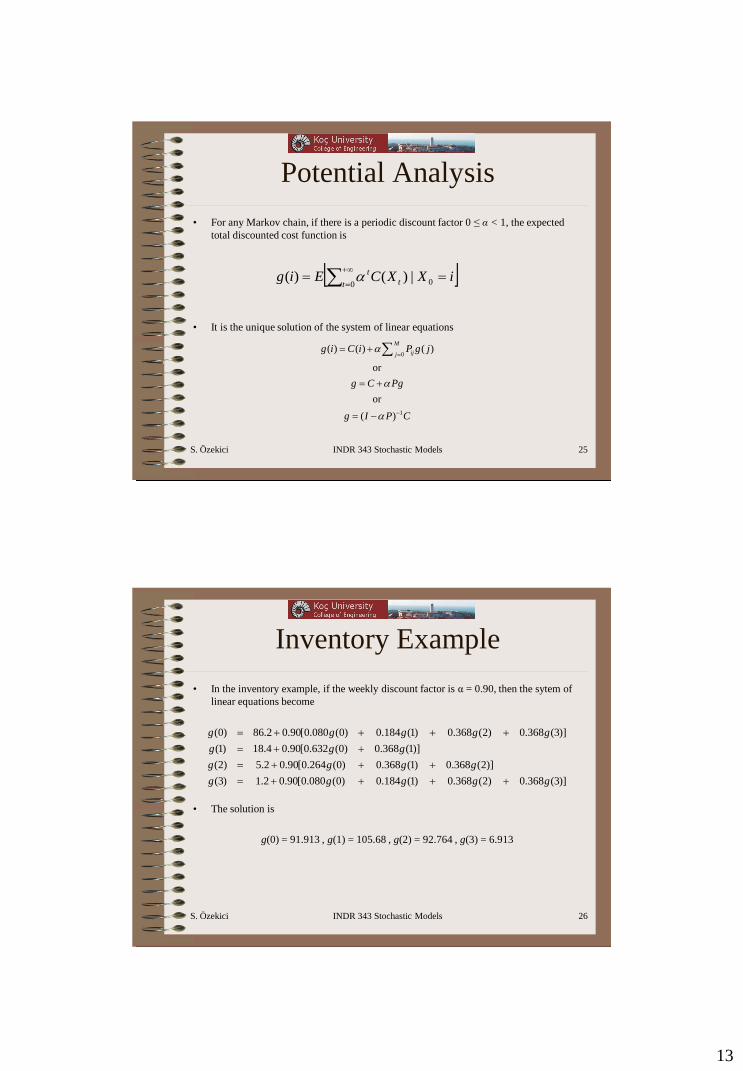

S. Özekici INDR 343 Stochastic Models 25

Potential Analysis

• For any Markov chain, if there is a periodic discount factor 0 ≤ α < 1, the expected

total discounted cost function is

• It is the unique solution of the system of linear equations

+

0 0|)()(t t

t iXXCEig

0

1

( ) ( ) ( )

or

or

( )

M

ijjg i C i P g j

g C Pg

g I P C

+

+

S. Özekici INDR 343 Stochastic Models 26

Inventory Example

• In the inventory example, if the weekly discount factor is α = 0.90, then the sytem of

linear equations become

• The solution is

g(0) = 91.913 , g(1) = 105.68 , g(2) = 92.764 , g(3) = 6.913

)]3(368.0)2(368.0)1(184.0)0(080.0[90.02.1)3(

)]2(368.0)1(368.0)0(264.0[90.02.5)2(

)]1(368.0)0(632.0[90.04.18)1(

)]3(368.0)2(368.0)1(184.0)0(080.0[90.02.86)0(

ggggg

gggg

ggg

ggggg

++++

+++

++

++++

14

S. Özekici INDR 343 Stochastic Models 27

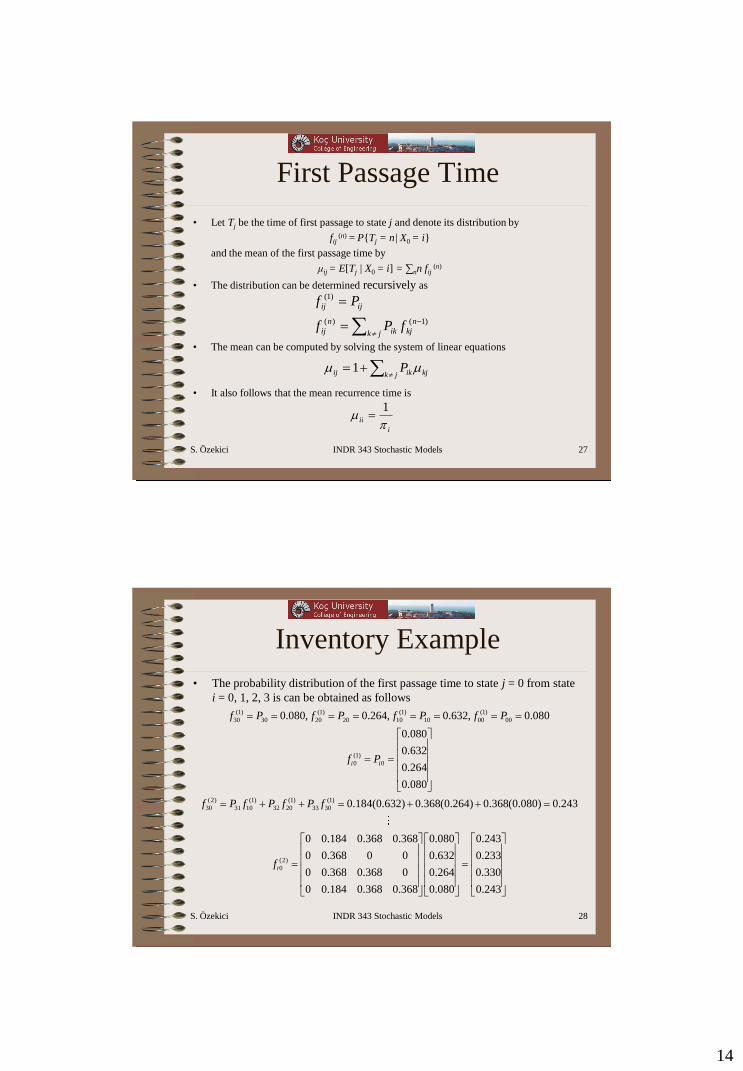

First Passage Time

• Let Tj be the time of first passage to state j and denote its distribution by

fij (n) = P{Tj = n| X0 = i}

and the mean of the first passage time by

μij = E[Tj | X0 = i] = ∑nn fij (n)

• The distribution can be determined recursively as

• The mean can be computed by solving the system of linear equations

• It also follows that the mean recurrence time is

jk

n

kjik

n

ij

ijij

fPf

Pf

)1()(

)1(

+

jk kjikij P 1

i

ii

1

S. Özekici INDR 343 Stochastic Models 28

Inventory Example

• The probability distribution of the first passage time to state j = 0 from state

i = 0, 1, 2, 3 is can be obtained as follows

(1) (1) (1) (1)

30 30 20 20 10 10 00 00

(1)

0 0

(2) (1) (1) (1)

30 31 10 32 20 33 30

(2)

0

0.080, 0.264, 0.632, 0.080

0.080

0.632

0.264

0.080

0.184(0.632) 0.368(0.264) 0.368(0.080) 0.243

0

i i

i

f P f P f P f P

f P

f P f P f P f

f

+ + + +

0.184 0.368 0.368 0.080 0.243

0 0.368 0 0 0.632 0.233

0 0.368 0.368 0 0.264 0.330

0 0.184 0.368 0.368 0.080 0.243

15

S. Özekici INDR 343 Stochastic Models 29

Inventory Example (MATLAB)

S. Özekici INDR 343 Stochastic Models 30

Inventory Example

00 10 20 30

10 10

20 10 20

30 10 20 30

1 0.184 0.368 0.368

1 0.368

1 0.368 0.368

1 0.184 0.368 0.368

+ + +

+

+ +

+ + +

00 10 20 30 3.50 weeks, 1.58 weeks, 2.51 weeks, 3.50 weeks

• The means can be computed by solving

00 00

10 10

20 20

30 30

1 0 0.184 0.368 0.368

1 0 0.368 0 0

1 0 0.368 0.368 0

1 0 0.184 0.368 0.368

+

16

S. Özekici INDR 343 Stochastic Models 31

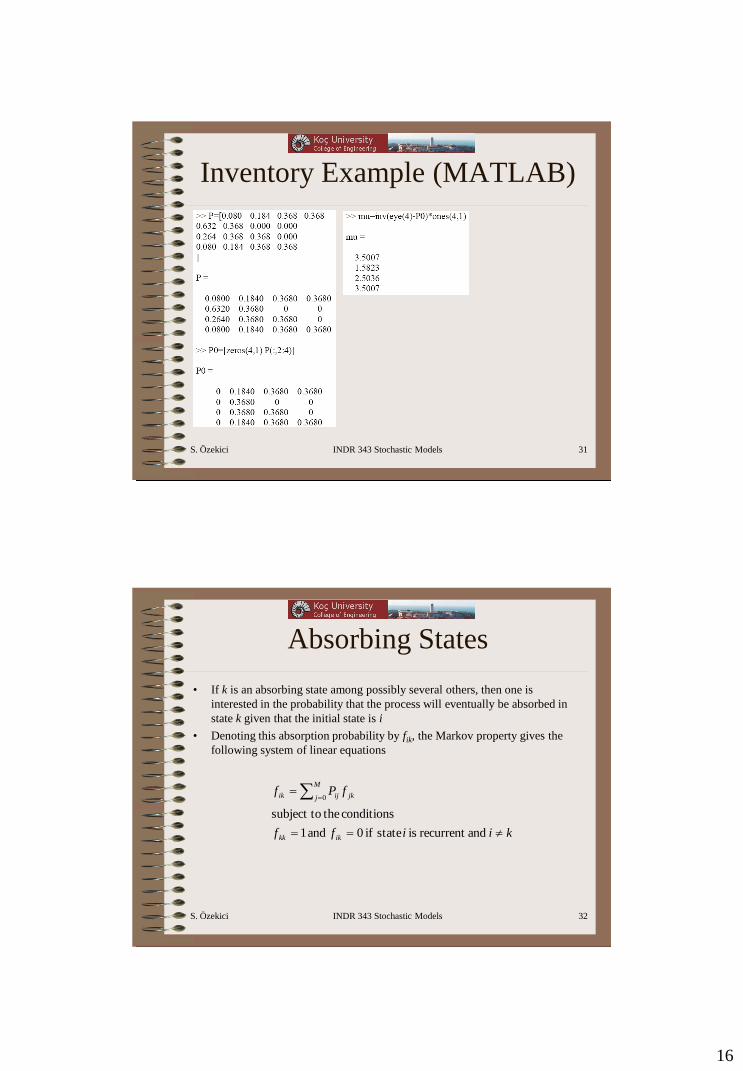

Inventory Example (MATLAB)

S. Özekici INDR 343 Stochastic Models 32

Absorbing States

• If k is an absorbing state among possibly several others, then one is

interested in the probability that the process will eventually be absorbed in

state k given that the initial state is i

• Denoting this absorption probability by fik, the Markov property gives the

following system of linear equations

kiiff

fPf

ikkk

M

j jkijik

andrecurrent is state if 0 and 1

conditions thesubject to

0

17

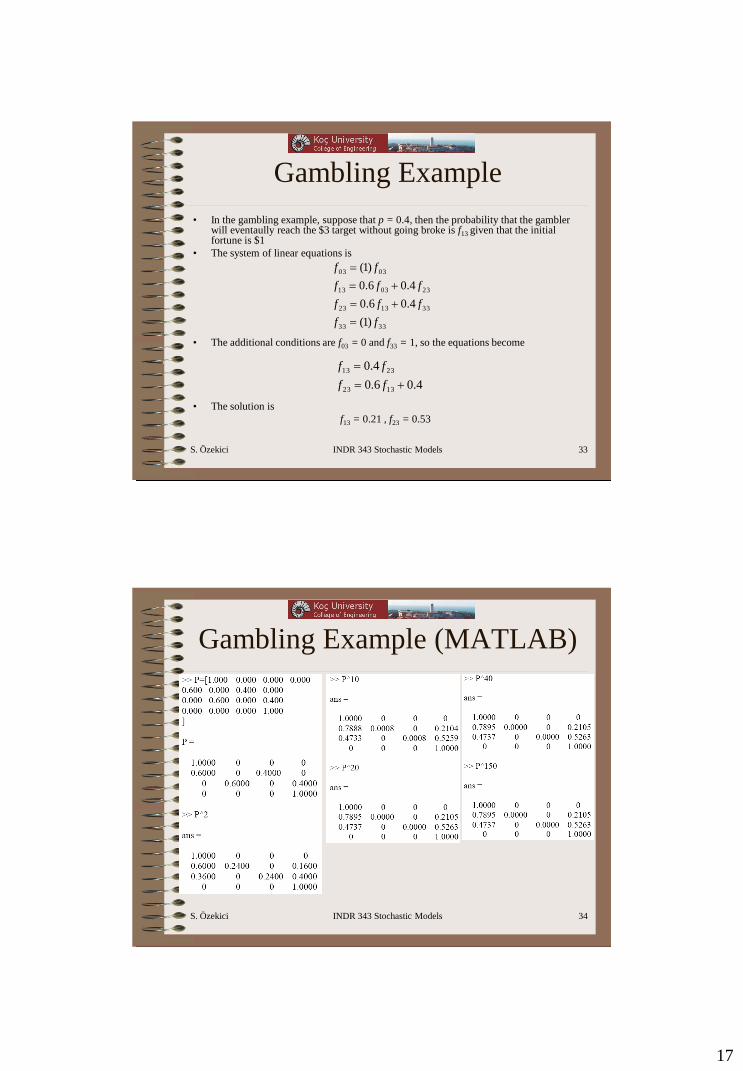

S. Özekici INDR 343 Stochastic Models 33

Gambling Example

• In the gambling example, suppose that p = 0.4, then the probability that the gambler will eventaully reach the $3 target without going broke is f13 given that the initial fortune is $1

• The system of linear equations is

• The additional conditions are f03 = 0 and f33 = 1, so the equations become

• The solution is

f13 = 0.21 , f23 = 0.53

3333

331323

230313

0303

)1(

4.06.0

4.06.0

)1(

ff

fff

fff

ff

+

+

4.06.0

4.0

1323

2313

+

ff

ff

S. Özekici INDR 343 Stochastic Models 34

Gambling Example (MATLAB)

18

S. Özekici INDR 343 Stochastic Models 35

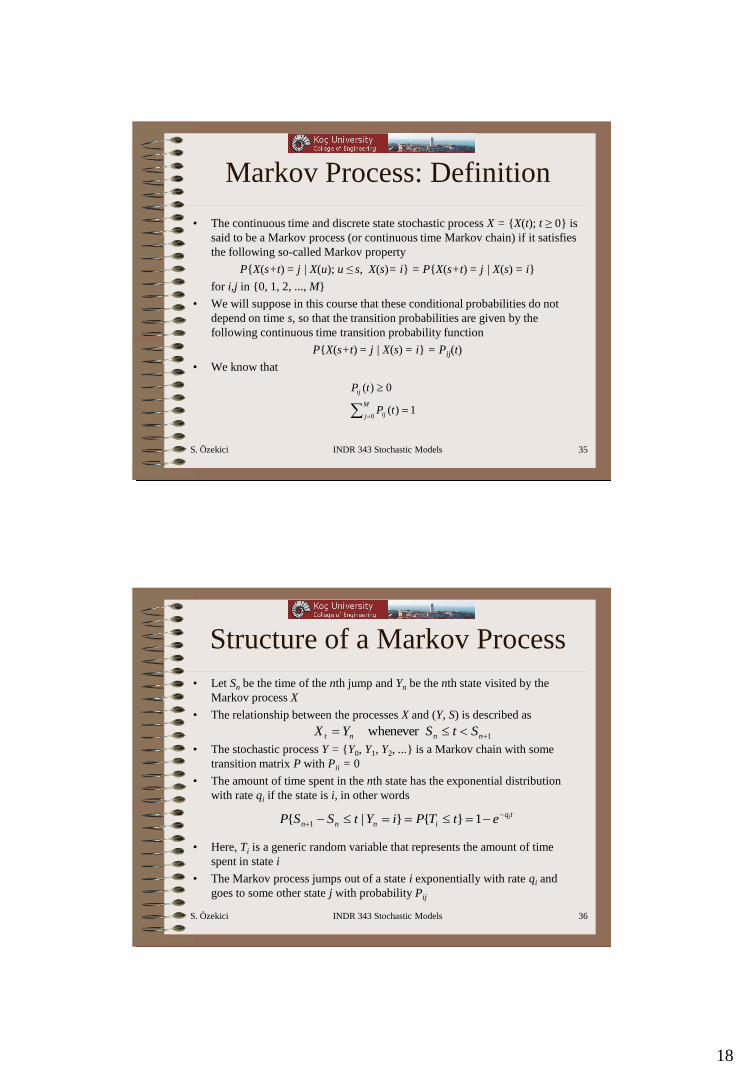

Markov Process: Definition

• The continuous time and discrete state stochastic process X = {X(t); t ≥ 0} is

said to be a Markov process (or continuous time Markov chain) if it satisfies

the following so-called Markov property

P{X(s+t) = j | X(u); u ≤ s, X(s)= i} = P{X(s+t) = j | X(s) = i}

for i,j in {0, 1, 2, ..., M}

• We will suppose in this course that these conditional probabilities do not

depend on time s, so that the transition probabilities are given by the

following continuous time transition probability function

P{X(s+t) = j | X(s) = i} = Pij(t)

• We know that

1)(

0)(

0

M

j ij

ij

tP

tP

S. Özekici INDR 343 Stochastic Models 36

Structure of a Markov Process

• Let Sn be the time of the nth jump and Yn be the nth state visited by the

Markov process X

• The relationship between the processes X and (Y, S) is described as

• The stochastic process Y = {Y0, Y1, Y2, ...} is a Markov chain with some

transition matrix P with Pii = 0

• The amount of time spent in the nth state has the exponential distribution

with rate qi if the state is i, in other words

• Here, Ti is a generic random variable that represents the amount of time

spent in state i

• The Markov process jumps out of a state i exponentially with rate qi and

goes to some other state j with probability Pij

1er whenev + nnnt StSYX

tq

innnietTPiYtSSP

+ 1}{}|{ 1

19

S. Özekici INDR 343 Stochastic Models 37

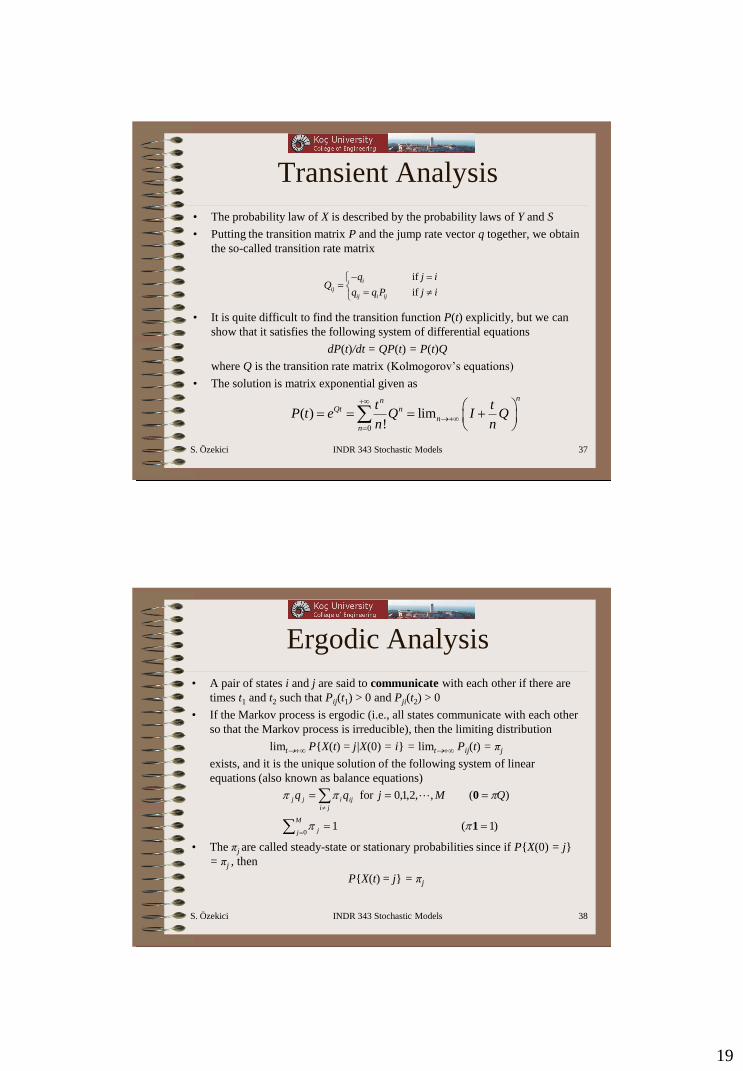

Transient Analysis

• The probability law of X is described by the probability laws of Y and S

• Putting the transition matrix P and the jump rate vector q together, we obtain

the so-called transition rate matrix

• It is quite difficult to find the transition function P(t) explicitly, but we can

show that it satisfies the following system of differential equations

dP(t)/dt = QP(t) = P(t)Q

where Q is the transition rate matrix (Kolmogorov’s equations)

• The solution is matrix exponential given as

if

if

i

ij

ij i ij

q j iQ

q q P j i

0

( ) lim!

nnQt n

n

n

t tP t e Q I Q

n n

+

+

+

S. Özekici INDR 343 Stochastic Models 38

Ergodic Analysis

• A pair of states i and j are said to communicate with each other if there are

times t1 and t2 such that Pij(t1) > 0 and Pji(t2) > 0

• If the Markov process is ergodic (i.e., all states communicate with each other

so that the Markov process is irreducible), then the limiting distribution

limt+∞ P{X(t) = j|X(0) = i} = limt+∞ Pij(t) = πj

exists, and it is the unique solution of the following system of linear

equations (also known as balance equations)

• The πj are called steady-state or stationary probabilities since if P{X(0) = j}

= πj , then

P{X(t) = j} = πj

)1( 1

)( ,,2,1,0for

0

1

0

M

j j

ji

ijijj QMjqq

20

S. Özekici INDR 343 Stochastic Models 39

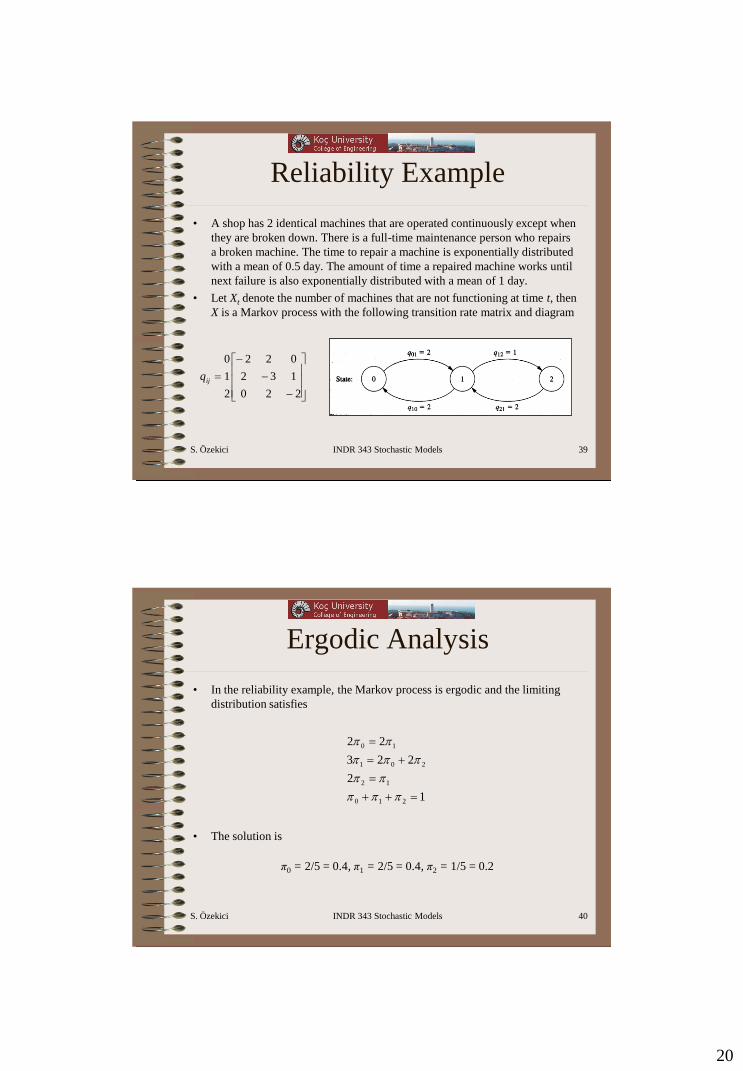

Reliability Example

• A shop has 2 identical machines that are operated continuously except when

they are broken down. There is a full-time maintenance person who repairs

a broken machine. The time to repair a machine is exponentially distributed

with a mean of 0.5 day. The amount of time a repaired machine works until

next failure is also exponentially distributed with a mean of 1 day.

• Let Xt denote the number of machines that are not functioning at time t, then

X is a Markov process with the following transition rate matrix and diagram

220

132

022

2

1

0

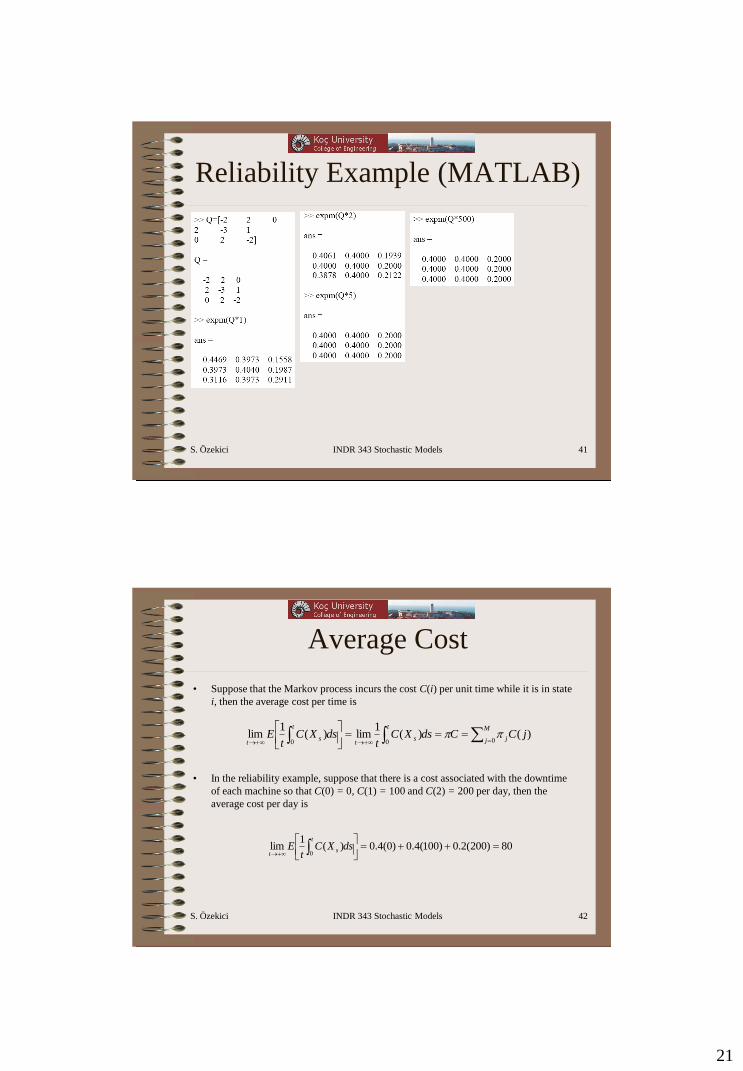

ijq

S. Özekici INDR 343 Stochastic Models 40

Ergodic Analysis

• In the reliability example, the Markov process is ergodic and the limiting

distribution satisfies

• The solution is

π0 = 2/5 = 0.4, π1 = 2/5 = 0.4, π2 = 1/5 = 0.2

1

2

223

22

210

12

201

10

++

+

21

S. Özekici INDR 343 Stochastic Models 41

Reliability Example (MATLAB)

S. Özekici INDR 343 Stochastic Models 42

Average Cost

• Suppose that the Markov process incurs the cost C(i) per unit time while it is in state

i, then the average cost per time is

• In the reliability example, suppose that there is a cost associated with the downtime

of each machine so that C(0) = 0, C(1) = 100 and C(2) = 200 per day, then the

average cost per day is

++

M

j j

t

st

t

st

jCCdsXCt

dsXCt

E000

)()(1

lim)(1

lim

80)200(2.0)100(4.0)0(4.0)(1

lim0

++

+

dsXCt

Et

st

22

S. Özekici INDR 343 Stochastic Models 43

Potential Analysis

• For any Markov process, if there is a continuous discount factor α > 0, the

expected total discounted cost function is

• It is the unique solution of the system of linear equations

+ iXdsXCeEig s

s

00

|)()(

0

1

( ) ( ) ( )

or

or

( )

M

ijjg i C i q g j

g C Qg

g I Q C

+

+

S. Özekici INDR 343 Stochastic Models 44

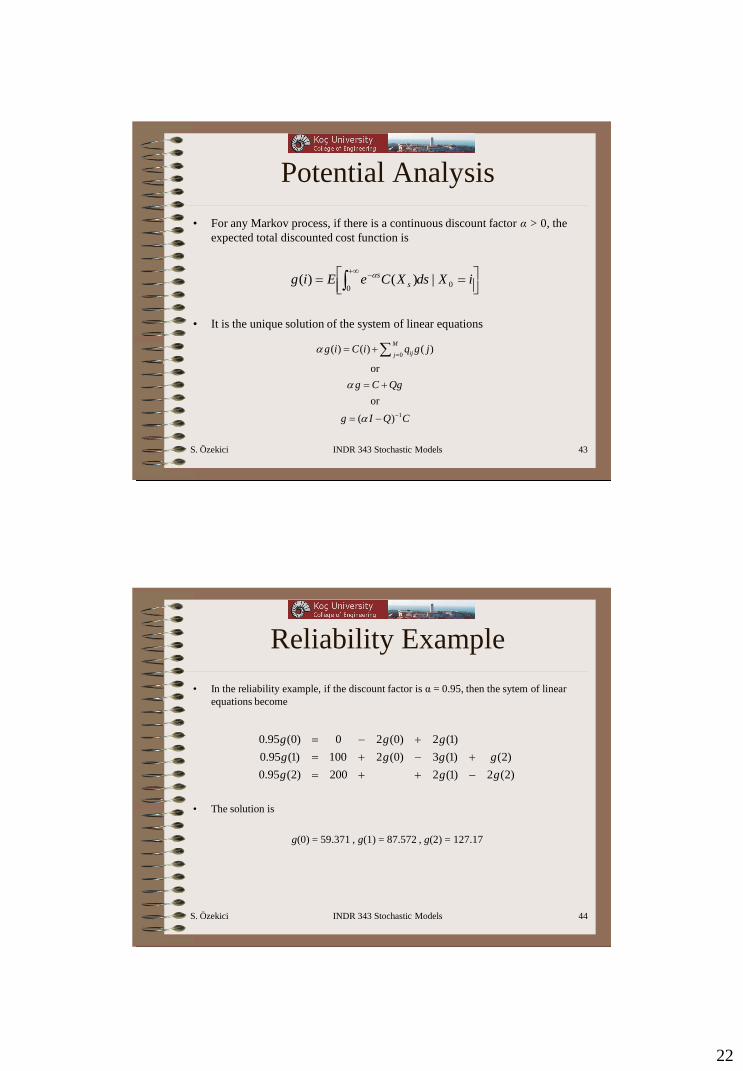

Reliability Example

• In the reliability example, if the discount factor is α = 0.95, then the sytem of linear

equations become

• The solution is

g(0) = 59.371 , g(1) = 87.572 , g(2) = 127.17

)2(2)1(2200)2(95.0

)2()1(3)0(2100)1(95.0

)1(2)0(20)0(95.0

ggg

gggg

ggg

++

++

+

23

S. Özekici INDR 343 Stochastic Models 45

Homework 1 & 2

• Homework 1

– 29.2-2

– 29.2-3

– 29.3-2

– 29.4-2

– 29.4-5

• Review Exercises 1

– 29.4-3

– 29.5-5

– 29.6-1

– 29.7-1

– 29.7-2

• Homework 2

– 29.5-4

– 29.5-9

– 29.6-5

– 29.8-1

– 29.8-2