needham growth investor...

TRANSCRIPT

NEEDHAM GROWTHINVESTOR CONFERENCERoger Shannon – SVP of Finance & CFO

January 18, 2018

2018 © ADTRAN, Inc.G ener al Business

Safe Harbor StatementDuring the course of this meeting, ADTRAN representatives expect to make forward-looking statements, which reflect management’s best judgment, based on factors currently known. However, these statements involve risks and uncertainties, including the successful development and market acceptance of core products, the degree of competition in the market for such products, the product and channel mix, component cost, manufacturing efficiencies, foreign exchange rate variations and other risks detailed in our Annual Report on Form 10-K for the year ended December 31, 2016. These risks and uncertainties could cause actual results to differ materially from those in the forward-looking statements, which may be made during this meeting.

2

© 2015 ADTRAN, Inc. All rights reserved.

STRATEGIC FOCUS

FOR THE PAST THREE DECADES,ADTRAN HAS BEEN ENABLING A FULLY CONNECTED WORLD.

2018 © ADTRAN, Inc.G ener al Business

Corporate Strategic Plan Focus

§ Capitalize and expand our position in enabling Service Providers to:§ Increase competitiveness through advanced broadband speeds/capacity§ Provide ubiquitous broadband availability§ Expand adjacent markets into Cable/MSO broadband access

§ Exploit two distinct and major shifts in the environment1. Evolution of the Service Delivery Platform for scale and service agility2. Expansion of wireless in the network

4

Near Term Focus (0-3 yrs)

Med/Long Term Focus (3+ yrs)

2018 © ADTRAN, Inc.G ener al Business

Market DynamicsOperator Perspective

CompetitivePositioning

Scale and

Agility

BroadbandAvailability

Connect America Fund• $9B to connect 3.6M homes• 6yr build out• 10Mbps/1Mbps

European Commission• Digital agenda Evolution of Service

Delivery Platform• Open source / White box• 70% of AT&T’s network will

be software by 2020

Gigabit speeds & expansion of wireless in the network• Comcast 2Gbps• AT&T Fiber - Gigabit• 5G – 1Gbps up to 500yds

o 2018 commercial launch (Vz)

5

Strategic Plan 0-3yrs

Strategic Plan 3yrs+

2018 © ADTRAN, Inc.G ener al Business

ADTRAN’s Market Focus

ADTRAN

DomesticTier 1

DomesticTier 2

DomesticTier 3

Cable / MSO

Int’l

6

Operator Focus• SDN Transformation• Gigabit Competition• Netflix/Amazon/Google competition

ADTRAN Focus• 10G PON, G.fast, Vectoring, SD-Access, Services

Operator Focus• CAF2 • Cable competition• Rapid follower

ADTRAN Focus• FTTN / Vectoring, PON,

Services

Operator Focus• RoR CAF• Cable competition• Slow SDN adopter

ADTRAN Focus• PON• Subscriber Experience

Operator Focus• SDN Transformation• Regulatory Hurdles• EU Gigabit Society

ADTRAN Focus• G.fast, Vectoring,

10G PON, Services

Operator Focus• Deep Fiber• DOCSIS 3.1 Transition• SDN Transformation• Protect market share

ADTRAN Focus• 10G PON

2018 © ADTRAN, Inc.G ener al Business

ADTRAN History of Innovation

DIVESTITURE ERA

INTERNET ERA

IP TRANSITIONERA

GIGABITERA

SDN ERA

Created T1 Access Market

Broke $1000 Economic Barrier with HDSL, 95%

market share

Disrupted WesternElectric Monopoly

Redefined Economics for D4 channel cards

Drove Innovationin DSL andConverged Services

Repeaterlessbreakthru

Total Reach ISDN

Redefined economics for SONET Fiber Access(OPTI-3, OPTI-6100)

1st ConvergedVoice & Data

Business Gateways

1st AllEthernetMSAN

1st VDSLDeployment

Based on IP DSLAM

1st demo of VDSL2 825Mbps

w/ phantom, bonding, vectoring

Global Leader in OSP

broadband solutions

Market Leader in DSL and

Converged Services

350 Gig Communities by 2016

Frequency DivisionVectoring

(FDV)

1st Edged Optimized

Packet-Optical

Networking Platform

MarketLeadership

In G.fastinnovation

Breakthrough In NGPON2Tunable Optics

1st Deployment of System Level Vectoring (SLV) (US)

1st converged, multi-service

Gigabit enterprise and MTU gateways

1st Cloud-based WLAN

ProCloudWi-Fi services

Leading SDN/NFV Access in Broadband

Forum

Mosaic Activate SD- Automation

for Service Activation

1st Open Platform for G.fast DPU

1st system level CORD

demo

Mosaic Cloud Platform wins 13 Industry Awards

MosaicCloud

PlatformLaunch

7

2018 © ADTRAN, Inc.G ener al Business

The Access Mosaic

8

2018 © ADTRAN, Inc.G ener al Business

Broadband Access§ Market leader in 10 Gigabit optical access innovation

§ XGS PON – commercial deployments, standards leadership§ NGPON-2 – customer trials underway with US Tier 1

§ Over 100 G.fast trials/deployments announced on six (6) continents

§ 5 Nationwide commercial deployments on 4 continents US Tier 1s, DT (Croatia), Bezeq (Israel), nbn (Australia)

§ Europe’s (and World’s) and NA’s largest deployment of Vectoring and SuperVectoring

§ Over 400 Gigabit Communities§ Leader in CAF2 solutions

9

Innovation Leadership

2018 © ADTRAN, Inc.G ener al Business

ADTRAN Gfast/FTTdp Leadership

World’s 1st

FTTdp (UBE) Architecture

Best Fixed Access Product (UBE)

World’s 1st

Fully SealedG.fast Demo

BTGOLD Project

World’s Only Chipset AgnosticG.fastArchitecture

World’s 1st

SD-Access G.fastSolution

Global Leader for Sealed FTTxSolutions

Fully sealedSymmetric serviceReverse power

2010

UBE wins World Vendor Award 100,000 sealed

units deployed

2012 2014 2015 2015 2015 2015

Most G.fastTrials and Demos

World’s 1st

G.fast over Coax

Top 2 Global G.fast Vendors

Broadband Forum Circle of Excellence Award

World’s 1st

Public Demo of G.fast 212 MHz

Most Innovative and Broadest G.fast Portfolio

Five Nationwide G.fast Deployments on Four Continents Broadband Trends

Customer SurveyDevelopment of SD-Access Yang Models

ITU-T meeting in Huntsville, AL Power, port and

placement variants

Primary Vendorto Tier I operators

With DTA DemoOver 100 acrosssix continents

2016 2016 2016 2017 2017 2017 2017

2018 © ADTRAN, Inc.G ener al Business

SDN Access§ Complete cloud-edge to subscriber-edge solution set§ 1st to integrate and deploy complete FTTx portfolio with an

open source SDN controller§ Only vendor with a complete Software Defined Access

solution set built around a CORD architecture§ 1st (and only) 10G PON vOLT CORD demo in a Tier 1§ 1st industry interop - vCPE portfolio

§ Modular software architecture with Agile/DevOps model§ Leadership in Broadband Forum, ITU, ETSI, Celtic-Plus, and

UK NICC standards activities§ Industry’s Most Awarded (13) ADTRAN Mosaic Cloud Platform

11

Innovation Leadership

2018 © ADTRAN, Inc.G ener al Business

2017 © ADTRAN, Inc.

MosaicMost Awarded SD-Access Solution

in the Industry

2018 © ADTRAN, Inc.G ener al Business

13

Company Financial Performance

14

Financial Stability§ Nearly 3 Decades of

Continuous Profitability§ Ongoing Strong Balance

Sheet and Cash Flow§ Publicly Traded for 23 Years

with Full Transparency(NASDAQ-ADTN)

2018 © ADTRAN, Inc.G ener al Business

Historically Strong Cash Flow and Solid Balance Sheet

2012-2017 Dec. 31, 2017Cash Returned to Shareholders Cash & Investments Debt Total Assets

Dividends

$233M $27M $665M $118MShare Buybacks

$354M

2018 © ADTRAN, Inc.G ener al Business

ADTRAN - FY 2017 Financial Highlights FY 2017 FY 2016

Revenue $667M $637M

Gross Margin 45.6% 45.8%

Operating Expense (GAAP) $266M $257M

Operating Margin (%) (GAAP) 5.7% 5.5%

GAAP EPS (diluted) $0.49* $0.72

Non-GAAP EPS (diluted) $0.89 $0.84

* FY 2017 GAAP EPS includes the one-time tax impact of 11.9 million relating to the Tax Cuts and Jobs Act of 2017.

2018 © ADTRAN, Inc.G ener al Business

2015 – 2017 Revenue by Segment and Categories

$527 $526 $541

$73 $111 $126$600

$637$667

$0

$100

$200

$300

$400

$500

$600

$700

2015 2016 2017

Products Services

$406 $436 $474

$126$138

$138$69$63

$55$600$637

$667

$0

$100

$200

$300

$400

$500

$600

$700

2015 2016 2017

AccessandAggregation CustomerDevices TraditionalProducts

2018 © ADTRAN, Inc.G ener al Business

2015 – 2017 Gross Margin by Segments

44.3%48.5% 48.3%

45.9%

32.8% 33.8%

44.5% 45.8% 45.6%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

2015 2016 2017

Products Services Total

ü 2017 GM% flat with 2016 despite 17% increase in International Revenueü Services GM% up 1% point on 13% increase in Services Revenue

2018 © ADTRAN, Inc.G ener al Business

Revenue – U.S. vs. International

$419$501 $508

$181$135 $159

$600$637

$667

$0

$100

$200

$300

$400

$500

$600

$700

2015 2016 2017

Domestic International

20

2017 Summary§ 2017 ended with 2nd best revenue performance in company

history § Record 1H Revenue§ Ties Record revenue through 3Q17 (2011); Full year up 5%§ Record Services Revenue in Q3

§ Disappointing 4Q revenue due to unforseen event§ 10% customer temporarily paused spending in 4Q due to a merger-

related review§ Prudent management of Q4 margins and OPEX§ All other accounts and market segments remain on track

§ Gross Margin Improvements in 2017§ Total Gross Margin % flat to 2016 despite 17% Int’l Revenue growth§ Services gross margins up 1% point over 2016 on 13% Revenue

growth§ Outstanding engagement by Tier 1s globally

§ High interest / acceptance of next gen SD-Access solutions (Mosaic, G.fast, NGPON2)

§ Historic breadth of opportunities, both domestically and internationally

2018 © ADTRAN, Inc.G ener al Business

Quarterly Financial Highlights

$170$185 $185

$127

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

$200

Q1 Q2 Q3 Q4

2015 2016 2017

After strong three quarters in line with ongoing major investment cycle in wireline networks…

…4Q17 performance impacted by a merger-related review & slowdown in the spending at a domestic Tier 1 customer.

Revenue (M)

2018 © ADTRAN, Inc.G ener al Business

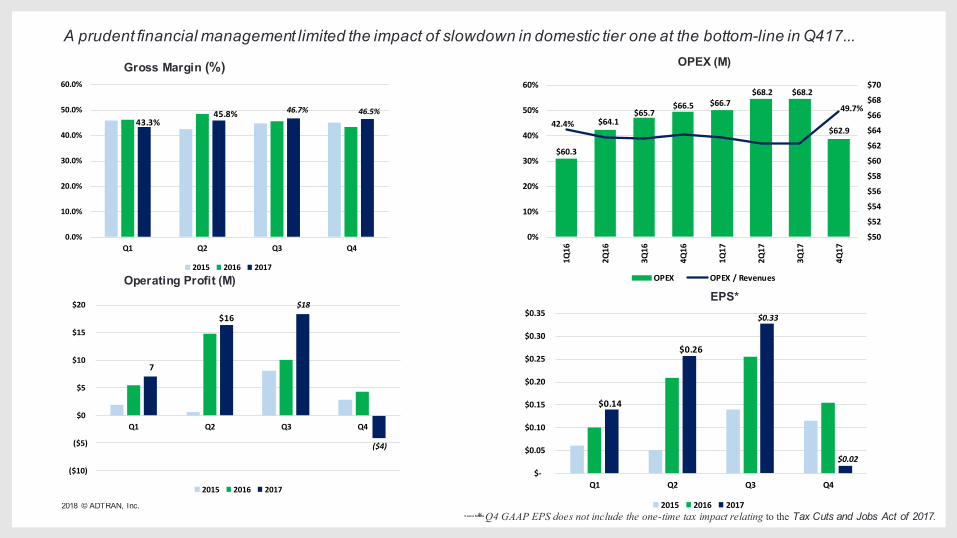

A prudent financial management limited the impact of slowdown in domestic tier one at the bottom-line in Q417...

43.3%45.8% 46.7% 46.5%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Q1 Q2 Q3 Q4

2015 2016 2017

$60.3

$64.1$65.7

$66.5 $66.7$68.2 $68.2

$62.942.4%

49.7%

$50

$52

$54

$56

$58

$60

$62

$64

$66

$68

$70

0%

10%

20%

30%

40%

50%

60%

1Q16

2Q16

3Q16

4Q16

1Q17

2Q17

3Q17

4Q17

OPEX OPEX/Revenues

Gross Margin (%) OPEX (M)

Operating Profit (M)

7

$16$18

($4)

($10)

($5)

$0

$5

$10

$15

$20

Q1 Q2 Q3 Q4

2015 2016 2017

$0.14

$0.26

$0.33

$0.02$-

$0.05

$0.10

$0.15

$0.20

$0.25

$0.30

$0.35

Q1 Q2 Q3 Q4

2015 2016 2017

EPS*

* Q4 GAAP EPS does not include the one-time tax impact relating to the Tax Cuts and Jobs Act of 2017.

2018 © ADTRAN, Inc.G ener al Business

Q4 FY 2017 Q3 FY 2017 Q4 FY 2016Amount ($M) GM (%) Amount ($M) GM (%) Amount ($M) GM (%)

Network Solutions 96.1 48.3 145.5 49.5 126.8 46.5Services & Support 30.5 40.9 39.6 36.7 36.2 32.6Total 126.5 46.5 185.1 46.7 163.0 43.4

Revenue & Gross Margin (GM) by Operating Segment

Revenue by Categories

Q4 FY 2017 Q3 FY 2017 Q4 FY 2016Access and Aggregation 78.9 136.0 119.7Customer Devices 32.8 35.6 31.4Traditional Products 14.9 13.6 11.9Total 126.5 185.1 163.0

U.S. and International Revenue

Q4 FY 2017 Q3 FY 2017 Q4 FY 2016United States 93.7 147.9 123.7International 32.8 37.2 39.3Total 126.5 185.1 163.0

2018 © ADTRAN, Inc.G ener al Business

Business Outlook*

Q1 18

Revenue Flattish (QoQ)

Gross Margin 40% range

OpEx $64-$65M range

Tax Low-20% range

Guidance or Outlook with respect to Q118 is as of January 17, 2018, the date presented on the 4Q17 earnings call. Actual results may differ materially from these forward looking statements.

Going forward, all of our programs and opportunities remain unchanged and on track as we had

previously communicated, with the exception of the slowdown in the domestic tier one.

Summary

• Proven history and well positioned• Leader in fixed broadband access• Leader in SDN-Access

ü Open, scalable and standards-basedü Leading transition to software/service model

• Ramping broadband investment cycleü Emerging technologies in fiber & copperü Imperative for service agility & automation

25

2018 © ADTRAN, Inc.G ener al Business

ADTRAN IS BRINGING THE WORLD TOGETHER